What Is a Robo Advisor? Structure, Regulation, and Compliance

A robo advisor is often described as simple investing automation. In practice, it sits at the intersection of software, financial advice, and regulation.

For fintech founders and executives, that intersection is where most of the real complexity lives.

This article breaks down what a robo advisor actually is, how these platforms operate, and when they become regulated investment advisors under US law. We’ll walk through the core components of a robo advisor, the regulators involved, and the compliance obligations that apply once personalized investment advice enters the picture.

At InnReg, we help fintech companies design, register, and operate robo advisor platforms within the US regulatory framework. Contact us to learn more.

What a Robo Advisor Actually Is

A robo advisor is a digital platform that provides automated investment advice to users. That advice typically covers portfolio construction, asset allocation, and ongoing management, with limited or no direct human involvement.

What matters from a regulatory perspective is not the technology, but the outcome. If the platform uses client-specific inputs to recommend or manage securities portfolios, it is providing investment advice. The fact that the advice is generated by software does not change how regulators view the activity, although it can determine who regulates the advisor.

Most robo advisor platforms rely on algorithms grounded in established portfolio management concepts, often implemented through low-cost ETFs. The system determines how client assets are allocated, rebalanced, and maintained over time. In many cases, the platform also has discretionary authority to trade on the client’s behalf once the account is opened.

How a Robo Advisor Works: The Core Components

A robo advisor combines user-facing software with backend investment logic and regulated financial infrastructure. While implementations vary, most platforms follow a similar operational flow from onboarding through ongoing portfolio management.

