Fintech Product Compliance 101: What Fintechs Need to Know

Product compliance is not just a legal checkpoint. It is a core operational requirement for fintech companies building financial products.

Whether a fintech firm is launching a payments app, credit feature, or embedded investment offering, it is operating in one of the most heavily regulated sectors in the world. Regulators do not give early-stage startups a free pass.

This article breaks down what fintech founders, legal teams, and product leaders need to know about product compliance, from licensing triggers and consumer protection rules to data handling, AML, and evolving expectations around AI and open banking.

At InnReg, we provide outsourced Chief Compliance Officer (CCO) services supported by a full team of compliance specialists with deep fintech experience. We offer guidance on product design and help teams consider regulatory implications from the start.

What Is Product Compliance in Fintech?

In fintech, product compliance means aligning the mechanics of a product with financial regulations. That covers licensing, AML, data privacy, consumer disclosures, and more. The rules apply based on what the product does, not how it is branded.

For example, a feature that advances funds will likely trigger lending rules. A digital wallet that moves customer money may need money transmission licenses. What matters is the function. The technology layer doesn’t exempt it from oversight.

Product compliance in fintech does not begin and end at launch. It continues as the product grows. New features, third-party integrations, and customer behaviors often change the regulatory risk profile.

Teams that handle this well look at how the product works, where it fits in the regulatory landscape, and build controls into the infrastructure.

Why Product Compliance Matters: Risk, Trust, and Growth

Fintech products operate in a space where the margin for error is small.

Not meeting regulatory requirements can trigger fines, regulatory investigations, or operational restrictions. This holds true even when a company uses a sponsor bank or third-party platform. The liability is shared, and so is the scrutiny.

Compliance also affects credibility. Investors look closely at how risk is managed. Banking partners often demand evidence of sound controls before signing off on integrations. And customers, especially in financial services, are quick to walk away if they lose confidence in how their money or data is being handled.

A well-structured product compliance framework does not just reduce downside. It creates space for growth. When internal systems are built with compliance in mind, fintechs move faster. Launch timelines are tighter, and when it is time to scale or enter new markets, fewer roadblocks get in the way.

See how InnReg supports fintech product compliance by providing outsourced CCO services →

Who Regulates Fintech Products? Key Federal and State Agencies

A patchwork of federal and state regulators governs fintech product compliance. Which agencies are involved depends on the product’s features, delivery model, and legal structure.

For most fintechs, multiple layers of oversight apply, sometimes directly, sometimes through a partner.

