What Is an NFT? A Regulatory and Business Guide for Fintechs

Key Takeaways

An NFT is a unique digital token recorded on a blockchain that can represent ownership, access rights, credentials, or interests in digital and real-world assets.

NFTs are not automatically exempt from regulation, and their legal treatment depends on how they function, are marketed, and are used within a product or platform.

An NFT may be treated as a security if it is sold with an expectation of profits, tied to business performance, or structured around shared ownership or investment returns.

NFT platforms can trigger money transmission, AML, sanctions, or custody obligations when they facilitate transactions, control assets, or handle user funds.

Common fintech uses for NFTs include digital identity, token-gated access, rewards programs, proof of ownership, and the representation of real-world assets.

Fintech companies should evaluate NFT products for securities, money transmission, consumer protection, sanctions, and custody risks before launch, as compliance obligations are driven by function rather than technology.

What is an NFT, and why does it matter to fintechs navigating compliance? While the non-fungible token (NFT) market first drew attention from digital art and collectibles, fintech innovators have begun to explore its broader applications in investment products, rewards systems, identity, and more.

But innovation in this space doesn’t mean exemption from regulation. When NFTs intersect with financial use cases, they may fall under securities laws, money transmission requirements, or AML obligations. The same technology that powers new business models also raises complex compliance questions for founders, lawyers, and regulators alike.

This guide breaks down what fintech leaders need to know about NFTs. If you want to learn about the regulatory aspects surrounding NFTs, keep reading!

At InnReg, we help fintechs integrate NFTs into products with a practical compliance approach. We support regulatory strategy, licensing, AML program buildouts, and day-to-day compliance operations.

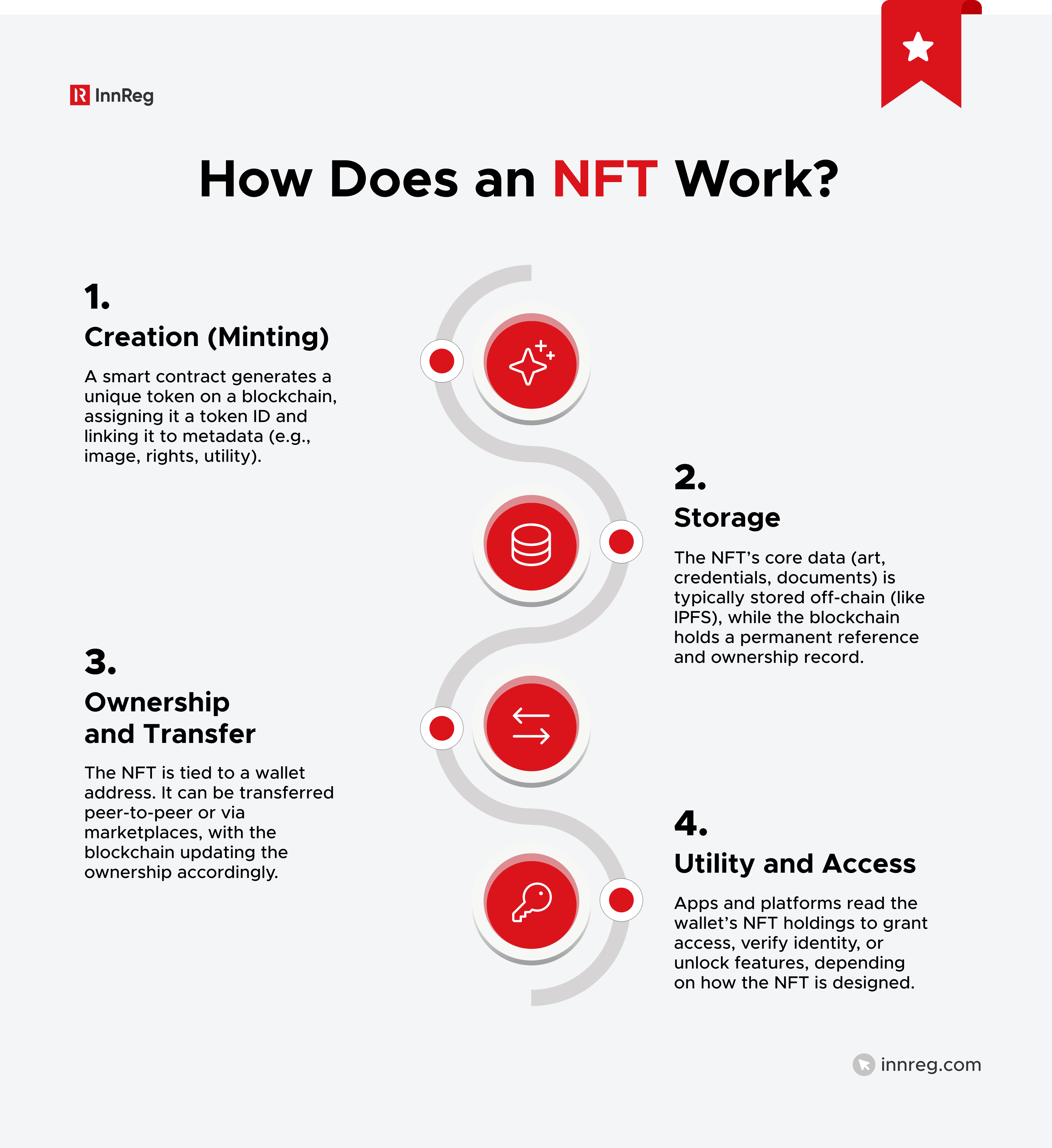

What Is a Non-Fungible Token?

