What Is Tokenization In Fintech? A Guide to Tokenized Assets

Tokenization in fintech has become one of the most discussed innovations in financial services, and it’s not hard to see why. Imagine taking something as traditional as company shares, a real estate property, or even a gold bar, and turning it into a digital token you can hold, trade, or transfer on a blockchain. That is tokenization in action.

For fintech founders, compliance teams, and legal professionals, tokenization is reshaping how finance works by merging regulation and technology. In this guide, we break down what tokenization means, how tokenized assets actually work, and why they matter. We will also highlight the benefits, limits, and the main regulatory frameworks in the US and globally.

At InnReg, we help fintechs structure tokenized asset offerings and trading platforms within existing securities and digital asset rules, from assessing Howey/ MiFID classifications to broker-dealer, ATS, and crypto licensing strategy. Contact us to learn more.

What Tokenization Means in Fintech

Tokenization in fintech is all about turning ownership of real assets into digital tokens on a blockchain. Think of it as a way to represent something you already know, like shares in a company, a bond, a piece of real estate, or even a commodity, in a digital format that can be tracked and traded more easily.

Unlike cryptocurrencies, which are their own separate assets, tokenized securities are tied directly to something tangible or financial in the real world. That connection is what makes them different.

The power of tokenization comes from how it changes ownership records. Instead of relying on paper documents or siloed databases, a blockchain keeps a secure, transparent ledger of who owns what. Tokens can be divided into smaller pieces, transferred across borders, and traded with far fewer barriers.

Tokenization vs. Traditional Asset Ownership

When you own shares the traditional way, you're dealing with paper certificates or electronic records that are passed between transfer agents, custodians, and clearinghouses. These middlemen keep track of who owns what. The problem? Settlement drags on for days while everyone in the chain verifies the transaction.

Tokenization flips this system. Your ownership rights become digital tokens living on a blockchain, which works like a shared ledger that everyone can see. You don't need as many intermediaries checking and double-checking every move. The underlying asset stays the same. A share is still a share, but moving it from one person to another gets a whole lot simpler.

Tokenized Assets vs. Payment/Data Tokenization

The word “tokenization” is often used in different ways, which can cause confusion. When it comes to payments, tokenization usually means replacing sensitive data such as credit card numbers with random strings of characters. This protects information during transactions but has nothing to do with ownership rights.

Tokenized assets are something different. They are digital representations of real-world value. A token can represent a share in a company, a bond, or even a piece of real estate. These tokens carry the same economic rights as the underlying asset, and when they are transferred, it reflects a change in ownership rather than a simple swap of data.

How Tokenized Assets Work

Tokenized assets are transforming how ownership is tracked and traded in finance. Instead of relying on paper or centralized systems, blockchain records make transfers faster, more secure, and easier to manage.

Here’s how tokenized assets work.

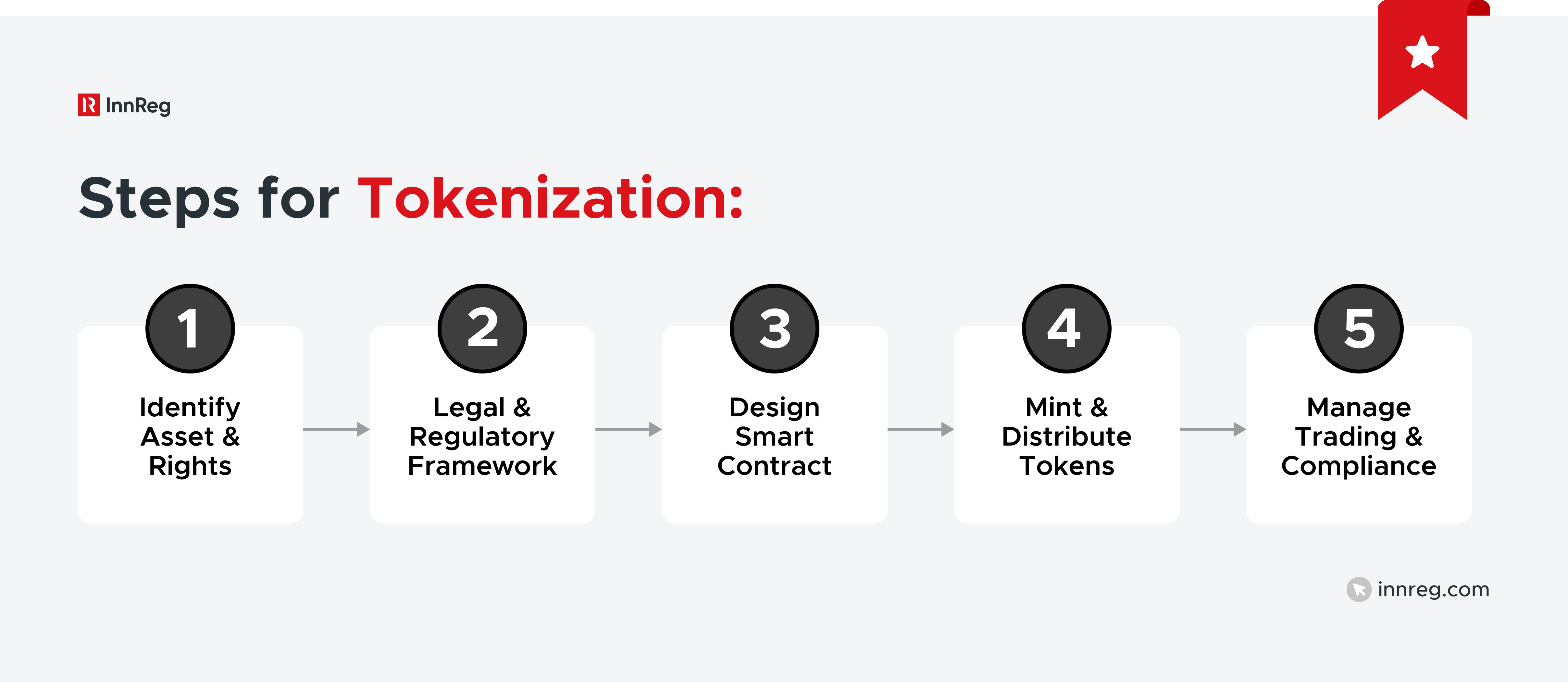

The Tokenization Process Step by Step

Building tokenized assets is not as simple as minting tokens on a blockchain. Each step combines legal structuring, regulatory analysis, and technical execution. Skipping or mishandling any step can create serious compliance risks or operational gaps.