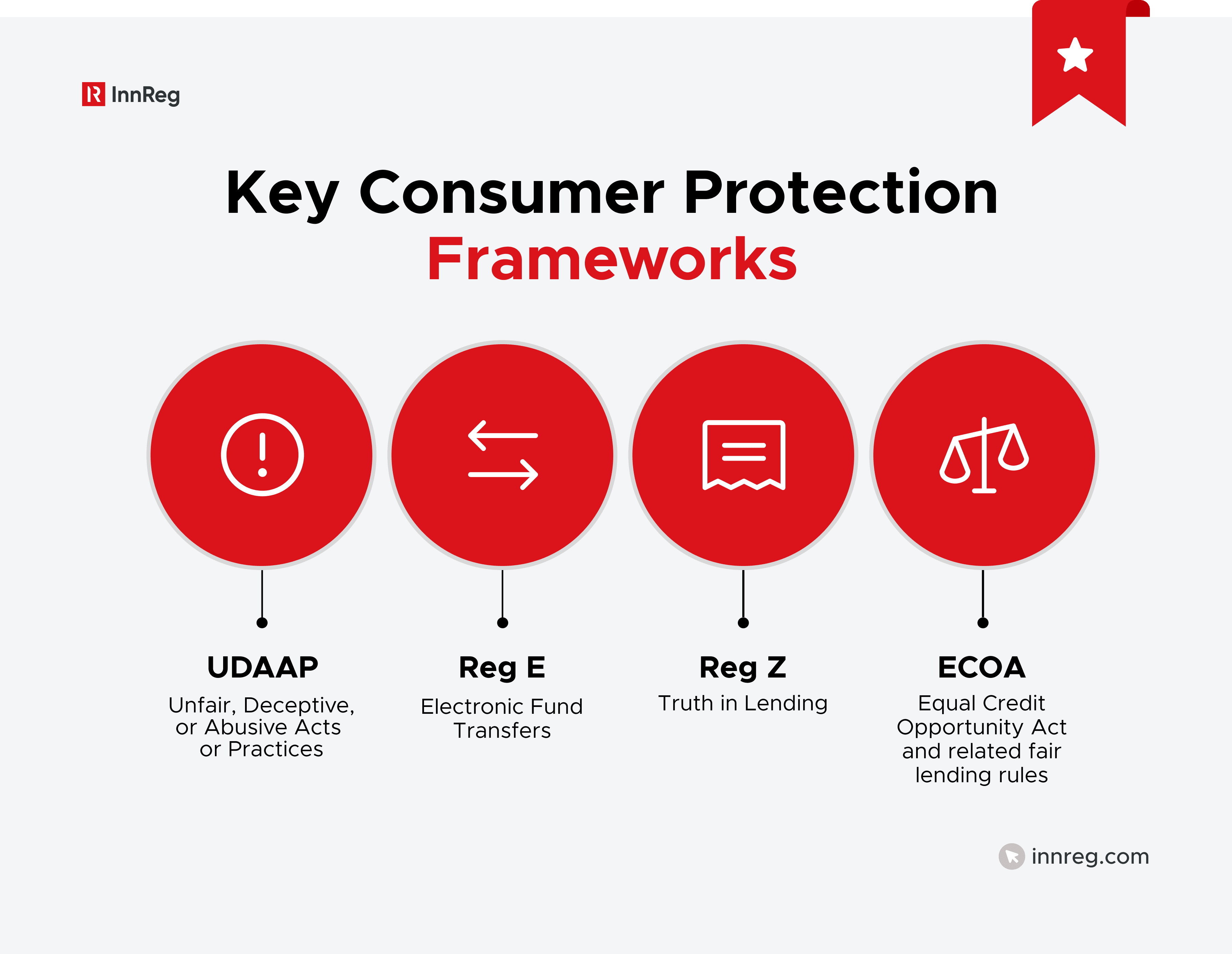

At the federal level, the Consumer Financial Protection Bureau (CFPB) is often the most visible regulator. It oversees consumer-facing financial products and enforces laws like the Electronic Fund Transfer Act (Reg E), the Truth in Lending Act (Reg Z), and UDAAP rules. The Federal Trade Commission (FTC) also has jurisdiction, particularly around unfair or deceptive business practices.

For fintechs that move money, the Financial Crimes Enforcement Network (FinCEN) plays a central role. Companies classified as Money Services Businesses (MSBs) must register with FinCEN and implement an AML program. Some fintechs may also fall under the scope of the Office of the Comptroller of the Currency (OCC) or the Federal Reserve if they work with national banks or hold special-purpose charters.

On the state level, licensing regimes vary widely. Fintechs offering money transmission, lending, or digital asset services often need licenses in each state where they operate. States like New York, California, and Texas maintain their own regulatory frameworks. For example, the New York Department of Financial Services (NYDFS) enforces the BitLicense regime for crypto businesses and has imposed high standards on transaction monitoring and cybersecurity.

Regulator | Primary Focus Areas |

|---|---|

CFPB | Consumer finance, Reg E, Reg Z, UDAAP, fair lending, supervision of large nonbank fintechs |

FTC | Unfair/deceptive practices, data privacy, marketing claims |

FinCEN | Anti-money laundering (AML), Money Services Business (MSB) registration, SAR/CTR filings |

OCC | National banks, bank-fintech partnerships, special-purpose charters |

Federal Reserve | Oversight of bank holding companies, financial stability, and certain payment systems |

FDIC | Deposit insurance and consumer protection at insured banks |

SEC | Securities regulation, digital asset offerings, investment platforms, and broker-dealer compliance |

CFTC | Derivatives, crypto commodities, swaps, and futures platforms |

State Financial Regulators | Money transmission, lending licenses, digital asset regulation, and consumer protection at the state level |

Product compliance in this environment requires a clear understanding of where the regulatory lines fall. Misjudging which agency has authority, or assuming a partner is covering every base, can create significant exposure.

