Investment Advisers Act Rules: Key Requirements for RIAs

Key Takeaways

The Investment Advisers Act of 1940 is the primary US law that regulates investment advisors, defining who must register and how advisory firms must operate.

You’re likely considered an investment advisor if you provide advice about securities, are in the business of doing so, and receive compensation (even if your product looks like software).

You need to register as an RIA once advisory activity begins and clients rely on it, not when you decide to label your business as advisory.

You’re required to act in your client’s best interest and clearly disclose conflicts, as fiduciary duty applies across how advice is given, priced, and presented.

Your day-to-day obligations are driven by rules covering compliance programs, custody of assets, marketing practices, and recordkeeping.

Your disclosures, including Form ADV, Form CRS, and marketing content, must match how your business actually operates, as inconsistencies are a common source of regulatory issues.

The Investment Advisers Act of 1940 is central to how Registered Investment Advisors operate in the US. Its rules define who must register, how advisors interact with clients, and what regulators expect regarding disclosures, controls, and ongoing oversight.

For fintech companies, these rules often apply even when the product looks more like software than traditional advisory services.

This article breaks down the key requirements under the Investment Advisers Act of 1940 and the SEC rules built around it, focusing on the areas that matter in practice, including fiduciary obligations, compliance program expectations, marketing restrictions, custody requirements, and recordkeeping.

At InnReg, we help RIAs and fintechs navigate the Investment Advisers Act rules. From registration and licensing to building and managing compliance programs, our team supports firms as they grow and evolve.

What Is the Investment Advisers Act of 1940?

The Investment Advisers Act of 1940 is the primary federal law governing investment advisors in the US. It establishes the legal framework for how advisory firms register, operate, and interact with clients. Most of the investment advisers act rules that firms deal with day to day come from this statute, and the SEC rules are built around it.

While the statute itself is relatively concise, its practical impact is extensive. Most of the day-to-day requirements come from SEC rules and guidance, which turn high-level principles into specific expectations around disclosures, marketing, custody, and recordkeeping.

The purpose of the Act is straightforward. It is designed to protect investors. It sets standards for how advice is given, how conflicts are handled, and what firms need to disclose. At the center is fiduciary duty, which means advisors are expected to put client interests first and be upfront about any conflicts.

