The SEC's 2026 Exam Priorities: What Fintech Firms Need to Know

The SEC’s 2026 exam priorities set the tone for how the US Securities and Exchange Commission (SEC) will examine broker-dealers, RIAs, investment companies, and fintech firms over the coming year.

For fintech operators, this document is a practical signal of where examiners will focus, what they will ask for, and how they will evaluate risk, controls, and documentation.

The 2026 priorities reflect the SEC's response to increasing complexity in financial products, technology stacks, and operating models, especially where automation, AI, and third-party vendors are involved. Across business lines, the message is consistent: firms are expected to maintain controls that are tailored, tested, and documented. In other words, controls should not be generic or theoretical.

In this article, we’ll explore the SEC exam priorities for 2026, explaining who the priorities apply to, what examiners are actually testing, where firms commonly fall short, and how to prepare in a way that aligns with how modern fintechs operate.

At InnReg, we help broker-dealers, RIAs, and fintech firms prepare for SEC examinations through registration support, compliance program development, and ongoing outsourced compliance management. Our team works as your compliance department, aligning supervision, documentation, AML, trading oversight, and technology governance with how your business actually operates.

What Are the SEC Exam Priorities 2026?

The SEC exam priorities are published annually by the SEC’s Division of Examinations. They outline the areas of higher risk the SEC expects to focus on during examinations, based on market activity, prior exams, enforcement outcomes, and emerging trends.

They are not new rules. They are a roadmap for how the SEC plans to deploy its examination resources across registrants, products, and risk areas.

How the Division of Examinations Uses Priorities

The Division of Examinations uses exam priorities to guide risk-based exams, not to limit them.

Examiners rely on these priorities to decide which firms to examine, which business lines to focus on, and which controls, records, and workflows to test more deeply.

While not every exam will cover every priority, firms operating in higher-risk or complex areas should expect alignment between these priorities and actual exam requests.

What Exam Priorities Are (and Are Not)

The SEC’s 2026 exam priorities are a public articulation of where the Division of Examinations intends to focus its attention. They reflect observed weaknesses from prior exams, enforcement activity, and current market developments, and they are used to shape the scope and depth of examinations.

They are not formal rulemaking, they don’t create safe harbors, and they are not intended to function as a checklist that limits an examiner’s review.

SEC Exam Priorities | |

|---|---|

Are: | Are Not: |

|

|

In practice, SEC examinations often expand beyond the stated priorities when examiners identify elevated risk, weak controls, or inconsistent documentation.

How Fintech Firms Should Read This Document

Fintech firms should approach the SEC's 2026 exam priorities as a practical diagnostic tool rather than a checklist to be completed.

The question is not whether a specific priority applies in theory. The more useful question is where the firm’s actual business model intersects with the risk areas the SEC is signaling.

For many fintechs, that overlap shows up in automated decision-making, reliance on third-party vendors, offering newer or more complex products to retail customers, and scaling quickly while controls are still maturing.

Who Does the SEC's 2026 Exam Priorities Apply To?

The SEC's 2026 exam priorities apply broadly across the SEC-regulated ecosystem, but the level of scrutiny varies based on business model, complexity, and regulatory history.

At a high level, the priorities affect any firm registered with the SEC or operating in a structure the SEC oversees directly or indirectly:

Registered Investment Advisors: As the SEC prioritizes RIA audits, the emphasis has shifted to the operational integrity of compliance programs. Beyond standard fiduciary and disclosure reviews, regulators are interrogating the risks inherent in automated advice. Firms relying on external technology must demonstrate that their oversight keeps pace with their technical delivery.

Broker-Dealers and Trading Platforms: As the SEC continues to prioritize examinations of RIAs, examiners evaluate disclosures, conflicts, marketing practices, and compliance program effectiveness, focusing on models that depend on automated systems or third-party technology.

Investment Companies and Funds: Regulators prioritize the integrity of fund disclosures and the effectiveness of liquidity controls. For funds involving unconventional assets or complex structures, the SEC is drilling down into the robustness of internal risk assessments. There is a clear mandate for boards to demonstrate active supervision over any emerging technologies used in fund operations or portfolio management.

Fintechs Operating Across Multiple Regulatory Regimes: These hybrid models often trigger wider exams focused on cross-entity controls, conflict management, supervision, and allocation of compliance responsibility across the organization.

It’s also worth noting that the SEC continues to prioritize firms that have never been examined and those that have recently registered. These firms often face more detailed reviews, even when operations appear straightforward.

For fintech startups, early exams tend to focus on whether the compliance program is reasonably designed for the business as it actually operates, not as described at registration.

The Core Theme of the SEC's 2026 Exam Priorities: Complexity and Documentation

Across all registrant types and business models, the SEC's 2026 exam priorities are anchored in a single idea: increasing complexity requires stronger, more visible controls. As products, technology, and operating structures evolve, examiners are placing greater weight on how firms identify risk, manage it, and document their decisions.

Why Documentation and Evidence Are the Unifying Expectation

The 2026 priorities make clear that written policies alone are not enough, as the examiners are focused on whether controls function in practice and whether firms can show that through documentation.

That typically includes evidence of testing, supervisory reviews, issue tracking, and remediation. When decisions are made informally or without records, firms often struggle to support their conclusions during an exam.