A non-fungible token (NFT) is a digital asset that represents ownership of a unique item or record on a blockchain. Unlike cryptocurrencies, which are interchangeable on a 1:1 basis, NFTs are distinct and cannot be exchanged for one another at equal value. Each token contains identifying information that makes it non-fungible, hence the name.

Most NFTs are built on smart contract platforms like Ethereum. They can link to digital files (art, documents, credentials) or real-world assets (property, physical goods, event tickets). The NFT itself does not always contain the asset; it typically points to it, often via metadata or an off-chain link.

In fintech and financial services, NFTs have moved beyond novelty. They're being used for:

Identity verification

Investor access tiers

Fractional ownership models

As the functionality expands, so does the likelihood that regulators will view certain NFTs as financial instruments rather than just digital collectibles.

Common NFT Business Models

Not all NFTs are built alike. Fintech companies exploring this space need to understand how NFT business models differ because the structure affects regulatory exposure. The NFT you’re issuing or integrating might look simple on the surface, but could carry hidden compliance obligations depending on how it's used.

Here are the most common NFT business models seen in fintech and financial-adjacent sectors:

Model Type | Description |

|---|---|

NFT Issuers | Creators minting and distributing NFTs, often tied to brand, access, or perks |

NFT Marketplaces | Platforms facilitating NFT sales, auctions, or trades between third parties |

NFT-Enabled Products | Fintechs embedding NFTs into user-facing apps, games, or wallets |

NFT Financialization | Use of NFTs for staking, lending, or fractional ownership models |

Custodial Models | Platforms managing NFTs on behalf of users, holding keys and assets directly |

Non-Custodial Models | Systems that leave NFT custody fully in the user’s wallet or an external service |

Each of these models carries different operational and regulatory implications. Here is an in-depth guideline on the different models and what they mean on the regulatory fronts:

NFT Issuers

NFT issuers are at the front line of regulatory scrutiny. These are the businesses or individuals who create, mint, and distribute NFTs, often to users, investors, or customers. Whether the NFTs are tied to art, access, digital rights, or tokenized value, what matters legally is how the issuance is structured and presented.

Regulators tend to evaluate:

What the NFT conveys (e.g., rights, utility, financial upside)

How it’s marketed (e.g., speculative language or passive income claims)

Who it’s offered to (general public vs. accredited users)

Whether the issuer retains control post-sale

Issuers who promote NFTs as appreciating assets, or tie them to company performance, may trigger securities regulations, especially under the Howey test. Likewise, if the NFT represents a fractional interest in an underlying asset (like a revenue stream, artwork, or real estate), it may be treated as a security, even if the token itself is non-fungible.

Marketing language is a high-risk zone. Statements that imply future profits, liquidity, or investor benefits can reframe an otherwise neutral non-fungible token into a regulated instrument.

If your fintech is issuing NFTs as part of a rewards, membership, or investment product, it's critical to review the entire customer journey: from the whitepaper and website to user onboarding and post-sale communications.

At InnReg, we’ve worked with fintechs that bring complex concepts to market like stock-plus-crypto hybrids or tokenized real-world assets. What makes those launches viable is a grounded regulatory framework, not a speculative roadmap.

NFT Marketplaces and Platforms

NFT marketplaces play a central role in facilitating the buying, selling, and trading of NFTs, but operating a marketplace is not legally neutral. Depending on how the platform is structured and how transactions flow, it may fall within the scope of money transmission, securities exchange, or other regulated activities.

The core compliance questions come down to:

Does the platform custody user funds or assets?

Does it set terms, pricing, or match buyers and sellers?

Does it handle fiat, crypto, or both in NFT transactions?

Are secondary market trades supported or incentivized?

If a platform touches user funds even momentarily, it could be viewed as a money transmitter under FinCEN rules. This applies whether the funds are in dollars, crypto, or both. Marketplaces that support NFT-for-crypto exchanges (e.g., ETH for an NFT) may also fall into virtual asset service provider (VASP) categories, especially in international jurisdictions.

Some platforms opt for a non-custodial model where trades happen wallet-to-wallet. That can reduce certain obligations, but it doesn't eliminate risk. Smart contract vulnerabilities, enforcement actions, and state-by-state licensing rules (especially in New York and California) may still apply.

For fintechs looking to integrate or white-label NFT marketplaces, compliance must be part of vendor due diligence. Even if your company isn’t running the backend, your brand could be implicated if the platform mishandles AML, sanctions, or customer funds.

Learn about the requirements surrounding the New York Money Transmitter license →