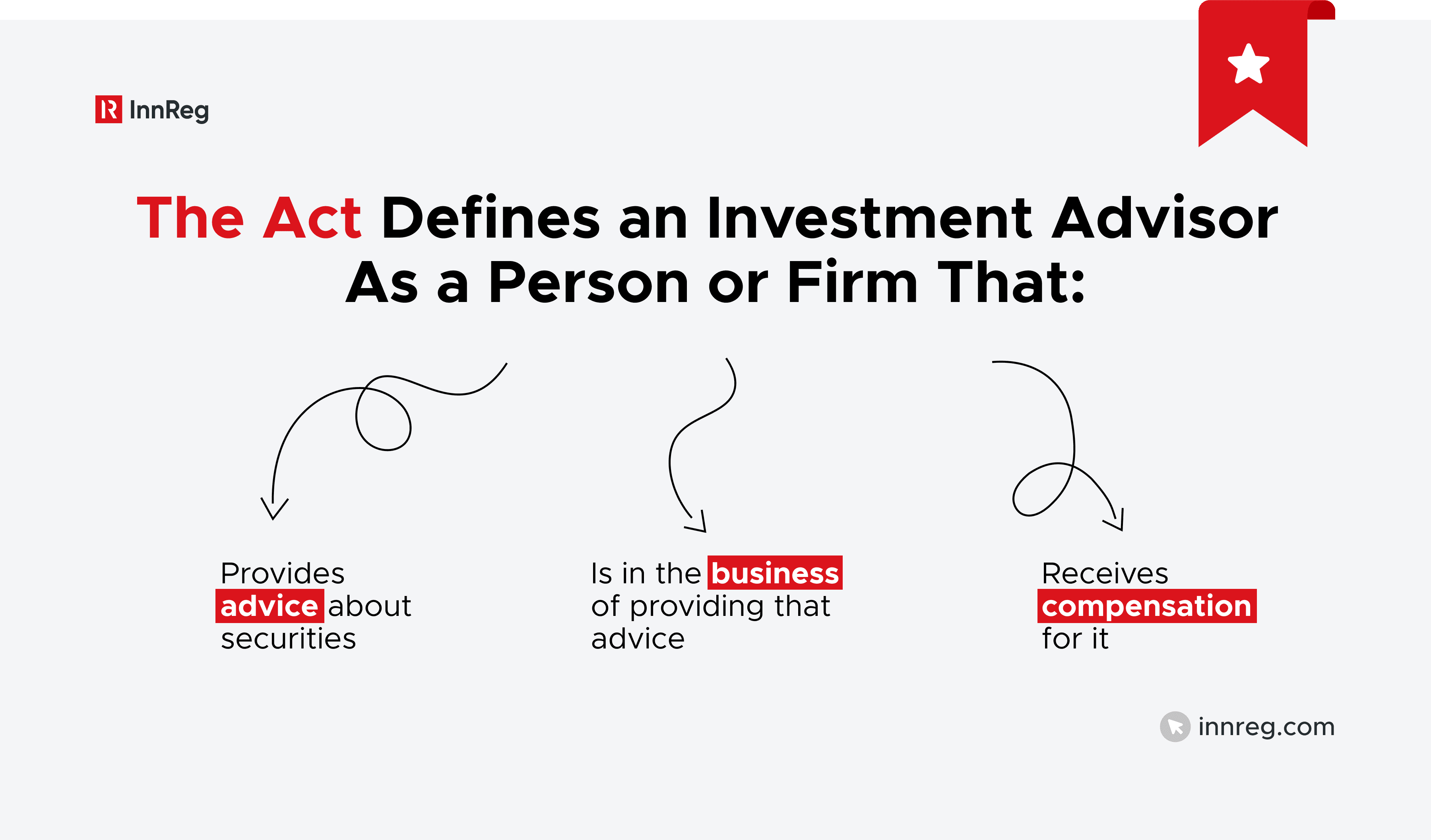

The Act defines an investment advisor as a firm that provides advice about securities, is in the business of providing advice, and receives compensation for it.

If all three elements are met, the firm is likely subject to the Advisers Act unless an exclusion or exemption applies.

This definition is broad and technology-neutral, which is why many fintech models fall within scope even if they are not labeled as advisory services.

In fintech, the key question is often whether a product feature qualifies as investment advice. Platforms frequently evolve from infrastructure into tools that influence investment decisions. When that transition occurs, the Investment Advisers Act rules may apply, triggering registration and ongoing compliance obligations.

Who Is Considered an Investment Advisor Under the Act

The scope of the definition goes beyond traditional advisory firms. It can include automated investment tools, platforms offering portfolio guidance, and research-driven services that influence client decisions.

Many fintech products fall into this category as they evolve from tools into decision-making interfaces.

What matters is not how the firm labels itself, but how the product functions in practice. If users are receiving recommendations about securities and are expected to rely on them, the activity may fall within the scope of the Act. The analysis is driven by substance over form.

When Firms Must Register as RIAs

A firm must register as a Registered Investment Advisor when it falls within the scope of the Advisers Act and does not qualify for an available exemption.

This usually involves providing investment advice about securities as part of a business and receiving compensation, whether directly or indirectly. The analysis focuses on the substance of the activity rather than formal titles or business descriptions.

The timing of registration is often where firms make mistakes. Many fintech companies delay the analysis, assuming they are still operating as a tool or platform. In reality, once advisory features are introduced and clients begin relying on them, the obligation to register may already be triggered.

SEC vs. State Registration for Investment Advisors

Whether a firm registers with the SEC or at the state level depends primarily on assets under management and business structure. In general, firms with $100 million or more in assets under management register with the SEC, while smaller firms are regulated by state authorities.

This distinction is more than administrative. SEC-registered advisors operate under a federal framework with national oversight, while state-registered firms must comply with individual state requirements, which can vary. For firms operating across multiple states, this can introduce additional complexity.

Learn more about RIA state vs. SEC registration →

Why the Investment Advisers Act Matters for RIAs

The Investment Advisers Act goes beyond registration. It sets expectations for how advisory firms operate day to day, including how they manage clients, controls, and disclosures. The Investment Advisers Act rules define what regulators expect in practice, not just what gets filed.

1. Investor Protection and Fiduciary Obligations

The Act is built around the idea that advisors must put client interests first. This fiduciary standard requires firms to address conflicts openly and provide advice that aligns with the client’s objectives. It affects everything from pricing and fee structures to how recommendations are framed.

Rather than being tied to one rule, fiduciary duty runs throughout the Investment Advisers Act rules, shaping how firms approach disclosures, marketing, and internal decision-making. It is a standard that applies across the full lifecycle of the client relationship.

2. Oversight of Advisory Activities and Client Relationships

The Act also drives how firms oversee their advisory activities.

This includes how client accounts are managed, how recommendations are generated, and how decisions are documented. Supervisory structures are expected to reflect the firm’s actual business model.

For fintech firms, this can become complex. Automated tools, algorithms, and third-party integrations all play a role in how advice is delivered. Oversight needs to account for these components, not just traditional human-driven processes.

3. Regulatory Transparency and Disclosure Requirements

Transparency is a recurring theme throughout the Act. Firms are expected to provide clear, accurate, and up-to-date disclosures to both clients and regulators. This includes information about services, fees, conflicts, and business practices.

Disclosure is not just about providing documents. It is about making sure information is complete, consistent, and aligned with how the business actually operates. Gaps between disclosures and reality are a common source of regulatory issues.