Here’s a practical overview of how most projects approach tokenization.

1. Identify the asset and define rights: Choose the asset to tokenize and clarify exactly what each token represents. This could be equity in a startup, a share of a property, or a fixed-income instrument. Founders also need to decide whether the token carries voting rights, dividend rights, or other entitlements. Without this clarity, investors and regulators may see the structure as incomplete or unreliable.

2. Establish the legal and regulatory framework: Tokenization does not erase existing laws. If the token is structured or offered in a way that brings it within the scope of securities laws, regulators such as the Securities and Exchange Commission (SEC) will treat it as one. The issuer must choose whether to register the offering or rely on an exemption such as Regulation D, Regulation A+, Regulation CF, or Regulation S. Each path has different rules on who can invest, what disclosures are required, and how tokens can be resold. At this stage, legal counsel and compliance experts play a critical role in building a structure that can withstand regulatory review.

3. Design the smart contract: Once the legal framework is in place, developers build the smart contract on a blockchain. This contract automates how tokens are created, transferred, and sometimes how payments such as dividends are distributed. It can also include restrictions, like limiting transfers to approved investors or enforcing lock-up periods. The smart contract becomes the operational backbone of the tokenized asset, but it must stay fully aligned with the legal agreements that sit off-chain.

4. Mint and distribute tokens: With the structure in place, tokens are issued and distributed to investors. This can happen through a broker-dealer, a specialized platform, or directly to accredited investors under an exemption. Investors hold the tokens in digital wallets, which makes custody, key management, and recordkeeping important compliance considerations. Issuers or platforms also need to maintain accurate off-chain records that mirror blockchain activity for regulatory reporting.

5. Manage secondary trading and compliance: After issuance, tokenized assets may trade on secondary markets. In the US, this usually requires an SEC-regulated Alternative Trading System (ATS) or another licensed venue. Compliance teams must continue monitoring transfers to confirm that restrictions such as holding periods or investor eligibility are respected. Ongoing oversight is essential to connect the technology with the legal framework and to prevent unauthorized resales that could create liability.

Taken together, these steps show that tokenization is a blend of financial law and blockchain development. For fintech founders, success depends on bringing legal and technical teams together early and maintaining strong compliance oversight every step of the way.

Common Types of Tokenized Assets

Tokenization is flexible, but the way it applies to different asset classes varies. Each category brings its own legal, operational, and compliance challenges.

Equity: Tokenized equity is usually issued in two ways: private offerings under exemptions such as Regulation D, or smaller public offerings under Regulation A+. The tokens represent the same ownership rights as traditional shares, but they can be split into fractions and transferred on digital platforms. For compliance teams, the main challenge is secondary trading. If investors want to resell tokenized shares, trading usually has to happen on an SEC-regulated ATS or another approved marketplace. Without the proper infrastructure, the promise of liquidity can run into regulatory walls.

Debt Instruments: Bonds, notes, and other fixed-income products are also going digital. A tokenized bond can even use a smart contract to automate interest payments, which reduces manual processing. The challenge is making sure that automation lines up with investor-protection and disclosure rules. Even if coupon payments are coded into the smart contract, issuers must still meet the same regulatory requirements as a traditional bond offering.

Real Estate: Real estate is one of the most visible examples of tokenization. A property can be divided into tokens, making fractional ownership possible. This lets investors take part in deals that would typically require significant capital commitments. Firms can structure tokens to give investors returns tied to rental income or appreciation in property value. The regulatory issue is classification.

In many cases, tokenized real estate is treated as a security, depending on how the offering is structured and how investor rights are defined. That means offerings must follow securities laws, disclosure requirements, and resale restrictions. Another challenge is linking on-chain token records with off-chain property rights so that ownership is enforceable in the real world.

Commodities: Gold, silver, oil, and other commodities can also be tokenized. This makes it easier for investors to gain exposure without taking physical delivery. Paxos Gold (PAXG) is a well-known example: each token corresponds to a specific quantity of gold stored in a vault. Here, custody and verification are critical. Regulators and investors want proof that the underlying commodity actually exists and is properly safeguarded. For fintech firms, this means building reliable partnerships for storage, audits, and independent verification.

Funds and Investment Vehicles: Investment funds are exploring tokenization. Franklin Templeton’s OnChain US Government Money Fund is one example of a registered mutual fund that uses blockchain for recordkeeping and transactions. Tokenization in this setting can lower minimum investment amounts, expand trading windows, and simplify investor onboarding. Still, fund managers must navigate the same SEC requirements around disclosure, custody, and investor eligibility. The compliance workload does not shrink just because the fund is digital.

Smart Contracts and Investor Rights

Smart contracts are self-executing programs on a blockchain that govern how tokenized assets operate. They act as the link between the legal framework set by regulators and the technical framework built by developers. When designed properly, smart contracts can automate critical functions that would otherwise require intermediaries, while still fitting within existing securities laws.

Here’s what smart contracts can do:

Automate payments such as dividends, interest, or rental income

Restrict transfers to approved investors or whitelisted wallets

Embed lock-up periods for restricted securities

Record every transaction on-chain to create an auditable trail

While powerful, smart contracts cannot replace legal documentation. Investor rights such as voting, redemption, and dispute resolution should still be defined in offering documents and contracts. If conflicts arise, regulators and courts will look to these documents first, even if the smart contract says otherwise.

From a regulatory perspective, the level of reliance on an issuer or promoter remains important when determining whether an arrangement involves a security. As projects mature and become less dependent on a central party, the regulatory analysis may evolve, which is a concept increasingly reflected in recent SEC guidance.

For compliance teams, the focus is on alignment. The code should reflect what is written in agreements, contingency plans should cover coding errors or lost keys, and traditional records must be maintained alongside blockchain records.

See also:

Why Tokenization Matters in Finance

Tokenization is changing how people invest, trade, and manage assets, making finance more accessible and efficient. Here’s its impact on financial markets.

