Fintech Market Makers: Roles and Risks

Market makers are foundational to how financial markets function, especially in sectors where liquidity and speed are critical.

In both traditional and crypto markets, market makers play a key role in maintaining consistent price discovery and execution. While their function is similar across environments, the underlying models, particularly in decentralized systems, can differ significantly.

For fintech companies, market makers impact platform liquidity, regulatory exposure, and overall scalability. Missteps in this area can result in operational delays or regulatory scrutiny.

This article breaks down what a market maker is, how they work across different business models and asset classes, what compliance teams need to watch out for, and how current regulations are evolving.

At InnReg, we help fintechs and broker-dealers navigate market structure and market maker-related compliance risk. If your platform relies on liquidity providers or market-making activity, our team can support your regulatory strategy and operational readiness.

What Is a Market Maker?

A market maker is an individual or firm that continuously quotes buy and sell prices for a given asset and stands ready to transact at those prices. Their role is to facilitate liquidity, making it easier for others to enter and exit positions without significant price swings.

They do this by maintaining inventory and accepting the risk of holding that inventory in exchange for profit through the bid-ask spread.

In traditional markets, these firms often operate on exchanges or over-the-counter (OTC) platforms. In crypto, they may operate on centralized exchanges or provide algorithmic liquidity to decentralized protocols.

Core Functions in Financial Markets

Market makers provide quotes on both sides of a trade. They step in when buyers outnumber sellers, or vice versa, and take on inventory risk in the process. That activity supports price discovery, especially when the market is uncertain or lacks depth.

By narrowing price gaps and absorbing order flow, they help keep trading orderly. This applies across public exchanges and newer fintech platforms offering less traditional products.

Types of Market Makers

Market makers can be categorized by the business models and regulatory roles they operate under. Some act on behalf of clients, others take risks directly onto their own balance sheet. Some are registered with regulators; others operate in decentralized environments with no formal designation.

Market Maker Type | Description |

|---|---|

Dealer | Use proprietary capital to quote and fill trades; registered broker-dealers in traditional markets. |

Wholesale | Internalize retail order flow from brokers; focus on execution quality and spread capture. |

Exchange-Designated | Operate under exchange agreements with quoting obligations; receive incentives. |

Electronic and Algorithmic | Rely on algorithms to quote across venues; active in FX, crypto, and derivatives. |

Agency | Match trades without holding inventory; common in OTC and peer-to-peer platforms. |

Liquidity Providers | Quote assets without formal obligations; common in crypto, may still face regulatory scrutiny. |

Automated Market Makers (AMMs) | Use smart contracts to set prices and pool liquidity; found in decentralized finance. |

Hybrid Market Makers | Combine principal, agency, and protocol-based models; flexible but complex to manage. |

Dealer Market Makers (Principal Trading Firms)

Dealer market makers take positions using their own capital. They quote both buy and sell prices and fill trades directly from their inventory. Their revenue typically comes from capturing the spread between those two sides.

In equity markets, this role is usually held by broker-dealers registered with the SEC and FINRA. In crypto, the same approach is used by trading firms that provide liquidity on centralized exchanges. Many of them operate across multiple venues and maintain high volumes.

Since these firms take on exposure with every trade, they are subject to closer regulatory oversight and financial risk.

Learn how InnReg helps fintech with broker-dealer registration →

Wholesale Market Makers (Retail Wholesalers)

These firms specialize in internalizing retail order flow, often from commission-free brokers. Instead of sending a trade to an exchange, the broker routes it to a wholesaler who fills it directly.

Well-known names like Citadel Securities and Virtu fall in this category. They provide tight execution, often with price improvement, while profiting from flow volume and spread capture.

For fintech brokers, wholesale market makers may play a behind-the-scenes but critical role in execution quality and cost structure.

Exchange-Designated Market Makers

Certain exchanges work with selected firms to help maintain active trading in specific securities. These firms commit to quoting both sides of the market at agreed sizes and keeping spreads within a defined range during the day.

To compensate, exchanges may offer benefits such as reduced fees or access to specific order flow programs.

