Why Blue Sky Laws Matter for Modern Fintech

Blue sky laws are a state-level regulatory layer that many fintechs do not fully anticipate. While most teams focus on federal compliance with SEC regulations, every state in the US enforces its own securities laws to protect local investors.

These laws can trigger registration, licensing, and disclosure obligations for both capital-raising and product-launch activities, even when federal exemptions apply.

This article breaks down how blue sky laws work, where they fit in the broader regulatory framework, and what they mean for fast-moving fintech companies.

At InnReg, we help fintechs navigate blue sky law compliance and multi-state regulatory requirements: from fundraising notice filings to product launch strategy. If you’re raising capital or expanding across state lines, our team can support your licensing, filings, and compliance program buildout.

What Are Blue Sky Laws?

Blue sky laws are state-level securities regulations designed to protect investors from fraud and unfair practices. Every US state and territory enforces its own version, separate from, but often overlapping with, federal securities laws.

These laws typically require companies to register securities offerings, license sales personnel, and provide full disclosure to investors within the state.

Whether a firm is raising a seed round or offering a new investment product, blue sky obligations can apply based on where its investors or users live (not where your company is based).

The term originated in the early 1900s, when judges referred to speculative investments as having "no more substance than so many feet of blue sky." That principle still applies: if a company is offering securities, states want to know what’s being sold and how.

Why Blue Sky Laws Still Matter in Modern Fintech

Even in an environment dominated by federal exemptions and digital fundraising, state-level oversight remains active and enforceable. Blue sky laws have not faded into the background. They continue to play a central role, especially when investment activity crosses state lines.

Most fintech companies do not operate within a single jurisdiction. Whether offering securities to accredited investors, enabling users to invest through an app, or structuring alternative assets like tokenized notes, state regulators may have a say in how the offering is conducted and disclosed.

Many times, these laws are enforced not just through filings but also through investigations and cease-and-desist orders. Fintech platforms working with securities, whether directly or through partners, must keep state rules on their radar from day one.

