California Money Transmitter License Guide

Key Takeaways

A California Money Transmitter License is generally required if your business receives, holds, or transmits money or monetary value on behalf of others within the state.

The California Department of Financial Protection and Innovation (DFPI) regulates money transmitters and evaluates licensing based on how funds move through your product, not how the business is marketed.

Many fintech business models, including payment platforms, remittance providers, crypto businesses, custodial wallets, and products using pooled customer accounts, may require a California MTL.

Holding a California MTL does not replace federal requirements, as money transmitters must also register with FinCEN as a Money Services Business and comply with Bank Secrecy Act obligations.

Obtaining a California MTL requires meeting financial, governance, and compliance standards, including minimum net worth, surety bond requirements, audited financial statements, and a risk-based AML program.

Receiving a license is only the beginning, as licensed money transmitters must maintain ongoing reporting, safeguard customer funds, renew their licenses, and prepare for periodic DFPI examinations.

If you’re evaluating California money transmitter license requirements, you’re likely dealing with a product that moves funds, stores value, or facilitates payments on behalf of users. In California, those activities fall under one of the most closely supervised money transmission regimes. The licensing process in this state is detailed, documentation-heavy, and tied to both state and federal oversight.

This guide explains how the California money transmitter license works in practice. It walks through what activities require a license, who regulates money transmitters in California, how the application process works, and what ongoing compliance looks like after approval. Let’s begin!

At InnReg, we support fintechs pursuing a California money transmitter license and preparing for DFPI review. We assist with licensing strategy, application documentation, and ongoing compliance operations after approval.

What the California Money Transmitter License Covers

The California money transmitter license (MTL) governs how companies receive, hold, and transmit funds or monetary value for others. It applies based on what the product actually does, not how it’s marketed or labeled. The DFPI focuses on transaction mechanics, custody of funds, and settlement responsibility.

If your company touches customer money before final delivery, the California MTL is often relevant. This is especially true for fintech products that rely on programmatic fund flows, pooled accounts, or intermediated settlement.

For digital asset businesses, money transmission analysis is often only one part of the licensing review. Companies that custody, exchange, or facilitate transactions involving digital financial assets may also need to evaluate California's Digital Financial Assets Law requirements.

Read more about the money transmitter license steps and requirements →

Activities That Trigger an MTL in California

In California, an MTL is generally required when a business engages in receiving money or monetary value for transmission within the state. The trigger is control, not duration. Even brief custody of funds can be enough.

Common triggering activities include:

Accepting funds from users and transmitting them to another person or entity

Holding customer funds in wallets, accounts, or stored value balances

Settling payments on behalf of third parties

Transmitting funds across state or national borders

Issuing or redeeming prepaid access or stored value

California evaluates the full transaction lifecycle. If your platform controls the movement or release of funds, licensing risk is high, regardless of whether the process is automated or manual.

Common Fintech Business Models That Require Licensing

Many modern fintech products fall within the scope of the California MTL, even when they don’t resemble traditional money services businesses.

Business models that frequently require licensing include:

Peer-to-peer payment applications

Payment facilitators and marketplace platforms

Crypto exchanges and custodial wallet providers (which may also be subject to California's Digital Financial Assets Law)

Remittance and cross-border payment providers

Fintech platforms using FBO or pooled customer accounts

Founders often assume that using a bank partner eliminates licensing exposure. In California, the presence of a bank doesn’t automatically remove MTL obligations. The regulator will examine which party has operational control over funds and compliance responsibilities.

