KYC Requirements and Due Diligence in Fintech Explained

Key Takeaways

KYC is the process of identifying and verifying who the customer is before an account is opened or allowed to transact.

CDD goes further by assessing customer risk, understanding how the account will be used, and monitoring that risk throughout the relationship.

FinCEN and the Bank Secrecy Act drive KYC and CDD expectations in the US, with a focus on risk-based controls, recordkeeping, and suspicious activity reporting.

Fintech firms need more than basic identity checks, as effective programs also cover beneficial ownership, screening, risk profiling, and ongoing monitoring.

Regulators expect KYC and CDD controls to match how the business actually operates, especially in digital onboarding models and fast-scaling products.

Common problems include unclear ownership of controls, weak beneficial ownership review, poor data quality, manual review backlogs, and product flows that bypass compliance controls.

Know Your Customer (KYC) and Customer Due Diligence (CDD) requirements are at the center of how regulated fintech companies onboard customers, manage risk, and satisfy regulatory expectations.

Founders and executives seem to understand that Know Your Customer and Customer Due Diligence matter. Their challenge is in understanding what regulators actually expect in practice and how those expectations apply to modern, fast-moving business models.

This article explains how KYC and CDD fit together, what the Financial Crimes Enforcement Network (FinCEN) and other regulators focus on, how customer identity, beneficial ownership, screening, and monitoring work in practice, and where fintech teams commonly run into trouble.

At InnReg, we help fintechs design and operate effective KYC and due diligence programs. From customer onboarding to ongoing monitoring and reporting, our team provides practical support tailored to fintech business models.

What Is KYC in Fintech?

Know Your Customer (KYC) happens before fintechs establish a relationship with their customers. KYC refers to the controls fintech and financial services firms use to identify and verify a potential customer’s identity. At its core, KYC answers a single regulatory question: Who is the customer using the platform?

In practice, KYC involves collecting key identifying information and taking reasonable steps to confirm that the customer is who they claim to be. This applies to both individual customers and legal entities and is most visible during the onboarding process, before an account is permitted to transact.

KYC requirements exist because criminals, terrorists, and other bad actors may attempt to use legitimate financial platforms to conceal their identity and access the financial system.

Regulators, therefore, require firms to implement identity verification controls designed to prevent impersonation, fraud, and anonymous misuse of regulated products and services.

What Is CDD in Fintech?

Customer Due Diligence (CDD) is the ongoing process fintech firms use to understand, assess, and manage the risk a customer presents throughout the lifecycle of the relationship. While KYC establishes who the customer is, CDD focuses on how and why the customer uses the product or service, and whether that activity aligns with the firm’s risk expectations.

CDD involves evaluating the nature and purpose of the customer relationship, developing a customer risk profile, and applying appropriate monitoring based on that risk. This includes understanding expected transaction behavior, ownership and control structures for legal entities, geographic exposure, and changes in activity over time.

Unlike KYC, which focuses on onboarding, CDD is continuous. It follows the customer through the entire relationship, covering transaction monitoring, periodic reviews, screening updates, and escalation whenever something shifts, whether that’s behavior patterns, ownership, or risk factors.

Know Your Customer (KYC) vs. Customer Due Diligence (CDD)

Know Your Customer (KYC) and Customer Due Diligence (CDD) are related but distinct components of a compliance program. Treating them as interchangeable is a common source of gaps, particularly in fintech environments where onboarding is fast and largely automated.

KYC is the starting point. It focuses on identifying and verifying who the customer is before a relationship is established by collecting required identifying information and taking reasonable steps to confirm identity. While KYC addresses the question of identity, it doesn’t assess how the customer will use the product or the risk they may present.

CDD builds on KYC and applies throughout the life of the customer relationship. It focuses on understanding the nature and purpose of the account, assessing customer risk, and applying appropriate ongoing monitoring. This includes evaluating expected activity, ownership and control, geographic exposure, and changes in behavior over time.

