What Is General Solicitation in Financial Services?

General solicitation is one of the most commonly misunderstood areas in fundraising compliance, especially for fintech companies navigating complex regulatory environments.

Whether you are running a broker-dealer, launching a crypto platform, or raising capital through a new RIA, understanding what qualifies as general solicitation (and when it’s allowed) is critical.

This article breaks down what general solicitation is, when it applies, and what rules govern its use under SEC regulations. We will cover the key exemptions, such as Rule 506(b), Rule 506(c), Reg CF, and Reg A, and highlight what each permits (and restricts) regarding advertising and investor outreach.

At InnReg, we help fintech companies manage the regulatory challenges of general solicitation and capital raising. Whether you're structuring an offering or building controls around public messaging, our team supports licensing, compliance program design, and day-to-day operations.

What Is General Solicitation?

General solicitation refers to public-facing communications used to promote a securities offering. These can include online advertising, public websites, social media posts, press releases, mass emails, or speaking engagements where the offering is discussed with an unrestricted audience.

The key factor is who receives the message. Sharing fundraising information with individuals outside a company’s existing network can be enough to classify the outreach as general solicitation, regardless of whether the company asked anyone to invest.

Most private offerings, particularly those conducted under Rule 506(b), prohibit general solicitation entirely. Only specific exemptions, such as Rule 506(c), Regulation Crowdfunding (Reg CF), and Regulation A, permit it under strict conditions. Each exemption carries its own compliance requirements and operational implications.

For financial services firms, especially those operating in fintech, understanding what qualifies as general solicitation is foundational. A misstep in public communications can put an entire raise at risk, even if the business itself is fully compliant in other areas.

When Does General Solicitation Apply?

General solicitation applies when a company communicates about an offering in a way that reaches individuals outside its existing network. This includes any outreach to people with whom the company does not have a substantive, pre-existing relationship.

It does not take much for a communication to be considered a solicitation. A social media post about a current raise, a mention in a podcast, or an email sent to a purchased list could all trigger regulatory scrutiny. Even subtle references to investment opportunities, if made in a public or broadly distributed format, may qualify.

Regulators focus less on the intent behind the message and more on its reach and context. The broader the audience, and the less targeted or relationship-based the communication, the more likely it falls under general solicitation.

Why General Solicitation Matters for Fintech Companies

General solicitation can determine whether a raise is compliant or subject to regulatory action. Fintech companies, by nature, tend to operate in highly visible, fast-paced markets. As a result, public communication is frequent and often central to product launches, user growth, and investor engagement.

In crypto and other fintech verticals, it is common to post product updates or business milestones. But if a company is raising capital at the same time, those updates, depending on how they are framed, can inadvertently qualify as general solicitation.

This matters because most exemptions used in early-stage or growth fundraising place clear limits on public promotion. Violating those terms, intentionally or not, can result in an offering being deemed unregistered and illegal. At best, that may mean refilling or restructuring. At worst, rescission offers will be required, enforcement exposure, and long-term reputational damage can result.

Fintech founders and compliance leads must factor solicitation rules into their broader capital strategy. That includes coordinating with legal and marketing teams, identifying which exemption is in use, and building investor pipelines that support it. For teams moving quickly, having regulatory advisors or outsourced compliance support with fintech-specific experience can help avoid common missteps.

Key Exemptions and How They Treat General Solicitation

Most private offerings in the US rely on exemptions from SEC registration. Each exemption handles general solicitation differently; some prohibit it entirely, others permit it with specific conditions. Choosing the right exemption is often the first decision a fintech company needs to make when structuring a raise.

Exemption | General Solicitation Allowed? | Investor Requirements | Verification Required? | Max Raise Limit |

|---|---|---|---|---|

Rule 506(b) | No | Unlimited accredited, up to 35 non-accredited | No | Unlimited |

Rule 506(c) | Yes | Accredited investors only | Yes | Unlimited |

Reg CF | Yes | Accredited and non-accredited allowed | No | $5 million per year |

Regulation A (Tier 2) | Yes | Accredited and non-accredited allowed | No | $75 million per year |

Rule 506(b): No General Solicitation Allowed

Rule 506(b) is the most commonly used exemption for private offerings, but it comes with a strict prohibition on general solicitation. That means no public promotion, no broad outreach, and no advertising in any form.

Under this exemption, companies can raise an unlimited amount of capital from accredited investors and up to 35 non-accredited investors. However, all outreach must be private and targeted. The SEC expects that the company has a pre-existing, substantive relationship with any investor before discussing the offering.

