Form ADV Guide for Investment Advisors and Fintechs

Form ADV is a central filing requirement for US investment advisors. It is the document that regulators, investors, and even competitors use to understand how your advisory business operates.

For fintechs, Form ADV is often the first regulatory hurdle when launching an advisory model, whether through a digital platform, robo-advisor, or hybrid investment service.

This form covers services, fees, conflicts of interest, and operational structure. The SEC and state regulators rely on it to monitor compliance, and investors use it to assess transparency. In other words, Form ADV is both a compliance obligation and a public disclosure tool.

In this article, we break down the requirements, common challenges, and recent regulatory updates to help you navigate the process with clarity.

At InnReg, we help fintech advisors and RIAs manage Form ADV filings and the broader advisory compliance framework. Our team supports registration, disclosure drafting, marketing rule alignment, and ongoing updates as your business evolves. Contact us to learn more.

What Is Form ADV?

Form ADV is the uniform application used for Investment Advisor registration. It is also the primary disclosure document that clients and prospects can review through the SEC’s public database.

The filing requirements depend on the firm’s size and activities:

SEC registration: Firms with $100 million or more in assets under management (AUM) must register with the SEC. Some firms, such as advisors to certain funds, must register with the SEC regardless of AUM.

State registration: Firms with less than $100 million AUM generally register at the state level. Most states require registration even for small firms serving local clients.

Exempt Reporting Advisors (ERAs): Certain firms, such as venture capital or private fund advisors below AUM limits, may qualify as exempt. They still file a limited version of Form ADV Part 1 to disclose basic information.

For fintech founders, this means that even an early-stage platform offering advisory services, whether algorithm-driven or hybrid, may trigger a Form ADV filing. Understanding where you fall on the SEC vs. state spectrum is one of the first compliance decisions you will face.

Regulators and Oversight

Form ADV sits at the intersection of federal and state securities regulation. Understanding who oversees your filing helps clarify why the form exists and how it will be used:

SEC and the Investment Advisers Act of 1940: SEC is the primary regulator for registered investment advisors with $100 million or more in assets under management (AUM). Its authority comes from the Investment Advisers Act of 1940, which sets the standards for advisor registration, disclosures, and fiduciary obligations. The SEC reviews Form ADV filings, conducts examinations, and can bring enforcement actions if disclosures are incomplete or misleading.

State securities regulators and NASAA: Advisors with less than $100 million AUM usually register with one or more state securities regulators. Each state enforces its own rules, though they generally follow the model framework promoted by the North American Securities Administrators Association (NASAA). States review Form ADV filings, approve registrations, and conduct routine examinations of firms.

The IARD electronic filing system: Form ADV is filed through the Investment Adviser Registration Depository (IARD). This electronic system, operated by FINRA, routes filings to the SEC or state regulators as appropriate. It also feeds into the Investment Adviser Public Disclosure (IAPD) website, where clients, prospects, and competitors can access your Form ADV.

The Parts of Form ADV Explained

Form ADV is not a single document but a collection of related parts that create a detailed picture of a firm for regulators and clients.

Each part serves a distinct purpose:

Part 1A and 1B: Core Business and Ownership Information

This section is structured as a form with checkboxes and data fields.

It captures information on a firm’s ownership, control persons, client types, advisory services, assets under management, and disciplinary history.

Part 1B applies only to state-registered advisors and adds a handful of state-specific questions.

Part 2A: The Firm Brochure

Part 2A is a narrative disclosure written in plain English. It explains services, fees, investment strategies, conflicts of interest, and how a firm is organized.

Advisors must provide this brochure to clients at the start of the relationship and keep it updated as material changes occur.

Read our article to learn more about Form ADV Part 2 →

Appendix 1: Wrap Fee Program Brochure

Advisors that sponsor wrap fee programs are required to prepare a brochure outlining the program’s terms, fee structure, portfolio manager selection process, and conflicts of interest. This brochure supplements Part 2A and is tailored specifically for wrap accounts.

Part 2B: Brochure Supplement for Individuals

This supplement provides background on the individual professionals who deliver advice. It includes education, professional history, disciplinary record, and compensation arrangements.

While not filed with the SEC, it must be available to clients and to regulators during exams.

See also:

Part 3 (Form CRS): Client Relationship Summary

Form CRS is a short, standardized disclosure that SEC-registered investment advisors must provide to retail clients.

