Compliance vs. Supervision in Financial Services

Key Takeaways

Within financial institutions, compliance and supervision perform separate functions. Compliance teams handle policy development and monitoring, while supervisors oversee staff and operational activity.

Supervisory responsibility typically sits with business management. Regulators generally hold managers and designated supervisors accountable for overseeing operational activity and preventing misconduct.

Compliance programs support supervision but do not replace it. Regulators expect firms to maintain active supervisory oversight rather than relying solely on compliance monitoring.

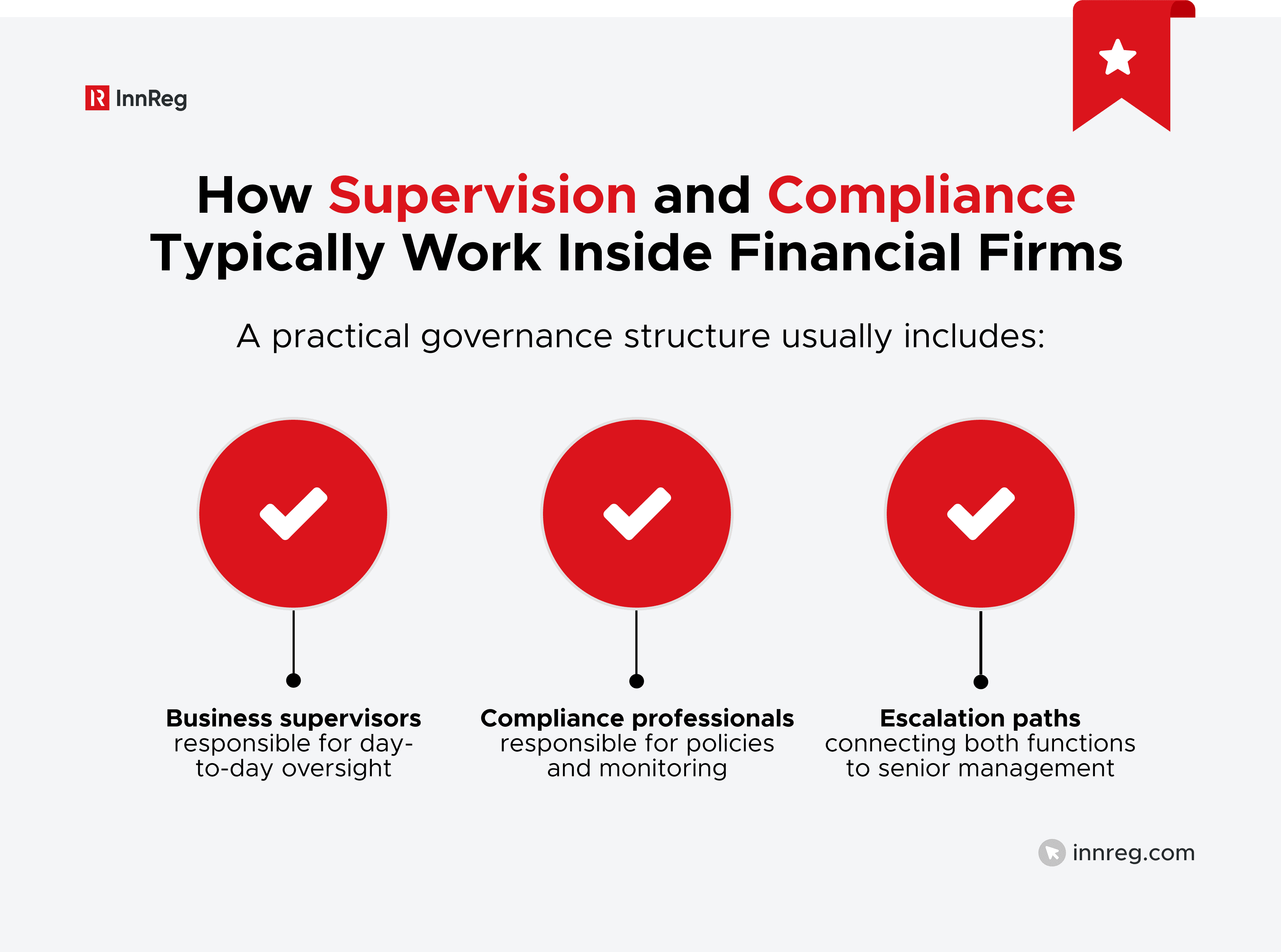

Clear governance structures help avoid regulatory confusion. Firms should document reporting lines, supervisory responsibilities, and escalation processes in policies, procedures, and organizational charts.

Written procedures must reflect how the firm actually operates. Regulators often compare documented policies with day-to-day workflows during examinations.

Supervisory systems must be actively tested. Internal reviews, compliance testing, and supervisory control checks help demonstrate that oversight frameworks are functioning.

