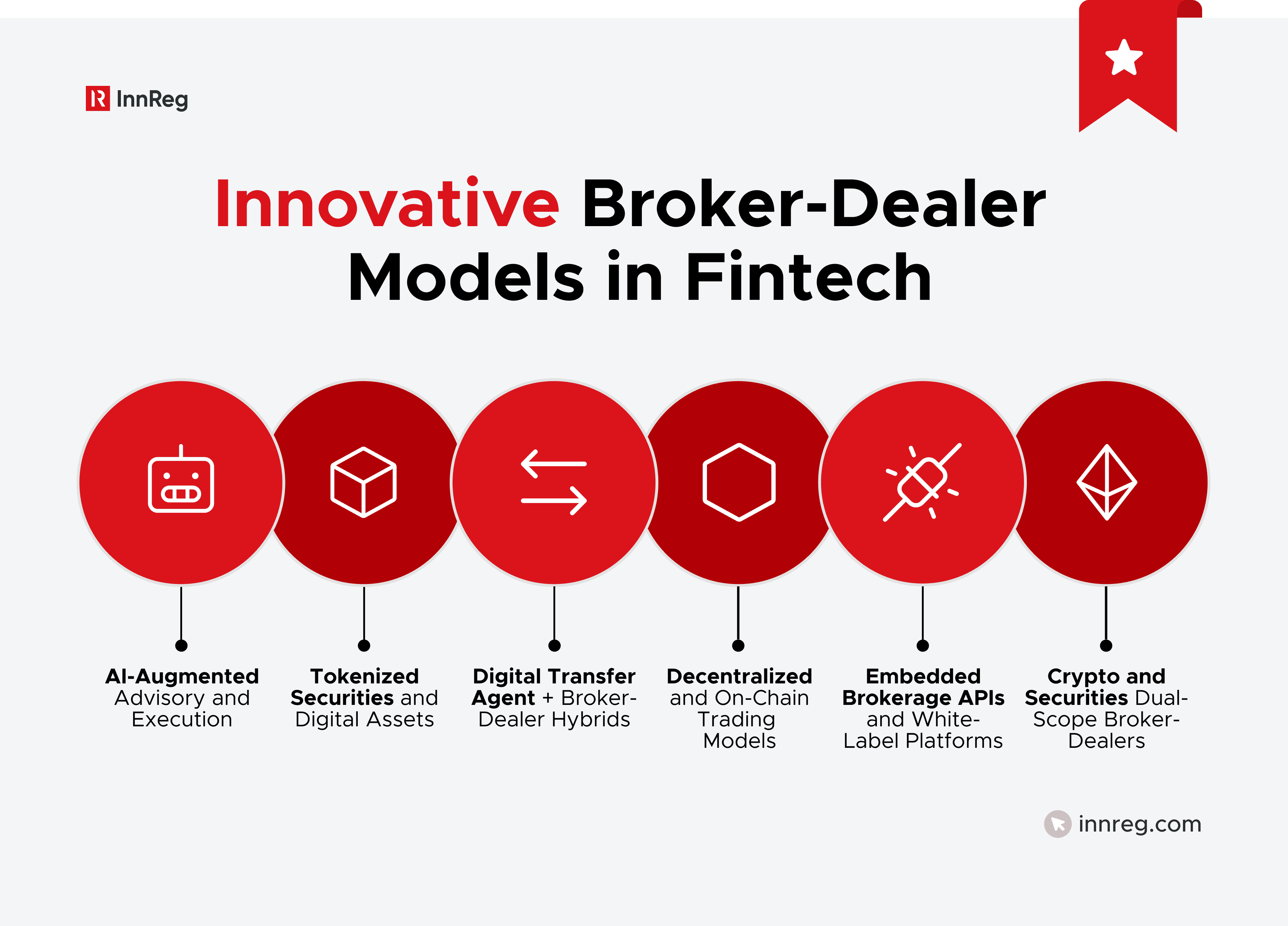

Top 6 Innovative Broker-Dealer Models in Fintech

Fintech is reshaping the brokerage landscape, and a wave of innovative broker-dealer models is redefining how financial products are structured, delivered, and regulated. From AI-enhanced execution strategies to tokenized securities and embedded investment platforms, both startups and incumbents are pushing the boundaries of traditional broker-dealer structures.

However, innovation in this sector extends beyond user experience and interface design.

It requires navigating complex regulatory frameworks, interpreting outdated rules in modern contexts, and establishing scalable compliance operations that can withstand scrutiny from regulators such as the SEC and FINRA.