This setup is common on platforms like the NYSE, where Designated Market Makers handle assigned stocks. Similar roles exist on Nasdaq and are now being adapted for tokenized assets and digital securities.

Electronic and Algorithmic Market Makers

These firms use proprietary systems and high-speed algorithms to quote across multiple venues, often in milliseconds. They operate in highly competitive environments and rely on low latency, strong technology infrastructure, and complex hedging logic.

Algorithmic market makers dominate in FX, futures, options, and now crypto. They do not rely on manual decision-making. Instead, strategies adapt dynamically based on flow, volatility, and market depth.

For fintechs building multi-venue trading platforms, these firms may be key partners in aggregating liquidity across fragmented markets.

Agency Market Makers (Matched-Principal or Riskless Principal Firms)

Not all market makers take principal risk. In agency models, the firm matches a buyer with a seller and earns a fee, but does not hold inventory. Some may briefly intermediate the trade (“riskless principal”) but without exposure to market movements.

This model is common in OTC FX, bonds, and some digital asset desks. From a regulatory standpoint, agency firms may have different obligations than principal dealers, depending on how trades are routed and executed.

Fintech platforms offering peer-to-peer execution or matching engines may resemble this model more than a traditional dealer.

See also:

Liquidity Providers (Non-Obligated Market Makers)

Not all liquidity providers operate under a formal market maker designation. In crypto, it’s common for firms to post buy and sell orders without any specific quoting requirements or ongoing obligations.

They may function like market makers in practice, but that does not always shield them from regulatory attention, especially when securities are involved. For fintech companies, it is important to evaluate how these partners operate and whether their activity falls under regulatory scope.

Need help with broker-dealer compliance?

Fill out the form below and our experts will get back to you.

Automated Market Makers (AMMs)

In DeFi, AMMs take the place of traditional market makers. Pricing is not set by a trading firm. It is handled by a smart contract, usually using a formula like x*y=k to keep things in balance.

Liquidity comes from users, not institutions. Anyone can add assets to a pool and earn a portion of the trading fees.

This setup powers protocols like Uniswap and Curve. But it also introduces friction, especially for liquidity providers. Risks like impermanent loss and MEV need to be factored in, particularly when fintechs are building DeFi-facing products.

Hybrid Market Makers

A growing number of firms combine elements from different market-making models. One operation might run automated strategies on exchanges, contribute assets to AMM pools, and support liquidity for regulated tokens.

This is now standard practice for many fintechs operating in mixed environments. These firms shift between principal trading, agency execution, and direct protocol interactions depending on the asset and venue.

It’s an efficient way to access liquidity, but it introduces layers of risk and compliance that need active management.

How Market Makers Work

Fintech companies dealing with execution and liquidity need a working grasp of how market makers really operate. Models vary, but the basic job doesn’t change: post prices, take trades, and manage risk around the spread.

Function | Purpose | Who Performs It |

|---|---|---|

Posting bid and ask quotes | Keeps the market two-sided and tradeable | Principal dealers, electronic firms |

Holding inventory | Allows instant execution for counterparties | Principal market makers |

Managing spread risk | Captures revenue while adjusting to volatility | All market makers |

Adapting to flow conditions | Reacts to buying/selling pressure in real time | Electronic and algorithmic firms |

Supporting price discovery | Helps anchor prices during low-volume or volatile periods | Designated and high-volume participants |

Liquidity Provision and Bid-Ask Spreads

At the heart of market making is the bid-ask spread. The difference between the price a firm is willing to buy at (bid) and the price it will sell at (ask). That spread compensates the firm for risk, capital use, and operational overhead.

Wider spreads typically reflect lower liquidity or higher volatility. Narrow spreads suggest competitive conditions with active participation from multiple firms.

For fintech platforms, especially those offering less liquid or novel products, understanding how spreads behave is key. The spread directly affects user execution quality and perceived platform fairness.

Inventory Risk and Profit Models

Every trade is a risk decision. Market makers buy and sell constantly, but timing does not always line up. They might sell first and scramble to cover. Or buy, only to see the price drift the wrong way.