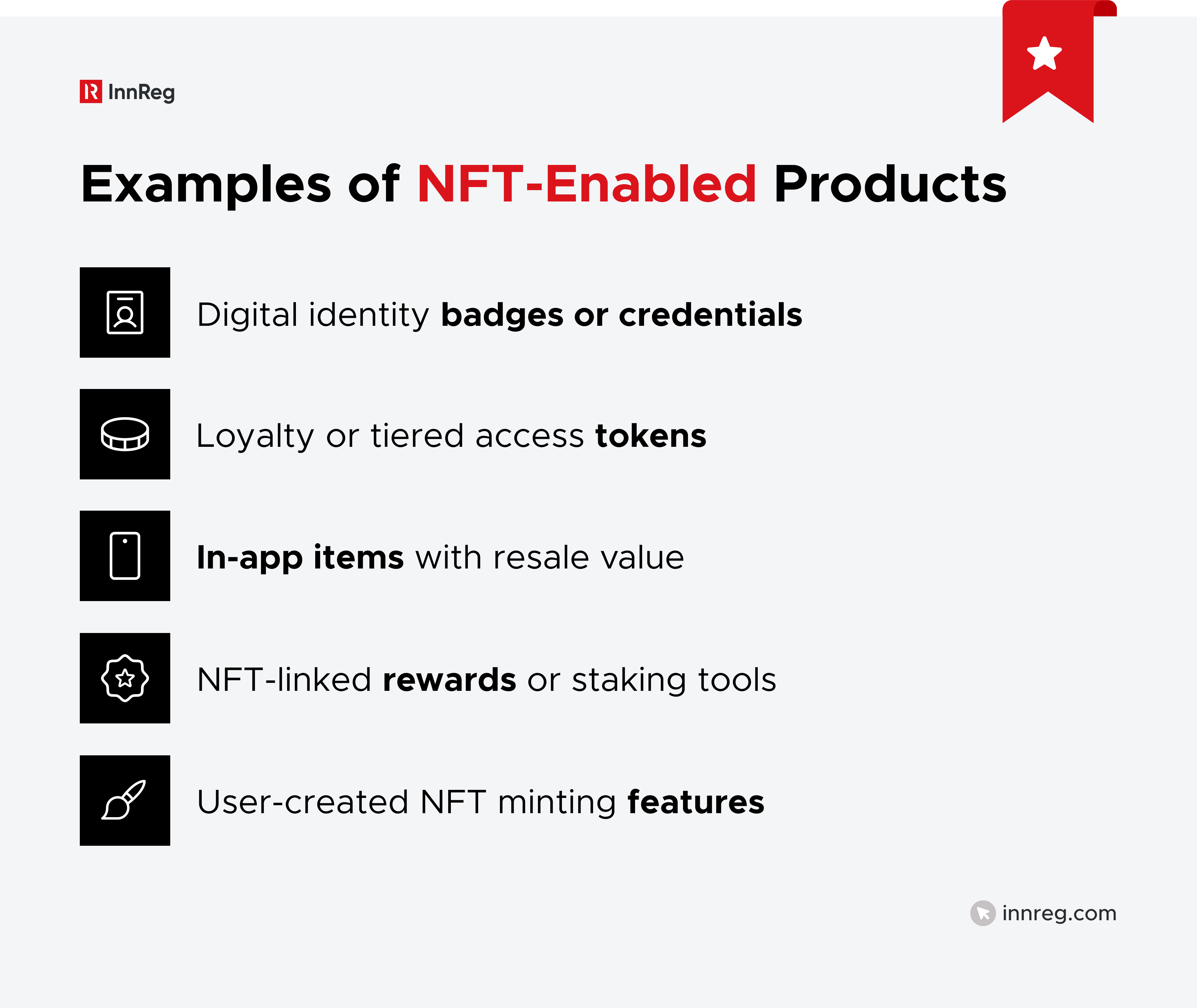

NFT-Enabled Products

Some fintechs are not issuing or selling NFTs directly, but they’re building products that integrate NFTs into broader user experiences. These may include digital wallets, mobile apps, investment platforms, or games where NFTs are embedded as functionality, rewards, or identity assets.

This “middle layer” is often where compliance gets overlooked. Teams treat NFTs as UI features rather than financial elements. But embedding NFTs into a financial product introduces new risk vectors, especially if those NFTs hold value, are tradable, or interact with tokens or user balances.

If your app allows users to mint, transfer, or exchange NFTs, you may be responsible for transaction monitoring, KYC, and jurisdictional screening even if you don’t touch the asset directly. The logic is simple: if your platform facilitates financial activity, regulators will ask how you're controlling it.

From a compliance standpoint, NFTs can behave like mini financial instruments, even when wrapped in entertainment or engagement layers. That’s why reviewing product flows, permissions, and user interfaces is key before rollout.

NFT Financialization Models

As the NFT space matures, some fintechs are developing financial products around NFTs, not just using them as access tokens or collectibles. These models include lending against NFTs, staking NFTs for rewards, and offering fractionalized NFT ownership to groups of users.

In these cases, the NFT is the wrapper for a financial activity. And that changes everything from a compliance standpoint.

Examples of financialized NFT models:

Fractional NFTs: Dividing a single NFT into fungible shares

NFT-backed loans: Using NFTs as collateral for lending arrangements

NFT staking: Locking NFTs in a protocol in exchange for yield or access

NFT index products: Bundling NFTs into a structured asset for trading or exposure

These models carry a much higher risk of being treated as securities or investment contracts. If your platform offers fractional interests or pools investor funds around NFTs, you're likely touching securities regulation. And if the NFTs are used to generate yield or profit, you may also trigger registration or licensing obligations depending on jurisdiction.

Smart contracts are often used to facilitate these models, but code doesn't eliminate legal risk. If the product invites speculation or represents shared ownership in a revenue-generating asset, regulators may view it like a fund or security, even if it’s packaged as “just an NFT.”

Custodial vs. Non-Custodial NFT Models

How a platform handles NFT custody is a core design decision with direct regulatory consequences. Custody shapes how regulators view your role in the transaction and the corresponding compliance obligations.

In a custodial model, the platform holds the NFTs (or the private keys controlling them) on behalf of users. This means the business has ongoing access to user assets and may be responsible for:

Safeguarding user property

Managing transfers and access permissions

Implementing loss and dispute protocols

Meeting licensing requirements in some states or jurisdictions

By contrast, non-custodial platforms leave full control of NFTs with the user. Transactions happen wallet-to-wallet, often with smart contracts automating transfers. While this reduces some licensing risk, it doesn’t eliminate broader compliance concerns like KYC, sanctions, or fraud monitoring.

The key question regulators ask is: who controls the asset at key points in the transaction flow? If the answer is “the platform,” that control likely brings additional oversight, including state money transmission laws or international VASP standards.