4. Enforcement Authority and Regulatory Examinations

The Act gives regulators broad authority to examine advisory firms and assess how they operate. These examinations are not limited to written policies. They focus on how firms apply the Investment Advisers Act rules in practice, including how decisions are made and how controls function in real situations.

For RIAs, this means compliance needs to be embedded in day-to-day operations. Regulators will review records, client communications, marketing materials, and internal processes. The focus is on whether the firm’s actual practices align with its disclosures and policies, not just whether documentation exists.

Being prepared for an examination requires more than organized files. Firms need to be able to explain how their compliance program works in practice and how key decisions are made. The ability to demonstrate consistency between what the firm says and what it does is a central expectation under the Investment Advisers Act rules.

Core Investment Advisers Act Rules RIAs Must Follow

The Investment Advisers Act is applied through a set of SEC rules that govern how RIAs operate in practice. These Investment Advisers Act rules cover areas like compliance, disclosures, custody, marketing, and recordkeeping.

Fiduciary Duty Under Section 206 of the Advisers Act

Section 206 is the anti-fraud provision of the Act and forms the basis of fiduciary duty. It prohibits advisors from engaging in deceptive, manipulative, or fraudulent practices. In practice, this standard applies broadly across client interactions.

Fiduciary duty under Section 206 requires advisors to act in the client’s best interest and to disclose conflicts in a way that clients can understand. This obligation extends beyond formal disclosures and applies to how advice is delivered, how fees are structured, and how services are described.

See also:

Rule 206(4)-7: The Compliance Program Rule

Rule 206(4)-7 requires firms to implement written compliance policies and procedures that reflect their actual operations. This includes considering the firm’s services, structure, and risk exposure. Policies that are not tailored to the business often fail to address key risks.

Firms are also required to conduct an annual review of their compliance program and designate a chief compliance officer responsible for its administration.

The rule focuses on whether the compliance program reflects the firm’s actual operations and risk profile, not just whether policies exist.

Learn more about Rule 206(4)-7 →

Need help with RIA compliance?

Fill out the form below and our experts will get back to you.

Rule 204A-1: Code of Ethics Requirements

Rule 204A-1 requires firms to adopt a code of ethics that sets clear standards for employee conduct.

This includes policies on personal trading, the handling of material non-public information, and reporting obligations for access persons. The goal is to create a structured framework for managing employee activity that could impact clients.

The code of ethics is designed to address conflicts between employee behavior and client interests. This is particularly relevant in areas such as personal trading and the use of sensitive information.

Firms are also expected to monitor compliance through reporting, certifications, and ongoing oversight, rather than treating the code as a static document.

Learn more about Rule 204A-1 →

Rule 204-2: Books and Records Requirements

Rule 204-2 sets the baseline for recordkeeping across an RIA’s operations. Firms must keep records connected to advisory work, client communications, transactions, marketing, and compliance activities.

These records must be retained for specified periods and be accessible for regulatory review. Recordkeeping is not just administrative. It is how firms demonstrate compliance with the Investment Advisers Act rules during examinations.

Learn more about Rule 204-2 →

Rule 206(4)-2: Custody Rule

The Custody Rule applies when a firm has custody of client assets, which can include direct possession or certain forms of authority over client funds or securities. The rule introduces requirements around safeguarding assets and providing transparency to clients.

This typically involves using qualified custodians, delivering account statements, and, in some cases, undergoing an independent verification of client assets.

Custody is interpreted broadly, and firms often underestimate when they fall within scope, especially in fintech models involving control or access to assets.

Learn more about Rule 206(4)-2 →

Rule 206(4)-1: The Marketing Rule

The Marketing Rule governs how RIAs advertise their services and communicate performance. It applies to traditional marketing, digital content, testimonials, endorsements, and third-party ratings.

The rule focuses on preventing misleading statements and requires firms to substantiate claims, especially around performance. Marketing content must be consistent with actual services and supported by records, tying directly into disclosure and recordkeeping requirements.

Learn more about the SEC Marketing Rule →

Rule 206(4)-5: Pay-to-Play Restrictions

Rule 206(4)-5 addresses political contributions made by advisors and their personnel. It is designed to prevent firms from obtaining government business through political influence.

The rule imposes restrictions on contributions and can limit a firm’s ability to receive compensation from certain government clients if violations occur.

Even relatively small contributions can trigger restrictions, making monitoring and pre-clearance important in practice.

Learn more about Pay-to-Play Rule →

Rule 206(4)-6: Proxy Voting Requirements

Rule 206(4)-6 applies to RIAs that have authority to vote client securities. It requires firms to adopt written policies and procedures that are reasonably designed to vote proxies in the best interest of clients. These policies should reflect how the firm approaches voting decisions and how conflicts are identified and handled.