They try to stay ahead with smart tools and quick adjustments. Sometimes it works. Sometimes it doesn’t. That’s why limits, alerts, and human eyes are always part of the process.

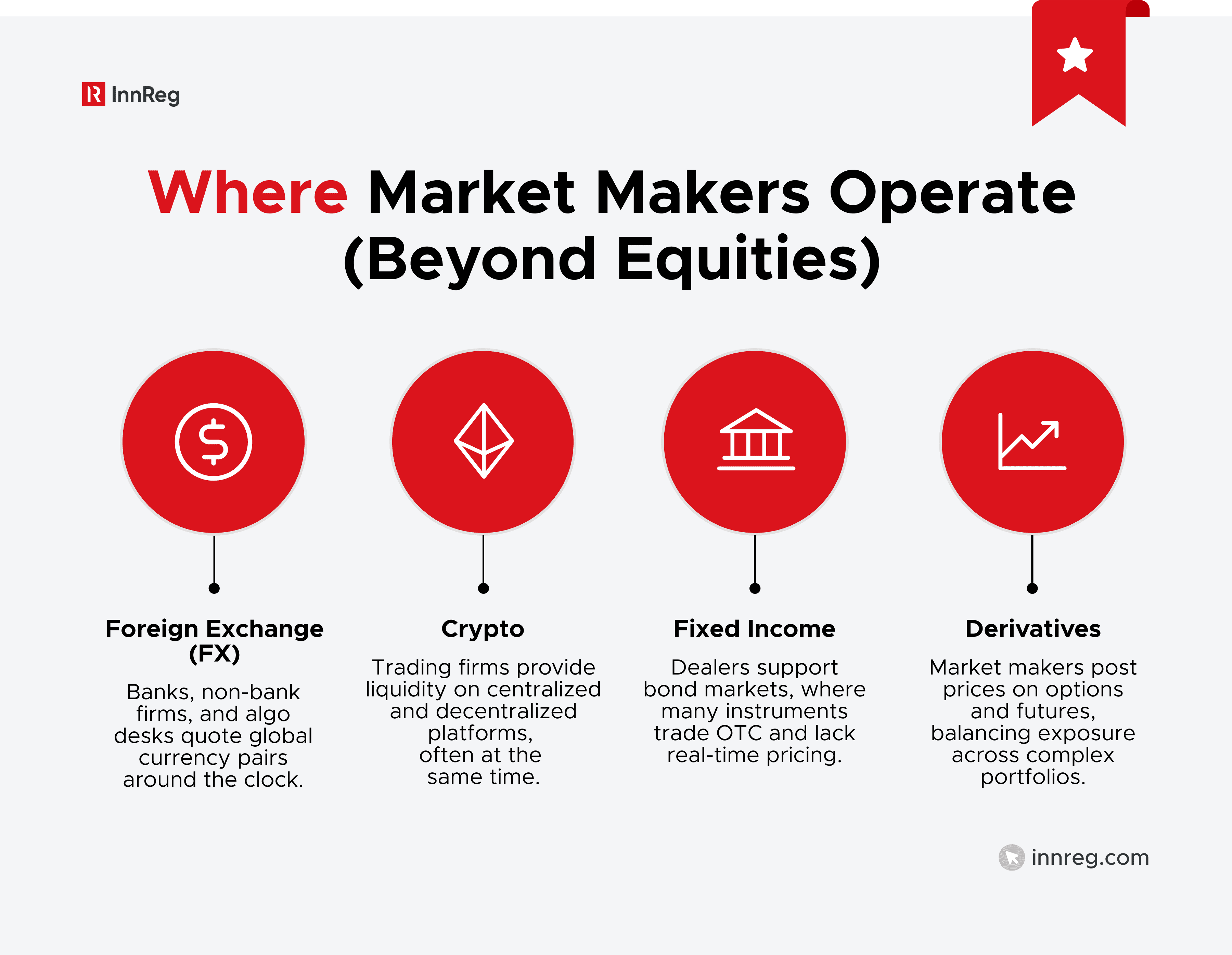

Examples Across Asset Classes

Market making is not confined to public equities. It shows up across financial markets. each with its own trading rhythms, risk models, and regulatory layers.

