What Is the SEC? Understanding Its Role in Financial Regulation

Key Takeaways

The SEC is the primary US securities regulator and oversees how securities are issued, traded, and disclosed across the financial markets.

Its core mission is to protect investors, promote fair and orderly markets, and support capital formation.

The SEC’s oversight extends across broker-dealers, investment advisers, funds, exchanges, and some fintech platforms, depending on how they operate.

The agency uses examinations and investigations to identify compliance, and enforcement actions to address violations, which can result in penalties, remediation requirements, and operational restrictions.

For fintech companies, whether the SEC applies often depends on how the product is structured, what it offers, and how users interact with it.

The Securities and Exchange Commission (SEC) is the primary regulator of the US securities markets. It oversees how companies raise capital, how securities are traded, and how market participants operate. If your business involves securities, trading, or financial products, the SEC is likely part of your regulatory landscape.

Through rulemaking and enforcement, the SEC governs key parts of the securities ecosystem. This includes disclosure requirements for public companies, oversight of broker-dealers and investment advisors, and action against fraudulent or manipulative practices. These powers largely stem from the Securities Exchange Act of 1934, which continues to guide the regulatory structure today.

For fintechs operating as broker-dealers, investment advisors, trading platforms, or offering securities-related products, the SEC directly affects licensing decisions, product design, marketing practices, and day-to-day operations.

This article breaks down how the SEC works, what it regulates, and what compliance looks like in practice, with a focus on real-world implications for modern financial businesses.

At InnReg, we help fintech companies navigate SEC regulation in practice. From registration and licensing to building and managing compliance programs, our team supports your operations as they evolve.

What Is the United States Securities and Exchange Commission?

The Securities and Exchange Commission, or SEC, is an independent federal agency that oversees the US securities markets. It was created in 1934 following the stock market crash and the broader breakdown in investor confidence. Its role is to regulate how securities are issued, traded, and disclosed to investors.

Unlike industry organizations, the SEC has government authority. It writes rules, supervises firms, and takes enforcement action when violations occur. This combination of responsibilities is what gives the SEC its central role in the regulatory system.

In practice, the SEC is involved throughout a firm’s lifecycle. From registration to ongoing reporting and examinations, it shapes how regulated businesses operate. For fintech companies, understanding this structure is a necessary starting point.

What Does the SEC Do?

The SEC’s role goes beyond rulemaking. It actively shapes how the securities markets function on a day-to-day basis. At a high level, the SEC regulates market participants, requires disclosures, and enforces securities laws. These responsibilities apply across public companies, broker-dealers, investment advisors, and trading platforms.