These demands often create friction for founders, legal teams, and compliance officers, particularly when introducing a model that lacks precedent.

This article outlines the most notable innovative broker-dealer models emerging in fintech, explains what differentiates each one, and details the corresponding compliance and regulatory challenges.

At InnReg, we support fintechs building innovative broker-dealer models. From regulatory structuring to day-to-day compliance operations, our broker-dealer services help teams align with SEC, FINRA, and cross-border expectations.

What Makes a Broker-Dealer Model “Innovative” in Fintech

Innovation in broker-dealer structures often has less to do with novelty and more to do with complexity at scale.

In fintech, the most forward-leaning models are not reinventing what a broker-dealer does. They are redefining how those activities are delivered, structured, and governed under existing regulations.

These models do not just add new features. They push against the boundaries of how brokerage has traditionally been structured. Custody, trade execution, and registration categories start to overlap. This overlap is where both the innovation and the compliance challenges tend to concentrate.

Key categories of innovative broker-dealer models currently shaping fintech include:

AI-Augmented Advisory and Execution | Platforms that use algorithmic tools to personalize portfolios or dynamically route orders, often triggering questions about suitability, Reg BI, and the line between education and recommendation. |

|---|---|

Tokenized Securities and Digital Asset Broker-Dealers | Some firms are structuring tokens on blockchain networks as regulated securities. This introduces complications around how those assets are held, whether trading systems meet ATS requirements, and how ownership transfers are controlled under SEC rules. |

Digital Transfer Agent + Broker-Dealer Hybrids | Firms combining broker-dealer activity with transfer agent functionality, often to enable real-time settlement or blockchain-native security issuance. |

Decentralized and On-Chain Trading Models | Firms exploring decentralized or hybrid trading models must address how core brokerage functions, such as trade execution and asset transfer, are handled when they occur on-chain. This often complicates compliance reviews, especially when there is no clear point of control. |

Embedded Brokerage APIs and White-Label Platforms | Infrastructure providers that allow fintechs or consumer-facing apps to offer securities trading without being broker-dealers themselves require careful delegation of compliance responsibilities. |

Crypto and Securities Dual-Scope Broker-Dealers | Platforms offering both traditional securities and crypto assets under one roof, navigating dual licensing regimes, AML programs, and custody frameworks. |

These models stand out not because of branding or UI, but because of how they reshape core regulatory and operational requirements. They often bring legal, product, and compliance teams to the table earlier than usual because there is no off-the-shelf blueprint.

