Tokenized real estate is gaining traction across fintech, real estate, and investment circles. But for many founders, compliance officers, and legal teams, the concept of tokenization still feels vague. Is it crypto? Is it a security? Is it even legal? The short answer is it depends on how it’s structured, and the details matter.

In this guide, we’ll break down key aspects of tokenized real estate. We’ll explain how it works, how regulators treat it in the US and abroad, the most common deal structures, and the practical compliance hurdles that even experienced teams often encounter.

If you're trying to build something innovative with your tokenized real estate that mitigates regulatory risks, you're in the right place. But first, let’s clear the basics:

At InnReg, we help fintech and real estate platforms structure tokenized offerings the right way. From Reg D/Reg A+/Reg S strategies to KYC/AML, custody workflows, and ATS/broker-dealer integrations, our team supports launch and ongoing operations. Contact us to discuss your roadmap.

What Is Tokenized Real Estate?

Tokenized real estate refers to converting real-world property rights into digital tokens that live on a blockchain. These tokens can represent ownership, income rights, equity in a legal entity, or even a share of rental profits.

In short, tokenization takes traditional real estate interests and turns them into programmable, trackable digital assets.

The tokens themselves don’t hold the property. Instead, they represent legal rights tied to a structure, usually an LLC or other entity that owns the property. Buyers of the tokens become fractional owners or investors in that entity, depending on how the deal is set up.

The concept isn’t new in substance since real estate has long been fractionalized through vehicles like Real Estate Investment Trusts (REITs), syndications, and private placements. What’s new is the use of blockchain technology to issue, manage, and potentially trade those interests more efficiently and transparently.

In most cases, tokenized real estate offerings fall under securities regulations. That’s because the token often represents an investment interest with an expectation of profit based on the efforts of others.

As a result, tokenized real estate typically requires the same legal and compliance infrastructure as any traditional securities offering, including proper disclosures, investor onboarding, and transfer restrictions.

Is Tokenized Real Estate a Security?

In most cases, yes. Tokenized real estate is typically treated as a security under US law. That’s because the token often represents an investment in a common enterprise, with profits expected from the efforts of a sponsor, manager, or platform—meeting the SEC’s Howey Test criteria for an “investment contract.”

The SEC has recently intensified its focus on tokenization, launching Project Crypto and opening multiple rulemaking dialogues around tokenized securities. This reinforces that tokenized real estate falls squarely under existing securities laws.

It doesn’t matter if the asset is represented by a blockchain token instead of a paper share certificate. Regulators focus on substance over form. The token becomes a security if it offers investors rights to:

Income

Appreciation

Ownership in a property-holding entity

As a result, tokenized real estate must comply with federal securities laws. That includes either registering the offering with the SEC or relying on an exemption like Regulation D, Regulation S, or Regulation A+. It also means you have to:

Enforce transfer restrictions

Verify investor eligibility

Make appropriate disclosures

This is where fintech teams often need specialized support. InnReg specializes in guiding fintech companies through the intricacies of securities compliance, including determining the appropriate exemptions (like Reg D, Reg S, or Reg A+) and implementing necessary disclosures and investor verifications.

