Securities Exchange Act of 1934 Explained: Summary and Rules

The Securities Exchange Act of 1934 was a turning point for US financial markets. It set lasting ground rules for how securities are regulated after they start trading, and those rules still shape the market today.

For fintech founders, lawyers, and compliance officers, the Act continues to guide everyday business decisions. This includes how companies are structured as well as how they manage investor relationships and compliance in a competitive market.

In this guide, we will walk you through the key elements of the Securities Exchange Act of 1934 and explain why it still matters. We will also highlight its practical impact on modern financial firms, giving you a clear picture of where it fits in the broader regulatory landscape.

At InnReg, we support broker-dealers and fintech trading platforms with Exchange Act compliance, from policies and procedures to trade surveillance, books and records, and reporting workflows. We collaborate with fintechs to translate SEC and FINRA rules into practical day-to-day processes. Contact us to learn more.

Overview of the Securities Exchange Act of 1934

Here is why the Securities Exchange Act of 1934 was enacted, how it differs from the 1933 Act, and the key provisions that continue to shape today’s markets.

What Is the Securities Exchange Act?

The Securities Exchange Act of 1934 is the law that governs what happens after securities begin trading in the market. Instead of focusing on the initial sale of stocks or bonds, it covers the everyday activity between investors, companies, and intermediaries like broker-dealers and exchanges.

One of the most important changes the Act introduced was ongoing disclosure. Public companies cannot simply share information once and move on. They must keep investors updated on a regular basis, which helps reduce surprises and keeps markets built on reliable information.

The Act also created the Securities and Exchange Commission (SEC). For the first time, a dedicated regulator had the authority to write rules, monitor activity, and step in when misconduct occurred. This gave investors greater confidence that the markets were being actively supervised.

Ultimately, the Securities Exchange Act of 1934 set the stage for how modern markets still operate today. It made transparency and accountability part of the system, shaping the environment in which financial firms and fintech businesses continue to work.

Why Was the Securities Exchange Act of 1934 Enacted?

The Securities Exchange Act of 1934 came out of a period of crisis. After the 1929 stock market crash, confidence in the financial system collapsed. Many investors lost money because companies often withheld information, and market manipulation was widespread.

Lawmakers responded with stronger rules to rebuild trust. The Act set clear standards for transparency and gave regulators the power to step in when markets were abused. By requiring ongoing reporting and placing limits on practices like insider trading, it aimed to create a more fair and stable environment for investors.

For businesses, the Act also signaled a turning point. Operating in public markets now came with responsibilities, not just opportunities.