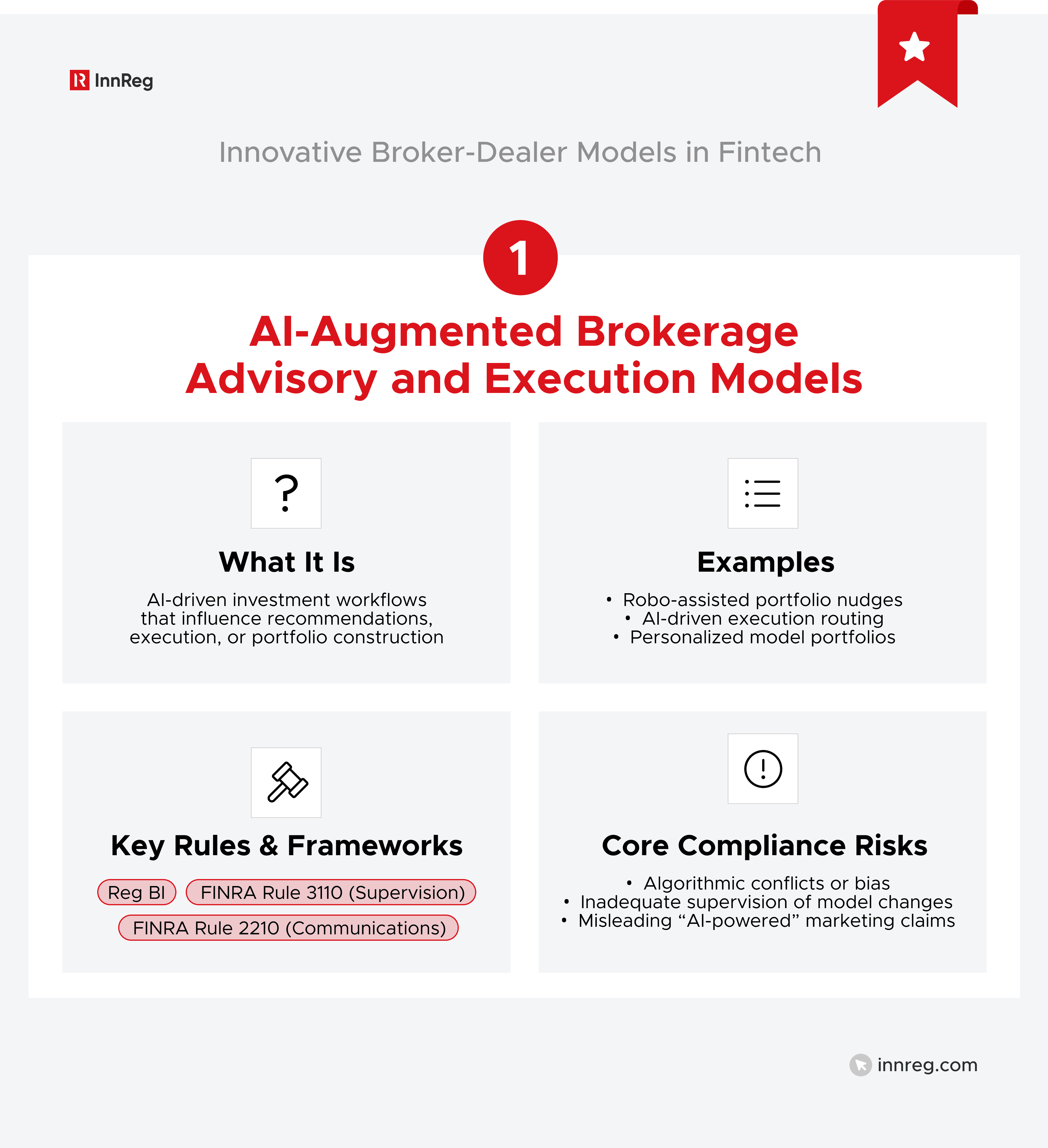

1. AI-Augmented Brokerage Advisory and Execution Models

Some broker-dealers are incorporating AI into investment workflows, either to generate portfolio recommendations or to optimize execution strategies in real time. These tools are often positioned as enhancements to the client experience, but in practice, they introduce regulatory complexity that firms must handle from day one.

Firms need to look closely at what the AI is actually doing. A tool that adjusts investments or offers model portfolios may be treated as a recommendation under Reg BI or as an advisory activity under federal law. That classification drives everything from licensing to disclosure.

Automated systems are subject to the same supervisory standards as any other source of investment input. FINRA expects firms to review these tools for suitability, maintain documentation, and identify any built-in conflicts as they would with a human advisor.

A related concern is how clients interpret the output. Many assume that algorithmic suggestions are objective or tailored, even when they are not. If the system favors certain products or relies on narrow historical assumptions, the firm needs to explain what the user is actually seeing, and it qualifies as advice under regulatory definitions.

Learn more about AI compliance →

Regulatory Considerations

Regulators have not created a separate rulebook for AI-driven brokerage tools. Instead, they apply existing standards to new situations. That means firms must look closely at how the tool operates and how it is presented to users.

Depending on the setup, multiple rules may apply:

Reg BI obligations for broker-dealers making recommendations

Fiduciary duty for registered investment advisors

FINRA Rule 3110 (Supervision) and FINRA Rule 2210 (Communications)

SEC guidance on digital engagement and gamification

Firms pursuing this model must also address how errors are caught. If the AI malfunctions, who notices? What is the remediation process? Regulators will expect internal controls around these questions, even if the firm considers the tool to be passive or educational.