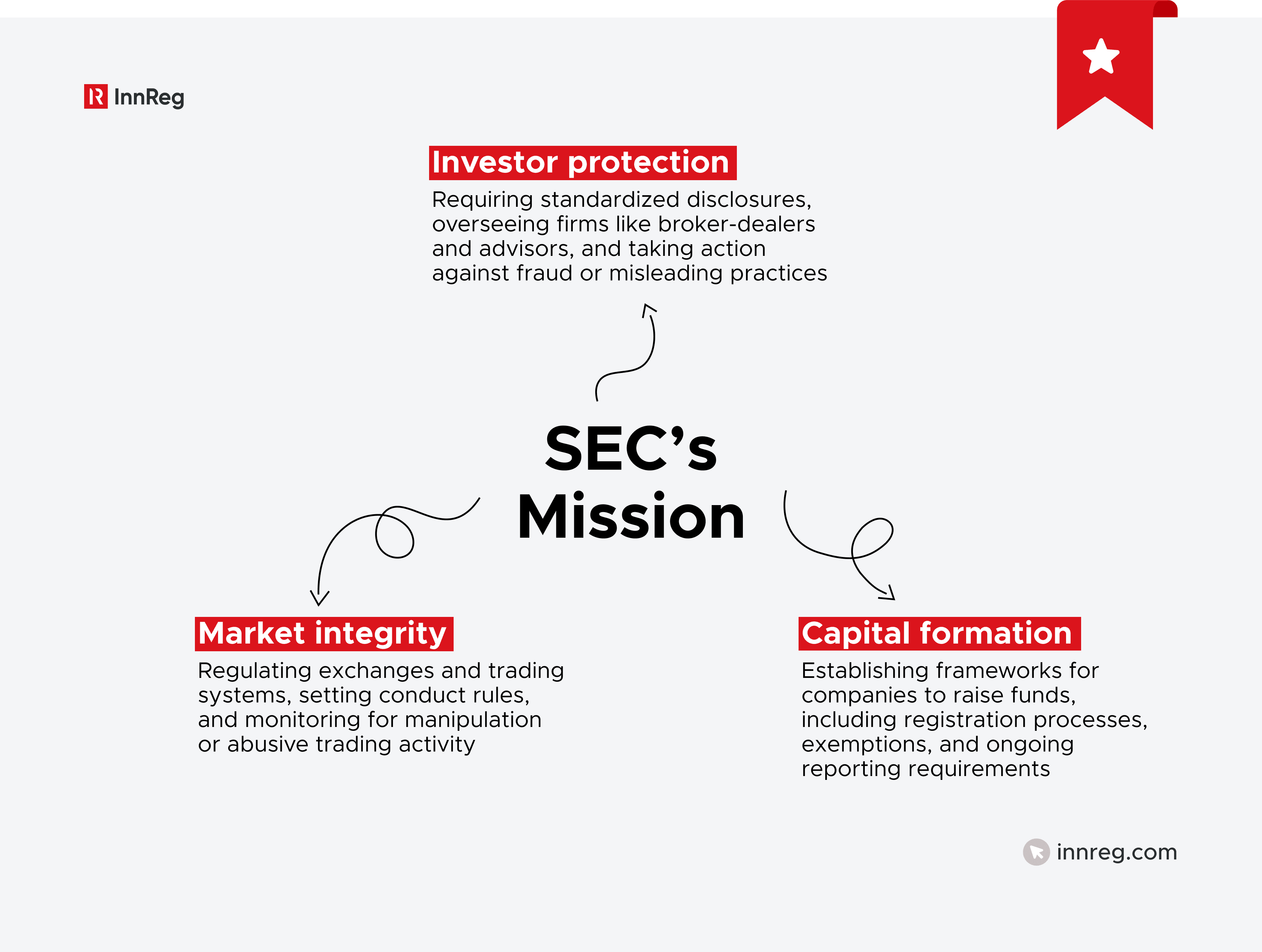

Core Mission and Objectives

The SEC’s activities are anchored in a three-part mission that defines its role in the financial system. It focuses on investor protection, market integrity, and capital formation. These priorities guide both day-to-day supervision and longer-term regulatory initiatives.

Maintaining fair and orderly markets involves setting standards for trading practices, transparency, and participant conduct. This includes oversight of exchanges, trading platforms, and intermediaries such as broker-dealers. The goal is to reduce manipulation, improve transparency, and support efficient price discovery.

At the same time, the SEC is tasked with facilitating capital formation. This means creating a regulatory environment where companies can raise funds while still meeting disclosure and compliance requirements. These objectives often work together, with transparency and enforcement supporting both investor confidence and capital access.

The SEC’s Role in Financial Markets

The SEC plays a central role in how US securities markets function on a daily basis. It regulates key participants, including exchanges, broker-dealers, and alternative trading systems, and sets the rules that govern how securities are bought and sold. This includes requirements around transparency, execution practices, and market access.

A major part of this role is maintaining fair and orderly markets. The SEC establishes standards to reduce manipulation, improve price discovery, and promote consistent trading practices across platforms. It also reviews market structure issues, such as how orders are routed and how different trading venues interact.

The SEC’s oversight extends to infrastructure that supports trading activity. This includes clearing agencies, transfer agents, and other entities involved in the settlement process. Together, these functions help maintain confidence in the markets and support efficient capital flows.

