What Are Private Placements? Definition and Examples

Key Takeaways

Private placement is a way to raise capital without registering the offering with the SEC.

Regulation D rules, including 506(b), 506(c), and 504, set conditions around investor eligibility, solicitation, and offering structure

Accredited investors play a central role in private placements, as their eligibility and verification requirements help determine how the offering can be structured.

Form D must typically be filed with the SEC after the first sale of securities, along with any required state Blue Sky filings.

Private placements also carry compliance risks, including improper solicitation, inadequate investor verification, and the use of unregistered intermediaries.

Raising capital is one of the first real challenges most fintech companies face. As founders start looking at their options, private placements are often a simpler way to bring in investors without going through a full public offering.

That’s why they’re used across early-stage rounds, private funds, and more complex financial products. For many teams, private placements are a practical entry point into the capital markets while still operating within US securities rules.

In this article, we’ll explore what private placements are and why they matter for founders and compliance teams.

At InnReg, we help fintech companies navigate the compliance side of private placements. From choosing the right exemption to handling filings, investor requirements, and ongoing obligations, our team supports each stage of the process.

Private Placements Definition

A private placement is an alternative to a public offering for raising capital by selling securities to a limited group of investors. These investors are usually institutions or individuals who meet specific financial criteria, such as being accredited.

Instead of going through full SEC registration like a public offering, the company relies on an exemption under US securities law, most commonly under Regulation D. This streamlines the process, but doesn’t reduce regulatory responsibilities, such as rules around disclosures, investor eligibility, and required filings.

Private placements are commonly used by startups, private funds, and even established companies looking to raise capital without the time and cost of a public offering.

How Private Placements Differ from Public Offerings

The main difference between private placements and public offerings comes down to:

Who you can sell to

How the process is handled.

In a public offering, securities are offered to the general public and must be registered with the SEC. That process is detailed, time-consuming, and comes with ongoing reporting obligations.

Private placements take a different route. They’re limited to a smaller group of investors and rely on exemptions from SEC registration. While the upfront burden shrinks, regulatory responsibility remains, like disclosure and investor eligibility requirements.

Another key difference is visibility. Public offerings are marketed broadly and involve significant public disclosure. Private placements are more controlled, with tighter restrictions on how offerings are communicated and who can participate.

Why Do Companies Use Private Placements?

Many companies turn to private placements because they offer a more practical route to raising capital. Instead of navigating the full SEC registration process required for a public offering, businesses can raise money through a more streamlined approach. For startups and growing fintech companies, this can make a major difference in both timing and execution.

Speed and flexibility are a big part of the appeal. Private placements give companies more control over how they structure the deal and which investors they work with. That can be especially valuable for businesses with models that are still evolving or that don’t fit cleanly into traditional categories.

There’s also a practical cost consideration. Going public involves legal, accounting, and ongoing reporting expenses that can be difficult to justify early on. Private placements can be a more cost-effective way to raise capital while still operating within US securities laws.

Private Placements vs. Public Offerings

Private placements and public offerings both raise capital, but they follow very different paths. Here’s a simple comparison:

Feature | Private Placement | Public Offering |

|---|---|---|

Investor access | Limited group (often accredited investors) | Open to the general public |

SEC registration | Not required (must comply with exemptions) | Required |

Disclosure level | Limited, but still structured | Extensive public disclosures |

Timeline | Generally faster | Longer and more complex |

Ongoing reporting | Reduced | Continuous reporting obligations |

For many fintech companies, the choice depends on stage, resources, and strategy. Private placements are often used earlier on, while public offerings come into play when a company is ready for broader market access and regulatory exposure.

How Do Private Placements Work?

Even without a public offering, private placements still follow a defined process. Every step, from setting the terms to bringing investors on board, has to line up with what securities law requires.