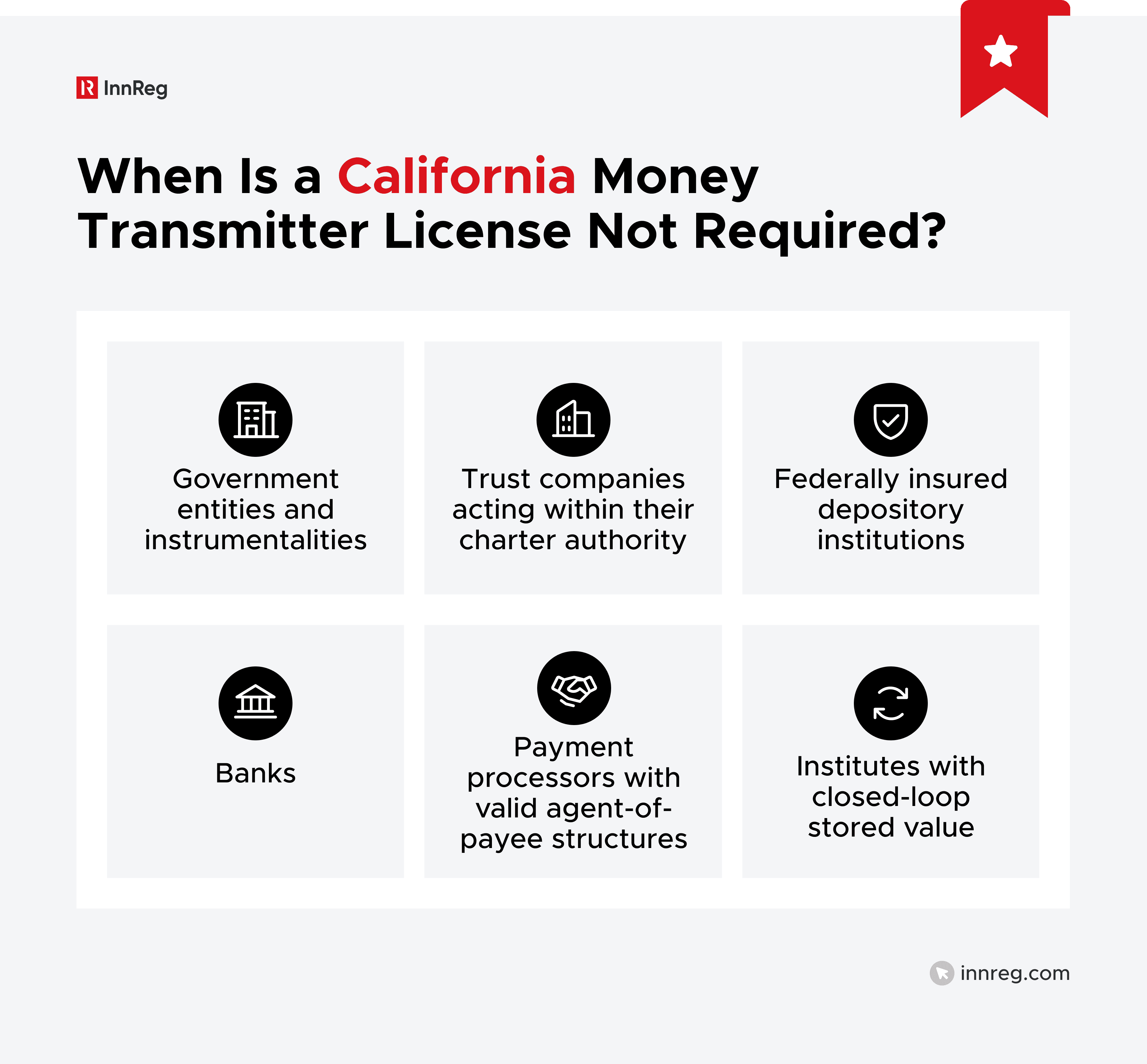

When a California MTL Is Not Required

California law includes several exemptions, but they’re narrow and fact-specific. Relying on them without a clear analysis creates regulatory risk.

Common exemptions include:

Banks and federally insured depository institutions

Certain trust companies and government entities

Payment processors operating under a valid agent-of-payee structure

Entities engaged in activities explicitly excluded by statute

The agent-of-payee exemption is frequently misunderstood. It requires a written agreement, proper disclosure, and clear liability alignment. Misapplying this exemption is one of the most common reasons fintechs operate without a license and later face regulatory scrutiny, enforcement actions, or civil penalties.

