Form CRS: Requirements, Common Mistakes, and Best Practices

Form CRS is one of the shortest regulatory documents most broker-dealers and investment advisers are required to produce, but it carries outsized regulatory and operational weight.

For fintech firms, Form CRS often creates more complexity than its length suggests. Innovative business models, hybrid registrations, digital onboarding flows, and non-traditional fee structures all make it more difficult to accurately describe services and conflicts while abiding by formatting and plain-language requirements.

This article explores who must file Form CRS, what it must include, how it differs from Form ADV Part 2, and how delivery and update obligations work in practice. It also covers common mistakes regulators see in exams and how Form CRS impacts modern fintechs.

At InnReg, we help broker-dealers, investment advisors, and fintech firms manage Form CRS as part of their broader compliance programs: from registration and disclosure drafting to delivery workflows and ongoing updates.

What Is Form CRS, and Why Does It Matter for Fintech Firms?

The Customer Relationship Summary (CRS) is a short disclosure document required by the SEC for broker-dealers and investment advisors that work with retail investors. Its purpose is to give investors a clear, standardized snapshot of the firm’s services, fees, conflicts of interest, and disciplinary history before or at the start of a relationship.

Form CRS is designed to help retail investors compare firms and understand the nature of their relationship by requiring firms to explain complex business models in plain language, within strict formatting limits. The document must follow a prescribed structure, include specific disclosures, and present required “conversation starter” questions that prompt client discussions.

For fintech firms, this requirement often has broader implications as innovative models are more difficult to summarize accurately in two pages. Form CRS often becomes the first place regulators test whether a fintech’s business model is clearly understood internally and communicated consistently to retail investors.

Who Must File Form CRS

Form CRS applies to broker-dealers and investment advisors that provide recommendations to retail investors, meaning that an SEC-registered broker-dealer with retail customers must file and deliver Form CRS, even if it does not offer traditional brokerage accounts or operate through a digital-only platform. The obligation is driven by registration status and client type, not firm size, maturity, or technology.

Furthermore, SEC-registered investment advisors must file Form CRS if they serve retail investors (including high-net-worth individuals, who are still treated as retail investors for this purpose). Robo-advisors, hybrid models, and other technology-driven advisory platforms are not exempt.

Firms registered as both broker-dealers and investment advisors are allowed to file a single combined Form CRS. Still, the document must clearly distinguish between each role, including differences in services, fees, and standards of conduct.

When Form CRS Does Not Apply

Form CRS is not required in every registration scenario. The obligation is narrowly tied to SEC registration and the presence of retail investors, which creates a few clear but often misunderstood carveouts.

Broker-dealers that exclusively serve institutional clients are not required to file or deliver Form CRS. If a firm’s customers are limited to entities such as funds, banks, or corporations and no natural persons receive services for personal or household purposes, Form CRS does not apply.

State-registered investment advisors are generally not subject to Form CRS requirements. Most states did not adopt an equivalent rule, meaning advisors registered only at the state level typically do not file Form CRS. That said, if an advisor transitions to SEC registration, Form CRS becomes required as part of the disclosure process.