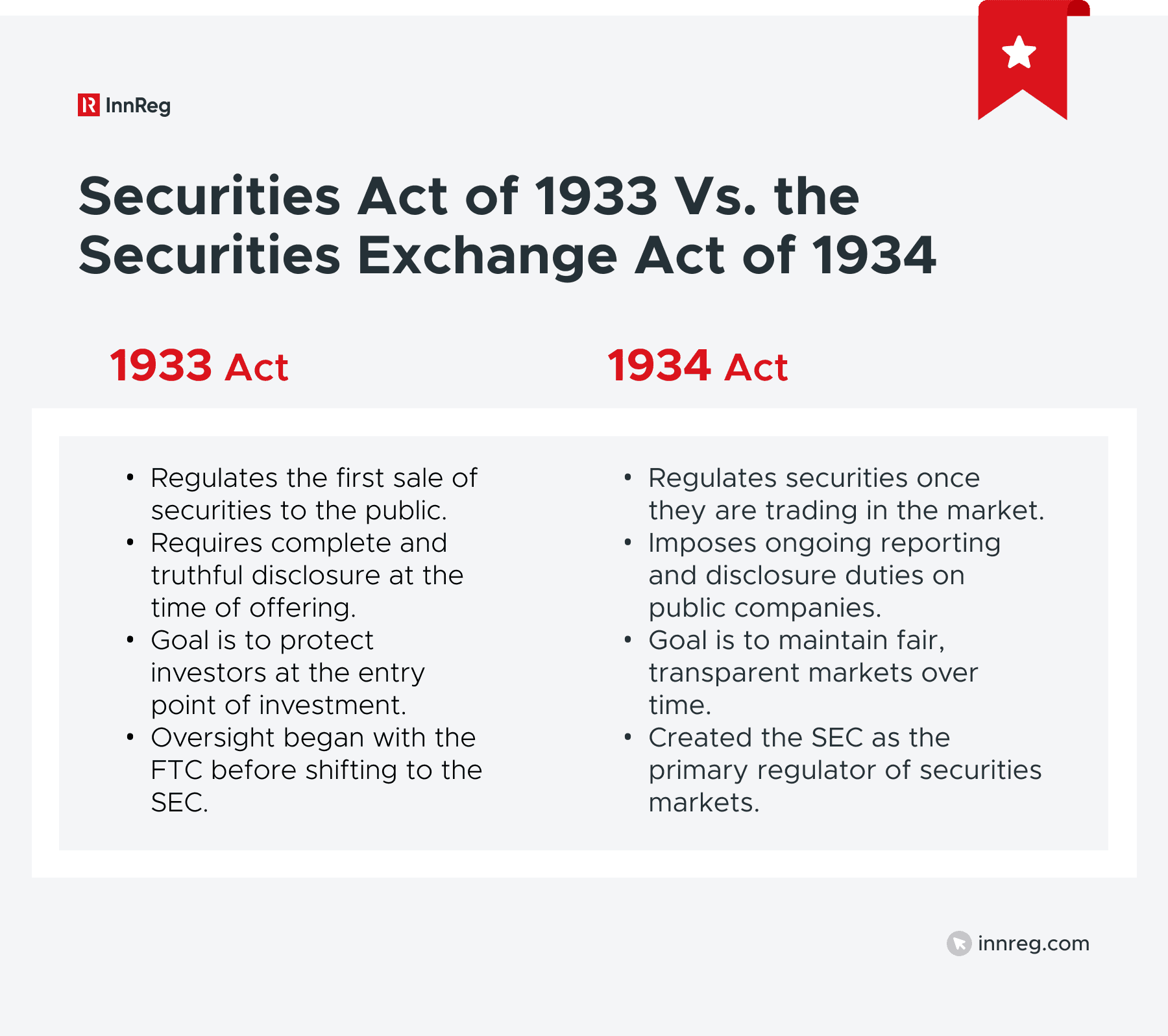

Securities Act of 1933 vs. the Securities Exchange Act of 1934

The Securities Act of 1933 and the Securities Exchange Act of 1934 are often mentioned together, but they serve very different roles. Think of them as two parts of the same system.

The 1933 Act focuses on the first step: when a company offers securities to the public. It requires full and truthful information at the time of the sale so investors can make informed decisions before buying.

The 1934 Act picks up from there. Once those securities are in the market, it regulates the ongoing trading, the responsibilities of exchanges and broker-dealers, and the continuous disclosure obligations of public companies.

Together, the two laws form the foundation of modern US securities regulation. The 1933 Act protects investors at the entry point, while the 1934 Act provides oversight for everything that happens after.

Key Provisions of The Securities Exchange Act Of 1934

The Securities Exchange Act of 1934 covers everything from how companies share information with investors to the way brokers, dealers, and exchanges do business. Here are the key provisions and why they still matter for financial markets and compliance programs.

Provision | What It Covers | Why It Matters |

|---|---|---|

Ongoing Reporting and Disclosure | Public companies must file annual, quarterly, and current reports | Keeps investors informed with timely and reliable information |

Anti-Fraud and Insider Trading | Prohibits false statements, omissions, and trading on nonpublic information | Promotes fair markets and holds individuals accountable |

Regulation of Brokers, Dealers, and Exchanges | Sets registration, supervision, and conduct rules for intermediaries | Establishes standards for how trading platforms and professionals operate |

Proxy Rules and Shareholder Communications | Requires clear proxy statements for shareholder votes | Gives investors transparency on major corporate decisions |

Insider Reporting and Short-Swing Profit Rules | Requires insiders to report trades and return short-term profits | Discourages unfair advantages and builds accountability |

Margin and Market Manipulation | Limits leverage and bans manipulative trading practices | Mitigates systemic risk and protects market integrity |

1. Ongoing Reporting and Disclosure Requirements

One of the core ideas behind the Securities Exchange Act of 1934 is that investors should not be left in the dark once a company goes public. To address this, the Act requires public companies to share updated information regularly, not just at the time of an offering.