See also:

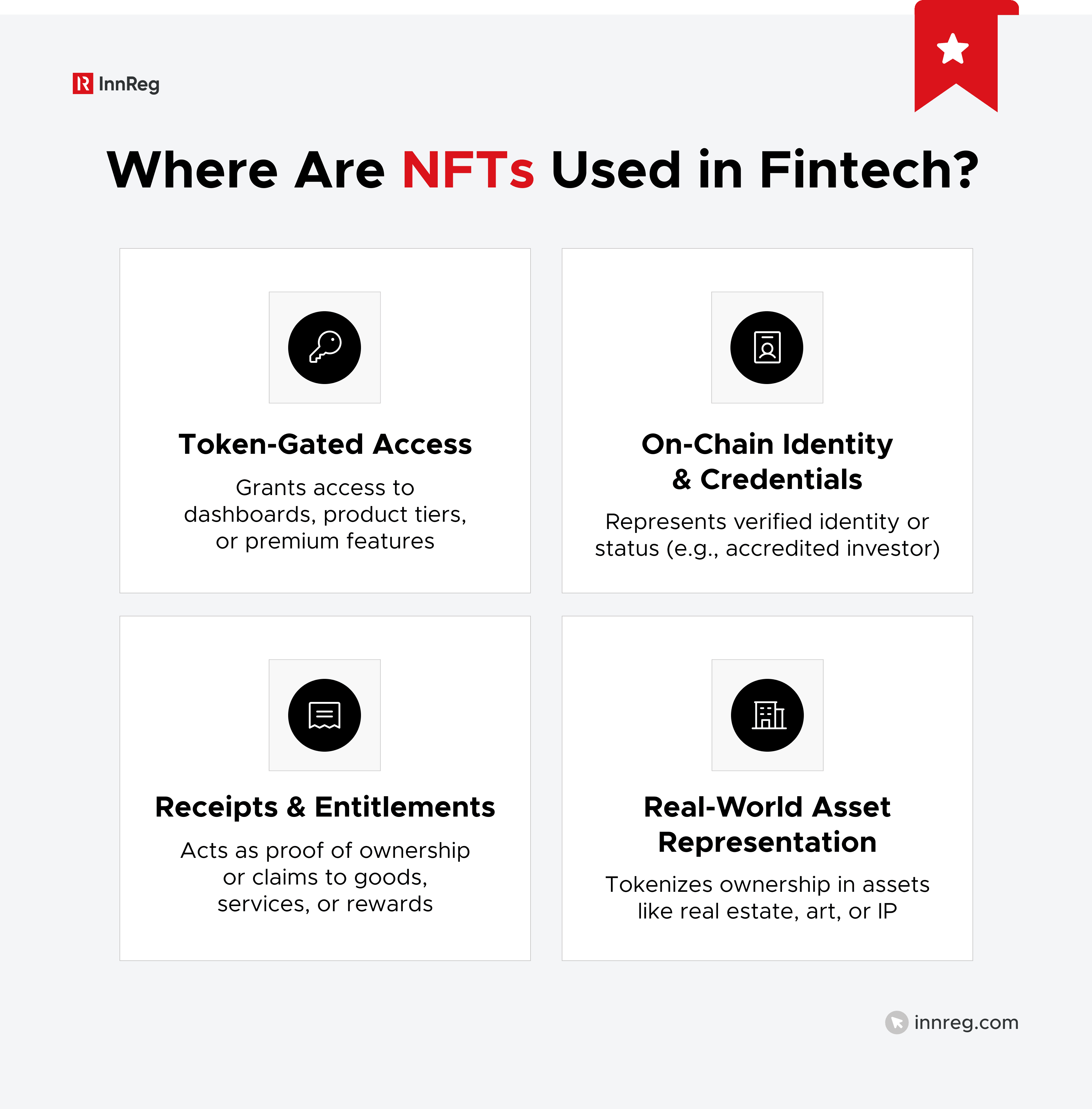

How NFTs Are Used in Financial Services and Fintech

NFTs are finding functional roles in financial services, often quietly powering back-end infrastructure or enhancing user-facing features. While not every use case raises regulatory red flags, each one should be reviewed through a financial lens.

Here are common ways non-fungible tokens are being used in fintech environments:

Token-gated access: NFTs can serve as digital gatekeepers, controlling access to investor dashboards, high-yield product tiers, or premium features. Instead of usernames or account flags, access is granted through wallet ownership of a specific NFT. This creates a flexible and transferable permission layer but can also raise custody and KYC concerns if access ties to regulated financial products.

On-chain identity and credentials: Some fintechs use NFTs to represent user verification, KYC completion, or regulatory classification (e.g., accredited investor status). These NFTs don’t carry financial value but act as durable, verifiable credentials. However, they may trigger data privacy obligations and require controls around issuance, revocation, and linking to personally identifiable information (PII).

Receipts, proof of ownership, or entitlement: NFTs can function as transaction records or digital receipts, especially in peer-to-peer environments or decentralized apps. In some models, they represent claim rights to off-chain assets or services, such as a voucher for a physical product or ticket. When NFTs imply entitlement to a financial asset or return, regulators may assess them as securities or derivatives, depending on structure.

Real-world assets (RWAs) and asset representation: Some startups are experimenting with using NFTs to represent shares of real estate, vehicles, art, or other physical assets. While NFTs can help make ownership more flexible or tradable, tokenizing real-world assets introduces complexities around legal title, custody, and enforceability. Fractionalization also heightens the risk of crossing into regulated territory.

In all of these use cases, the NFT itself is just a container. What it represents and how it’s integrated into a fintech product determines whether compliance obligations arise. That’s why functional design should never be separated from regulatory review in fintech NFT projects.

Need help with fintech compliance?

Fill out the form below and our experts will get back to you.