Fractional Ownership and Access: High-value assets such as commercial real estate, private equity funds, or fine art have long been accessible only to institutions or wealthy investors. Tokenization allows these assets to be divided into smaller, tradable units. An investor who might not be able to buy into a building worth millions can instead purchase a fraction through tokens. This opens doors for broader participation, but also raises regulatory questions around disclosures, suitability, and how to manage a more diverse investor base.

Liquidity for Illiquid Assets: Illiquidity has always been a challenge in private markets. Tokenization can introduce new avenues for secondary trading. A tokenized equity stake or bond can be listed on an SEC-regulated Alternative Trading System (ATS), creating exit opportunities where none existed before. However, liquidity is not guaranteed. It requires a compliant market structure, investor demand, and careful monitoring of transfer restrictions, especially when exemptions like Reg D impose holding periods.

Faster Settlement and Cost Efficiency: Traditional securities trades often move through a chain of brokers, custodians, and clearinghouses. This process takes time and creates costs at each step. Tokenized assets can settle almost instantly on a blockchain, reducing counterparty exposure and reconciliation work. The efficiency is real, but it depends on integrating blockchain settlement with existing regulatory requirements, such as custody rules and audit trails. For fintech founders, this balance between speed and compliance is critical.

Transparency and Auditability: Every transaction in a tokenized asset can be recorded on-chain, creating a tamper-evident history of ownership. This transparency can simplify audits and give regulators confidence in the integrity of records. For compliance officers, it also offers a practical advantage: disputes over who owns what are easier to resolve when there is a verifiable ledger. The challenge is aligning blockchain records with traditional books and records, since regulators still expect both.

Programmability and New Use Cases: Tokenized assets are programmable through smart contracts. This means compliance checks, payout schedules, and transfer restrictions can be built directly into the code. For example, a smart contract can block transfers to non-accredited investors or automatically distribute dividends. These features reduce manual intervention, but they also require oversight to confirm that the code reflects legal agreements. In this way, programmability creates opportunities for innovation, but it also brings regulators closer into product design.

Need help with fintech compliance?

Fill out the form below and our experts will get back to you.

Tokenized Assets Regulation in the US

In the US, tokenized assets are generally treated under the same laws that apply to traditional securities. Regulators focus on the substance of what the token represents, not the technology behind it. If a token functions like a security, it will be regulated as one, whether it is issued through a blockchain or a paper certificate. This approach shapes how offerings are structured, how secondary trading is conducted, and what responsibilities fall on issuers, platforms, and investors.

More recent SEC guidance expands this approach by introducing clearer distinctions between different types of crypto assets, including digital securities and non-security crypto assets. This reflects a shift from relying solely on case-by-case analysis toward a more structured classification framework, while still applying existing securities laws where appropriate.

SEC and the Howey Test

The SEC relies on the Howey Test to decide whether a token is a security. This test, which comes from a 1946 Supreme Court case, asks four key questions:

Is there an investment of money?

Is the investment in a common enterprise?

Do investors expect profits?

Are those profits expected to come primarily from the efforts of others?

If the answer to all four is yes, the token is considered a security. This framework has been used for decades in traditional finance, and the SEC applies it directly to tokenized assets.

For fintech founders, this has direct implications. Many tokenized assets, such as tokenized equity, bonds, or real estate shares, clearly meet the Howey criteria. Once they do, they fall under the Securities Act of 1933, which governs how securities can be issued and sold in the US. Issuers must either register with the SEC or rely on an exemption, such as Regulation D for private placements, Regulation A+ for smaller public offerings, or Regulation CF for crowdfunding.

The Howey Test is also used in enforcement. When the SEC brings cases against token issuers, it often argues that the tokens were sold with an expectation of profit based on the issuer’s efforts, making them unregistered securities. This is why structuring tokens carefully at the outset is so important. It is not enough to call a token a “utility token” or claim it has another purpose. Regulators look at how it functions in the market and how it is marketed to investors.

While the Howey Test remains central, the SEC has recently clarified that not all crypto assets are securities and that the existence of an investment contract may depend on specific facts and circumstances. The SEC has also acknowledged that an investment contract can evolve or come to an end over time, which means that the regulatory treatment of a token may change as a project develops.

Registration vs. Exemptions

When a tokenized asset qualifies as a security, issuers have two broad choices: pursue complete SEC registration or rely on one of the available exemptions.

Registration

Registering a tokenized security under the Securities Act of 1933 allows the issuer to sell broadly to the public, including retail investors. This route provides maximum fundraising flexibility and opens the door to secondary trading on public exchanges.

The tradeoff is the level of regulatory scrutiny. Issuers must prepare and file a detailed registration statement, deliver a prospectus with extensive disclosures, and comply with ongoing reporting obligations similar to those of a public company. The process can take months, requires significant legal resources, and introduces recurring compliance costs.

For fintech startups, this path is often considered impractical unless the offering is very large and investor access must extend beyond accredited buyers.

Exemptions

Most tokenized securities are offered under exemptions. The main options are:

Regulation D: Reg D is the most common route for tokenized offerings. It allows issuers to raise unlimited capital from accredited investors, with relatively limited disclosure requirements compared to registration. Under Rule 506(c), issuers must verify investor accreditation, often through third-party checks. The main limitation is liquidity: securities sold under Reg D are “restricted,” meaning they cannot be freely resold for at least 12 months, unless through another exemption.

Regulation A+: Reg A+ allows companies to raise up to $75 million annually, and unlike Reg D, it permits participation from non-accredited investors. This makes it more attractive for companies seeking broader distribution. However, it is not a free pass. Issuers must file an offering circular with the SEC, undergo a review process, and commit to ongoing reporting obligations, though less burdensome than those for a fully registered public company. Token issuers that want wider retail access but cannot commit to full registration often look at this path.

Regulation CF: Crowdfunding rules permit smaller companies to raise up to $5 million in a 12-month period from both accredited and non-accredited investors. Investor limits are tied to income and net worth, which means participation is capped for many individuals. Tokenized assets issued under Reg CF are subject to resale restrictions for at least 12 months. While this route can help early-stage fintechs test demand, it is rarely suitable for larger-scale tokenized securities offerings.

Regulation S: Reg S provides a way to raise capital from investors outside the US. It applies when an offering is conducted entirely offshore and targets only non-US persons. Issuers must build controls to prevent tokens sold under Reg S from being resold into the US market too quickly, as that could be viewed as a backdoor into the domestic system. For companies with a global investor base, Reg S is often used alongside Reg D or another exemption.

