Suitability vs. Best Interest: What’s the Difference?

Key Takeaways

The suitability standard requires a recommendation to be appropriate for a client’s financial situation and objectives.

The best interest standard requires firms and representatives to put the client’s interests ahead of their own when making recommendations.

Suitability and best interest are often used interchangeably, but they’re not the same. Each standard creates different obligations for firms and representatives, and applying the wrong one can lead to regulatory risk that may only surface during an exam.

This article explains how the suitability standard under FINRA rules differs from the best interest obligations under Regulation Best Interest (Reg BI). It also looks at the fiduciary duty that applies to investment advisors.

InnReg helps broker-dealers, RIAs, and fintech platforms interpret and apply suitability, Regulation Best Interest (Reg BI), and fiduciary standards in real-world operations. If you need support aligning policies, supervision, and documentation with these regulatory obligations, contact us to learn how our compliance team can help.

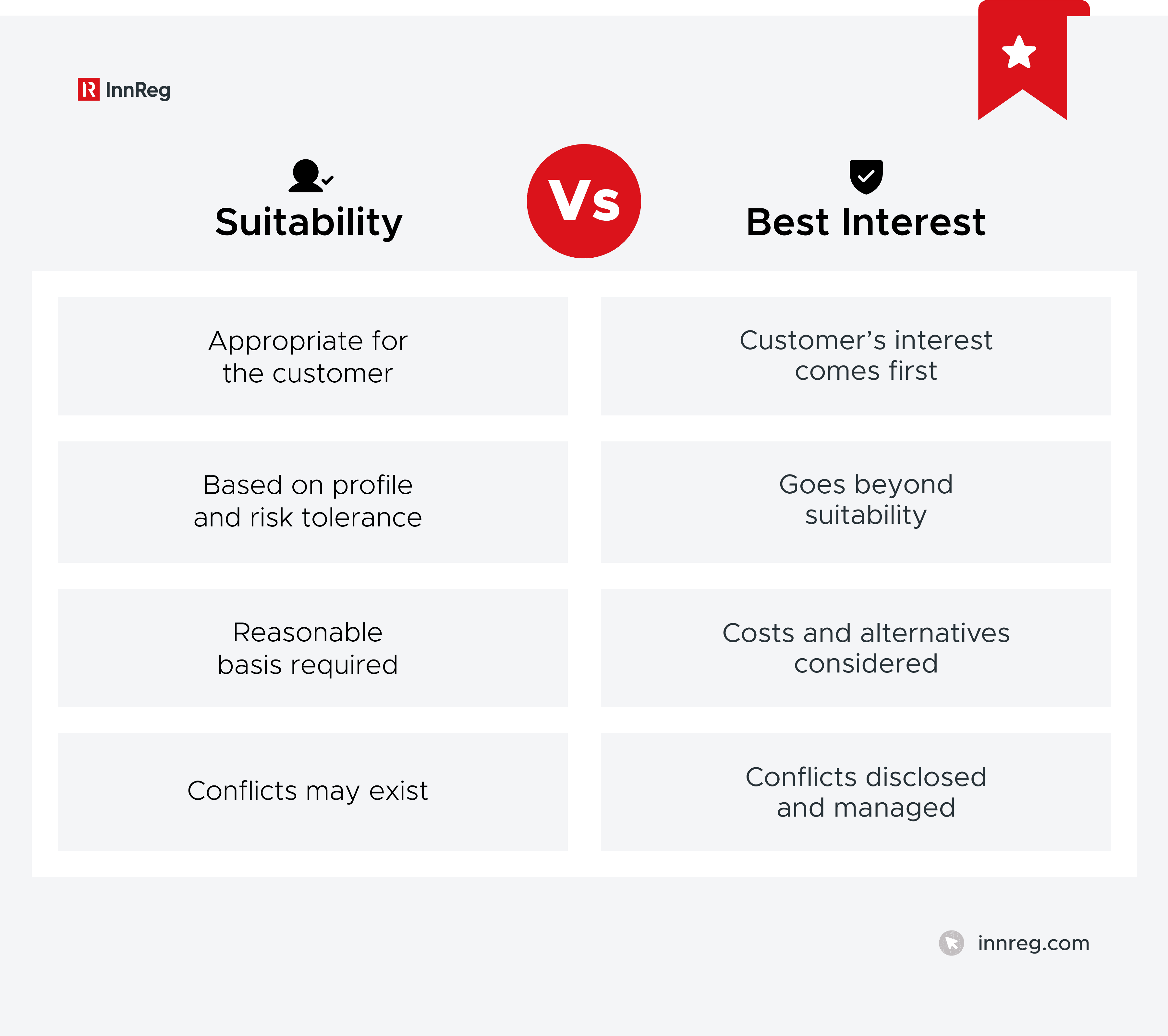

Suitability vs. Best Interest at a Glance

The simplest way to understand suitability vs. best interest is to look at what each standard asks of the firm when making a recommendation.

Suitability focuses on whether a product or strategy fits the customer’s profile. Best interest goes further. It requires the firm to put the retail customer’s interests ahead of its own when making that recommendation.

A broker following the suitability standard must have a reasonable basis to believe a recommendation fits the client’s:

Financial situation

Goals

Risk tolerance

That analysis is still required under the best interest standard, but it isn’t enough on its own. Firms must also:

Manage conflicts of interest

Provide clear disclosures

Avoid putting their financial incentives ahead of the client’s interests

One simple way to understand the difference is this. Suitability asks, “Is this appropriate for the customer?” Best interest asks, “Is this recommendation being made in the customer’s interest rather than the firm’s?”

This distinction may sound subtle, but regulators treat it as a meaningful difference that affects supervision, documentation, and product governance.

When Does the Standard Apply? Understanding “Recommendations”

Both standards apply only when a recommendation is made. They don’t cover every interaction with a client, which makes the definition of a recommendation one of the most important and often misunderstood concepts in this area.

SEC and FINRA Definition of a Recommendation

Regulators assess whether the customer would reasonably view a communication as a call to action. A recommendation doesn’t have to be explicit. It can be implied through:

Wording

Presentation

Context

