What Is FINRA? Understanding the US Broker-Dealer Regulator

If you’re building or growing a fintech business in the US, chances are you’ve come across FINRA. But what is FINRA, and why does it matter? Whether you’re launching a trading platform, expanding into securities, or trying to make sense of the regulations, this is one of the regulatory bodies you need to understand.

This article walks you through FINRA’s role, where it fits in the bigger US regulatory picture, and the types of firms it oversees. We’ll also look at its primary responsibilities, what broker-dealers need to do to mitigate risks, and some recent trends that show where FINRA is focusing its attention.

At InnReg, we help broker-dealers, ATSs, and investment platforms navigate FINRA membership and ongoing broker-dealer compliance, from licensing and registration to supervisory programs, Reg BI, AML, and surveillance workflows. Contact us to learn more.

What Is the Financial Industry Regulatory Authority (FINRA)?

The Financial Industry Regulatory Authority (FINRA) is a self-regulatory organization that oversees broker-dealers and their registered representatives in the US. Although it’s not a government agency, it operates as a membership-based body, funded through broker-dealer fees and fines from enforcement actions.

At its core, FINRA’s job is to protect investors and keep markets fair and orderly. It does this by writing and enforcing rules, examining firms, and offering resources to both businesses and the public.

These rules directly affect how broker-dealers operate day to day. For example, FINRA Rule 4530 covers reporting obligations, while Rule 2210 sets standards for communications with the public. Together, they highlight the breadth of FINRA’s oversight and why firms entering the securities space need to understand its role from the start.

How FINRA Fits Into the US Regulatory System

FINRA does not operate in isolation. It is part of a layered system of oversight that governs US financial markets.