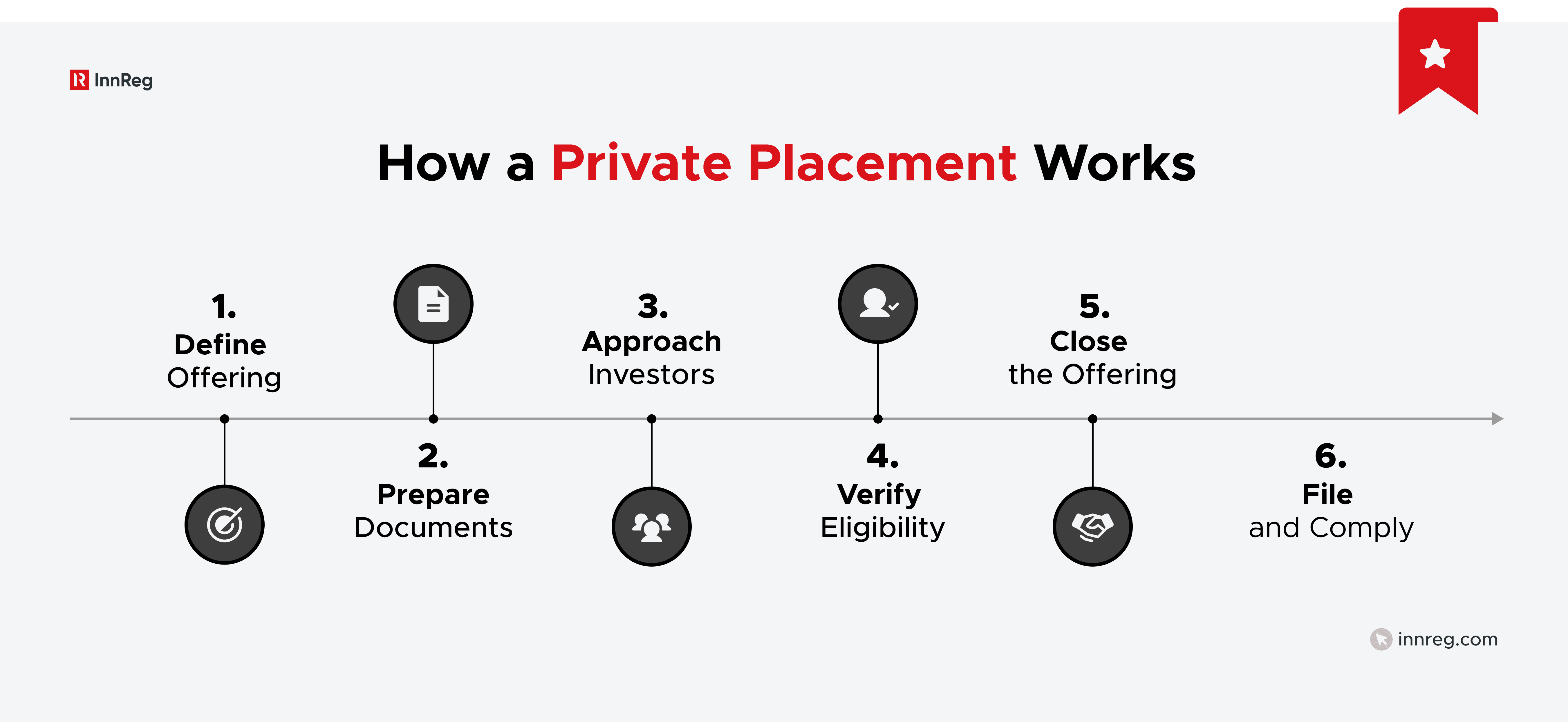

Typical Structure of a Private Placement

A private placement usually follows a clear sequence, even if the details vary by deal. It starts with defining the terms of the offering, including:

The type of security

Pricing

Target investors

This sets the foundation for everything that follows.

Next comes documentation. Companies prepare materials like a private placement memorandum (PPM), subscription agreements, and investor questionnaires. These documents outline the investment terms, risks, and required disclosures so investors can make informed decisions.

