Preparing For a Regulatory Exam: A Fintech Guide

Key Takeaways

Regulatory exams are supervisory reviews that assess a firm’s compliance program, records, internal controls, and actual business operations.

Exams may be triggered by a firm’s initial registration, conducted on a routine risk-based cycle, initiated for cause, or performed as part of an industry-wide sweep.

Oversight is typically conducted by regulators such as the SEC, FINRA, state agencies, the CFPB, and various banking regulators, depending on the firm’s structure and activities.

Regulators commonly request materials including written policies and procedures, books and records, testing documentation, marketing materials, and vendor oversight records.

Frequent findings include outdated or incomplete policies, gaps in recordkeeping, weak supervisory frameworks, and issues related to vendor management and disclosures.

Regulatory exams are a key part of running a regulated financial services business. Broker-dealers, investment advisors, money transmitters, and other fintech companies should expect periodic reviews from regulators such as the SEC, FINRA, state agencies, or the CFPB.

But most people don’t know what these exams are designed to evaluate. Furthermore, for many firms, regulatory exam prep becomes urgent only after receiving an exam notice. In practice, preparation works best when it is ongoing. Regulators often request extensive documentation, interview key personnel, and review how compliance policies operate in real business workflows.

So in this guide, let’s explain how regulatory exams work, what they’re looking to evaluate, and how you can practically prepare for them. The guide also covers common findings during these examinations and how to build a compliance process that keeps pace with your fintech model.

At InnReg, we support fintech firms preparing for regulatory exams and strengthening their compliance programs. Our team assists with regulatory documentation, supervisory procedures, and ongoing compliance operations. Contact us to discuss your regulatory exam prep.

What Is a Regulatory Exam?

A regulatory exam is a formal review conducted by a financial regulator to evaluate whether a firm is complying with applicable laws and regulatory obligations. These exams apply to a wide range of regulated entities, such as:

Regulators use exams to assess how a firm operates in practice. They review policies and procedures, but they also examine books and records, transaction data, communications, and internal controls. The goal is to determine whether the firm’s compliance program is reasonably designed and whether its day-to-day operations match its written policies.

The exams typically follow a structured process, which we’ll discuss later in this article. But it’s critical to understand that regulatory exams are not enforcement actions. They are supervisory reviews. That said, issues identified during an exam can lead to remediation requirements or, in some cases, referrals to enforcement if serious problems are discovered.

How Regulators Supervise Firms Through Exams

Regulators rely on examinations as one of their primary supervisory tools. A regulatory exam allows agencies to verify that firms are following the rules that apply to their licenses and business models. It also gives regulators visibility into how firms manage risk, handle customer assets, and supervise their operations.

Exams are typically risk-based. This means regulators do not review every firm in the same way or on the same schedule. Instead, the scope and frequency of a regulatory exam often depend on factors such as:

Firm size

Business activities

Customer base

Past compliance history

For fintech companies, supervision often extends beyond traditional compliance topics. Regulators frequently review how technology platforms, third-party providers, and product design affect compliance controls. This is particularly relevant for firms operating hybrid models such as brokerage platforms with embedded payments or digital asset features.

Types of Regulatory Exams

Not all regulatory exams are the same. Regulators conduct different types of examinations depending on the firm’s risk profile, recent activity, and supervisory priorities. Understanding the type of regulatory exam helps firms anticipate what regulators are likely to review.

Below are the most common exam types financial firms encounter:

Routine Examinations

Routine exams are the most common form of regulatory supervision. These are periodic reviews conducted as part of a regulator’s standard oversight program. Broker-dealers, investment advisors, and other regulated firms are typically examined on a recurring cycle.

The timing depends on the regulator and the firm’s risk profile. Some firms may be examined every one to two years, while others may see longer gaps between exams. Routine exams usually cover core areas such as compliance programs, recordkeeping, supervision, and customer protection.

Cause Examinations

Cause exams occur when regulators identify a potential issue that requires closer review. These exams are triggered by specific concerns rather than a routine supervisory schedule.

Common triggers include customer complaints, regulatory tips, unusual trading activity, or deficiencies identified in prior exams. Cause exams often focus on a narrower set of issues, but regulators may expand the scope if additional concerns arise during the review.

Unusual trading activity means filing a suspicious activity report. Read here to learn how to file one yourself →

Industry Sweep Examinations

Sweep exams are targeted reviews conducted across multiple firms in the same sector. Regulators use sweep exams to evaluate how an entire industry handles a particular regulatory risk.

For example, a regulator may conduct a sweep focused on digital marketing practices, crypto-related brokerage activity, or client onboarding procedures. Firms selected for a sweep exam may receive similar document requests so regulators can compare practices across the industry.

Regulators That Conduct Regulatory Exams

Several regulators oversee financial firms in the US, and many have examination authority. The specific regulator conducting a regulatory exam depends on the firm’s licenses, activities, and jurisdiction. Some firms may be examined by multiple regulators.