For fintech platforms that cross asset classes, it is not enough to understand how market-making works in one vertical. The underlying mechanics shift depending on what’s being traded.

That matters early in the product lifecycle. Whether you are supporting tokenized assets or building rails for FX or derivatives, liquidity and execution models must match the asset’s structure.

See also:

Market Makers in Fintech and Crypto

Trading platforms need liquidity to work. In fintech and crypto, that often means working with market makers. These roles look different depending on the product. Some are centralized. Some are decentralized. Some sit in between.

Centralized Crypto Market Makers

In centralized crypto markets, market makers quote prices and manage risk across multiple trading venues. Many of them use high-speed algorithms and cross-exchange inventory strategies to stay competitive.

Some are hired directly by token issuers or exchanges to support new listings. Others operate independently and profit from spreads and volume-based incentives. In either case, they are essential to narrowing spreads and absorbing volatility, especially during the early stages of a token’s trading life.

Unlike in equities, crypto market makers are not always bound by formal designation or quoting obligations. Still, their trading activity may fall under dealer regulations if the assets are later deemed securities.

Automated Market Makers (AMMs) in DeFi

AMMs introduced a different approach. Instead of quoting prices manually or through algorithms, a smart contract sets prices based on a fixed formula. Traders interact directly with the pool, and liquidity comes from users rather than professional desks.

Uniswap, Curve, and Balancer are well-known examples. While the model creates open access to trading, it also introduces risks like impermanent loss and front-running.

For fintech companies integrating with DeFi protocols, understanding how these mechanics work is critical, not just for execution, but for compliance and risk disclosures as well.

Role of Market Makers in Token Launches and Novel Trading Models

Market makers often play a behind-the-scenes role during token launches or the rollout of alternative trading platforms. They help by quoting prices and stepping in when natural volume is low.

But regulators look closely at these relationships, especially when the asset has characteristics of a security. Payments, quote requirements, or side agreements can all come under scrutiny if they resemble price maintenance.

Founders should approach these arrangements with care. A solid market maker can be an asset, but only if the legal structure supports the role cleanly and transparently.

Learn how InnReg helps innovative fintechs develop a regulatory strategy →

Regulatory Landscape for Market Makers in the US

Regulatory oversight depends on what a market maker does and what it trades. In the US, much of that hinges on whether the firm is considered a dealer.

Broker-Dealer Registration and FINRA Oversight

Most market makers in the securities space operate as registered broker-dealers. Once registered, they take on obligations like internal controls, regular filings, and FINRA supervision.

The requirement generally applies when a firm engages in the business of buying and selling securities for its own account as part of a regular business. Simply quoting both sides of a trade, especially with high-frequency or customer-facing intent, can trigger the dealer threshold.

Learn how InnReg supports broker-dealer registration →

SEC's Definition of a “Dealer” and Market Maker Obligations

The SEC has recently updated its interpretation of what constitutes a “dealer,” with a focus on firms that play a regular role in providing liquidity, even if not formally labeled as market makers.

The key factor is function: if a firm routinely stands ready to trade in a manner that impacts liquidity or price formation, it may fall under dealer rules. This applies whether the firm trades equities, debt, or digital assets that meet the definition of a security.

New rules emphasize “liquidity providing behavior,” which captures a broad range of activity, including algorithmic trading and high-frequency quoting.

This shift means that more crypto and fintech firms may be treated as dealers, even if they have not registered as such. The risk is not theoretical: enforcement actions have already targeted unregistered participants engaging in market-making activity.

See also:

CFTC and Other Regulatory Touchpoints

Not every market maker deals in securities. Some quote prices in commodities, crypto products, or FX, areas that fall under CFTC rules instead of the SEC.

Firms that touch multiple asset types may need both licenses. It is not uncommon to see dual registration for those trading in both derivatives and securities.

And that’s just the federal level. States have their own money transmitter laws. Major exchanges set their own conduct standards. If a fintech firm is working across asset classes or mixing centralized and DeFi systems, it needs to account for all of it.