Once the structure and documents are in place, the company begins reaching out to investors. After commitments are secured, funds are collected, and the securities are issued. The process ends when all funds have been received and all securities have been issued. An important notice filing is Form D, which is required to be filed within 15 days of the initial sale.

Key Participants in Private Placements

Several parties play specific roles in a private placement.

The issuer: The company raising capital, responsible for structuring the offering and preparing the required documentation. The issuer sets terms and manages investor communications.

Investors: Typically, the accredited investors, institutions, or funds that meet certain financial thresholds. They review the offering materials, assess the risks, and decide whether to participate.

Managing Broker-Dealers: They help coordinate investor outreach, support the distribution process, and assist with structuring the offering following applicable securities regulations.

Placement Agents: They help connect issuers with potential investors and support capital raising efforts, particularly in private offerings.

Legal Counsel: Legal counsel advises on securities law requirements, prepares offering documents, and helps to structure and execute the transaction in compliance with applicable regulations.

Private Placement Securities and Restricted Securities

Securities sold through a private placement usually count as restricted securities, which means you can't just turn around and resell them on the open market. Investors have to hold them for a set period or satisfy certain conditions before they can transfer them to someone else.

The restriction traces back to how the securities were issued in the first place. Because the offering was never registered with the SEC, resale limits exist to keep these securities from slipping into the public market without the oversight that would normally apply.

That carries real consequences on both sides. Investors need to go in knowing their money won't be easy to access, and issuers need to spell out these limitations plainly in their offering documents.

Types of Private Placements Under US Securities Law

Private placements don't all work the same way. Which rules apply depends on the exemption a company relies on under US securities law, and each exemption comes with its own conditions as to who can invest, what has to be disclosed, and how the offering can be marketed.

See also:

1. Rule 506(b) Private Placements

Rule 506(b) is one of the most commonly used private placement exemptions. It allows companies to raise an unlimited amount of capital without registering with the SEC, as long as they follow specific conditions.

Under this rule, companies can raise funds from accredited investors and up to 35 non-accredited investors who meet certain standards. However, general solicitation isn’t allowed, which means you can’t publicly advertise or broadly market the offering.

Because of this limitation, companies often rely on existing relationships or targeted outreach. They also need to have a reasonable belief that investors meet the required criteria, especially when non-accredited investors are involved.

Need help with broker-dealer compliance?

Fill out the form below and our experts will get back to you.

2. Rule 506(c) Private Placements

Rule 506(c) gives companies more flexibility in how they market an offering. It allows general solicitation, so you can publicly advertise and reach a broader audience of potential investors.

There’s an important tradeoff:

All investors must be accredited

The company must take reasonable steps to verify that status

This goes beyond relying on an investor’s statement and often involves reviewing financial documents or getting confirmation from a third party.

For companies that want broader visibility while raising capital, this exemption can be attractive. But it also comes with stricter verification requirements that need to be handled carefully.

3. Rule 504 Offerings

Rule 504 is another exemption companies can use to raise capital without going through full SEC registration, though it comes with limits. Under the rule, a company can raise up to $10 million over a 12-month period.

Unlike Rule 506 offerings, Rule 504 doesn’t automatically limit participation to accredited investors. However, the ability to broadly market the offering depends on state-level rules and whether certain conditions are met. This can make the structure more complex to navigate.

Because of that, Rule 504 offerings tend to require careful coordination between federal and state compliance requirements. The regulatory approach can vary quite a bit depending on how the offering is structured and where the investors are located. 4. Section 4(a)(2) Private Placement Exemption

Section 4(a)(2) is the original private placement exemption under US securities law. It allows companies to raise capital without SEC registration when the offering is made to investors who can evaluate the risks on their own.