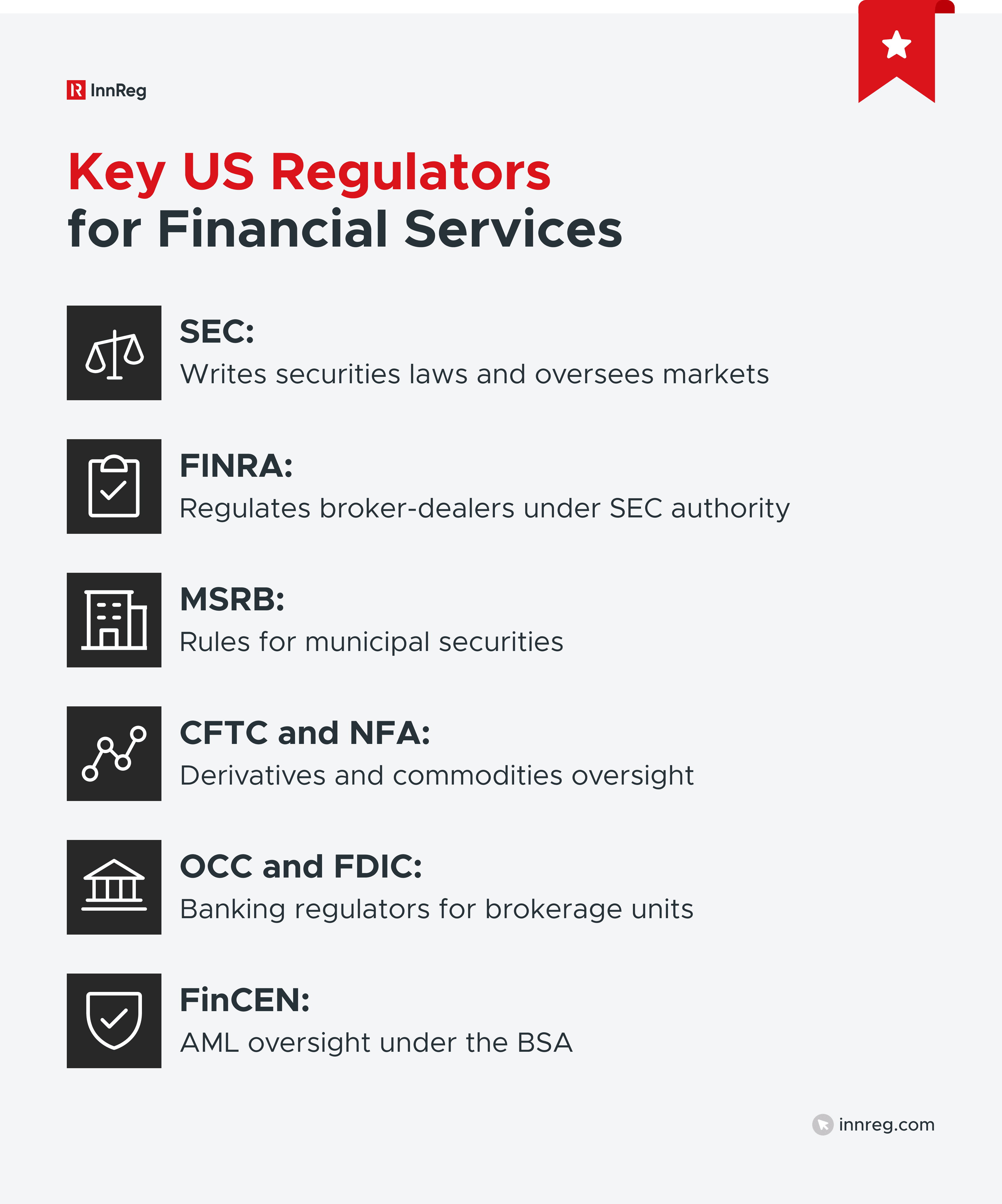

While FINRA regulates broker-dealers, it does so under the authority of the Securities and Exchange Commission (SEC), which must approve its rules and supervise its operations.

In practice, the main difference between FINRA and the SEC is that FINRA handles the day-to-day regulation of brokers, while the SEC sets wider securities laws and market standards. For example, the SEC establishes capital requirements and disclosure rules, and FINRA checks that firms are following them.

Depending on the business model, other regulators may also come into play. A broker-dealer offering municipal securities would follow rules from the Municipal Securities Rulemaking Board (MSRB). Firms trading futures or commodities fall under the Commodity Futures Trading Commission (CFTC) and the National Futures Association (NFA). Banks that run brokerage units may also be supervised by the OCC or the FDIC.

For fintech companies, this overlapping system can feel like a maze, and a business that combines securities with payments or crypto may find itself answering to several regulators at once. The best way to approach it is by first understanding where FINRA’s role begins and ends, then looking at how agencies such as the SEC or FinCEN might also apply.

FINRA vs. SEC

The SEC and FINRA both oversee the securities industry, but they do so in different ways. The SEC sets the big-picture rules: it writes securities laws, oversees public companies, and regulates exchanges and investment advisors.

FINRA’s role is narrower. It applies those rules to broker-dealers on a day-to-day basis, checking how firms supervise their business, communicate with clients, and handle conflicts of interest. A good example is Regulation Best Interest (Reg BI). The SEC introduced the rule, and FINRA now reviews how broker-dealers apply it in practice.

For firms, this split means compliance is shared. The SEC may bring the headline enforcement cases, but FINRA examiners are usually the ones reviewing records, testing supervisory systems, and flagging issues during routine exams.

Read more about the differences between FINRA and the SEC →

Other Regulators Fintech Firms May Encounter

Some of the main regulators fintech firms may encounter include:

Municipal Securities Rulemaking Board (MSRB): The MSRB sets rules for broker-dealers and banks that underwrite, trade, or sell municipal securities. These rules cover areas such as disclosure, fair dealing, and advertising in the municipal market. Enforcement is handled by FINRA and the SEC, so a fintech offering municipal bond trading services would need to follow MSRB standards alongside FINRA requirements.

Commodity Futures Trading Commission (CFTC): The CFTC oversees derivatives markets, including futures, options, and swaps. Its role becomes vital when fintech firms build platforms for digital asset derivatives or trading strategies linked to commodities. Working alongside the CFTC is the NFA, its self-regulatory partner, much like FINRA’s relationship with the SEC. Firms active in derivatives or crypto-related futures may therefore be regulated by both the CFTC and the NFA, in addition to FINRA.