In practice, proxy voting is not just an administrative task. It involves evaluating proposals, determining how votes align with client interests, and documenting the rationale behind those decisions. Firms are expected to have a clear and consistent process for how proxy votes are reviewed and cast.

Firms must maintain records of proxy voting activity (pursuant to the Books & Records rule) and provide clients with information about those votes upon request. Proxy voting is treated as part of the advisor’s fiduciary responsibility, and regulators expect firms to show how their process supports that obligation.

Rule | Area Covered | Key Requirement |

|---|---|---|

Section 206 | Anti-fraud / fiduciary duty | Act in client’s best interest and avoid misleading conduct |

Rule 206(4)-7 | Compliance programs | Maintain written policies, annual review, CCO oversight |

Rule 204A-1 | Code of ethics | Govern employee conduct and personal trading |

Rule 204-2 | Recordkeeping | Maintain and retain required records |

Rule 206(4)-2 | Custody | Safeguard client assets and provide transparency |

Rule 206(4)-1 | Marketing | Prevent misleading advertising and require substantiation |

Rule 206(4)-5 | Pay-to-play | Restrict political contributions tied to advisory business |

Rule 206(4)-6 | Proxy voting | Vote client securities in the client's best interest |

See also:

Disclosure Requirements Under the Investment Advisers Act

Disclosure is a core part of the Investment Advisers Act rules. Firms are expected to provide clear and accurate information about their services, fees, and conflicts, and keep that information up to date as the business changes.

Form ADV Registration and Public Disclosure

Form ADV is the central disclosure document for RIAs and the foundation of regulatory reporting. It describes the firm’s services, fees, conflicts, and disciplinary history. Filed with regulators and available to the public, it supports both compliance and transparency.

In practice, Form ADV is often one of the first documents reviewed during an examination. Regulators use it to understand how the firm describes its business and then compare that description to actual operations. Inconsistencies between Form ADV and how the firm operates are a common source of regulatory scrutiny.

Maintaining Form ADV requires more than periodic updates. Firms need to review it whenever there are changes to services, fees, or business structure. This includes new product offerings, changes in compensation models, or the introduction of new conflicts that need to be disclosed.

Learn more about Form ADV →

Brochure Requirements Under Rule 204-3

Rule 204-3 requires RIAs to provide clients with a narrative brochure, typically delivered through Form ADV Part 2. This document is written in plain language and explains how the firm operates, including services, fees, conflicts, and key personnel. It is designed to be understandable to clients, not just regulators.

The brochure must be delivered at the start of the relationship and updated at least annually. It also needs to be revised whenever there are material changes. The expectation is that clients can rely on the brochure as an accurate description of the firm’s current business practices.

In practice, this means the brochure needs to stay aligned with marketing materials, internal processes, and client agreements. Differences between these sources can create confusion and raise questions during regulatory reviews.

Form CRS for Retail Investors

Form CRS is a short-form disclosure required for RIAs that work with retail investors. It provides a high-level summary of services, fees, conflicts, and disciplinary history in a standardized format. The goal is to make it easier for clients to compare firms.

Although the document is brief, it carries significant weight. Regulators expect it to be consistent with more detailed disclosures, such as Form ADV and marketing materials. Even small inconsistencies between Form CRS and other documents can raise concerns about disclosure accuracy.

For fintech firms, Form CRS can be particularly important when services are embedded into broader platforms. The challenge is to clearly describe the advisory component in a way that matches how the product actually functions.

Learn more about Form CRS →

Ongoing Disclosure Updates and Amendments

RIAs need to update their disclosures when material changes occur and file annual amendments to Form ADV. This can include changes to services, fees, business practices, or conflicts of interest.

Keeping disclosures aligned can be challenging. Changes to products or new partnerships can create gaps if updates are not made at the same time. Regulators often look at whether disclosures reflect how the business is actually operating.

In practice, this requires coordination across teams. Legal, compliance, product, and marketing all play a role in maintaining consistency. When disclosures, marketing, and operations diverge, it becomes difficult to demonstrate compliance during examinations.

Requirement | Purpose | Key Expectation |

|---|---|---|

Form ADV | Core regulatory disclosure | Provide accurate, up-to-date information on services, fees, conflicts, and operations |

Rule 204-3 Brochure (ADV Part 2) | Client-facing disclosure | Clearly explain services, fees, and conflicts in plain language |

Form CRS | Retail investor summary | Deliver standardized, concise disclosure aligned with other documents |

Books, Records, and Documentation Requirements

Recordkeeping is a core part of the Investment Advisers Act rules. Firms are expected to maintain records that reflect their advisory activities, communications, and compliance processes. These records are the primary way regulators assess whether a firm is operating in line with its obligations.

Required Records for RIAs

RIAs are expected to keep records across most parts of their business. That includes client communications, agreements, transaction data, marketing materials, and internal compliance documents.

The idea is straightforward. Regulators want to see how the firm actually operates, not just what it files. Records should reflect how advice is delivered and how decisions are made over time.