Unlike Regulation D rules, this exemption doesn’t come with detailed safe harbor requirements. Instead, it relies on principles, such as:

Limiting the offering to sophisticated investors

Avoiding any form of public solicitation

Because the rules are less standardized, companies have to think carefully about how they put these offerings together. Many end up going with Regulation D instead, simply because it lays out a clearer set of rules and a more predictable path to staying compliant.

Private Placements and Accredited Investors

Who you’re allowed to solicit is a key part of any private placement. Accredited investors often sit at the center of these offerings because of how securities laws are structured.

Who Qualifies as an Accredited Investor

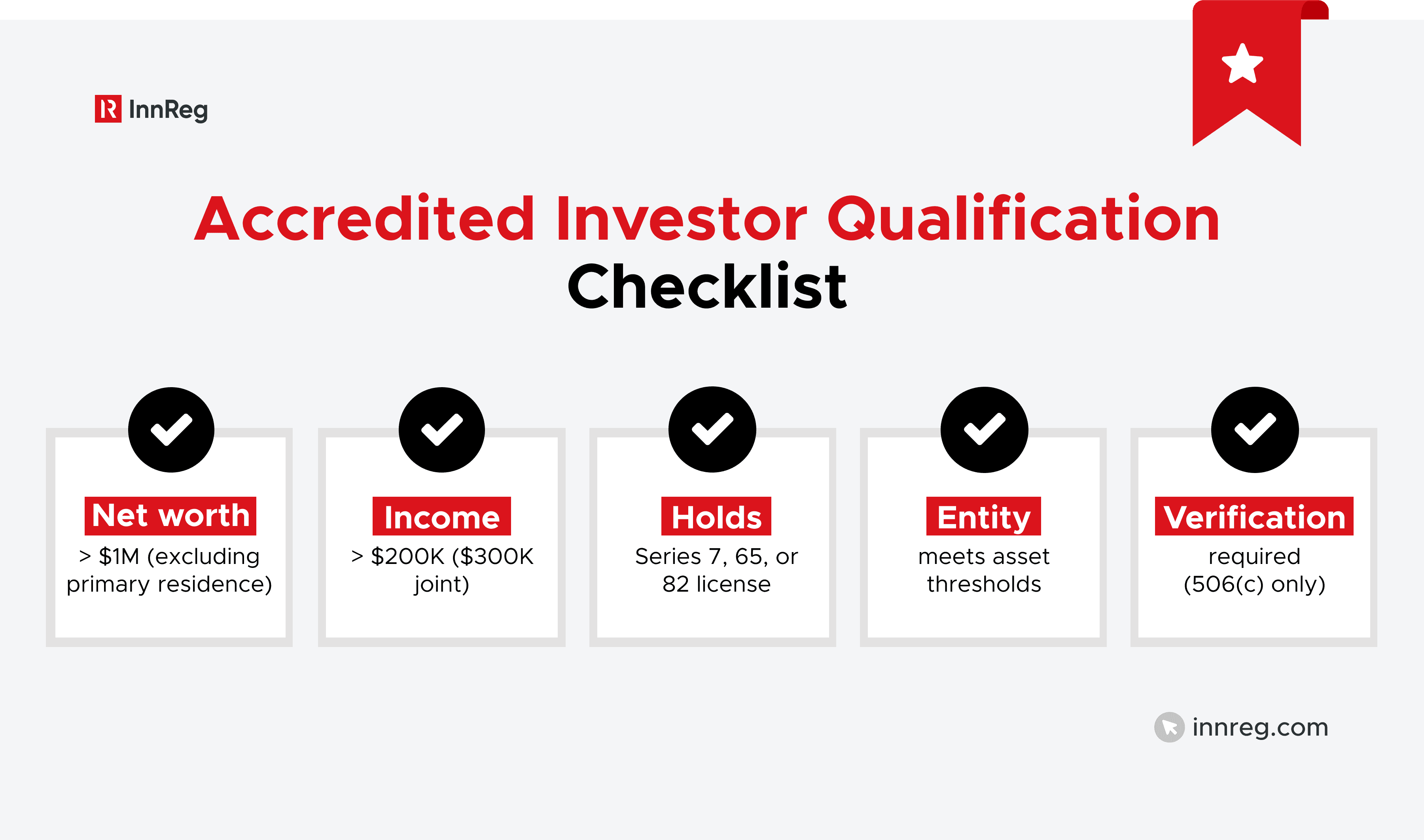

An accredited investor is someone who meets specific financial or professional criteria defined by the SEC. The most common path is based on income or net worth, such as earning over $200,000 annually or having a net worth above $1 million, excluding a primary residence.

There are also other ways to qualify. Certain professionals, like holders of Series 7, Series 65, or Series 82 licenses, are considered accredited. Entities, such as funds, trusts, and companies, may also qualify if they meet asset thresholds or are made up of accredited investors.

For companies raising capital, this classification matters. It determines who can participate in the offering and what compliance requirements apply.

Verification Requirements in Rule 506(c)

If you’re relying on Rule 506(c), it’s not enough for investors to simply say they’re accredited. You need to take reasonable steps to verify their status before accepting their investment.

This usually involves reviewing documents such as:

Tax returns

Bank statements

Brokerage accounts

In some cases, a third party, like a CPA, attorney, or registered broker-dealer, can provide written confirmation. The key point is that verification must be based on actual evidence, not just a checkbox or self-certification.

For a lot of companies, this step can become a bottleneck if it isn't handled early. Setting up a clear process for collecting and reviewing investor information goes a long way toward avoiding delays and keeping the offering on track.

Reasonable Belief Standard in Rule 506(b)

Rule 506(b) takes a different approach to investor eligibility. Instead of verifying accredited status through documents, you need to have a reasonable belief that the investor qualifies.

This often comes from information gathered during the onboarding process. Investor questionnaires, prior relationships, and discussions about financial background all play a role. The standard isn’t as strict as 506(c), but it still requires a thoughtful and documented approach.