Investors may self-certify accredited status under Rule 506(b). While this lowers the verification burden, it also restricts how the raise can be promoted. Communications must be limited to individuals the company already knows. Public outreach, even if indirect, puts the exemption at risk.

This exemption is best suited for companies that already have strong relationships with prospective investors. It also appeals to firms that want to keep their fundraising activity discreet, especially in the early stages.

Rule 506(c): General Solicitation Permitted With Verification

Rule 506(c) allows companies to publicly advertise their offering, but only if all investors are accredited and properly verified. This exemption is often used when a broader outreach strategy is needed, such as through websites, email campaigns, or investor-facing platforms.

Under Rule 506(c), firms must go beyond investor declarations. They are expected to collect documents or use verified third-party tools to confirm accredited status. This requirement is non-negotiable, even for friends or longtime contacts.

Public promotion is permitted, but only if the investor vetting process is thorough and well-documented. Any gap in the process may expose the offering to compliance risks.

This approach is often selected by fintech firms seeking to grow their reach during fundraising. It is compatible with digital outreach strategies but demands clear internal controls and reliable execution.

Regulation Crowdfunding (Reg CF): Limited Advertising, Strict Rules

Reg CF lets companies advertise their raise, but only if the offering is conducted through a regulated crowdfunding platform. Any public communication that includes terms must stick to a strict format and direct people back to the portal.

Firms may share the basics, but that is where it stops. If they want to talk about terms, pricing, or risks, that information needs to live on the portal and not in blog posts, interviews, or ads.

This structure allows outreach to a wider pool of investors, including retail participants. But it also requires careful coordination. Companies must monitor all messaging and avoid discussing the raise outside approved channels.

See also:

Regulation A: Public-Like Offering With SEC Oversight

General solicitation is allowed under Regulation A once the SEC has reviewed and qualified the offering circular. Tier 2 provides access to a wider investor pool and supports raises of up to $75 million, compared to Reg CF’s $5 million cap.

To use this exemption, the issuer must prepare and file an offering circular with the SEC. The review process typically takes several weeks. Once qualified, the company may promote the offering publicly—through its website, social media, investor webinars, or paid media.

Tier 2 of Regulation A is most relevant to fintech firms seeking broader investor participation or institutional credibility. Tier 2 preempts state-by-state review, which simplifies the process compared to Tier 1. That said, it adds complexity elsewhere. Firms must provide audited financials, maintain regular reporting, and build out compliance systems to support the offering.

This exemption is often used by consumer-facing fintechs, especially those with large user bases or community investors. While it expands marketing flexibility, it also requires strong legal and operational coordination to handle disclosures, filings, and post-raise obligations.

Learn how InnReg supports compliance filings →

Need help with crowdfunding compliance?

Fill out the form below and our experts will get back to you.