Understanding which agencies may examine your business is an important part of regulatory exam prep.

SEC Examinations for RIAs and Investment Companies

The Securities and Exchange Commission examines registered investment advisors and investment companies through its Division of Examinations. SEC exams evaluate whether firms are complying with federal securities laws, including the Investment Advisers Act of 1940.

These exams typically review areas such as:

Compliance programs

Fiduciary obligations

Fee calculations

Custody arrangements

Marketing practices

Conflicts of interest

The SEC also publishes annual exam priorities that highlight specific risks or industry practices receiving increased scrutiny. For SEC-registered advisors, the first SEC exam occurs within the first few years after registration. The scope of the review often reflects the firm’s size, services, and client base.

FINRA Examinations for Broker-Dealers

Broker-dealers are primarily examined by the Financial Industry Regulatory Authority. FINRA conducts regular cycle exams as well as targeted reviews based on risk signals identified through market surveillance and regulatory reporting.

FINRA exams focus heavily on supervision and sales practices. Examiners frequently review trading activity, written supervisory procedures, customer communications, AML programs, branch supervision, and account documentation.

FINRA also conducts thematic exams and industry sweeps when new risks emerge. These reviews often focus on areas such as digital communications, complex products, or new brokerage technology.

State Securities Regulators

State securities regulators oversee broker-dealers and investment advisor firms that are registered at the state level rather than with the SEC. They also enforce state securities laws, commonly referred to as blue sky laws.

State exams often mirror many aspects of SEC reviews. Regulators examine compliance policies, books and records, client disclosures, advertising practices, and custody of client assets. For smaller advisory firms, state regulators are often the primary examination authority.

Because each state has its own regulatory agency, examination practices may vary slightly depending on the jurisdiction.

See also:

State Regulators For Money Transmitters and Payment Companies

Money transmitters and certain payment companies are regulated at the state level in the US. Firms operating nationally often hold dozens of state licenses and may face examinations from multiple state regulators.

These exams typically focus on financial condition, safeguarding of customer funds, transaction monitoring, complaint handling, and vendor oversight. State regulators also review whether firms are complying with licensing requirements and reporting obligations.

Many states now coordinate exams through the Nationwide Multistate Licensing System (NMLS) and multistate examination programs, which can streamline the process for firms operating across several jurisdictions.

Need help with fintech compliance?

Fill out the form below and our experts will get back to you.

CFPB and Other Federal Financial Regulators

Some fintech companies fall under the supervision of the Consumer Financial Protection Bureau or other federal regulators, depending on the products they offer. This often applies to companies involved in consumer lending, payments, servicing, or credit reporting.

CFPB exams focus primarily on consumer protection obligations. Regulators review disclosures, marketing practices, complaint handling, fair lending controls, and servicing processes.

Other federal regulators may also conduct exams depending on the structure of the business. For example, firms affiliated with banks may face oversight from prudential regulators such as the OCC, Federal Reserve, or FDIC.

When and Why Firms Receive a Regulatory Exam

Many founders assume exams happen on a fixed schedule. In reality, most regulatory exams are triggered by a regulator’s risk assessment process rather than a strict timeline. The timing often depends on the firm’s activities, size, and supervisory history.

Below are the most common situations in which firms receive a regulatory exam.