For fintechs building trading platforms or market-facing products, decisions around order handling, custody models, and access to liquidity often fall within SEC oversight and require careful regulatory alignment.

How the SEC Is Structured

The SEC operates through a leadership structure supported by specialized divisions and offices. It separates rulemaking, supervision, and enforcement while keeping them coordinated. The agency is led by commissioners who set policy and approve major actions, while divisions handle areas like disclosures, trading, and investment management.

The Five Commissioners

The SEC is led by five commissioners appointed by the President and confirmed by the Senate. One of them serves as Chair and acts as the head of the agency. No more than three commissioners can belong to the same political party, which is intended to maintain a level of balance in decision-making.

The commissioners are responsible for setting the SEC’s agenda, adopting new rules, and approving enforcement actions. They also provide direction on regulatory priorities, which can shift over time depending on market developments and policy focus.

While firms do not typically interact directly with commissioners, their decisions influence the regulatory environment. Leadership changes can lead to shifts in areas such as enforcement focus, disclosure expectations, or emerging technology oversight.

Key Divisions and Offices

The SEC’s work is carried out through several core divisions, each responsible for a specific area of regulation. These divisions handle rulemaking, supervision, and enforcement within their respective domains.

The SEC is divided into the following divisions:

Division of Corporation Finance | This division oversees public company disclosures. It reviews filings such as registration statements and periodic reports to confirm that investors receive material information. Its focus is on transparency in capital markets. |

|---|---|

Division of Trading and Markets | This division regulates broker-dealers, exchanges, and trading infrastructure. It develops rules for market structure and monitors how securities transactions are executed. It plays a key role in how trading platforms and intermediaries operate. |

Division of Investment Management | This division oversees investment advisors, mutual funds, and other investment companies. It focuses on regulatory requirements related to fiduciary duties, disclosures, and fund structures. It is central for RIAs and asset managers. |

Division of Enforcement | This division investigates potential violations of securities laws. It can bring civil actions against firms and individuals for misconduct such as fraud, insider trading, or market manipulation. It is responsible for holding market participants accountable. |

Division of Examinations | This division conducts routine and risk-based exams of regulated firms. It reviews compliance programs, internal controls, and adherence to SEC rules. It is often the primary point of interaction for firms during regulatory reviews. |

What the SEC Regulates

The SEC regulates a broad range of entities involved in securities markets, including firms engaged in issuing, trading, or managing securities, from traditional institutions to fintech models:

Public Companies

Public companies are one of the SEC’s primary areas of oversight. These are companies that offer securities to the public or are listed on exchanges. They are required to file detailed disclosures, including financial statements and material updates.

These filings, such as annual and quarterly reports, are designed to give investors consistent and comparable information. The SEC reviews these disclosures and can issue comments or require revisions if information is incomplete or unclear.

See also:

Broker-Dealers

To operate as a broker-dealer, a firm has to register with the SEC and usually also join FINRA. That means oversight comes from both a federal regulator and a self-regulatory body. This applies across the board, from legacy brokerage firms to newer app-based trading platforms.

The requirements don’t stop at registration. Firms are expected to hold a certain level of capital, follow strict rules in how they deal with customers, and actively supervise their operations. On top of that, there are ongoing reporting obligations, detailed recordkeeping, and periodic exams. The expectations are the same whether the business runs through a traditional desk or a mobile interface.

For fintech companies, broker-dealer status often arises earlier than expected. Features such as order routing, trade execution, custody arrangements, or even how customer accounts are structured can fall within this framework. Small product decisions can shift a platform from a technology provider to a regulated intermediary.

Learn how InnReg helps broker-dealers navigate regulatory requirements →

Need help with fintech compliance?

Fill out the form below and our experts will get back to you.

Investment Advisors

Investment advisors are firms or individuals that provide advice about securities for compensation. Depending on their size and structure, they register with either the SEC or state regulators. Larger firms typically register with the SEC, while smaller advisors fall under state oversight.