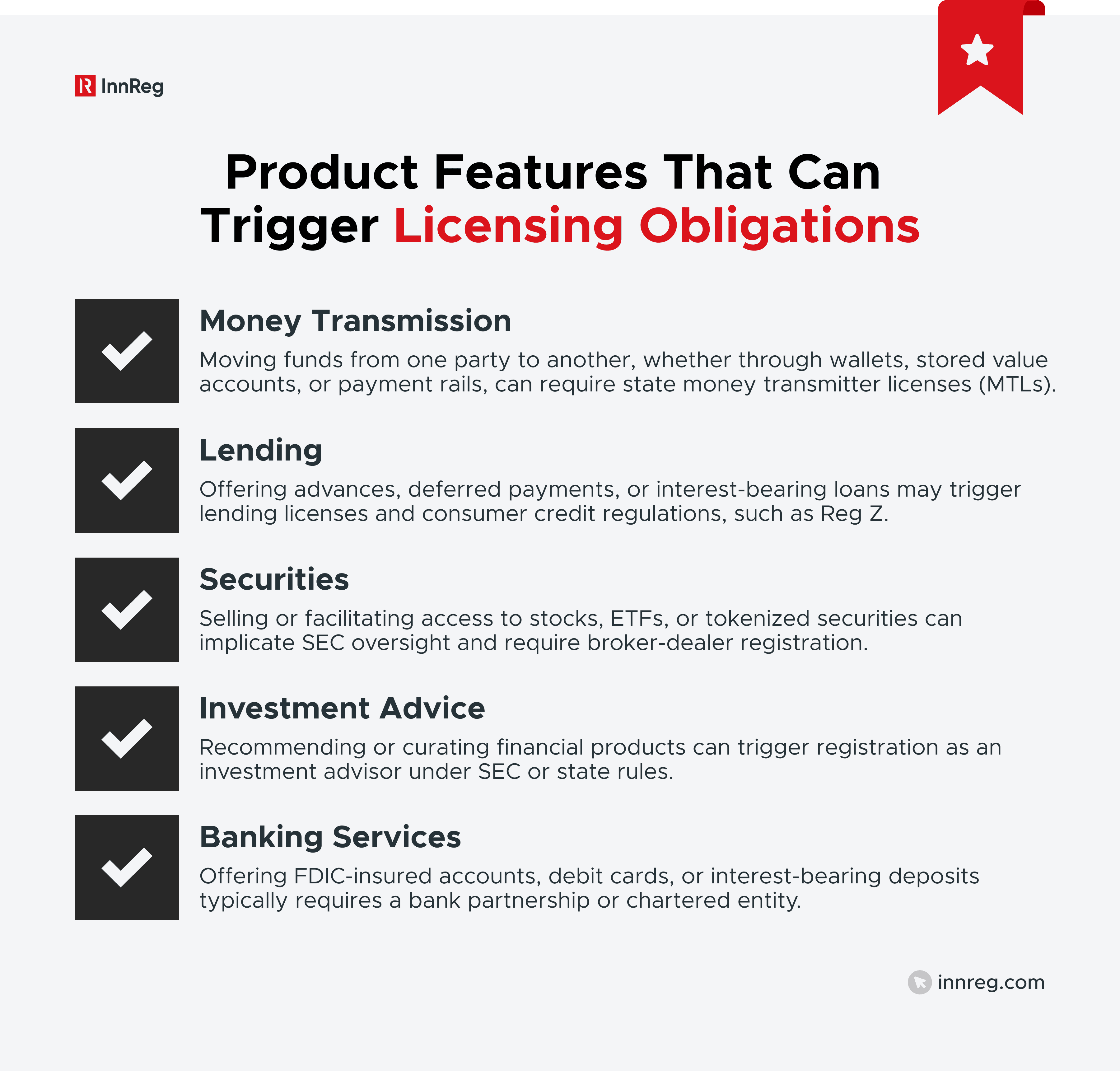

When Is a License Required? Understanding Regulatory Triggers

Fintech product compliance often hinges on one key question: Does the product trigger a licensing requirement? The answer depends not on how the product is described in marketing materials, but on how it functions under law.

Some fintechs work under sponsor banks or licensed partners, which can reduce the need for direct licensing, but this approach has limits. Regulatory agencies increasingly expect fintechs to maintain their own controls, even when operating under another entity’s license.

Misjudging licensing triggers is one of the most expensive compliance mistakes a fintech can make. It can delay launches, attract scrutiny, or result in retroactive enforcement.