The choice between registration and exemptions shapes not only who can invest but also how tokens can be traded in the future. For compliance officers, mapping out this decision early is essential because each path comes with different disclosure requirements, filing obligations, and restrictions on resale.

Secondary Trading Rules

Issuing tokenized assets is only the first step. The bigger challenge is how they can be traded after the initial sale. In the US, securities laws tightly control secondary markets, and tokenized securities are no exception.

Alternative Trading Systems (ATS): Most secondary trading of tokenized securities takes place on SEC-regulated ATS platforms. These venues operate under the same regulatory framework as traditional electronic trading systems but are adapted to support blockchain-based assets. Without access to an ATS or a registered exchange, investors holding tokenized securities may find their ability to resell limited.

Broker-Dealers: If a company or platform facilitates the buying and selling of tokenized securities, it often must register as a broker-dealer or work with one. Broker-dealers are responsible for customer protection, trade reporting, and supervisory controls. For fintech founders, this means that launching a trading venue or offering secondary liquidity typically requires a broker-dealer partnership or licensing strategy.

Custody: Under SEC rules, customer securities must be safeguarded by qualified custodians that meet specific standards. With tokenized assets, custody can involve digital wallets, private keys, and blockchain transactions. Regulators expect these to be handled with the same protections as traditional securities, including segregation of client assets, recordkeeping, and audit trails. Some broker-dealers are now expanding their custody solutions to cover tokenized securities, but the infrastructure is still developing.

For compliance officers, secondary trading highlights why tokenization does not bypass regulation. The same requirements for exchanges, brokers, and custodians apply, even when ownership is recorded on a blockchain. Planning for liquidity, custody, and compliance early can prevent major roadblocks later in a project.

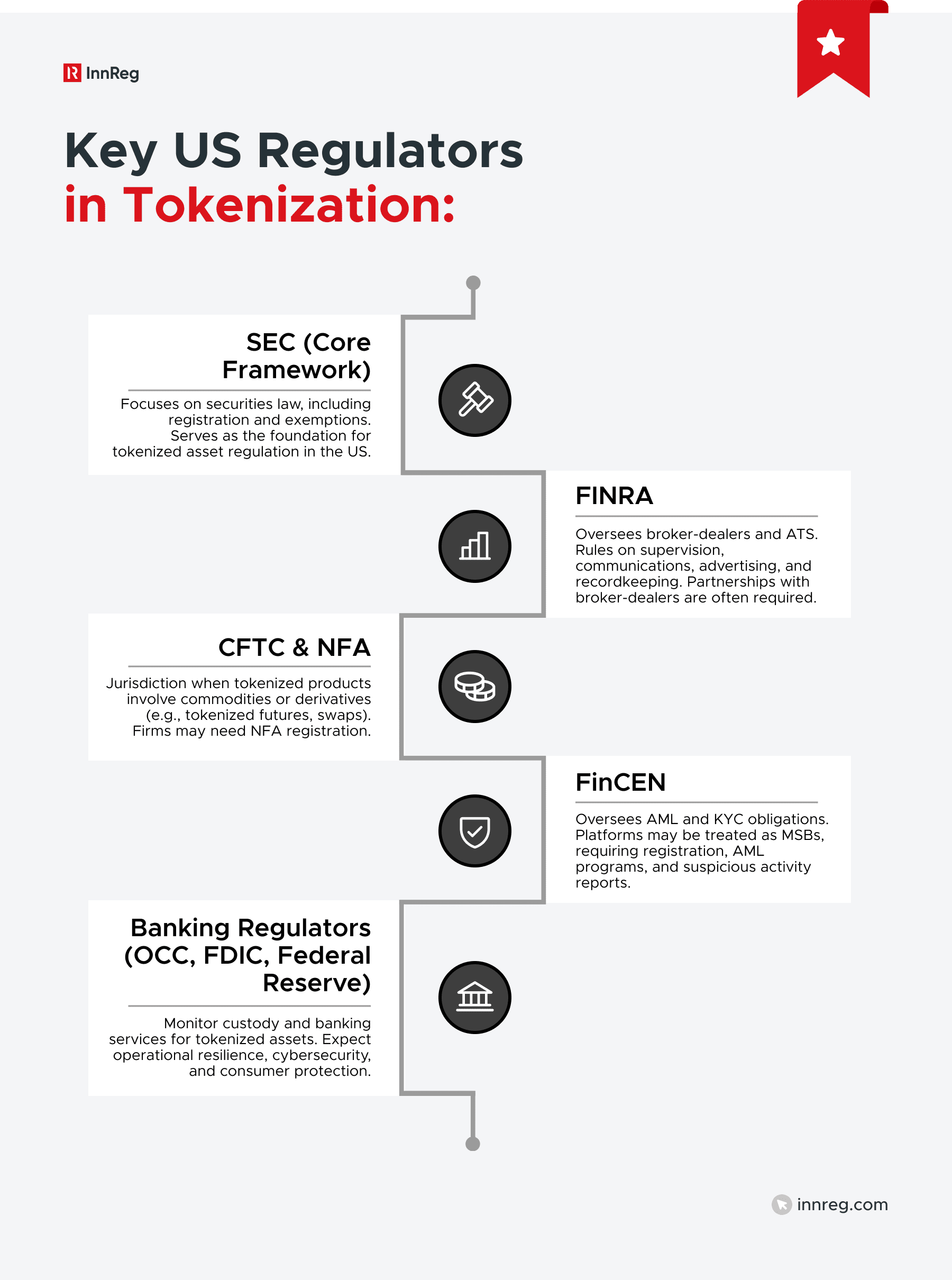

Role of FINRA and Other US Regulators

While the SEC sets the core framework for tokenized securities, other regulators play important roles in how these assets are offered, traded, and supervised.

FINRA: FINRA oversees broker-dealers and Alternative Trading Systems. Any firm dealing in tokenized securities must comply with FINRA rules on supervision, communications, advertising, and recordkeeping. For fintech firms, this often means that partnerships with registered broker-dealers are not optional but essential if they want to operate within the regulated market. FINRA also reviews how firms market tokenized offerings to confirm that materials are fair and not misleading.