In practice, companies should evaluate exemptions only after mapping transaction flows in detail. The DFPI expects documentation, not assumptions, when an exemption is claimed.

Who Regulates Money Transmitter Licenses in California

Money transmitter licensing and supervision in California is handled by the California Department of Financial Protection and Innovation (DFPI). The DFPI is responsible for reviewing applications, issuing licenses, conducting examinations, and enforcing compliance with the Money Transmission Act.

The agency evaluates money transmitters through a risk-based lens. Its reviews focus less on product novelty and growth metrics and more on:

Financial condition

Safeguarding of customer funds

Governance

Compliance controls

This approach applies equally to early-stage fintechs and large, established platforms. For applicants, this means the DFPI expects clear and concise information. Transaction flows must be documented. Compliance ownership must be defined. Gaps in responsibility or reliance on informal explanations often lead to follow-up questions or delays.

The DFPI also administers California's Digital Financial Assets Law, making it the primary regulator for both money transmission and many digital asset activities conducted within the state.

Relationship Between California MTLs and FinCEN MSB Registration

State licensing and federal registration apply at the same time. Therefore, holding a California MTL doesn’t replace federal obligations. Money transmitters must also register with FinCEN as a Money Services Business and comply with the Bank Secrecy Act.

The two regimes serve different purposes:

FinCEN oversees AML, sanctions screening, and federal reporting

California regulates licensing, consumer protection, and financial safeguards at the state level

Both apply at the same time. FinCEN registration alone doesn’t authorize money transmission in California, and DFPI won’t issue an MTL without evidence of federal MSB registration.

The table below summarizes how the two regimes differ and how they interact.

Area | California MTL (DFPI) | FinCEN MSB Registration |

|---|---|---|

Regulator | California Department of Financial Protection and Innovation | Financial Crimes Enforcement Network |

Primary Focus | Licensing, consumer protection, and safeguarding of funds | AML, sanctions compliance, and financial crime monitoring |

Legal Basis | California Money Transmission Act | Bank Secrecy Act |

Required Before Operating in CA | Yes | Yes |

Ongoing Oversight | Examinations, reporting, enforcement | Audits, SAR/CTR filings, enforcement |

Gaps between state and federal compliance programs are a common source of follow-up questions during licensing and examinations.

California's Digital Financial Assets Law (DFAL)

Companies dealing with digital assets should be aware that a California money transmitter license may not be the only state license required.

The Digital Financial Assets Law (DFAL) establishes a separate regulatory framework for businesses engaged in digital financial asset activities in California. Depending on a company's business model, activities involving cryptocurrencies, stablecoins, or custodial digital asset services may fall under DFAL requirements in addition to money transmitter licensing obligations.

Examples of businesses that should evaluate DFAL applicability include cryptocurrency exchanges, custodial wallet providers, stablecoin businesses, digital asset payment platforms, and crypto brokerage and trading platforms.

For many crypto companies, licensing analysis now involves determining whether the business requires:

A California Money Transmitter License

A DFAL license

Both licenses simultaneously

The answer depends on the specific transaction flow, custody model, and digital asset activities being performed.

For a detailed discussion of the law, see our guide to the Digital Financial Assets Law (DFAL) →

California Money Transmitter License Eligibility Requirements

Before reviewing an application, the DFPI assesses whether the applicant is legally and operationally eligible to hold a California money transmitter license. If eligibility issues exist, the application won’t progress, regardless of product readiness or market traction.

Eligibility is evaluated based on entity structure, ownership, control, and the background of key individuals. This review is conservative by design and closely tied to consumer protection and financial integrity concerns. Here are the two sides of the eligibility requirement for a California money transmitter license:

Entity Type and Business Structure Rules

Only certain entity types can hold a California MTL. The applicant must be a corporation or limited liability company, whether formed in California or registered as a foreign entity doing business in the state.