In financial services, the terms compliance and supervision are often used together, sometimes interchangeably. But regulators treat them as distinct responsibilities with different implications for governance, accountability, and liability.

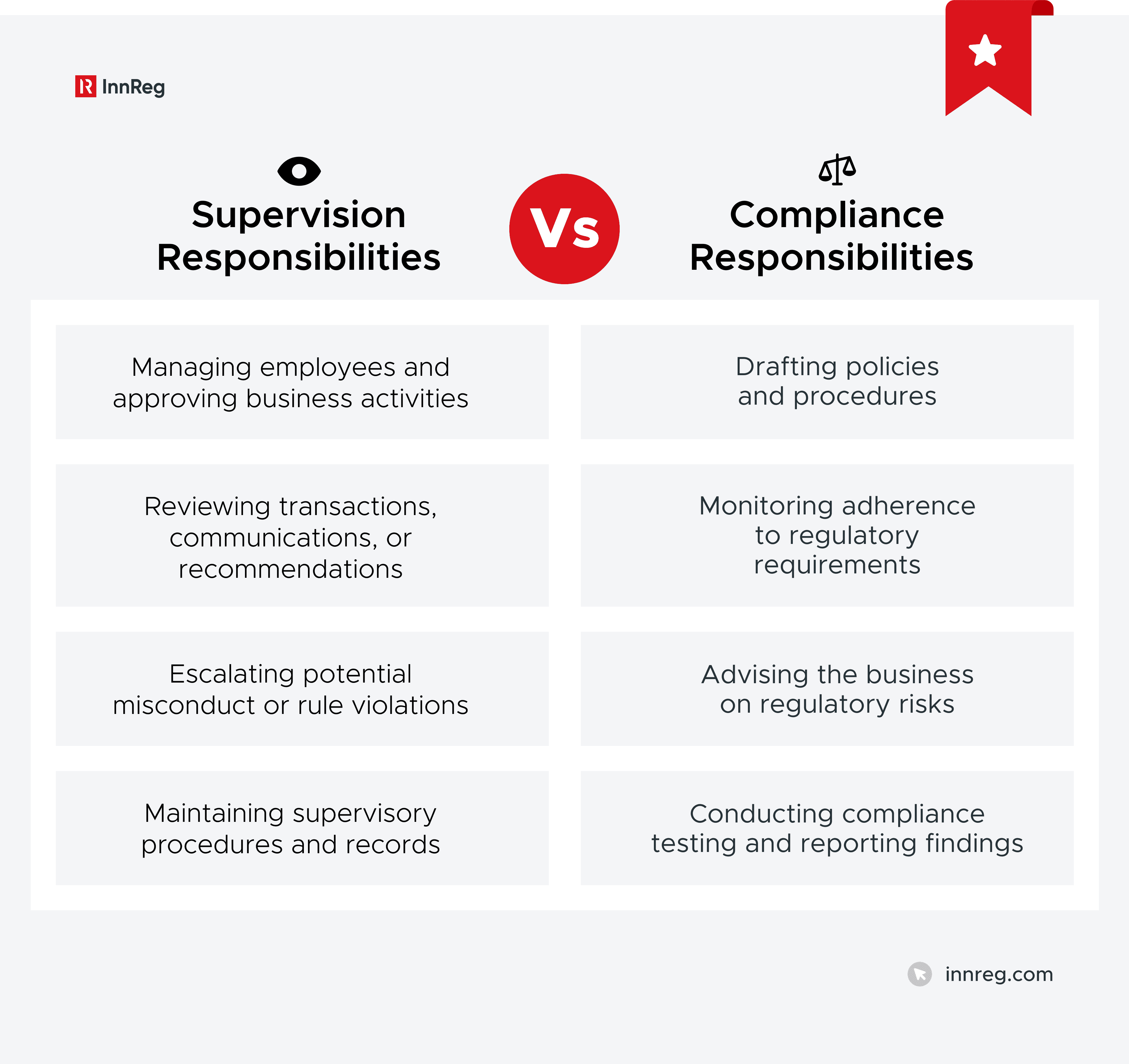

For fintech companies entering regulated markets, understanding the difference is important. Supervisors are responsible for overseeing business activities and employees, while compliance functions typically focus on designing policies, monitoring adherence, and advising the business on regulatory obligations.

This article explains how regulators define compliance and supervision, how the two functions interact, and why the distinction matters when structuring oversight in financial institutions.

At InnReg, we help fintech companies and financial institutions build and operate practical compliance programs. Our team supports licensing, regulatory strategy, policy development, and day-to-day compliance operations.

Compliance vs. Supervision: What’s the Difference?

Supervision refers to the responsibility of management to oversee business activities and employees.

On the other hand, compliance refers to the function that designs and monitors systems intended to meet regulatory requirements.

