AI for Financial Planning: What RIAs Should Know

Key Takeaways

Firms are using AI for practical functions such as meeting notes, CRM automation, financial modeling, risk profiling, and client communications.

AI-generated recommendations may be treated as regulated investment advice when they are personalized and influence investment decisions.

Using AI does not change a firm’s core obligations around fiduciary duty, marketing compliance, or supervisory oversight.

AI introduces compliance risks related to data privacy, vendor oversight, recordkeeping, and model governance.

A strong AI compliance approach starts with mapping use cases, assessing regulatory risk, updating policies, and training staff.

Artificial intelligence is rapidly entering advisory workflows. AI for financial planning is now embedded in tools that analyze portfolios, summarize meetings, generate client communications, and update planning data. Many registered investment advisors (RIAs) are experimenting with these capabilities, often through features built directly into CRM systems, portfolio tools, and financial planning platforms.

At the same time, the regulatory expectations around technology have not changed. Using AI does not change an advisor’s fiduciary obligations, marketing responsibilities, or supervisory duties. The SEC and FINRA have repeatedly emphasized that existing rules still apply when firms deploy new technologies. That means RIAs must understand where AI fits into their advisory process and how to supervise it appropriately.

This article explains what RIAs should know before adopting AI for financial planning. It covers how advisory firms use these tools today, where AI intersects with regulated investment advice, and how regulators are approaching the technology.

At InnReg, we help RIAs evaluate how AI tools fit into their compliance framework. Our team supports firms with compliance program design, written policies and procedures, vendor reviews, and ongoing operational compliance.

What AI for Financial Planning Actually Means

“AI for financial planning” is often used as a catch-all phrase. In practice, it refers to a range of technologies that assist advisors in analyzing financial data, generating insights, automating workflows, or interacting with clients.

Most AI tools used by RIAs do not replace the advisor. They support specific parts of the planning process, such as summarizing information, identifying patterns in client data, or modeling financial scenarios.

In the advisory context, AI typically works alongside existing planning systems. It may pull information from CRMs, portfolio management tools, and financial planning software to generate summaries, recommendations, or alerts.

The advisor remains responsible for reviewing outputs and determining whether the information is appropriate for a client’s circumstances. AI should be viewed as a productivity layer on top of existing advisory workflows rather than a fully autonomous planning system.

For compliance teams, the key question is how the technology interacts with the firm’s advisory process. When AI tools influence investment decisions, client communications, or planning recommendations, they become part of the firm’s regulated advisory activity and must be supervised accordingly. Understanding this distinction is the first step in evaluating how AI fits into a compliant financial planning practice.

Explore the key differences between RIAs and broker-dealers here →

Internal Productivity Tools vs. Client-Facing Advice Tools

AI tools used by RIAs generally fall into two broad categories. Some tools support internal operations, while others interact directly with clients or influence recommendations. The regulatory implications differ depending on whether AI assists internal workflows or participates in the advisory process.

Internal productivity tools help advisors manage information and administrative work. Client-facing systems operate closer to the advisory function. The difference can be easier to see when the two categories are compared side by side:

Category | What the AI Does | Typical Examples | Primary Compliance Focus |

|---|---|---|---|

Internal productivity tools | Supports internal workflows and administrative tasks | Meeting transcription, note summaries, CRM updates, document data extraction, draft emails | Data privacy, cybersecurity, vendor oversight, recordkeeping |

Planning support tools | Assists advisors in analyzing financial planning scenarios | Retirement projections, tax strategy analysis, portfolio scenario modeling | Model oversight, accuracy review, supervision of advisor use |

Client-facing advisory tools | Interacts with clients or produces personalized planning outputs | Client chat interfaces, automated planning insights, personalized recommendations | Fiduciary duty, supervision of advice, disclosures, and marketing rule |

For RIAs evaluating AI for financial planning, the closer the tool operates to client recommendations, the more oversight and documentation will typically be required. Internal tools may fall under operational controls, while systems that shape planning advice should be treated as part of the firm’s advisory process.

Generative AI, Predictive Models, and Optimization Engines

AI for financial planning includes several types of technologies, each serving a different purpose in advisory workflows:

Generative AI tools create text, summaries, or reports based on prompts and available data. Advisors commonly use them to draft meeting notes, generate client communications, or prepare planning summaries. These systems are useful for productivity, but their outputs must be reviewed because they can occasionally produce inaccurate or incomplete information.

Predictive models analyze historical data to estimate potential future outcomes. In financial planning, they may support forecasting of retirement income, portfolio performance scenarios, or client cash flow projections. These tools help advisors evaluate possibilities rather than produce definitive predictions.

Optimization engines take planning inputs and attempt to identify efficient strategies. For example, a system may evaluate tax strategies, withdrawal sequences, or portfolio allocations to identify potential improvements. These tools have existed in financial planning software for years, but newer AI approaches can process larger datasets and produce more dynamic recommendations.

Understanding these categories helps RIAs evaluate where AI fits into their advisory process. Each type of tool introduces different supervision, testing, and documentation considerations that compliance teams should address before widespread adoption.