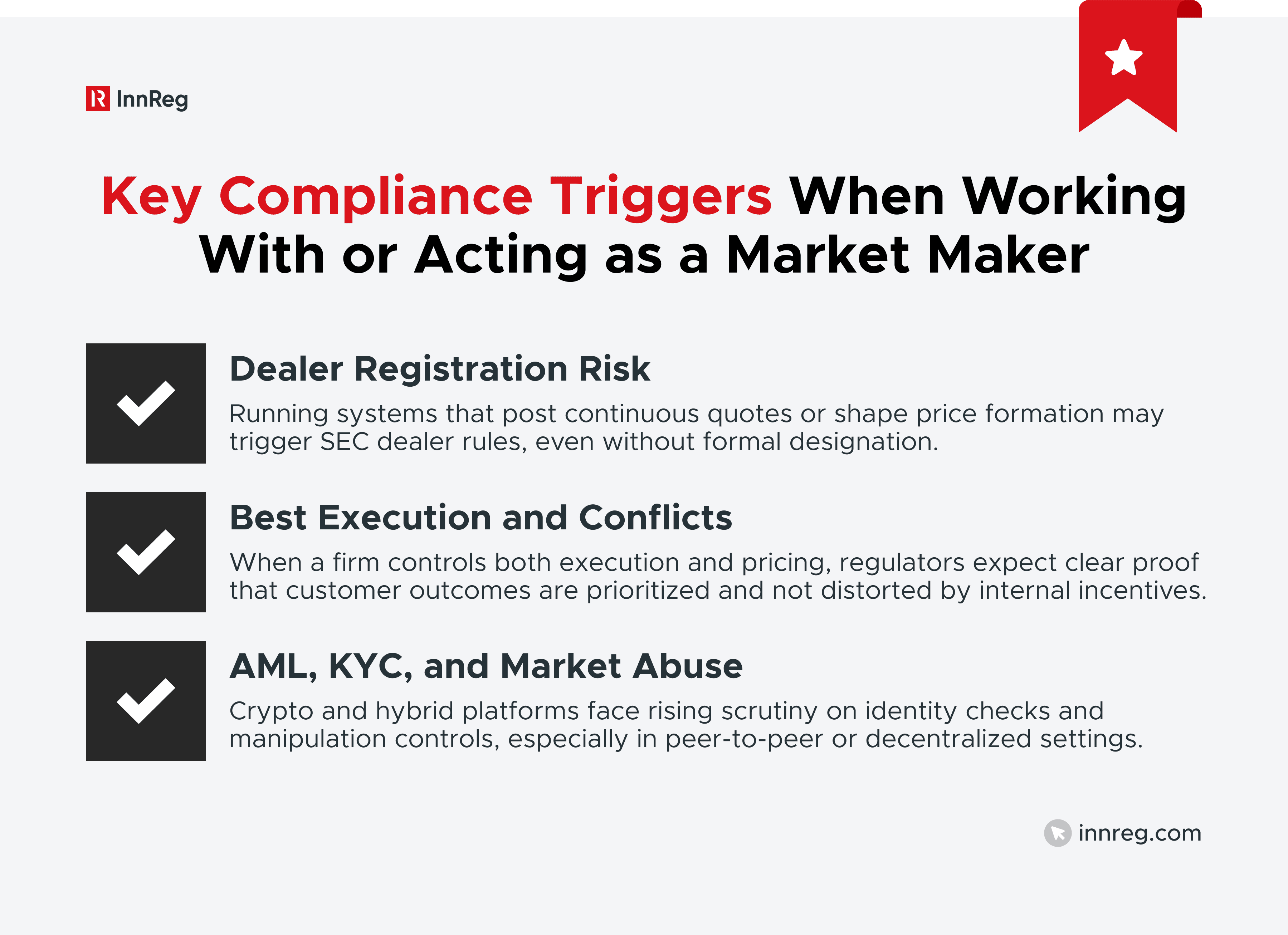

Compliance Challenges for Fintechs Working With or Acting as Market Makers

Market-making activity often overlaps with regulated functions. Whether a fintech is building internally or relying on outside firms, understanding the compliance risks is essential.