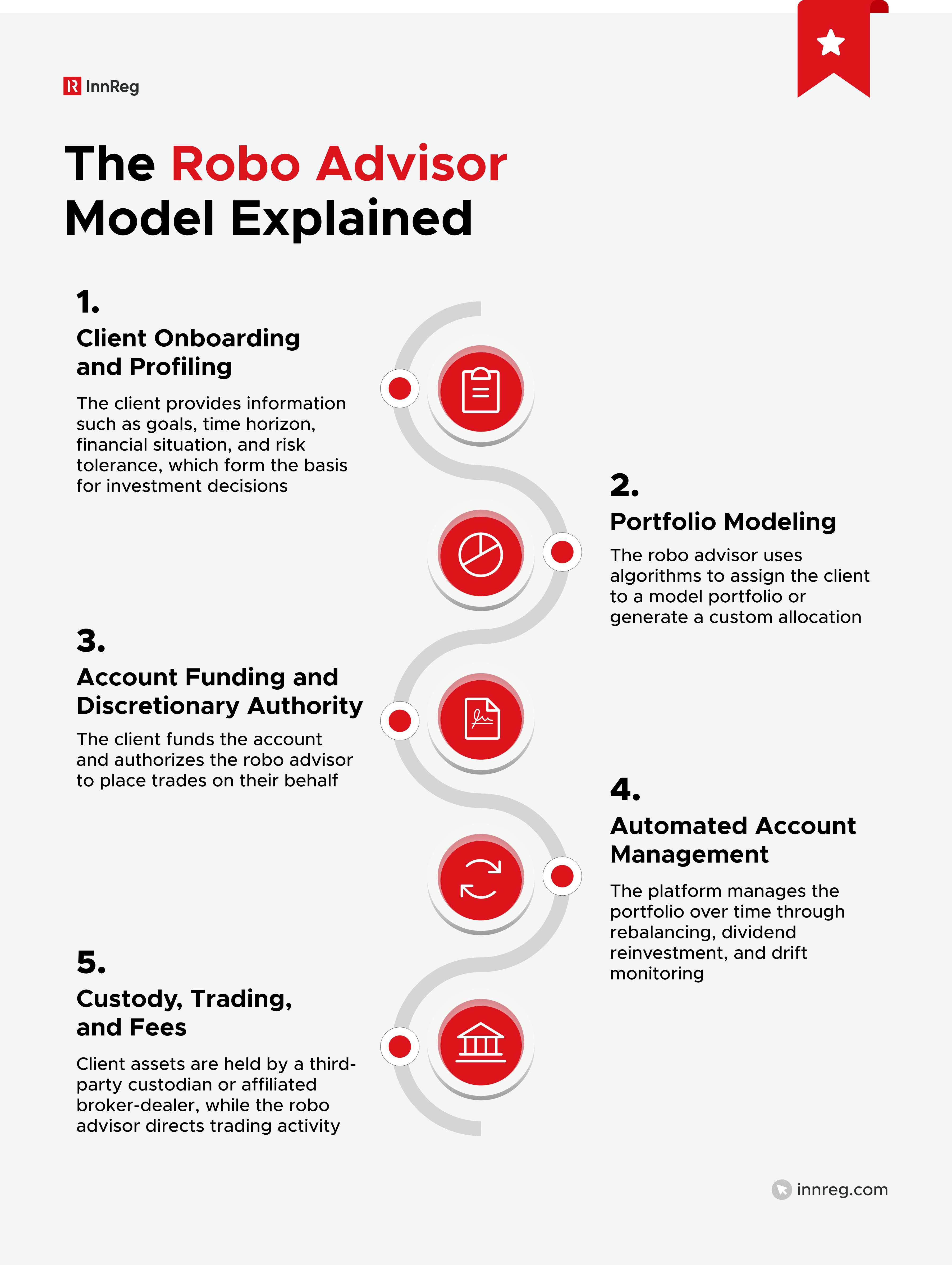

Client Onboarding and Profiling

The process typically starts with a digital onboarding flow. Users are asked a series of questions about goals, time horizon, financial situation, and risk tolerance.

These inputs drive everything that follows. If the questionnaire collects client-specific information and feeds directly into portfolio recommendations, it becomes part of the regulated advice process. Poorly designed questions or limited ability to surface inconsistencies are common regulatory weak points.

From a compliance standpoint, onboarding is where suitability begins. The platform must be able to explain how client responses map to investment outcomes.

See how InnReg helps fintechs optimize client onboarding →

Portfolio Modeling

Once user data is collected, the robo advisor assigns the client to a model portfolio or generates a custom allocation.

Most platforms rely on predefined models built around asset classes such as equities, fixed income, and cash equivalents, often implemented through ETFs. The algorithm determines asset allocation logic, rebalancing thresholds, and any tax-related strategies offered.

This modeling process must be documented. Regulators expect firms to understand, test, and supervise how portfolio decisions are generated, even when no human is involved day to day.

Automated Account Management

After the account is funded, the robo advisor can begin to manage the portfolio on an ongoing basis.

This usually includes periodic rebalancing, dividend reinvestment, and monitoring for drift from target allocations, while some platforms also offer features like tax-loss harvesting, subject to defined rules and limitations.

Remember that automation does not remove responsibility. Firms are still accountable for how these features operate, including how changes to code or logic affect client investments.

Custody, Trading, and Fees

Typically, robo advisors do not hold client assets directly. Instead, they rely on third-party custodians or affiliated broker-dealers to execute trades and safeguard funds and securities.

Robo advisors usually have discretionary authority, which the user grants during registration/opening an account. Fees are typically charged as a percentage of assets under management and deducted periodically.

This creates shared regulatory responsibilities: robo advisor, custodian, and any broker-dealer partners must operate within their respective regulatory frameworks.

Why Robo Advisors Matter in Fintech

The robo advisor model is at the intersection of scale, cost, and access. This allows fintech companies to deliver investment management at a volume and price point that traditional advisory models struggle to support. That makes robo advice a viable way for many firms to serve smaller accounts without building a large advisory staff.

As such, robo advisors may be an operational leverage. Once the platform, models, and compliance framework are in place, the marginal cost of adding new clients is relatively low. This scalability is one of the primary reasons robo advisor models continue to attract founders and investors.

Robo advisors also fit naturally into broader fintech ecosystems as they are often embedded into digital banking platforms, brokerage apps, retirement tools, or employer benefit programs. In these setups, automated advice becomes one component of a larger financial product rather than a standalone service.

At the same time, this reach also increases regulatory exposure. A single design decision can affect thousands of clients. The combination of scale and automation is why regulators expect clear governance, documented processes, and ongoing oversight when robo advisors are involved.