From a regulatory perspective, KYC is necessary but not sufficient. Examiners focus heavily on whether firms actively use KYC information to assess risk and adjust controls through CDD. Programs that meet regulatory expectations treat KYC as the foundation and CDD as the framework that turns identity data into ongoing risk management.

The Role of FinCEN

In the US, the law governing KYC/CDD is the Bank Secrecy Act (BSA), enforced by the Financial Crimes Enforcement Network (FinCEN), a bureau of the U.S. Department of the Treasury. While the BSA was passed in 1970, current provisions have been heavily influenced by amendments passed after the September 11, 2001, terror attacks and the resulting USA PATRIOT Act.

FinCEN has the power to investigate and enforce a wide range of AML provisions. It can take enforcement actions, including civil money penalties levied on companies, partners, directors, officers, or employees who participate in violations. It can even make criminal referrals for further investigation and prosecution.

Areas of FinCEN scrutiny are compliant registration, recordkeeping, and reporting. The strength of compliance programs affects whether and how seriously FinCEN pursues potential violations, as well as how severely it penalizes violations.

Establishing Customer Identity Under FinCEN Rules

As the phrase “Know Your Customer” implies, regulated financial institutions are required to establish and verify customer identity before permitting access to products or services. In the US, commonly used identifiers include Social Security Numbers or Federal Tax Identification Numbers, along with other core identifying information necessary to confirm that customers are who they claim to be.

Firms are also expected to collect reliable address information and, where relevant, additional details that help inform customer risk. This may include indicators such as foreign residency, cross-border activity, complex ownership structures, or the nature and purpose of the products or services being used. The specific information collected should reflect the firm’s business model, customer base, and risk exposure.

FinCEN does not prescribe a single set of data elements or verification methods. Instead, it focuses on whether firms have designed and implemented reasonable, risk-based policies, procedures, and processes that are followed consistently and in good faith. Regulators evaluate whether identity controls are appropriate given how the business operates, not whether a particular tool or checklist is used.

That means the firm is responsible for determiningwhat information is adequate and appropriate based on its products, delivery channels, and customer risks. While this flexibility allows fintechs to tailor identity controls to modern business models, it also raises the bar. Firms must be able to clearly justify how their KYC requirements align with their risk profile and demonstrate that those requirements are applied in practice.

What Is the FinCEN CDD Rule?

FinCEN’s Customer Due Diligence rule defines the core expectations regulators use to evaluate KYC/CDD programs. Rather than prescribing specific tools or technologies, the rule focuses on outcomes.

Scope and Applicability

The CDD Rule applies to “covered financial institutions,” including banks, federally insured credit unions, mutual funds, brokers or dealers in securities, futures commission merchants, and introducing brokers in commodities.

The Rule spells out four core components of customer due diligence: customer identification, beneficial ownership identification, understanding the nature and purpose of the customer relationship, and ongoing monitoring.

Regulatory Integration

The CDD Rule is designed to operate as part of a broader AML framework, not as a standalone requirement.

By requiring firms to formally embed risk-based customer due diligence into their written AML policies and day-to-day processes, it reinforces existing program elements, such as internal controls, independent testing, designated compliance personnel, and training.

Learn more about AML compliance →

Flexibility and Risk Basis

While the Rule mandates what outcomes are required, it does not rigidly prescribe how firms must achieve them.

FinCEN has clarified that firms can rely on beneficial ownership information provided by the customer unless there are known reliability concerns. The agency also expects the depth of due diligence beyond baseline requirements to match the customer’s risk profile.