When NFTs Trigger Financial Regulation

NFTs aren’t automatically exempt from financial oversight just because they’re labeled as “non-fungible” or used in a novel way. If an NFT mimics the behavior of a regulated financial product, it can trigger oversight from agencies like the SEC, FinCEN, CFTC, or state regulators.

There are the primary regulatory triggers fintechs should evaluate when launching or integrating NFTs:

Economic substance over technical form: Regulators focus on how an NFT functions, not how it’s described. If users buy NFTs with the expectation of profit tied to a business effort, you may be in securities territory. If NFTs are exchanged for value or used in payments, money transmission rules may apply.

Transaction flow and custody: Platforms that take custody of, or exercise control over, user funds or digital assets may fall under money services business (MSB) obligations. This includes situations where NFTs are traded for crypto or fiat, and where the platform manages keys, escrow, or smart contract permissions.

Secondary market behavior: A token may be unregulated at issuance but acquire characteristics of a security or investment contract when traded in a particular way. If your users expect resale value, pooled profits, or dividend-like benefits, that shifts the risk profile.

Non-fungible tokens often sit in regulatory gray zones until they don’t. Enforcement actions in 2023 showed that agencies are willing to bring cases when a product resembles a security, regardless of whether the issuer “meant” it that way.

Could an NFT Be a Security?

Yes, some NFTs can be securities, depending on how they’re structured, marketed, and sold. Not all NFTs fall into that category, but the ones that do typically involve financial incentives, shared profits, or speculative resale models.

The SEC uses the Howey test to determine whether something qualifies as an investment contract (and therefore a security). The test looks for four elements:

An investment of money

In a common enterprise

With a reasonable expectation of profits

Derived from the efforts of others

If your NFT offering hits all four, you may be operating in securities territory. This can apply even if the NFT has a functional use, such as access, membership, or digital art, if it’s sold or promoted in a way that emphasizes financial upside.

Non-fungible tokens that often carry securities risk include:

Fractionalized NFTs: Ownership is divided into multiple tradable units, resembling shares

Royalties or profit-sharing NFTs: Holders receive ongoing benefits tied to company performance or platform revenue

Investment-framed drops: NFTs sold with messaging focused on price appreciation, roadmap-based value growth, or influencer-driven hype

In 2023, the SEC brought enforcement actions against projects that framed NFTs as investment opportunities, regardless of the underlying tech. Founders and product teams should be cautious about any structure that mimics equity, pooled capital, or return-on-investment language.

When NFT Activity May Trigger Money Transmission Regulation

NFT projects that involve moving value between parties can trigger money transmission laws at the federal or state level. This applies even if the platform doesn’t think of itself as handling funds.

In the US, FinCEN’s regulation focuses primarily on the transmission of fiat or convertible virtual currency (“value that substitutes for currency”). If a non-fungible token platform facilitates:

NFT-for-crypto transactions

NFT-for-fiat payments

The transfer of fiat or crypto between users as part of NFT transactions

Then the platform could be viewed as a money transmitter or a broader money services business (MSB).

Here’s how typical NFT-related actions map to potential money transmission risk:

Platform Function | Risk of Triggering Money Transmission Laws |

|---|---|

Custodies crypto or fiat for NFT transactions | High; may qualify as a money transmitter under FinCEN and state law |

Facilitates NFT-for-crypto or NFT-for-fiat swaps | Moderate-to-high, especially if the platform controls pricing, clearing, or execution |

Non-custodial wallet-to-wallet transfers only | Lower risk but still subject to scrutiny if the platform orchestrates or monetizes flows |

Smart contract manages crypto or fiat settlement logic | Moderate; risk depends on who controls the assets or contract execution, timing, and degree of automation |

Platform profits from transaction fees or flow | Increases scrutiny; may suggest you're providing a value-transfer service |

When NFTs May Fall Under Commodity or Derivatives Regulation

While most NFT discussions focus on securities law, some use cases may bring NFTs into the scope of the Commodity Futures Trading Commission (CFTC), especially when platforms introduce derivatives-like mechanics or structured trading features.

The CFTC defines commodities broadly. And it has already asserted jurisdiction over digital assets like Bitcoin and Ether when used in certain financial products. NFTs aren’t categorically excluded. If they’re used in speculative instruments, they may fall under the same scrutiny.

Scenarios that could trigger CFTC oversight:

NFTs used in leveraged or margined trading: If your platform allows users to buy or trade NFTs on leverage or margin, the CFTC may treat this as a commodity derivative or futures-like activity.

NFT-linked swaps or structured products: Platforms offering financial contracts or tokens that reference the value of NFTs may trigger registration or reporting requirements.

NFT-based prediction markets or betting structures: If an NFT’s value is tied to a future event (e.g., game results, business milestones) and used for speculation, it may be treated as a form of binary option or futures contract.

In general, the risk increases when NFTs are used to simulate price exposure without transferring ownership of the underlying asset. This is what differentiates traditional collectibles from derivatives.

Fintechs exploring financial engineering around non-fungible tokens should evaluate whether the platform offers synthetic exposure, pooled trading, or yield generation in ways that resemble CFTC-regulated products. Because the commodity definition is broad, NFTs could potentially fall within that category depending on how they are structured or used.

When NFTs Implicate Consumer Protection and Unfair Practices Laws

Even when an NFT doesn't qualify as a security, commodity, or payment instrument, it can still fall under consumer protection laws.

Federal and state regulators, including the Federal Trade Commission (FTC) and state attorneys general, have broad authority to investigate business practices that deceive or harm consumers. In the NFT space, this often centers on:

Misleading claims about the nature or future value of the NFT

Omissions around rights, functionality, or resale restrictions

Deceptive UI patterns (e.g., rushing users into a mint, hiding fees)

Bait-and-switch behavior, such as promising roadmap features that never launch

In some cases, platforms may also face scrutiny over how they handle refunds, disputes, and user complaints. One recurring issue: buyers often assume they’re purchasing the underlying asset, when in reality they’re just receiving a license or pointer to off-chain content. If that nuance isn’t clearly disclosed, regulators may interpret the sale as deceptive or materially incomplete.