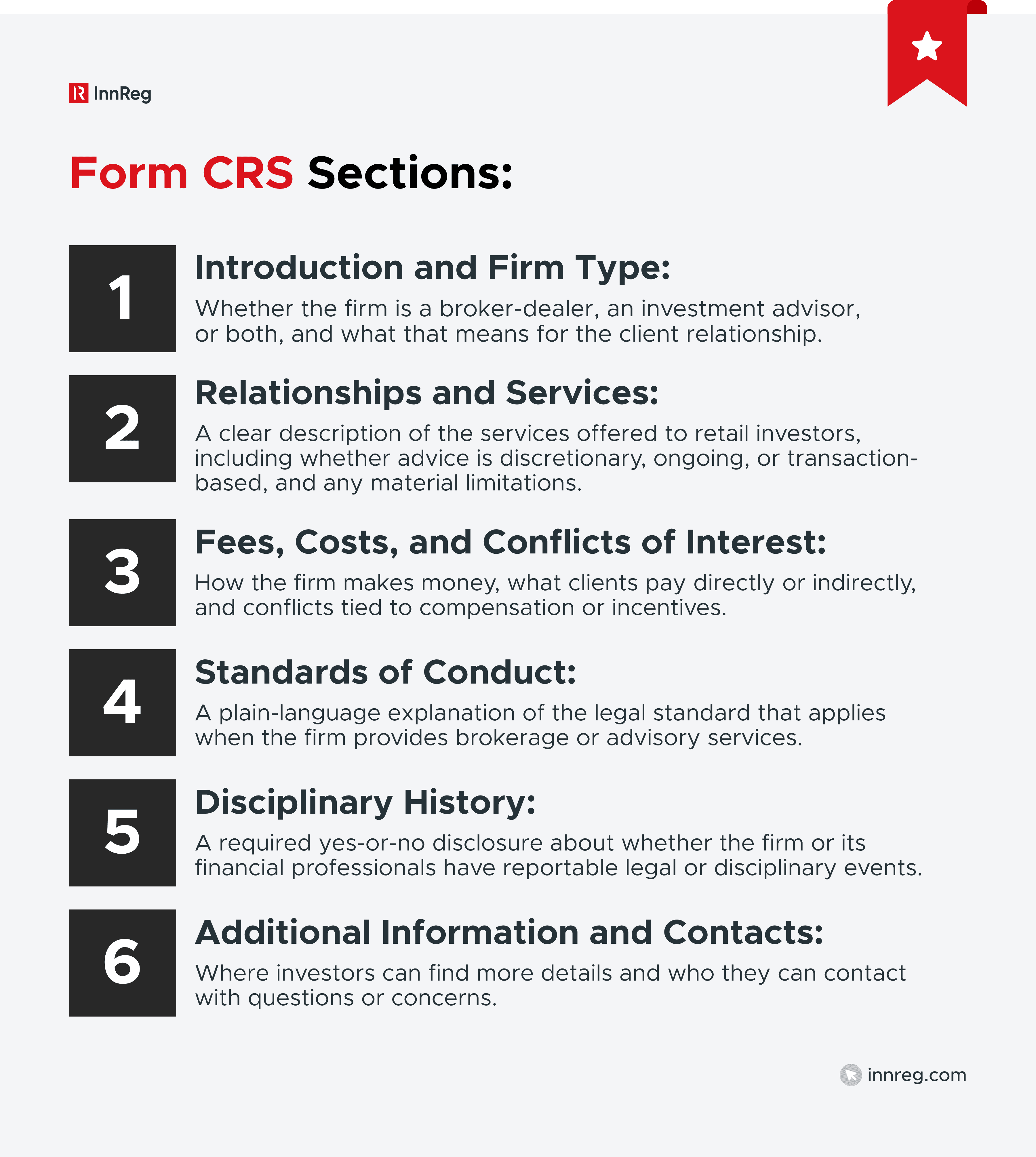

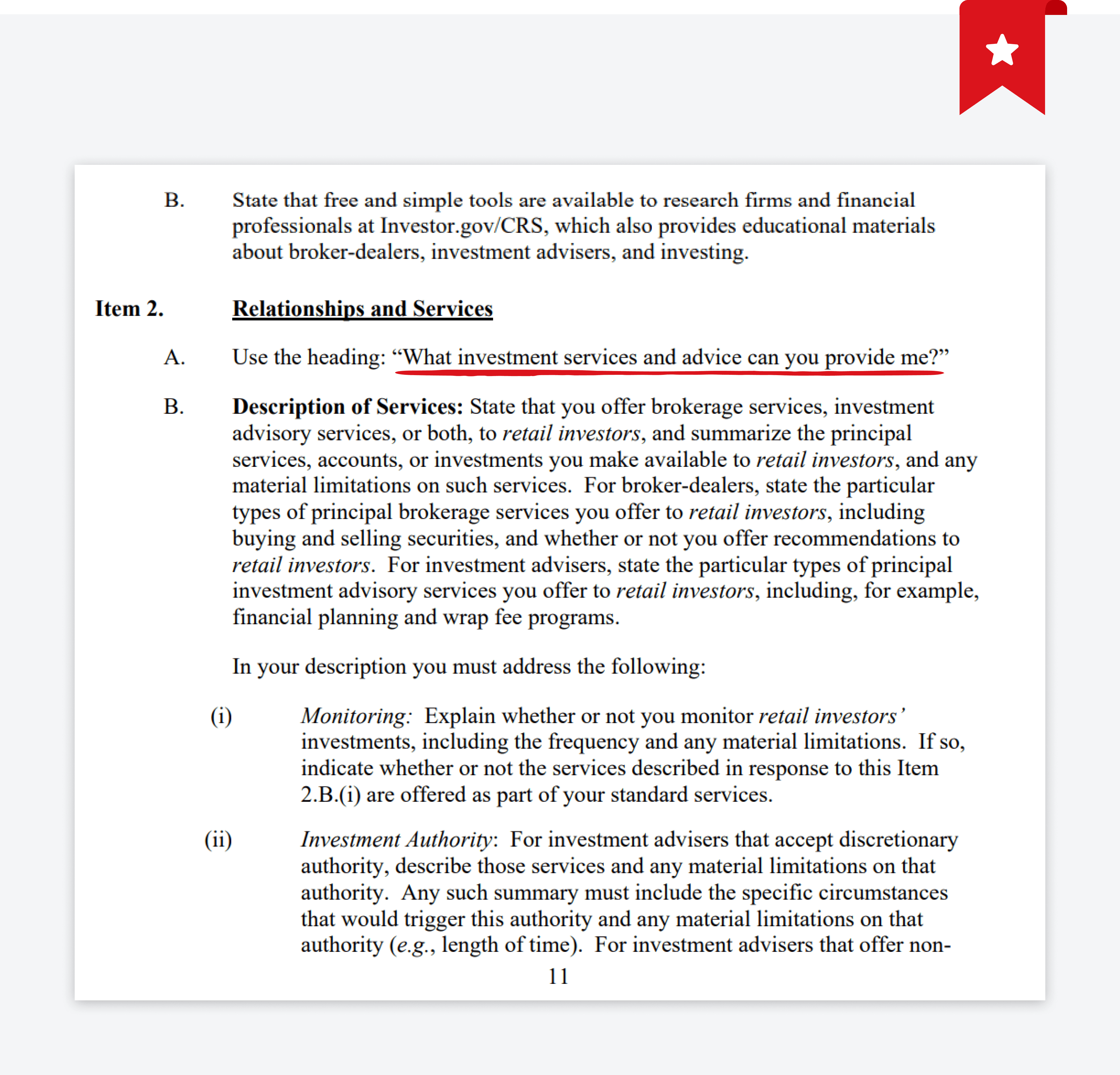

What Form CRS Must Include

The SEC prescribes a structure that Form CRS must follow. That means firms cannot reorganize sections, omit required topics, or replace mandated language with marketing copy.

Every Form CRS must cover the same core categories so retail investors can compare firms on a like-for-like basis.

Required Conversation Starters

Each Form CRS must include specific, SEC-prescribed questions known as conversation starters. These questions are not optional and must appear as written.

Their purpose is to prompt retail investors to ask questions about fees, conflicts, services, and disciplinary history. In exams, regulators often check whether these questions are present and whether staff are prepared to address them consistently.