See also:

When a Robo Advisor Becomes a Regulated Investment Advisor

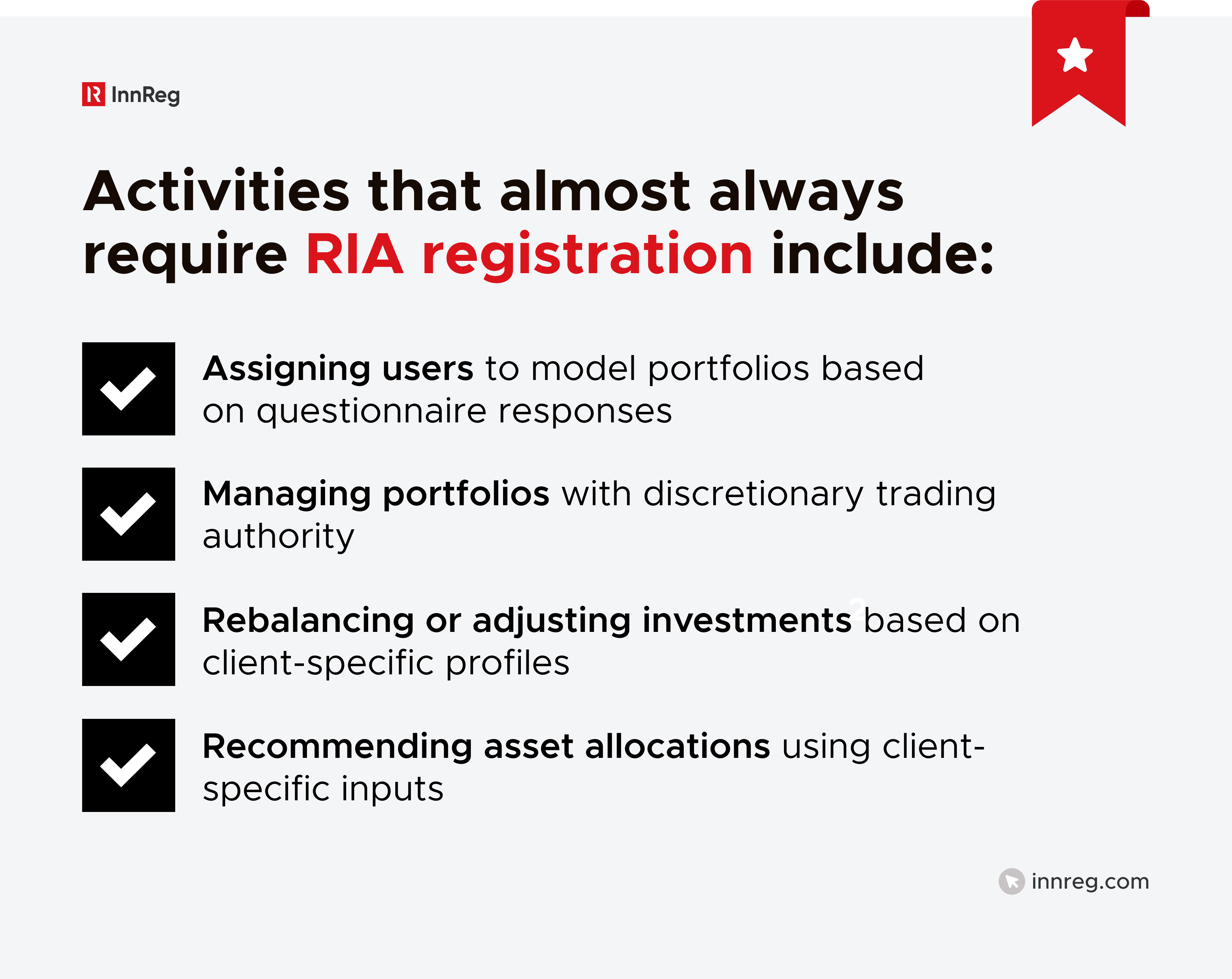

A robo advisor is required to register as an investment advisor when it provides investment advice about securities for compensation. In practice, most platforms described as robo advisors meet this threshold.

What determines the need to register is not branding, automation, or interface design. Instead, functionality triggers registration, specifically when investment advice about securities is used to generate recommendations or manage portfolios. The fact that advice is delivered through software does not change its regulatory treatment under US law.