How RIAs Are Using AI for Financial Planning

Advisory firms are adopting AI gradually, often through tools already embedded in their existing platforms. Financial planning software, CRM systems, and portfolio management tools increasingly include AI features that assist with analysis, documentation, and client communications. In most cases, AI for financial planning is being used to support advisors rather than replace them.

Many RIAs start with operational use cases. These tend to carry lower regulatory risk and provide immediate productivity benefits. Over time, firms often expand AI usage into planning analysis, client engagement, and portfolio insights.

The sections below highlight some of the most common ways advisory firms are currently applying AI within financial planning workflows.

Meeting Notes, Summaries, and CRM Automation

Meeting documentation is one of the earliest and most common uses of AI in advisory firms. AI tools can record meetings, generate structured summaries, extract key financial details, and create follow-up task lists.

For advisors, this reduces manual note-taking and administrative work. Client conversations can be captured more consistently, and relevant information can be pushed into the firm’s CRM or planning system. These tools primarily function as operational support rather than advice generation.

Typical applications include:

Automatic meeting transcription and summaries

Extracting client financial details discussed during meetings

Creating follow-up tasks and reminders

Drafting post-meeting emails to clients

Updating CRM records with new information

Even though these tools focus on internal workflows, they still interact with sensitive client information. Firms should consider data security, vendor access to client information, and record retention obligations when deploying them.

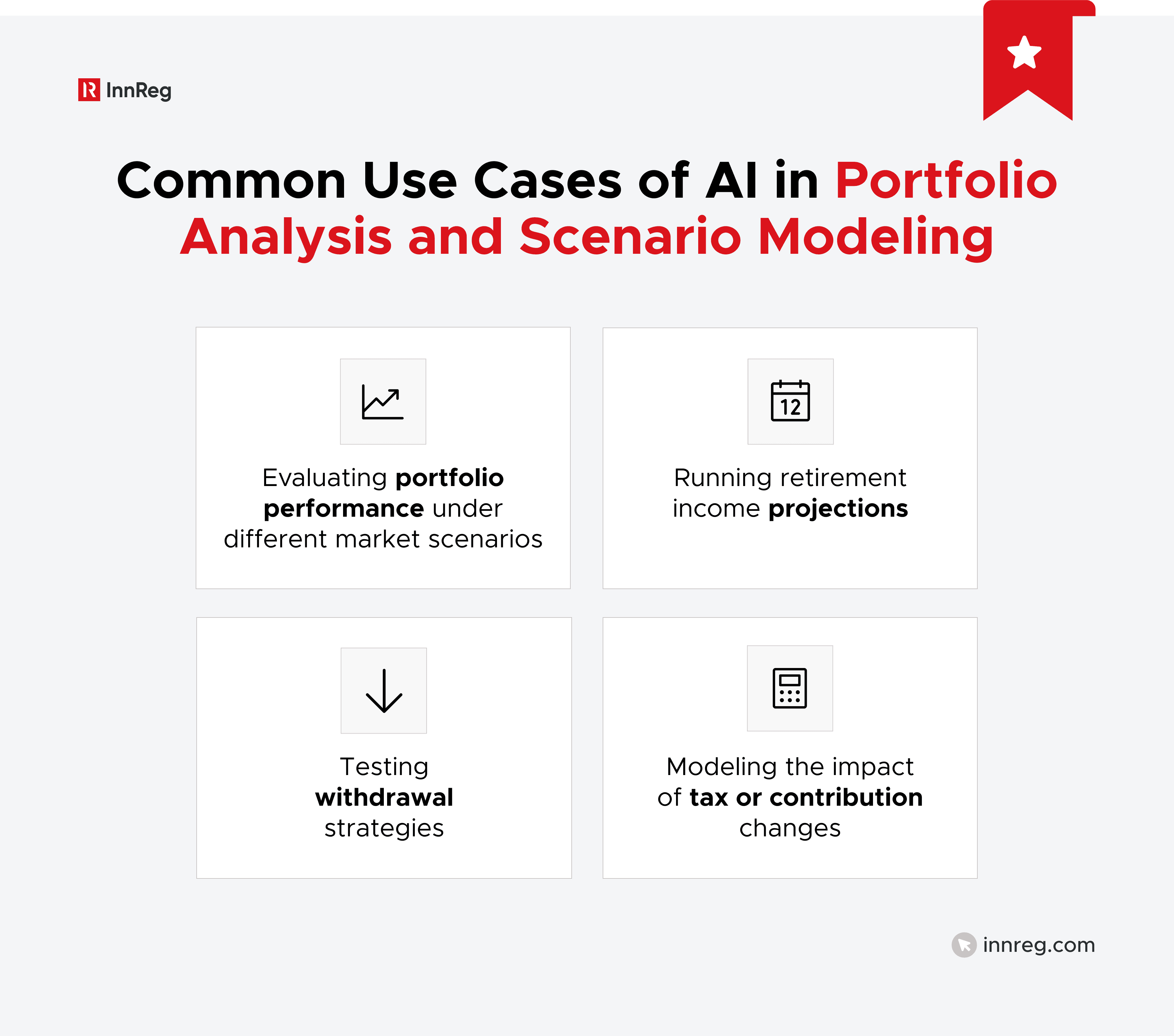

Portfolio Analysis and Scenario Modeling

AI tools are also being integrated into portfolio analysis and planning models. These systems can evaluate multiple market scenarios, analyze portfolio allocations, and generate projections based on historical and current data.