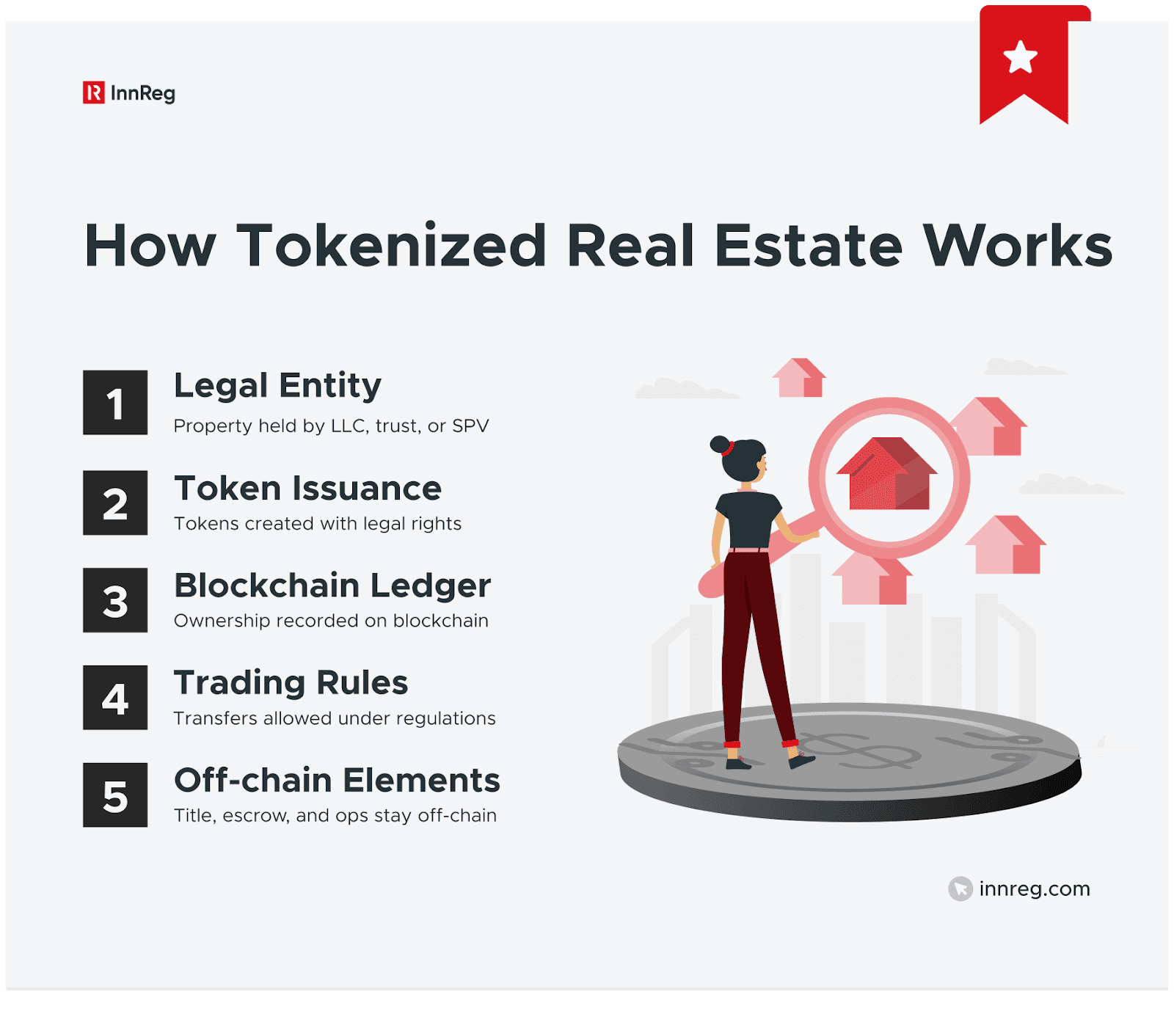

How Does Tokenized Real Estate Work?

Tokenized real estate combines traditional legal structures with blockchain-based technology. Here's how it typically comes together:

Step 1: The Real Estate Is Placed Into a Legal Structure

The property is not tokenized directly. Instead, it's held by an entity in the form of an LLC, a trust, a limited partnership, or another form of SPV. This entity owns the title to the property. Investors purchase interests in the entity, not the property itself.

Step 2: Digital Tokens Represent Ownership or Economic Rights

Each token is tied to legal rights defined in offering documents and entity agreements. These rights are enforceable through contracts, not just code. Depending on the structure, a token might give the holder:

A fractional ownership interest in the SPV

A share of rental income

Voting rights on key decisions

A claim to proceeds from a future sale

Step 3: Blockchain Records Token Ownership

Tokens are issued on a blockchain platform, such as Ethereum. The blockchain acts as a ledger that tracks ownership and transfers.

Smart contracts can be programmed to enforce transfer restrictions (e.g., accredited investors only) and automate distributions (e.g., rental income or dividends). They can also be programmed to manage investor whitelists and cap tables.

Step 4: Trading and Transfers (When Allowed)

Secondary trading may be possible, but only under specific conditions. Tokens representing securities can’t be traded freely unless:

The platform is a registered broker-dealer or ATS

The offering has passed the applicable holding period

Transfers comply with regulatory exemptions

In some cases, peer-to-peer transfers are allowed if the legal framework supports it and proper controls are in place.

Step 5: Off-Chain Functions Still Apply

Tokenization adds efficiency, but it doesn’t replace the real-world infrastructure. Blockchain handles the digital layer, but core real estate functions remain off-chain. For example, the title and deed are still recorded with the local authorities.

Escrow, legal review, and compliance processes still apply. As for property management and tenant operations, they remain unchanged as well.

Common Tokenized Real Estate Structures

Tokenized real estate can be structured in different ways depending on the type of asset, the investor base, and the regulatory strategy. Most offerings use legal wrappers that are familiar to private markets but add a blockchain-based token layer for tracking and transferability.