It includes information about services, fees, and conflicts in a two-page format that is designed for easy comparison across firms.

Need help with RIA compliance?

Fill out the form below and our experts will get back to you.

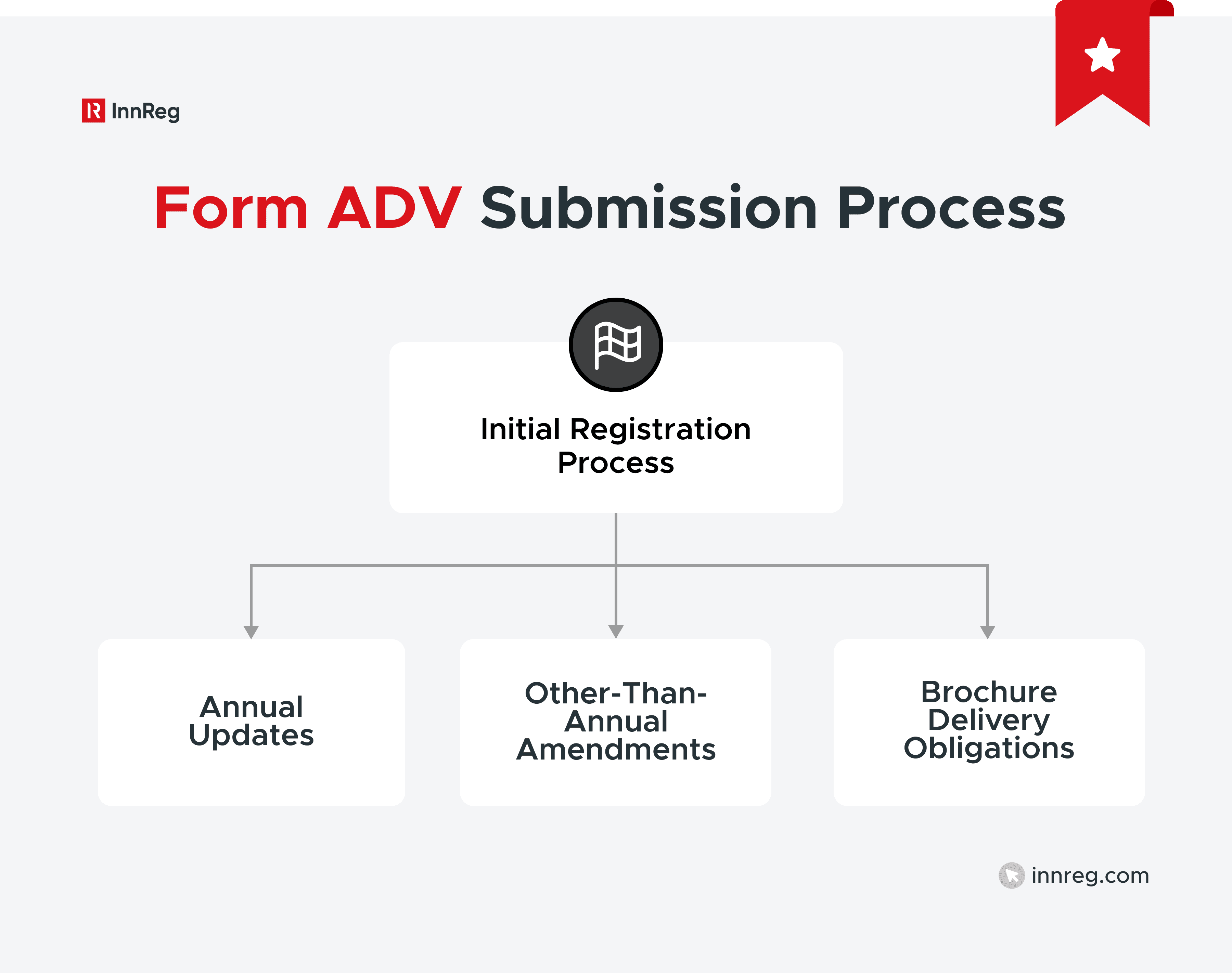

Filing Form ADV: Process and Timing

Form ADV is an ongoing requirement that follows a structured timeline:

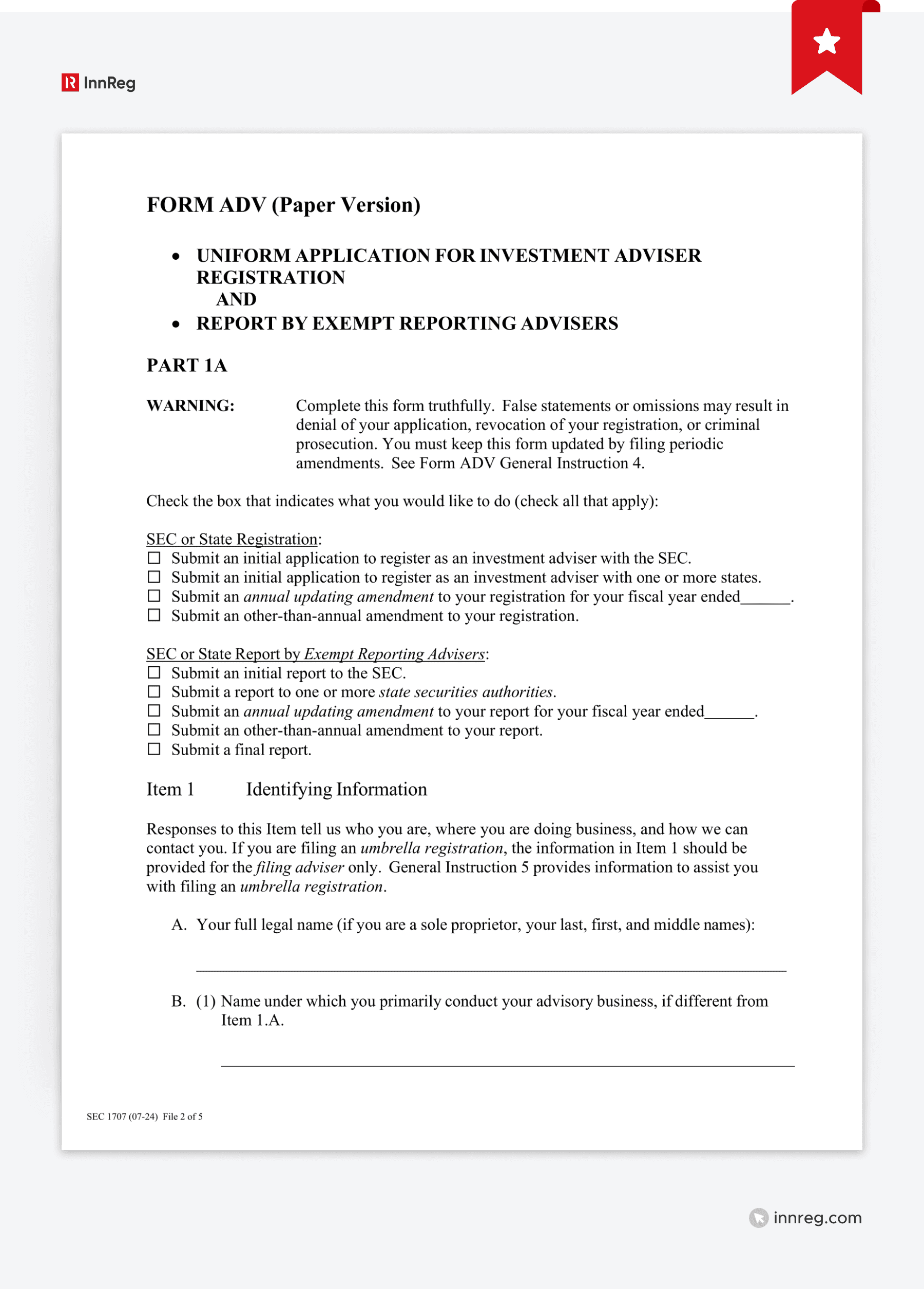

Initial Registration Process

A new advisor must submit Form ADV through the IARD system before starting advisory activities. The filing includes Part 1, Part 2A, Appendix 1, Part 2B (for supervised persons), and for SEC-registered Advisors, Part 3.

For SEC-registered advisors, the Commission generally has up to 45 days to approve or deny the application. States’ timelines can exceed 45 days, though the process varies by jurisdiction.

Annual Updating Amendment Requirements

Every advisor must amend Form ADV at least once a year. This annual updating amendment is due within 90 days of the end of the firm’s fiscal year.