For advisors, this can accelerate planning analysis. Instead of manually running multiple projections, AI systems can generate several potential scenarios in seconds. The advisor still determines whether the outputs are reasonable and appropriate for the client’s financial situation.

These tools are not new in concept. Financial planning software has included modeling capabilities for years. What is changing is the scale and speed of analysis. AI allows platforms to process larger datasets and generate more dynamic planning insights.

Risk Profiling and Client Data Collection

Another growing use case involves collecting and analyzing client information during the onboarding or planning process. AI tools can assist with risk questionnaires, financial data collection, and preliminary analysis of client financial situations.

For example, some platforms analyze responses from client questionnaires and suggest potential risk profiles or planning priorities. Others help organize complex financial information into structured planning data.

In these cases, AI for financial planning acts as a data organization and analysis layer, helping advisors interpret client inputs more efficiently.

However, risk profiling has regulatory implications. Firms must document how client information is collected and how recommendations are formed. AI-generated insights should be reviewed by an advisor before they influence portfolio decisions or investment recommendations.

See also:

AI in Client Communications and Marketing

AI is increasingly used to draft communications with clients. Advisors may use AI tools to generate explanations of market events, planning updates, or educational materials.

This can reduce the time required to produce written communications. It also allows advisors to quickly generate drafts that can be edited before distribution.

Examples include:

Drafting market commentary or client newsletters

Preparing educational explanations of financial concepts

Creating planning summaries or meeting recaps

Drafting personalized client updates

Even though these communications may begin as AI-generated drafts, they are still subject to regulatory oversight. Client communications must comply with the SEC Marketing Rule and the firm’s supervisory procedures, regardless of how the content was generated.

Need help with RIA compliance?

Fill out the form below and our experts will get back to you.