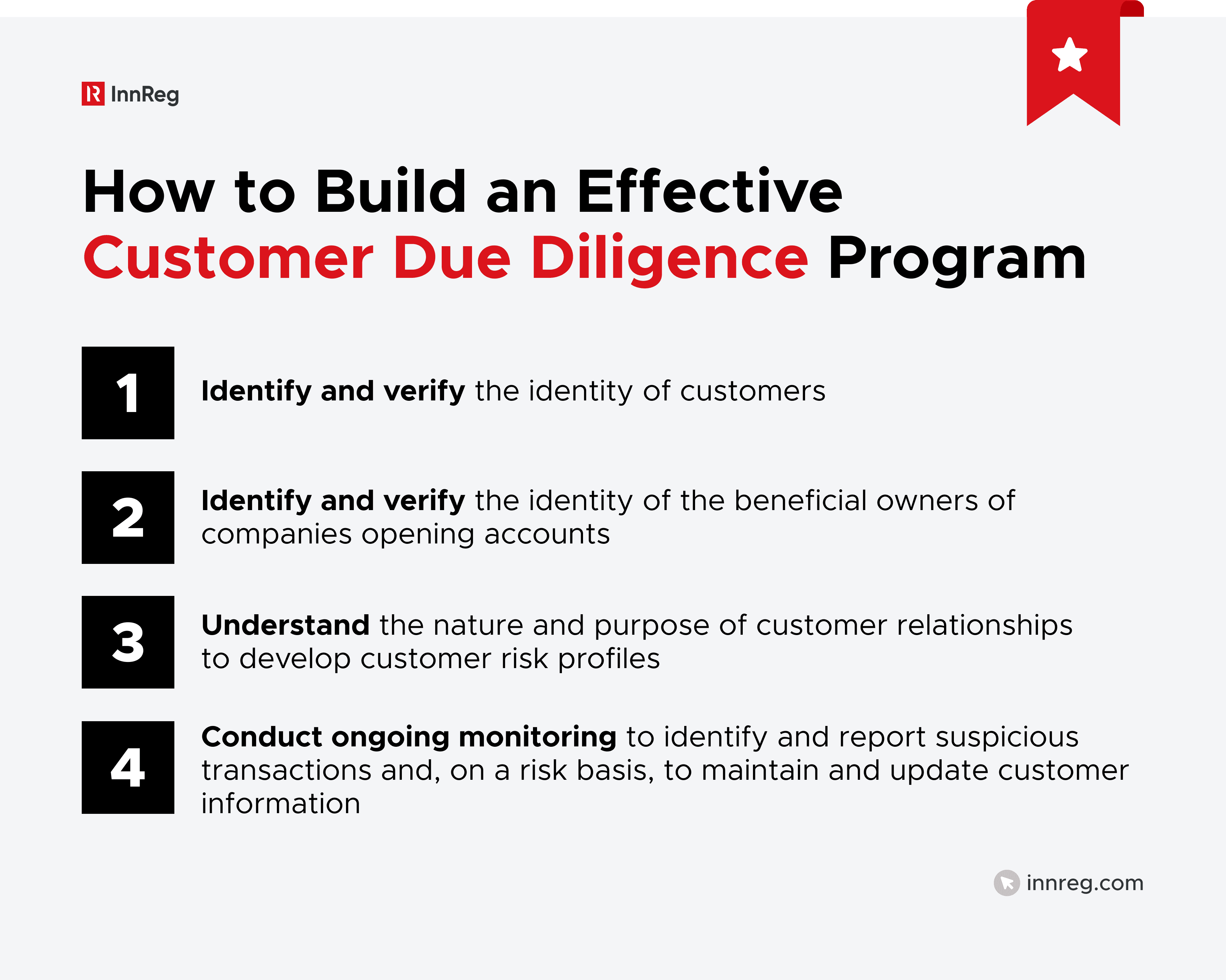

How to Build an Effective Customer Due Diligence Program

An effective customer due diligence program is risk-based and designed to operate across the full customer lifecycle, not just at onboarding. Regulators expect firms to connect identity verification, ownership analysis, risk profiling, and monitoring into a structured framework that’s documented, consistently applied, and responsive to changes in customer risk over time.