Their core obligation is fiduciary in nature. Advisors are expected to act in the best interest of their clients, which affects how they provide recommendations, manage conflicts, and disclose fees. This also includes maintaining a written compliance program and keeping disclosures up to date, including Form ADV.

The regulatory expectations go beyond advice itself. Advisors must document decisions, monitor client accounts where applicable, and maintain records that support their activities. They are also subject to periodic examinations, where regulators review how the firm operates in practice.

For fintech companies, this category often includes robo-advisors and digital wealth platforms. The use of algorithms does not remove regulatory obligations. How advice is generated, presented, and monitored can all fall under SEC oversight.

See how InnReg helps RIAs navigate regulatory requirements →

Investment Companies and Funds

This category includes mutual funds, ETFs, and other pooled investment structures. They are regulated under specific frameworks covering structure, disclosures, and operations.

The SEC oversees how these funds are established, managed, and marketed.

It also tends to be more complex. Custody rules, valuation requirements, and limits on certain activities add additional considerations for firms operating in this space.

Exchanges and Alternative Trading Systems

The SEC regulates securities exchanges as well as alternative trading systems (ATSs), which provide trading functionality outside traditional exchanges. These platforms must meet requirements related to transparency, fair access, and operational controls.

For fintech firms building trading venues or matching engines, this category is highly relevant. The regulatory classification of a platform can significantly impact licensing and compliance obligations.

Learn how InnReg helps ATS services providers →

Category | What They Do | SEC Requirements | Fintech Relevance |

|---|---|---|---|

Public Companies | Raise capital from the public and list securities on exchanges | Ongoing disclosures (10-K, 10-Q, 8-K), financial reporting, SEC review of filings | Relevant for fintechs planning IPOs or issuing securities |

Broker-Dealers | Execute trades and facilitate buying/selling of securities | SEC registration, FINRA membership, capital requirements, supervision, reporting, exams | Applies to trading apps, brokerage platforms, and execution infrastructure |

Investment Advisors | Provide investment advice or manage portfolios for a fee | SEC or state registration, fiduciary duty, Form ADV, compliance program, recordkeeping, exams | Includes robo-advisors, wealth platforms, and automated investment tools |

Investment Companies | Pool investor capital (e.g., mutual funds, ETFs) | Structural rules, disclosures, custody requirements, valuation standards, operational restrictions | Relevant for fintechs building funds or structured investment products |

Exchanges & ATSs | Provide marketplaces for trading securities | Registration, transparency rules, fair access requirements, operational controls | Applies to trading venues, matching engines, and secondary market platforms |

SEC Filings and Reporting

SEC filings are a core part of how the agency regulates markets. They create a standardized way for companies and regulated firms to disclose information to investors and regulators. These filings form the backbone of transparency in the securities ecosystem.

The SEC requires different forms depending on the type of entity and activity. Common SEC forms include:

Form S-1

Form S-1 is filed when a company plans to offer securities to the public for the first time. It lays out key details about the business, including financial performance, risk factors, and management structure. It serves as the main registration document for IPOs and similar offerings.

Putting together an S-1 takes time. It usually involves several drafting cycles, back-and-forth with the SEC, and coordination between legal, finance, and compliance teams.

Form 10-K

Form 10-K is an annual report filed by public companies. It provides a comprehensive overview of financial performance, risks, and operations. It is one of the most detailed disclosures required by the SEC.

This filing is closely reviewed by investors and regulators. It also sets the baseline for ongoing disclosures.

See also:

Form 10-Q

Form 10-Q is a quarterly report that includes financial statements and material developments. It is less detailed than the 10-K but still provides insight into a company’s performance. It helps maintain regular transparency between annual reports.

Companies must file it within strict timelines, which requires consistent and timely internal reporting processes.

Form 8-K

Form 8-K is used to report significant events that occur between regular filings. This can include mergers, leadership changes, or material agreements. It is triggered by specific events and must be filed promptly. Delays or incomplete disclosures can raise regulatory concerns.