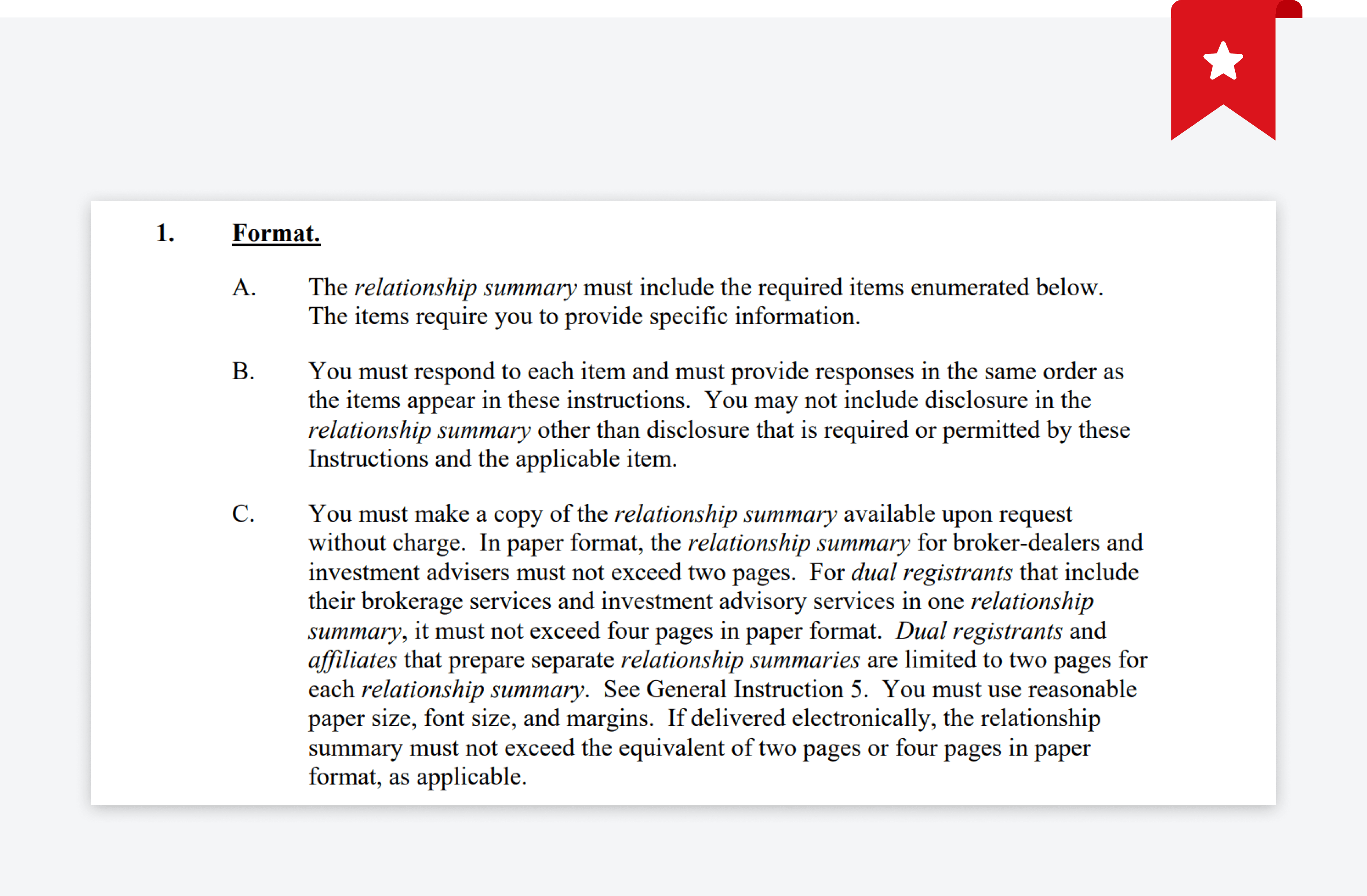

Required Form CRS Formatting Rules

Form CRS is subject to strict formatting and presentation requirements:

Two pages for single registrants, four pages for dual registrants

Plain-language writing with short sentences and everyday terms

No legal disclaimers, dense footnotes, or cross-references that replace required content

Page 1 of Form CRS covers the formatting rules:

The SEC evaluates Form CRS as both a disclosure document and a communication tool. Clarity, accuracy, and alignment with real-world practices matter as much as technical completeness.

Form CRS vs. Form ADV Part 2

Form CRS and Form ADV Part 2 are both required disclosures for SEC-registered investment advisors, but they serve very different purposes.

Form CRS is a short, standardized summary designed for retail investors. Form ADV (and Form ADV Part 2, specifically) is a detailed narrative brochure that provides fuller explanations of the firm’s business, fees, conflicts, and practices.