Banking Regulators (OCC, FDIC, Federal Reserve): When a fintech partners with a bank or operates within a bank holding company, banking regulators may also become involved. The OCC supervises national banks, the FDIC oversees insured depository institutions, and the Federal Reserve regulates bank holding companies. If broker-dealer activity is tied to a banking entity, firms often need to coordinate across all three regulators.

Financial Crimes Enforcement Network (FinCEN): FinCEN administers the Bank Secrecy Act (BSA) and is responsible for anti-money laundering (AML) oversight across financial services. Any fintech that handles customer funds has to meet BSA requirements, which include customer due diligence, suspicious activity reporting, and recordkeeping. Even FINRA-registered firms must keep AML programs in place that meet FinCEN’s standards.

Who Must Register with FINRA

Firms that act as broker-dealers must register with FINRA. This includes businesses that buy or sell securities for customers or for their own accounts. Individuals who work directly with clients or make recommendations, known as “associated persons,” also need to register by passing qualification exams such as the Series 7 or Series 6.

Examples include online trading platforms that let customers trade stocks and ETFs, firms that handle orders for retail clients, and market makers. FINRA oversees all of them, and that means they need to be registered. But registration isn’t just about filling out forms. Firms also have to put solid supervisory systems in place, meet financial requirements, and prove they’re ready to run their business responsibly.

Need to register as a broker-dealer? InnReg provides end-to-end support with applications, supervisory systems, and compliance programs.

How This Differs from Investment Advisors and Other Entities

FINRA regulates broker-dealers, but not every financial services firm falls into that category.

Investment advisors, for example, are regulated by the SEC or state securities regulators and typically charge fees for advice or asset management rather than commissions on trades. Although they are not FINRA members, some employees may need FINRA licenses if they also handle brokerage activities, along with state licenses if they provide investment advice. Other firms outside FINRA’s scope include futures and commodities firms, payment processors and money transmitters, and lending platforms.

For fintechs, the boundaries aren’t always clear. A company might have a brokerage arm that needs FINRA registration, while also running an advisory or payments division that falls under other regulators. Knowing exactly where FINRA’s oversight starts and stops helps founders avoid costly compliance missteps and sets them up to build a smarter regulatory strategy from day one.

What Does FINRA Do?

FINRA’s responsibilities go beyond writing rules. It is involved in licensing, supervision, monitoring, and enforcement.