Form ADV

Form ADV is the primary disclosure document for investment advisors. It provides detailed information about the advisor’s business, including services offered, fee structures, conflicts of interest, and any disciplinary history. Both regulators and clients use it to understand how the firm operates.

The document is structured in multiple parts. Some sections are filed with regulators, while others are delivered directly to clients in plain language. This makes it both a compliance filing and a client-facing disclosure.

Maintaining Form ADV is an ongoing responsibility. Advisors are expected to review and update it at least annually and more frequently if there are material changes. Updates are not just procedural. They reflect how the business evolves over time.

In practice, regulators often review Form ADV closely during examinations. Inconsistencies between the document and actual operations can raise questions, especially around fees, conflicts, or services provided.

Learn more about Form ADV →

Common SEC forms include:

Form S-1 | Initial registration filing for public offerings; includes business, financials, risks, and management; used for IPOs and reviewed through multiple SEC comment rounds |

|---|---|

Form 10-K | Annual report with detailed financials, risks, and operations; serves as the baseline disclosure for investors and regulators |

Form 10-Q | Quarterly report with detailed financials, risks, and operations; serves as an interim update for investors and regulators |

Form 8-K | Required disclosure for material events; maintains ongoing transparency for investors |

Form ADV | Investment advisor disclosure covering services, fees, conflicts, and disciplinary history; updated annually and upon material changes; used by both regulators and clients |

How the SEC Enforces Regulations

The SEC does not just write rules. It actively monitors the market and takes action when violations occur. Enforcement is a core part of how the SEC maintains market integrity and investor confidence. This function is primarily carried out by the Division of Enforcement, which investigates potential misconduct across the securities markets.

Investigations and Enforcement Actions

Investigations by the SEC usually start with fact-finding. Firms may receive requests for documents, be asked to participate in interviews, or be subject to subpoenas. Some matters remain informal, while others move into formal investigations. The focus is on understanding whether the firm is operating in line with regulatory requirements and its own disclosures.

Learn more about the SEC exam priorities →

A large portion of enforcement activity is linked to examination findings. The SEC’s annual exam priorities outline where regulators are focusing, including areas like fiduciary obligations, disclosures, and emerging technologies. These priorities are not just guidance. They often reflect where issues are being identified.

When the SEC determines that a violation has occurred, it can bring enforcement actions through courts or administrative proceedings. These actions may target firms, individuals, or both. Common areas include fraud, misleading disclosures, and weaknesses in compliance programs.

For many firms, the risk comes from how processes are implemented in practice. Gaps in supervision or inconsistencies in disclosures can be identified during exams and lead to escalation. Strong internal processes and exam readiness play a direct role in managing that risk.

Penalties and Consequences

When the SEC determines that a violation has occurred, it can impose different types of sanctions. These can include monetary penalties, requiring firms to return improperly obtained profits, or restricting their ability to operate. In more serious cases, individuals or firms may be suspended or barred from participating in the industry.

In addition to penalties, firms are often required to address underlying issues. This can mean revising compliance programs, improving internal controls, or working with external consultants to review operations. Individuals may also face restrictions on the roles they can hold going forward.

Regulatory consequences are only part of the picture. When an enforcement case becomes public, it can affect the reputation and how the firm is viewed by key stakeholders.

SEC Compliance Requirements for Financial Firms

SEC compliance involves a continuing set of obligations around disclosures, supervision, and internal controls. The specific requirements depend on how the firm is structured and what it does.