CFTC and NFA: If a tokenized product represents a commodity or a derivative, the Commodity Futures Trading Commission (CFTC) may have jurisdiction. For example, tokenized futures or swaps would be regulated by the CFTC, and firms may need to register with the National Futures Association (NFA).

FinCEN: The Financial Crimes Enforcement Network (FinCEN) applies AML and KYC obligations. Platforms that facilitate tokenized transactions may be treated as money services businesses (MSBs) and must register with FinCEN, implement AML programs, and file suspicious activity reports.

Banking Regulators: The OCC, FDIC, and Federal Reserve may become involved if banks custody tokenized assets or engage in related services. These agencies are still developing guidance, but they expect the same operational resilience, cybersecurity controls, and consumer protections applied to traditional financial products.

In short, the regulation of tokenized assets in the US is multi-layered. The SEC focuses on securities law, FINRA governs intermediaries, the CFTC oversees derivatives, FinCEN enforces AML, and banking regulators monitor custody when banks are involved. For fintech leaders, coordination across these agencies is a practical necessity when planning a compliant tokenization strategy.

Tokenized Assets Regulation in the EU

The European Union has taken a structured approach to regulating tokenized assets. Rather than creating an entirely new system, EU regulators apply existing securities laws while also introducing frameworks specific to digital assets.

MiFID II and Tokenized Financial Instruments

Under the Markets in Financial Instruments Directive II (MiFID II), tokenized assets that qualify as financial instruments are regulated the same way as their traditional counterparts. This means that if a token represents equity, debt, or another security, it must follow the same rules on investor protection, disclosure, and market conduct.

For fintech issuers, the classification question is critical. A token that confers voting rights or profit participation will almost always be treated as a security. Once classified, the issuer must comply with MiFID II requirements around transparency, suitability, and reporting.

Intermediaries also face obligations. Trading platforms that want to list tokenized securities need authorization as regulated markets, multilateral trading facilities (MTFs), or organized trading facilities (OTFs). This confirms that secondary trading is subject to the same oversight as traditional securities markets.

MiFID II anchors the EU’s stance: tokenized securities are not exempt from existing rules. Instead, the token format is simply another way to represent assets that already fall under regulatory oversight.

MiCA and Its Scope Limitations

The Markets in Crypto-Assets Regulation (MiCA), which came into effect in 2024, is the EU’s dedicated framework for digital assets. Its goal is to create consistency across member states by regulating crypto-assets that fall outside existing financial instruments legislation.

MiCA covers three broad categories: asset-referenced tokens (such as stablecoins tied to a basket of currencies or assets), e-money tokens, and other crypto-assets not classified as securities. It sets requirements for issuers, including white papers, authorization, and operational standards for custody and governance.

However, MiCA does not apply to tokenized securities. If a token qualifies as a financial instrument under MiFID II, it falls outside MiCA and must comply with securities regulation instead. For fintech firms, this distinction is crucial. Calling a token a “crypto-asset” does not exempt it from securities laws if its features meet the MiFID II definition.

The result is a dual framework: MiFID II governs tokenized securities, while MiCA governs other forms of digital assets. Founders and compliance officers must evaluate their product carefully to determine which set of rules applies.

The DLT Pilot Regime for Market Infrastructure

The EU launched the Distributed Ledger Technology (DLT) Pilot Regime in 2023 to test how tokenized securities can be traded and settled within a regulated environment. The program allows certain market participants to operate with temporary exemptions from parts of MiFID II and related rules, giving regulators a controlled way to study the risks and benefits of blockchain-based infrastructure.

Under the regime, approved entities like trading facilities or central securities depositories can test DLT-based systems. These platforms may handle tokenized shares, bonds, or fund units, but only within set limits on market size and asset types. The goal is to see how settlement, custody, and investor protection work when tokens replace traditional records.

For fintech firms, the DLT Pilot Regime shows that EU regulators are open to experimenting with tokenization. Participation, however, is not a free pass. It requires formal approval and strict compliance with risk management, cybersecurity, and reporting standards.

National Regulators and Prospectus Requirements

Even with EU-wide rules, national regulators remain central to the oversight of tokenized assets. In most jurisdictions, public offerings of tokenized securities require a prospectus approved by the national authority, unless the issuer qualifies for an exemption. These exemptions may apply to small offerings, private placements, or offerings targeted at professional investors only.

For example, BaFin in Germany and the AMF in France have each published guidance confirming that tokenized securities fall under existing securities laws. They require issuers to prepare disclosures that explain both the underlying asset and the technical features of the token, such as custody arrangements and transfer mechanics. This added layer of detail reflects regulators’ concern that investors understand the risks of digital formats as well as the economics of the asset itself.

National regulators also monitor trading venues. Platforms that want to admit tokenized securities must seek authorization, and in some cases, regulators may apply additional supervision to test how blockchain-based settlement interacts with existing market infrastructure.

See also:

Tokenized Assets Regulation in the UK

The UK takes a similar approach to the EU in treating tokenized assets: if a token qualifies as a security under existing law, it is regulated as one. For fintech companies, the classification matters because once a token is deemed a security, all of the rules around disclosure, custody, and trading apply. This includes requirements for firms arranging deals, holding client assets, or operating trading venues.

FCA Approach to Security Tokens

The Financial Conduct Authority (FCA) treats security tokens in the same way as traditional securities. If a token represents rights such as ownership, dividends, or repayment of debt, it falls under the Financial Services and Markets Act. Once classified, the token and any activity around it require authorization or exemption.

This means platforms that list tokenized securities must be recognized as regulated markets, MTFs, or other authorized venues. Firms that arrange or promote investments also need FCA approval. The regulator looks closely at how tokens are marketed to promote fair and clear communications.

For fintech founders, the FCA’s stance highlights an important point: the technology used to issue or trade securities does not change the legal outcome. If the product is a security, it is regulated as one. That’s why compliance planning should begin with classification and then move to choosing the correct authorization path.

Authorization and Licensing Requirements

In the UK, firms dealing with tokenized securities must obtain the same authorizations required for traditional financial instruments. The type of license depends on the activity. Issuers offering securities to the public may need approval for their offering documents. Trading platforms that facilitate buying and selling must also be authorized as regulated markets or MTFs.