Saying something is “educational” or “informational” won’t matter if the message steers the customer toward buying, selling, or holding a particular security or strategy. Firms should assume that anything tailored to an individual’s situation could be viewed as a recommendation.

This interpretation matters because once a communication is treated as a recommendation, the applicable standard immediately applies. The firm must then show that the recommendation met either the suitability or the best-interest obligations based on the relationship with the customer.

Account-Type and “Hold” Recommendations

Recommendations aren’t limited to buy-or-sell decisions. Account-type recommendations and recommendations to hold securities can also trigger suitability or best interest obligations.

Account-type recommendation: This can include suggesting a brokerage account instead of an advisory account, or recommending that a client move money from an employer retirement plan into an IRA. Under Regulation Best Interest, broker-dealers must consider costs, services, and other reasonable options before making that recommendation.

“Hold” recommendations: These include telling a customer to keep an existing investment, remain concentrated in a single stock, or avoid changing their portfolio after market volatility. Even encouraging a customer to take no action can be treated by regulators as a recommendation.

Digital Prompts, Nudges, and Algorithmic Outputs

Recommendations don’t just come from human conversations. Digital prompts, nudges, and algorithmic outputs can also qualify as recommendations. If a platform steers a user toward a specific action, regulators will scrutinize how and why that happened.

For example, a push notification highlighting a “top pick,” a default portfolio allocation that favors certain products, or a pop-up suggesting a rebalance after recent market moves can all influence investment decisions. Even when no person is directly involved, these communications and design choices can shape how users act.

Because of this, regulators focus on how a reasonable investor would interpret the message. If the wording, design, or timing encourages a particular transaction or strategy, it may be treated as a recommendation.

Labels like “educational” or “for you” won’t change that analysis if the functionality pushes users in a specific direction.

When No Trade Still Creates Regulatory Exposure

It’s a common mistake to assume that if no trade occurred, no regulatory standard applies. Regulators don’t see it that way. A recommendation can exist even when the result is inaction.

Telling a client to stay concentrated in a single stock is a recommendation. Encouraging investors to ride out volatility without reallocating is also considered one, and can trigger suitability or best interest obligations.

This is where firms get caught off guard. Buy-and-sell activity is usually documented and supervised. Hold recommendations often aren’t. If your communication influenced the client’s choice, you’ll need to show how the applicable standard was met.