When documentation is scattered or incomplete, it becomes harder to explain what the firm is doing. During an exam, that lack of clarity often creates problems, even if the underlying activity was reasonable.

Record Retention Periods and Storage Requirements

The Advisers Act sets specific retention periods for different types of records, often requiring firms to keep documents for several years. Some records must be easily accessible for a defined period, while others can be archived but still retrievable.

Firms also need to consider how records are stored. Electronic storage is common, but it must meet regulatory expectations around accessibility and integrity. Records must be preserved in a way that prevents alteration and allows regulators to review them when needed.

Advertising and Marketing Recordkeeping

Recordkeeping requirements extend to marketing and advertising activities. Firms must retain copies of advertisements, performance materials, and supporting documentation used to substantiate claims.

This is closely tied to the Marketing Rule. If a firm makes a claim about performance or services, it needs to maintain records that support that claim. Regulators often review marketing records alongside disclosures to identify inconsistencies or unsupported statements.

In practice, this means keeping both the final materials and the underlying data used to create them. Missing support can create issues even if the marketing content itself appears compliant.

Compliance Documentation and Annual Reviews

RIAs are also required to maintain records related to their compliance programs. This includes written policies and procedures, records of compliance reviews, and documentation of how issues are identified and addressed.

Annual compliance reviews are a key part of this process. Firms need to document what was reviewed, what issues were identified, and what changes were made. These records demonstrate how the firm monitors and updates its compliance program over time.

For growing firms, especially in fintech, documenting these processes consistently can be challenging. Changes in products, systems, and teams all need to be reflected in compliance records to maintain a clear audit trail.

Record Type | What It Covers | Key Expectation |

|---|---|---|

Advisory and Client Records | Client communications, agreements, transactions | Reflect on how advice is delivered and decisions are made |

Record Retention and Storage | Retention periods, accessibility, storage systems | Maintain records for required timeframes and keep them accessible |

Marketing and Advertising Records | Ads, performance data, supporting materials | Retain both final materials and supporting evidence for claims |

Compliance Documentation | Policies, procedures, reviews, and issue tracking | Document how the compliance program operates and evolves |

Annual Compliance Review Records | Review findings, updates, and remediation actions | Maintain a clear record of what was reviewed and updated each year |

The Custody Rule and Safeguarding Client Assets

Custody is one of the more sensitive areas under the Investment Advisers Act rules. It focuses on how firms handle client funds and securities, and what controls are in place to protect them. If a firm is deemed to have custody, additional requirements apply, even if the firm does not physically hold assets.

What Counts as Custody Under the Advisers Act

Custody is not limited to holding client assets. It can also come up when a firm has the ability to move a client’s money or securities, even if the firm never physically takes possession. In many cases, that authority comes from client authorization in advisory agreements.

For example, fee deductions or authority granted through a power of attorney can bring a firm into custody territory. These are common features, but they still count from a regulatory perspective.

In fintech setups, this often gets more complicated. Integrations with custodians, payment providers, or wallet infrastructure can introduce control in ways that are not always obvious. Small details in how access is structured can change whether a firm is considered to have custody.

Qualified Custodian Requirements

When a firm has custody, client assets generally must be held with a qualified custodian. This includes banks, broker-dealers, and other regulated financial institutions that meet specific criteria.

The purpose is to separate the control of assets from the advisor’s operations. Using a qualified custodian is intended to reduce the risk of misuse or loss of client assets, while providing an independent layer of oversight.

For firms working with multiple providers, it is important to clearly define who holds assets and who has authority over them. Misalignment between contractual roles and actual control is a common issue.

Account Statements and Client Transparency

Firms with custody are typically required to provide account statements to clients, either directly or through the qualified custodian. These statements must show holdings and transactions in a way that allows clients to track their assets.

This requirement supports transparency and allows clients to independently verify activity. Regular account statements are a key control that helps detect errors or unauthorized activity.

In practice, firms need to confirm that statements are delivered consistently and that the information matches internal records. Discrepancies can raise questions during examinations.

Surprise Examinations and Compliance Requirements

In certain cases, firms with custody are required to undergo an independent verification of client assets (aka “surprise examination”) by an independent public accountant. This examination reviews how client assets are handled and whether controls are operating as expected.

The requirement depends on how custody is structured and whether exceptions apply. Surprise examinations are designed to provide an external check on how firms safeguard client assets.

Preparing for these reviews requires more than documentation. Firms need to demonstrate how processes work in practice, including how access is controlled, how transactions are approved, and how records are maintained.

See also:

Compliance Program Requirements for RIAs

A compliance program is a core requirement under the Investment Advisers Act rules. It is how firms translate regulatory obligations into day-to-day processes. Regulators focus on whether the program reflects how the business actually operates, not just whether policies exist.