Key structural requirements include:

A valid US legal entity in good standing

Registration to do business in California, if formed elsewhere

A designated California registered agent

A clear operating structure that aligns with the licensed activity

Individuals, partnerships, and informal entities are not eligible. DFPI also reviews whether the proposed business activities match the entity’s governing documents. Mismatches between the operating agreement and actual product behavior often lead to follow-up questions.

See also:

Ownership, Control Persons, and Background Checks

California places significant emphasis on who controls the licensed entity. Owners, executives, directors, and other control persons are reviewed individually, not just at the company level.

This review typically includes:

Disclosure of direct and indirect ownership interests

Identification of control persons and key individuals

Criminal background checks and fingerprinting

Credit reports and personal history disclosures

Ownership structures must be transparent. Complex holding companies, nominee arrangements, or offshore entities receive heightened scrutiny. Any prior regulatory actions, litigation, or financial distress must be disclosed and explained.

Need help with money transmitter compliance?

Fill out the form below and our experts will get back to you.

California MTL Net Worth and Financial Requirements

California imposes minimum financial thresholds on money transmitters to mitigate consumer risk and limit undercapitalized operators. These requirements apply at the time of application and on an ongoing basis after licensure.

Because net worth is a gating requirement in California, the DFPI reviews financial strength in context. While early-stage fintechs aren’t expected to look like banks, they are expected to demonstrate stability, access to capital, and the ability to operate without relying on customer funds.

How DFPI Evaluates Financial Condition

At a baseline level, California requires money transmitters to meet a minimum tangible net worth threshold. That threshold is assessed using audited financial statements and is tied to both balance sheet strength and business scale.

In practice, DFPI looks beyond the number itself. The source of capital, burn rate, and liquidity profile matter, especially for venture-backed or pre-revenue companies.

Key factors DFPI typically reviews include:

Tangible net worth reflected in audited financials

Capital structure and funding history

Cash position relative to projected operating expenses

Reliance on debt, related-party funding, or short-term financing

Financial projections are also reviewed for reasonableness. Aggressive growth assumptions without corresponding capital support often trigger follow-up questions.

From a compliance standpoint, companies should treat net worth as an ongoing obligation, not a one-time hurdle. Falling below required thresholds post-licensing can lead to supervisory action, including reporting requirements or license restrictions.

California MTL Surety Bond Requirements

In addition to net worth, California requires licensed money transmitters to post a surety bond or maintain an approved securities deposit. The bond is designed to protect consumers, not the company. It functions as a financial backstop if customer funds are mishandled or obligations are not met.

Bond requirements apply at licensing and continue throughout the life of the license. As transaction volume grows, bond obligations often increase as well:

Bond Ranges for Money Transmission vs. Stored Value

California calculates surety bond requirements based on the type of licensed activity and the level of outstanding customer obligations. Different activities are assessed separately, and some business models trigger more than one bond component.

Here’s what the bond ranges and calculations look like for both licensed activities:

Licensed Activity | How the Bond Is Calculated | Typical Bond Range |

|---|---|---|

Money Transmission | Based on average daily outstanding transmission obligations | $250,000 minimum, up to $7,000,000 |

Stored Value Issuance | Based on outstanding stored value and prepaid balances | $500,000 minimum, up to $2,000,000 |

Combined Activities | Aggregated across transmission and stored value obligations | Can exceed $1,000,000 depending on volume |

Bond amounts are reviewed during licensing and reassessed as transaction volume increases. Rapid growth or changes in product scope often trigger bond increases, even if the original bond was sufficient at approval.

For fintechs operating multiple flows, bond planning should account for how obligations stack across products rather than evaluating each feature in isolation.

Common Bonding Pitfalls for Early-Stage Fintechs

Bonding is one of the most underestimated aspects of money transmitter compliance. For most, the issue lies within qualification and capacity instead of the premium. Some of the most common challenges include:

Assuming the bond amount is static and will not increase

Underestimating how transaction volume affects bond calculations

Relying on projected volumes that later exceed approved levels

Failing to coordinate bond updates with DFPI reporting cycles

From an operational perspective, bond planning should be aligned with growth plans, not treated as a one-time licensing task. Fintechs that scale quickly without adjusting bonding often encounter compliance friction during examinations or renewals.