What Is the Suitability Standard?

The suitability standard sets the baseline for broker-dealers when making recommendations. It asks whether a product or strategy fits the customer’s profile, goals, and risk tolerance.

Suitability has three main parts:

Reasonable-basis suitability: You need to understand the product and its risks before recommending it and have a reasonable basis to believe it is suitable for some investors.

Customer-specific suitability: The recommendation should match the individual customer’s investment profile.

Quantitative suitability: When a registered representative (RR) has de facto control over a customer account, regulators check trading patterns over time to spot excessive activity in light of the customer’s investment profile.

Legal Basis: FINRA Rule 2111 and Related Guidance

The suitability standard is grounded in FINRA Rule 2111. It requires a broker to have a reasonable basis to believe a recommendation is suitable for the customer based on that customer’s investment profile.

Based on the FINRA rule, that profile should include:

Age

Other investments

Income

Net worth

Tax status

Investment objectives

Investment experience

Investment time horizon

Liquidity needs

Risk tolerance

Any other information a customer discloses in connection with a recommendation.

If you’re making a recommendation, you’re expected to understand those details first. If the customer profile is thin or outdated, your suitability analysis will be too.

Regulators also rely on guidance, notices, and enforcement history. If your supervisory system hasn’t kept up with those interpretations, that gap can show up during an exam.

Read our guide to FINRA Rule 2111 →

Who Is Subject to the Suitability Standard

The suitability standard generally applies to broker-dealers and their representatives. Investment advisors, however, are held to a fiduciary standard. Firms that operate as both must determine which standard applies based on the type of relationship and service being provided.

The Three Components of FINRA Suitability

FINRA breaks suitability into three parts:

Reasonable-basis suitability: You have to understand the product or strategy before recommending it. If you don’t understand how it works, who it’s designed for, or its risks, you shouldn’t be recommending it.

Customer-specific suitability: The recommendation must fit the customer’s investment profile. A high-risk product might be suitable for one client and completely inappropriate for another.

Quantitative suitability: Even if each trade looks suitable on its own, excessive trading can still create problems. Regulators review who has control of the account, turnover ratios, cost-to-equity ratios, and cost impact over time.

Suitability isn’t just about the product. It’s about the match between the product, the customer, and the overall pattern of activity in the account.

Institutional Customer Considerations

Institutional customers operate differently from individual investors. They often have more resources, expertise, and internal controls. That means your recommendations need to match their objectives and risk tolerance.

Institutions also come in many forms. Pension funds, endowments, and hedge funds each have their own goals, liquidity needs, and risk limits. Knowing the type of institution you’re working with helps tailor your recommendations. A long-term strategy that works for a pension fund might not suit a short-term hedge fund.

Documentation is important, too. Many institutions have committees, policies, and compliance rules that guide their decisions. Your analysis should take these processes into account. Showing that you’ve considered the institution’s guidelines makes it clear that your recommendation is well thought out.

See also:

What Suitability Does Not Cover

Suitability rules require a recommendation to fit the customer’s profile. They don’t cover every part of investing. They don’t guarantee returns or protect against market losses. Even suitable investments can go down in value!

Suitability doesn’t replace other legal or regulatory obligations. Brokers still have to comply with disclosure rules, anti-fraud laws, and any contracts with customers. Meeting suitability alone isn’t enough to avoid liability.

Suitability isn’t a risk-free shield. Customers’ circumstances change, and what was suitable before might not be suitable now. Ongoing monitoring and maintaining updated investment profiles are still important.

Need help with fintech compliance?

Fill out the form below and our experts will get back to you.

Limitations of the Suitability Standard

The suitability standard has real limits worth understanding:

It focuses on whether a recommendation fits the customer’s profile, not on maximizing returns or avoiding all risks.

It depends on the information available. Incomplete or outdated client profiles can create gaps in the analysis.

It doesn’t require ongoing monitoring as a customer’s goals, finances, and risk tolerance change over time, but it does require recommendations to be suitable at the time they are made.

It doesn’t guarantee investment performance or protect against losses.

It doesn’t cover all legal or regulatory responsibilities on its own.

These limitations show the boundaries of the suitability standard. Keeping customer information up to date and reviewing client profiles regularly helps support better recommendations.

What Is the Best Interest Standard?