If a platform recommends asset allocations to select securities or manage portfolios on a discretionary basis, it is operating as an investment advisor under the Investment Advisers Act.

A platform may fall outside the investment advisor definition in limited situations, but these scenarios are narrow and easy to invalidate.

Tools that provide general education, display static model portfolios shown identically to all users, or offer calculators that do not generate recommendations may fall outside the advisor definition.

These tools must avoid personalization, discretion, and any implication that outputs are appropriate for a specific user.

In practice, many platforms that start outside the RIA scope later cross into regulated activity as features evolve. Product changes that introduce ongoing management often trigger registration, even if that was not the original intent.

InnReg helps fintechs register as investment advisors →

Need help with fintech compliance?

Fill out the form below and our experts will get back to you.

Robo Advisor Regulation in the US

No single regulator is assigned to robo advisors as a category. Its oversight depends on regulatory status, product structure, and supporting entities.

The main bodies regulating robo advisors are:

Securities and Exchange Commission (SEC)

The SEC is the primary regulator for robo advisors registered as a Large Advisory firm or an Internet-only advisor. Large Advisory firms meet the applicable assets under management threshold (or qualify under a federal registration exemption) when managing $100 million in AUM, and Internet-only advisors meet the threshold when they provide investment advice exclusively through an operational interactive website.

For robo advisors registered with the SEC, the SEC focuses on how advice is generated and delivered at scale. This includes whether client questionnaires support suitability determinations, whether portfolio algorithms operate as described in disclosures, and how firms oversee changes to models, rebalancing logic, and automated features.

The SEC also reviews compliance programs, marketing materials, and recordkeeping to assess whether advisory obligations are being met in practice. For most robo advisor models, SEC oversight is the long-term regulatory destination as platforms grow and expand nationally.

State Securities Regulators

State securities regulators oversee robo advisors that do not qualify for SEC registration.

These firms need to register in each state where their clients reside and comply with state-level investment advisor rules.

State oversight often applies during early growth stages. Many fintech robo advisors begin with state registration before transitioning to SEC registration as assets and geographic reach increase.

Read our article to learn about the difference between RIA State vs. SEC Registration →

Financial Industry Regulatory Authority (FINRA)

FINRA does not regulate investment advisors directly. Its role arises when a robo advisor relies on, or operates alongside, a broker-dealer.

If an affiliated or third-party broker-dealer handles trade execution, custody, or brokerage communications, FINRA rules apply to those activities.

This is common in robo advisor structures that include brokerage accounts or hybrid advisory models.

Banking and Consumer Protection Regulators

Additional regulators may be involved, depending on how the robo advisor is embedded into broader financial products.

Banking regulators can become relevant when robo advisors partner with insured institutions or offer cash management features. Consumer protection and data privacy authorities may also have jurisdiction over cybersecurity, data handling, and customer disclosures.

—

Regulatory oversight follows function, not branding. A robo advisor’s regulatory obligations are determined by what the platform does and how it operates, not by how it is described in marketing materials.

5 Examples of Robo Advisors

Robo advisors vary widely in structure, scope, and regulatory complexity. Looking at real-world models helps clarify how different approaches operate within the same regulatory framework:

See also:

1. Direct-to-Consumer Robo Advisors

These platforms offer automated investment management directly to individual retail clients. Users complete a digital questionnaire, fund an account, and receive ongoing portfolio management with limited human interaction.

This is the most common robo advisor model. The platform maintains a direct advisory relationship with the end client and is responsible for onboarding, suitability, portfolio management, disclosures, and ongoing compliance.

2. Hybrid Robo Advisors

Hybrid robo advisors combine automated portfolio management with access to human advisors, often positioned as a premium offering. Clients may receive algorithm-based portfolios by default, with human advisors available for planning discussions, life events, or higher-value accounts.

This model can improve client experience, but it does not reduce regulatory obligations. The presence of human advisors does not alter fiduciary duty or disclosure requirements, and regulators apply the same standards as they would to a fully automated platform.

However, hybrid advisor models are usually more challenging to manage as firms must supervise both algorithms and people, align disclosures across delivery methods, and maintain consistency between automated recommendations and human advice.