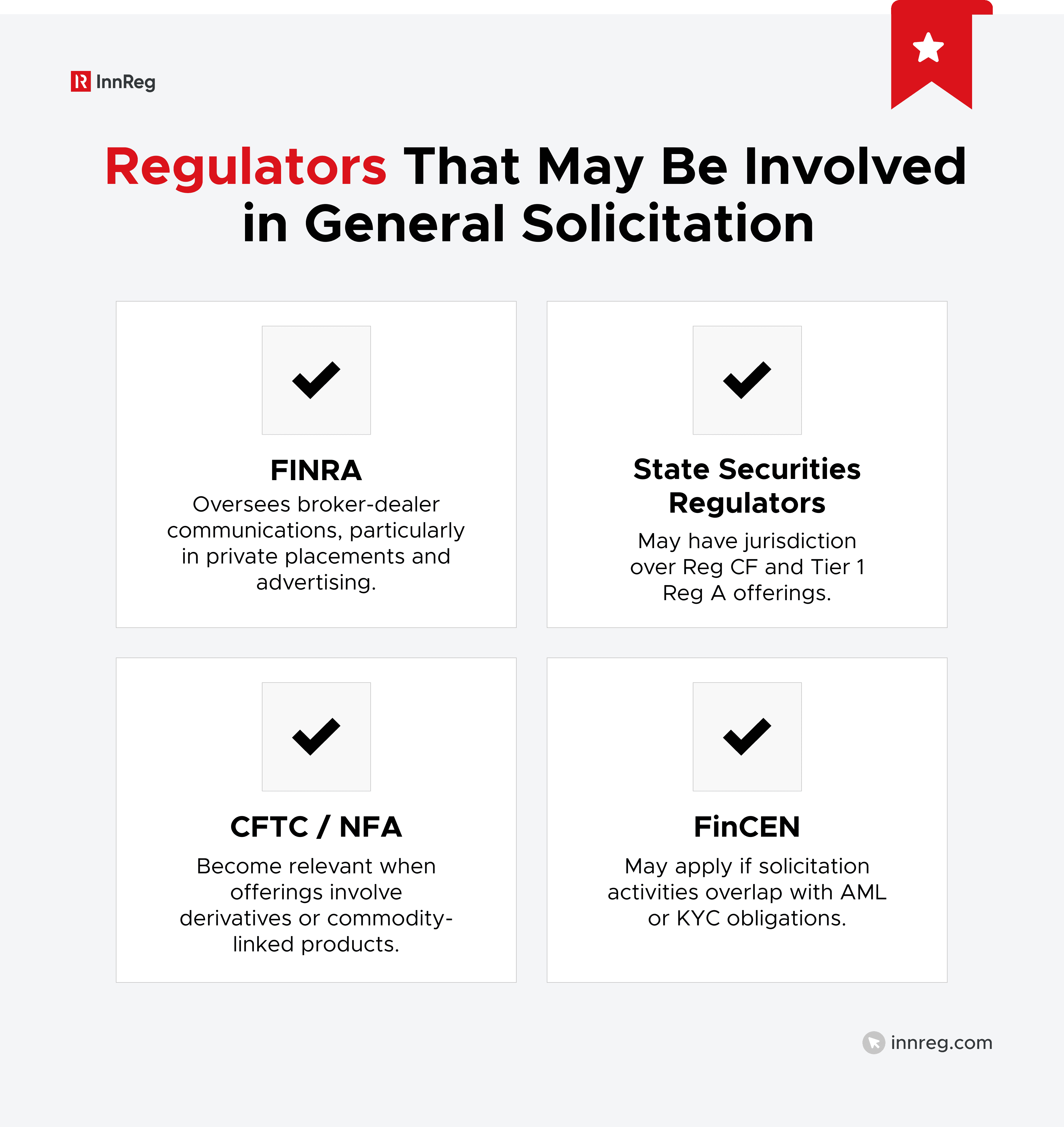

Regulators Involved in General Solicitation Oversight

General solicitation rules are shaped and enforced by multiple regulatory bodies. For companies operating in the financial sector, especially fintech, understanding who regulates what is essential.

The Securities and Exchange Commission (SEC) is the primary authority governing general solicitation. It sets the standards for exemptions like Rule 506(b), Rule 506(c), Regulation Crowdfunding, and Regulation A. It also reviews offering filings, oversees enforcement, and provides interpretive guidance through rules and no-action letters.

Fintech companies must understand how general solicitation intersects with their licensing status, investor base, and regulatory footprint. Oversight can be multi-layered, and errors in communication may trigger scrutiny from more than one agency.

Common Compliance Challenges With General Solicitation

General solicitation rules are often misunderstood or misapplied, especially by fast-moving teams. The regulatory thresholds are not always obvious, and small missteps can have broader consequences.

Here are some of the most common issues fintech companies encounter:

Accidental general solicitation. Public posts, press mentions, or podcast appearances made during a raise, often without legal review, can violate exemption rules.

Mixing exemptions. Companies may start under Rule 506(b) and later switch to 506(c) without adjusting their process. That can create compliance gaps if the transition is not carefully documented.

Insufficient investor verification. Under Rule 506(c), relying on self-attestation or outdated documentation fails to meet the “reasonable steps” standard required by the SEC.

Improper use of platforms. Announcing a raise on a company website or product landing page, without gating or proper disclaimers, may qualify as general solicitation unless the exemption permits it.

Overly broad marketing. Mass email campaigns or online ads targeting a general audience can trigger regulatory concerns unless conducted under an exemption that allows public solicitation.

Lack of internal controls. When legal, marketing, and executive teams operate independently during a raise, communications can easily become inconsistent or non-compliant.

Most of these issues are avoidable with a coordinated, well-documented approach. Teams that build compliance into their fundraising process, rather than layering it on afterward, tend to navigate these rules more effectively.