Reverse solicitation is sometimes viewed as a way to avoid licensing. However, this is not the case. It is a narrow, highly scrutinized exception that typically applies only in limited cross-border contexts and requires strict conditions to be met. Many teams overestimate its applicability or misunderstand how regulators interpret it.

Learn more about reverse solicitation in financial services →

Product Compliance for Consumer Financial Products

Fintech products that interact with consumers must navigate a range of regulatory obligations tied to transparency, fairness, and error handling. These rules are often triggered by how a product functions, not how it is marketed.

Unfair, Deceptive, and Abusive Acts or Practices (UDAAP)

UDAAP enforcement is based on how consumers experience a product. If a feature misleads, confuses, or takes advantage of users, it may fall under UDAAP.

This includes unclear pricing, missing disclosures, or workflows that limit a user’s ability to exit or dispute. Regulators often cite UDAAP even when no other violation exists, making it a common starting point for investigations.

That makes UDAAP especially important for product teams. Decisions about copy, user flows, and third-party tools can all become relevant. The best approach is to review the full customer experience, not just the legal terms.

Reg E: Electronic Fund Transfers

Reg E applies to digital tools that let consumers move or access their money. That includes debit cards, peer-to-peer apps, and wallets tied to stored value or bank accounts.

Fintechs that offer these services must explain how transfers work, how to authorize them, and what happens when something goes wrong. Dispute handling is time-sensitive, and customers may be entitled to temporary refunds while investigations are underway.

Common areas where fintechs fall short include:

Inadequate or missing disclosures at onboarding

Friction in the error resolution process

Confusion over roles when multiple parties (e.g., sponsor bank, processor, app) are involved

Importantly, Reg E liability may still apply even if the fintech isn’t the entity holding customer funds. If the product presents itself as a way to move or manage money, compliance expectations usually follow.

See also:

Reg Z and Truth-in-Lending Requirements

Reg Z outlines the standards for how companies must present and structure consumer credit products. Fintechs offering tools like deferred payments, cash advances, or installment billing may fall under these rules.

It is not the branding that matters, but whether the user is expected to repay. That includes BNPL services, early wage access, and overdraft-like tools. If the product qualifies as credit, fintechs must make specific disclosures upfront. These include repayment terms, fees, and timing, as well as limits on misleading or incomplete marketing.

Fintechs often run into issues when product and marketing teams push changes that impact pricing, repayment timing, or the cost of funds, without checking whether new disclosures are needed. Teams building “credit-adjacent” products should consult legal and compliance early to map product behavior to regulatory requirements.

Learn more about Regulation Z (Truth In Lending) →

Need help with fintech compliance?

Fill out the form below and our experts will get back to you.

ECOA, Fair Lending, and Credit Algorithms

The Equal Credit Opportunity Act (ECOA) prohibits discrimination in credit decisions based on race, gender, age, and other protected characteristics. This applies whether humans, algorithms, or a mix of both make lending decisions.

For fintechs using credit models, fair lending rules require more than just predictive accuracy. Firms must test for bias, explain key factors influencing decisions, and offer adverse action notices when credit is denied. This is especially important in products using alternative data or nontraditional underwriting.

Problems often arise when teams fail to retain visibility into vendor models or validate performance across demographic groups. Regulators expect firms to regularly audit credit logic and explain why a given consumer received a certain outcome.

Learn more about the Equal Credit Opportunity Act (ECOA) →

Framework | Applies to | Risk Areas |

|---|---|---|

UDAAP | Any consumer-facing fintech product | Misleading disclosures, confusing UX, abusive terms |

Reg E | Electronic money movement tools (e.g., debit cards, wallets, P2P apps) | Disclosures, error resolution, and authorization flows |

Reg Z | Consumer credit products and features | Loan disclosures, fee transparency, and marketing accuracy |

ECOA | Any product involving credit decisions | Discriminatory lending, algorithmic bias, adverse actions |