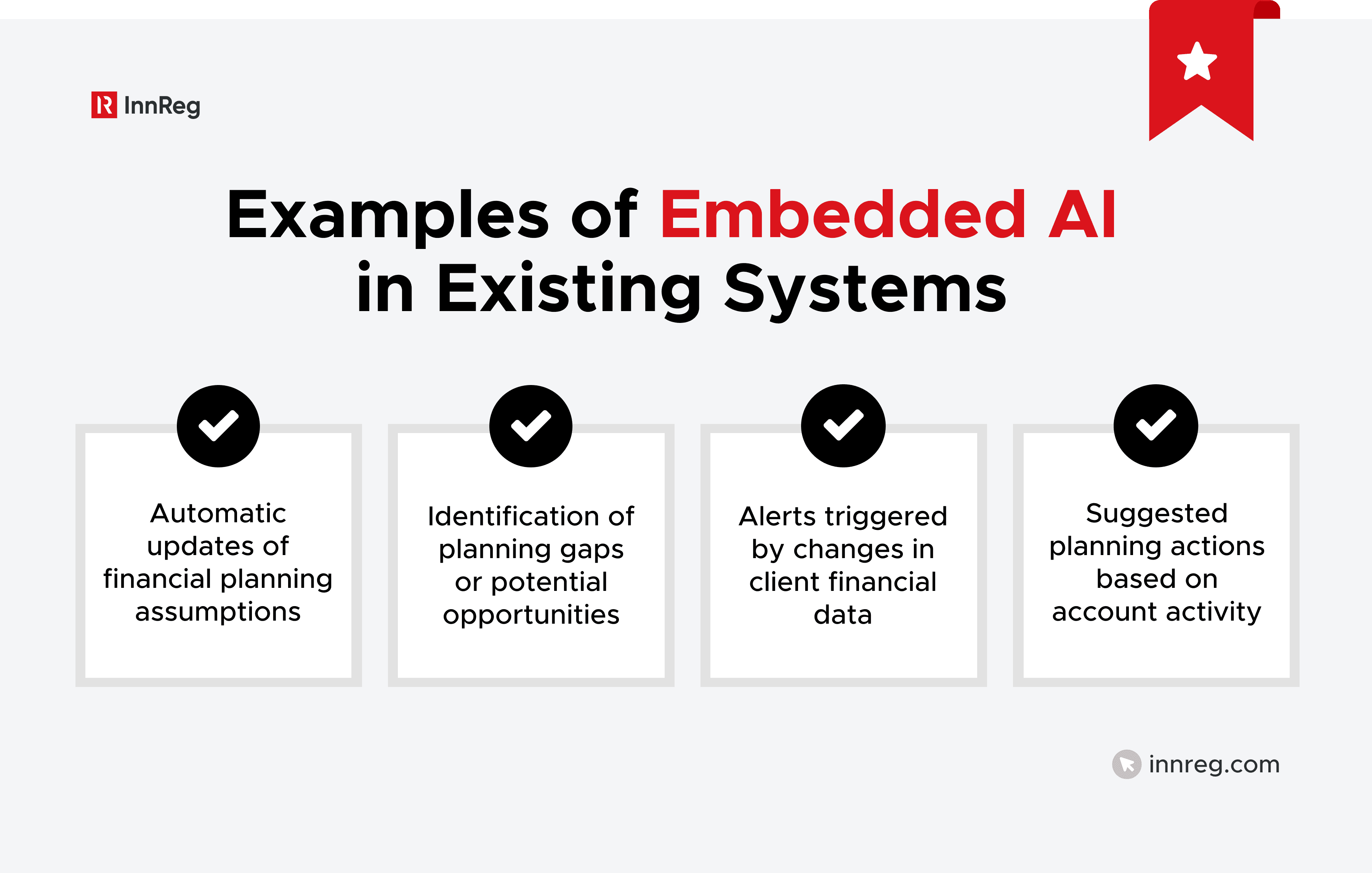

AI Embedded in Financial Planning Platforms

Many advisors encounter AI through features embedded directly in the software they already use. Financial planning platforms, portfolio tools, and CRM systems are gradually adding AI-driven functionality.

These features may include automated data extraction, planning insights, or suggestions based on client financial data. Advisors may not always perceive these functions as “AI,” but they still rely on algorithmic analysis.

For RIAs, this trend raises an important operational question. When AI capabilities are embedded inside third-party platforms, firms still remain responsible for supervising how those tools are used within their advisory process.

This is where compliance teams often focus their attention. Vendor features can affect planning recommendations, documentation, and client communications. Firms should understand how these tools function and incorporate them into their supervisory framework.

When AI Becomes Investment Advice

AI tools often begin as operational support. Over time, however, their outputs can influence planning decisions or client recommendations.

If an AI tool analyzes client-specific data and produces individualized recommendations, regulators may treat the output as advisory activity. In that situation, the firm’s fiduciary obligations, supervisory controls, and documentation standards apply just as they would for advice produced directly by an advisor.

For RIAs using AI for financial planning, the key issue is supervision. Firms must understand where technology fits into their advisory process and how recommendations are generated:

Lessons From SEC Robo-Advisor Guidance

The SEC addressed automated advice years ago in guidance on robo-advisors. While the technology has evolved, the underlying regulatory logic still applies to modern AI tools used in financial planning.

The guidance focused on three practical areas:

How client information is collected and analyzed

How recommendations are generated

How the firm discloses the role of technology in its advisory process

Even when advice is generated through automated systems, the SEC expects firms to gather sufficient client information and apply it appropriately in the recommendation process. Technology does not change the obligation to base advice on a client’s financial situation, objectives, and risk tolerance.

For firms using AI tools, this means reviewing how the system operates. Compliance teams often examine questions such as:

What client data does the tool use?

How are recommendations or insights generated?

Does the advisor review outputs before they reach the client?

How does the firm explain the technology in disclosures?

These questions help determine whether the technology is acting as an internal analytical tool or as part of the advisory function itself.