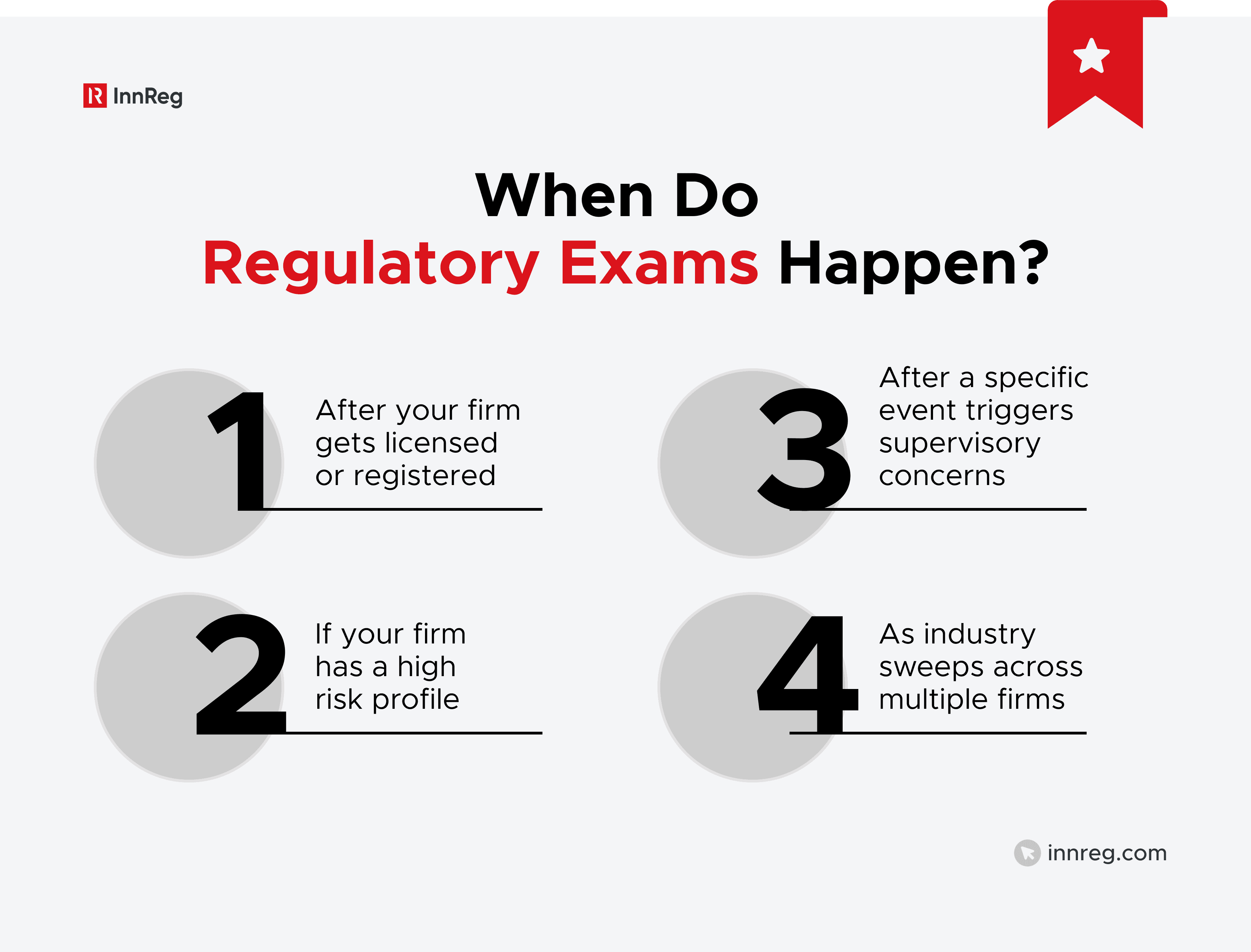

First-Time Exams After Registration

Many regulators conduct an initial exam after a firm becomes registered or licensed. These first-time exams are designed to confirm that the firm’s compliance program operates as described in its registration filings.

Regulators typically review policies, operational workflows, disclosures, and supervisory controls. They also want to understand how the firm implemented its compliance program after receiving regulatory approval.

For fintech companies launching new models, these exams often include detailed questions about technology platforms, vendor arrangements, and product design.

Routine Risk-Based Examinations

Most regulators follow a risk-based approach when scheduling exams. This means firms with higher risk profiles may be examined more frequently.

Factors regulators often consider include:

Firm size and growth rate

Complexity of products or services

Customer base and geographic reach

Prior examination findings

Regulatory reporting patterns

This approach allows regulators to allocate exam resources toward firms that present greater potential risk to investors or consumers.

Triggered or Cause Exams

Some regulatory exams occur because a regulator identifies a potential issue. These cause exams are initiated when specific events raise supervisory concerns.

Customer complaints, unusual transaction patterns, regulatory tips, or inconsistencies in filings or reports can trigger regulatory attention. In some cases, findings from a previous exam can also lead to a follow-up review.

Although cause exams may begin with a specific concern, regulators sometimes expand the review if additional issues appear during the examination.

Industry Sweeps and Thematic Reviews

Regulators also conduct exams that target specific practices across multiple firms. These are known as industry sweeps or thematic exams.

In these cases, regulators review how firms handle a particular regulatory risk or emerging business model. Examples may include digital marketing practices, crypto-related brokerage activity, or vendor oversight in fintech platforms.

Firms selected for a sweep exam often receive similar document requests so regulators can compare compliance approaches across the industry.

What Regulators Typically Request During a Regulatory Exam

Once a regulatory exam begins, the regulator will usually send an exam notice along with a document request list. This request list outlines the information regulators need to evaluate the firm’s compliance program and operations.

The scope of the request can vary depending on the regulator and the firm’s business model. However, most regulatory exams focus on several core categories of documentation.

Exam Notification Letters and Document Requests

Most exams begin with a formal notification letter. This letter typically explains the scope of the exam, the regulatory authority involved, and the initial documents the regulator wants to review.

The document request list is often extensive and time-sensitive. Firms may be asked to provide policies, internal reports, communications, and transaction data within a short timeframe. Regulators may also issue additional requests as the exam progresses.

For many firms, organizing and producing these materials becomes one of the most demanding parts of regulatory exam prep.

Policies and Procedures

Regulators almost always review the firm’s written compliance program. This includes supervisory procedures, compliance manuals, AML programs, and other internal governance documents.

Examiners compare these policies against the firm’s actual operations. If the firm has launched new products or services without updating its procedures, that gap may become a finding during the exam.