Written Policies and Procedures

RIAs are required to maintain written policies and procedures that address the risks in their business. These typically cover areas such as conflicts of interest, trading practices, marketing, custody, and recordkeeping.

The content of these policies should match how the firm operates in practice. Generic documents often leave gaps, especially for firms with more complex or technology-driven models. Policies need to reflect actual workflows, systems, and decision-making processes.

In practice, this means reviewing and updating policies as the business evolves. New products, integrations, or services often introduce risks that need to be addressed in writing.

Chief Compliance Officer Responsibilities

Each RIA must designate a chief compliance officer responsible for administering the compliance program. The CCO oversees policies, monitors activity, and acts as the primary point of contact for regulatory matters.

The role is not limited to oversight on paper. It involves understanding how the business operates and identifying where risks may arise. Regulators expect the CCO to have visibility into the firm’s operations and authority to address compliance issues.

For many firms, especially startups, this function can be difficult to build internally. Some choose to work with external partners who can act as an extension of the team while maintaining independence and oversight.

Annual Compliance Program Reviews

RIAs are required to review their compliance programs at least annually. This review is meant to assess whether policies and procedures remain effective and aligned with the firm’s current activities.

The process typically involves evaluating key risk areas, identifying gaps, and documenting any changes made. The annual review is not just a checklist exercise. It is an opportunity to reassess how the program functions in practice.

In fast-moving environments, this review often highlights areas where the business has outgrown its existing controls. Capturing and documenting those changes is an important part of demonstrating compliance.

Training and Supervision Expectations

A compliance program also needs to cover training and supervision. Employees should know what the firm’s policies require and how those expectations apply to their day-to-day work.

This becomes more important when new products or processes are introduced. Teams need to stay aligned as things change, and supervision plays a role in catching issues early before they turn into larger problems.

For fintech firms, this often involves coordinating across different teams, including product, engineering, and operations. Clear communication and consistent training are key to maintaining alignment.

Regulatory Oversight of Investment Advisors

RIAs operate under active regulatory oversight. This includes supervision by the SEC or state regulators, depending on registration, as well as interaction with other agencies in specific areas. Oversight is not limited to filings. It focuses on how firms apply the Investment Advisers Act rules in practice.

SEC Oversight and Examination Authority

The SEC oversees RIAs that are registered at the federal level. As part of that role, it conducts examinations to understand how firms are actually operating, with attention on areas like disclosures, custody, marketing, and compliance.

Exams are not random. Firms are typically selected based on factors such as size, business model, or areas that present higher risk. The focus is on how the firm operates in reality and whether that matches what has been disclosed, not just whether policies exist.

During an examination, firms are expected to walk through their processes. This usually involves reviewing records, speaking with staff, and looking at how controls function in practice.

State Securities Regulators

Firms that are not registered with the SEC are typically overseen by state regulators. Each state has its own regulatory framework, although many follow similar principles to the Advisers Act.

State oversight can be more fragmented, especially for firms operating across multiple jurisdictions. Firms may need to comply with different requirements depending on where clients are located, which adds complexity to compliance programs.

State examinations also focus on how firms operate in practice, including disclosures, client interactions, and recordkeeping. Coordination across states can become a key operational challenge.

FinCEN and Future AML Requirements for RIAs

In addition to securities regulators, RIAs may also become subject to anti-money laundering requirements under rules adopted by FinCEN. In 2024, FinCEN finalized a rule that would bring certain RIAs and exempt reporting advisers under Bank Secrecy Act obligations, including AML program, suspicious activity reporting, and related requirements.

However, FinCEN subsequently delayed the effective date of the rule from January 1, 2026 to January 1, 2028 while it reviews the framework and implementation approach. As a result, these requirements are not currently in effect for affected RIAs.

For fintech firms, this remains an important development to monitor. Many already operate in environments where AML controls are common, and future implementation could require additional compliance processes, monitoring controls, and reporting obligations.

Regulator | Scope of Oversight | Key Focus |

|---|---|---|

SEC | Federally registered RIAs | Examinations focused on disclosures, custody, marketing, and compliance practices |

State Regulators | State-registered RIAs | Supervision across state-specific rules and multi-jurisdiction requirements |

FinCEN | AML obligations for certain RIAs (2028) | Customer identification, transaction monitoring, and suspicious activity reporting |

Investment Advisers Act Rules in Fintech Business Models

The Investment Advisers Act rules apply based on how a product functions, not how it is labeled. This creates challenges for fintech firms, where features often evolve over time. Many platforms move into advisory territory without a clear transition point, which makes regulatory analysis more complex.

Robo Advisors and Automated Investment Advice

Robo advisors are one of the most direct applications of the Advisers Act in fintech. These platforms provide portfolio recommendations or automated allocation based on user inputs, which typically meet the definition of investment advice.

Even though the process is automated, the regulatory expectations are similar to traditional advisory models. Firms still need to address disclosures, conflicts, and oversight. Automation does not reduce regulatory obligations; it changes how they are implemented.