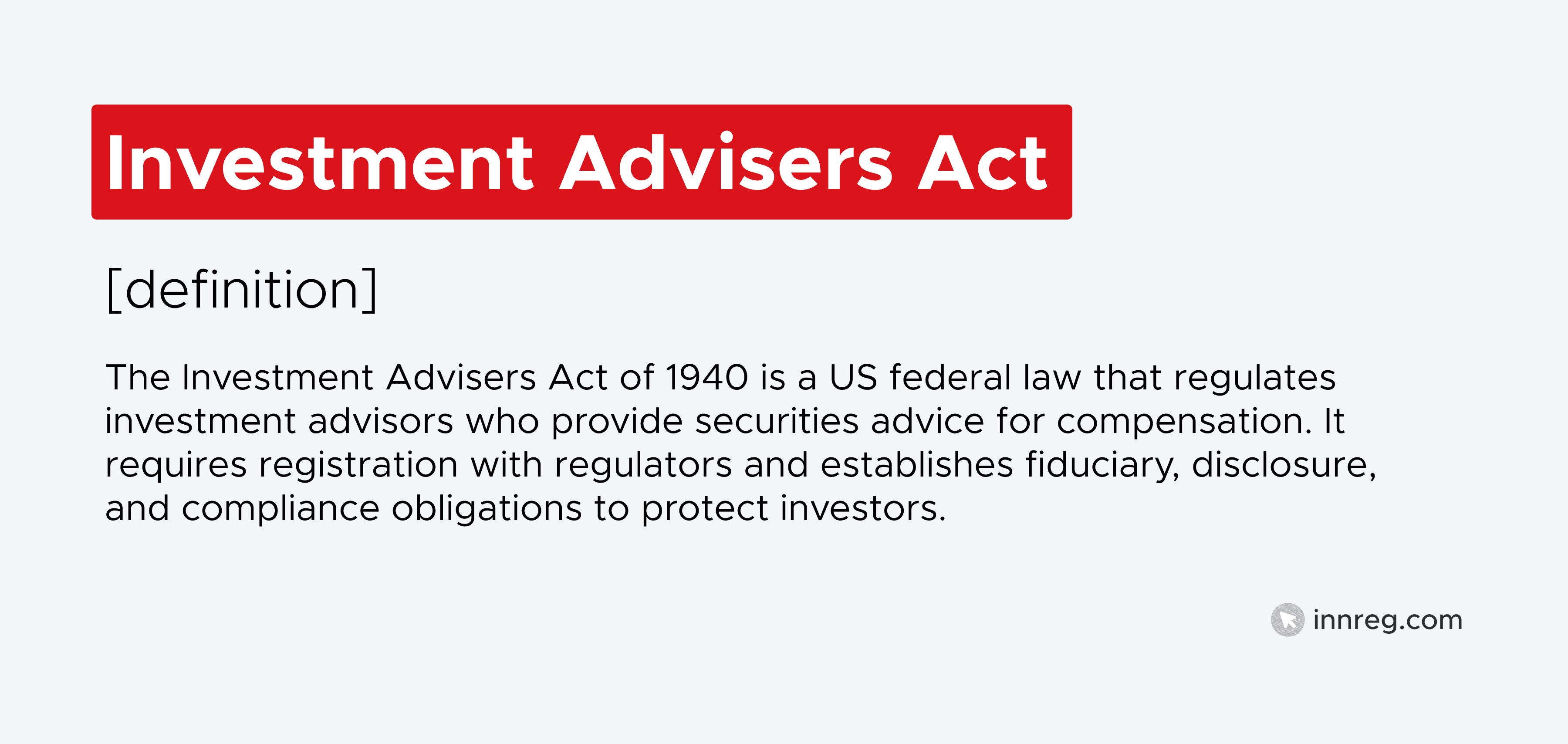

Fiduciary Duty Implications Under the Advisers Act

RIAs operate under a fiduciary duty established by the Investment Advisers Act. This duty includes both a duty of care and a duty of loyalty toward clients. The use of AI does not change those obligations.

If an AI system contributes to investment recommendations, the advisor remains responsible for the quality and appropriateness of those recommendations. Technology may assist with analysis, but it does not transfer the advisor’s responsibility to the system.

Several fiduciary considerations are particularly relevant when AI tools are used in financial planning:

Advisors must understand the factors influencing recommendations generated by the system.

Firms should monitor whether the tool produces outputs consistent with the client’s financial situation.

Conflicts related to algorithms, data sources, or embedded recommendations should be disclosed where relevant.

In practice, this means advisors should treat AI-generated insights as inputs rather than final conclusions. The advisor reviews the output, evaluates whether it aligns with the client’s needs, and determines whether it should influence a recommendation.

SEC and FINRA Oversight of AI for Financial Planning

Regulators are paying close attention to how firms use emerging technology. The SEC and FINRA have both been explicit that existing regulatory frameworks apply to AI-driven systems used in advisory services.

For RIAs, this means evaluating AI tools through the same lens used for other advisory activities. If an AI system influences recommendations, client communications, or marketing materials, the firm must supervise that activity and maintain appropriate records.

Regulators have also signaled that AI will be an examination focus. The SEC has specifically identified generative AI and advanced analytics as areas of interest in its examination priorities. Firms using these tools should expect questions about how the technology works, how outputs are reviewed, and how the firm documents its use.

How the SEC Applies Existing Rules to AI

The SEC has not introduced a comprehensive AI rule for investment advisors. Instead, it evaluates AI use under established obligations in the Investment Advisers Act and related regulations.

In practice, that means compliance teams should review AI tools against the same standards applied to traditional advisory activities. Key areas include fiduciary duty, marketing practices, written supervisory procedures, and recordkeeping.

If AI-generated outputs influence advice, marketing, or client communications, they fall under the same regulatory framework as any other advisory activity.

Learn the differences between RIA and IAR here →

Fiduciary Duty and Duty of Care

Under the Advisers Act, RIAs must act in the best interests of their clients. This includes providing advice that is based on a reasonable understanding of the client’s financial circumstances.

When AI tools assist with portfolio analysis or financial planning recommendations, advisors still carry responsibility for the final recommendation. The duty of care requires advisors to evaluate whether AI-generated insights are reasonable and appropriate for the client.

Firms should be able to explain how AI tools contribute to their advisory process and how advisors review the results before recommendations are delivered.

Marketing Rule and Substantiation

AI is increasingly used to generate marketing content, including blog posts, newsletters, and market commentary. These communications remain subject to the SEC Marketing Rule.

This means statements about AI capabilities must be accurate and supported. Regulators have already taken enforcement action against firms that made misleading claims about their use of AI.

For example, firms have faced scrutiny for suggesting that advanced AI systems drive investment strategies when the underlying technology doesn’t operate as described. Marketing materials should reflect how the technology actually functions.

Compliance Rule and Written Policies

The SEC Compliance Rule requires RIAs to adopt written policies and procedures designed to address risks associated with their business activities.

When firms introduce AI tools into their advisory process, those tools may require updates to internal policies. Areas often affected include technology supervision, vendor oversight, and documentation of advisory decisions.