This distinction matters across nearly every regulated financial sector. Broker-dealers, investment advisors, payment companies, and derivatives firms all operate under frameworks where management must supervise the business, and compliance teams support that oversight through policies, monitoring, and guidance.

Regulators consistently emphasize that compliance programs cannot replace active supervision by business leadership. Firms are expected to maintain governance structures where supervisors manage risk within their business lines, and compliance officers provide expertise, monitoring, and escalation when issues arise.

In practice, this creates a partnership between two core functions. Supervisors control how the business operates day to day. Compliance teams help design the systems that allow those supervisors to meet regulatory obligations and identify risks before they become enforcement issues.

Understanding the difference between compliance and supervision is especially important for fintech companies entering regulated markets. New products, complex partnerships, and rapid growth can blur governance roles.

Regulators, however, expect firms to clearly define responsibilities, maintain effective oversight, and demonstrate that both compliance and supervision functions are working together to manage regulatory risk.

Internal Supervision vs. Regulatory Supervision

The word supervision appears frequently in financial regulation, but it can refer to two different types of oversight. Understanding the difference helps clarify how regulators evaluate governance inside financial institutions.

Internal supervision refers to oversight performed within the firm by managers and designated supervisors. These individuals monitor employees, review business activities, and address potential misconduct. In many regulated firms, supervisors include registered principals, department heads, or senior executives responsible for specific business units.

Regulatory supervision refers to oversight conducted by regulators themselves. Financial regulators use examinations, inspections, and enforcement actions to assess whether firms are operating within applicable rules.

While internal supervision focuses on monitoring the firm's operations, regulatory supervision evaluates whether the firm's oversight systems are functioning as intended.

Why the Distinction Matters in Practice

The difference between internal and regulatory supervision affects how firms organize oversight and responsibility. Regulators expect firms to run their own supervisory systems rather than rely on regulatory exams to detect problems.

Examinations are designed to evaluate a firm’s controls, not replace them. During an exam, regulators typically look at whether supervisory procedures exist, whether managers are actively reviewing activity, and whether issues are escalated when they appear.

For that reason, financial regulations across multiple sectors require firms to maintain formal supervisory systems. These systems are intended to monitor employee conduct and identify potential violations before regulators become involved.

Regulators typically hold management accountable when internal supervision fails, not simply when a compliance program contains weaknesses. Enforcement actions often focus on whether supervisors had the authority and responsibility to prevent or detect misconduct.

For fintech companies and other rapidly growing firms, the distinction can become blurred. Startups often build strong compliance functions early, but supervisory responsibilities may not be clearly defined across product teams or business units.

When these roles are clearly defined, firms can demonstrate to regulators that supervision and compliance operate together rather than as competing responsibilities.

Compliance vs. Supervision: A Comparison

The difference between compliance and supervision becomes clearer when looking at how each function operates inside a financial institution.

Both roles support regulatory adherence, but they focus on different responsibilities within the organization:

Category | Compliance | Supervision |

|---|---|---|

Primary purpose | Develop and monitor systems designed to meet regulatory requirements | Oversee employees and business activities |

Organizational role | Control and advisory function | Operational management function |

Authority over employees | Usually indirect; advises and monitors | Direct authority to manage, approve, or escalate activity |

Core responsibilities | Policies and procedures, regulatory guidance, compliance monitoring, training | Transaction reviews, employee oversight, approvals, and escalation of misconduct |

Accountability | Responsible for maintaining the compliance program | Responsible for supervising conduct and business operations |

Regulatory focus | Whether policies, monitoring, and reporting processes are effective | Whether supervisors actively oversee employees and prevent violations |

Typical reporting line | Often reports to senior management or the board | Typically embedded within business units or management structures |

In practice, compliance and supervision function as complementary parts of the same governance framework. Supervisors manage day-to-day activities within the business, while compliance teams provide the structure, monitoring, and regulatory expertise that support those supervisory efforts.

Compliance vs. Supervision in Broker-Dealers (FINRA Framework)

The distinction between compliance and supervision becomes especially clear in the broker-dealer regulatory framework. FINRA rules place significant emphasis on supervision as a core responsibility of business leadership. Compliance programs support that structure, but they do not replace the supervisory duties assigned to management.

Broker-dealers must maintain supervisory systems that oversee employee activity and business conduct. FINRA rules require firms to assign supervisory responsibilities to registered principals and business leadership. Compliance teams support those efforts by developing procedures and monitoring adherence to regulatory requirements.

The following sections examine how this structure works in practice. They review the key FINRA rules governing supervision, explain where compliance fits within the supervisory framework, and clarify how regulators view the role of the chief compliance officer in broker-dealer oversight.

Rule 3110: The Supervisory System Requirement

FINRA Rule 3110 is the foundation of the broker-dealer supervisory framework. The rule requires firms to establish and maintain supervisory systems designed to oversee the activities of associated persons and monitor compliance with securities laws and FINRA rules.