Policies are also reviewed to determine whether responsibilities are clearly assigned and whether supervisory controls are documented.

Explore our guide on written supervisory procedures for broker-dealers →

Books and Records

Books and records are a central focus of most regulatory exams. Regulators rely on these records to verify transactions, communications, and operational activity.

Common record requests include customer account records, transaction data, communications, and internal reports. Regulators may also review how records are stored, retained, and retrieved.

In many cases, the speed at which a firm can produce records becomes an important factor during the exam.

See also:

Compliance Testing and Monitoring Documentation

Regulators often review how the firm tests its own compliance program. This includes internal reviews, monitoring reports, exception tracking, and remediation documentation.

These materials demonstrate whether the firm actively monitors compliance risks rather than relying only on written policies. Examiners may also review how issues were escalated and resolved.

A well-documented testing process can help demonstrate that the firm’s compliance program is functioning as intended.

Marketing and Client Communications

Marketing practices are frequently reviewed during regulatory exams. Regulators want to confirm that communications with clients are accurate, balanced, and compliant with applicable rules.

This review may include:

Website content

Advertisements

Social media posts

Email communications

Pitch materials

Examiners often test whether marketing claims are supported by appropriate disclosures and documentation. For fintech companies, digital marketing channels are often a particular area of regulatory attention.

Vendor Management and Third-Party Oversight Records

Many financial firms rely on vendors for key operational functions. Regulators often review how firms manage those relationships.

Vendor oversight documentation may include due diligence reviews, service agreements, monitoring reports, and incident management records. Regulators want to understand how the firm supervises third-party providers that support regulated activities.

This area is especially relevant for fintech companies that depend heavily on platform providers, banking partners, or specialized technology vendors.

Common Findings in Regulatory Exams

Regulatory exams often reveal similar compliance weaknesses across firms. In many cases, the issue is not misconduct but gaps between written policies, operational processes, and documentation.

Examiners typically focus on whether a firm’s compliance program is reasonably designed and whether staff actually follow it. Over time, regulators have highlighted several recurring issues in exam reports, deficiency letters, and risk alerts:

Outdated or Incomplete Compliance Programs

A common exam finding is a compliance program that no longer reflects how the firm operates. Fintech companies evolve quickly. Products change, vendors change, and new services are introduced.

Regulators expect written policies to reflect the firm’s current business model. When procedures describe workflows that are no longer used or fail to address new services, examiners often identify this as a supervisory weakness.

For example, a brokerage platform that adds crypto trading or fractional shares may need to update supervisory procedures, disclosures, and surveillance controls to reflect the new activity.

Books and Records Deficiencies

Books and records remain one of the most heavily scrutinized areas during regulatory exams. Federal securities laws, FINRA rules, and state regulations all impose strict recordkeeping requirements.

If a firm cannot produce records quickly or if records are incomplete, regulators may treat that as a compliance failure.

Examiners often encounter issues such as:

Missing transaction documentation

Inconsistent client records across systems

Communications stored outside approved archiving systems

Delays in producing requested records during an exam

For broker-dealers, these requirements are heavily influenced by SEC Rules 17a-3 and 17a-4, which govern record creation and retention.

Read about the compliance essentials for recordkeeping according to Rule 17a-4 here →

Weak Supervisory Controls

Supervisory controls determine how firms monitor regulated activity and escalate potential issues. During exams, regulators review both the structure of supervision and the documentation supporting it.

Examiners typically look for evidence that supervision is active, not just assigned on paper. This may include supervisory reviews of transactions, communications, exception reports, and compliance testing results.

For instance, a firm may designate a supervisor responsible for reviewing advertising or communications. If those reviews are not documented, regulators may conclude that supervision is not functioning effectively.

See also:

Vendor Oversight Gaps

Vendor oversight has become a major regulatory focus, particularly for fintech firms that rely on third-party technology providers.

Regulators increasingly expect firms to demonstrate how they monitor vendors that support regulated activities. If critical services are outsourced, regulators still hold the licensed firm responsible for compliance.

Vendor oversight reviews often include:

Due diligence conducted before onboarding the vendor

Written service agreements and responsibilities

Ongoing monitoring and performance reviews

Incident escalation and remediation procedures

This issue frequently appears in exams involving embedded finance platforms, payments infrastructure providers, and outsourced compliance tools.

Marketing and Disclosure Issues

Marketing practices are another frequent exam focus. Regulators evaluate whether communications with customers are fair, balanced, and supported by appropriate disclosures.

Digital marketing has received increasing attention in recent regulatory exams. Websites, social media posts, and online promotions often fall within the scope of review.

For investment advisors, this area is shaped by the SEC Marketing Rule (Rule 206(4)-1 under the Investment Advisers Act), which governs testimonials, endorsements, and performance advertising. Firms that promote performance results or client experiences without proper disclosures may face regulatory findings during exams.