If that belief ever gets challenged, you'll want to be able to show how you arrived at it. Keeping clear records of how you assessed each investor's status helps back up your position if questions come up down the line.

See also:

Key Regulatory Requirements for Private Placements

Private placements still come with a set of regulatory requirements that companies need to follow. These rules shape how the offering is structured, documented, and maintained over time.

SEC Rules Governing Private Placements

Private placements in the US are mainly governed by the Securities Act of 1933 and related SEC rules. Most offerings rely on exemptions like Regulation D, which set the conditions for raising capital without full registration.

These rules define key elements such as:

Who can invest

What disclosures are required

How the offering can be marketed

They also create the framework companies need to follow to avoid triggering a public offering by mistake.

For fintech companies running more complex models, applying these rules can take some careful interpretation. The way a product is structured or described can affect which exemption fits and how the offering needs to be handled.

Form D Filing Requirements

Most private placements under Regulation D require a Form D filing with the SEC. This is a notice filing that provides basic information about the:

Offering

Issuer

Exemption being used

The filing is due within 15 days after the first sale of securities. It’s submitted electronically through the SEC’s EDGAR system. While it’s relatively straightforward, missing the deadline or filing incorrect information can raise regulatory issues later.

In addition to the federal filing, companies often need to track related state notice filings.

State “Blue Sky” Notice Filings

In addition to federal requirements, private placements often trigger state-level filings. These are known as Blue Sky notice filings and apply in each state where investors are located.

Most states require a copy of the Form D, along with a filing fee and sometimes additional information. The timing can vary, but it’s often tied to the first sale in that state. Missing a state filing doesn’t invalidate the offering, but it can lead to penalties or complications later.

For companies raising funds from investors across multiple states, this can add up quickly. Tracking where investors are based and managing filings accordingly is an important part of staying organized and compliant.

Resale Restrictions and Rule 144

Securities sold through private placements can’t be freely resold right away. Rule 144 sets the conditions under which these restricted securities can be resold in the public market.