1. Licensing and Registration

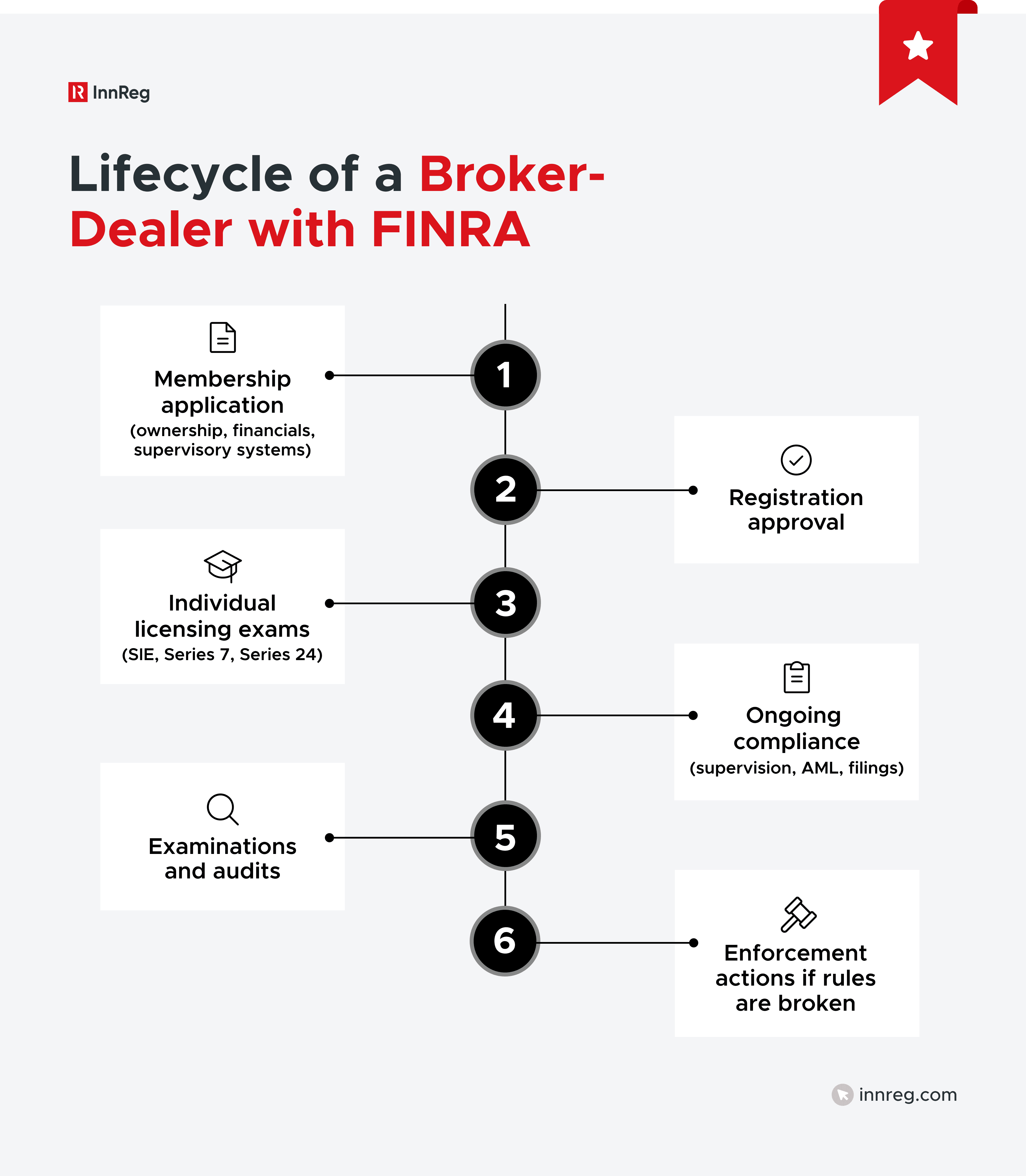

FINRA controls the gateway into the brokerage industry. Any firm that wants to operate as a broker-dealer must go through FINRA’s membership application, which asks for detailed information about ownership, financial condition, business plans, and supervisory systems. The goal is to confirm that a firm is ready to operate responsibly and follow the rules.

It is not only about the firm itself. Individuals who work for broker-dealers also need to register with FINRA. This involves passing qualification exams that show they understand securities products, regulations, and professional duties. Once licensed, they must keep their registrations active through ongoing education.

For fintech founders, licensing can be especially challenging if the team doesn’t yet include registered professionals. In those cases, firms often bring in experienced hires or partner with outsourced compliance experts like InnReg to meet FINRA’s requirements.

2. Rulemaking and Supervision

FINRA creates and enforces a detailed rulebook that guides how broker-dealers operate. The rules touch on everything from sales practices and conflicts of interest to trading standards, advertising, and client communications. A key example is FINRA Rule 3110, which requires firms to establish and maintain supervisory systems that are appropriate for their business.

Supervision is also a central expectation. Every member firm must adopt written supervisory procedures (WSPs) that match its business model and risks. These procedures should explain how the firm supervises its securities activities, monitors employee conduct, reviews and approves accounts, and spots potential violations.

3. Examinations and Audits

FINRA regularly examines broker-dealers to check how well they follow both its rules and federal securities laws. These reviews can be broad, looking at a firm’s financial, operational, and supervisory systems. They can also be more focused, depending on the risks FINRA sees in a particular business.

Common focus areas include:

Anti-Money Laundering (AML): Does the firm have a program that detects and reports suspicious activity? Does the firm test its AML program?

Cybersecurity: Are controls in place to protect sensitive client data and trading systems? Learn more in our guide about the FINRA cybersecurity checklist →

Books and Records: Are the firm’s records accurate, current, and retained according to regulatory standards?