How a Regulatory Exam Typically Works

Although each regulator has its own procedures, most exams follow a similar structure. A regulatory exam is typically a multi-stage process that begins with a notification and ends with written findings or feedback.

Understanding how the process unfolds can make regulatory exam prep more manageable and help firms allocate resources effectively during the review:

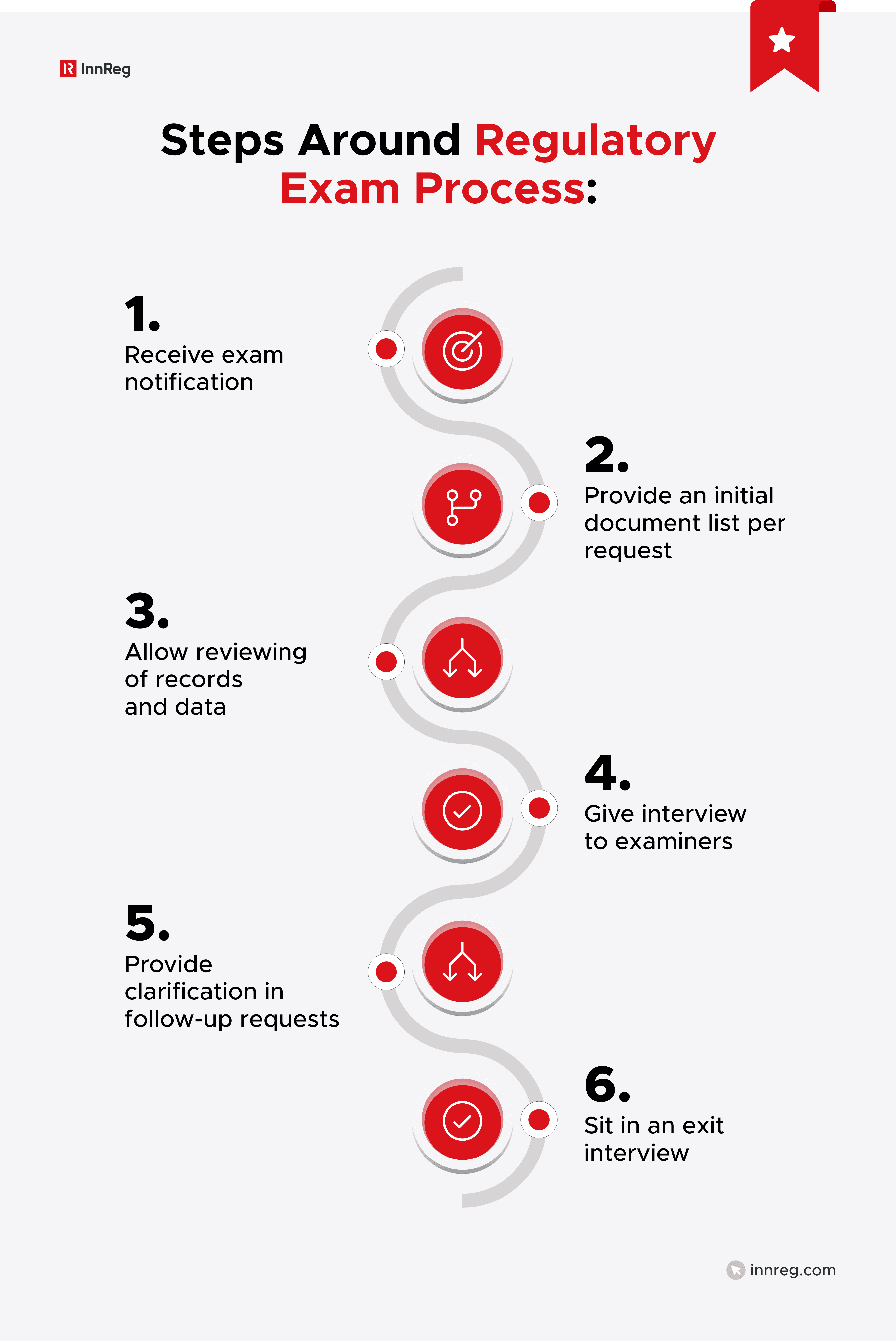

Step 1: Exam Notification

Most regulatory exams begin with a formal notification from the regulator. This notice is usually sent as an official letter or email to the firm’s compliance contact, Chief Compliance Officer, or registered supervisory principal.

For broker-dealers, FINRA typically sends the notice through its regulatory portal or by email to the firm’s compliance leadership. SEC exams are often initiated through a formal letter from the Division of Examinations. State regulators may contact the firm through licensing portals such as NMLS or directly through the compliance contact listed in the firm’s filings.

The notification usually includes several key details, such as:

The scope of the regulatory exam

The exam team or regulator conducting the review

The time period being examined

The initial document request list

Deadlines for submitting materials

In many cases, regulators request documents within 10 to 30 days, though the timeline can vary depending on the exam type and the size of the firm.