Topic | Form CRS | Form ADV Part 2 |

|---|---|---|

Primary purpose | High-level relationship summary | Detailed disclosure document |

Intended audience | Retail investors | Clients and prospective clients |

Length | 2 pages (4 for dual registrants) | No fixed page limit |

Structure | Prescribed SEC format | Principles-based narrative |

Plain-language requirement | Strict | Expected, but more flexible |

Filing method | Filed with the SEC | Filed with the SEC |

Delivery timing | At or before the relationship starts | At or before the signing of the advisory contract |

Update requirement | Within 30 days of a material change | Annually and as updated |

For fintechs, the risk is inconsistency. Regulators frequently compare Form CRS language against Form ADV Part 2, client agreements, onboarding disclosures, and marketing materials. A Form CRS that oversimplifies or contradicts the longer disclosures may become a regulatory issue.

Learn more about Form ADV Part 2 →

See also:

How and When to Deliver Form CRS

Filing Form CRS with the SEC is only part of the obligation. Form CRS must also be delivered to retail investors at specific points in the client relationship, and regulators routinely test whether delivery timing, method, and recordkeeping align with the rules.

Delivery requirements apply regardless of whether the relationship is established in person, through an app, or via automated onboarding.

Need help with fintech compliance?

Fill out the form below and our experts will get back to you.

Delivery Triggers for New Retail Investors

Form CRS must be delivered to a retail investor at the earliest of the following events:

Before entering into an investment advisory agreement

Before opening a brokerage account

Before recommending a service or investment

In practice, Form CRS is often required earlier than firms expect, especially when recommendations are embedded in digital interfaces or product flows. If a platform suggests a portfolio, asset allocation, or transaction, delivery obligations are likely triggered.

Delivery Requirements for Existing Clients

Existing clients must receive Form CRS again in certain situations, including:

When opening a new account that differs from the existing relationship

When receiving a recommendation for a new service or account type

When the firm recommends a rollover or similar transaction

Clients may also request a copy at any time, in which case the firm must provide it promptly. Form CRS is not a one-time document tied only to initial onboarding.

Posting and Recordkeeping Requirements

Firms with public websites must post their current Form CRS in an easily accessible location. The document should be clearly labeled and reachable without excessive navigation.

From an operational standpoint, firms are expected to maintain records showing when and how Form CRS was delivered. During exams, regulators often ask for delivery logs, timestamps, or system evidence tied to specific clients. For fintechs, automated tracking within onboarding and CRM systems is typically the most reliable way to manage this requirement.

Form CRS delivery failures are frequently cited alongside broader supervision and recordkeeping issues. Treating delivery as a core compliance process rather than a filing task reduces that risk.