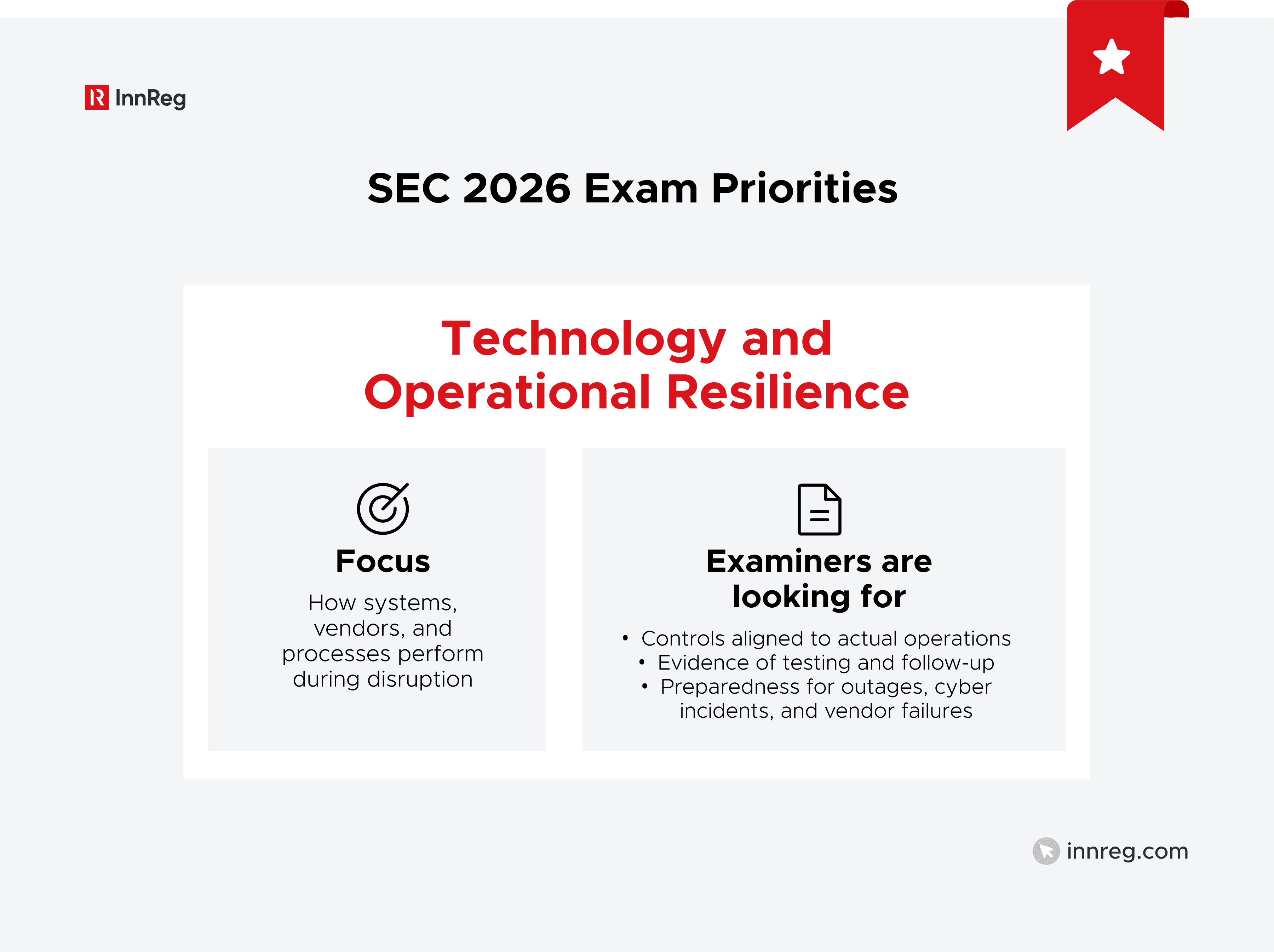

What Examiners Mean by Operational Resilience

Operational resilience, as viewed by examiners, extends well beyond cybersecurity. It covers a firm’s ability to function during disruptions such as system outages, vendor incidents, data issues, or periods of rapid expansion.

Examiners assess resilience through preparedness. They look for evidence of risk assessments, response planning, testing, and follow-up actions. Where critical functions are outsourced, firms are expected to show clear oversight and accountability, similar to what would exist for internal teams.

The Difference Between Having Controls and Proving They Work

From the examiner's perspective, a policy manual is only as good as the trail of evidence it leaves behind. The most common pitfall is not the absence of rules, but the failure to prove they are actually being followed in the daily workflow.

Regulators evaluate controls, expecting firms to provide tangible examples of how their oversight has identified issues, adapted to new risks, and matured over time.

—

Taken together, the SEC's 2026 exam priorities reflect a consistent expectation: firms must be able to explain how their controls operate in real conditions, not just how they are designed on paper.

These expectations carry through the rest of the priorities and shape how exams are structured in practice.