3. Robo Advisors Embedded in Brokerage Platforms

In this model, a broker-dealer integrates a robo advisor into its existing brokerage platform, and the automated advice becomes one of several ways clients interact with the firm.

Regulators treat advisory and brokerage activities separately, even when delivered through the same product: each function must comply with its own regulatory framework, including registration, supervision, and recordkeeping.

Operationally, this requires strong internal controls. Firms must oversee algorithms, registered representatives, and platform communications without allowing advisory and brokerage roles to overlap improperly.

4. Robo Advisors Within Digital Banks or Fintech Ecosystems

Robo advisors are often embedded into digital banking platforms, retirement tools, or employer benefit programs. Investment management becomes one feature within a larger financial product.

These models can involve multiple regulators, depending on partnerships and services offered. Integration increases reach, but it also increases regulatory coordination requirements.

5. Enterprise or White-Label Robo Platforms

Some fintechs build robo advisor technology that is licensed to registered investment advisors, banks, or wealth management firms rather than offering advice directly to end users.

In these cases, the licensing firm may avoid direct advisor registration. The regulated entity is the entity providing investment advice for a fee, not necessarily the technology provider, assuming roles and responsibilities are properly structured.

The Core Compliance Requirements for Robo Advisors

When a robo advisor operates as a registered investment advisor, a defined set of compliance obligations applies.

The core compliance areas regulators consistently examine when reviewing robo advisor programs include:

Fiduciary Duty and Suitability

Robo advisors owe clients a fiduciary duty under US investment advisor regulation. Advice must be suitable based on each client’s financial situation, objectives, and risk tolerance.

Suitability starts with onboarding and continues throughout the relationship. Firms must be able to explain how client inputs lead to specific portfolio outcomes, and how those outcomes remain appropriate over time.

Disclosures and Client Communications

Robo advisors are required to explain their services in a way that clients can reasonably understand. This means describing how the platform operates, what it does for clients, and what it does not.

Key points typically include how investment decisions are generated, whether human advisors are involved, how fees are charged, and the limits of the service. Disclosures must reflect how the platform actually functions in practice, not how it was originally designed to work.

Conflicts of Interest

Like all investment advisors, robo advisors must identify and manage conflicts of interest. Common conflicts include proprietary products, revenue sharing, cash sweep arrangements, or affiliated service providers.

Conflicts must be disclosed and, where possible, mitigated.

Automation does not eliminate conflicts. However, it can make them harder to detect if governance is weak.

Recordkeeping and Supervision

Robo advisors are required to maintain books and records covering advice delivered, trades executed, communications, and changes to models or logic.

Supervision extends to both technology and people. Firms must supervise algorithms the same way they supervise human advice, including testing, monitoring, and escalation processes.

InnReg helps fintechs by providing recordkeeping services →

Compliance Program and CCO Oversight

Every robo advisor is required to maintain written policies and procedures that address its specific regulatory risks. These policies must reflect how the platform actually operates, not just how it was designed on paper.

A designated Chief Compliance Officer is responsible for implementing and overseeing this program. That role includes monitoring adherence to rules, reviewing disclosures, and responding to regulatory inquiries. Regulators expect the CCO to have real authority and visibility into the business.

For fintechs, this often means close coordination between compliance, product, and engineering teams. Algorithm updates, feature changes, and new partnerships can all affect regulatory exposure.

InnReg supports fintechs by acting as an outsourced CCO →

Compliance Area | What Regulators Expect |

|---|---|

Fiduciary Duty and Suitability | Advice must be based on each client’s financial situation, objectives, and risk tolerance, with a clear link between client inputs and portfolio construction over time. |

Disclosures and Client Communications | Advisors must provide clients with information regarding how the robo advisor works, including how decisions are made, fees are charged, and where the service has limitations. |

Conflicts of Interest | Firms must identify, disclose, and manage conflicts such as proprietary products, revenue sharing, cash sweeps, or affiliated service providers. |

Recordkeeping and Supervision | Robo advisors must retain records of advice, trades, communications, and model changes, and actively supervise both algorithms and personnel. |

Compliance Program and CCO Oversight | A Chief Compliance Officer with authority and operational visibility must oversee written policies tailored to the platform’s actual operations. |

Algorithm Governance and Oversight

For a robo advisor, the algorithm is the advice engine. Regulators expect firms to understand how it works, how it is supervised, and how changes are controlled. Automated decision-making is not treated as a black box, even when built by engineering teams.