The FCA reviews applications by looking at governance, financial resources, compliance controls, and risk management. For fintech startups, this usually means preparing detailed documentation that explains business models, policies, and technology. The regulator wants firms to show that tokenized operations provide the same level of investor protection as traditional ones.

Many early-stage companies partner with authorized broker-dealers or custodians so they can operate on established infrastructure. These partnerships can help, but they do not remove the firm’s own responsibility to meet FCA requirements. That’s why licensing decisions should be built into strategic planning from the very beginning.

Prospectus and Disclosure Obligations

In the UK, tokenized securities offered to the public must meet prospectus requirements unless an explicit exemption applies. A prospectus outlines key details about the issuer, the rights attached to the tokens, and the risks involved. The FCA reviews these documents to verify that investors have the information they need to make informed decisions.

Even with available exemptions, such as for smaller offerings, private placements, or sales to professional investors only, issuers must still follow general disclosure rules and anti-fraud standards. Marketing materials also come under scrutiny, which means whitepapers or promotional decks for tokenized offerings must be prepared with the same care as traditional securities disclosures.

These responsibilities extend beyond the initial offering. Firms may also face ongoing reporting and disclosure obligations, particularly when they rely on exemptions or list tokens on regulated platforms. For compliance teams, the key is to anticipate these requirements from the start so that regulatory gaps do not emerge later.

Regulatory Sandboxes and Innovation Initiatives

The UK has built a reputation as a hub for financial innovation by introducing regulatory sandboxes. These programs let firms test tokenized securities and related services under FCA supervision, while receiving temporary relief from some requirements. The aim is to assess risks and benefits in a controlled environment before moving to full compliance.

For fintech startups, joining a sandbox can validate new business models and show regulators a willingness to operate within the rules. We’ve already seen several pilots run with tokenized bonds, fund shares, and settlement systems. The FCA closely monitors these projects, gathering insights on investor protection, operational resilience, and market stability.

At the same time, the UK government and regulators are exploring broader digital asset initiatives, such as research into digital securities infrastructure and potential reforms to make tokenized trading easier. These steps highlight the country’s openness to innovation, but it is important to note that sandbox participation does not remove the need for licensing and long-term compliance. Instead, it provides a temporary space to experiment under regulatory oversight.

Other Global Perspectives on Tokenization

Outside the US, EU, and UK, other countries are finding their own ways to regulate tokenized assets. Together, these examples show how tokenization is moving from small pilots to structured rules across global financial hubs.

Singapore: MAS and Project Guardian

The Monetary Authority of Singapore (MAS) has taken a proactive stance on tokenized assets. Its approach is technology-neutral: if a token represents a security, it is regulated as one under the Securities and Futures Act. Issuers, trading platforms, and custodians must meet the same licensing and compliance requirements as traditional financial market participants.

Singapore is also notable for its industry collaboration. Through Project Guardian, MAS has partnered with banks, asset managers, and technology providers to test real-world use cases for tokenized bonds, funds, and cross-border settlement. These pilots aim to explore efficiency gains while keeping investor protection at the center.

For fintech firms, Singapore’s framework provides both clarity and opportunity. The rules are strict, but they are clearly defined, and the sandbox environment allows for experimentation under regulatory supervision. This combination has made Singapore one of the leading hubs for tokenization projects in Asia.

Switzerland: Legal Recognition of Tokenized Securities

Switzerland has been one of the first jurisdictions to give tokenized securities explicit legal recognition. In 2021, the country introduced the Federal Act on the Adaptation of Federal Law to Developments in Distributed Ledger Technology (DLT Act). This law created a new category of “DLT securities,” giving blockchain-based representations of financial instruments the same legal standing as traditional paper or book-entry securities.

For issuers, this means tokens representing equity, bonds, or other instruments can be directly recognized as enforceable rights under Swiss law. Trading venues can also obtain special licenses to operate DLT-based exchanges, where tokenized securities are admitted and traded under regulatory oversight.

Switzerland got this right from a compliance angle. They straight-up said tokens can be legal securities, which cut through all the gray areas that plague issuers and investors elsewhere. That clarity sparked a rush of tokenization projects, especially in private markets and alternative assets. Now firms that want clear rules know exactly where to set up shop.

UAE: ADGM and FSRA Frameworks

The United Arab Emirates, particularly through the Abu Dhabi Global Market (ADGM), has established a clear regulatory framework for tokenized assets. The Financial Services Regulatory Authority (FSRA) treats security tokens as regulated financial instruments and applies existing securities laws to them. This means issuers, exchanges, and custodians must be licensed, just as they would for traditional securities.

ADGM has also introduced a dedicated framework for digital securities, covering issuance, custody, and trading. The rules require firms to demonstrate governance, risk management, and cybersecurity standards appropriate for institutional markets. As a result, several exchanges and service providers have obtained licenses to support tokenized securities in the region.

For fintech firms, the UAE offers a combination of regulatory clarity and growing investor appetite. The framework makes it possible to launch compliant tokenized offerings, but only if firms meet the FSRA’s strict authorization and operational requirements.

Japan: STO Regulations and FSA Oversight

Japan regulates tokenized securities through a clear framework built into its Financial Instruments and Exchange Act (FIEA). Security token offerings (STOs) are treated as public or private offerings of securities, meaning they must follow the same requirements as traditional equity or debt issuances.

The Financial Services Agency (FSA) oversees compliance for tokenized securities. Issuers need to file registration statements for public offerings or qualify for exemptions in private placements. Intermediaries like broker-dealers and exchanges must also be licensed, with the FSA enforcing strict rules on investor protection and disclosure.

In recent years, leading Japanese financial institutions have launched regulated STOs, including tokenized corporate bond offerings. These projects show Japan’s commitment to bringing blockchain into its capital markets while maintaining strong regulatory safeguards.

For fintech firms, Japan offers a relatively mature environment for tokenized securities, but one that comes with significant compliance obligations. The FSA’s oversight is detailed and conservative, making it critical to closely align tokenized products with existing securities frameworks.

Compliance Challenges for Fintechs Using Tokenization

Tokenization opens the door to new ways of raising capital and accessing markets, but it doesn’t make compliance any easier. In fact, it often adds complexity, since firms need to layer traditional securities rules on top of blockchain operations.