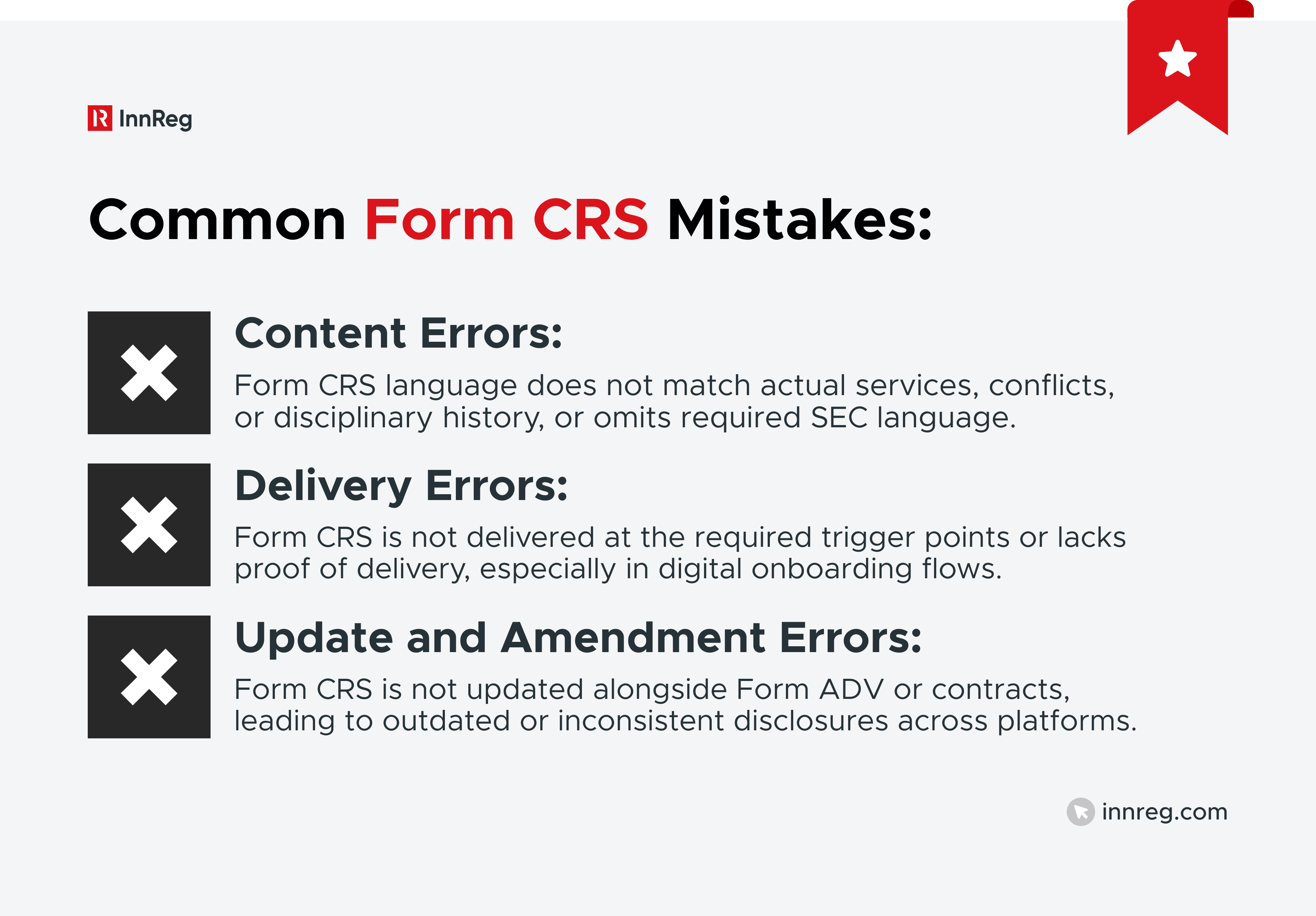

Common Form CRS Mistakes Found in Exams

Most findings fall into a small number of repeatable categories, many of which are avoidable with basic controls.

Content Errors

Content errors are a common driver behind Form CRS findings. These mistakes usually involve inaccuracies or omissions rather than layout issues.

Some examples of content errors include incorrect disciplinary history responses, service descriptions that don’t match actual operations, missing SEC-required language such as conversation starters, and language that understates fees or conflicts.

Regulators routinely cross-check Form CRS against Form ADV, client agreements, and firm practices. Misalignment across these important disclosures often results in follow-up findings.

Delivery Errors

Even when the Form CRS content is correct, delivery failures remain a frequent issue in exams.

Typical delivery-related findings include:

Form CRS was not delivered at the correct trigger point

Reliance on passive website posting without affirmative delivery

Poor placement of Form CRS links on websites or platforms

Lack of evidence showing when and how clients received the document

For fintech firms, delivery errors often stem from incomplete integration into digital onboarding or recommendation flows.

See also:

Update and Amendment Errors

Update failures are a frequent source of Form CRS exam findings that usually arise when disclosure maintenance is not clearly assigned or monitored.

Common problems include missing amendment deadlines, distributing outdated versions after business changes, and version mismatches across platforms and filings.

Exams often show that firms revised Form ADV or contractual disclosures but failed to update Form CRS. Regulators view this as a governance issue, not a drafting problem, and expect firms to manage Form CRS as an active disclosure.

How Form CRS Impacts Fintech Business Models

Form CRS applies the same disclosure framework to all firms, but the impact is not evenly distributed. Fintech business models tend to feel the constraints of Form CRS more acutely because they combine multiple services, automated decision-making, and non-traditional revenue structures.

Robo-Advisors

Robo-advisors must be precise about the nature of the advice they provide. This includes whether advice is discretionary, how portfolios are constructed, and whether human oversight plays a role.

Common Form CRS issues for robo-advisors include unclear descriptions of monitoring, rebalancing, and limitations on personalization.

Overly broad statements can conflict with how the algorithm actually functions or how services are marketed.