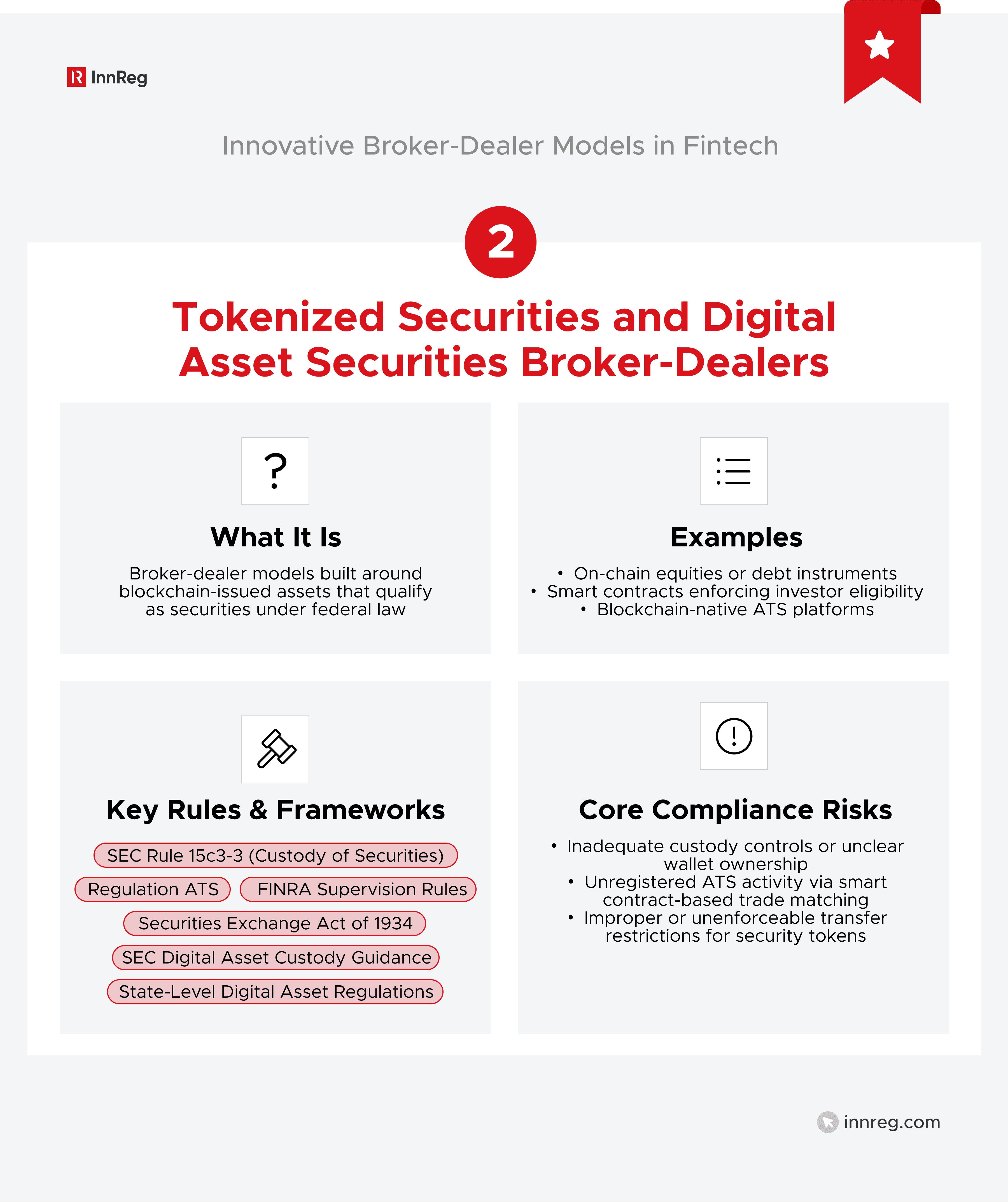

2. Tokenized Securities and Digital Asset Securities Broker-Dealers

A growing number of firms are exploring broker-dealer models built around tokenized securities: digital assets issued and transferred on blockchain infrastructure that meet the definition of a security under federal law.

These platforms aim to modernize issuance, custody, and trading by using distributed ledger technology instead of legacy systems.

The regulatory questions start immediately. If a token represents a security, the platform offering, holding, or matching trades for that asset must meet the same requirements as any other broker-dealer.

That includes rules on custody, reporting, customer protection, and, if applicable, operation as an Alternative Trading System (ATS). It also raises questions about how ownership transfers are validated and how restrictions (such as lock-ups or investor limits) are enforced on-chain.

Learn more about tokenized securities →

Design Considerations and Compliance Risks

Unlike traditional securities, tokenized assets may settle instantly, carry programmable features, or support peer-to-peer transfers outside of centralized infrastructure.

Firms also need to account for ever-evolving rules.

The SEC and FINRA revised their approach in 2024, pulling prior guidance and replacing it with a more workable structure. Under this new structure, broker-dealers may now custody digital asset securities if they have appropriate controls in place and can support proper oversight.

Regulatory Considerations

Tokenized broker-dealer models often fall under a mix of securities, banking, and digital asset oversight. Key frameworks and rules include:

SEC Rule 15c3-3 (Customer Protection Rule, custody of securities)

FINRA supervision and cyber controls

ATS registration requirements under the Securities Exchange Act of 1934

State-level rules for digital asset businesses (if the platform also handles non-security crypto)

New SEC guidance on custody and digital asset recordkeeping

Platforms must also consider the risk of inadvertently offering unregistered securities, particularly with retail investors. Each token must be analyzed individually to determine whether it qualifies as a security, how it was issued, and what exemptions (if any) apply.