Suitability and Reg BI: Are recommendations in line with client profiles and in the clients’ best interest?

Examinations often identify deficiencies that require remediation. For startups, these exams can be resource-intensive, especially if compliance functions are not well integrated into operations.

4. Enforcement and Disciplinary Actions

When firms or individuals break the rules, FINRA can step in with disciplinary action. Penalties can range from fines and suspensions to expulsion from membership or even permanently barring someone from the industry. These rules apply to firms of every size, not just the big Wall Street players.

Because enforcement is such a powerful tool, FINRA sets its priorities based on where it sees the most significant risks in the market. In recent years, the focus has been on Reg BI, gaps in AML programs, and recordkeeping problems, especially around digital communications.

A good example that shows the scope of FINRA is Rule 2010, which requires firms and their representatives to uphold high standards of commercial honor and fair trade. The rule is broad, but it is often used as the foundation for disciplinary cases, showing how FINRA can apply general principles in practice.

5. Market Surveillance

Beyond rulemaking and enforcement, FINRA also monitors trading activity across US markets. Its surveillance systems review billions of trades each day to spot potential manipulation, insider trading, or abusive practices.

This responsibility connects directly to broker-dealer obligations. Firms are required to submit accurate trade reports, which FINRA then uses to flag unusual activity. For example, under Rule 6110, firms must report equity trades that are outside of traditional exchanges. By analyzing this data, FINRA can identify patterns like spoofing or layering and take action when necessary.

For firms, this means market surveillance is not something happening in the background. Every trade and every report contributes to FINRA oversight, making accurate reporting and transparent practices critical for compliance.

6. Dispute Resolution and Arbitration

Most broker-dealer customer agreements require dispute resolution through FINRA arbitration instead of court. Arbitration is usually faster and less expensive than litigation, but the outcomes are binding and can carry serious financial consequences.

FINRA provides a panel of arbitrators and mediators to handle disputes involving customers, firms, and brokers. The process follows a formal code of procedure, and a court can enforce the awards. For firms, this also means disputes are not hidden from view, as certain disputes are disclosable and arbitration outcomes can become part of a broker’s public record.

7. Investor Education Tools

Beyond regulation and enforcement, FINRA provides tools for investors. BrokerCheck allows the public to research brokers and firms, including past disciplinary history. FINRA also publishes alerts on fraud schemes, educational materials on investment basics, and calculators for common financial decisions.

These resources serve two purposes: helping investors make informed choices and reinforcing confidence in regulated markets. For firms, the transparency created by BrokerCheck means reputational risks are high, as disciplinary actions and customer complaints are publicly visible.

See also:

Key FINRA Compliance Requirements for Broker-Dealers

Once a firm becomes a FINRA member, compliance is an ongoing obligation that touches almost every aspect of operations. The requirements below highlight where broker-dealers must focus resources and expertise.

Requirement | What It Means | Why It Matters |

|---|---|---|

Membership and Qualification Exams | Firms submit detailed applications; individuals must pass qualification exams | Verifies firms and reps are competent before operating |

Written Supervisory Procedures (WSPs) | Firms develop and maintain supervisory procedures aligned to comply with the rules and manage business risks | Guidance for firm processes and creates accountability |

AML Programs | Policies, AML officer, training, annual testing | Detects money laundering and reports suspicious activity |

Net Capital Rules | Maintain minimum liquid assets; FinOp oversight | Protects customers and promotes financial stability |

Communications Rules (2210) | Ads and client materials must be fair and not misleading | Protects investors from bad information |

Reg BI and Suitability | Must act in clients’ best interests when providing recommendations | Raises the bar for client protection |

Reporting and Disclosures | Timely and accurate filings (CRD, TRACE, CAT, etc.) | Allows regulators to conduct surveillance and promotes transparency with investors |

Need help with broker-dealer compliance?

Fill out the form below and our experts will get back to you.

1. Membership and Qualification Exams

Joining FINRA is not just a formality. Firms seeking membership must submit a detailed application that covers ownership, business lines, supervisory systems, and financial condition. The review process can take months and often involves multiple rounds of questions from FINRA staff. Approval signals that the firm has the structure and resources to operate within the regulatory framework.