Rule 3110 places responsibility for supervision on the firm’s business management and designated principals, not the compliance department. Firms must assign qualified supervisors who have the authority to oversee employees, review business activity, and address potential misconduct.

These responsibilities are typically carried out by registered principals, such as Series 24 supervisors or other appropriately licensed personnel.

Rule 3110 also requires firms to maintain Written Supervisory Procedures (WSPs) that describe how supervisory responsibilities are carried out. These procedures must identify who supervises each business activity and how oversight is performed.

Compliance teams often assist with drafting and maintaining these procedures, but the supervisory authority itself remains with the designated principals responsible for overseeing the business.

Learn more about FINRA Rule 3110 →

Rules 3120 and 3130: Testing, Controls, and CEO Certification

FINRA Rules 3120 and 3130 build on the supervisory structure established under Rule 3110. While Rule 3110 focuses on supervisory systems, these rules address how firms test and validate those systems over time.

Rule 3120 requires broker-dealers to establish supervisory control systems designed to test the effectiveness of their supervisory procedures. In practice, this means firms must periodically review whether their supervisory processes are functioning as intended. The goal is not simply to maintain procedures on paper, but to evaluate how they operate in daily business activity.

Supervisory control testing often involves reviewing areas such as:

Supervisory approvals of transactions or recommendations

Monitoring of employee communications

Branch office supervision and oversight

Escalation and documentation of compliance issues

These reviews are typically conducted by personnel independent from the supervisors being tested. The process helps firms identify gaps in oversight and adjust supervisory procedures when necessary.

Rule 3130 adds another layer of accountability. The rule requires the firm’s chief executive officer to certify annually that the firm has processes in place to establish, maintain, and review supervisory procedures. This certification connects senior leadership directly to the firm’s supervisory framework.

The CEO certification does not mean the executive personally supervises day-to-day activity. Instead, it requires management to confirm that the firm maintains structured processes to evaluate supervisory systems and address weaknesses when they appear.

Together, Rules 3120 and 3130 reinforce an important principle within the compliance vs. supervision framework. Supervisory systems must be actively maintained and tested, and senior management remains accountable for the overall structure of those systems.

Where Compliance Fits Inside the Supervisory Structure

Supervision and compliance are both part of broker-dealer regulatory structures but they have different roles. Supervisors oversee all business activities in a firm as well as the behavior of employees. Compliance is responsible for developing systems that assist with the firm's compliance with rules and regulations.

FINRA has made it clear that supervision must rest with managerial personnel (brokers) and designated principals, not within the compliance department. Supervisors review transactions; oversee the daily activity of employees; and take action when violations of rules may occur on an ongoing basis as part of their day-to-day responsibilities.

Compliance functions typically work alongside supervisors by developing procedures for transaction processing and other businesses, interpreting rules and regulations, monitoring how those procedures are followed, identifying potential risks, and communicating these findings to supervisors, senior management, etc.

As such, the role of compliance is that of a control and advisory function, while the role of supervision remains operational. This distinction is key to understanding financial regulation's compliance vs. supervision framework. Firms must maintain both functions. Supervisors must actually manage the firm's business, and compliance must provide support to the firm's oversight structure.

What FINRA Expects in Written Supervisory Procedures

Broker-dealers must have written supervisory procedures (WSPs), which include the supervisory responsibilities throughout the entire organization. FINRA expects firms to maintain clear, documented procedures that describe how supervisory responsibilities are carried out across the organization.

The procedures generally address which supervisor is responsible for overseeing various aspects of the firm, how reviews are conducted on those aspects, and what process will be followed if problems are identified during these reviews.

Regulators often focus on whether WSPs reflect how the firm actually operates. Procedures that exist only as formal documentation but are not followed in practice are a common issue identified during regulatory examinations. Supervisors should be able to demonstrate that the procedures described in the WSPs align with their day-to-day oversight responsibilities.

Compliance teams frequently assist with drafting and updating these procedures. However, supervisory responsibility still rests with the principals and managers assigned to oversee specific business activities.

For fintech broker-dealers and other fast-growing firms, supervisory procedures rarely stay static. Product launches, workflow changes, and new technology can quickly outdate existing procedures. WSPs need to be updated as the business evolves, so supervisory responsibilities remain clear.

Learn more about Written Supervisory Procedures (WSPs) →

See also:

Compliance vs. Supervision and the CCO Role

The distinction between compliance and supervision becomes particularly important when discussing the role of the Chief Compliance Officer (CCO). In many firms, especially startups and smaller organizations, the boundaries between these functions can become unclear.

Regulators typically treat the CCO as the person responsible for running the firm’s compliance program, not supervising the business itself. Holding the compliance title alone does not make someone a supervisor. Supervisory authority usually sits with registered principals and business managers who oversee employees and operational activity.