SPVs, LLCs, and Legal Wrappers

In nearly all cases, the underlying property is held by a legal entity, not directly by the investors. That entity is usually structured as:

A limited liability company (LLC)

A limited partnership (LP)

A statutory trust or business trust

A corporation (less common for private deals)

The entity owns the property. Investors hold tokens that represent an interest in the entity, similar to membership units or limited partnership interests in traditional real estate syndications.

This approach provides legal separation between the asset and the investors and allows for clear governance, profit distribution, and transfer rules. It also makes it easier to comply with securities laws, tax rules, and real estate title requirements.

Equity vs. Debt Tokenization

Most tokenized real estate offerings fall into one of two categories:

Feature | Equity Token | Debt Token |

|---|---|---|

Description | Represents ownership in an entity that owns the property | Represents a lender’s position, such as a tokenized mortgage or note |

Rights | Rights to profits, appreciation, and possibly voting rights | Entitled to repayment of principal plus interest |

Best For | Longer-term investments | Short-term investments or fixed-income products |

Typical Assets | Rental properties, commercial buildings, and development projects | Real estate-backed loans, mortgages |

Risk Profile | Higher exposure to market fluctuations and property value changes | Lower risk with more predictable returns (interest-based) |

Return Type | Profit sharing, capital appreciation | Interest income |

In either case, the token reflects a legal claim under contract. Whether structured as equity or debt, the offering must be drafted to align the token’s features with enforceable investor rights.

Benefits of Tokenized Real Estate

Tokenized real estate offers potential benefits over traditional deal structures, especially for platforms and sponsors operating in fintech. The value isn’t just in the technology. It’s in what that technology enables when applied thoughtfully and within the legal framework.

Liquidity

Here’s a fact: real estate is traditionally illiquid. But tokenization can reduce friction by allowing fractional interests to be traded more easily, either peer-to-peer or on regulated secondary markets.

That said, liquidity is never automatic. Transfer restrictions, investor eligibility, and platform limitations still apply. When structured properly, tokenization can create more opportunities for liquidity, but it doesn’t eliminate the need for regulatory compliance or market demand.

Lower Investment Minimums

By fractionalizing ownership, tokenized offerings can lower the barrier to entry for investors. Instead of committing hundreds of thousands of dollars, investors might participate with just a few hundred or a few thousand.

This may help lower investment barriers and broaden access to more investors, especially when using Regulation D, Regulation A+, or similar frameworks that support scalable distribution.

Operational Efficiency

Blockchain technology allows platforms to automate routine tasks like:

Tracking ownership

Distributing income

Managing cap tables

Enforcing transfer restrictions

Smart contracts can simplify internal processes, reduce administrative overhead, and support better data integrity. For fintech teams, this creates opportunities to scale without expanding compliance headcount at the same rate.

Transparency and Auditability

The blockchain ledger records every token transaction in real time. This automatically creates a transparent, auditable trail of ownership, which is useful for both investor reporting and regulatory oversight for you.

And if we zoom in on platforms that manage multiple offerings or investor types, tokenization can actually help standardize how information is tracked and verified across the lifecycle of the investment.

See also:

Challenges of Tokenized Real Estate

Tokenization introduces flexibility, but also complexity. Beyond technical challenges, there are legal, operational, and regulatory challenges ahead. Here are five areas where fintech teams, platforms, and sponsors often run into friction.

Securities Law Compliance

If the token represents an investment interest with the expectation of profit from someone else’s efforts, it’s a security. That triggers SEC oversight.

You’ll need to either register the offering or use an exemption like Reg D, Reg S, or Reg A+. That also means handling investor accreditation, disclosures, transfer restrictions, and more. Failing to treat tokenized real estate as a security is one of the fastest ways to attract regulatory scrutiny.

Custody and Investor Safeguards

Holding real estate tokens on a blockchain wallet creates questions around custody. Can investors self-custody? Do you need a qualified custodian? What happens if keys are lost?

In the US, digital asset custody rules are still evolving. Platforms need to think through not just how tokens are stored, but how investor rights are protected, especially if tokens represent real legal claims to cash flows or asset ownership.

Smart Contracts vs. Legal Realities

Smart contracts can enforce rules, but they don’t replace legal agreements. Token holders still rely on contracts, operating agreements, and local real estate law.

If a dispute arises over cash flow distributions, governance, or anything else, blockchain code alone won’t resolve it. The outcome depends on how the rights are documented off-chain. Fintech teams need to coordinate legal and technical design early in the process.