Learn how InnReg helps fintech develop a regulatory strategy →

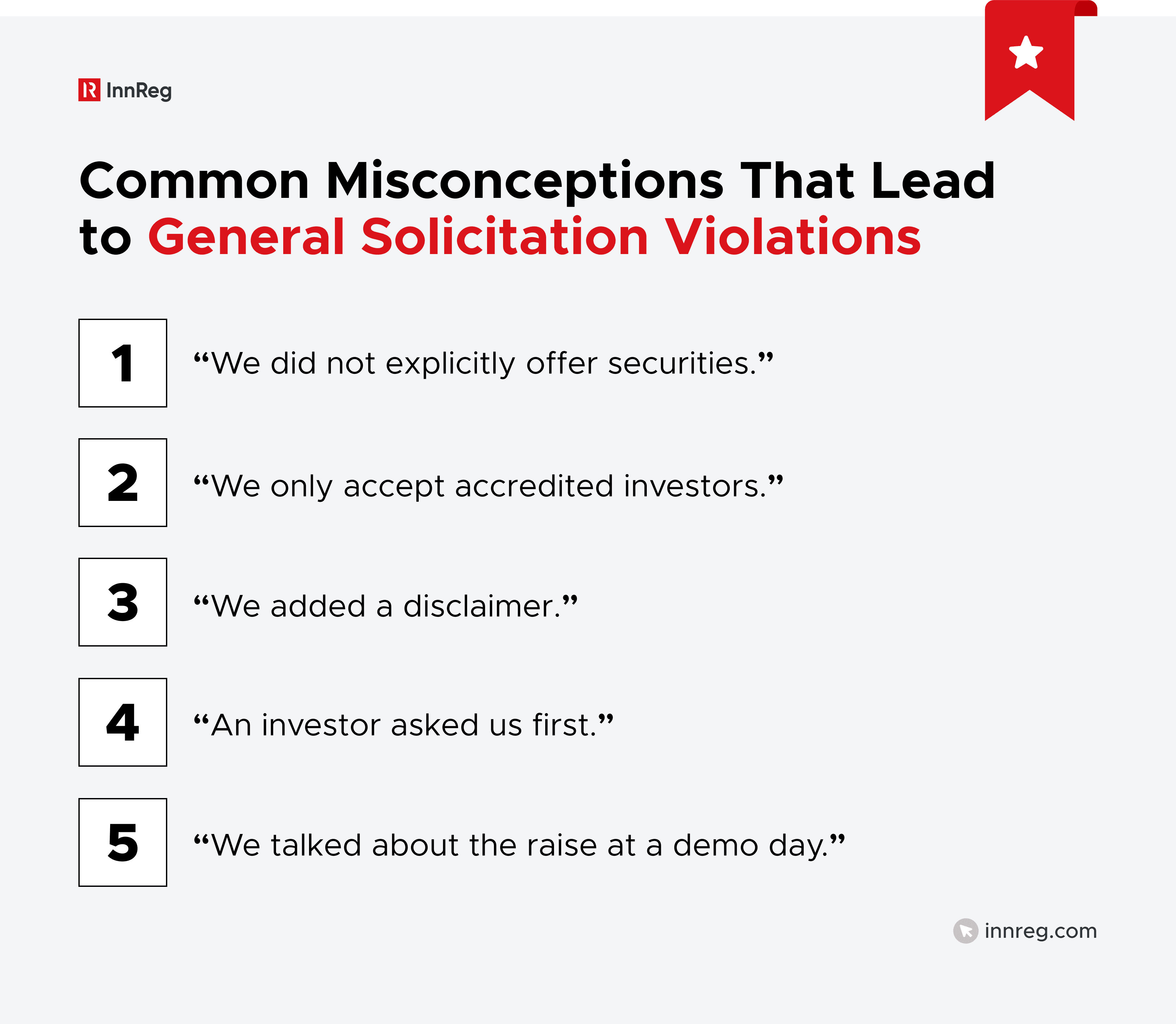

Misconceptions That Lead to Violations

In many cases, companies run into problems with general solicitation because they misread the rules. The difference between acceptable communication and something that crosses the line is often less obvious than it seems.

“We did not explicitly offer securities.”

Even if there’s no direct ask, statements like “We are raising” or “We are halfway through our round” may still be viewed as general solicitation.

The SEC looks at whether the communication is designed to generate interest, not just at the words used.

“We only accept accredited investors.”

This is not a free pass to advertise.

Unless the raise is structured under Rule 506(c), Reg CF, or Reg A, and verification procedures are in place, the offering must remain private and targeted.

Simply restricting participation is not enough.

“We added a disclaimer.”

Phrases such as “This is not an offer to sell securities” do not override the substance of the message. Regulators assess whether the communication is promotional or conditioning the market, regardless of disclaimers.

“An investor asked us first.”