Money Transmitter License Application Checklist for California

Applying for a California money transmitter license is a document-intensive process. The DFPI expects applicants to submit a complete, internally consistent package that reflects how the business will actually operate once licensed. Missing or misaligned materials are one of the most common sources of delay.

This section outlines the DFPI’s expectations before and during submission. While details vary by business model, the core expectations are consistent across fintech use cases.

Pre-Filing Preparation and DFPI Expectations

Before filing through NMLS, companies should be able to clearly explain their product, transaction flows, and compliance ownership. DFPI reviews applications holistically, not as a collection of independent documents.

Here are the typical pre-filing preparation elements to consider:

Mapping end-to-end fund flows, including custody and settlement

Defining which entity is responsible for compliance decisions

Confirming licensing scope aligns with actual product behavior

Aligning business plans with financial and compliance materials

DFPI encourages pre-filing discussions for complex models. These conversations aren’t approvals, but they often surface issues that would otherwise delay review.

See also:

Required Documents and Disclosures

California requires extensive documentation to support the application. These materials are submitted through NMLS and, in some cases, directly to the DFPI.

Commonly required items include:

Detailed business plan and product descriptions

Organizational and ownership charts

Personal disclosures for control persons and key individuals

Sample consumer disclosures and transaction receipts

All disclosures must be accurate and internally consistent. Discrepancies across documents frequently trigger follow-up questions, especially around ownership, control, and product scope.

AML, BSA, and Compliance Program Requirements

Applicants must submit a written AML and compliance program tailored to their specific risk profile. Generic templates are usually insufficient.

At a minimum, DFPI expects documentation covering:

Customer identification and verification processes

Transaction monitoring and escalation procedures

Sanctions screening and reporting obligations

Independent testing and compliance oversight

The program should reflect how compliance operates day to day. DFPI evaluates whether policies are operational, not just well-written.

Financial Statements and Audit Expectations

Financial materials are central to the application. California generally requires audited financial statements prepared per US accounting standards. DFPI reviews:

Audited balance sheets and income statements

Capitalization and funding sources

Financial projections and assumptions

Liquidity relative to operating needs

Weak or outdated financials often slow the review. From a practical standpoint, financial readiness should be addressed before submission, not during regulator follow-up.

How to Apply for a Money Transmitter License in California Through the NMLS

California uses the Nationwide Multistate Licensing System to manage MTL applications. The DFPI reviews applications after submission. The system standardizes submissions, but doesn’t simplify the underlying requirements.

Here are the typical steps one would take to apply for a California money transmitter license:

Company Application (MU1)

The MU1 filing captures core information about the applicant entity and its proposed activities. This filing sets the baseline for the entire application.

Key components include:

Legal entity details and business addresses

Description of licensed activities and products

Ownership structure and control relationships

Financial condition and funding sources

Information entered in MU1 must match the business plan and compliance documentation. Inconsistencies between MU1 and supporting exhibits are a frequent cause of delays.

Individual Filings for Owners and Executives (MU2)

Each owner, executive, director, and other control person must submit an MU2 filing. These disclosures are reviewed individually.

MU2 filings should include:

Personal history and employment background

Criminal and regulatory disclosures

Credit report authorization

Fingerprinting and background checks

DFPI evaluates both individual fitness and collective governance. Undisclosed issues or incomplete explanations often lead to follow-up requests.

Supplemental DFPI Forms and Mail-In Requirements

Not all required materials are submitted through NMLS. California also requires firms to complete and deliver supplemental forms directly to the DFPI.

These may include:

Personal financial statements

Confidential resumes for key individuals

Authorization and attestation forms

Emergency contact and service of process documents

Submission timing matters. NMLS filings and DFPI mail-in materials should be coordinated, not staggered, to avoid processing delays.