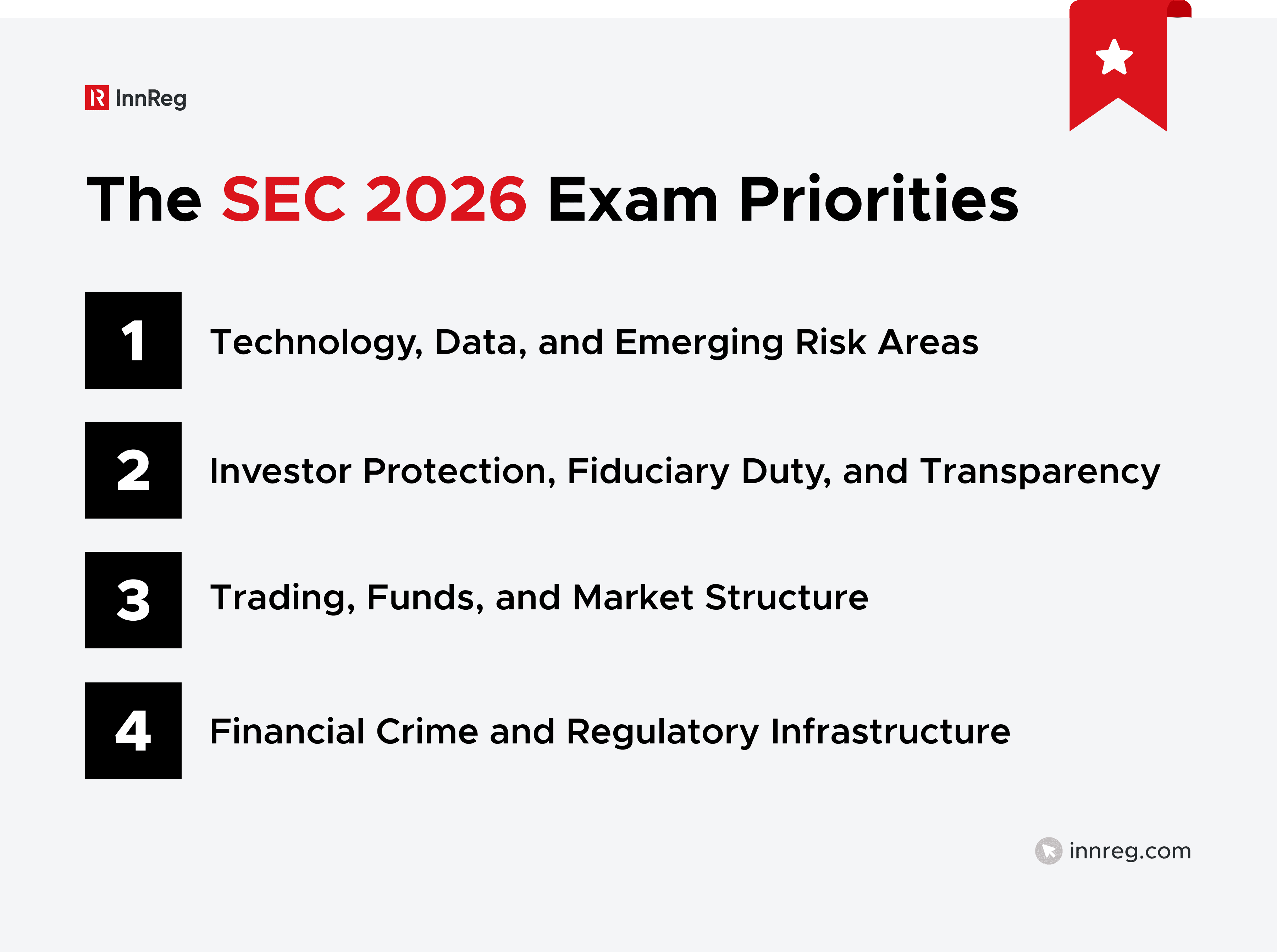

The focus areas that follow fall into four broad categories: technology, data, and emerging risk areas; investor protection and fiduciary obligations; trading practices and market structure; and financial crime and regulatory infrastructure.

1. Technology, Data, and Emerging Risk Areas

Technology and data risk feature prominently in the SEC exam priorities for 2026, as examiners will focus on assessing how technology influences compliance, investor protection, and operational stability.

This review extends to cybersecurity, data governance, vendor oversight, and AI. Where automation is central to the business, firms are expected to show supervision, testing, and accountability.

Technology, Cybersecurity, and Operational Resilience

Technology, cybersecurity, and operational resilience form the foundation of the SEC’s technology-focused review under the SEC's 2026 exam priorities.

Examiners are assessing whether firms understand their technology risk profile and whether controls are designed to reflect how the business actually operates.

What Examiners are Actually Testing

In exams, cybersecurity reviews focus less on theoretical threats and more on execution. Examiners look for evidence that controls are implemented, monitored, and tested, not just described in policies. (Examination Priorities, p.12)

Common exam requests include documentation showing:

How access to systems and data is controlled

How security incidents are identified and escalated

How technology risks are reviewed at the management level

Firms are often asked to walk through real examples rather than explain frameworks at a high level.

Vendor Dependency and Third-Party Risk

For the modern fintech, third-party dependencies are a structural reality rather than an operational choice. Whether it’s cloud hosting, KYC verification, or order routing, each external integration introduces a layer of dependency risk that regulators no longer view as "outsourced."

Under the SEC's 2026 exam priorities, vendor oversight is treated as an extension of internal controls, not a separate function. Examiners expect firms to understand which vendors are critical, how those vendors are monitored, and how issues would be handled if a vendor fails. (Examination Priorities, pp.13-14)

Simply relying on contractual assurances or SOC reports without internal review often raises follow-up questions.

Vendor and Third-Party Risk | ||

|---|---|---|

SEC focus: | Examiners look for: | Common Gap: |

Reliance on vendors that perform critical functions. | Identification of critical vendors Ongoing oversight and review Defined response if a vendor fails | Over-reliance on contracts or SOC reports without internal review. |

Incident Response, Business Continuity, and Testing Expectations

Preparedness carries significant weight in exams. Examiners review whether incident response and business continuity plans are current and aligned with the firm’s operations.

Testing is a key part of that review. Firms are expected to demonstrate that plans have been exercised, weaknesses addressed, and changes documented, whether the risk involves cybersecurity, system failures, or vendor outages. Operational resilience is measured by readiness and execution.

Common Fintech Gaps in this Area

In practice, fintech compliance often falters at the implementation stage. It’s common to find robust policies undermined by a lack of rigorous, documented testing. Reliance on "handshake" vendor oversight and aging incident response protocols suggests a lack of operational maturity that examiners are increasingly unwilling to overlook.

The issue examiners focus on most is the lack of documentation connecting technology controls to real operational decisions. As fintech businesses scale and systems become more complex, that gap often grows unless it is addressed intentionally.

Safeguarding Customer Information and Data Governance

Safeguarding customer information remains a priority under the SEC's 2026 exam priorities. But the focus has shifted from high-level policies to how data is actually governed and protected in day-to-day operations. Examiners are paying closer attention to internal access, data flows, and how firms control sensitive information across systems and vendors.

This review cuts across cybersecurity, privacy, supervision, and recordkeeping. The core question is whether firms know where customer data lives, who can access it, and how that access is controlled and monitored.

Internal Access Controls and Insider Risk

Examiners increasingly focus on internal risk, not just external threats. (Examination Priorities, p. 13) This includes how firms manage employee access to customer data and critical systems.

Reviews often look at:

Role-based access controls and approval processes

Periodic access reviews and terminations

Monitoring for inappropriate or excessive access

Firms with broad or poorly documented access rights often face deeper questioning, particularly where staff roles have evolved or systems were added quickly.

Privacy Obligations Under Regulation S-P and Regulation S-ID

Data governance reviews frequently reference compliance with Regulation S-P and Regulation S-ID, especially in light of recent amendments and enforcement activity. (Examination Priorities, p.13)

Examiners assess whether firms have:

Updated privacy and safeguarding policies that reflect current operations

Controls around data sharing with vendors and affiliates

Processes to detect, respond to, and document data incidents

Privacy compliance is evaluated in practice. Disclosures, procedures, and actual handling of customer information are expected to align.

Additional Resources: | |

|---|---|

What the SEC Expects Around Data Governance Frameworks

For the SEC, data governance is less about a specific framework and more about the visibility of controls. Regulators prioritize the "human element" of data risk: Who is held accountable when automation or AI tools mishandle customer information.