1. Identify and Verify the Identity of Customers

The starting point is knowing who the customer actually is. This applies to individuals and legal entities and usually happens during onboarding.

Firms are expected to collect basic identifying information and take reasonable steps to verify it. Document collection is not the goal here. This first step is for firms to develop a reasonable understanding of customer identity. How that verification is done should reflect the product, how customers access it, and the risks involved.

For fintechs with digital onboarding, this typically means combining document checks with non-documentary methods, along with clear escalation steps when results are unclear or inconsistent.

2. Identify and Verify the Identity of the Beneficial Owners

When the customer is a legal entity, regulators expect firms to understand who actually stands behind it. That means identifying the individuals who own or control the business, not just the company name on the account.

This generally involves identifying beneficial owners based on ownership thresholds and at least one person who exercises meaningful control. Beneficial ownership is a common area of regulatory scrutiny, especially where ownership is layered, foreign, or poorly documented.

Verification of beneficial owners should follow the same general standards used for individual customers, with adjustments based on risk.

See also:

3. Understand the Nature and Purpose of Customer Relationships

CDD requires more than identity. Firms must understand why the customer is opening the account and how the account is expected to be used.

This information forms the basis of the customer risk profile. It may include the type of activity expected, transaction volumes, geographic exposure, and the products or services being used. Without a clear understanding of expected activity, effective monitoring is not possible.

For fintech companies, this step is especially important because innovative products often fall outside traditional risk assumptions. Documenting the business rationale and risk considerations behind customer onboarding decisions is critical for both internal governance and regulatory exams.

See how InnReg helps fintech navigate regulatory exams →

Need help with fintech compliance?

Fill out the form below and our experts will get back to you.

4. Conduct Ongoing Monitoring

KYC/CDD efforts do not stop once a customer opens an account. Depending on the customer's risk or the nature of certain account transactions, lenders may also need to carry out ongoing monitoring of a customer’s account.

Examples of potentially suspicious activity:

A customer begins making loan payments from a suspicious source of funds, such as a non-US bank account, a second loan or line of credit, a cryptocurrency account, etc.

Loan payments are made from a third-party account that wasn’t identified during the KYC/CDD process or not directly linked to the borrower.

There’s unusual activity in a line-of-credit loan: a high volume of small debits and credit transactions, or large transactions well outside historical transaction amounts.

Online lenders must build and maintain robust processes to flag suspicious activity, pause or prevent suspicious loan account payments or withdrawals, and follow reporting protocols, including using the BSA’s E-Filing system to submit formal Suspicious Activity Reports as warranted.

The Importance of a Customer Identification Program (CIP)

Customer Identification Program (CIP) requirements sit at the front end of KYC/CDD. They define what information firms collect at onboarding and how identity is verified before a customer is permitted to transact.

CIP Minimum Information Requirements

At a baseline, CIP requires firms to collect specific identifying information before opening an account. The exact data elements depend on whether the customer is an individual or a legal entity.

Customer Type | Common CIP Information Collected |

|---|---|

Individual | Name, date of birth, address, government-issued ID number |

Legal Entity | Legal name, address, EIN, formation details |

Beneficial Owners | Name, date of birth, address, ID number |

Firms must also take reasonable steps to verify accuracy:

Verification Methods: Documentary and Non-Documentary

FinCEN allows flexibility in how identity is verified. Most fintechs use a combination of methods rather than relying on a single check.

Documentary methods typically include government-issued IDs or formation documents. Non-documentary methods may involve database checks, knowledge-based verification, device data, or other corroborating information. The mix should reflect customer risk and how the product is accessed.

For digital-first fintechs, the key is consistency and defensibility, not sophistication. Regulators tend to focus on whether firms apply verification methods as designed and handle exceptions in a controlled way.

Remote and Digital Onboarding Considerations

Onboarding customers online introduces risks that do not exist in face-to-face environments. Impersonation and synthetic identities are the most common.