InnReg helps fintech by providing outsourced CCO services →

This distinction matters because supervisory liability usually applies to people who have authority over business activity. Those individuals can direct employees or influence how operations are carried out. Compliance officers typically operate in a control role, monitoring adherence to rules, providing regulatory guidance, and raising issues when they identify risks.

In practice, however, roles can overlap. Smaller firms or early-stage fintech companies may rely heavily on the CCO to manage multiple oversight functions. When that happens, regulators look closely at how responsibilities are defined and whether the CCO has been given supervisory authority over business operations.

Clear role definitions draw a clean line between what compliance handles and what supervisors own.

Most firms spell this out in their written procedures. They define who is responsible for supervising day-to-day business activity, who runs the compliance program, and how issues get escalated when something needs senior management’s attention.

FINRA Regulatory Notice 22-10 Explained

FINRA addresses the relationship between compliance and supervision in Regulatory Notice 22-10, clarifying how it views the role of chief compliance officers and other compliance personnel.

The notice explains that compliance officers generally operate in an advisory and monitoring role rather than a supervisory one. Their responsibility is to administer the compliance program, identify regulatory risks, and escalate concerns to supervisors and senior management.

FINRA also notes that enforcement actions against CCOs should be relatively uncommon. Regulatory liability typically focuses on supervisors and managers with authority over business activity and employee conduct.

At the same time, the notice emphasizes that compliance officers may face liability if they are assigned supervisory responsibilities or assume supervisory authority in practice.

SEC Guidance on Supervisory Liability

The SEC also clarifies supervisory liability within financial firms. Liability generally applies to individuals with authority to influence or control business activity. In practice, this usually includes managers, executives, and designated supervisors responsible for overseeing employees.

The SEC also states that compliance and legal personnel are not automatically supervisors simply because they administer compliance programs or provide regulatory advice. However, if a compliance professional has authority over business conduct or employee activity, they may be treated as a supervisor for regulatory purposes.

When a CCO Can Become a Supervisor in Practice

Compliance personnel are usually not treated as supervisors. However, that assessment can shift based on how the firm structures those responsibilities. Regulators look closely at who has authority over business operations or employee activity, rather than relying only on job titles.

A compliance officer may be treated as a supervisor when they exercise authority over the business rather than simply monitoring it. This can happen when the CCO is responsible for approving transactions, managing front-line personnel, or directly overseeing specific business functions.

Because of this, firms typically document governance structures carefully. Written procedures and organizational charts often describe who supervises business activity, who administers the compliance program, and how issues move from compliance monitoring.

Learn how InnReg helps fintechs by providing outsourced CCO services →

Need help with fintech compliance?

Fill out the form below and our experts will get back to you.

Compliance vs. Supervision for Investment Advisors (RIAs)

The distinction between compliance and supervision also appears in the regulatory framework governing investment advisors. Although RIAs are not subject to FINRA supervision rules, the SEC still expects firms to maintain clear oversight structures that separate compliance program administration from business supervision.

The following sections explain how this structure works under the Investment Advisers Act and how regulators evaluate compliance and supervisory responsibilities within advisory firms:

Rule 206(4)-7: The Compliance Program Rule

Rule 206(4)-7 under the Investment Advisers Act requires RIAs to put written compliance policies and procedures in place that actually fit how the firm operates. That means the policies should be tailored to the firm’s business model, the services it provides, and how it runs day to day.

The rule also requires firms to name a chief compliance officer to run the program. The CCO is responsible for building, maintaining, and monitoring the firm’s compliance framework.

That said, compliance isn’t something leadership can hand off and forget about. Firm management is still responsible for supervising advisory activities and employee conduct. A strong compliance program helps by surfacing risks, tracking whether policies are being followed, and raising issues when something needs attention.

RIAs must also review their compliance policies and procedures at least annually. This review typically evaluates whether existing controls reflect how the firm operates and whether any regulatory, operational, or product changes require updates to the compliance framework.

Learn more about Rule 206(4)-7→

Supervised Persons and Internal Oversight

The Investment Advisers Act refers to employees and other individuals working under an advisor as “supervised persons.” This group typically includes officers, employees, and anyone involved in providing advisory services under the firm’s direction.

Advisory firms remain responsible for overseeing the conduct of these individuals. Supervisory responsibility usually sits with firm leadership or designated managers who oversee advisory activity and client interactions.

Compliance personnel support oversight by monitoring adherence to policies and identifying potential risks. Supervisors, however, remain responsible for managing the conduct of advisory staff and addressing issues when they arise.