Modern fintechs often face challenges here because their data is siloed across various vendors. The SEC expects a unified explanation of how security standards are maintained across the entire technological ecosystem.

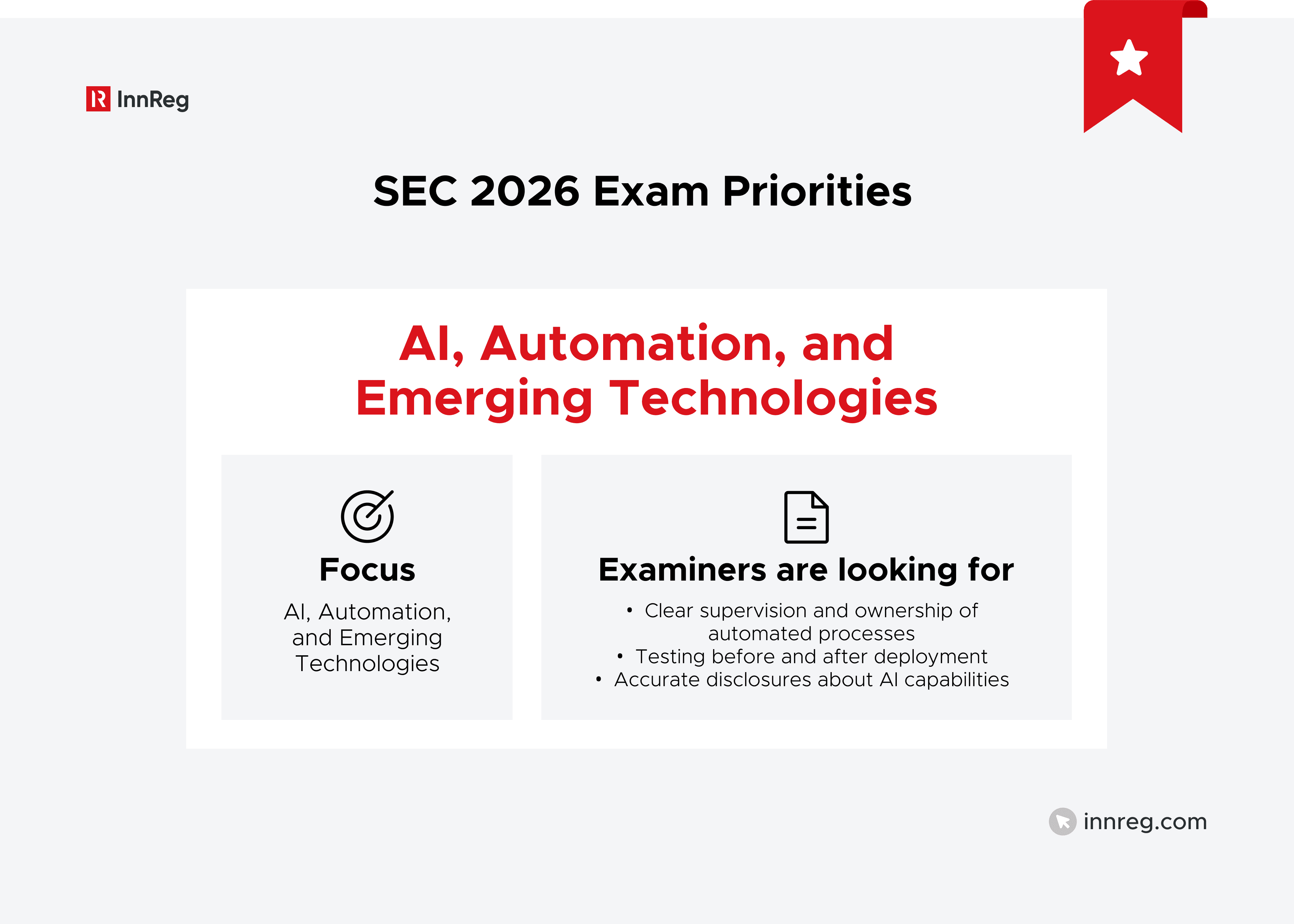

Oversight of Emerging Technologies, Automation, and AI

Oversight of emerging technologies features more prominently in the SEC's 2026 exam priorities than in prior years. As fintech firms expand their use of automation and AI across advice, trading, surveillance, marketing, and operations, examiners are paying closer attention to how those tools are supervised.

The SEC’s view is clear. Automation doesn’t shift regulatory responsibility. Firms remain accountable for compliance, disclosures, and outcomes, whether decisions are made by people or by a system.

How the SEC Views AI Risk in 2026

The SEC views AI primarily through a risk lens. (Examination Priorities, p.12) Efficiency gains are acknowledged, but examiners are focused on how automation can introduce conflicts, bias, errors, or inconsistent outcomes if left unsupervised.

Reviews often focus on whether AI tools influence regulated decisions or outcomes, such as recommendations, order handling, or risk scoring, or are used to generate, personalize, or deliver customer communications that are subject to disclosure, marketing, or supervisory requirements. Where that influence exists, examiners expect firms to understand and manage the associated risks.

Marketing claims about AI also receive attention. Firms are expected to accurately describe what AI tools do and how they are used, without overstating capabilities or outcomes.

What “Adequate Supervision” Means for Automated Tools

Regulatory expectations for automated tools mirror traditional supervisory requirements. The focus is on the "human-in-the-loop" model: identifying which regulated functions are automated and who is tasked with their oversight.

That typically includes:

Identifying where automation affects regulated activity

Assigning responsibility for oversight and review

Establishing thresholds for human intervention

Effective governance is evidenced by formal review cycles and documented escalation protocols.

Model Testing, Validation, and Documentation

Testing is a central theme in AI-related exams. Examiners expect firms to demonstrate that automated tools were reviewed before deployment and monitored after implementation.

This includes documentation showing how models were tested, how outputs are reviewed, and how issues are addressed. Testing doesn’t need to be academic, but it does need to be repeatable and tied to regulatory risk.

Ongoing monitoring matters as much as initial validation, especially as data inputs, customer behavior, or business use cases change.

AI Disclosures: Where Firms Often Get It Wrong

Disclosure issues usually stem from firms describing AI in broad or promotional terms while disregarding how the tools are actually used or supervised.