When NFTs Trigger Sanctions or Export Control Obligations

NFT platforms and fintechs operating in global markets need to consider sanctions laws and export controls, especially when NFT transactions involve users, wallets, or jurisdictions subject to restrictions.

The Office of Foreign Assets Control (OFAC) has made it clear: sanctions rules apply to digital assets just like traditional financial products. This includes NFTs, even when platforms don’t think of themselves as financial intermediaries.

Key exposure points include:

Allowing access from sanctioned jurisdictions (e.g., Iran, North Korea, Cuba)

Facilitating NFT sales involving designated individuals or wallet addresses

Enabling cross-border transfers of high-value NFTs without proper screening

Failing to implement geo-blocking, wallet screening, or export classification procedures

NFTs may also implicate US export control laws when they involve encryption technology, digital media, or are sold across borders in ways that classify them as controlled digital goods. While this may sound niche, several NFT platforms have already faced enforcement attention for inadequate controls around country-level access.

Unlike securities or money transmission rules, there’s no threshold for sanctions liability. Even one prohibited transaction can lead to penalties. And OFAC has emphasized that platforms are expected to adopt risk-based compliance programs, including:

IP and geolocation blocking

Blockchain wallet address screening

Internal flagging of high-risk jurisdictions or users

For fintechs entering NFT markets, sanctions exposure is often underestimated. But if your platform is reachable globally, regulators will expect controls.

Learn about the Digital Financial Assets Law (DFAL) before launching your own digital assets →

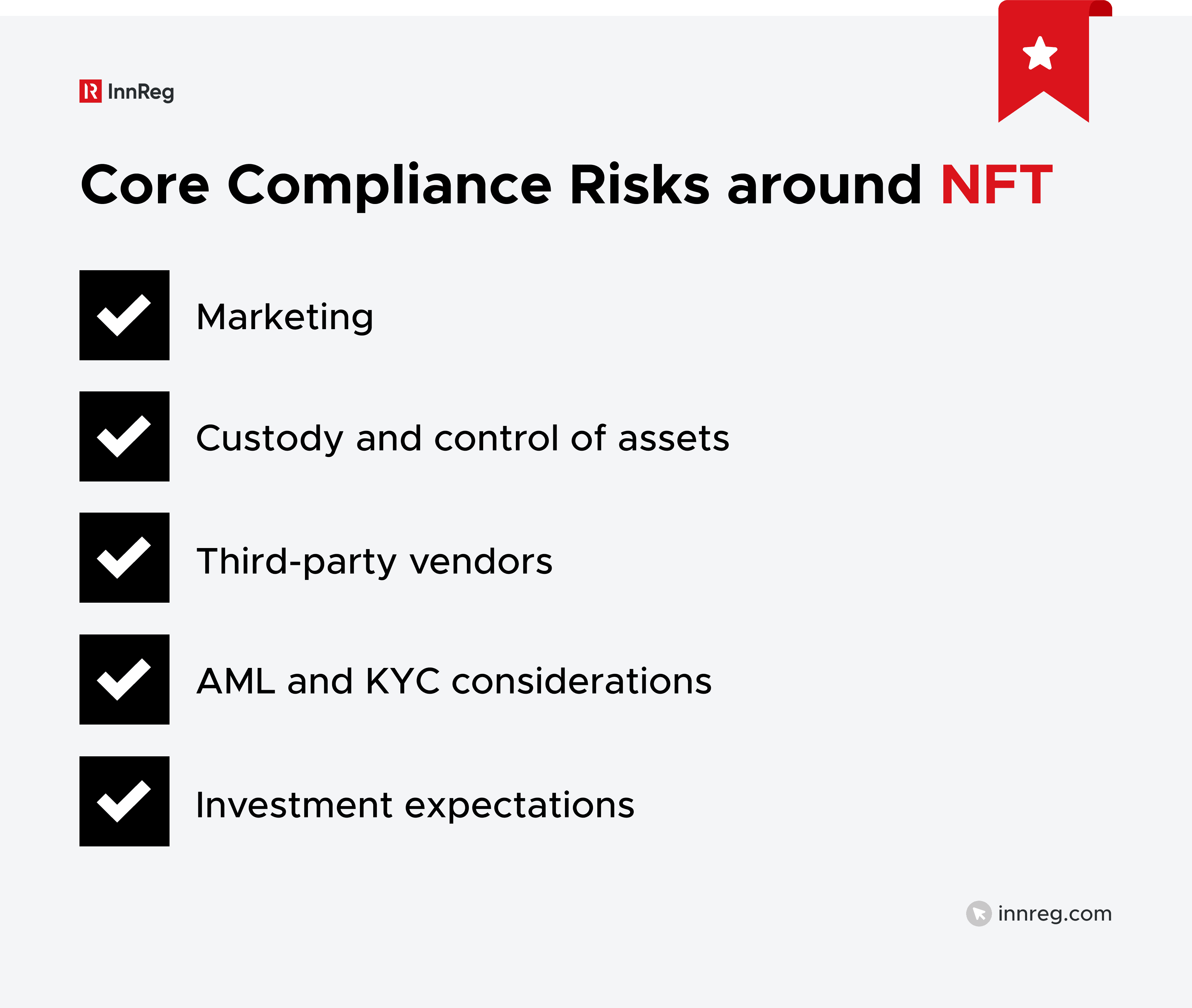

Key NFT Compliance Risks for Fintechs

Even if a fintech isn’t directly issuing or trading NFTs, integrating them into a product stack creates regulatory risk vectors. Many of these risks emerge from how the NFT interacts with money, access, identity, or data.