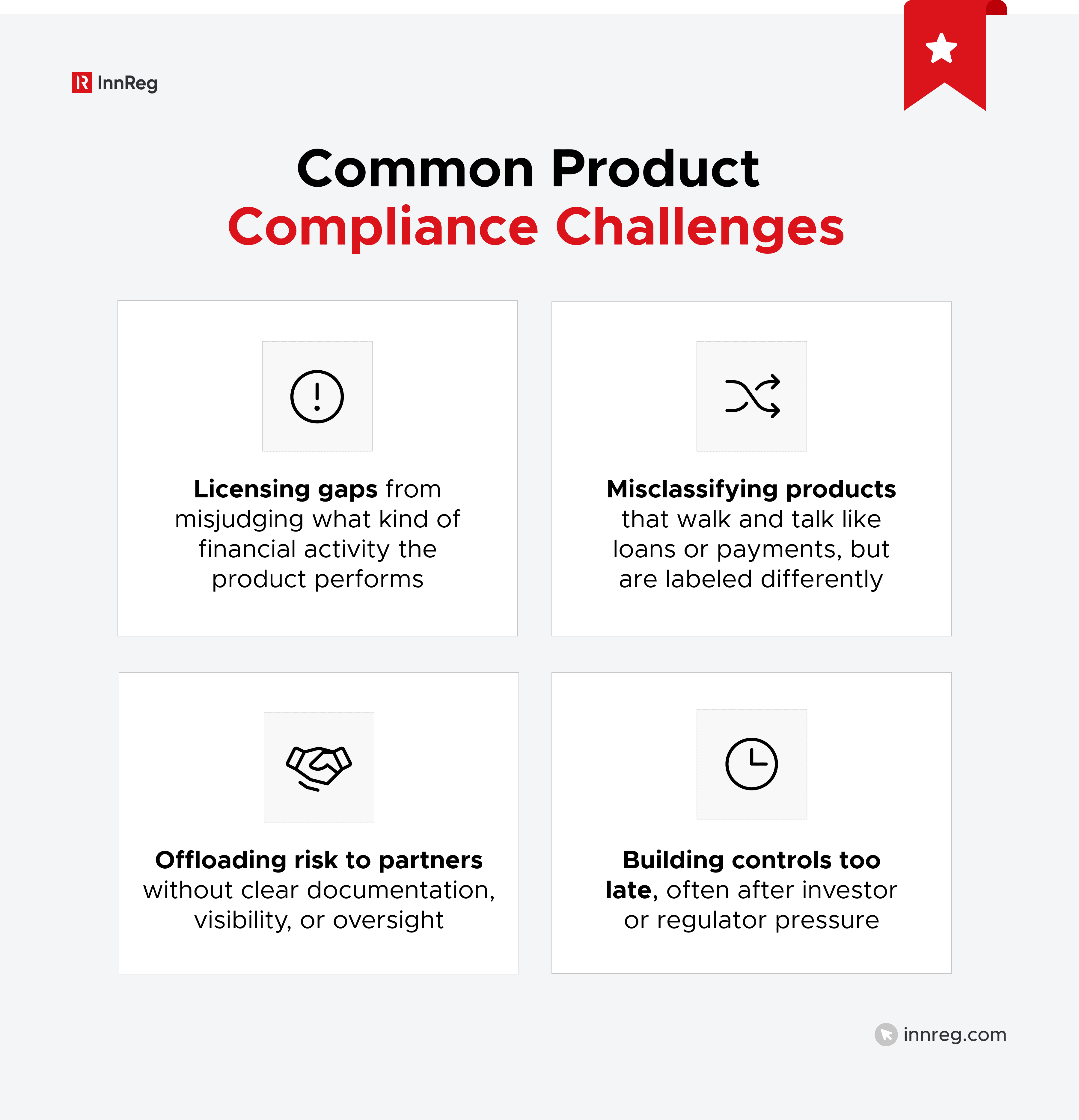

Common Product Compliance Challenges

Even well-intentioned fintech teams run into regulatory friction. Many compliance problems start with product design choices, not bad actors.

Licensing Gaps

Licensing issues are one of the most expensive mistakes in fintech product compliance. A product may require state or federal licenses even if it’s delivered through a slick UI or described as “just software.”

These gaps usually emerge when teams underestimate what their product is actually doing from a legal standpoint.

For example:

A digital wallet may trigger money transmission laws in multiple states

A salary advance feature might qualify as a loan under credit laws

An investment tracking tool could be seen as offering advice if it suggests trades

A partner’s licence does not protect a firm from liability as supervisors evaluate who holds real control over the product. If the fintech manages customer communications or drives the financial terms, it may still be seen as the regulated entity.