These reporting requirements come in several forms:

Annual reports (Form 10-K): A detailed look at a company’s financial performance, business operations, and risks.

Quarterly reports (Form 10-Q): Updates throughout the year that keep investors informed about earnings and developments.

Current reports (Form 8-K): Filed when something material happens, such as a merger, leadership change, or regulatory action.

This framework creates a steady flow of information into the market. This then helps investors evaluate companies on facts rather than rumors and provides regulators with the data they need to monitor activity.

For fintech firms, these rules highlight the responsibilities that come with growth. Even companies that are not yet public may be impacted if they work with partners or investors who rely on Exchange Act disclosures. Staying familiar with the reporting system can make it easier to anticipate future obligations and avoid compliance gaps down the road.

2. Anti-Fraud and Insider Trading Rules

The Securities Exchange Act of 1934 is best known for its stance against fraud and unfair trading practices. At its core, the Act makes it illegal to mislead investors, distort market prices, or take advantage of inside information that the public does not have.

Key elements include:

Rule 10b-5: This is a broad anti-fraud provision that prohibits making false statements, omitting key facts, or engaging in deceptive practices tied to the purchase or sale of securities.

Insider trading restrictions: Executives, employees, and others with access to confidential information cannot use it for personal gain or tip off others to trade ahead of the market.

These rules matter because they help create fair markets where prices reflect real information instead of hidden advantages. They also hold people accountable, not just companies.

For fintech businesses, this is especially relevant. Many firms handle sensitive data, operate innovative trading platforms, or launch fast-moving products that raise questions about access to nonpublic information. Putting compliance processes in place early helps mitigate risk and shows regulators that the firm is serious about protecting market integrity.

3. Regulation of Brokers, Dealers, and Exchanges

Another key part of this Act is its regulation of the people and platforms that make trading possible. Brokers, dealers, and exchanges all have to follow specific rules that protect investors and keep markets fair.

For instance, the act requires broker-dealers to register with the SEC and join a self-regulatory organization such as FINRA. Once registered, their sales practices, financial condition, and overall conduct are closely monitored. Exchanges are also subject to oversight, with rules designed to promote fair access and prevent manipulative trading.

These responsibilities go beyond registration. Broker-dealers are expected to keep good records, stay financially healthy, and have systems that keep an eye on how employees are doing their jobs. Exchanges also play their part by posting clear trading rules and watching for any suspicious activity in the market.

This is especially important for fintechs building trading platforms or acting as intermediaries. Even innovative models in digital assets or alternative securities can face the same obligations as traditional firms. Knowing how the Exchange Act treats these roles helps leaders shape their business models and prepare for the compliance responsibilities that come with growth.

4. Proxy Rules and Shareholder Communications

The Securities Exchange Act of 1934 also governs how companies communicate with their shareholders, especially when votes are involved. These rules are known as proxy regulations, and they apply whenever shareholders are asked to make decisions about issues such as electing directors or approving major transactions.

Companies must provide clear and complete information in proxy statements so that investors can make informed choices. These statements typically include details on executive compensation, board structure, and significant corporate actions. The goal is to give shareholders a fair view of what they are voting on and how it might affect their investment.

For fintech founders thinking about going public, it helps to understand proxy obligations early. These rules show that engaging with shareholders is not only about raising capital but also about building trust and maintaining transparency once investors are part of the company’s future.

5. Insider Reporting and Short-Swing Profit Rules

The Securities Exchange Act of 1934 sets special requirements for insiders of public companies, such as officers, directors, and large shareholders. These individuals are in positions of trust and often have access to sensitive information that the public does not.

To promote transparency, insiders must file reports with the SEC when they buy or sell company stock. This makes their trading activity visible to investors and regulators. The Act also includes the “short-swing profit rule,” which requires insiders to return any profits made from buying and selling their company’s stock within a six-month period.

These rules are meant to prevent insiders from making quick, unfair gains and to give investors confidence that company leaders are acting responsibly. For growing fintechs, it’s a reminder that leadership roles come with regulatory duties as well as management ones.