Below are the most common compliance friction points we’ve seen in fintech environments:

See also:

Marketing and Investment Expectations

How you talk about an NFT can be just as risky as how you build it. Promotional language that hints at profit, future value, or investment upside can shift a product into regulatory territory, especially under securities law.

Key red flags in marketing include:

Phrases like “early access,” “rare drop,” or “limited supply” when paired with resale incentives

Statements that imply appreciation, such as “grab it before prices go up” or “get in before the floor rises”

Mentioning future utility or roadmap milestones in a way that ties to the token value

Highlighting past sales volume or secondary market activity to imply investment viability

Even if the NFT is primarily functional, such as a loyalty token or access pass, overemphasizing potential resale value can invite SEC scrutiny. In its 2023 enforcement actions, the agency focused not just on how the NFT worked, but on how it was framed to buyers.

Marketing copy, social media campaigns, pitch decks, and community engagement channels (like Discord or X) are all fair game for regulatory review. What’s said by founders, affiliates, or influencers can carry weight even if it wasn’t part of the core product site.

Custody and Control of User Assets

If your platform holds, routes, or controls access to NFTs or related funds, even temporarily, regulators may view it as engaging in safekeeping, money transmission, or custodial services.

But how can you see it in action? Some of the common examples are holding NFTs in a platform-controlled wallet before delivering to the buyer or even managing private keys or access permissions for user-owned NFTs. In some cases, operating escrow mechanisms for trades, claims, or auctions and retaining control through smart contracts that delay or stage transfers can also count as custody and control.

In these cases, the platform assumes responsibility for protecting user assets and may be required to register as a money transmitter or obtain state-level licensing, depending on the jurisdiction. If fiat or crypto moves alongside the NFT, that further increases exposure.

Even platforms that claim to be “non-custodial” can encounter issues if their smart contracts retain upgrade privileges, withhold assets under certain conditions, or aggregate NFTs into pooled contracts. The test is how much control the platform has over the asset.

Third-Party Vendors and Smart Contract Design

Many fintechs rely on NFT platforms or embedded tools without fully auditing their smart contract behavior, permissions, or financial flows. If a vendor handles custody, price logic, or financial routing, their risk becomes your risk.

Here are some of the key vendor risks:

Smart contract logic that automates financial flows, like royalties, staking rewards, or time-locked asset releases. These mechanisms may trigger regulatory obligations, especially if they resemble securities or payment systems.

Upgradeable contracts controlled by the platform or vendor. If your team retains the ability to pause, modify, or redirect NFT behavior post-deployment, you may be viewed as retaining functional control.

Oracles and data dependencies that affect pricing, unlocks, or token behavior. If your NFTs rely on off-chain inputs to trigger in-app changes or benefits, those sources must be trustworthy, verifiable, and clearly disclosed to users.

Vendor compliance gaps, especially around KYC, AML, data privacy, or IP rights. If your NFT partner mishandles regulated data or uses infringing content, your brand could be implicated.

Smart contracts are powerful but not legally neutral. The design, permissions, and integrations matter. Before launching, review each contract’s functions through a compliance lens.

AML and KYC Considerations for NFT Platforms

If your platform facilitates NFT trades or transfers, and those NFTs represent value, regulators may expect basic AML controls even if you’re not a registered financial institution. This includes transaction monitoring, sanctions screening, and high-risk jurisdiction flagging.

The way users resell, bundle, fractionalize, or derive income from NFTs can reshape your compliance profile overnight. That’s why a one-time legal review isn’t enough. Ongoing monitoring, cross-functional oversight, and coordination between product, compliance, and legal teams are essential.

NFT Fraud, Market Manipulation, and Enforcement Trends

As NFTs take on more financial characteristics, the line between product innovation and market misconduct gets thinner. Fraud in the NFT space has evolved beyond simple phishing links and fake mints.

In financialized or fintech-adjacent projects, fraud and market manipulation raise legal risk. Here are some of the latest trends to keep in mind:

Rug Pulls and Misleading NFT Projects

When an NFT project markets utility, value, or community features that it never intends to deliver, it can cross into fraud, even without formal investment language.

Regulators are watching for:

Vanishing founders post-mint, especially where project roadmaps implied ongoing development or perks

NFTs pitched as access to future tools, rewards, or income, but quietly abandoned

Affiliate and influencer campaigns that manufacture urgency or hype floor prices

Projects with no functioning support, dispute, or refund channels

In fintech, the stakes are higher. Even if your company didn’t launch the non-fungible token, you could be exposed if your product, wallet, or platform helped it scale without oversight. Deceptive marketing, fake scarcity, or roadmap vaporware are all triggers for consumer protection or fraud investigations.

Wash Trading and Market Integrity Issues

Wash trading isn't just a problem in crypto exchanges. It’s rampant in NFT markets, especially where platforms rely on trading volume to attract attention or establish credibility. Fake or coordinated trades between related parties can artificially inflate floor prices, distort demand, and mislead users.

Red flags for wash trading in NFT environments include:

Repeated trades of the same NFT between two or more wallets

Volume spikes tied to influencer campaigns or token incentives

Platform fee rebates or rewards that create incentives to trade with yourself

Trades between wallets controlled by the same user or team member

While some NFT platforms claim they’re just “open marketplaces,” regulators don’t always accept neutrality as a defense, especially if the platform profits from inflated activity or fails to detect patterns.