Licensing Triggers and Unregistered Dealer Risk

When fintechs run systems that post quotes around the clock or manage flow in a way that moves the market, they may be taking on dealer responsibilities, whether they know it or not.

The SEC has made clear that functional behavior matters more than labels. If a fintech platform facilitates or engages in market-making activity without proper registration, it may face enforcement action, especially if the underlying asset is a security.

This applies not just to in-house activity but also to relationships with third-party liquidity providers. If those partners act as de facto dealers, the regulatory exposure may extend to the platform itself.

Best Execution, Conflicts of Interest, and Fair Dealing

When a firm falls within the regulatory scope, a new set of requirements applies. Among the most important are best execution and fair dealing. Market makers that are connected to trading venues or broker-dealers must show that trades are handled in a way that prioritizes the customer’s outcome.

Conflicts often emerge when execution and pricing are handled within the same structure. Internal routing, pricing discretion, and incentive arrangements all carry potential regulatory weight.

AML/KYC Considerations and Market Abuse Risks

Market makers in crypto and hybrid asset spaces face additional scrutiny on anti-money laundering (AML) and know-your-customer (KYC) protocols. This is particularly true in peer-to-peer or decentralized environments where identifying counterparties can be difficult.

At the same time, firms must guard against manipulation. Spoofing, wash trading, and layering are not unique to crypto, but decentralized systems may lack the built-in surveillance tools used by traditional markets. Platforms that work with market makers, or build their own liquidity engines, need to incorporate surveillance, alerting, and post-trade review into their workflows.

Developed based on InnReg’s experience of working with 100+ fintechs, Regly’s FinCrime platform helps fintechs with their AML and KYC/KYB obligations →