This creates practical challenges around model governance, assumptions, and how recommendations are presented. Firms need to be able to explain how their algorithms work and how they align with client objectives.

Learn more about robo advisors →

Multi-Asset Platforms and Crypto Integration

Platforms that combine traditional securities with crypto or other asset classes often fall into gray areas. The advisory component may apply to securities even if other parts of the platform fall outside that scope.

This can lead to mixed regulatory treatment within the same product. A single platform may be subject to the Investment Advisers Act rules for some features but not others, depending on how services are structured.

Embedded Investment Advice in Financial Apps

Many fintech apps include features that guide users toward certain investment decisions. This can include portfolio suggestions, asset allocation tools, or prompts based on user behavior.

These features are often introduced gradually and may not be labeled as advisory services. However, once the app begins influencing user decisions about securities, it may be treated as providing investment advice.

The challenge is that these features are often integrated into broader user experiences. Compliance needs to account for how advice is delivered within the product, not just through standalone advisory services.

Technology Governance and Algorithm Oversight

As advisory functionality becomes more automated, regulators expect firms to oversee the technology driving those decisions. This includes understanding how algorithms are built, tested, and updated.

Firms need to document how models are designed and how changes are managed over time. Algorithm-driven advice still requires supervision, documentation, and review, even if decisions are generated automatically.

For fintech companies, this often involves coordination between compliance, engineering, and product teams. Clear ownership and documentation are important when explaining how the system operates during an examination.

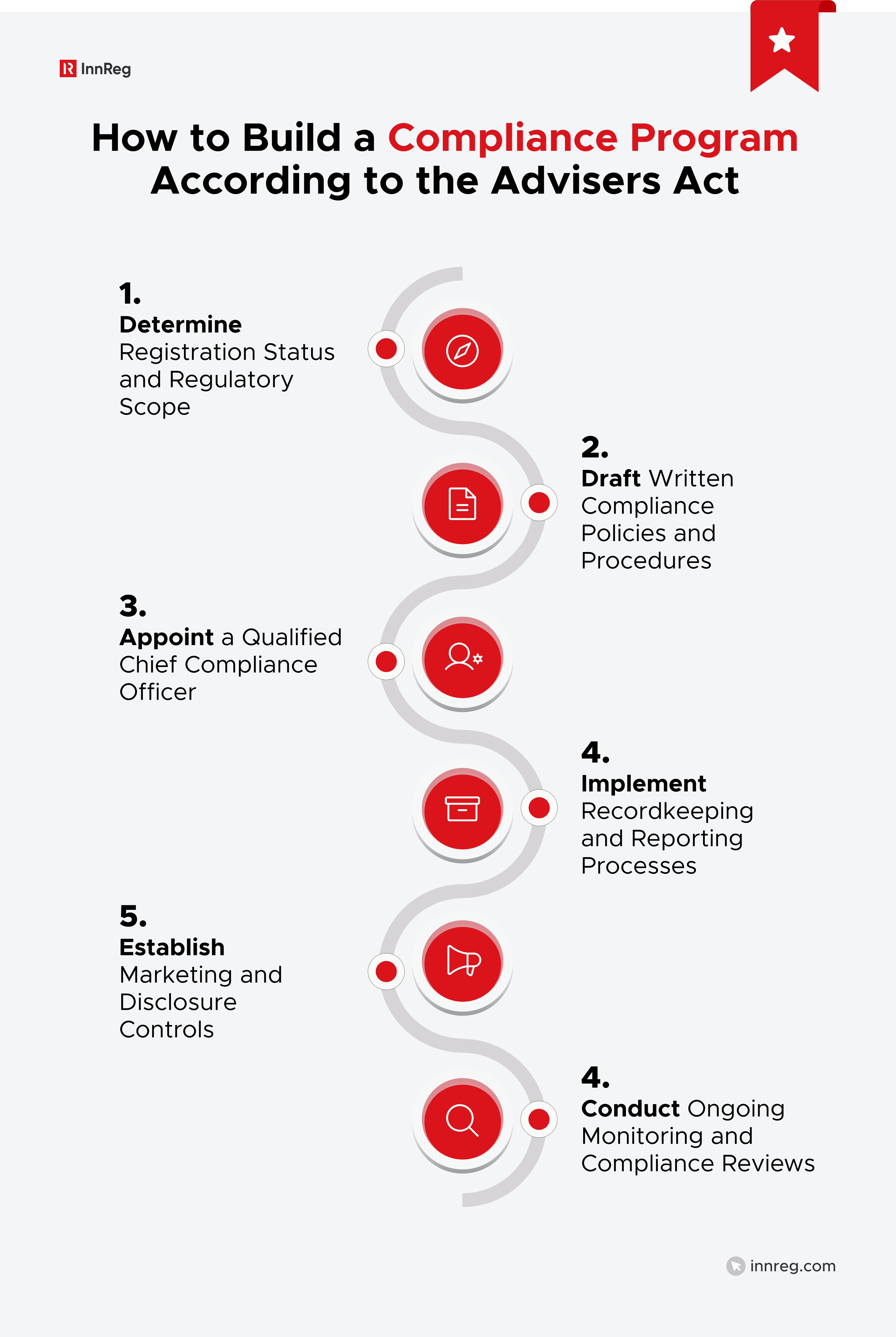

How to Build a Compliance Program According to the Advisers Act

Building a compliance program under the Investment Advisers Act rules involves aligning policies, processes, and day-to-day operations with how the business actually works. Regulators look for a program that reflects real activities.