See also:

California MTL Review Process and Timeline

Once an application is submitted through NMLS and all supplemental materials are received, the DFPI begins a substantive review. During review, DFPI typically examines transaction flows, custody of customer funds, financial condition, compliance ownership, and alignment between the business plan and supporting documents.

There is no statutory approval timeline for a California MTL application. In practice, initial feedback often arrives several weeks after submission, followed by one or more rounds of information requests. End-to-end review frequently exceeds nine months, particularly for first-time applicants or fintechs with complex products.

Most delays are caused by incomplete explanations of fund flows, late changes to ownership or product scope, or compliance programs that do not reflect actual operations.

Ongoing Compliance Obligations After Approval

Receiving a California money transmitter license is not the end of regulatory oversight. It marks the start of an ongoing supervisory relationship with the DFPI. Licensed money transmitters are expected to maintain financial condition, compliance controls, and reporting discipline on a continuous basis.

Therefore, post-licensing obligations become operational as the DFPI evaluates how requirements are implemented day to day:

Annual Reporting, Renewals, and DFPI Fees

California MTL holders are subject to recurring reporting and fee obligations. These requirements apply regardless of transaction volume or growth stage.

Ongoing obligations typically include:

Annual license renewal through NMLS

Periodic financial and transaction reporting

Annual DFPI license and assessment fees

Timely updates for ownership, control, or business changes

Missed filings or late updates often lead to supervisory follow-up. DFPI expects proactive reporting, not corrective disclosures after the fact.

Permissible Investments and Safeguarding Customer Funds

Money transmitters have to hold enough permissible investments to cover their outstanding customer obligations. The idea is straightforward: if the business runs into financial trouble, customer funds should still be protected.

What does this look like day to day? You’ll need to keepeligible assets on hand that match your outstanding transmission and stored value liabilities, segregate customer funds when required, and monitor balances as transaction volume changes.

This isn't something the DFPI only checks during exams. Permissible investment compliance is monitored on an ongoing basis. We often see problems when companies grow quickly but don't adjust their investment holdings to keep pace.

Examinations, Audits, and Regulatory Oversight

The DFPI conducts periodic examinations of licensed money transmitters. These examinations focus on how compliance operates in practice, not whether policies exist on paper. These reviews are detailed and often resource-intensive.

The core of these examinations is to cover:

Transaction processing and fund safeguarding

AML and sanctions compliance

Financial condition and capital adequacy

Governance, policies, and internal controls

For many fintechs, this level of operational rigor is difficult to maintain with a single internal hire. That’s why companies often engage firms like InnReg to operate as an outsourced compliance function.

InnReg supports day-to-day compliance execution, examination preparation, and regulator interaction. This model allows teams to meet DFPI expectations without building a full in-house compliance department before scale.

—

Navigating California money transmitter license requirements is as much an operational exercise as it is a regulatory one. From licensing through ongoing supervision, the DFPI evaluates how money transmission works in practice, how risks are managed, and how compliance is executed over time.

Teams that approach the process with clear documentation, realistic financial planning, and defined compliance ownership are better positioned as their business grows.

If you’re preparing to apply for a California money transmitter license or managing post-approval compliance, contact InnReg to learn more about how we can help support licensing, as well as building and running compliance programs as an extension of your team.

José is a Compliance Consultant with over 6 years of experience across Tier-1 financial institutions including KPMG, Deutsche Bank, ICBC, and Citco. He specializes in KYC/AML, transaction monitoring, forensic financial investigations, and emerging frameworks such as MiCA and DORA. He holds a Master's from SOAS University of London.

How Can InnReg Help?

InnReg is a global regulatory compliance and operations consulting team serving financial services companies since 2013.

We are especially effective at launching and scaling fintechs with innovative compliance strategies and delivering cost-effective managed services, assisted by proprietary regtech solutions.

If you need help with money transmitter compliance, reach out to our regulatory experts today:

Related Articles

Featured LinkedIn Posts