Key Compliance Requirements

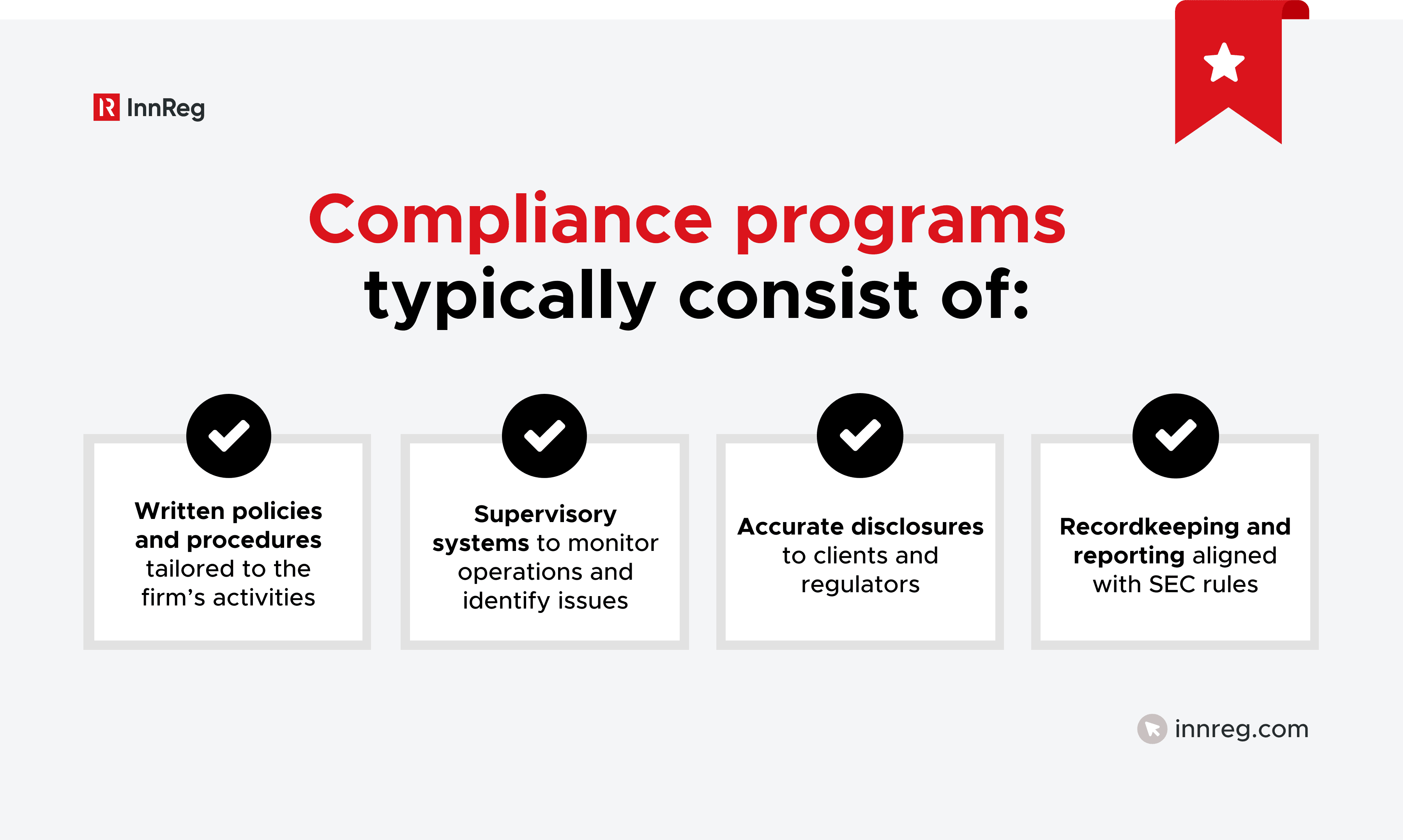

Firms regulated by the SEC are expected to build and maintain a compliance framework that reflects how they actually operate. There is no single template. Requirements vary depending on the firm’s activities, structure, and regulatory status.

In practice, most firms rely on a few core components. This typically includes documented policies, oversight of day-to-day activity, and clear disclosures to clients and regulators. Recordkeeping and reporting are also central, as regulators often focus on what can be evidenced, not just what is written.

These elements need to be maintained over time. As products change or the business expands, the compliance framework has to evolve with it. Static policies tend to fall out of sync with operations, which is where issues often start.

Ongoing Obligations

Compliance does not end after registration. Firms are expected to maintain their programs on a continuous basis. This includes monitoring activity, updating disclosures, and responding to regulatory developments.