Cross-Jurisdiction Compliance

Tokenized real estate platforms often attract investors globally. That brings complexity. Securities laws, tax rules, and property rights vary by country, and sometimes by state.

You’ll need a compliance plan that maps out where investors are located, what rules apply, and what limitations you need to bake into the offering. One wrong assumption can trigger legal exposure in a market you didn’t mean to enter.

Secondary Market Liquidity Constraints

Trading tokenized assets isn't plug-and-play. In most cases, secondary market activity is restricted by law. Tokens can't be freely sold to the public unless you're using a registered exchange or ATS, and even then, compliance requirements still apply.

That makes liquidity harder to deliver than many assume. You need to structure the offering carefully, choose the right trading partners, and avoid overpromising liquidity that may not materialize.

Need help with blockchain compliance?

Fill out the form below and our experts will get back to you.

US Regulatory Framework for Tokenized Real Estate

In the United States, tokenized real estate is governed by the same core financial regulations that apply to any securities offering.

The technology may be new, but the legal requirements are not. If the tokenized interest qualifies as a security, you’ll need to comply with federal securities laws and, in some cases, state-level rules as well.

Here are the key regulatory components fintech teams should understand:

Securities and Exchange Commission (SEC)

As previously mentioned, the SEC treats most tokenized real estate offerings as securities offerings. That means you must either:

Register the offering with the SEC

Rely on an exemption such as

Regulation D,

Regulation S, or

Regulation A+

Each exemption comes with specific conditions, such as investor eligibility, advertising limits, disclosure requirements, and resale restrictions. Ignoring these details can lead to enforcement action, even if the underlying project is legitimate.

The SEC also governs secondary trading. If your platform facilitates token trades, you may need to register as a broker-dealer or operate through a regulated Alternative Trading System (ATS).

Financial Industry Regulatory Authority (FINRA)

If you're using a broker-dealer to distribute tokens or facilitate trades, that entity must be registered with FINRA. This also applies if you're working with a third-party ATS.

FINRA enforces rules around:

Communications with investors (FINRA Rule 2210)

Suitability obligations (FINRA Rule 2111)

Recordkeeping and operational controls (FINRA Rule 4511)

Tokenized real estate may involve novel tech, but broker-dealer obligations still apply in full.

State Securities Regulators

While federal exemptions can preempt many state-level filing requirements, you may still need to submit notices (e.g., Form D) and pay state fees depending on where your investors are located.

Some states also scrutinize tokenized offerings under real estate or consumer protection laws. It's essential to understand how your structure fits under local rules, especially if you're marketing to retail investors.

Other Agencies (As Applicable)

Depending on your structure and operations, other regulators may get involved:

CFTC: If you offer derivative exposure to real estate values

IRS: For tax treatment of income and capital gains

FinCEN: If your platform handles payments or crypto, triggering AML obligations

OCC and state banking agencies: If custody is offered through a trust company or bank partner

The key takeaway: Tokenized real estate doesn’t exempt you from the regulatory framework. It adds more layers to manage. This is where experienced compliance support can help navigate complexity and reduce friction, especially for fintech teams moving fast.

International Rules on Tokenized Real Estate

While this article focuses on the US regulatory landscape, many tokenized real estate projects attract international investors or operate across borders. That adds complexity.

Global jurisdictions are moving at different speeds when it comes to regulating digital assets, securities, and cross-border offerings.

Several jurisdictions have recently taken concrete steps, such as Dubai’s large-scale tokenized property initiatives, Hong Kong’s pause on certain RWA activities, and India’s deposit-tokenization pilots.

Here’s a look at how a few key regions are approaching tokenized real estate, and what US fintech teams should keep in mind when marketing or onboarding foreign investors.

See also:

European Union (EU)

The EU’s Markets in Crypto-Assets Regulation (MiCA) framework applies to utility and payment tokens, but not to tokenized securities. Those still fall under existing financial services rules, including MiFID II.

Tokenized real estate offerings in the EU typically require:

Prospectus disclosures (unless exempt)

Licensing for investment services or platforms

Country-by-country compliance (passporting is limited for non-EU issuers)

If you’re onboarding EU investors from the US, you’ll need to check local rules and may need an EU-facing legal wrapper or local partner.

United Kingdom

The UK treats most tokenized real estate offerings as security tokens under the Financial Conduct Authority’s (FCA) guidance.

To market these tokens to UK investors, you may need to:

Register with the FCA or work with a regulated firm

Comply with the prospectus rules or exemptions

Follow AML and investor protection requirements

The UK’s sandbox program has supported several tokenization pilots, but formal requirements still apply when securities are involved.