Individuals also face qualification requirements. The entry point is the Securities Industry Essentials (SIE) exam, which covers basic industry knowledge. From there, representatives take more specific exams, such as the Series 7 for general securities (or the Series 6 for mutual funds and variable annuities). Passing these exams is a requirement for obtaining a registration to sell securities.

2. Written Supervisory Procedures (WSPs)

Every FINRA member must develop and maintain WSPs. These documents explain how the firm supervises employees, reviews customer accounts, and monitors trading activity. They form the backbone of a compliance program.

To be effective, WSPs must reflect the realities of the business. A retail brokerage might focus on suitability reviews and Reg BI compliance, while an institutional firm might emphasize market access controls and trade reporting. Regulators expect this kind of alignment, and FINRA examiners often test whether a firm’s daily practices match what is written in its procedures.

3. Anti-Money Laundering (AML) Programs

Broker-dealers must comply with the BSA and FINRA rules that require firms to establish an AML program. The program must be in writing, approved by senior management, and designed to identify and report suspicious activity.

An effective AML program includes several required elements:

Policies and procedures that address customer due diligence, monitoring, and reporting.

A designated AML officer with authority and responsibility for oversight.

Training for employees on recognizing red flags and reporting obligations.

Independent testing of the program, conducted annually, to confirm it is operating as intended.

Firms must decide what monitoring systems to use, how to escalate unusual activity, and when to file SARs. The complexity grows when firms handle higher-risk products or clients, such as cross-border accounts or digital assets.

4. Net Capital and Financial Responsibility Rules

Broker-dealers must follow strict financial requirements to protect customers and support market stability. One of the most important is the SEC’s Net Capital Rule (Rule 15c3-1), which requires firms to maintain a minimum level of liquid assets relative to their liabilities. This rule prevents firms from becoming over-leveraged and unable to meet obligations to clients.

FINRA enforces these requirements by reviewing filings and testing them during examinations. Errors in calculations or recordkeeping are common, particularly for firms without experienced financial staff. To mitigate this risk, every broker-dealer must appoint a Financial and Operations Principal (FinOp), licensed through the Series 27 or Series 28 exam, to oversee financial compliance.

5. Communications and Advertising Rules (Rule 2210)

FINRA Rule 2210 sets the standards for how broker-dealers communicate with the public, and applies to advertising, marketing, websites, social media, and client correspondence. The central principle is that all communications must be fair, balanced, and not misleading.

The rule places communications into three categories: retail, correspondence, and institutional. Each category has its own review and recordkeeping requirements. For example, retail communications often need advance approval from a registered principal.

For fintech firms, digital channels add extra complexity. Social media posts, app notifications, and text messages can all fall under Rule 2210, and firms are expected to capture and retain these records. Because of this, technology choices for messaging, archiving, and monitoring are a critical part of building a reliable compliance program.

Looking for clarity on compliance and advertising terms? Check out InnReg’s Compliance Glossary for Fintech Marketing to support your compliance program.

6. Sales Practice Standards and Reg BI Obligations

Broker-dealers have long been required to recommend only investments that are suitable for their clients, taking into account factors such as age, financial situation, investment objectives, and risk tolerance.

In 2020, the SEC raised this standard with Regulation Best Interest. Under Reg BI, broker-dealers must act in the client’s best interest when making recommendations, not simply provide a suitable option. Compliance goes beyond product selection. It also involves managing and disclosing conflicts of interest, providing clear disclosures about fees and services, and documenting the reasoning behind each recommendation.

See also:

7. Reporting and Disclosure Duties

FINRA requires broker-dealers to report significant events and keep accurate records through systems such as the Central Registration Depository (CRD). This includes disclosures about customer complaints, arbitration claims, regulatory actions, bankruptcies, and certain criminal or civil proceedings.

For individuals, updates are filed through Form U4 when registering and Form U5 when leaving a firm. Firms also update Form BD when ownership or business operations change. These filings feed into BrokerCheck, which is publicly available to investors and regulators.