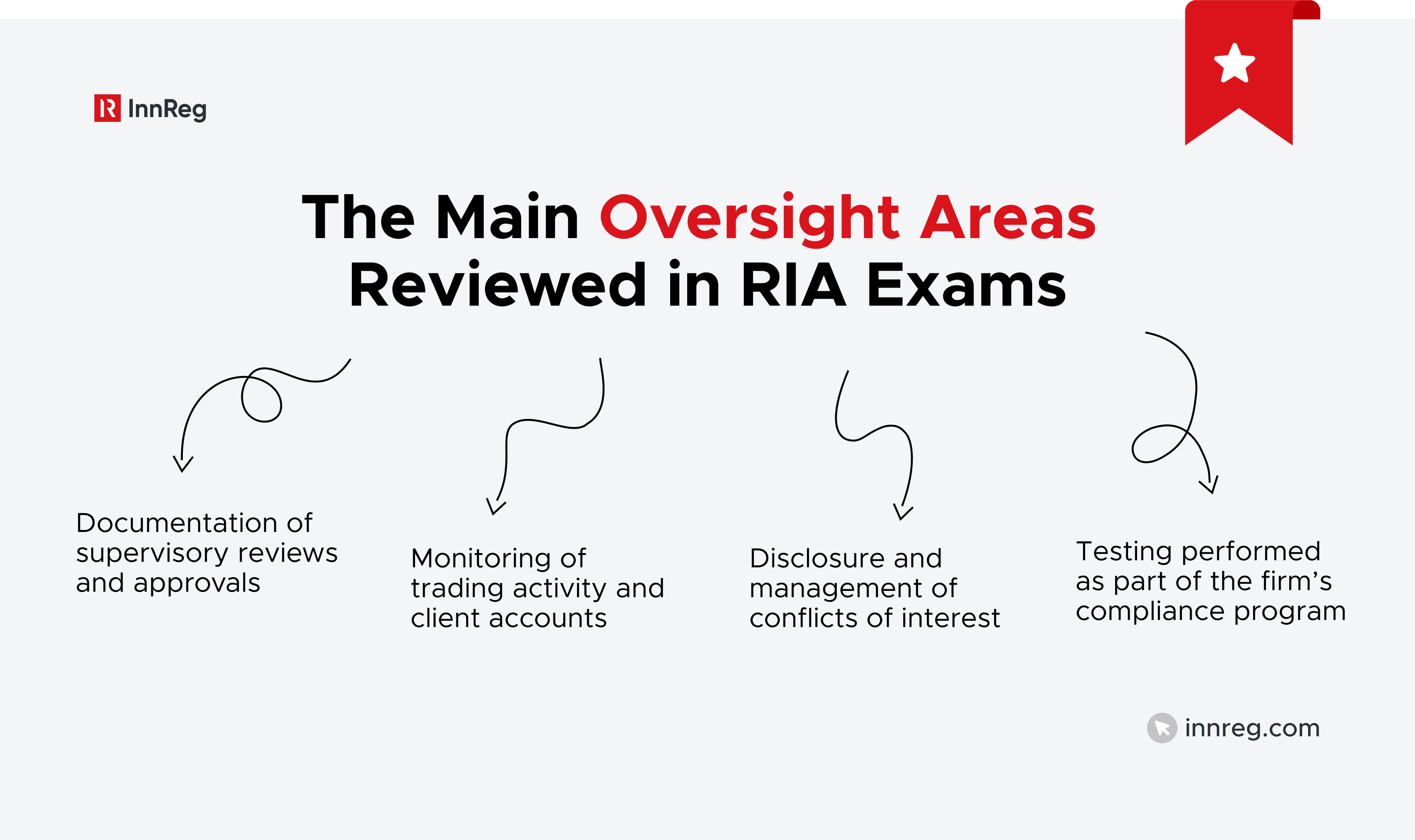

What the SEC Exam Staff Focuses On

When SEC examiners come in, they're not just reading your policies. They're testing whether those policies reflect how your firm actually operates, and the gap between the two is often where findings happen.

In many cases, exam evaluators will look at how advisory firms supervise client interactions, investment recommendations, and portfolio management decisions. Management is expected to oversee advisory activity, while the compliance program monitors adherence to regulatory requirements.

These reviews help regulators determine whether compliance monitoring and supervisory oversight operate together as part of the firm’s governance framework.

Learn how InnReg helps RIAs navigate regulatory requirements →

Compliance vs. Supervision in Payments and Money Transmission

The compliance vs. supervision distinction also appears in the regulation of payment companies and money transmitters. These businesses are typically subject to both federal and state oversight, which requires structured compliance programs alongside active operational supervision.

Most payment and money transmission businesses must maintain formal compliance programs addressing areas such as anti-money laundering (AML), consumer protection, and transaction monitoring. Compliance functions typically develop policies, monitor regulatory adherence, and report risks to management.

At the same time, management remains responsible for supervising the firm’s operations. Supervisors oversee how products are offered, how transactions are processed, and how employees interact with customers. In practice, compliance programs identify risks while business leadership supervises the activities that create those risks.