FinCEN, the SEC, and the DOJ have all indicated interest in market integrity in digital asset ecosystems. If your fintech product touches NFT volume metrics or promotes top traders or collections, you need internal guardrails against spoofing, self-dealing, and collusion.

See also:

Insider Abuse and Recent Enforcement Actions

As NFT ecosystems grow more sophisticated, insider activity becomes a key focus for regulators. This includes both direct manipulation and indirect benefit schemes.

Common forms of insider abuse in NFT environments include:

Buying NFTs before they're featured, promoted, or integrated

Using privileged access to data (like upcoming drops or pricing changes)

Front-running community disclosures or partnership news

Team wallets quietly offloading inventory while promoting bullish narratives

The SEC’s 2023 enforcement actions signal a shift: they’re treating undisclosed conflicts and information asymmetry as investor harm. This mirrors how public company insiders are regulated under securities law.

Fintechs involved in NFT drops, embedded tokens, or token-linked rewards should define trading policies for team members and contractors, limit access to sensitive roadmap information, and disclose any holdings or promotional incentives clearly.

Even if the asset isn’t formally a security, regulators may still bring cases under antifraud statutes or deceptive practices laws.

How Other Global Jurisdictions Treat NFTs

NFT regulation isn’t just a US concern. Fintechs operating globally need to evaluate how different jurisdictions interpret NFT activity, especially as more regions move toward digital asset frameworks that capture non-fungible tokens explicitly or by proxy.

Here are regional snapshots of how non-fungible tokens are currently treated or referenced in financial or consumer protection regimes:

European Union

The EU’s Markets in Crypto-Assets Regulation (MiCA) excludes most NFTs, but with a catch. If NFTs are “fungible in practice” or tied to financial use cases like revenue-sharing or access to investment products, they may still fall under existing EU securities laws. Even outside MiCA, GDPR, consumer rights directives, and platform liability rules still apply.

United Kingdom

The UK’s Financial Conduct Authority (FCA) evaluates NFTs by how they function. An NFT tied to profit expectations or investor-like perks can trigger financial promotions rules or securities oversight. The new Consumer Duty framework also raises the bar for platforms targeting retail users with speculative products, even if those products are framed as “collectibles.”

Singapore

Singapore treats NFTs primarily as unregulated unless they mimic securities or payment tokens. The Monetary Authority of Singapore (MAS) has warned against:

NFTs used in lending, staking, or fractionalized investments

Platforms marketing NFTs as financial products without licenses

While personal use cases are generally left alone, financialized or profit-driven models are under close watch.

United Arab Emirates

The UAE, and especially Dubai, is rolling out a formal licensing regime for virtual assets. Under Dubai’s VARA framework, NFTs that involve custody, trading, or financial features require explicit approvals. Regulatory treatment may differ between zones like Dubai and Abu Dhabi, so firms need to assess each separately when operating in the region.

Other Key Regions

In Japan, NFTs can be regulated under the Financial Instruments and Exchange Act when used as securities or pooled investments. South Korean authorities have raised red flags about NFT speculation in games and reward programs.

In Canada, treatment varies by province, but regulators have brought enforcement actions against those promoting NFTs as investment products.

Compliance Checklist Before Launching or Integrating NFTs

FT projects don’t need to be risky by default. But fast-paced fintechs often overlook key compliance checkpoints that could surface during audits, due diligence, or enforcement.

Here’s a foundational checklist to review before going live:

What is the actual function of the NFT? Access pass? Credential? Revenue share? The answer will shape which laws apply.

How is it being marketed? Review all messaging for investment-like language, including blog posts, social media, and affiliate content.

Is the platform custodial or non-custodial? This affects licensing obligations, particularly around money transmission and safekeeping.

Are users transferring value? If crypto or fiat changes hands, even through smart contracts, consider MSB rules and AML controls.

Who controls the smart contracts? Upgrade privileges, transfer logic, or admin keys may count as platform control even in “decentralized” systems.

Is there secondary market activity? If NFTs are expected to be resold, and the platform benefits from or promotes that activity, regulatory exposure increases.

Are third-party vendors involved? Any marketplace, wallet provider, or protocol partner should be vetted for regulatory posture and operational risk.

Do your users understand what they’re buying? Provide clear disclosures around rights, risks, and the nature of the asset, including what the NFT does not represent.

Fintechs that treat NFT compliance as part of product design are better positioned to scale, partner, and withstand scrutiny. If you're unsure where your risk lies, a structured review before launch is faster and cheaper than a remediation effort after the fact.

—

NFTs are no longer fringe experiments. As fintechs integrate non-fungible tokens into products, platforms, and user flows, they step into a fast-evolving compliance environment. The novelty of NFTs doesn’t shield them from regulation. The regulators are watching, and enforcement is catching up to innovation.

That’s where InnReg comes in. We work with fintech companies exploring these gray areas. Whether you're assessing vendor risk, designing NFT flows, or preparing for licensing or investor diligence, we build custom compliance frameworks that match your roadmap. If your platform touches NFTs and money, it’s time for a compliance conversation. Let’s have it before the regulators do.

Adriana is a Principal Consultant at InnReg with 8 years of compliance experience specializing in VASP licensing and regulatory frameworks across Europe and LATAM. She has held senior compliance roles at leading global crypto and financial institutions, including Gate.io, Binance, Santander Bank, and BNP Paribas, with deep expertise in KYC/AML operations, MiCA adaptation, and building compliance programs from the ground up.

How Can InnReg Help?

InnReg is a global regulatory compliance and operations consulting team serving financial services companies since 2013.

We are especially effective at launching and scaling fintechs with innovative compliance strategies and delivering cost-effective managed services, assisted by proprietary regtech solutions.

If you need help with compliance, reach out to our regulatory experts today:

Related Articles

Featured LinkedIn Posts