The rule includes holding periods, volume limits, and other requirements that depend on whether the issuing company is public or private. For example, investors may need to hold the securities for a minimum period before selling. Even after that, additional conditions may apply based on the size of the sale and the investor’s relationship to the company.

For both issuers and investors, these restrictions affect liquidity. Understanding when and how securities can be resold helps set clear expectations from the beginning.

The Role of Broker-Dealers in Private Placements

Broker-dealers often play a key role in private placements, especially when companies need help reaching investors or structuring the offering. Their involvement can affect how the offering is conducted and what regulatory requirements apply.

1. When a Placement Agent Is Required

Not every private placement needs a placement agent, but plenty of companies choose to work with one. If you're actively soliciting investors or getting paid to raise capital, you may need to bring a registered broker-dealer into the picture.

Placement agents help connect issuers with investors and support the fundraising process. They often:

Handle outreach

Coordinate discussions,

Sometimes assist with structuring the deal

Their involvement can also help align the offering with securities regulations, especially around solicitation and compensation.

2. FINRA Rules Affecting Private Placements

When a broker-dealer is involved in a private placement, FINRA rules come into play. These rules focus on how the offering is reviewed, marketed, and presented to investors.

Broker-dealers are expected to conduct a reasonable investigation of the issuer and the offering. This includes understanding:

The business

The risks

How the proceeds will be used

They also need to review offering materials to confirm they’re fair, balanced, and not misleading.

There are also rules around communications and compensation. How the offering is described to investors and how fees are structured both fall under FINRA oversight. This adds another layer of review that companies need to account for when working with a broker-dealer.

3. Broker-Dealer Due Diligence Responsibilities

When a broker-dealer participates in a private placement, due diligence becomes a core responsibility. They’re expected to review the issuer and the offering carefully before presenting it to investors.

This review typically covers the company’s:

Business model

Financials

Management team

Terms of the offering

The goal is to understand what’s being sold and identify any red flags. If something doesn’t add up, the broker-dealer is expected to dig deeper before moving forward.

This process also shapes how the offering is presented. The information shared with investors needs to be accurate, complete, and consistent with what was reviewed during due diligence.

Common Compliance Challenges in Private Placements

Private placements can run into issues when key requirements are misunderstood or handled too loosely. Many problems come from small gaps in the process rather than intentional mistakes.

General solicitation mistakes: Companies sometimes cross the line when promoting an offering, especially under Rule 506(b). Sharing details publicly, even unintentionally, can be treated as general solicitation and affect the exemption being used.

Accredited investor verification issues: Relying on incomplete or informal checks can create problems, particularly under Rule 506(c). If investor status isn’t properly verified, the offering may not meet exemption requirements.

Integration of multiple offerings: Running multiple fundraising rounds too close together can raise questions about whether they should be treated as a single offering. This can impact compliance with exemption rules and investor limits.

Use of unregistered finders or intermediaries: Paying individuals who aren’t registered broker-dealers to help raise capital can trigger regulatory concerns. This is a common issue, especially for early-stage companies trying to move quickly.

Marketing and communications risks: Inconsistent or overly promotional messaging can create exposure. All materials shared with investors should align with the actual terms of the offering and clearly present risks.

See also:

Examples of Private Placements

Private placements show up across different types of deals and industries. They’re used in a range of scenarios, from early-stage fundraising to more structured investment offerings.

Venture Capital Funding Rounds

Venture capital rounds are one of the most common examples of private placements. Startups raise capital from a group of investors in exchange for equity, often across multiple funding stages like seed, Series A, and beyond.

These deals are typically structured under Regulation D exemptions. Investors are usually accredited, and the process involves:

Term sheets

Subscription agreements

Investor disclosures

The focus is on aligning investor expectations with the company’s growth plans and risk profile.