In exams, disclosures are compared directly to system behavior.

Issues often surface when AI is presented as independent or objective without context, when human review is vague or overstated, or when data inputs and limitations are not clearly described. Under the SEC's 2026 exam priorities, examiners consistently focus on whether disclosures, controls, and system behavior align.

See also:

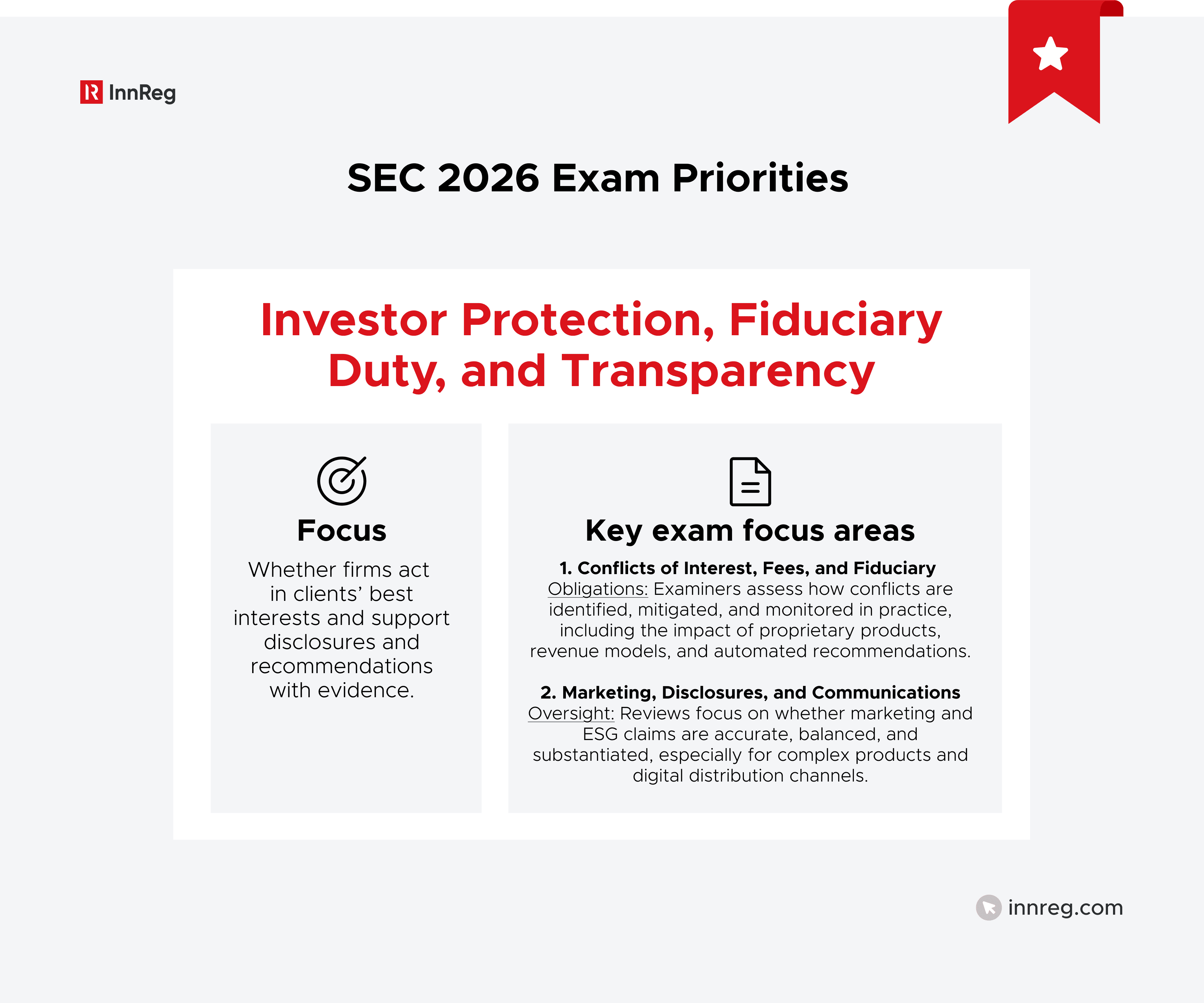

2. Investor Protection, Fiduciary Duty, and Transparency

Investor protection remains a central pillar of the SEC exam priorities for 2026, particularly as fintech firms introduce new products, distribution models, and automated decision-making. Examiners are focused on whether firms are acting in clients’ best interests and whether disclosures, pricing, and recommendations hold up under scrutiny.

Need help with broker-dealer compliance?

Fill out the form below and our experts will get back to you.

a. Conflicts of Interest, Fees, and Fiduciary Obligations

Conflicts of interest and fee practices continue to receive sustained attention under the SEC's 2026 exam priorities. (Examination Priorities, p.4) This applies to both RIAs (Examination Priorities, p.4) and broker-dealers (Examination Priorities, p.8), particularly where firms offer proprietary products, receive indirect compensation, or operate multiple business lines.

Examiners are less interested in whether conflicts are disclosed in theory and more focused on how they are identified, mitigated, and monitored in practice.

How Fiduciary Duty is Examined in Practice

For RIAs, fiduciary duty remains at the center of the exam process as examiners are not just reviewing disclosures, but how recommendations are actually formed and whether firm incentives influence outcomes.

They look at how recommendations are generated, whether alternatives are considered, and how conflicts are handled in real time. If automated tools are involved, examiners expect fiduciary considerations to be part of the design.

Conflicts Tied to Proprietary Products and Revenue Models

Fintech business models frequently involve embedded conflicts, including proprietary products, revenue-sharing arrangements, or affiliated services.

Examiners look closely at:

How conflicts are disclosed to clients

Whether disclosures are specific and current

Whether controls exist to mitigate the impact of those conflicts

Generic disclosures often trigger follow-up questions, particularly when revenue incentives are significant.

AI-Driven Recommendations and Best-Interest Analysis

As firms increasingly rely on automation and AI to support recommendations, examiners assess whether those tools introduce new conflicts or bias.

The key question is not whether technology is used, but whether firms can explain why a particular recommendation was made and how it aligns with client interests. Firms remain responsible for outcomes, regardless of whether people or systems generate recommendations.