Licensing should be mapped early. It shapes how the product is built, marketed, and scaled. Waiting until launch, or worse, after enforcement, is a costly choice.

Misclassifying Products

Fintech products often operate in gray areas. A service may be marketed as a convenience or customer benefit, but if it touches money movement, credit, or investment functions, legal definitions may apply.

When teams move quickly, there is a risk of overlooking those distinctions. Without early compliance input, a product designed to drive engagement might cross into regulated territory without warning. By the time issues surface, the damage may already be done.

Offloading Risk to Partners

Many fintechs partner with banks, program managers, or infrastructure providers to launch faster. While these relationships offer clear benefits, they also create blind spots, as relying too heavily on another party's license or control framework can lead to problems.

Regulators increasingly expect firms to have independent oversight, even when they operate under someone else's regulatory umbrella.

The most common mistakes happen when responsibilities are not clearly documented. For example, a fintech firm might assume a sponsor bank is covering a compliance function, only to discover in an audit or enforcement action that the expectation was mutual.

Shared liability does not mean shared execution. Each party needs a defined role, and fintechs should validate that core obligations, such as transaction monitoring, disclosures, and customer support, are not falling through the cracks.

A structured vendor oversight program helps reduce risk. That includes clear documentation, regular audits, and working relationships between compliance teams. Fintechs that treat oversight as an ongoing function, not a one-time onboarding step, tend to avoid surprises.

Built on InnReg’s experience working with over 100 fintechs, Regly includes a vendor management module that helps firms organize and assess their third-party relationships →

Building Controls Too Late

Some compliance issues do not surface until a product is in the hands of users or on a regulator’s radar. By then, gaps are harder and more expensive to close.

It’s common for firms to add controls like transaction monitoring, disclosure review, or customer support procedures in the final weeks before launch. But by that point, core workflows are already built. Retrofits do not just slow things down. They increase the risk that something critical is missed.

Compliance works best when built alongside the product, not after it. Teams that treat it as a parallel track from design through launch are more likely to meet regulatory expectations and avoid emergency rewrites.

Practical Steps for Founders and Executives

Product compliance shapes how a company builds, scales, and survives scrutiny. While legal and compliance teams handle execution, the roadmap often starts at the top.

Below are three areas where founders and executives can make early, strategic decisions that mitigate long-term risk:

Setting a Compliance Roadmap

A compliance roadmap is not meant to slow down product development. It exists to help teams identify where and when controls are needed.

Begin by mapping what the product actually does. Identify the financial activities involved and the corresponding legal or licensing requirements. That map becomes the foundation for planning regulatory reviews at key build stages.

The roadmap does not need to be long. But it should be written down, tied to specific owners, and updated as the product evolves. If everyone is loosely responsible, no one is truly accountable.

Hiring or Outsourcing the Right Expertise

Early-stage teams may not need a full legal department, but they do need someone who understands financial regulation and how it applies to product decisions. That can be an in-house hire, a part-time advisor, or a specialized firm. What matters is that compliance questions are answered by people who’ve seen the landscape before.

Relying on general counsel or outside law firms alone often is not enough. Product compliance work touches design, engineering, marketing, and operations. It needs someone who can bridge those worlds, not just spot issues in a memo.

Learn how InnReg helps fintechs by providing outsourced chief compliance officer services →