The notice may also specify whether the exam will be conducted remotely, on-site, or through a hybrid process. In recent years, many regulatory exams have shifted toward remote document reviews, with interviews conducted through video calls or follow-up meetings.

Once the notification arrives, most firms immediately begin organizing internal records, assigning responsibilities for document production, and preparing staff who may be interviewed during the exam.

Step 2: Initial Document Request List

After the notification, regulators typically request a broad set of materials related to the firm’s operations and compliance program.

These requests may include policies and procedures, transaction records, communications, supervisory reports, and compliance testing documentation. The first request list is rarely the final one. Regulators often submit additional requests as they review the information.

For larger firms or complex fintech platforms, these document requests can involve multiple internal teams.

Step 3: Regulator Review Of Records And Data

Once documents are submitted, examiners begin analyzing the firm’s records. This stage often involves reviewing transaction activity, customer communications, marketing materials, and supervisory reports.

Examiners may also perform targeted testing of transactions or operational workflows. For example, they may select a sample of client accounts or transactions to confirm that procedures were followed.

This review stage can last several weeks depending on the scope of the exam.

Step 4: Interviews With Management and Compliance Staff

Examiners frequently conduct interviews with key personnel. These discussions help regulators understand how policies operate in practice and how decisions are made within the firm.

Interviews often involve senior management, compliance officers, operations staff, and sometimes product or technology teams. Regulators use these conversations to compare written procedures with real operational workflows.

For fintech companies, questions often focus on platform architecture, vendor relationships, and automated compliance controls.

Step 5: Follow-Up Requests and Clarifications

During the exam, regulators typically submit additional questions or document requests. These follow-ups may relate to information discovered during the initial review.

This stage is common and should not be interpreted as a negative signal. Follow-up requests simply reflect the regulator’s effort to clarify how the firm operates or to gather additional context. In some exams, this stage accounts for a significant portion of the overall timeline.

Step 6: Exit Interview and Preliminary Findings

Toward the end of the exam, regulators often conduct an exit interview or closing meeting. During this discussion, examiners may summarize observations or highlight potential concerns.

After the exam concludes, firms may receive a deficiency letter describing any issues identified during the review. The letter usually outlines areas where the regulator expects remediation or additional documentation.

The firm may then need to respond with a remediation plan or provide evidence that the issues have been addressed.

Regulatory Exam Prep: Preparing Before an Exam Starts

The most effective regulatory exam prep happens long before a regulator sends an exam notice. Preparation does not require building new systems every time an exam occurs. Instead, it involves the following process:

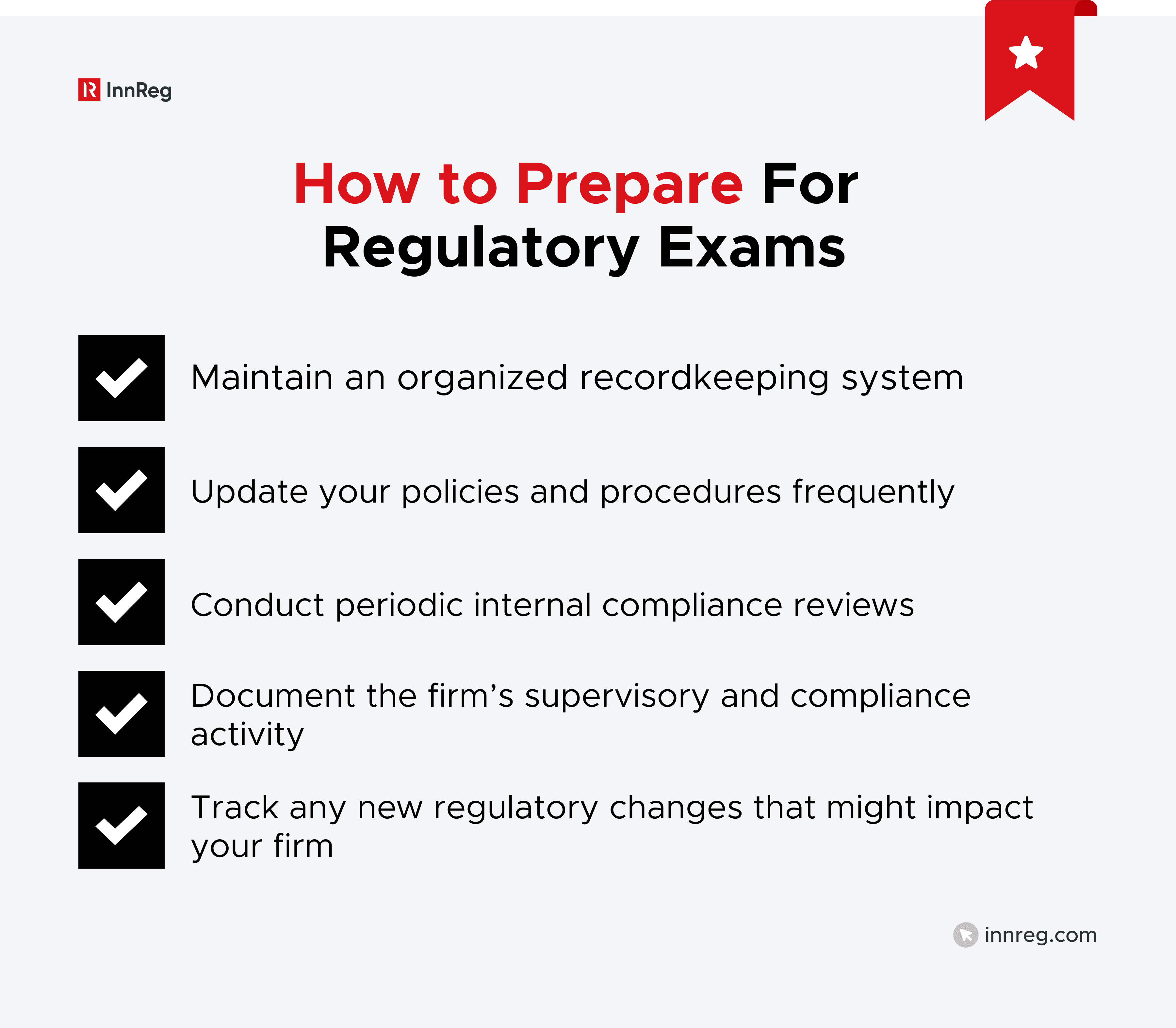

Maintain Organized Books and Records

Recordkeeping is one of the first areas regulators review during a regulatory exam. If documents are scattered across systems or difficult to retrieve, the exam process can quickly become more complicated.

Firms should be able to locate and produce key records quickly. This includes:

Customer account documentation

Transaction data

Communications

Supervisory reports

Compliance logs

For fintech companies that rely on multiple platforms, this often means maintaining a clear system for retrieving records from different vendors and internal tools.

Keep Policies and Procedures Current

Compliance policies should reflect how the firm actually operates. When a firm launches a new product, changes its onboarding process, or introduces a new vendor, policies should be updated accordingly.

Regulators often compare written procedures with real workflows during a regulatory exam. If policies describe processes that no longer exist, examiners may identify this as a compliance weakness.

Regular policy reviews can help firms keep documentation aligned with operational changes.

Conduct Periodic Internal Compliance Reviews

Internal reviews help firms identify compliance gaps before regulators do. Many firms conduct periodic compliance testing or internal audits to evaluate how controls are functioning.

These reviews often examine areas such as recordkeeping, marketing practices, vendor oversight, and supervisory controls. Documented internal reviews demonstrate that the firm actively monitors its compliance program.

When issues are identified, regulators also expect to see how they were addressed.

Document Supervisory and Compliance Activity

Supervisory activity should be documented consistently. Regulators frequently review how supervisors monitor transactions, communications, and operational activity.

Written evidence of supervision is often as important as the supervisory activity itself. Exception reports, review logs, and escalation records help demonstrate how issues are identified and addressed.

Without documentation, regulators may question whether supervision is actually occurring.

Track Regulatory Changes Affecting The Business

Regulatory expectations evolve over time. New rules, risk alerts, and enforcement trends often influence what regulators review during exams.

Firms should monitor developments from regulators such as the SEC, FINRA, CFPB, and state agencies. Staying informed about regulatory priorities helps firms anticipate the areas examiners may focus on.

For example, recent regulatory priorities have placed greater attention on digital communications, marketing practices, vendor oversight, and emerging fintech business models.

Watch out for these fintech trends in 2026 →

Regulatory Exam Prep Checklist

Preparing for a regulatory exam often comes down to organization. When regulators send a document request list, firms need to locate policies, records, and supervisory documentation quickly. A structured checklist helps compliance teams confirm that key areas of the business are exam-ready before regulators request them.

The table below highlights the core areas regulators commonly review during exams:

Area | What Regulators Typically Look For |

|---|---|

Policies and Procedures | Current compliance manuals, supervisory procedures, AML policies, and governance documentation that reflect the firm’s actual business model |

Books and Records | Customer account records, transaction data, communications archives, and required regulatory records |

Compliance Testing | Internal reviews, monitoring reports, exception tracking, and documentation of issue remediation |

Supervisory Controls | Evidence of supervisory reviews, escalation procedures, and clearly assigned oversight responsibilities |

Vendor Oversight | Due diligence files, service agreements, monitoring reports, and documentation of vendor supervision |

Before an exam begins, many firms review these areas internally to confirm documentation is complete and accessible. Regulators often evaluate not only whether records exist, but also how quickly the firm can produce them when requested.

For fintech companies, this preparation often includes confirming that records stored across multiple systems, platforms, or vendors can be retrieved efficiently. This is particularly important for firms that rely on external infrastructure for onboarding, payments, trading, or compliance monitoring.