For fintech companies, these rounds can become more complex depending on the product. When the business involves regulated activities, the structure of the offering and the disclosures need to reflect those regulatory considerations.

Private Equity Investments

Private equity is another route that runs through private placements. Here, capital gets raised from a pool of investors to buy into, fund, or overhaul companies.

These deals are usually led by private equity firms that pool investor capital into a fund. The fund then deploys that capital across selected investments over time. Investors commit capital upfront, but the funds are typically drawn down as opportunities arise.

All of this gets more tangled than your typical early-stage round. You're looking at intricate agreements over who governs what, how fees work, and how everyone eventually cashes out. Each of those points has to be nailed down in the offering documents.

Private Placements by Public Companies

Public companies also use private placements to raise capital. Instead of going through a new public offering, they sell securities directly to a select group of investors.

These deals are often used when a company wants to move quickly or avoid the cost and timing of a registered offering. They may involve issuing new shares, convertible securities, or other instruments. The investors are typically institutions that can evaluate the risks and negotiate terms.

Even with an issuer that's already public, these transactions still play by private placement rules. Companies have to handle disclosures with care and think through how the offering squares with the reporting obligations they already carry.

Private Fund Offerings

Private funds, such as hedge funds and venture funds, are typically raised through private placements.

Fund managers offer interests in the fund to a limited group of investors, usually accredited investors or qualified purchasers. Once investors commit capital, the fund deploys it according to its strategy, whether that’s investing in startups, public securities, or other assets.

The offering documents explain how the fund operates, including how fees are structured and returns are distributed.

Advantages and Limitations of Private Placements

Private placements offer clear benefits, but they also come with tradeoffs. Understanding both sides helps set realistic expectations before starting a raise.

Advantages of Private Placements

Faster path to capital: Private placements can move more quickly than public offerings since there’s no full SEC registration process. This can help when timing is important.

More control over investors: Companies can choose who participates, which allows for better alignment with long-term goals.

Lower upfront costs: Legal and regulatory costs are generally lower compared to public offerings, especially for early-stage companies.

Flexible deal structures: Terms can be tailored to fit the company’s needs, including pricing, rights, and investor protections.

Reduced public disclosure: Companies aren’t required to share the same level of information as in a public offering, which can help protect sensitive business details.

Limitations of Private Placements

Limited investor pool: Offerings are typically restricted to accredited investors or a defined group, which can limit reach.

Resale restrictions: Investors can’t freely sell their securities right away, which limits liquidity.

Ongoing compliance requirements: Even without SEC registration, companies still have to manage filing, disclosure, and recordkeeping obligations.

Potential for regulatory missteps: Small mistakes in solicitation, investor verification, or filings can create regulatory risks if not handled carefully.

—

Private placements are central to how companies raise capital, especially in fintech, where business models don't always follow the traditional path. They're a practical way to bring investors on board while staying within US securities laws.

At the same time, the process comes with clear rules around investor eligibility, communications, and filings. Small details can have a real impact, so having a structured approach from the start helps avoid issues later.

For companies working in complex or fast-moving environments, getting the structure right early can make all the difference. Bringing in an experienced compliance team helps line up the offering with what regulators expect, all while keeping the process moving efficiently.

InnReg was founded in 2013 by Francesco Matteini, former Chief Compliance Officer who helped launch and scale some of the most innovative digital broker-dealers over the last two decades. He built compliance programs to support the first zero-commission broker and the first BD-sponsored investor social network. Since its founding, InnReg has attracted highly experienced fintech consultants with long careers in compliance, risk management, and a deep understanding of the fintech industry.

How Can InnReg Help?

InnReg is a global regulatory compliance and operations consulting team serving financial services companies since 2013.

We are especially effective at launching and scaling fintechs with innovative compliance strategies and delivering cost-effective managed services, assisted by proprietary regtech solutions.

If you need help with broker-dealer compliance, reach out to our regulatory experts today:

Related Articles

Featured LinkedIn Posts