6. Margin and Market Manipulation Provisions

This Act also sets rules to limit risky trading practices. Two areas stand out: margin requirements and restrictions on market manipulation.

Margin rules control how much money an investor can borrow from a broker to buy securities. By placing limits on borrowing, the Act reduces the chance of excessive leverage that could destabilize markets during downturns.

Market manipulation provisions, on the other hand, make it unlawful to create false or misleading appearances of trading activity. Practices like spreading false information, artificially inflating prices, or coordinating trades to distort supply and demand fall under this category.

These measures protect investors and help keep markets grounded in real value rather than artificial signals. For fintech firms, especially those building trading platforms or products that rely on leverage, understanding these rules is essential to building models that regulators will accept and investors will trust.

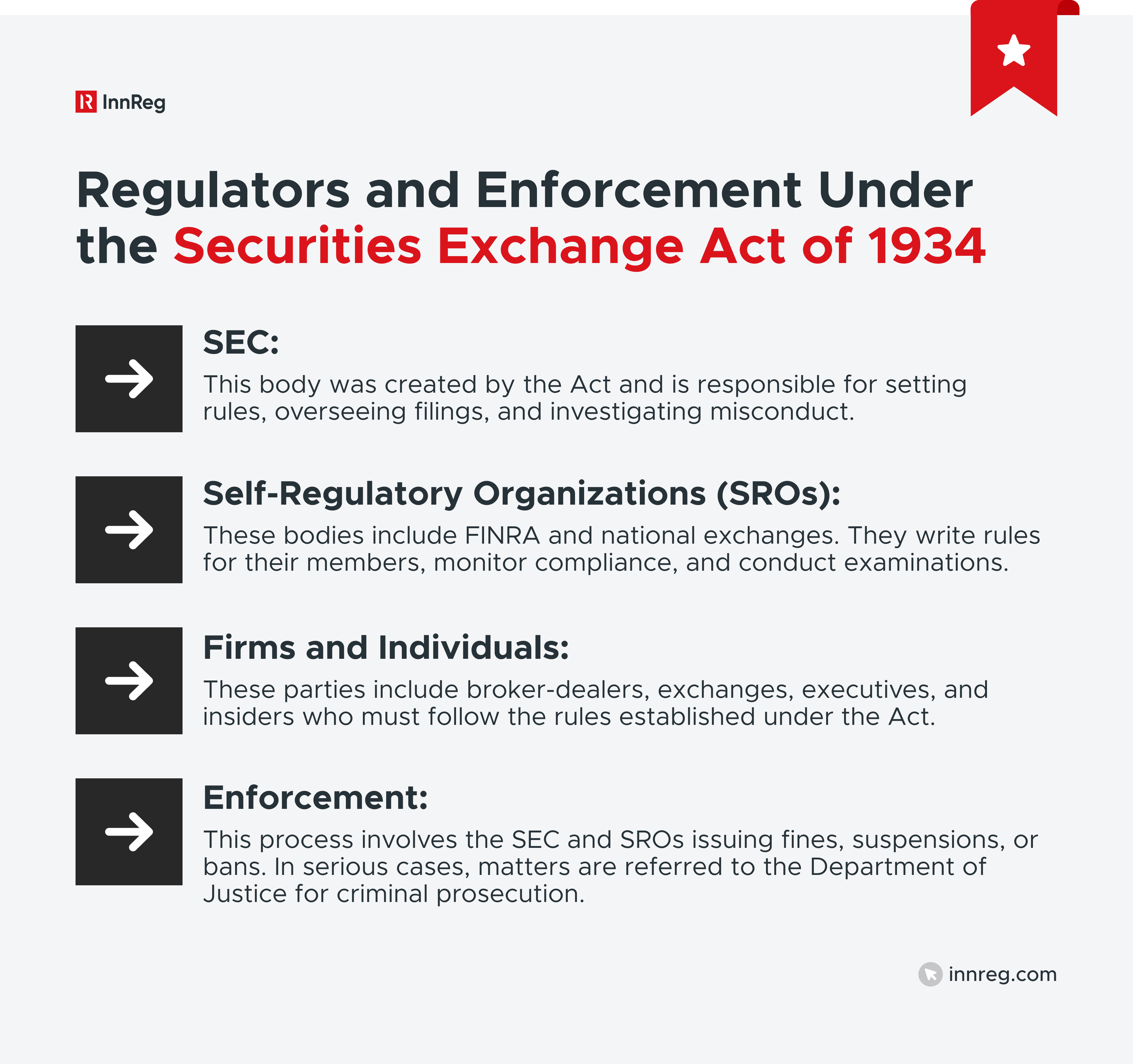

Regulators and Enforcement Under the Securities Exchange Act of 1934

The Securities Exchange Act of 1934 didn't just create rules. It built a system to make those rules stick. The SEC takes the lead, and self-regulatory organizations like FINRA handle day-to-day supervision of their members, while the exchanges police trading on their own platforms. Together, they form multiple layers of oversight, watching for violations and taking action when firms or individuals cross the line.

The Role of The SEC

The Securities Exchange Act of 1934 gave life to the SEC. This was the first time the US had a dedicated agency with the power to write rules, monitor markets, and bring enforcement actions when needed.

The SEC’s responsibilities cover a wide range. It reviews company filings, oversees broker-dealers and exchanges, and investigates misconduct such as insider trading or fraud. It also updates regulations to keep pace with changes in the market.

For fintech firms, the SEC often feels like the most visible regulator. Whether a business is thinking about registering as a broker-dealer, exploring digital asset offerings, or preparing for public reporting, the SEC’s rules and guidance shape what is possible.

See also:

The Role of Self-Regulatory Organizations

Alongside the SEC, SROs play an essential role in enforcing this Act. The most familiar example is FINRA, which oversees broker-dealers, but national securities exchanges also act as SROs.

These organizations write rules for their members, monitor compliance, and conduct examinations to check that firms are meeting standards. They often serve as the first line of oversight, handling day-to-day supervision while the SEC focuses on broader enforcement and policy.