Asset classification risk: Determining whether a token is a security or a non-security crypto asset is now a central compliance challenge. This analysis affects licensing, disclosures, custody, and trading requirements, and may evolve over time as the project develops.

Structuring offerings and licensing hurdles: The first step in designing a compliant tokenized security is figuring out whether the asset qualifies as a security under existing law. If it does, issuers need to either register or rely on an exemption. Each option comes with limits on who can invest, how tokens can be marketed, and when they can be resold. For many fintechs, licensing is a genuine hurdle, since broker-dealer partnerships, custody solutions, and ATS access are often required.

KYC/AML and investor verification: Blockchain may streamline transactions, but regulators still expect full compliance with AML and KYC rules. Platforms must verify investor identities, monitor activity, and file suspicious reports when needed. The challenge is combining smooth, automated onboarding with strong compliance controls, especially when investors come from multiple jurisdictions.

Transfer restrictions and lock-ups: Securities issued under exemptions like Reg D or Reg CF come with holding periods and resale restrictions. Smart contracts can enforce these rules, but only if they’re carefully coded and tested. Compliance teams also need to monitor secondary transfers closely, since regulators will hold issuers accountable if restricted tokens move improperly.

Cross-border regulatory risks: While tokens can move easily across borders, the laws that govern them do not. A structure that works in the US might not be valid in the EU or Asia. That means fintech firms have to decide whether to geo-fence their offerings, apply for multiple approvals, or work with licensed partners in each jurisdiction.

Custody, recordkeeping, and smart contract design: Custody is one of the most unsettled parts of tokenization. Regulators expect client assets to be safeguarded by qualified custodians, but digital wallets and private keys introduce new risks. At the same time, smart contracts must match legal agreements exactly, or investor rights could be at risk. Compliance officers often end up bridging the gap, making sure blockchain records and traditional books both line up for audits.

See also:

Notable Real-World Examples of Tokenized Assets

Tokenization has moved beyond whitepapers and small pilots. Real-world projects across different asset classes now show how tokenized assets work in practice, offering valuable lessons on regulation and investor outcomes.

Real Estate: St. Regis Aspen Resort

The St. Regis Aspen Resort became a landmark case in 2018 when its owners launched a Regulation D offering to tokenize equity in the property. Accredited investors could buy Aspen Coins, digital tokens that represented fractional ownership in the luxury hotel, and the sale raised about $18 million.

The project showed both the potential and the limits of tokenization. It gave more investors access to a high-value asset and hinted at new liquidity through secondary markets. At the same time, resale was still restricted by securities laws, making it clear that tokenization does not remove holding periods or accredited investor requirements.

Private Equity: KKR

In 2022, KKR partnered with Securitize to tokenize part of its Health Care Strategic Growth Fund II. This was a milestone moment, as one of the world’s top private equity firms opened blockchain-based access to a flagship product. Accredited investors could participate through a digital platform, with tokens representing ownership stakes in the fund.

For compliance professionals, the lesson is clear: KKR managed to balance innovation with regulation. The fund followed US securities law, with accreditation checks and resale restrictions built into the digital process. It proved that even large institutional players see tokenization as a way to expand investor access while staying firmly within regulatory boundaries.

Bonds: The World Bank’s “bond-i”

The World Bank’s Blockchain Operated New Debt Instrument, known as “bond-i,” was issued in 2018 on a private Ethereum blockchain. This bond raised more than AUD 100 million and was managed with the Commonwealth Bank of Australia. It became the first bond to be created, allocated, transferred, and managed entirely through distributed ledger technology.

Bond-i showed how blockchain can make issuance and settlement faster and more efficient, cutting down both costs and time. Just as important, it highlighted the value of regulatory and institutional collaboration. By working closely with regulators and global banks, the World Bank proved that tokenized debt instruments could be rolled out responsibly and at scale.

Commodities: Paxos Gold (PAXG)

Paxos launched Paxos Gold as a regulated digital token backed by allocated gold bars stored in Brink’s vaults in London. Each token represents one fine Troy ounce of gold, and holders can even redeem their tokens for the physical metal. Oversight from the New York State Department of Financial Services confirms that custody and issuance meet regulatory standards.

This case shows how tokenization can make access to traditional commodities much easier. Instead of handling storage, transport, or logistics, investors can hold a token that carries the same value as physical gold. The regulated structure also gives investors confidence that every token is tied to a real, safeguarded asset.

Funds: Franklin Templeton

In 2023, Franklin Templeton expanded its OnChain US Government Money Fund, the first US-registered mutual fund to process transactions and record ownership on a blockchain. The fund invests in government securities and cash, and investors can buy tokenized shares through a digital platform.

What makes this important is that the SEC approved the structure, bringing a traditional mutual fund into a blockchain setting. The blockchain handles recordkeeping and transparency, while the fund itself still follows the Investment Company Act of 1940. This balance of innovation and compliance shows how tokenization can fit directly into mainstream asset management.

Recent Updates and Trends in Tokenization

The regulatory and market landscape for tokenized assets is changing fast. Early projects were mostly pilots or small-scale offerings, but in recent years, we’ve seen clearer regulatory guidance and growing interest from major institutions. For fintech founders, keeping up with these shifts is key to building strategies that stay compliant and competitive.

SEC Guidance and Roundtables in 2025

In 2025, the SEC used staff roundtables and public statements to reinforce its view that tokenized securities are not a new asset class but simply a new format for existing ones. Regulators emphasized disclosure, investor protection, and the need to align smart contract features with legal documentation. A recurring theme is that technology cannot override the law.

For example, if a tokenized bond automates coupon payments but does not disclose risks, it is still non-compliant. The SEC is also exploring whether blockchain features such as immutable ledgers can support audit and reporting, but it has made clear that these cannot replace statutory obligations.

SEC FAQs Relating to Crypto Asset Activities and Distributed Ledger Technology

In December 2025, the SEC’s Division of Trading and Markets released detailed FAQs addressing crypto asset activities and distributed ledger technology.

Rather than introducing new rules, the guidance explains how existing securities regulations apply when blockchain and tokenized assets are used within regulated financial markets. The central message is consistent with prior SEC statements: tokenization does not change the legal framework. It changes the format.