The best interest standard goes beyond suitability. It asks brokers to put the customer’s interests first when making recommendations. That means recommending products and strategies that serve the customer, not just ones that meet their profile.

It applies mainly to investment advisors and certain broker-dealers in specific situations.

Best Interest for Broker-Dealers (Reg BI)

The best interest standard under Regulation Best Interest (Reg BI) builds on suitability but adds extra requirements around:

Conflicts

Disclosure

Documentation

Broker-dealers still need to evaluate whether a recommendation is a good fit for the customer. They also have to identify potential conflicts, provide clear disclosures, and show how the customer’s interests are prioritized.

It’s important to note that Reg BI applies whenever a recommendation is made to a retail investor, not just when a trade occurs, i.e., account-type recommendations.

Learn more about Regulation Best Interest (Reg BI) →

The Four Core Obligations

Reg BI outlines four key obligations.

Obligation | What It Requires | What Firms Must Do in Practice |

|---|---|---|

Disclosure Obligation | Provide full and fair disclosure of material facts about the relationship, services, costs, and conflicts | Deliver Form CRS and explain fees, compensation structures, and material conflicts clearly |

Care Obligation | Exercise reasonable diligence, care, and skill when making a recommendation | Evaluate the customer’s profile, consider costs, risks, and reasonably available alternatives, and document the analysis |

Conflict of Interest Obligation | Identify, disclose, and mitigate or eliminate certain conflicts | Review compensation structures, sales incentives, revenue sharing, and product preferences |

Compliance Obligation | Establish, maintain, and enforce written policies and procedures | Implement supervision, training, testing, and recordkeeping aligned with Reg BI |

Documentation and Disclosure Expectations

Documentation and disclosure play a significant role in meeting suitability and best-interest standards. They show that a recommendation considered the customer’s profile and followed proper processes.

For disclosures, firms must clearly explain costs, fees, and conflicts of interest. Customers should also understand how a recommendation may affect their finances and what alternatives were considered.

Key points for documentation include:

Keep records of the recommendation and how it fits the customer’s profile

Document the decision-making process and the options considered

Show how conflicts of interest were addressed

Maintain notes that support supervision and review

Proper documentation shows the firm acted responsibly and kept the customer’s interest in mind. Regularly updating records and disclosures helps keep the process transparent and mitigates risk over time.

Best Interest for Investment Advisors (Fiduciary Duty)

Investment advisors operate under a fiduciary duty, which is a higher standard than suitability or even Reg BI. They must always put the client’s interests first and act with honesty, care, and full transparency.

Duty of Care

Advisors should make recommendations based on a thorough understanding of the client’s financial situation, goals, and risk tolerance. This means analyzing options carefully, considering costs and risks, and explaining alternatives so the client can make informed decisions.

Duty of Loyalty

Advisors should avoid conflicts of interest or, if unavoidable, manage them in a way that prioritizes the client. Their own compensation, incentives, or business goals shouldn’t influence the advice they give. Being upfront about potential conflicts builds trust and clarity.

Monitoring and Scope

Fiduciary duty doesn’t end after a single recommendation. Advisors should monitor accounts, review strategies, and adjust advice as the client’s goals, finances, or risk tolerance change. Ongoing attention helps keep recommendations aligned with what’s truly best for the client.

Suitability vs. Best Interest: Side-By-Side Comparison

Suitability and best interest may sound similar, but they create very different obligations for firms and representatives. Here are the key differences.

Differences in Legal Standard

Suitability assesses whether a recommendation aligns with the customer’s profile, including age, risk tolerance, financial situation, and investment goals.

Best interest goes further. It requires the firm to put the customer’s interests ahead of its own, so that the recommendation serves the client, not the firm’s revenue or incentives.

See also:

Differences in Conflict of Interest Treatment

Under suitability, conflicts of interest can exist as long as the recommendation matches the customer’s profile. Best interest requires firms to identify, disclose, and mitigate conflicts so they do not influence the recommendation.

The objective is to place the customer’s needs first in every decision.

Differences in Disclosure Requirements

Under the suitability standard, firms follow general disclosure rules, but there isn’t a separate requirement to provide detailed explanations beyond what regulations already call for.