To address this, fintechs typically use multiple verification signals instead of a single check. What matters most is having a clear process for handling conflicting results and situations that cannot be resolved through automation alone.

When Identity Cannot Be Verified

CIP rules require firms to define what happens when identity verification fails. This is often overlooked until it becomes a problem.

Programs should clearly address when accounts are restricted, delayed, or declined, and how those decisions are documented. Ignoring or bypassing unresolved verification issues does not make them disappear. They tend to surface later through monitoring failures or exam findings.

For fintechs operating at scale, clear CIP decision logic reduces operational friction and limits inconsistent treatment across customers. It also provides examiners with a clear view of how identity risk is handled in practice.

See also:

Legal Entities and Beneficial Ownership Due Diligence

When the customer is a legal entity, KYC/CDD goes beyond the company name. Firms are expected to understand who owns or controls the entity and how that structure affects risk.

Beneficial Owners vs. Control Persons

Beneficial ownership reviews usually focus on two categories: beneficial owners and control persons.

Beneficial owners are individuals who own a meaningful portion of the entity, based on regulatory ownership thresholds. Control persons are individuals with authority over the business, such as executives or senior managers, even if they do not hold an ownership stake.

Both are relevant. Ownership shows who benefits economically, while control shows who makes decisions. Regulators expect firms to identify and document each where required.

What Information Is Collected and Verified

For each beneficial owner and control person, firms generally collect the same core identifying details required for individual customers. This usually includes name, date of birth, address, and an identification number.

Verification should follow the same general approach used for individuals, with adjustments based on risk. Entities with opaque or cross-border ownership often require additional review.

Handling Complex and Layered Ownership Structures

Many fintech customers operate through multi-layered corporate structures. These are not inherently problematic, but they demand clear ownership mapping.

Teams should be able to articulate how ownership was reviewed and where conclusions were drawn. Problems typically arise when assumptions are made without supporting documentation.

Practical guidance on tracing ownership, escalating complexity, and recording decisions helps avoid inconsistency as onboarding accelerates.

Corporate Transparency Act Considerations

The Corporate Transparency Act (CTA) introduces a parallel beneficial ownership reporting regime administered by FinCEN. While it does not eliminate existing CDD obligations, it changes the broader context in which beneficial ownership information is collected and validated.

Learn more about reporting beneficial ownership under CTA →

For now, fintechs should continue to follow existing CDD requirements while tracking how CTA implementation evolves. Firms should design programs that can adapt as regulators clarify how CTA data will interact with customer due diligence expectations.

Ownership Changes Over Time

Beneficial ownership due diligence does not end at onboarding. Changes in ownership or control can materially alter customer risk.

Effective programs define when ownership information must be refreshed and how changes are reviewed and documented. FinCEN often treats failing to update ownership information the same as failing to collect it in the first place.

For fintech teams managing high volumes of entity customers, having clear and consistent procedures for ownership updates reduces both compliance risk and operational friction.