The following sections explain how this oversight structure works in areas such as AML programs, state regulatory supervision, and vendor oversight in bank-fintech relationships:

AML Programs and FinCEN Requirements

Money transmitters and other MSBs must maintain anti-money laundering programs under the Bank Secrecy Act (BSA). These programs are designed to detect and report suspicious financial activity and prevent the misuse of financial systems.

Under FinCEN regulations, firms must implement a risk-based AML program that includes internal controls, independent testing, training, and a designated compliance officer. The compliance function typically develops and administers these program elements.

Having an AML program in place does not mean management can step back. Leaders are still responsible for making sure those controls are applied consistently in day-to-day work, including transaction monitoring, suspicious activity reporting, and employee adherence to AML procedures.

For payment companies and money transmitters, AML is tightly woven into operations. Supervisors oversee how transactions move through the system, while compliance evaluates whether the controls are effective and escalates concerns when something looks off.

Learn more about AML compliance →

State Examinations and Regulatory Supervision

Typically, state examinations focus on "how" a business is running. Therefore, regulators will evaluate both your company's compliance program and how you supervise operations. These types of evaluations are often in the form of transaction monitoring, new account or customer onboarding process, complaint processing, and recordkeeping.

In addition, examiners will generally compare your company's written procedures to how work actually flows through an operation (i.e., AML controls, consumer protection obligations, etc.), and examine how customer monies are managed.

Fintech firms operating in several states may face multiple exams throughout the year. Managing those reviews often requires clear oversight processes and organized documentation across jurisdictions.

Vendor Oversight and Bank-Fintech Relationships

The difference between supervision and compliance also affects other areas of financial regulation, such as vendor oversight, especially regarding bank-fintech partnerships. Fintech companies typically rely upon vendors for technology, payment processing, customer onboarding, and transaction monitoring.

Regulators have expectations that firms oversee their third-party relationships. While delegating a process or function to a vendor may transfer some of the firm’s operational responsibilities, firm management is still responsible for the performance of the delegated services and the associated risk.

This oversight may involve reviewing vendor performance, monitoring service-level agreements, and addressing operational issues when they arise. For fintech companies working with multiple vendors or bank partners, maintaining clear oversight processes can help demonstrate that both compliance monitoring and operational supervision are functioning as expected.

Based on InnReg’s 10+ years of industry experience, Regly’s vendor management helps fintech track, organize, and assess relationships with third parties →

Bank-Fintech Partnerships: When Supervision Means Prudential Oversight

Bank-fintech partnerships add another dimension to the compliance vs. supervision discussion. In these arrangements, a fintech may design the product or user experience, while the bank provides the regulated financial infrastructure.

From the regulator’s perspective, the bank remains the supervised institution. Bank regulators hold the bank responsible for activities conducted through the partnership, even when the fintech manages much of the technology or customer interface.

Because of this structure, banks typically maintain close oversight of their fintech partners. Reviews often cover onboarding practices, transaction monitoring, consumer disclosures, and operational controls tied to the partnership.

How to Structure Compliance and Supervision in a Fintech Organization

For fintech companies, the compliance vs. supervision distinction eventually becomes a governance question. Firms must decide who manages the compliance program, who supervises business activity, and how oversight responsibilities are documented.

Role Clarity and Reporting Lines

Clear reporting lines are one of the first steps in structuring compliance and supervision. Supervisors typically sit within business units where operational decisions are made. Compliance functions often operate as a control function that monitors regulatory adherence.

Supervisory authority usually sits with business managers or designated principals. Compliance teams typically focus on running the compliance program and monitoring regulatory risks.

Firms often document these responsibilities through organizational charts and written procedures. Regulators frequently review those materials during examinations to understand how oversight is assigned within the firm.