Best interest raises the bar. Firms need to clearly explain costs, fees, and any potential conflicts tied to the recommendation. Customers should understand how the recommendation may affect their finances and what alternatives were looked at before it was made.

Differences in Ongoing Monitoring Obligations

Suitability focuses on the recommendation at the time it’s made. Once the recommendation is complete, ongoing review isn’t specifically required.

Best interest adds a duty to monitor accounts, review strategies, and adjust recommendations if the customer’s goals, finances, or risk tolerance change. This ongoing attention helps keep advice aligned with what’s truly best for the customer.

Aspect | Suitability | Best Interest (Reg BI/Fiduciary) |

|---|---|---|

Legal Standard | Fits customer profile | Puts customer interest first |

Conflict Treatment | Conflicts may exist | Identify, disclose, and mitigate conflicts |

Disclosures | General regulatory requirements | Clear, specific, meaningful disclosures |

Monitoring | One-time evaluation | Ongoing review and adjustments as needed |

This comparison shows that suitability is a baseline standard, while best interest imposes stronger obligations regarding conflicts of interest, disclosure, and ongoing care.

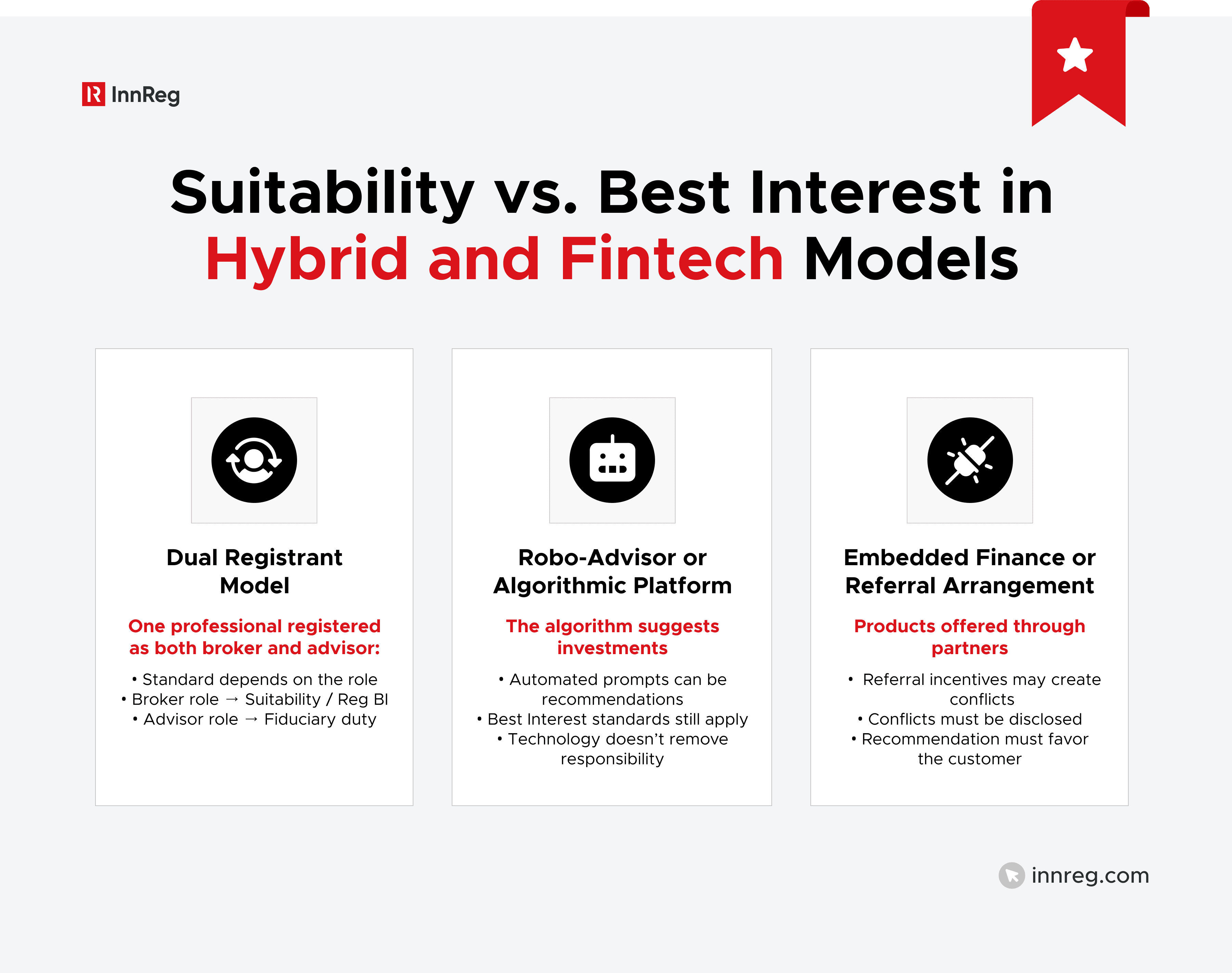

Suitability vs. Best Interest in Hybrid and Fintech Models

Technology and hybrid business models can make it harder to apply suitability and best interest standards. Firms need to be careful when roles, tools, and products overlap.

Dual Registrants and Overlapping Standards

Some professionals are both registered representatives and investment advisors. That means a recommendation could trigger either suitability or fiduciary obligations, depending on their role at the time.

Firms need clear policies that address these overlaps and apply the correct standard.

Robo-Advisors and Algorithmic Recommendations

Automated platforms and digital tools can offer personalized guidance to customers. Even though a human isn’t making the suggestion, the output can still count as a recommendation.

If the system steers someone toward a specific investment or strategy, regulators may treat it the same way they’d treat advice from a human representative.

That means firms can’t treat the technology as hands-off. The algorithm needs to take the customer’s profile, costs, and available alternatives into account. Firms also need to explain how those recommendations are generated so customers understand what’s behind the suggestion.

Digital Assets and Complex Products

Products like cryptocurrencies or alternative investments can be high-risk and complex. Suitability requires a fit with the customer’s profile. Best interest adds a duty to explain risks, disclose conflicts, and consider whether alternatives better meet the customer’s needs.

See also:

Embedded Finance and Referral Arrangements

When financial products are embedded in other services or offered through referral arrangements, conflicts of interest can arise.

Firms must disclose these relationships, mitigate conflicts, and confirm that recommendations align with the customer’s interests rather than the firm’s or a partner’s incentives.

Common Compliance Challenges

Applying suitability and best interest standards isn’t always straightforward. Firms often struggle with consistency, documentation, and managing conflicts while keeping the customer’s interests first.

Here are the most common compliance challenges.

Conflicts of interest and compensation structures: Compensation models can create real or perceived conflicts of interest. Firms must disclose these conflicts, mitigate their impact, and confirm that the recommendations genuinely serve the customer’s interests.

Product complexity and retail investor risk: Complex products can be hard to understand. Advisors need to match them to the client’s profile and clearly explain the risks.

Supervisory systems and written policies: Clear policies and strong supervision help track recommendations, conflicts, and disclosures.

Marketing language and disclosure misalignment: Marketing must match disclosures. Wording should be clear and align with regulatory standards.

Training representatives on standard differences: Representatives who act in multiple roles or use digital tools need proper training on the differences between suitability, Reg BI, and fiduciary duty.

Recent Enforcement Trends and Regulatory Focus

Regulators have been paying close attention to how firms meet their suitability and best-interest obligations. Recent enforcement actions reveal where gaps often arise and which areas receive the most scrutiny.

What Changed with Reg BI in 2020

Regulation Best Interest (Reg BI) went into effect in June 2020, creating a new standard for broker-dealers when making recommendations to retail customers. It built on suitability but added stronger requirements around conflicts of interest, disclosure, care, and compliance procedures.

Before Reg BI, broker-dealers mainly focused on whether a recommendation fit a customer’s profile. After Reg BI, they had to document how the recommendation served the customer’s interest, disclose potential conflicts, and show that they considered costs, risks, and alternatives.

The change aimed to bring broker-dealer standards closer to the expectations investors already had for fiduciary advisors. Firms had to update policies, train staff, and improve recordkeeping to meet these new obligations.

SEC Reg BI Enforcement Themes

Since Reg BI went into effect, the SEC has paid close attention to how broker-dealers apply the standard when making real-world recommendations. It’s not just about written policies. It’s about what actually happens when advice is given.