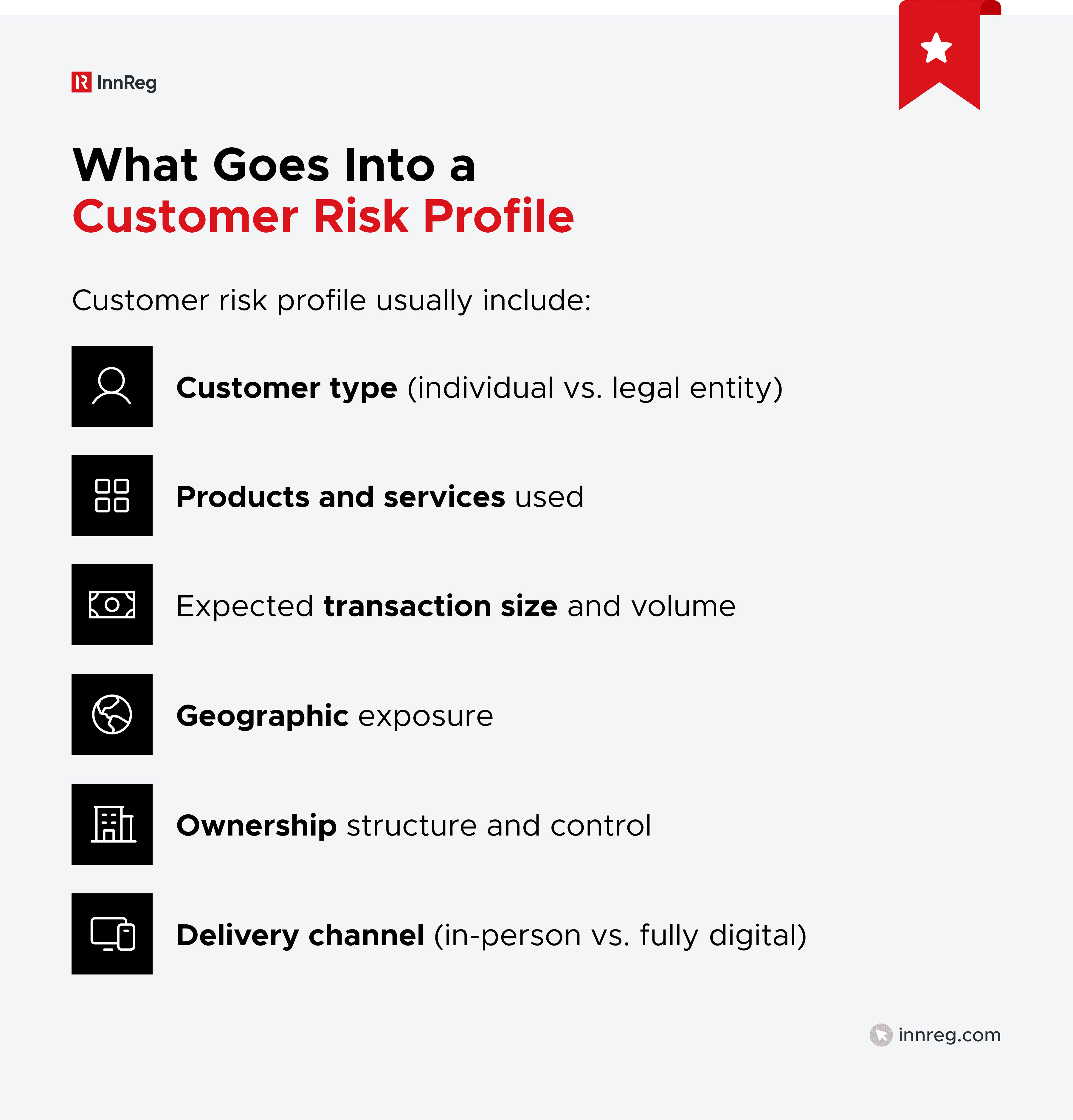

Risk Profiling: Turning KYC Data into a Customer Risk Rating

Collected information needs to be analyzed and translated into a clear view of customer risk. Risk profiling is how firms decide which customers require closer oversight and which can be monitored through standard controls.

Regulators expect risk profiling to be systematic and tied to documented criteria. It does not need to be complex, but it does need to be consistent and defensible.

Certain attributes tend to increase customer risk, such as PEP status, sanctions exposure, or connections to higher-risk sectors or regions.

Having one of these characteristics does not automatically disqualify a customer. Instead, it affects how the relationship is managed. Well-defined criteria allow teams to apply enhanced controls in a structured and repeatable way.

Note: Risk profiling is not static. New products, changes in ownership, shifts in transaction behavior, or new adverse information can all require reassessment.

See also:

Screening Requirements

Screening sits alongside identity verification and risk profiling. While it often happens automatically in the background, regulators view screening as a substantive control. Screening is how firms identify customers and activities that may present sanctions, corruption, or financial crime risk.