A single investor reaching out with interest does not give a company the green light to respond publicly.

If that exchange moves to a visible forum, such as a comment thread, social post, or public webinar, the SEC may still view it as general solicitation. The “reverse inquiry” concept only applies when both the inquiry and response stay private.

“We talked about the raise at a demo day.”

Not all demo day appearances are exempt from general solicitation rules. If a company is relying on Rule 506(b), the event must meet specific SEC criteria to avoid triggering a violation.

To qualify under the safe harbor, the event must be hosted by a sponsor such as a university, angel group, or government program. The audience should be limited in scope, and the company must avoid sharing offering terms like pricing or valuation during the presentation.

Sharing a pitch publicly, especially through an unrestricted video or event stream, can push it into general solicitation territory. That type of outreach conflicts with Rule 506(b), and companies may be required to switch to a different exemption if they proceed.

—

Understanding these traps can help companies avoid preventable mistakes. Many of these misconceptions stem from marketing instincts that conflict with regulatory constraints. Founders, compliance teams, and marketing leads should align early to avoid sending mixed signals.

InnReg helps fintech navigate general solicitation requirements. Contact us to learn more →

Consequences of Violating General Solicitation Rules

Missteps around general solicitation are not just procedural. They carry real consequences. A single miscommunication can compromise an entire raise, even if the rest of the offering is compliant.

Improper solicitation can void the exemption entirely, forcing the company to register the offering with the SEC. That can lead to rescission risk, where investors have the right to demand their money back. In some cases, this forces companies to unwind the raise entirely.

There is also the risk of regulatory enforcement. The SEC or state securities regulators may impose fines, penalties, or restrictions on future fundraising activities. For regulated entities like broker-dealers or RIAs, this can trigger additional reviews from FINRA or other oversight bodies.

Reputational fallout is often harder to fix than technical missteps. Investors tend to pull back from raises that show signs of non-compliance, even if the legal risk is minimal. The same applies to banking partners or strategic allies. They often pass once a red flag appears. These concerns tend to surface during due diligence, which can complicate a round at the worst possible time.

Even without formal enforcement, prior violations may follow a company into future exams or audits. Regulators often revisit past communications, especially if fundraising language was vague or inconsistent. Explaining those decisions after the fact can slow things down and trigger more scrutiny.

For firms operating in regulated fintech verticals, that kind of exposure adds unnecessary operational strain.