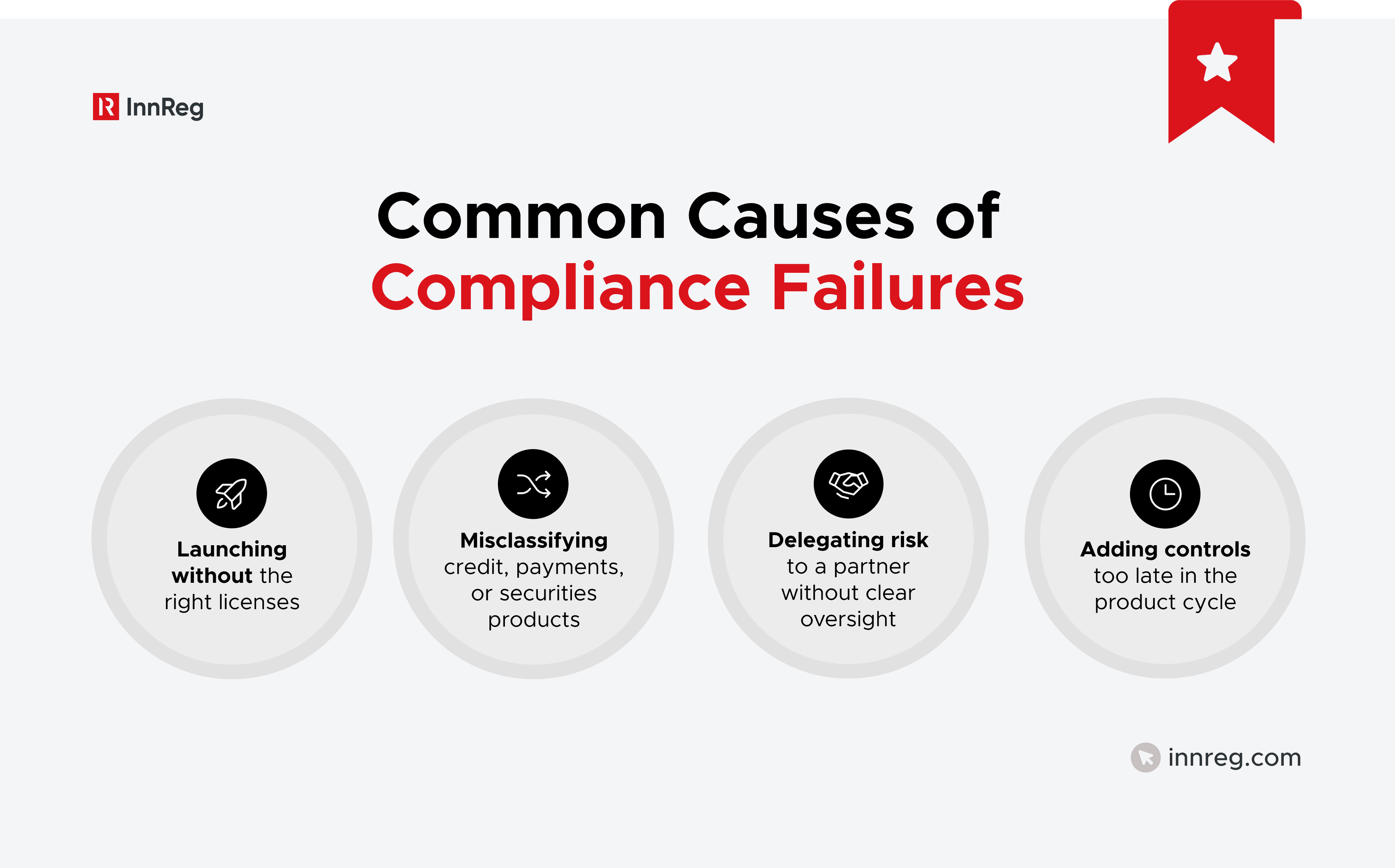

Avoiding the Most Expensive Mistakes

Some of the most damaging compliance issues do not come from obscure laws or edge cases. They come from decisions that repeat across startups that are moving quickly, short on regulatory experience, or unclear on who owns the risk.

Founders do not need to know every rule, but they must understand where compliance fits into product strategy, how to spot early warning signs, and why treating it as a side function is a risk multiplier.

See also:

—

Building fintech products means operating in one of the world's most complex regulatory environments.

The biggest risks often stem from small gaps: a license not scoped, a control added too late, a partner assumed to be covering something they are not. These gaps widen fast and can become expensive to fix.

As such, compliance should be treated as a core function. It gets mapped, staffed, tested, and built into product development. That shift in mindset often makes the difference between a quick stop and a scalable platform.

Francesco is the Founder & CEO of InnReg with over 15 years of experience in fintech compliance and operations. He previously served as CCO at TradeKing and Zecco, helping grow the firm into the 6th largest US online broker before its $275M acquisition by Ally Bank. He holds FINRA Series 4, 7, 24, 53, and 63 licenses and an MPA from Harvard Kennedy School.

How Can InnReg Help?

InnReg is a global regulatory compliance and operations consulting team serving financial services companies since 2013.

We are especially effective at launching and scaling fintechs with innovative compliance strategies and delivering cost-effective managed services, assisted by proprietary regtech solutions.

If you need help with compliance, reach out to our regulatory experts today:

Related Articles

Featured LinkedIn Posts