Interested in learning more? Find out more about how to handle a regulatory exam inquiry →

What Happens After a Regulatory Exam

A regulatory exam does not end when document requests and interviews are completed. After the review phase, regulators typically communicate their observations and any issues they identified. This might appear within written findings that outline improvement areas for your fintech.

Deficiency Letters and Findings

Many exams conclude with a deficiency letter. This document summarizes issues identified during the review and explains the regulator’s concerns.

Deficiency letters usually focus on specific compliance gaps or supervisory weaknesses. The letter may reference missing documentation, outdated policies, marketing concerns, or insufficient supervisory controls.

The firm is typically asked to respond within a set timeframe and explain how it plans to address the findings.

Remediation Expectations

After receiving the findings, firms are expected to implement corrective actions. This may involve updating policies, improving documentation, strengthening supervisory reviews, or adjusting operational workflows.

Regulators usually expect firms to provide evidence of remediation, such as updated procedures, revised disclosures, or documented compliance reviews.

In many cases, the remediation process becomes a key part of ongoing regulatory supervision.

Follow-Up Examinations

In some situations, regulators may conduct follow-up exams to review whether identified issues were addressed. These reviews are typically more focused and concentrate on the specific findings from the earlier exam.

Follow-up exams are common when regulators want to confirm that remediation steps were implemented. They are particularly likely when the original exam identified structural weaknesses in supervision or compliance controls.

Potential Enforcement Referrals

Most regulatory exams do not lead to enforcement actions. However, if regulators identify serious violations, the matter may be referred to an enforcement division for further investigation.

This typically occurs when examiners believe the issue involves significant regulatory breaches, misconduct, or harm to customers. In those cases, the exam findings may form part of a broader enforcement inquiry.

For most firms, however, the regulatory exam process ends with remediation and continued supervisory oversight rather than formal enforcement proceedings.

When Firms Seek Outside Help With Regulatory Exam Prep

Preparing for a regulatory exam can require significant internal coordination and time that fast-moving fintechs don’t often have. In these situations, firms sometimes bring in outside compliance support to help manage preparation and exam responses.

Below are the top three times when it’s almost always wiser to bring in outsourced compliance professionals:

Preparing For a First Regulatory Exam

The first regulatory exam can be challenging because firms may not yet know what regulators will focus on. Early-stage fintech companies often move quickly, which can leave gaps between operational workflows and written compliance documentation.

External compliance specialists can help review policies, records, and procedures before the exam begins. This type of preparation often focuses on identifying documentation gaps, organizing regulatory records, and preparing staff who may be interviewed during the exam.

For firms launching new products or operating complex platforms, outside support can also help explain how the business model fits within regulatory expectations.

Addressing Internal Compliance Gaps

Some firms seek outside support after identifying weaknesses in their compliance program. This may occur during internal reviews, mock exams, or when preparing responses to regulator requests.

External advisors can provide an independent assessment of the compliance framework and identify areas that may require remediation. This often includes reviewing supervisory procedures, vendor oversight programs, and documentation practices.

For fintech companies operating hybrid financial models, specialized regulatory experience can be particularly useful when aligning innovative products with traditional regulatory requirements.

Managing Regulator Communications and Remediation

Responding to regulators often involves multiple rounds of document production, follow-up questions, and remediation planning. Firms sometimes engage outside compliance teams to help manage these interactions.

Support may include organizing document responses, preparing written explanations, and helping coordinate remediation efforts after exam findings. This type of support can be especially valuable when firms need to address complex compliance issues while continuing day-to-day operations.

In some cases, firms also rely on outsourced compliance teams to help maintain ongoing exam readiness, particularly when building an internal compliance department is not yet practical.

—

Regulatory exams are a routine part of operating a licensed financial services business. But regulatory exam prep should not start when the first notification letter arrives. If your firm is preparing for a regulatory exam or wants to strengthen its compliance program before one arrives, InnReg can help.

We work directly with fintech companies to build exam-ready compliance operations. Our team can act as your outsourced compliance department or an extension of your internal team, helping organize regulatory documentation, review policies and procedures, and manage exam responses with regulators such as the SEC, FINRA, and state agencies.

If you want experienced compliance specialists supporting your regulatory exam prep, contact InnReg to discuss your firm’s regulatory readiness.

Maria is a Compliance Consultant at InnReg delivering compliance solutions for fintech clients across broker-dealer, RIA, and money transmitter verticals. She brings prior experience at Finalis, Fenix Securities and PwC, with expertise in AML, CCO support, investment banking operations and securities compliance. She holds FINRA Series 14, 24, and 82 licenses and actively supports regulatory and compliance processes revolving broker-dealer activities.

How Can InnReg Help?

InnReg is a global regulatory compliance and operations consulting team serving financial services companies since 2013.

We are especially effective at launching and scaling fintechs with innovative compliance strategies and delivering cost-effective managed services, assisted by proprietary regtech solutions.

If you need help with compliance, reach out to our regulatory experts today:

Related Articles

Featured LinkedIn Posts