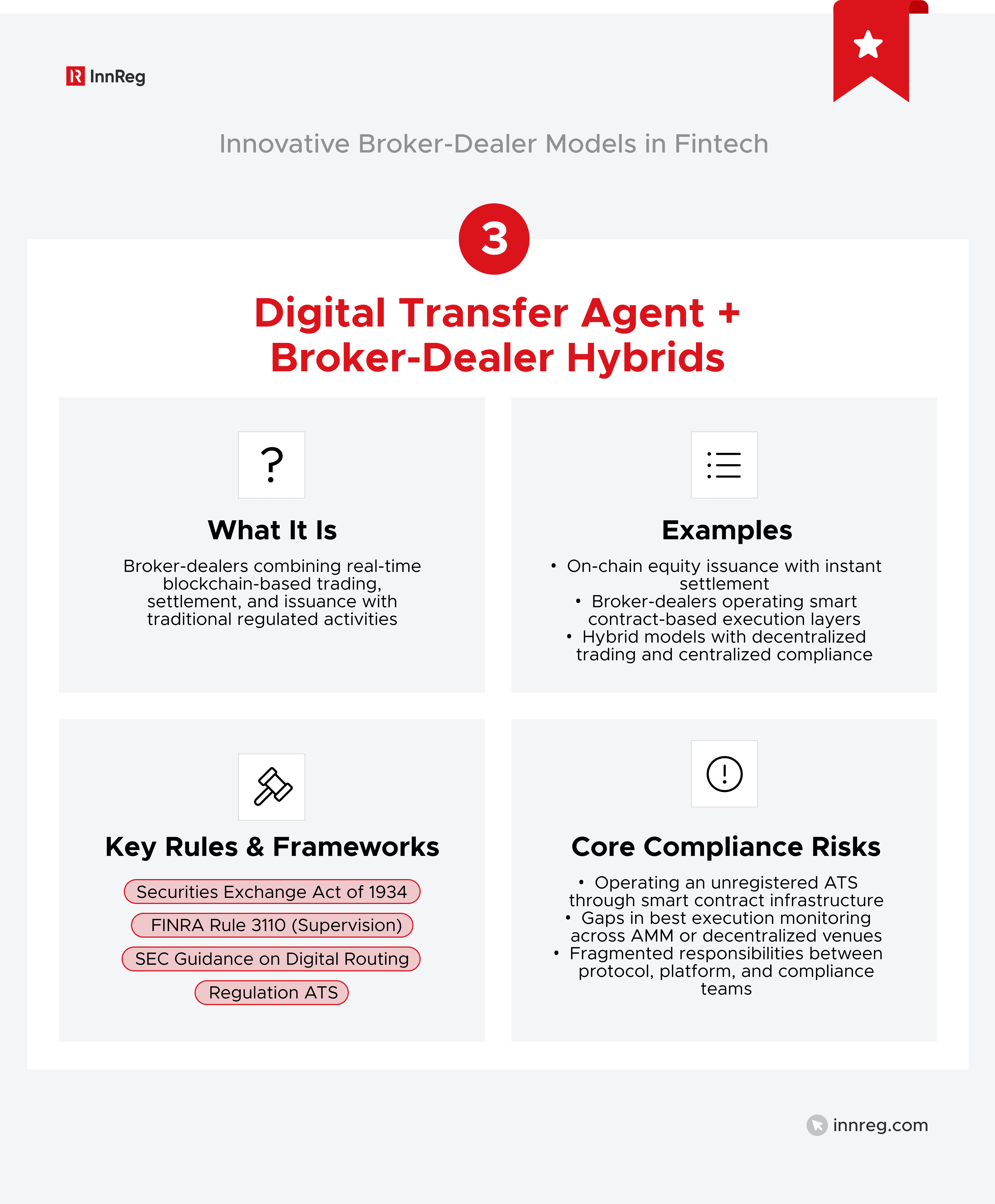

3. Digital Transfer Agent + Broker-Dealer Hybrids

Some broker-dealers are using models that connect to blockchain-based trading environments. These setups often involve handling core tasks (order flow, execution, settlement, etc.) using decentralized or partially decentralized systems.

The appeal is clear: more transparency, faster execution, and fewer intermediaries. But these models introduce new friction points for compliance, especially when there is no centralized counterparty or when governance is distributed across code, DAOs, or third-party operators.