Documentation Examiners Expect to See

During exams, documentation becomes the backbone of conflict and fiduciary analysis. Examiners want to see how recommendations took shape and who reviewed them along the way.

When that trail is incomplete or inconsistent, it becomes harder for firms to show that decisions were driven by client interests rather than firm incentives.

b. Marketing, Disclosures, and Communications Oversight

Marketing and communications remain a consistent exam focus, particularly as fintech firms expand their use of digital channels, performance metrics, and ESG-related claims. (Examination Priorities, pp. 5-6)

Examiners assess whether statements made to clients and the public are accurate, balanced, and supported by underlying data.

Accuracy and Substantiation of Marketing Claims

Examiners compare marketing materials against actual practices and performance.

Marketing Claims Review Focus |

|---|

|

Claims that cannot be substantiated through records or analysis often raise concerns, even if they appear reasonable at a high level.

Learn more about the SEC Marketing Rule →

ESG Disclosures and Greenwashing Risk

ESG disclosures remain an area of close attention in exams. Examiners look at whether ESG-related statements align with how investments are actually selected and managed.

Problems tend to arise when ESG language is used broadly without defined criteria, or when disclosures do not reflect portfolio construction. Firms are expected to be able to explain how ESG factors are defined, applied in practice, and monitored over time.

Complex Strategies and Heightened Disclosure Expectations

Products that involve leverage, digital assets, derivatives, or more complex structures always receive closer attention in exams. Examiners focus on whether risks, limitations, and potential outcomes are explained clearly and in a way that matches the intended investor audience.

As product complexity increases, expectations around disclosure detail and clarity increase as well.

Common Marketing Exam Deficiencies

Marketing exams frequently surface the same issues: outdated materials, inconsistent disclosures across channels, and insufficient review or approval processes.

Problems tend to arise when marketing evolves faster than compliance oversight, particularly in high-growth fintech environments.

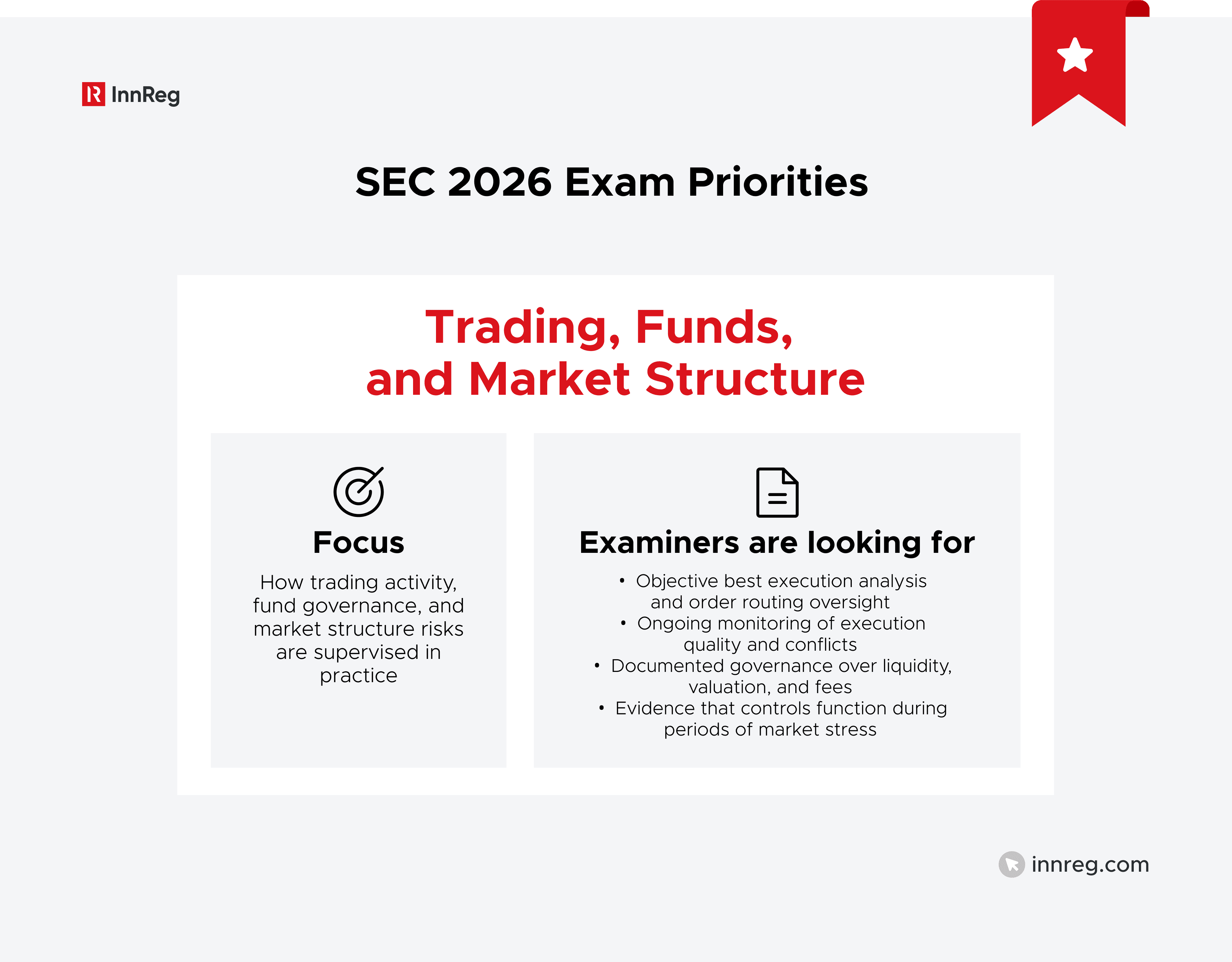

3. Trading, Funds, and Market Structure

Trading activity and fund operations remain a significant focus under the SEC exam priorities for 2026 (Examination Priorities, p. 4). Examiners are focused on whether market activity is fair, well-supervised, and supported by controls that reflect how trading and portfolio management actually occur.

a. Trading Practices and Best Execution

Examiners continue to focus on best execution, especially when it comes to retail trading environments that rely on automated routing and focus on whether execution quality is monitored in practice.