For fintech firms, SROs may feel closer to the ground than federal regulators. Membership means adapting to detailed rulebooks, reporting systems, and regular exams. While this adds to operational demands, it also creates a structured framework for building credibility with investors and regulators alike.

Need help with broker-dealer compliance?

Fill out the form below and our experts will get back to you.

Enforcement Actions and Penalties

When firms or individuals break the rules under the Act, regulators can respond with enforcement actions. These can range from fines and trading suspensions to bans on serving in leadership roles. In serious cases, violations may even lead to bars from the industry and criminal charges.

The SEC often works alongside SROs and, when necessary, with the Department of Justice. This layered approach means misconduct can be addressed on multiple fronts, from administrative penalties to courtroom proceedings.

For fintech founders and compliance officers, the takeaway is simple. Enforcement is not limited to large public companies. Startups and emerging firms that touch securities markets are also on the radar. Staying proactive with compliance, therefore, helps mitigate the risk of costly disputes and reputational damage.

Why the Securities Exchange Act of 1934 Matters for Fintechs

The Securities Exchange Act of 1934 may have been written nearly a century ago, but its reach is still felt in fintech today. For founders, lawyers, and compliance officers, the Act influences how companies grow, manage risk, and maintain credibility in the market.

Here are some of the main reasons it matters:

Wide coverage: The Act does not just apply to public companies. It also governs brokers, dealers, and exchanges. Fintech firms that provide custody, order execution, or trading platforms may be subject to its rules even if they do not plan to go public.

Regulatory authority: The SEC uses the Act as the basis for enforcement. This means investigations into fraud, insider trading, or misleading disclosures often start here. Fintech firms offering new products or trading systems are often watched closely to verify that investor protections are not compromised.

Ongoing disclosure: Public companies must share regular financial updates through reports like 10-Ks and 10-Qs. For fintech firms considering going public or partnering with listed companies, understanding these obligations is critical to planning ahead.

Insider accountability: The Act imposes strict rules on corporate insiders, requiring them to disclose trades and avoid quick profits. This highlights the personal responsibility that executives and directors carry in a regulated market.