Step 1: Determine Registration Status and Regulatory Scope

The starting point is understanding whether the firm falls within the scope of the Advisers Act and what type of registration applies. This includes evaluating services, compensation models, and how the product interacts with users.

This analysis is not always straightforward, especially for fintech models that combine multiple features.

Registration status drives the entire compliance framework, so getting this step right is critical.

Step 2: Draft Written Compliance Policies and Procedures

Once the regulatory scope is clear, firms need to document how they will manage compliance. Policies should cover key areas such as disclosures, trading, custody, marketing, and recordkeeping.

These documents should reflect how the firm actually operates. Copying generic templates often leads to gaps, especially when workflows involve technology or third-party providers.

After defining the regulatory scope, firms need to translate those requirements into written policies. These documents should outline how the firm handles key areas like disclosures, trading, custody, marketing, and recordkeeping.

The challenge is making those policies match the reality of how different aspects of the business function on the ground. This often involves aligning them with product features, internal workflows, and third-party relationships. If policies do not reflect real processes, they are difficult to follow and harder to defend during an exam.

Generic templates are a common starting point, but they rarely fit without significant changes. For fintech companies, where systems and integrations play a central role, policies need to account for how those components interact in practice.

Step 3: Appoint a Qualified Chief Compliance Officer

Firms are required to designate a chief compliance officer responsible for administering the compliance program. The CCO oversees how policies are implemented, monitors ongoing activity, and serves as the primary point of contact for regulatory matters.

The role goes beyond maintaining documentation. It involves understanding how the business operates, identifying areas of risk, and responding to issues as they arise. Regulators expect the CCO to have visibility into the firm’s operations and the authority to address compliance concerns.

In practice, this means the CCO needs access to key systems, decision-making processes, and senior leadership. For fintech firms, this often includes working closely with product, engineering, and operations teams to understand how advisory activity is delivered.

Learn how InnReg helps fintechs by providing outsourced CCO services →

Step 4: Implement Recordkeeping and Reporting Processes

Firms need systems in place to capture and retain records across their operations. This includes communications, transactions, marketing materials, and compliance documentation.

The focus is on accuracy, consistency, and accessibility. Records should be organized in a way that allows firms to explain decisions and demonstrate compliance during an examination.

Step 5: Establish Marketing and Disclosure Controls

Marketing and disclosure processes need to be closely aligned. This includes reviewing how services are described, how performance is presented, and how conflicts are communicated across different channels.

This means considering how marketing content is created, reviewed, and approved, and how it connects to formal disclosures. Differences between marketing language and disclosure documents are a common source of regulatory questions.

Controls are most effective when they are part of the workflow. When review processes happen only at the end, inconsistencies are harder to catch and correct.

Step 6: Conduct Ongoing Monitoring and Compliance Reviews

Compliance programs need to be maintained over time. This includes monitoring systems and activities, reviewing controls, and updating policies as the business evolves.

Annual reviews are part of this process, but ongoing monitoring is equally important. Changes in products, systems, or partnerships should trigger updates to the compliance program.

—

The Investment Advisers Act sets standards for how RIAs disclose information, manage conflicts, supervise activities, maintain records, and structure their compliance programs over time.

For firms operating in fintech, that framework becomes especially important because advisory features often develop gradually, through product design, automation, and integrations rather than through a traditional advisory model.

That is why the real challenge is not just identifying whether the rules apply. It is building a compliance program that matches how the business actually works. Disclosures need to align with operations, marketing needs to match formal filings, and policies need to reflect real workflows rather than generic templates.

Marina is a Compliance Consultant at InnReg with over 15 years of experience in operations and financial services. She has held senior roles at Amity Services and HSBC, with expertise in operations management, client portfolio growth, and end-to-end service delivery. She holds an MBA from the British School of Commerce.

How Can InnReg Help?

InnReg is a global regulatory compliance and operations consulting team serving financial services companies since 2013.

We are especially effective at launching and scaling fintechs with innovative compliance strategies and delivering cost-effective managed services, assisted by proprietary regtech solutions.

If you need help with RIA compliance, reach out to our regulatory experts today:

Related Articles

Featured LinkedIn Posts