Core Regulatory Challenges

When a broker-dealer integrates with a decentralized protocol, regulators will ask several core questions:

Who controls trade execution? | If the firm writes the smart contracts or governs the protocol, it may be treated as the operator of an ATS or exchange. |

How is best execution monitored? | If order flow is routed into a public pool or AMM, the firm must show how it evaluates execution quality compared to other venues. |

What entity is accountable? | In many on-chain models, it’s unclear who owns or operates the trading infrastructure. The SEC and FINRA expect a clear line of supervisory responsibility. |

In fully decentralized models, a common problem emerges: no single party has clear responsibility for meeting regulatory requirements. To work around this, some firms adopt a hybrid setup while keeping trading mechanics on-chain while shifting onboarding, disclosures, and surveillance to a centralized layer.

Regulatory Considerations

Using decentralized trading protocols does not remove broker-dealers from existing oversight. Depending on how the system is designed, several regulatory layers may apply.

These include the Securities Exchange Act of 1934 (for platforms that resemble ATSs), Regulation ATS itself, FINRA’s supervision rules, and SEC expectations around digital routing. If the system allows anonymous or pseudonymous activity, AML and KYC compliance also becomes a key concern.

Additional Resources: | |||

|---|---|---|---|

The key risk in this model is fragmentation. Compliance responsibilities become harder to assign when critical functions are handled by separate parties or are spread across smart contracts with no centralized oversight.

Most firms pursuing this path find that the regulatory lift is not technical, but structural. The business model must be designed from day one to support full traceability and accountability, even when the infrastructure is distributed.

Learn how InnReg helps innovative fintechs develop regulatory and product strategy →

4. Decentralized and Hybrid On-Chain Trading Broker-Dealers

These setups often rely on decentralized or partially decentralized infrastructure to handle order routing, execution, or settlement. For some firms, the entire trading stack is built on-chain; for others, only select functions are decentralized.

This approach can reduce reliance on intermediaries and offer greater speed and transparency. But it introduces structural challenges that traditional compliance frameworks were not designed to handle.

When critical actions are performed by code rather than a registered entity, regulators will ask who is ultimately accountable.

Core Regulatory Challenges

Firms entering this space face multiple layers of scrutiny.

To address these gaps, some firms lean toward hybrid models. They keep trading mechanics on-chain but handle compliance tasks, such as onboarding, disclosures, and oversight, through a centralized entity.

Regulatory Considerations

Using decentralized protocols does not remove regulatory exposure. If the platform supports securities trading, it will likely fall under existing broker-dealer and exchange rules.

The relevant frameworks often include:

SEC expectations for routing and engagement

AML and KYC enforcement, especially where users operate through wallet addresses

Fragmented infrastructure poses a unique challenge. With no central actor managing all aspects of the system, regulators will ask how firms are enforcing supervision, disclosures, and compliance. A strong legal structure is critical.

5. Embedded Brokerage APIs and White-Label BDs

Embedded broker-dealer models allow fintech apps and non-financial platforms to offer investment features without becoming broker-dealers themselves.

These firms integrate APIs or white-label services from licensed partners who handle execution, custody, and regulatory responsibilities behind the scenes.

For the end user, it may look like a seamless experience inside a budgeting app, rewards platform, or digital wallet. But behind that interface are layered compliance arrangements that need to be carefully structured, documented, and supervised.

Delegated Compliance, Retained Risk

The moment a third party delivers broker-dealer functionality through its own app or platform, oversight becomes more complex.

The licensed firm still holds the risk. It must supervise how that functionality is offered, how users are onboarded, and whether the compliance obligations are being met in a way that regulators would accept.

Three areas often need active coordination:

Onboarding: Who gathers the required identity documents? Who checks for red flags or matches against watchlists?

Execution and suitability: If a third party’s interface offers model portfolios, nudges, or triggers, how is that activity reviewed for regulatory impact?

Marketing and messaging: Are the claims made by the partner subject to broker-dealer advertising rules, especially FINRA’s requirements for balance and substantiation?

Additional Resources: | ||

|---|---|---|

Disclaimers do not close the loop. What matters is control and supervision. Firms using this model typically build out WSPs, name responsible principals, and set up regular reviews with their partners to stay within regulatory expectations.

Regulatory Considerations

Several regulatory layers typically apply in embedded brokerage arrangements:

FINRA Rule 2210 (Communications with the public)

FINRA Rule 3110 (Supervision)

SEC Rule 15c3-3, especially if the partner touches funds or customer securities

State-level registration requirements for the platform or its affiliates

When the broker-dealer and the front-end partner operate independently, even minor misalignments can create exposure. A marketing campaign that pushes too far or a product feature that suggests a specific investment can trigger regulatory questions.