Ongoing reporting goes beyond registration details. Broker-dealers must also submit financial reports, transaction data, and trade activity through systems such as TRACE for fixed-income securities and CAT for equities. Errors or omissions in these filings often lead to exam findings or disciplinary action.

Recent FINRA Developments and Trends

FINRA’s rules are well established, but its priorities shift with market conditions. In recent years, it has focused on new technologies, investor protection, cybersecurity, and legal challenges to its authority. For broker-dealers and fintech firms, keeping up with these changes is critical because they directly affect how FINRA reviews compliance programs in exams and enforcement actions.

2025 Supreme Court Case Reaffirming FINRA’s Authority

In June 2025, the US Supreme Court declined to hear a challenge questioning whether FINRA has constitutional authority to discipline member firms. The case stemmed from a broker-dealer arguing that FINRA, as a private self-regulatory organization, should not be allowed to wield quasi-governmental enforcement powers.

By refusing to take the case, the Court left in place lower court rulings that upheld FINRA’s authority. This decision also reinforced the self-regulatory model that has governed broker-dealers for decades.

For compliance officers and fintech founders, the outcome is significant. It confirms that FINRA remains the front-line regulator for broker-dealers, and firms cannot rely on legal challenges to weaken its enforcement reach. Instead, the focus should remain on preparing for examinations, monitoring regulatory updates, and maintaining compliance programs that align with FINRA’s expectations.

Reg BI Enforcement Ramp-Up

Since Regulation Best Interest (Reg BI) took effect in 2020, FINRA has steadily increased its focus on how broker-dealers apply it. By 2023, Reg BI was one of the most common issues in FINRA enforcement. This rule goes beyond the old suitability standard by requiring firms to put the client’s best interest first.

For fintech platforms, Reg BI presents additional challenges. Digital interfaces and algorithms that guide clients toward certain products can be considered recommendations under the rule. This means compliance must cover both human advisors and automated systems, including disclosure practices, conflict management, and decision documentation.

Enforcement cases are also public, and firms facing Reg BI violations often appear in FINRA’s disciplinary reports. That’s why it’s necessary to follow how enforcement trends develop over time.

Crypto Asset Guidance for Broker-Dealers

As crypto and digital assets move closer to mainstream finance, FINRA has been issuing guidance on how broker-dealers can engage in this space. The regulator’s stance is cautious: crypto assets that qualify as securities fall under federal securities laws, and broker-dealers handling them must comply with the same rules that apply to traditional securities.

Firms need to evaluate whether a digital asset is a security, update supervisory and AML programs to address risks like volatility and cross-border transfers, and seek approval for activities such as custody or trading. Hybrid models that mix securities with crypto can also trigger state money transmitter requirements, adding another layer of compliance.

AI and Algorithmic Supervision Concerns

FINRA is paying closer attention to how broker-dealers use AI and algorithms. Recommendation engines that steer clients toward certain products may count as recommendations under Reg BI, while automated trading models raise broader concerns about supervision, risk controls, and market integrity.

Generative AI adds another layer of risk when used for marketing or client interactions. Content created this way still needs review, approval, and retention. FINRA expects firms to connect these practices to broader operational requirements such as FINRA Rule 4370 on business continuity and preparedness.

Although there are no AI-specific rules, FINRA has made clear that existing frameworks apply. Firms should document how their systems function, track potential conflicts, and assign clear responsibility for oversight.

Cybersecurity and Fraud Focus

Cybersecurity has become one of FINRA’s highest priorities because broker-dealers handle sensitive client data and trading systems. Examinations now look closely at how firms protect data, oversee vendors, prepare for incidents, and train employees. FINRA treats weak controls as compliance failures, not just technology gaps.

This focus is closely tied to fraud prevention. FINRA has highlighted risks such as imposter websites, account takeovers, and microcap stock schemes. Under Rule 3110, firms are expected to implement monitoring for these risks directly into their supervisory systems.

For fintech startups, the challenge is twofold. Strong technical defenses are essential, but regulators also expect those controls to be documented in supervisory procedures and tested regularly.