Learn more about FINRA Rule 5310 (Best Execution and Interpositioning) →

Order Routing and Execution Quality

Exams often look at how orders are routed and how execution quality is assessed across venues. This includes reviewing routing logic, execution analysis, and how issues are identified and addressed over time.

Firms are expected to show that routing decisions are based on objective factors, not convenience or revenue arrangements.

Payment for Order Flow Considerations

Where payment for order flow or similar arrangements exist, examiners focus on evaluating how those arrangements are disclosed and managed.

The focus is on whether firms understand the conflicts involved and whether controls exist to evaluate execution quality independently of compensation received.

Clear documentation of routing decisions and execution reviews is often central to this analysis.

Oversight of Automated and High-Risk Trading Strategies

Automated trading and higher-risk products tend to draw closer scrutiny in exams, particularly in retail environments.

Examiners focus on supervision of automated strategies, controls around model changes, and how risk limits are set and monitored. Firms are expected to explain how automated trading activity is reviewed and how issues are identified and addressed.

b. Investment Company Governance and Risk Management

For investment companies and funds, governance and risk management remain core exam priorities. This is especially true for funds that are using complex strategies or holding assets that may be difficult to value or liquidate.

Liquidity Risk and Redemption Planning

Examiners assess whether firms have evaluated liquidity risks, established appropriate monitoring, and planned for stressed redemption scenarios.

Documentation showing how liquidity decisions are reviewed and updated is often requested.

Valuation of Complex or Illiquid Assets

Asset valuation remains an exam focus when pricing involves judgment, models, or third-party data. Examiners review how valuation methodologies are applied, how price challenges are handled, and how third-party pricing services are overseen.

Firms are expected to be able to explain how valuation decisions are made and reviewed, particularly during periods of market stress.

Board Oversight and Documentation

Examiners continue to focus on reviewing whether boards receive sufficient, relevant information and whether key decisions are documented in meeting materials and minutes.

Weaknesses often appear when risk discussions, approvals, or follow-up actions are not clearly recorded, especially in connection with complex strategies or new product launches.

Fee Transparency and Disclosures

Fees and related disclosures continue to receive close attention in fund exams.

Examiners compare what’s disclosed to investors against what’s actually charged and review whether expenses are allocated in line with governing documents.

Problems often arise when disclosures fall out of date or when fee practices change without corresponding updates to documentation and investor communications.

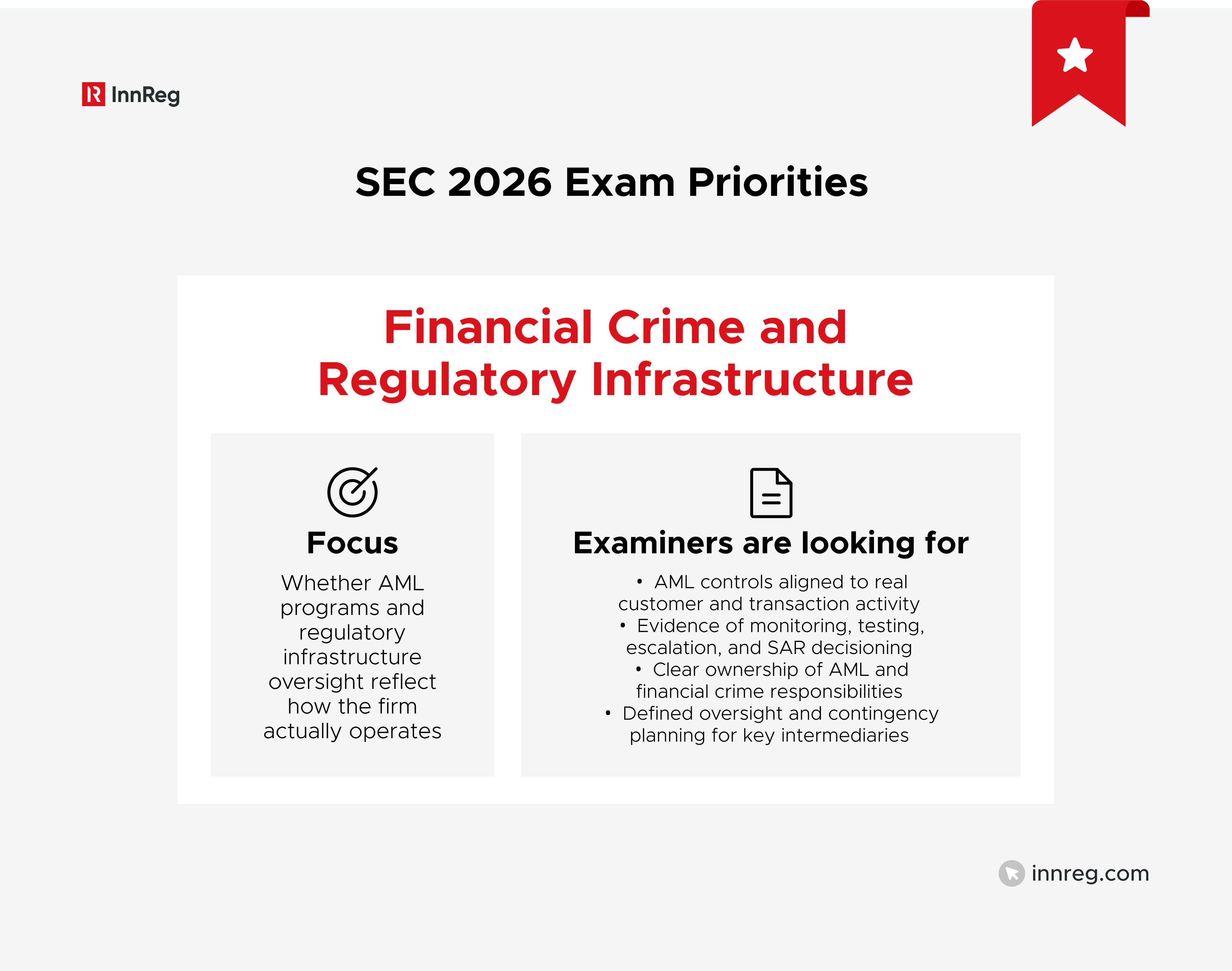

4. Financial Crime and Regulatory Infrastructure

Financial crime controls and regulatory infrastructure remain a core focus of the SEC's 2026 exam priorities, particularly as fintech firms expand into new products, customer segments, and jurisdictions. Examiners are less concerned with whether a firm has a program on paper and more focused on whether controls are tailored, effective, and supported by documentation.