Learn more about robo-advisors →

Trading Apps and Neo-Brokers

Trading apps often struggle with how Form CRS intersects with product design, as some features, such as suggested trades, curated lists, or alerts, can blur the line between execution-only services and recommendations.

Form CRS must clearly describe how the firm makes money, including payment for order flow or other transaction-based incentives. If product features influence user behavior, Form CRS disclosures must reflect that reality, even if the platform avoids advisory language.

Crypto-Adjacent or Hybrid Models

Hybrid platforms that combine securities and crypto products often struggle with Form CRS disclosures. When securities services are part of the offering, Form CRS obligations still apply, regardless of how the products are bundled or branded.

The focus should be on clear boundaries. Form CRS needs to state which services are regulated, which are not, how compensation and conflicts arise, and what protections apply to each. Lack of precision here is a common exam trigger.

Best Practices for Drafting Form CRS

The firms that avoid repeat exam issues tend to treat Form CRS as a core disclosure that reflects how the business actually works, not as a filing artifact. Good Form CRS drafting starts with alignment between compliance, legal, and product teams.

Best practices for drafting Form CRS include:

Using Plain Language Techniques

The SEC expects Form CRS to be readable by a retail investor with no industry background. That doesn’t mean oversimplifying but choosing clarity over precision when possible, and precision where required.

Common plain-language practices include:

Use short sentences with one idea per sentence

Avoid defined terms unless required

Replace abstract descriptions with concrete actions

Write in the second person where appropriate

Unclear Language | Clear Language |

|---|---|

We offer a range of advisory solutions | We provide ongoing investment advice and manage your portfolio |

Fees may vary based on services | You pay an annual fee based on the assets we manage for you |

Conflicts may exist | We earn more when you trade more often |

Conflict Disclosure

Conflict disclosures should describe how incentives arise, not why they are acceptable. This is a common drafting failure, especially for fintech platforms with multiple revenue streams.

Effective conflict disclosures typically:

State the incentive directly

Link the incentive to client impact

Avoid defensive or explanatory tone

For example, instead of explaining why a conflict is mitigated, Form CRS should explain how the conflict exists. Mitigation belongs elsewhere, not in the relationship summary.

Operational Tips

Drafting Form CRS in isolation often leads to inconsistencies later. Operational integration reduces that risk.

Practical steps include:

Tie the Form CRS review to product or pricing changes

Maintain a single owner responsible for Form CRS updates

Train client-facing teams on Form CRS language and conversation starters

Track versions across filings, websites, and onboarding flows

Firms that manage Form CRS as an active disclosure, rather than a static document, tend to spend less time remediating issues during exams and audits.

When to Update Your Form CRS

Form CRS must be updated when it becomes materially inaccurate. This requirement is often triggered by business changes that feel operational rather than regulatory, which is why updates are frequently missed.

The following changes commonly require Form CRS amendments

Changes to services offered or how advice is provided

New or revised fee structures or compensation models

Introduction of new conflicts of interest

Material changes to disciplinary history

Shifts between brokerage and advisory activities

Firms that manage Form CRS updates effectively usually tie them to broader change management processes. Product launches, pricing changes, and regulatory events should automatically trigger a Form CRS review.

—

Form CRS may be short, but it plays a central role in how regulators evaluate disclosure quality, governance, and day-to-day compliance discipline.

For fintech firms, the challenge is not simply meeting the formal requirements but keeping Form CRS up to date with evolving products, digital workflows, and real client interactions.

When it moves in step with Form ADV, client agreements, onboarding flows, and product changes, Form CRS can reduce friction during exams and limit downstream remediation.

Marina is a Compliance Consultant at InnReg with over 15 years of experience in operations and financial services. She has held senior roles at Amity Services and HSBC, with expertise in operations management, client portfolio growth, and end-to-end service delivery. She holds an MBA from the British School of Commerce.

How Can InnReg Help?

InnReg is a global regulatory compliance and operations consulting team serving financial services companies since 2013.

We are especially effective at launching and scaling fintechs with innovative compliance strategies and delivering cost-effective managed services, assisted by proprietary regtech solutions.

If you need help with compliance, reach out to our regulatory experts today:

Related Articles

Featured LinkedIn Posts