It updates core information such as assets under management, client numbers, and any changes to services or fees. Even if nothing has changed, firms must still submit a filing confirming accuracy.

Other-Than-Annual Amendments

Material changes cannot wait until year-end. If information in Form ADV becomes inaccurate or misleading, advisors must file an other-than-annual amendment promptly. Examples include changes to firm ownership, new conflicts of interest, or new websites and social media accounts.

Brochure Delivery Obligations to Clients

Filing with regulators is only part of the responsibility. Advisors must also deliver an updated Part 2A brochure to new clients at or before the start of the relationship.

Existing clients must receive either the updated brochure or a summary of material changes within 120 days of the fiscal year-end. Part 2B supplements and Form CRS (if applicable) follow similar delivery requirements.

Common Compliance Challenges with Form ADV

Filing Form ADV is not simply about completing forms once a year. The real challenge lies in keeping disclosures accurate, consistent, and aligned with how your business actually operates.

For fintech firms moving quickly, this can be a particular pressure point.

Accuracy and Honesty in Disclosures

Form ADV requires complete and truthful information. Even some minor omissions (e.g., missing a conflict of interest or failing to list all advisory personnel) can trigger regulatory scrutiny.

The SEC has fined firms for failing to update ownership changes or misrepresenting how fees are charged.

Timeliness of Filings and Updates

Annual updates are due within 90 days of the fiscal year-end, and material changes require prompt amendments. Late filings, even if accidental, can lead to penalties or suspension at the state level. Compliance calendars and clear ownership of filing tasks are critical to staying current.

Inconsistent Marketing vs. Disclosures

What is stated in the marketing materials must align with what appears in your Form ADV.

Regulators often compare brochures with websites, pitch decks, and client communications. If an app or website describes services not disclosed in Form ADV, or downplays risks highlighted in your brochure, that mismatch can raise red flags.

Read our article to learn more about the SEC Marketing Rule →

Operational Changes in Fast-Moving Fintechs

Startups pivot quickly, adding new services, asset classes, or client segments.

Each change can affect what needs to be disclosed in Form ADV. Without a process to review disclosures during business shifts, firms risk operating with outdated filings.

Recordkeeping and Supporting Documentation

Disclosures in Form ADV must be backed up by records. If you state you manage $50 million in assets, regulators may ask to see the data behind that number. If you disclose quarterly reviews, you should have logs proving they happened. For digital-first firms, good recordkeeping also includes archiving client communications and marketing content.

See also:

Hidden Challenges in Form ADV Compliance

Some aspects of Form ADV compliance are less obvious but can create real issues for fintech firms if overlooked:

Navigating Dual Registrations (RIA + Broker-Dealer)

Firms that operate as both a registered investment advisor (RIA) and a broker-dealer must comply with two regulatory regimes.

Form ADV disclosures must accurately reflect the advisory side, while FINRA rules apply to the broker-dealer. Inconsistencies with disclosures between the two business types can raise concerns.

Additional resources: | |

|---|---|

ERA Filings and “Exempt But Reporting” Status

Exempt Reporting Advisors (ERAs) are not fully registered, but they still must submit a shortened Form ADV Part 1A. Many fintechs mistakenly think “exempt” means no filing at all, which can create compliance gaps later during audits, fundraising, or regulatory reviews.

Social Media, Digital Marketing, and Disclosure Obligations

Form ADV must include all firm-controlled websites and social media accounts. This requirement often surprises fintech firms that use multiple channels for client engagement.

Each platform likely requires disclosures and recordkeeping obligations. Regulators may review these accounts against the firm’s Form ADV for inconsistencies.

Operational Changes That Require Mid-Year Amendments

Product pivots, new asset classes, or revised fee models are common in fintech. Each can materially affect disclosures in Form ADV.

Waiting until the next annual update to make changes can leave filings inaccurate for months. Building a process to review disclosures before business models shift is essential.

Recent Developments in Form ADV

Form ADV requirements evolve as regulators respond to market practices. Both the SEC and state agencies update rules and guidance, and they bring enforcement actions when firms fall short.

Social Media and Website Disclosure Rules

Since 2017, advisors must disclose all firm-controlled websites and social media accounts in Form ADV.

This applies to LinkedIn, Twitter, Facebook, Instagram, and other platforms used for client communication. Regulators may review these accounts and compare them against your disclosures.