Market conduct standards: Anti-manipulation provisions and margin requirements limit risky behavior that can distort prices and create undue leverage. Fintech platforms offering leverage, algorithmic tools, or innovative trading products need to be mindful of how these rules apply.

Investor trust: A key principle of the Act is fair and equal access to information. Clear disclosures and transparent practices are not just legal requirements but also business advantages when competing for investors and partners.

Operational impact: Recordkeeping, reporting, and registration requirements under the Act directly influence how fintechs set up compliance programs, hire specialized staff, and select technology vendors to support regulatory processes.

Compliance Challenges for Founders and Compliance Teams

This Act creates responsibilities that reach into many parts of a business. For fintech founders and compliance officers, this can complicate growth in unexpected ways. Here are some of the common areas where challenges arise and why they matter for fintech companies.

1. When Private Companies Trigger Exchange Act Reporting

The Securities Exchange Act of 1934 is often thought of as applying only to public companies. In reality, certain private companies can also fall under its reporting requirements if they reach specific thresholds.

A private company may be required to file reports with the SEC if it has more than 2,000 total shareholders, or 500 shareholders who are non-accredited investors, and more than $10 million in assets. At that point, the company is treated much like a public company when it comes to disclosure.

For fintechs, these requirements can come up sooner than expected. Rapid fundraising, a growing investor base, or employee stock programs can all push a company past its limits. Once that happens, ongoing reporting obligations kick in, bringing higher costs, tighter controls, and closer regulatory oversight.

Founders and compliance teams who keep an eye on shareholder numbers and asset levels can prepare before crossing that threshold. With early awareness, companies can make an informed choice: stay private with tighter limits on investors, or take on reporting obligations as part of a longer-term growth strategy.

2. Insider Trading Risks and Misconceptions

Insider trading is one of the most well-known risks under the Securities Exchange Act of 1934, but it is also one of the most misunderstood. Many founders and executives assume it only applies to senior officers making obvious trades. In reality, the rules cover a much wider range of situations.

Insider trading occurs when someone with material, nonpublic information about a company buys or sells securities before that information is made public. This can include executives, employees, contractors, or even friends and family who receive tips. Violations can lead to SEC enforcement, heavy fines, and reputational damage.

Common misconceptions include:

Only executives can be liable: Anyone with access to inside information can face liability, including employees at all levels.

Intent always matters: Even accidental or poorly timed trades can raise red flags if they create the appearance of unfair advantage.

Private companies are exempt: If securities are being traded, the rules may apply regardless of whether the company is public.

The risks can be even higher for fintechs that handle sensitive financial data, get early access to transaction flows, or build innovative trading tools. Strong training programs and clear monitoring systems around insider trading help lower that risk and give teams confidence about what is and is not allowed.

3. Ongoing Reporting and Disclosure Pitfalls

Meeting the reporting requirements under this Act is not just about filing documents on time. The real challenge lies in the details of what is reported and how consistent the information is across different filings.

Some of the most common pitfalls include:

Incomplete disclosures: Leaving out material information, even unintentionally, can create liability. Investors and regulators expect a complete picture, not selective highlights.

Inconsistent reporting: Numbers or narratives that differ across annual, quarterly, or current reports raise questions about accuracy. Consistency is often as important as timeliness.

Weak internal controls: Without strong systems for collecting and verifying data, filings can contain errors that undermine credibility.

Failure to update investors: Significant events, such as leadership changes or pending deals, must be disclosed quickly. Delays can result in penalties or enforcement actions.

Disclosure can be especially challenging for fintech companies. Innovative products, new revenue models, and rapid growth often do not fit neatly into traditional reporting categories. Compliance teams, therefore, have to bridge that gap, turning complex business realities into filings that meet regulatory standards while still giving investors a clear and honest picture.

4. Individual Liability for Executives and Directors

The Securities Exchange Act of 1934 places responsibility not only on companies but also on the individuals who lead them.

Executives and directors can face personal liability if they approve disclosures that turn out to be false or misleading, even if the errors were unintentional. They are also closely watched when it comes to trading their own company’s stock, since they often have access to information that the public does not.

Liability can also extend to how leaders supervise their organizations. Directors and senior officers are expected to take an active role in overseeing compliance systems. Failing to act when problems are visible, or neglecting oversight altogether can expose individuals to penalties.