Governance starts with documentation and testing, and firms are required to be able to explain portfolio logic, client inputs, rebalancing rules, and any tax-related features. Algorithms must be monitored over time, with issues investigated and documented rather than attributed to automation.

Change management is a recurring regulatory focus. As updates to models or code can affect large numbers of clients at once, regulators expect firms to assess compliance impact before changes go live and to keep disclosures aligned with actual platform behavior.

Marketing Rules for Robo Advisors

Marketing is where robo advisors often face regulatory scrutiny, as the statements about performance, portfolio management, or automation must be grounded in how the platform actually works.

The SEC Marketing Rule applies to robo advisors in the same way it applies to traditional firms. This includes testimonials, endorsements, performance references, and third-party rankings. All public-facing content is in scope.

Automation does not lower the standard. If a feature is promoted, it must operate as described across client accounts.

Learn more about the SEC Marketing Rule →

Cybersecurity and Data Privacy Requirements

Cybersecurity is a recurring examination focus for robo advisors. As advice and account access are delivered digitally, system weaknesses can affect large numbers of clients.

Regulators expect firms to address data protection, access controls, monitoring, and response planning. The standard is reasonableness, not perfection, based on business complexity.

Oversight extends beyond internal systems. Vendor integrations and data flows must be understood and managed.