Learn how InnReg helps fintechs develop vendor risk management programs →

6. Broker-Dealers Handling Both Crypto and Securities

Some broker-dealers are expanding their scope to support both traditional securities and crypto assets. These firms offer a single interface for equities, ETFs, and digital tokens, often aiming to serve younger or more crypto-native investors.

While the unified user experience has appeal, the regulatory architecture behind it is rarely simple. Broker-dealers must separate, document, and govern two very different sets of rules, especially when the crypto assets fall outside SEC jurisdiction.

Dual Oversight, Parallel Risk

When a firm handles both asset types, it operates under a dual lens. It must meet broker-dealer obligations for securities, while also complying with FinCEN rules (and sometimes state-level money transmitter laws) for crypto.

The dividing line is not always clear. Some assets start as unregulated tokens and later evolve into securities, or are reclassified after regulatory action. That uncertainty requires internal processes to flag, classify, and update how each asset is treated.

Key areas of operational complexity include:

Custody | Disclosures | Surveillance and AML |

|---|---|---|

Securities must comply with SEC Rule 15c3-3, while crypto may require a trust, wallet, or third-party custodian with SOC audits. | Risk disclosures for securities are well-established. Crypto often needs custom language around volatility, fraud risk, and lack of SIPC coverage. | Securities surveillance focuses on market manipulation. Crypto requires additional tools to track on-chain activity, the source of funds, and wallet behavior. |

Regulatory Considerations

Running a platform that supports both securities and crypto assets means working under two different regulatory frameworks, which often overlap. A few of the key touchpoints include:

SEC and FINRA rules governing broker-dealer conduct

FinCEN requirements for AML programs under the Bank Secrecy Act

State-by-state money transmitter laws, if applicable

SEC guidance on how to classify digital assets and how custody should be handled

CIP and CDD obligations under the Patriot Act

Classification errors carry the most exposure. Mislabeling a token that meets the Howey Test, even unintentionally, can result in enforcement. Most firms solve for this by building shared controls across compliance, legal, and product teams so classification is not left to interpretation.

See also:

Core Compliance Challenges for Innovative Broker-Dealer Models

New broker-dealer structures in fintech frequently push up against the limits of current regulatory frameworks. That pressure creates unique challenges, not just in how the rules are interpreted, but in how day-to-day compliance is implemented and managed. Despite the differences across models, certain risk themes appear again and again.

Chellange | Context |

|---|---|

Conflicts of Interest | PFOF, embedded brokerage |

Algorithmic Supervision | Robo-advisors, AI execution tools |

Messaging platforms, in-app engagement | |

Trade Reporting | Fractional shares, embedded APIs |

Dual-Regime Oversight | Crypto/securities hybrids, multiple rulebooks |

Partner Oversight | Embedded, white-label setups |

Custody of Digital Assets | Tokenized securities, crypto models |

Reg BI/Suitability | AI tools, nudges, portfolio suggestions |

Cross-Border Issues | Global platforms, social/copy trading |

Need help with broker-dealer compliance?

Fill out the form below and our experts will get back to you.

1. Conflicts of Interest in Zero-Commission and PFOF Structures

Commission-free trading is attractive to users, but behind the scenes, it often involves compensation models that require extra scrutiny. PFOF is the most common, but exchange rebates and internalized order flow can raise similar concerns. The issue is not that these models exist; it is how they are implemented and supervised.

Firms need to ask the following questions: Are our routing decisions being made with the client's best interest in mind, or are they leaning toward what drives the highest rebate? If a regulator asks to see how execution quality is monitored, is there documentation? These are not theoretical questions but standard exam items.

Disclosures are part of the solution, but not the entire fix. Users need to understand how the firm makes money, and compliance teams need to show how execution decisions are reviewed and compared across venues. It is this combination, clear communication and operational oversight, that will carry the most weight with FINRA and the SEC.

2. Supervision of Algorithmic and Automated Tools

When firms automate investment functions, they are expected to supervise those systems as they would human staff. That includes policies, testing logs, and update records.

FINRA and SEC are now pressing for deeper reviews. They want to see how decisions are made inside the algorithm, and whether risks are clearly flagged.

Tools that influence investment choices, especially in a personalized way, can pull the firm into Reg BI or fiduciary territory.

3. Recordkeeping Across Nontraditional Communication Channels

Today’s digital tools (chat prompts, embedded messaging, AI-driven interfaces, and similar) may feel modern, but regulators treat them like any other form of communication.

Under SEC and FINRA rules, firms are expected to keep a complete record of any business-related communications.

That includes having systems in place to log and retain these messages, even when they’re delivered through nontraditional channels.