On top of that, the Act imposes specific restrictions such as the short-swing profit rule, which requires insiders to return profits made from buying and selling stock within a six-month period.

For fintech executives, this means that compliance is not only a company-wide responsibility but also a personal one. Leaders who stay engaged in oversight and governance mitigate their risk of being held accountable for violations and set a stronger tone for the rest of the organization.

5. Keeping Pace With Rule Changes

This Act has been in place for nearly a century, but it is far from static. The SEC regularly updates its rules and interpretations to reflect changes in markets, technology, and investor behavior. For companies, this means compliance is not a one-time project but an ongoing process that requires constant attention.

Recent updates have focused on areas like insider trading plans, share repurchase disclosures, and beneficial ownership reporting. Each change adds new layers of responsibility for firms and individuals, often requiring adjustments to policies, recordkeeping, and training. For fintech businesses, these shifts can be especially challenging because many operate with innovative models that don't fit neatly into traditional regulatory frameworks. This also leaves regulators trying to figure out how decades-old rules apply to new technology.

Compliance teams need to look at how new rules apply to their business, adjust workflows, and share expectations across departments.

Recent Updates and Enforcement Trends

The Securities Exchange Act of 1934 has grown and adapted as markets and technology have changed. In recent years, the SEC has rolled out new rules and stepped up enforcement in ways that affect both traditional firms and fintech companies.

Here are some of the key updates shaping compliance today.

Beneficial Ownership Reporting Rule Changes

One of the biggest recent changes to the Securities Exchange Act of 1934 is the update to beneficial ownership reporting rules. These rules set the timeline for how quickly investors with significant stakes in public companies need to disclose their holdings.

In the past, investors who crossed the 5% ownership mark had 10 days to file a Schedule 13D. Now the SEC has shortened that window, giving investors up to five business days. The shift reflects today’s fast-moving markets, where trades happen quickly and large positions can be built before others even realize it.

These changes matter for companies bringing in institutional investors or thinking about going public. Faster reporting gives the market a clearer view of ownership shifts, reducing the chance of surprise moves that could affect price or control. For compliance teams, it means keeping close ties with investors and paying closer attention to ownership levels.

New Share Repurchase Disclosure Requirements

In 2023, the SEC adopted new rules to modernize share repurchase disclosures, aiming to increase transparency for investors regarding when and why companies repurchase their own stock. These rules would have required issuers to provide more frequent and detailed information, including daily reporting of repurchases, explanations for the buybacks, and disclosure of any insider trading policies related to the programs.

However, in December 2023, the US Court of Appeals for the Fifth Circuit vacated this rule change, citing deficiencies in the SEC’s cost-benefit analysis. As a result, the previous disclosure requirements remain in effect for now.

For compliance teams, this development highlights the importance of staying alert to regulatory reversals and litigation outcomes. While enhanced transparency remains a long-term trend in securities regulation, companies should continue following the existing reporting framework until the SEC issues further guidance.

See also:

Insider Trading Enforcement and 10b5-1 Plan Reforms

The SEC has recently tightened its focus on insider trading, especially around the use of Rule 10b5-1 trading plans. These plans were initially designed to let insiders sell stock on a pre-set schedule, reducing concerns that trades were based on material nonpublic information.

Over time, regulators saw that some insiders were using these plans in ways that raised red flags. For example, starting or canceling a plan right before a major announcement could make it look like the system was being misused. To respond, the SEC introduced reforms that bring new disclosure requirements, mandatory cooling-off periods before trades can begin, and limits on overlapping plans.

For fintech leaders, there are two clear takeaways. First, insider trading enforcement is still one of the SEC’s top priorities, so strong internal policies and education are key. Second, even long-standing practices like 10b5-1 plans are not set in stone. Compliance teams need to revisit policies and adjust as rules evolve.

SEC Focus on Whistleblower Protections and Recordkeeping

The SEC has made it clear that whistleblower protections and strong recordkeeping are central to its enforcement priorities. Under the Securities Exchange Act of 1934, companies must keep accurate books and records, and employees must be able to raise concerns without fear of retaliation.