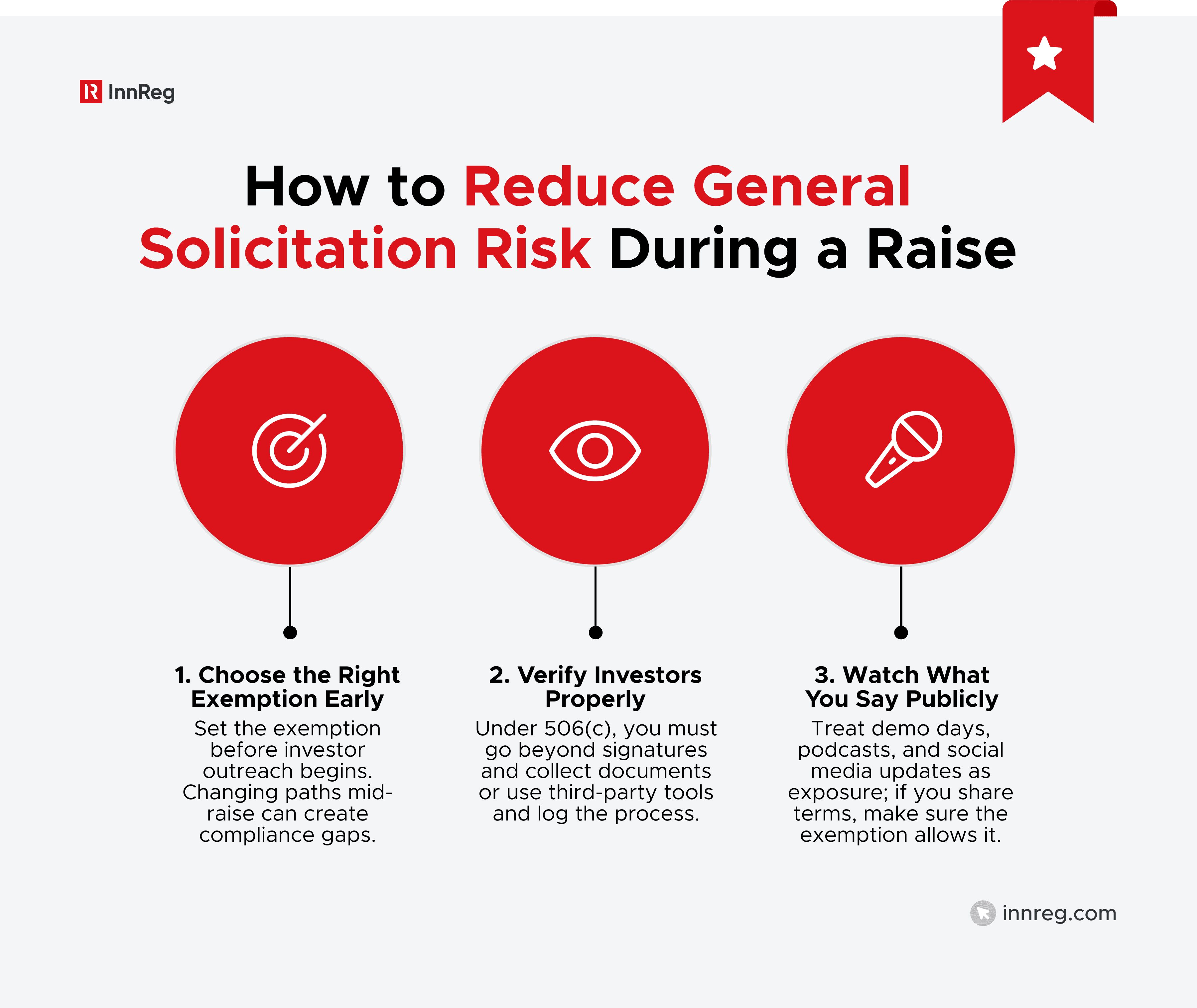

How to Mitigate the Risks of Non-Compliance When General Solicitation Is Involved

General solicitation becomes risky when companies fail to structure it properly. In fintech, where outreach spans public platforms, the real issue is not the exposure. It is how the team manages exemption rules, investor targeting, and messaging discipline.

Choosing the Right Exemption Early

The exemption must be determined before outreach begins. Each route (e.g., 506(b), 506(c), Reg CF, or Reg A) has different rules around general solicitation. Switching mid-raise is not just a process shift; it can trigger compliance issues.

For example, starting under 506(b) and later going public with the raise may invalidate the exemption. Moving to 506(c) after the fact brings new requirements that the original process may not meet.

It is far more effective to select the correct exemption at the outset. That way, everyone, from legal to marketing, can stay on track and build the process around the rules in play.

See also:

Investor Verification Best Practices

Investor verification under 506(c) is often misunderstood. A signature is not enough. The SEC expects a company to take real steps to confirm accredited status and to prove those steps if reviewed.

That means collecting documents or working with a trusted verification provider. Teams should log actions clearly. If audited, vague or missing records could cast doubt on the entire raise.

Handling Demo Days, Social Media, and Public Statements

Mentioning a raise during a live podcast or open event, even briefly, can create compliance issues if the content is later shared or posted publicly.

To manage that risk:

Do not disclose terms like pricing, valuation, or round size unless operating under an exemption that permits general solicitation.

Treat demo day pitches as exposure, not fundraising, unless the audience is controlled and the event qualifies for safe harbor.

Build a review process for social posts. Even brief updates (“We’re raising” or “Last chance to invest”) can cause problems.

Keep legal, marketing, and leadership teams in sync as messaging scales.

—

In fintech fundraising, general solicitation rules are not always intuitive, but the consequences of getting them wrong are very real.

Choosing the right exemption at the start, managing public messaging, and documenting investor verification are core to mitigating regulatory risks.

When in doubt, teams should pause, review, and realign before making public-facing statements.

InnReg was founded in 2013 by Francesco Matteini, former Chief Compliance Officer who helped launch and scale some of the most innovative digital broker-dealers over the last two decades. He built compliance programs to support the first zero-commission broker and the first BD-sponsored investor social network. Since its founding, InnReg has attracted highly experienced fintech consultants with long careers in compliance, risk management, and a deep understanding of the fintech industry.

How Can InnReg Help?

InnReg is a global regulatory compliance and operations consulting team serving financial services companies since 2013.

We are especially effective at launching and scaling fintechs with innovative compliance strategies and delivering cost-effective managed services, assisted by proprietary regtech solutions.

If you need help with crowdfunding compliance, reach out to our regulatory experts today:

Related Articles

Featured LinkedIn Posts