Recordkeeping Crackdowns on Messaging Apps

FINRA and the SEC have recently fined firms heavily for failing to capture business communications on unapproved channels such as text messages and WhatsApp. Without proper retention systems, these conversations violate books and records rules.

These enforcement actions have totaled hundreds of millions of dollars and have involved both large institutions and smaller broker-dealers. Regulators expect every firm to define which channels are allowed, apply monitoring, and keep complete records of business communications.

For fintech firms, the challenge is even greater because client interactions often take place in apps or chat platforms. Recordkeeping, therefore, cannot be an afterthought. Approved channels, reliable archiving, staff training, and periodic reviews all need to be part of the design from the very beginning.

Shifts in Continuing Education and Exams

FINRA has modernized its licensing and education framework to keep pace with industry changes. One major update was the introduction of the SIE exam, which anyone can take before joining a broker-dealer. This creates a broader pool of candidates who already have baseline industry knowledge.

Continuing education has also shifted from a three-year cycle to annual training. Content now reflects emerging risks such as cybersecurity, Reg BI, and digital assets. Firms must track completion, while supervisors have their own training requirements to maintain registrations.

FAQs About FINRA

Is FINRA a government agency?

No. FINRA is a self-regulatory organization (SRO), not a government agency. It operates under the supervision of the SEC, which approves its rules and oversees its enforcement. FINRA is funded by member fees and fines, not taxpayer dollars.

What’s the difference between FINRA and the SEC?

The SEC is a federal regulator that writes and enforces securities laws across markets. FINRA’s focus is narrower: it oversees broker-dealers and their representatives, verifying they comply with both SEC rules and FINRA’s own rulebook.

For a detailed comparison of these two regulators, read our complete guide: FINRA vs. SEC: 7 Key Differences in What They Regulate

What are the limits of FINRA’s authority?

FINRA regulates only broker-dealers and their associated persons. It cannot bring criminal charges or regulate investment advisers, banks, or futures firms. For criminal or civil cases, FINRA refers matters to the SEC or other authorities.

Do all financial firms need to register with FINRA?

No. Only firms that buy, sell, or recommend securities for clients must register. Investment advisors, lenders, and money transmitters generally fall under other regulators such as the SEC, CFPB, or state agencies.

How does FINRA protect investors?

FINRA protects investors by licensing brokers, writing rules, conducting exams, and bringing enforcement actions against firms and individuals that break them. It also provides tools like BrokerCheck so investors can review a firm or broker’s history before doing business.

How can investors check if a broker is registered?

Investors can search FINRA’s BrokerCheck database, which lists brokers’ employment history, licenses, and any disciplinary records. This tool is free and publicly accessible on FINRA’s website.

Does FINRA regulate cryptocurrencies or digital assets?

Only when a digital asset is considered a security. In that case, broker-dealers handling it must comply with FINRA and SEC rules. Activities like custody, placement, or trading of crypto securities require specific approvals.

—

FINRA’s oversight shapes how broker-dealers are licensed, supervised, examined, and disciplined, making it a key part of the US financial system. For fintech firms, understanding where FINRA fits and what it requires is essential for building compliant operations and protecting long-term growth.

As the market evolves with crypto, AI, and new business models, FINRA’s priorities are shifting too. Staying ahead of these changes helps firms reduce risk and prepare for examinations and enforcement. For fintech founders, taking the time to map out where FINRA applies and where other regulators step in can make all the difference in turning compliance into a competitive advantage.

Tarik is a Principal Compliance Consultant at InnReg with over 5 years of experience advising fintech clients across broker-dealer, RIA, and money transmitter verticals. He holds FINRA Series 3, 7, 24, 57, 63, 79, and 99 licenses, with expertise in regulatory strategy, supervisory systems, and compliance roadmap implementation.

How Can InnReg Help?

InnReg is a global regulatory compliance and operations consulting team serving financial services companies since 2013.

We are especially effective at launching and scaling fintechs with innovative compliance strategies and delivering cost-effective managed services, assisted by proprietary regtech solutions.

If you need help with broker-dealer compliance, reach out to our regulatory experts today:

Related Articles

Featured LinkedIn Posts