Recent enforcement cases show just how seriously the SEC takes these rules. Firms have been penalized for failing to keep proper records of business conversations, including those on personal devices or messaging apps. Regulators have also acted when confidentiality agreements or workplace practices made employees feel discouraged from speaking up.

The takeaway for fintechs is twofold. On the recordkeeping side, systems and controls need to capture all relevant business communications, even as teams adopt new tools and platforms. On the whistleblower side, compliance officers should work with leadership to foster a culture where employees feel safe raising issues. Both are critical for building credibility with regulators and investors.

Application to Fintech and Crypto Platforms

The SEC has taken the position that many digital assets fall under the Act, though this remains an evolving area with active court challenges. Trading apps, token exchanges, and digital platforms that function like broker-dealers or exchanges often fall under its rules, even if they present themselves as technology providers.

Recent enforcement actions drive this point home. The SEC has pursued crypto platforms for trading what it considers securities and gone after fintechs operating as unregistered dealers. The focus is not on the label a firm uses but on the activity itself. If a business looks and acts like a securities firm, regulators will treat it as one.

For compliance teams, this creates both challenges and opportunities. The challenge is that rules written in 1934 now apply to products that only emerged in recent years. The opportunity is that firms that adapt quickly can build stronger reputations with regulators, investors, and customers.

FAQs on the Securities Exchange Act of 1934

1. Which types of securities fall under the Exchange Act?

The Act covers a broad range of securities, including stocks, bonds, debentures, options, and other instruments that represent ownership or debt. It also applies to many derivatives and complex products that trade in secondary markets. In practice, if an instrument looks and functions like a security, it is likely subject to the Act.

2. Does the Securities Exchange Act of 1934 apply to private companies?

Generally, private companies are not subject to the Act’s full reporting requirements. However, once a private company exceeds certain thresholds, such as having more than 2,000 total shareholders or 500 non-accredited investors along with more than $10 million in assets, it must begin filing reports with the SEC. This is why some private firms unexpectedly find themselves subject to the Act.

3. What is the difference between civil and criminal liability under the act?

Civil liability usually involves enforcement actions by the SEC or self-regulatory organizations, leading to fines, suspensions, or other penalties. Criminal liability, on the other hand, can involve the Department of Justice and may lead to prosecution, larger fines, or imprisonment. The difference often comes down to the severity of the misconduct and the intent behind it.

4. How does the Exchange Act apply to foreign companies listed in the US?

Foreign companies that list securities on US exchanges must comply with many of the same disclosure and reporting requirements as domestic companies. Some accommodations exist, such as the use of Form 20-F instead of Form 10-K, but the overall goal is the same: to provide investors with transparent and comparable information.

5. Does the Securities Exchange Act of 1934 affect fintech and crypto platforms?

Yes. The SEC has made it clear that fintech and crypto platforms are not outside the scope of the Act. If a business is operating in a way that resembles a broker, dealer, or exchange, regulators may apply Exchange Act requirements. This has been the basis for several enforcement actions against trading apps, token marketplaces, and digital platforms.

—

The Securities Exchange Act of 1934 still sets the tone for how markets function and how businesses grow. For fintech founders, lawyers, and compliance officers, the takeaway is simple: knowing the Act is not just about meeting requirements, it’s about building stronger, more resilient companies.

With its reach into reporting, insider activity, market conduct, and firm responsibilities, this Act continues to evolve. Recent updates also make clear that regulators will keep adapting it to fit modern realities, from digital assets to new trading technologies.

Francesco is the Founder & CEO of InnReg with over 15 years of experience in fintech compliance and operations. He previously served as CCO at TradeKing and Zecco, helping grow the firm into the 6th largest US online broker before its $275M acquisition by Ally Bank. He holds FINRA Series 4, 7, 24, 53, and 63 licenses and an MPA from Harvard Kennedy School.

How Can InnReg Help?

InnReg is a global regulatory compliance and operations consulting team serving financial services companies since 2013.

We are especially effective at launching and scaling fintechs with innovative compliance strategies and delivering cost-effective managed services, assisted by proprietary regtech solutions.

If you need help with broker-dealer compliance, reach out to our regulatory experts today:

Related Articles

Featured LinkedIn Posts