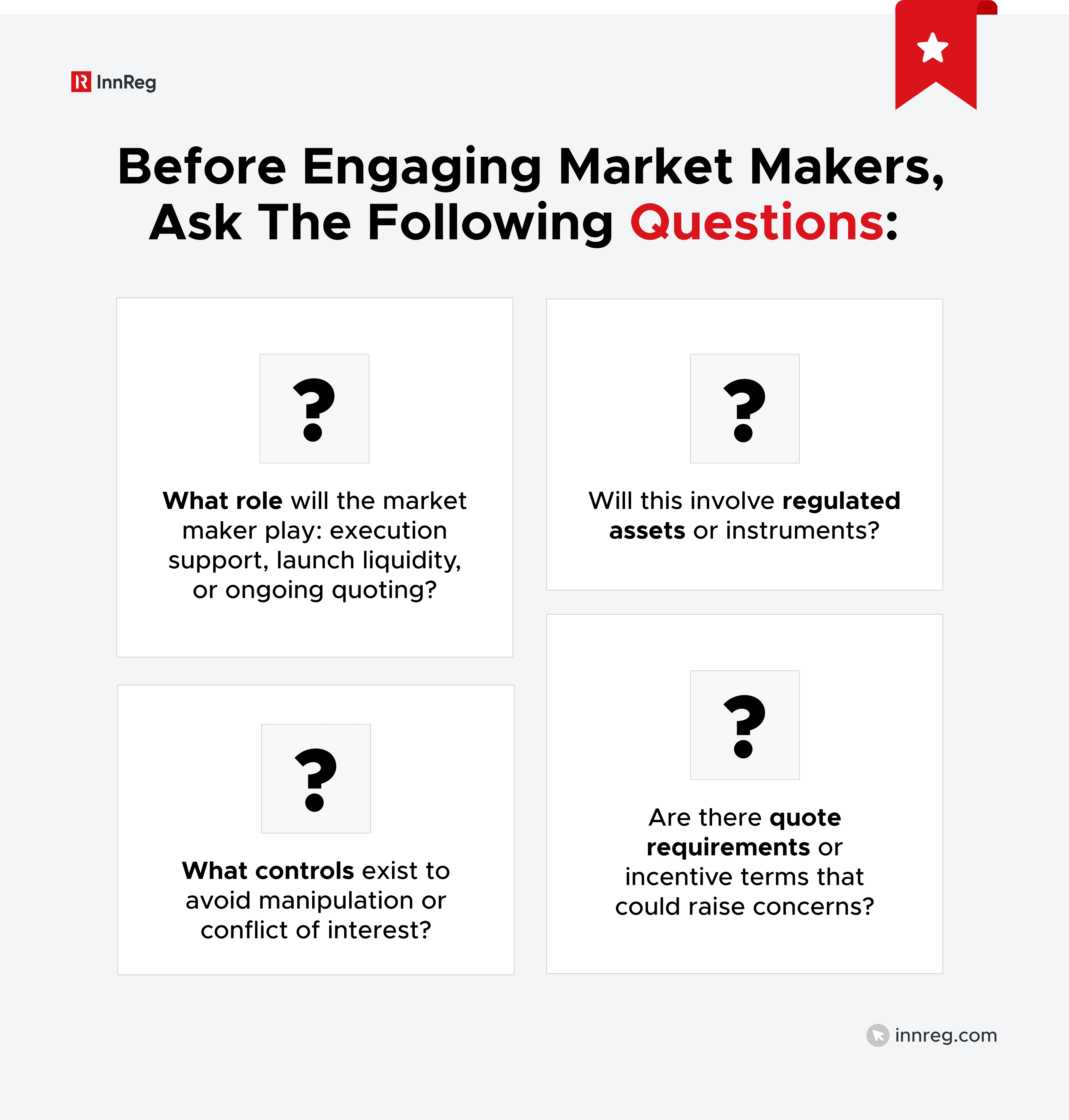

Best Practices for Fintechs Engaging Market Makers

Engaging market makers, internally or through partners, requires alignment, documentation, and active oversight. The best practices to engage with market makers include:

Asking the Right Questions

Before launching a relationship, leadership should align on purpose and boundaries.

Answering these questions early helps shape legal agreements, surveillance systems, and communication protocols.

Structuring Relationships Without Violating Rule 5250

Rule 5250 primarily requires disclosure of certain agreements involving listed companies, including some arrangements with market makers.

While the rule does not prohibit paying market makers for quoting activity, exchanges and regulators closely scrutinize arrangements that resemble undisclosed market-support or price-maintenance agreements.

Anything that looks like a perk or incentive tied to liquidity support may come under scrutiny.

Under this rule, fintechs should draw a firm line between listing terms and market-making arrangements, and put everything in writing.

That structure keeps the platform in a stronger position if questions come up later.

Internal Controls, Documentation, and Legal Review

When market-making is outsourced, the platform still carries much of the oversight burden. It is essential to assign clear responsibilities across legal, compliance, and operations, and to maintain regular visibility into quote behavior, spread patterns, and concentration of flow.

Consistent reporting from partners and documented surveillance protocols help mitigate risk and provide a more complete picture of how the market behaves under different conditions.

—

Market making adds value, but also complexity. Whether fintechs engage directly or through partners, these functions shape liquidity, pricing, and compliance exposure.

The right setup starts with understanding how market makers operate, where regulatory lines are drawn, and what controls must be in place. It is not just a trading function.

It is a strategic decision with legal and operational consequences.

Maria is a Compliance Consultant at InnReg delivering compliance solutions for fintech clients across broker-dealer, RIA, and money transmitter verticals. She brings prior experience at Finalis, Fenix Securities and PwC, with expertise in AML, CCO support, investment banking operations and securities compliance. She holds FINRA Series 14, 24, and 82 licenses and actively supports regulatory and compliance processes revolving broker-dealer activities.

How Can InnReg Help?

InnReg is a global regulatory compliance and operations consulting team serving financial services companies since 2013.

We are especially effective at launching and scaling fintechs with innovative compliance strategies and delivering cost-effective managed services, assisted by proprietary regtech solutions.

If you need help with broker-dealer compliance, reach out to our regulatory experts today:

Related Articles

Featured LinkedIn Posts