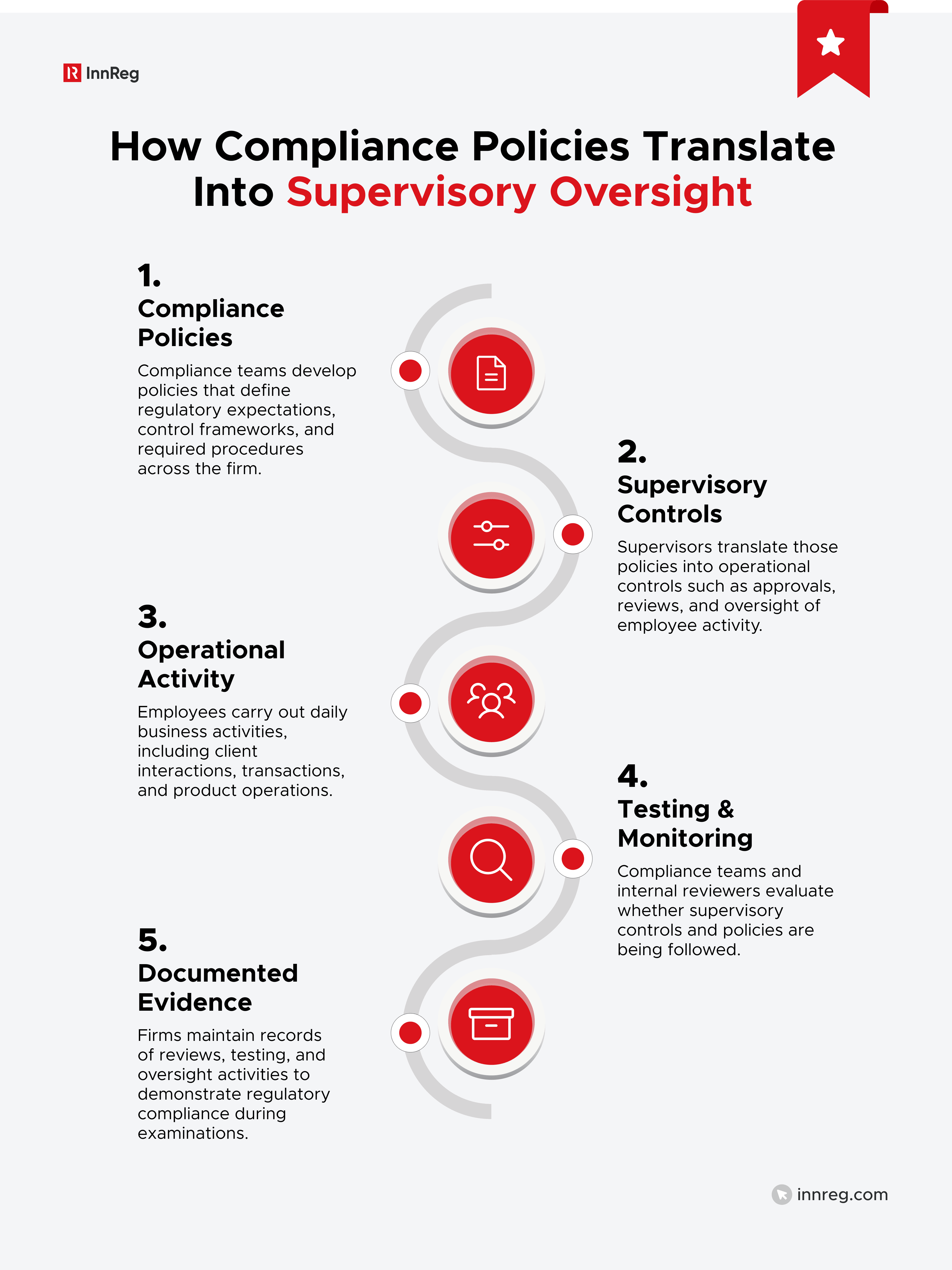

Mapping Policies to Supervisory Controls

Compliance policies are only effective when they connect to actual supervisory processes. Firms often map internal policies to specific supervisory controls so responsibilities are clear.

For example, an AML policy may describe how monitoring should work. Supervisors then oversee how those monitoring activities are carried out in daily operations.

Compliance teams usually develop the policy framework. Supervisors apply those controls in the business. This approach helps show that policies guide real oversight rather than sitting unused in documentation.

See also:

Testing and Evidence Framework

Firms also need a way to demonstrate that compliance and supervision operate as intended. This often involves periodic testing, internal reviews, and documentation of oversight activity.

Testing frameworks typically evaluate whether supervisory procedures are followed and whether compliance controls are functioning as expected. Firms may review transaction approvals, communication monitoring, training records, or escalation procedures.

Documented testing helps firms identify gaps in oversight and provides evidence during regulatory examinations that the governance framework is actively maintained.

Documenting Oversight in Fast-Moving Startups

Fintech companies often move quickly. New products, technology updates, and operational changes can alter how supervision and compliance functions operate.

Because of this, documentation becomes particularly important. Regulators often look at whether governance structures reflect how the business currently operates, not how it operated when policies were first written.

Many fintech firms manage this challenge by maintaining structured compliance workflows, centralized documentation, and clear records of supervisory reviews. These systems help track responsibilities and maintain visibility as the organization grows.

Tarik is a Principal Compliance Consultant at InnReg with over 5 years of experience advising fintech clients across broker-dealer, RIA, and money transmitter verticals. He holds FINRA Series 3, 7, 24, 57, 63, 79, and 99 licenses, with expertise in regulatory strategy, supervisory systems, and compliance roadmap implementation.

How Can InnReg Help?

InnReg is a global regulatory compliance and operations consulting team serving financial services companies since 2013.

We are especially effective at launching and scaling fintechs with innovative compliance strategies and delivering cost-effective managed services, assisted by proprietary regtech solutions.

If you need help with compliance, reach out to our regulatory experts today:

Related Articles

Featured LinkedIn Posts