Switzerland

Switzerland has been an early leader in tokenization frameworks. The Financial Market Supervisory Authority (FINMA) recognizes security tokens and allows for DLT-based trading venues.

That said, even in a friendly environment, most tokenized real estate offerings:

Must comply with securities laws

Are subject to AML regulations

Require licensing or registration if tokens are widely offered

Swiss structures are often used by platforms that want to reach international investors under a more flexible regime, but that flexibility still comes with legal obligations.

Singapore

The Monetary Authority of Singapore (MAS) treats tokenized real estate as a form of digital security.

If you're onboarding Singapore-based investors or operating a platform in the region, expect requirements related to:

Licensing under the Securities and Futures Act

AML/KYC controls

Disclosure standards for public offerings

MAS has supported digital asset experimentation, but remains strict when securities are involved.

UAE, Hong Kong, and Others

Other jurisdictions, such as the UAE, Hong Kong, and parts of the Caribbean, have created digital asset frameworks that support tokenized assets. Many focus on:

Sandboxes or innovation licenses

Fintech-friendly banking integration

Clear registration pathways for security token platforms

Managing cross-border regulatory challenges requires a nuanced understanding of international laws. InnReg offers expertise in multi-jurisdictional compliance, assisting platforms in mapping out investor locations, understanding applicable regulations, and implementing controls to mitigate regulatory risks in various markets.

Key Takeaways

Tokenized real estate sits at the intersection of finance, law, and technology. While the tools may be new, the regulatory obligations are not. As we’ve seen, most offerings are securities. Therefore, most platforms must manage risk, disclosure, and investor protections just like any other financial product.

For fintech teams, the opportunity is real, but so is the complexity. Tokenization can reduce friction, lower entry barriers, and modernize back-office operations. But it also introduces legal, technical, and jurisdictional challenges that require a coordinated compliance strategy.

At InnReg, we work with innovative financial companies navigating exactly these types of structures. Whether you're tokenizing a single asset or launching a broader investment platform, our team can assist in bridging the gap between vision and regulatory reality.

If you're exploring tokenized real estate and need to align your structure with US and global rules, we're here to assist you in aligning your structure with regulatory requirements from the outset.

Frequently Asked Questions

How does tokenized real estate work?

Tokenized real estate takes property ownership rights and turns them into digital tokens on a blockchain. The property itself gets held in an LLC or similar entity. When you buy tokens, you're buying into that entity, not the actual real estate. Your tokens give you whatever rights are spelled out in the legal docs (could be rental income, voting rights, a share of sale proceeds, etc.).

Blockchain handles the ownership tracking and can run distributions automatically through smart contracts. Most of the work still happens the old way, though. Titles, property management, compliance stuff - none of that changes. The token is just a cleaner way to track who owns what and maybe trade your stake if the structure allows it.

Is tokenization of real estate legal?

Yes, but it's regulated. Most tokenized real estate counts as a security under US law because it meets the SEC's investment contract test. You either register your offering or rely on an exemption (Reg D, Reg S, or Reg A+ are the common ones).

That means verifying investors, handling disclosures, and enforcing transfer restrictions. All the usual securities compliance applies. Blockchain doesn't give you a pass on any of this. Platforms that think the technology creates some kind of loophole find out quickly that regulators don't see it that way.

What is the difference between tokenized real estate and REITs?

Both let you invest in real estate without buying whole properties, but they work differently.

REITs are companies owning multiple properties that trade like stocks on public exchanges. You can buy and sell anytime the market's open, and they're required to pay out most of their income as dividends.

Tokenized real estate usually means specific properties in SPVs, with tokens representing your piece of that particular deal. Trading is much more restricted unless there's a proper secondary market. Most tokenized deals are private placements with fewer investors. The blockchain makes ownership tracking easier and might improve liquidity eventually, but right now, these deals are way less liquid than public REITs.

Ani is a Senior Compliance Consultant with over 10 years of experience in legal and regulatory compliance across fintech, RegTech, and cross-border payments. She has held roles at Remote and EY, with expertise in AML, GDPR, financial crime, and EU regulatory frameworks. She holds CAMS and CIPP/E certifications.

How Can InnReg Help?

InnReg is a global regulatory compliance and operations consulting team serving financial services companies since 2013.

We are especially effective at launching and scaling fintechs with innovative compliance strategies and delivering cost-effective managed services, assisted by proprietary regtech solutions.

If you need help with blockchain compliance, reach out to our regulatory experts today:

Related Articles

Featured LinkedIn Posts