The SEC has also looked closely at digital platforms, algorithmic advice, and complex products. This is to prevent technology from creating hidden conflicts or obscuring risks for retail customers.

FINRA Suitability Enforcement That Still Matters

The SEC is focusing on how broker-dealers actually put the customer’s interests first. Enforcement actions often highlight failures to disclose conflicts, properly document recommendations, or demonstrate that the customer’s needs were prioritized.

This scrutiny also extends to digital platforms and algorithmic advice. Regulators are examining whether automated recommendations create hidden conflicts or steer customers toward products that don’t serve their best interests.

Examination Focus Areas

Regulators pay close attention to how firms follow suitability and best-interest standards. They look at recommendations, disclosures, and how conflicts of interest are managed to confirm that the customer’s needs come first.

Examiners also review training and supervision. They want to see that staff understand the rules and apply them consistently, especially when dealing with complex products or digital tools.

Documentation Failures That Trigger Findings

Regulators often flag cases where documentation is incomplete or missing. Without proper records, it’s hard to show that a recommendation met suitability or best-interest standards.

Common problems include:

Failing to record the customer’s profile

Obtaining incomplete customer profile information

Skipping details on how a recommendation fits their goals

Failing to note conflicts and disclosures.

Gaps in supervisory reviews and ongoing monitoring also catch regulators’ attention.

Misconceptions About Suitability vs. Best Interest

Even experienced firms sometimes get the standards mixed up. Some misconceptions include:

“Best interest” means lowest cost: Best interest doesn’t automatically mean recommending the cheapest product. It means making a recommendation that puts the customer’s overall interests first.

Disclosures alone fix conflicts: Simply disclosing a conflict doesn’t remove it. Firms still have to manage or mitigate conflicts so they don’t influence the recommendation.

Automation lowers regulatory expectations: Using robo-advisors or algorithmic tools doesn’t reduce regulatory responsibility. Firms still need to align recommendations with the customer’s profile, manage conflicts of interest, and provide clear disclosures.

Crypto is outside securities rules: Digital assets can be high risk, but they’re not automatically exempt from securities regulations.

No trade means no recommendation: Even telling a customer to hold an investment or not make a move can be a recommendation.

Clearing up these misconceptions helps firms apply the right standard every time. Understanding what "best interest" really means, managing conflicts, and staying aware of digital and complex products keep recommendations aligned with the customer’s needs and build trust over time.

—

Suitability and best interest standards both govern how financial professionals make recommendations, but they impose different levels of responsibility. Suitability focuses on whether a recommendation fits the customer’s profile, while best interest requires firms to prioritize the customer’s interests and manage conflicts that could influence the advice.

Understanding which standard applies and documenting how recommendations meet that standard are critical for mitigating regulatory risk. Clear policies, strong supervision, and transparent disclosures help firms demonstrate that recommendations are made with the customer’s interests in mind.

Frequently Asked Questions About Suitability vs. Best Interest

1. What’s the main difference between suitability and best interest?

Suitability looks at whether a recommendation aligns with the customer’s profile, including their goals, risk tolerance, and financial situation. Best interest goes a step further. It asks the firm to put the customer’s interests ahead of its own and manage any conflicts along the way.

2. Does best interest mean I should always pick the lowest-cost product?

No. Best interest isn’t about choosing the cheapest option. It means recommending the product that best serves the customer’s goals while considering costs, risks, and available alternatives.

3. Are disclosures enough to handle conflicts of interest?

Disclosures help, but they don’t fix conflicts on their own. Firms also need to manage conflicts so they don’t influence the recommendation and show that the customer comes first.

InnReg was founded in 2013 by Francesco Matteini, former Chief Compliance Officer who helped launch and scale some of the most innovative digital broker-dealers over the last two decades. He built compliance programs to support the first zero-commission broker and the first BD-sponsored investor social network. Since its founding, InnReg has attracted highly experienced fintech consultants with long careers in compliance, risk management, and a deep understanding of the fintech industry.

How Can InnReg Help?

InnReg is a global regulatory compliance and operations consulting team serving financial services companies since 2013.

We are especially effective at launching and scaling fintechs with innovative compliance strategies and delivering cost-effective managed services, assisted by proprietary regtech solutions.

If you need help with compliance, reach out to our regulatory experts today:

Related Articles

Featured LinkedIn Posts