See also:

a. AML and Financial Crime Controls

Anti-money laundering continues to receive sustained exam attention, with a growing emphasis on effectiveness rather than formal design. This applies to broker-dealers, RIAs, and fintech firms that touch customer funds, trading activity, or payment flows.

Examiners assess whether AML programs reflect the firm’s actual business model, customer base, and risk profile.

Tailored AML Programs vs. Generic Templates

One-size-fits-all AML programs remain a common exam issue. Examiners expect AML controls to be tailored to the firm’s products, customers, geographies, and transaction activity, not copied from generic templates.

Reviews often focus on how risk assessments are performed and how those assessments drive monitoring, escalation, and reporting decisions. Programs that don’t evolve with the business tend to draw follow-up questions.

Learn how InnReg helps fintech develop KYC and AML programs →

Monitoring, Testing, and SAR Expectations

Transaction monitoring and surveillance remain an essential part of all AML exams. Examiners review how alerts are generated, investigated, and resolved, along with how suspicious activity is documented and reported.

Testing matters as the firms are expected to review monitoring rules periodically, while sampling results, and escalation outcomes.

Weak documentation around alert handling or SAR decisions often becomes a focal point during exams.

Learn more about suspicious activity reports in our guide →

Digital Assets, Omnibus Accounts, and Higher-Risk Activity

Fintech models involving digital assets, omnibus accounts, or complex payment flows receive closer scrutiny. Examiners assess whether firms understand how funds move through their platforms and where higher-risk activity may arise.

Firms are expected to explain how monitoring accounts for these structures and how controls adjust as products or transaction volumes change.

Read our article to learn more about omnibus broker-dealers →

Documentation Gaps the SEC Frequently Identifies

AML exams frequently surface familiar issues such as outdated risk assessments, limited evidence of testing, and inconsistent escalation practices.

The most common gap is the lack of documentation connecting AML controls to actual customer and transaction activity, especially as fintech platforms scale.

b. Oversight of Key Market Infrastructure and Intermediaries

Beyond firm-level controls, the SEC also reviews how key market infrastructure operates and how regulated firms interact with it. This includes exchanges, clearing agencies, and other intermediaries that support trading and settlement.

FINRA, Exchanges, and Clearing Agencies

Examiners look closely at how firms work with FINRA, exchanges, and clearing agencies, particularly where functions are outsourced or systems are shared.

Reviews often explore whether firms understand who is responsible for what and how problems are escalated when they occur.

Why These Reviews Matter for Platform-Based Models

In platform-based fintech models, infrastructure risk doesn’t stop at the firm’s perimeter. Examiners often trace issues back through clearing firms, exchanges, or other service providers to assess how oversight is maintained.

When problems arise at these counterparties, exams tend to expand to include questions about supervision, dependency risk, and business continuity. Firms are expected to demonstrate awareness of these risks and have plans in place to address disruptions.

How Fintech Firms Should Prepare for SEC Exams in 2026

The SEC's 2026 exam priorities are clear: Examiners are evaluating how firms manage risk in real time, not how well they can assemble documents under pressure.

When preparing for an examination, pay close attention to the following areas:

Exam-Focused Preparation Framework

Effective exam preparation begins with understanding where regulatory risk intersects with the business model. That means mapping products, technology, vendors, and customer flows to the controls that govern them.

Firms that perform well in exams typically have clear ownership of key risk areas, documented decision-making, and evidence of ongoing review. Preparation is continuous, not event-driven.

Documentation Readiness Checklist

Documentation remains the foundation of nearly every exam. Examiners use it to understand how controls operate and whether they are applied consistently.

The focus shouldn’t be volume but relevance and clarity.

Area of Review | What Examiners Look For |

|---|---|

Policies and procedures | Alignment with current operations and products |

Testing and reviews | Evidence controls are tested and adjusted |

Supervision | Records showing oversight and follow-up |

Issues and remediation | Documentation of how problems were identified and addressed |

Vendor oversight | Clear monitoring and escalation processes |

Internal Ownership and Accountability

Questions around ownership are common in exams. Examiners want to understand who is responsible for key processes, how oversight is structured, and where escalation occurs when problems are identified.

In hybrid or outsourced arrangements, unclear ownership is a frequent exam issue. Firms are expected to identify who is responsible for each regulated function, particularly where automation or vendor support plays a role.

When to Escalate Issues Before an Exam

Exams tend to expand when examiners uncover unresolved issues or inconsistent explanations. Identifying, documenting, and actively addressing known gaps before an exam puts firms in a better position.

Escalation doesn’t mean perfection. It means being able to explain what was identified, how it is being handled, and what steps are underway.

See also:

—

The SEC's 2026 exam priorities reflect a regulatory response to increasing complexity across financial services. Examiners are focused on how firms manage technology, data security, operational resilience, and risk in practice, not just how those controls are described.

As automation and AI become more and more common, the SEC is placing greater weight on supervision, testing, and documentation.

The same expectation applies across traditional exam areas, including conflicts, fees, marketing, trading practices, fund governance, and AML.

The common thread is whether controls work as intended and are supported by evidence.

For fintech firms, these priorities mirror how exams are already unfolding. Firms that understand their risk profile and can explain how controls operate day to day are better positioned as regulatory scrutiny continues to evolve.

Bruno is a Principal Compliance Officer at InnReg advising fintech clients across broker-dealer, RIA, and money transmitter verticals. He brings prior experience at Santander Brasil and Passfolio, with expertise in regulatory strategy, supervisory systems, and compliance execution. He holds FINRA Series 4, 7, 24, 63, and 99 licenses.

How Can InnReg Help?

InnReg is a global regulatory compliance and operations consulting team serving financial services companies since 2013.

We are especially effective at launching and scaling fintechs with innovative compliance strategies and delivering cost-effective managed services, assisted by proprietary regtech solutions.

If you need help with broker-dealer compliance, reach out to our regulatory experts today:

Related Articles

Featured LinkedIn Posts