For firms active across multiple channels, this means every new official account creates a disclosure and recordkeeping obligation.

Designed based on InnReg’s experience of working with 100+ fintechs, Regly helps firms centralize reviews and audit trails →

See also:

Form CRS Implementation and Enforcement Actions

Form CRS became mandatory in June 2020 for SEC-registered advisors serving retail clients. It must be filed, kept current, and delivered to both new and existing clients.

The SEC has already fined advisors for failing to file or deliver Form CRS on time, showing that regulators treat it as a priority.

Marketing Rule Changes and New ADV Item 5.L

The SEC Marketing Rule, which took effect in late 2022, redefined how advisors may use testimonials, endorsements, ratings, and performance results in their advertising.

To monitor compliance, the SEC introduced Item 5.L in Form ADV Part 1, requiring firms to disclose whether they rely on these practices.

Learn more about the SEC Marketing Rule →

SEC Focus on ESG Disclosures

As more advisors highlight environmental, social, and governance (ESG) strategies, the SEC has cautioned firms not to exaggerate or misstate how these factors are used.

Form ADV Part 2A should clearly describe how ESG considerations shape investment advice. Regulators have already taken action against firms with inaccurate ESG disclosures.

Learn more about Form ADV Part 2 →

Crypto and Digital Asset Considerations

Fintech advisors offering digital asset advice must treat it like any other security-related service in Form ADV. Risks tied to custody, volatility, and regulation should be described in the brochure. Skipping these disclosures can become an issue in regulatory examinations.

Best Practices for Managing Form ADV Compliance

Treating Form ADV as an ongoing obligation is essential. The following practices help in aligning it with your business:

Building Form ADV Into Product and Business Decisions: Every time your business adds a new service, changes its fee model, or enters a new client segment, consider how it affects Form ADV. Involving compliance staff early in product discussions helps keep disclosures current and accurate.

Internal Calendars and Reminders: Annual filings are due within 90 days of the fiscal year-end, and client brochure delivery must follow within 120 days. Setting clear deadlines, along with internal milestones for drafting, reviewing, and filing, helps avoid late submissions.

Plain Language and Client-Focused Disclosures: The SEC requires that Part 2A be drafted in plain English. Stripping out jargon and unclear phrasing makes the brochure easier for clients to understand and helps demonstrate transparency.

Consistency Across ADV, Contracts, and Marketing: Regulators often review Form ADV alongside your website, marketing materials, and client agreements. Any inconsistencies can raise concerns. Checking new documents against your ADV can help you with messaging alignment.

Using Technology and Outsourcing Support: Compliance management tools and outsourced specialists like InnReg can help track changes, archive records, and manage filings. For growing fintechs, this approach can be more practical than relying on a single in-house officer.

Maintaining Change Logs and Version Control: Maintain records of every amendment along with the reasons for the change. Having this audit trail helps during regulatory exams and clarifies your decisions for clients or investors.

Staying Current With Regulatory Updates: The SEC frequently revises guidance and expectations. Assign responsibility within your team, or to an outsourced compliance partner, for monitoring rule changes, enforcement actions, and FAQs that affect Form ADV.

InnReg helps fintechs keep up with the SEC expectations. Contact us to learn how we can help you.

—

Form ADV is a public document that defines how a firm is seen by regulators, clients, and investors.

For fintechs, it often marks the first major compliance milestone and sets the tone for how the business will be supervised going forward.

Managing Form ADV well means treating it as an important ongoing obligation. Accurate disclosures, timely updates, and consistency across your marketing and operations are key to mitigating regulatory issues and building credibility with stakeholders.

Tarik is a Principal Compliance Consultant at InnReg with over 5 years of experience advising fintech clients across broker-dealer, RIA, and money transmitter verticals. He holds FINRA Series 3, 7, 24, 57, 63, 79, and 99 licenses, with expertise in regulatory strategy, supervisory systems, and compliance roadmap implementation.

How Can InnReg Help?

InnReg is a global regulatory compliance and operations consulting team serving financial services companies since 2013.

We are especially effective at launching and scaling fintechs with innovative compliance strategies and delivering cost-effective managed services, assisted by proprietary regtech solutions.

If you need help with RIA compliance, reach out to our regulatory experts today:

Related Articles

Featured LinkedIn Posts