Screening typically includes checks against sanctions lists, politically exposed person lists, and other watchlists, as well as reviews for adverse media. These checks apply to customers, beneficial owners, and, in some cases, counterparties.

Screening does not replace broader due diligence. A clean screening result does not mean a customer is low risk, and a potential match does not automatically mean wrongdoing. Results must be reviewed in context.

When Is Screening Conducted?

Initial screening is generally performed during onboarding, before an account is allowed to transact. That’s only the starting point.

Regulators expect ongoing rescreening over time. This can happen periodically or when triggering events occur, such as changes in ownership, new products, or updates to sanctions lists. Ongoing screening is particularly important for entity customers and higher-risk profiles.

Recordkeeping and Audit Trails

Screening controls need to leave a clear record. Firms should be able to show when screening occurred, what lists were used, how matches were reviewed, and why decisions were made.

For fintechs using third-party screening tools, this also means understanding what the tool does and how results feed into internal workflows. Documentation and ownership become more important as automation increases.

Well-designed screening processes support the broader KYC/CDD framework by flagging elevated risk early and feeding accurate information into monitoring and escalation workflows.

Common Compliance Challenges

Even well-designed KYC/CDD programs can struggle in execution. In fintech environments, challenges tend to surface where responsibility, scale, data, and product decisions intersect.

Most issues are operational, with the most common being:

BaaS dependency and unclear ownership of controls: Fintechs that rely on banking-as-a-service partners often assume certain KYC/CDD responsibilities sit entirely with the bank. In practice, an unclear division of duties creates gaps. Regulators and partners expect roles to be defined, documented, and actively managed, not implied.

Scaling issues from manual reviews and backlogs: Processes that work at launch often break down as customer volume grows. Manual reviews pile up, alerts age out, and decisions become inconsistent across reviewers. Without clear thresholds and escalation logic, scale exposes weaknesses quickly.

Data quality issues: KYC/CDD programs depend on accurate inputs. Incomplete, inconsistent, or outdated data weakens risk profiling, screening, and monitoring. Automation does not fix poor data. It often amplifies it.

Misalignment between product and compliance: When product teams design flows without risk-based gating in mind, compliance teams are left reacting after launch. Features that bypass onboarding controls or allow unrestricted activity increase exposure. Effective programs align product access with customer risk from the start.

InnReg helps fintechs tackle these challenges in practical, operational ways. We help clarify who owns KYC/CDD controls across bank partners and vendors, build workflows that scale without excessive manual review, and align compliance with how products actually function.

Learn more about our KYC and AML compliance consulting services →

—

KYC/CDD requirements are operational controls that shape how fintechs onboard customers, manage risk, and interact with regulators, bank partners, and counterparties.

As this article outlines, effective KYC and CDD programs depend on clear ownership, documented reasoning, and controls that function beyond onboarding.

For fintechs, the challenge is rarely a lack of rules. It’s translating risk-based expectations into processes that scale with growth, support product innovation, and hold up under examination. Identity verification, beneficial ownership, risk profiling, screening, and monitoring all need to work together, not as isolated steps.

Maria is a Compliance Consultant at InnReg delivering compliance solutions for fintech clients across broker-dealer, RIA, and money transmitter verticals. She brings prior experience at Finalis, Fenix Securities and PwC, with expertise in AML, CCO support, investment banking operations and securities compliance. She holds FINRA Series 14, 24, and 82 licenses and actively supports regulatory and compliance processes revolving broker-dealer activities.

How Can InnReg Help?

InnReg is a global regulatory compliance and operations consulting team serving financial services companies since 2013.

We are especially effective at launching and scaling fintechs with innovative compliance strategies and delivering cost-effective managed services, assisted by proprietary regtech solutions.

If you need help with compliance, reach out to our regulatory experts today:

Related Articles

Featured LinkedIn Posts