4. Trade Reporting and Audit Trail Complexity

Recent FINRA guidance has tightened expectations around fractional share trading. Broker-dealers must maintain accurate timestamps, clear execution records, and documented links to each customer instruction. This is not limited to traditional brokerage platforms, and API-driven activity initiated through third-party apps is fully in scope.

For embedded models, the challenge lies in building a traceable audit trail that spans multiple systems. A trade may begin with a user action in a partner interface and complete in the broker-dealer’s back end. Each step must be captured, reconciled, and stored in a way that holds up during exams.

5. Dual-Regime Oversight for Securities and Non-Securities

Platforms that handle both securities and non-security crypto assets often face oversight from several regulators at once: the SEC and FINRA for securities, FinCEN for AML, and possibly state agencies for money transmission. Each layer has its own requirements.

Regulatory issues may arise when a token is mistakenly treated as outside securities law.

To mitigate this risk, firms need shared processes that help legal, compliance, and product teams align on how assets are classified and when escalation is required.

Learn how InnReg helps broker-dealers navigate regulatory challenges →

6. Oversight of Fintech Partners and Embedded Interfaces

When a fintech platform controls the user experience, the broker-dealer must still oversee how regulated features are delivered. That includes vetting how users are onboarded, which disclosures are shown, and how customer issues are handled.

This oversight cannot be informal. It usually involves a documented compliance framework, named supervisory staff, and periodic reviews to confirm responsibilities are being met in practice and not just on paper.

See also:

7. Custody and Safeguarding of Digital Assets

Holding digital assets as a broker-dealer involves more than managing wallets.

SEC expectations extend to how firms control access, protect balance sheet assets, and whether their systems support audits and regulatory review.

Platforms that custody both securities and non-securities often run into gaps. They need to define which protections apply under SIPC and assess whether their custody stack aligns with all applicable requirements.

8. Suitability, Reg BI, and the Blurred Line Between Tools and Advice

Prompts and visual cues in investment apps can walk a fine line. When designed carefully, they educate. But once tailored to a user’s account or suggestive of specific actions, they start to resemble recommendations.

This distinction matters. A one-size-fits-all chart poses little concern. But when the interface adapts to real-time user inputs, the firm must consider how regulators might interpret it and how to track and govern those outputs accordingly.

Under Regulation Best Interest (Reg BI), any suggestion that could be interpreted as a recommendation must meet the care, disclosure, and conflict-of-interest obligations imposed on broker-dealers. If the firm is also a registered investment advisor, fiduciary duties under the Advisers Act may apply. FINRA may additionally evaluate these tools under Rule 2111, especially if the design or language implies a call to action.

9. Cross-Border Licensing and Fragmented Oversight

Cross-border platforms must navigate a maze of financial rules. A single product, like copy-trading or token issuance, may carry different regulatory implications in each country where users interact with it.

The key risk is drift: unintentionally triggering foreign licensing or registration requirements due to user behavior, product features, or marketing reach. This makes it critical to monitor where users are located, what services they access, and how local rules treat each asset or activity.

Depending on the jurisdictions involved, firms may need to consider MiFID II, FCA guidance on financial promotions, MAS digital token regulations, EU crypto asset frameworks (MiCA), or Canadian provincial licensing rules.

Where services implicate US securities law abroad, Reg S may also apply. Without a structured licensing and product mapping process, cross-border fintech models can accumulate risk faster than teams realize.

—

The models outlined in this article highlight how far fintech has pushed traditional broker-dealer boundaries. But innovation without structure can backfire. Each shift toward automation, decentralization, or embedded delivery comes with legal exposure that needs to be addressed early and explicitly.

The most successful teams approach regulation not as a blocker but as a design constraint, baking oversight into architecture from the start. When the model is new, the responsibility to explain and defend it grows.

If you are developing an unconventional brokerage model, aligning legal, product, and compliance early is essential. InnReg supports fintech teams navigating this exact complexity.

InnReg was founded in 2013 by Francesco Matteini, former Chief Compliance Officer who helped launch and scale some of the most innovative digital broker-dealers over the last two decades. He built compliance programs to support the first zero-commission broker and the first BD-sponsored investor social network. Since its founding, InnReg has attracted highly experienced fintech consultants with long careers in compliance, risk management, and a deep understanding of the fintech industry.

How Can InnReg Help?

InnReg is a global regulatory compliance and operations consulting team serving financial services companies since 2013.

We are especially effective at launching and scaling fintechs with innovative compliance strategies and delivering cost-effective managed services, assisted by proprietary regtech solutions.

If you need help with broker-dealer compliance, reach out to our regulatory experts today:

Related Articles

Featured LinkedIn Posts