Compliance programs should address how AI tools are selected, monitored, and reviewed within the firm’s advisory workflow.

Books and Records Obligations

AI tools can generate a large volume of documentation, including meeting transcripts, planning summaries, client communications, and analytical outputs.

These materials may fall under the SEC’s Books and Records Rule. Firms should understand which AI-generated materials must be retained and how they are stored.

For example, if an AI system generates planning summaries that are sent to clients, those communications may need to be preserved in the firm’s records. Recordkeeping obligations apply regardless of whether content is generated by a human or a software system.

See also:

SEC Examination Priorities and Emerging Technology

The SEC’s Division of Examinations regularly identifies emerging technology as an area of interest during regulatory exams. AI and advanced analytics are now part of that conversation.

Examiners may focus on how firms evaluate risks associated with new tools, how advisors supervise automated outputs, and how firms communicate the role of technology to clients.

Common exam questions may include:

How the firm evaluates third-party AI vendors

Whether advisors review AI-generated recommendations

How AI-generated communications are supervised

How the firm documents the use of technology in its advisory process

Firms that adopt AI for financial planning should be prepared to explain how the technology fits into their supervisory framework.

FINRA Considerations for Dual Registrants

Many advisory firms operate as dual registrants or have affiliated broker-dealers. In those cases, FINRA rules may apply alongside SEC requirements.

FINRA has acknowledged the rapid development of generative AI and reminded member firms that existing supervisory and communications rules still apply. This includes rules governing public communications, supervision, and recordkeeping.

For dual registrants, AI-generated communications and planning outputs may fall under both regulatory frameworks. Firms should review how AI tools affect both their advisory and broker-dealer compliance obligations.

In practice, this often requires coordination between advisory compliance teams and broker-dealer supervisory functions. Firms that operate in both regulatory environments should evaluate AI use from both perspectives.

Data Privacy, Cybersecurity, and Regulation S-P

AI tools used in financial planning often process large amounts of sensitive client information. Financial plans, account balances, income details, tax data, and personal goals may all pass through these systems. When RIAs adopt AI for financial planning, the technology often expands how client data is collected, stored, and shared across systems.

That shift introduces new operational risks. Data may move between planning software, CRM platforms, AI vendors, and cloud services. Each integration creates another point where client information is processed or stored.

2024 Regulation S-P Amendments and Compliance Deadlines

In 2024, the SEC adopted amendments to Regulation S-P to strengthen requirements around safeguarding customer information and responding to security incidents.

The updates require firms to adopt written incident response procedures and provide notice to affected individuals in certain circumstances. These changes were designed in part to address modern technology environments where client data moves across multiple systems and vendors.

For RIAs using AI tools, these amendments are particularly relevant because AI systems often rely on shared infrastructure and external providers.

Regulation S-P Requirement | What It Means for RIAs Using AI |

|---|---|

Written incident response program | Firms must document how security incidents involving client information are handled |

Client notification requirements | Clients may need to be notified if certain data breaches occur |

Vendor involvement | Third-party providers may assist with the response, but responsibility remains with the RIA |

Data safeguarding obligations | Firms must maintain policies designed to protect customer information |

The key takeaway is that outsourcing technology does not outsource responsibility. Even when AI systems are provided by vendors, RIAs remain accountable for protecting client data.

Vendor Oversight and Incident Response Responsibilities

Most AI capabilities used by advisory firms come from third-party vendors. These vendors may host models, process transcripts, analyze client information, or generate planning insights.

Because of this, vendor oversight becomes a core part of the compliance framework. Firms should understand how vendors access data and how that data is protected.

Common vendor review questions include:

What client data is processed by the AI system?

Where is the data stored and how is it protected?

Does the vendor retain prompts, transcripts, or planning data?

How does the vendor respond to security incidents?

Vendor due diligence should be treated as part of the firm’s broader cybersecurity and privacy program.

Incident response planning also becomes more complex when multiple vendors are involved. If a data incident occurs inside a third-party system, the RIA still needs a process for assessing the situation, coordinating with the vendor, and determining whether notification obligations apply.

For many firms, this is where operational discipline matters. Clear procedures, defined vendor contacts, and documented escalation paths can make incident response more manageable when issues arise.

Model Governance and Risk Management for AI Systems

As AI becomes more integrated into financial planning workflows, firms must treat these tools as part of their operational infrastructure. That means establishing oversight around how models are selected, tested, and monitored. AI systems used in financial planning should be subject to governance and risk management controls similar to other analytical tools used by the firm.

In practice, many AI capabilities come from third-party vendors embedded in planning or CRM platforms. Even when the firm doesn’t build the model itself, the outputs can influence planning decisions, documentation, or client communications. RIAs remain responsible for supervising how these systems are used within the advisory process.

Governance doesn’t need to be overly complex. The goal is to understand how the technology works, how advisors rely on it, and how potential risks are monitored over time.

Governance and Oversight Expectations for RIAs

Governance begins with clear internal responsibility for technology oversight. Someone within the firm should understand how AI tools are deployed and how they interact with advisory workflows.