Regular internal reviews are part of this process. Many firms conduct annual compliance reviews or similar assessments to evaluate whether their controls are working as intended. Regulatory exams also play a role, as they test how policies are implemented in practice.

Common Compliance Challenges

Many compliance issues come from execution rather than intent. Firms may have policies in place, but struggle to apply them consistently. Gaps often appear in areas like supervision, documentation, and cross-team coordination.

For fintech firms, these challenges are often amplified by speed. Products evolve quickly, but compliance frameworks may lag behind. This is where a structured, process-driven approach becomes important, especially for teams operating without a large in-house compliance team.

How the SEC Impacts Fintech Companies

The SEC’s role becomes more complex when applied to fintech. Many fintech products do not fit neatly into traditional categories, but if a product involves securities or investment activity, SEC oversight is likely to apply.

Where Fintech Falls Under SEC Oversight

Fintech companies can fall under SEC oversight in several ways. This typically depends on the services offered and how users interact with the platform. Common triggers include brokerage activity, investment advice, and operating trading infrastructure.

Examples include:

Trading apps that execute or route securities orders

Robo-advisors providing portfolio recommendations

Platforms offering fractional shares or managed accounts

Marketplaces facilitating the secondary trading of securities

In many cases, the regulatory classification is not obvious at first. The same product can be treated differently depending on execution, custody, or how transactions are handled behind the scenes.

Crypto, Tokenization, and Digital Assets

Digital assets are an active area of SEC oversight. The determining factor is whether a token or related structure is considered a security under US law. Once that threshold is met, existing securities rules come into play.

This impacts multiple parts of a business, including how assets are issued, traded, and held. Firms may be required to register, disclose key information, and follow established regulatory frameworks.

For fintechs working with tokenized or mixed models, classification is not always straightforward. Product design and how it is presented to users can directly influence how it is regulated.

Learn about the SEC’s clarifications on crypto asset activities →

Marketing, AI, and Emerging Risks

The SEC has also increased its focus on how financial products are marketed, especially in digital environments. This includes social media, performance claims, and the use of testimonials. Firms are expected to present information in a way that is fair, balanced, and not misleading.

Learn more about the SEC Marketing Rule →

AI-driven tools are another area of attention. Whether used for investment recommendations, customer interactions, or internal processes, these systems raise questions around oversight, documentation, and accountability.

Read about SEC guidance on AI →

For fintech companies, these areas often intersect. Product design, marketing, and technology are closely linked, which means compliance considerations need to be integrated early in the process rather than added later.

SEC vs. Other Regulators: What’s the Difference?

The SEC is only one part of the regulatory landscape. Financial firms often deal with multiple regulators at both the federal and state levels. Which authority applies depends on the firm’s activities, products, and overall structure.

See also:

SEC vs. FINRA

The SEC and FINRA both regulate broker-dealers, but they operate at different levels. The SEC sets the regulatory framework and enforces securities laws, while FINRA is responsible for supervising firms within that framework.

FINRA’s role includes licensing, routine inspections, and enforcement within its network. The SEC oversees FINRA and has broader powers when it comes to rulemaking and enforcement across the market.

SEC | FINRA | |

|---|---|---|

Type | Federal regulator | Self-regulatory organization |

Role | Rulemaking, oversight, enforcement | Supervision of broker-dealers |

Scope | Broker-dealers & Investment advisors | FINRA member firms |

Interaction | Policy, exams, enforcement | Licensing, exams, daily supervision |

Learn more about the difference between SEC and FINRA →

SEC vs. CFTC

The SEC and CFTC split oversight based on the type of financial instrument. The SEC focuses on securities, while the CFTC regulates derivatives such as futures and certain commodities markets.

In practice, the line is not always clear. Some products, particularly in crypto or structured finance, can fall between categories. This can create overlap or uncertainty around which regulator applies.