The FAQs clarify how long-standing rules apply across custody, trading, settlement, and recordkeeping. For broker-dealers, the SEC emphasized that key obligations under the Customer Protection Rule, net capital requirements, and SIPA continue to apply when crypto assets qualify as securities.

The staff also confirmed that broker-dealers may establish possession or control of tokenized securities without physical certificates and that reliance on the 2020 Special Purpose Broker-Dealer framework is not mandatory.

SEC Interpretation on Crypto Asset Classification (2026)

In March 2026, the SEC issued an interpretation clarifying how federal securities laws apply to crypto assets and related activities. This marks a significant shift toward a more structured and transparent regulatory approach.

A key element of the interpretation is a clearer classification framework for crypto assets. The SEC now distinguishes between categories such as:

Digital commodities

Digital collectibles

Digital tools

Stablecoins

Digital securities.

Most importantly, the SEC acknowledged that most crypto assets aren’t securities themselves, even though certain transactions involving them may still fall under securities laws.

This reinforces a critical distinction: the asset itself isn’t automatically a security, but the way it’s offered, sold, or marketed can create an investment contract.

The SEC also clarified that an investment contract isn’t permanent. A crypto asset may initially be offered as part of a securities transaction, but over time, as reliance on a central issuer or promoter decreases, that classification may change. This introduces a more dynamic view of how regulatory treatment can evolve as projects mature.

In addition, the interpretation provides guidance on activities such as staking, mining, airdrops, and token wrapping, explaining how these functions may fall outside securities laws when they don’t involve an investment contract.

For tokenized asset projects, this update doesn’t reduce compliance obligations. Instead, it raises the importance of careful classification, clear disclosures, and ongoing monitoring, especially as tokens and platforms evolve over time.

FINRA/SEC Updates on Custody and Broker-Dealers

Custody of tokenized assets is still one of the toughest regulatory challenges. In late 2024 and early 2025, the SEC and FINRA issued new guidance making it clear that broker-dealers handling tokenized securities must meet the same standards as they do for traditional assets.

That means segregating client funds, conducting independent audits, and maintaining strong cybersecurity. The guidance also pointed out that wallet management creates new risks, like private key loss and fraud, so firms need layered security controls. For broker-dealers moving into tokenized trading, the big test is building custody systems that protect investors while fitting within long-standing rules.

In the recently published FAQs on Crypto Asset Activities and Distributed Ledger Technology, the SEC has clarified several long-standing points of uncertainty. For broker-dealers, the key distinction is whether a crypto or tokenized asset qualifies as a security.

Enforcement Trends in the US

The SEC is still cracking down on issuers that blur the line between utility tokens and securities. In several enforcement cases from 2024 and 2025, regulators focused more on how tokens were marketed than on how they were technically designed. Promises of profit, appreciation, or liquidity were treated as signs of an investment contract under the Howey Test.

The message is clear: even if a token has a real functional use, it will probably be regulated as a security if it is promoted as an investment. For compliance teams, the takeaway is the need to align legal analysis, product design, and marketing strategy right from the start.

International Pilots and Sandboxes

Around the world, regulators are testing tokenized markets in controlled settings. The EU’s DLT Pilot Regime has already admitted its first platforms, letting them trade tokenized shares and bonds under limited exemptions from MiFID II. In Singapore, Project Guardian expanded in 2024 to include cross-border settlement pilots with global banks, focusing on tokenized bonds and funds.

The UK’s sandbox is now looking at tokenized money market products. These programs matter because they show regulators experimenting with blockchain infrastructure while still keeping investor protection front and center. They also make it clear that wider acceptance will depend on proving resilience, security, and compliance at scale.

FAQs on Tokenization in Fintech

What’s the difference between tokenization and securitization?

Securitization takes assets like mortgages or loans and bundles them into tradable securities. Tokenization is different. It represents ownership of an asset in digital form on a blockchain. The two can overlap, for example, when securitized assets are also tokenized, but they are not the same thing.

How are tokenized assets taxed?

Tokenized securities are taxed just like their traditional counterparts. Equity tokens are subject to capital gains tax when sold, and dividends are treated as income. Bond tokens follow the usual tax rules for interest. The blockchain format does not change these rules, but keeping accurate records is essential.

Can retail investors buy tokenized securities?

Access to tokenized securities depends on how they are issued. Under exemptions like Regulation D, only accredited investors can take part. Regulation A+ and Regulation CF open the door to retail investors but come with limits and disclosure requirements. In the EU and UK, access is tied to prospectus rules and how the tokens are classified under securities law.

How does custody work for tokenized assets?

Custody means protecting both the tokens and the private keys that control them. Regulators expect custody to be handled by qualified custodians or licensed broker-dealers. The same standards used for traditional securities apply, including segregation of assets, independent audits, and strong operational resilience, only now in a blockchain environment.

Are tokenized assets treated as securities in the US?

In most cases, yes. If a token meets the criteria of the Howey Test, the SEC treats it as a security. This applies whether the token represents equity, debt, or another type of investment contract. Issuers must either register the offering or use an exemption, just as they would with traditional securities.

—

Tokenization is changing the way financial assets are issued, traded, and managed. It brings faster settlement, broader investor access through fractional ownership, and new possibilities with programmable smart contracts. But it also introduces complex regulatory and compliance challenges.

For fintech founders, lawyers, and compliance officers, the key takeaway is clear: tokenized assets are still governed by the same securities laws as traditional ones. The real innovation is in format and infrastructure, not in escaping regulation.

As tokenization moves from pilots to mainstream adoption, the firms that take a practical, compliance-first approach will be best positioned to unlock its benefits while avoiding unnecessary risks.

Adriana is a Principal Consultant at InnReg with 8 years of compliance experience specializing in VASP licensing and regulatory frameworks across Europe and LATAM. She has held senior compliance roles at leading global crypto and financial institutions, including Gate.io, Binance, Santander Bank, and BNP Paribas, with deep expertise in KYC/AML operations, MiCA adaptation, and building compliance programs from the ground up.

How Can InnReg Help?

InnReg is a global regulatory compliance and operations consulting team serving financial services companies since 2013.

We are especially effective at launching and scaling fintechs with innovative compliance strategies and delivering cost-effective managed services, assisted by proprietary regtech solutions.

If you need help with compliance, reach out to our regulatory experts today:

Related Articles

Featured LinkedIn Posts