This doesn’t mean every advisor must understand the technical design of the model. Instead, firms should maintain a basic understanding of how the tool functions and where it fits into the advisory process. Oversight should focus on how AI outputs are reviewed before they influence client recommendations or communications.

Typical governance practices include:

Identifying which AI tools are used across the firm

Documenting the purpose of each system

Defining when advisor review is required

Monitoring how outputs are incorporated into planning decisions

For smaller firms, this oversight may sit with the chief compliance officer or technology lead. Larger firms may involve risk committees or operational teams.

Data Quality, Bias, and Testing Controls

AI models depend heavily on the data used to train or operate them. Poor data quality can lead to inaccurate outputs or misleading insights.

For financial planning tools, data may come from several sources, such as client questionnaires, account data feeds, or manually entered financial information. If the underlying data is incomplete or inaccurate, the resulting analysis may also be unreliable.

Testing controls help identify potential issues before the system is widely used. These controls may include:

Reviewing outputs using sample client scenarios

Comparing AI-generated projections with traditional planning models

Evaluating whether outputs change unexpectedly after software updates

The goal is not to eliminate every possible error. Instead, firms should verify that the system behaves as intended.

Ongoing Monitoring and Change Management

AI tools evolve quickly. Vendors update models, add new features, and change how systems generate outputs. Because of this, oversight can’t be a one-time exercise.

Firms should periodically review how AI tools are performing in practice. Advisors may notice changes in output quality, system behavior, or planning recommendations after updates are introduced.

Ongoing monitoring allows firms to identify when technology changes affect advisory workflows. Monitoring activities may include:

Reviewing vendor update notices

Evaluating whether system changes affect planning outputs

Updating internal procedures if new features alter how advisors use the tool

Reassessing vendor risk if the scope of data processing expands

This approach helps maintain alignment between the firm’s supervisory framework and the technology it relies on.

Applying the NIST AI Risk Management Framework in Practice

Some firms look to structured frameworks to organize their AI governance efforts. One widely referenced example is the NIST AI Risk Management Framework.

The framework focuses on four practical functions: governance, mapping risks, measuring system performance, and managing risks over time. While it was not designed specifically for financial advisors, the structure can help compliance teams organize oversight activities.

Framework Function | Practical Application for RIAs |

Govern | Define responsibility for AI oversight and document policies |

Map | Identify where AI tools are used in advisory workflows |

Measure | Evaluate outputs, data quality, and model performance |

Manage | Monitor systems over time and adjust controls when risks change |

For RIAs adopting AI for financial planning, frameworks like this can provide structure without adding unnecessary complexity. The objective is simply to maintain visibility into how AI systems operate and how they affect the advisory process.

Some firms manage this internally. Others rely on external compliance specialists to help structure governance and documentation. Either approach can work as long as the firm maintains clear oversight of how AI tools influence financial planning activities.

Practical Implementation Framework for AI in an RIA

Adopting AI tools doesn’t need to be a major infrastructure project. Most RIAs begin by introducing AI capabilities through existing software platforms or targeted productivity tools. What matters more is how the firm evaluates the technology and integrates it into its compliance framework.

In practice, implementation often follows a few core steps. These steps help firms identify where AI is being used, assess potential risks, and establish appropriate oversight:

See also:

Map AI Use Cases Across the Firm

The first step is identifying where AI tools are already in use. In many firms, adoption begins informally through individual advisors experimenting with new tools or features embedded in vendor platforms.

A simple inventory can help establish visibility. Firms typically document:

Which AI tools are used across departments

What functions the tools perform

Whether the tool interacts with client data

Whether outputs reach clients directly or remain internal

Mapping use cases allows compliance teams to understand where AI intersects with regulated advisory activities. Some tools may remain operational in nature, while others may affect planning recommendations or client communications.

Conduct a Risk Assessment

Once AI use cases are identified, the firm can evaluate potential risks associated with each tool. This doesn’t require complex modeling. Most firms focus on a few practical areas:

Access to client data

Influence on financial planning recommendations

Client-facing communications generated by the system

Reliance on third-party vendors

The goal is to determine which tools require closer supervision. AI systems that shape planning recommendations or communicate directly with clients typically warrant the most oversight.

Update Policies, Procedures, and Controls

When AI becomes part of advisory workflows, existing compliance documentation may need to be updated. Written supervisory procedures should reflect how these tools are used and reviewed.

Areas that often require updates include:

Technology supervision policies

Vendor management procedures

Client communication review processes

Record retention practices

In many firms, these updates are modest. They clarify how advisors review AI-generated outputs and how the firm supervises the technology.

Perform Vendor Due Diligence

Most AI capabilities used by RIAs come from external vendors. These vendors may process client data, generate financial analysis, or support communication workflows.

Vendor due diligence helps firms understand how these providers operate. Common review areas include:

Data security and privacy protections

Data retention policies

System reliability and service continuity

The vendor’s use of underlying models or third-party services

Vendor oversight is especially important when AI tools process sensitive client financial information.

Train Staff and Establish Ongoing Monitoring

Advisors and staff should understand how AI tools fit into the firm’s workflows. Training doesn’t need to be technical. The focus is on responsible usage and supervision.