SEC | CFTC | |

|---|---|---|

Focus | Securities (stocks, bonds, funds) | Derivatives (futures, options on commodities) |

Key Role | Investor protection and disclosure | Market integrity in derivatives markets |

Entities | Broker-dealers, advisors, funds | Futures commission merchants, swaps dealers |

Fintech | Trading apps, advisors, tokenized securities | Derivatives platforms, commodities exposure |

SEC vs. State Regulators

State regulators work alongside the SEC and often supervise smaller firms or more localized activities. Investment advisors below certain size thresholds are usually required to register at the state level instead of with the SEC.

SEC | State Regulators | |

|---|---|---|

Level | Federal | State |

Focus | National securities markets | Local oversight and investor protection |

Registration | Larger advisors, public companies | Smaller advisors, certain offerings |

Authority | Federal securities laws | State-specific securities laws |

States also enforce their own securities laws, sometimes referred to as “Blue Sky Laws.” These can apply even when a firm is registered with the SEC, adding another layer of compliance.

Learn more about Blue Sky Laws →

—

The SEC plays a central role in shaping how financial markets operate, but for firms, the real impact is operational. From licensing to disclosures and ongoing supervision, its influence runs through the entire lifecycle of a business.

Firms that approach SEC compliance strategically and incorporate it into how they build and scale are better equipped to manage risk and adapt to regulatory change over time.

Frequently Asked Questions

What does SEC stand for?

SEC stands for the Securities and Exchange Commission. It is a US federal agency responsible for regulating the securities markets. Its role is to oversee how securities are issued, traded, and disclosed to investors.

The SEC was established in 1934 after the stock market crash to restore confidence in financial markets. Today, it supervises a wide range of participants, including public companies, broker-dealers, investment advisors, and trading platforms.

In practical terms, when people refer to the SEC, they are referring to the regulator that sets the rules for securities-related activities and enforces them across the market.

What is the SEC's stance on crypto?

The SEC’s position on crypto is based on applying existing securities laws rather than creating a separate framework. The key question is whether a crypto asset qualifies as a security. If it does, it is regulated the same way as traditional securities.

Recent guidance, including SEC FAQs and 2026 interpretations, clarifies how current rules apply across crypto-related activities such as custody, trading, settlement, and recordkeeping. Instead of introducing new rules, the SEC focuses on how established requirements fit these activities.

The approach combines two layers of analysis. First, what the firm is doing, such as operating a trading platform or holding assets. Second, what type of crypto asset is involved, and how it is classified. Both factors influence whether securities laws apply and what obligations follow.

For fintech companies, this means regulatory outcomes often depend on product design and structure. Small differences in how a token is issued, traded, or held can change how it is treated under SEC rules.

Who controls the SEC?

The SEC is led by five commissioners who are appointed by the President and confirmed by the Senate. One of them is designated as Chair and serves as the head of the agency. No more than three commissioners can belong to the same political party, which is intended to maintain balance in decision-making.

While the SEC operates independently, it is still part of the federal government. Commissioners set the agency’s agenda, approve rules, and authorize enforcement actions. Their priorities can influence how the SEC approaches areas such as enforcement, disclosures, and emerging technologies.

In practice, control is not centralized in a single person. The commissioners make decisions collectively, which means regulatory direction can shift over time depending on leadership and policy focus.

InnReg was founded in 2013 by Francesco Matteini, former Chief Compliance Officer who helped launch and scale some of the most innovative digital broker-dealers over the last two decades. He built compliance programs to support the first zero-commission broker and the first BD-sponsored investor social network. Since its founding, InnReg has attracted highly experienced fintech consultants with long careers in compliance, risk management, and a deep understanding of the fintech industry.

How Can InnReg Help?

InnReg is a global regulatory compliance and operations consulting team serving financial services companies since 2013.

We are especially effective at launching and scaling fintechs with innovative compliance strategies and delivering cost-effective managed services, assisted by proprietary regtech solutions.

If you need help with compliance, reach out to our regulatory experts today:

Related Articles

Featured LinkedIn Posts