Learn more about SEC Cybersecurity Guidelines →

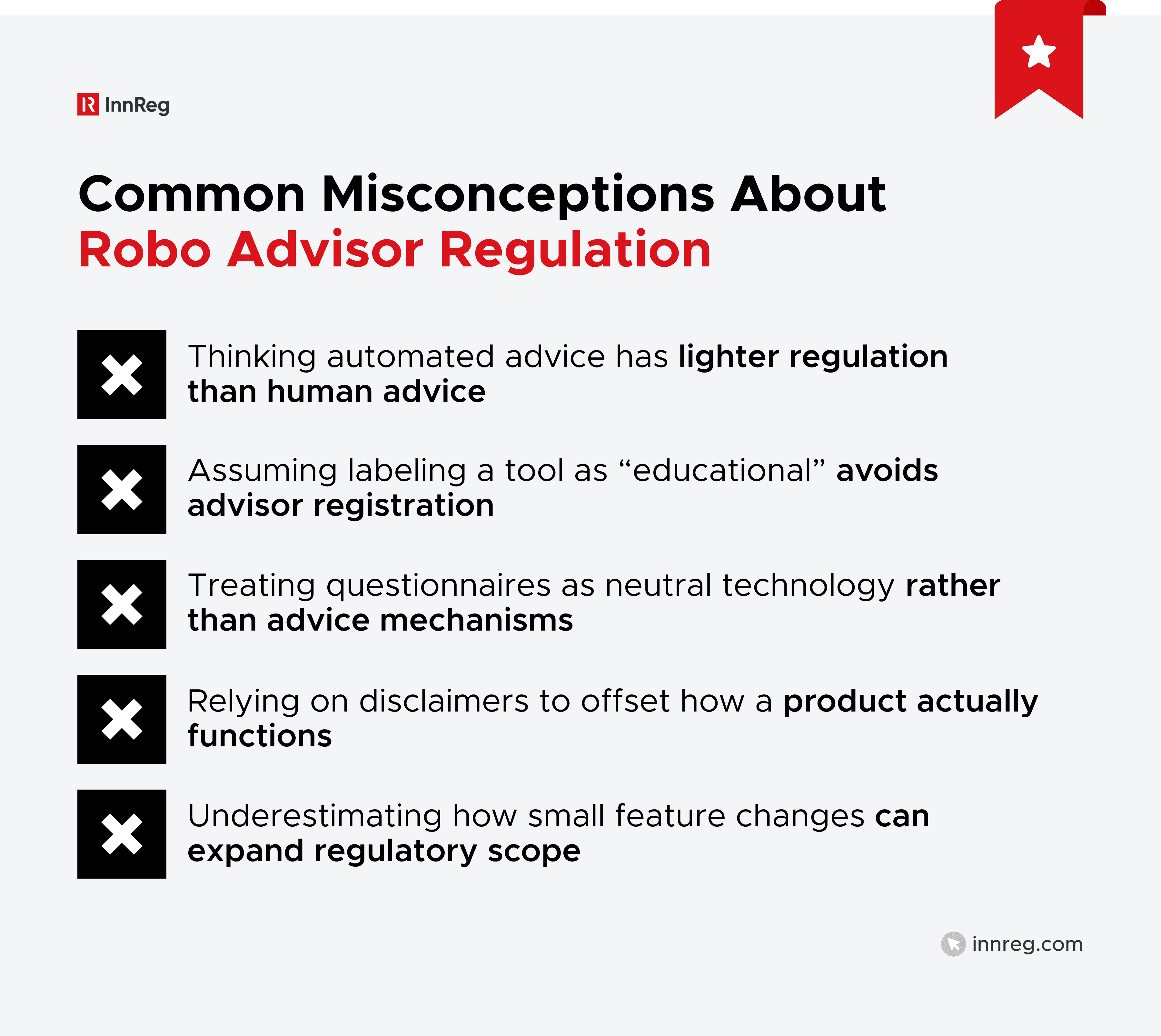

Common Misconceptions About Robo Advisor Regulation

Robo advisor regulation is frequently misunderstood, particularly by teams approaching wealth management from a technology-first perspective.

Many issues surface not from intent, but from assumptions about how automation fits into existing financial regulations. Automation changes delivery, not rules or regulatory expectations.

These misunderstandings often appear during product expansion. For example, a feature added to improve onboarding or engagement can shift a platform into a regulated advisory activity.

Regulators focus on what the system does in practice, not how it is described internally.

For robo advisors, product development and compliance are tightly linked. Changes to workflows, logic, or user inputs should be evaluated for regulatory impact before launch. Treating compliance as part of product planning helps avoid rework and regulatory friction.

At InnReg, we regularly work with product and engineering teams building robo advisor platforms and other regulated fintech products. Since 2013, we’ve supported more than 100 innovative fintechs as features evolved from concept to launch and beyond.

See also:

The 2024 Internet Adviser Exemption Change

In 2024, the SEC updated the so-called internet-only exemption that many robo-advisors rely on for federal registration. The change tightened the criteria and removed the flexibility that some firms had been using. The exemption now applies only to advisors who operate exclusively through an interactive website or application.

Under the updated rule, a robo-advisor relying on this exemption may not provide personalized advice outside its digital platform.

The prior allowance for a limited number of non-internet clients was eliminated from the exemption, and firms must now also maintain a continuously operational platform and attest to compliance through Form ADV.

For fintech teams, this means that product design, client support, and sales processes must align with a fully digital delivery model. Providing personalized investment advice outside the interactive platform will invalidate the exemption, requiring a shift to state registration or a different regulatory strategy.

Learn more about Internet Adviser Exemption →

—

Robo advisors combine technology, investment advice, and regulation in ways that are easy to underestimate. What looks like a product decision at first glance can carry regulatory consequences once client-specific advice and portfolio management are involved. Scaling responsibly is about understanding where automation ends and regulatory obligations begin.

For fintechs, the challenge is not avoiding regulation, but learning the rules well enough to design within them. Robo advisor models scale without constant rework when governance is clear, processes are documented, and product, engineering, and compliance teams are working in coordination. As robo advisor platforms continue to evolve, firms that build compliance into how they operate will be better positioned to adapt as rules and expectations change.

InnReg was founded in 2013 by Francesco Matteini, former Chief Compliance Officer who helped launch and scale some of the most innovative digital broker-dealers over the last two decades. He built compliance programs to support the first zero-commission broker and the first BD-sponsored investor social network. Since its founding, InnReg has attracted highly experienced fintech consultants with long careers in compliance, risk management, and a deep understanding of the fintech industry.

How Can InnReg Help?

InnReg is a global regulatory compliance and operations consulting team serving financial services companies since 2013.

We are especially effective at launching and scaling fintechs with innovative compliance strategies and delivering cost-effective managed services, assisted by proprietary regtech solutions.

If you need help with compliance, reach out to our regulatory experts today:

Related Articles

Featured LinkedIn Posts