Monitoring is also important as tools evolve. Vendors frequently update features and expand functionality. Firms should periodically review whether those changes affect compliance obligations.

AI Use Case Risk Mapping

A simple risk mapping exercise can help firms categorize AI tools based on how they interact with advisory activities:

AI Use Case | Potential Regulatory Risk | Typical Oversight Approach |

|---|---|---|

Meeting transcription and summaries | Client data exposure, recordkeeping | Vendor review, data security controls |

Planning scenario modeling | Influence on financial recommendations | Advisor review of outputs |

AI-generated client communications | Marketing rule and communication supervision | Content review and approval procedures |

Client-facing planning interfaces | Personalized advice delivered through technology | Stronger supervision, disclosures, and documentation |

This type of mapping helps firms prioritize oversight efforts. The closer a tool operates to personalized financial advice, the more structured the supervisory controls typically become.

For many advisory firms, implementation is less about technology and more about process. Firms that already maintain disciplined compliance programs can usually integrate AI tools with relatively modest adjustments.

FAQs About AI for Financial Planning

Is AI for financial planning regulated?

Yes. AI for financial planning is not regulated as a standalone technology, but its use falls under existing financial regulations. When RIAs use AI tools to analyze client data, generate recommendations, or support planning decisions, those activities are governed by the Investment Advisers Act and related SEC rules.

Regulators evaluate the activity rather than the technology. If an AI tool contributes to personalized investment recommendations, it may fall under the advisor’s fiduciary obligations, supervisory controls, and recordkeeping requirements.

Does using AI change an RIA’s fiduciary duty?

No, using AI for financial planning does not change an RIA’s fiduciary duty to its clients. Advisors must still act in the client’s best interest and base recommendations on the client’s financial situation, goals, and risk tolerance.

AI tools may assist with data analysis, projections, or planning scenarios. However, the advisor remains responsible for evaluating whether the output is reasonable and appropriate for the client.

From a regulatory standpoint, fiduciary obligations still require RIAs to:

Understand the basis of recommendations provided to clients

Evaluate whether technology-generated insights align with the client’s circumstances

Disclose relevant conflicts of interest where applicable

In practical terms, AI outputs should be treated as analytical inputs that support the advisor’s decision-making process rather than automated final recommendations.

Can AI-generated recommendations be considered advice?

Yes, depending on how the technology is used. AI-generated recommendations can be considered investment advice if they are personalized and intended to influence a client’s investment decisions.

Regulators typically look at whether the output:

Uses client-specific information

Produces individualized recommendations

Is intended to guide investment decisions

For example, a tool that analyzes a client’s financial profile and suggests a specific portfolio allocation could be viewed as providing investment advice.

By contrast, tools that provide general educational information or high-level market insights may not fall under the same definition.

For RIAs implementing AI for financial planning, the safest approach is to supervise AI-generated recommendations in the same way advisors supervise human-generated advice.

What disclosures are required when using AI tools?

Disclosure requirements depend on how the technology is used in the advisory process. This may involve updating documents such as Form ADV Part 2 disclosures, client agreements, website descriptions of advisory services, and marketing materials referencing AI capabilities.

Firms should also review whether their marketing language accurately reflects how the technology works. Regulators have already brought enforcement actions related to misleading claims about AI capabilities, often referred to as “AI washing.”

How should AI-generated communications be supervised?

AI-generated communications should follow the same supervisory procedures as any other client communication. If AI tools are used to draft emails, reports, newsletters, or planning summaries, those communications remain subject to regulatory oversight. Regulators focus on the final communication delivered to the client, not the method used to create it.

This means firms should apply existing supervisory controls, including advisor review of AI-generated drafts before sending them to clients, recordkeeping for communications delivered to clients, and even marketing review procedures for public-facing content.

Firms should also consider how AI tools store prompts, transcripts, or generated outputs, particularly when those materials contain client information.

—

AI is quickly becoming part of everyday advisory operations. From meeting summaries to portfolio analysis and planning insights, AI for financial planning is already embedded in many of the tools RIAs use to serve clients.

Adopting new technology inside a regulated advisory environment often raises practical compliance questions. Firms must balance innovation with supervisory obligations, vendor oversight, and regulatory expectations.

If your firm is exploring AI for financial planning and wants to understand the compliance implications, InnReg can help you evaluate how these tools fit into your advisory framework and regulatory obligations.

InnReg was founded in 2013 by Francesco Matteini, former Chief Compliance Officer who helped launch and scale some of the most innovative digital broker-dealers over the last two decades. He built compliance programs to support the first zero-commission broker and the first BD-sponsored investor social network. Since its founding, InnReg has attracted highly experienced fintech consultants with long careers in compliance, risk management, and a deep understanding of the fintech industry.

How Can InnReg Help?

InnReg is a global regulatory compliance and operations consulting team serving financial services companies since 2013.

We are especially effective at launching and scaling fintechs with innovative compliance strategies and delivering cost-effective managed services, assisted by proprietary regtech solutions.

If you need help with RIA compliance, reach out to our regulatory experts today:

Related Articles

Featured LinkedIn Posts