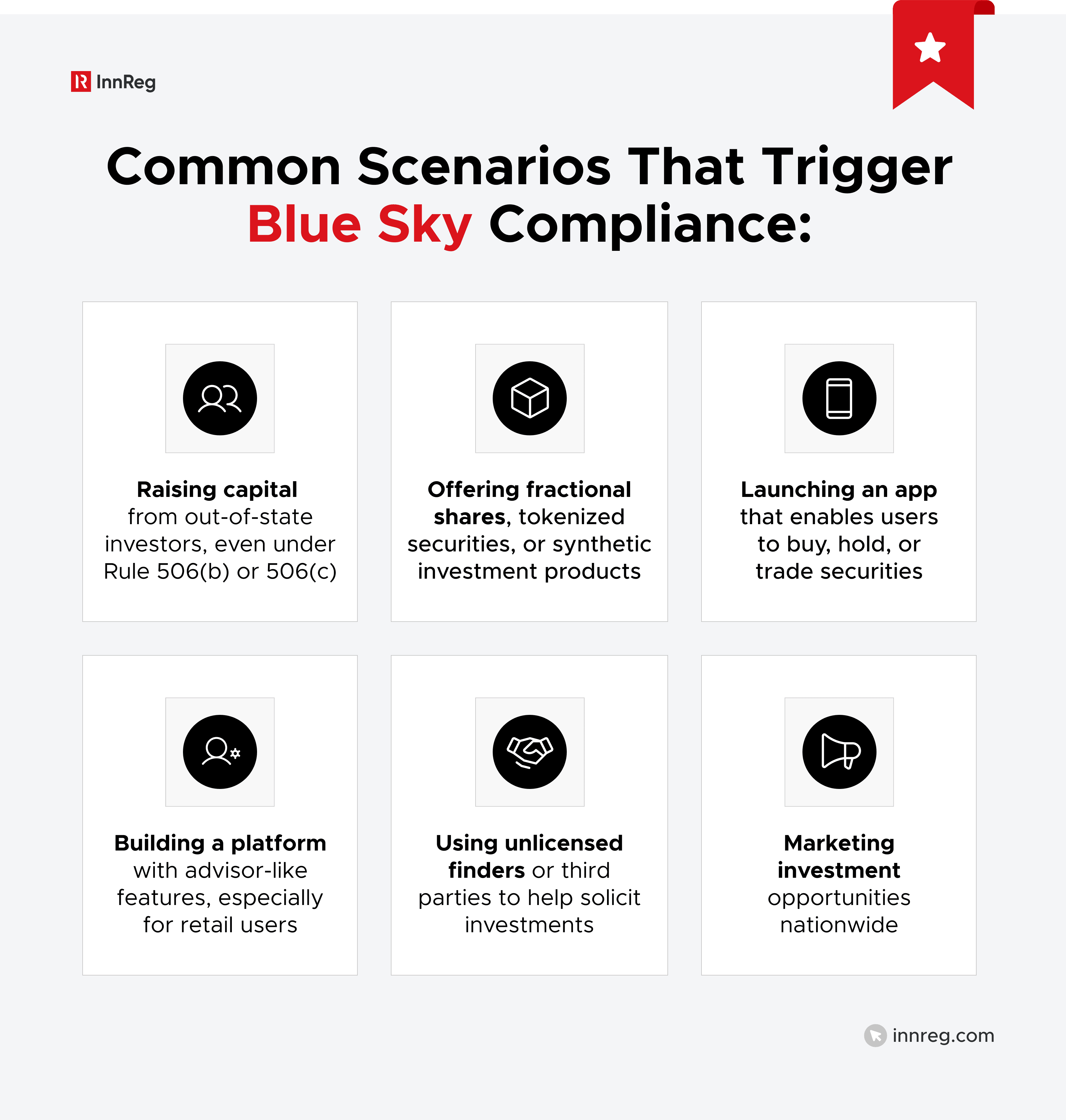

Common Triggers for Blue Sky Compliance in Fintech

Some teams encounter blue sky laws during a funding round. Others run into them while launching a new product or expanding into new states. In either case, the trigger is usually an activity that involves offering or selling securities across state lines.

If any part of the offering qualifies as a securities transaction, it likely touches blue sky law in every state where investors or users are located. This applies even if the product is novel, the company is early stage, or the investors are accredited.

Who Regulates Blue Sky Laws?

Blue sky laws are enforced at the state level, not by a single federal agency. Every state has its own regulator with the authority to review securities filings, investigate fraud, and penalize violations.

Unlike federal oversight, which runs through the SEC, state enforcement is local and often more targeted. The rules vary, the review standards differ, and the filing processes are not uniform. For fintech companies operating across multiple states, this complexity is easy to underestimate.

In many cases, state regulators are also watching for unlicensed selling activity or compliance gaps. If an investor or user resides in their state, they have jurisdiction, regardless of where the company is based.

The following state agencies frequently appear in filings, reviews, or enforcement actions involving fintech companies:

California Department of Financial Protection and Innovation (DFPI): Oversees securities regulation under the Corporate Securities Law. Known for proactive fintech supervision and broad enforcement powers.

New York Attorney General’s Office (Martin Act): Operates under one of the strongest anti-fraud statutes in the country. Frequently investigates unregistered offerings and digital asset activity.

Texas State Securities Board: Active in multi-state enforcement actions and crypto-related investigations. Requires filings and licensing for many securities transactions.

Florida Office of Financial Regulation: This regulator is involved in reviewing offerings and overseeing registration for firms and individuals selling securities.

Illinois Securities Department: Handles registration, licensing, and regulatory exams. Often follows NASAA guidance closely but enforces its own thresholds.

Even if a company does not physically operate in these states, offering security to a resident may trigger jurisdiction. State-level enforcement is based on where the investor or user is located, not where the firm is headquartered.

Role of NASAA in Coordinating State Regulation

While each state enforces its own blue sky laws, there’s an organization that helps bring some consistency: the North American Securities Administrators Association (NASAA). This group includes securities regulators from all 50 states, as well as Washington, DC, Puerto Rico, Canada, and Mexico.

NASAA helps create tools that states can use to shape their own regulations. That includes things like licensing exams (such as the Series 63) and sample legislation like the Uniform Securities Act. While states are not required to follow these models, many choose to build on them or use them as a starting point.

For fintech companies, NASAA is not a regulator in itself, but its policy direction often signals how state enforcement may evolve, especially around digital assets, crowdfunding, and alternative investment products. When multiple states act in coordination (as seen in crypto investigations), NASAA is often in the background organizing the effort.

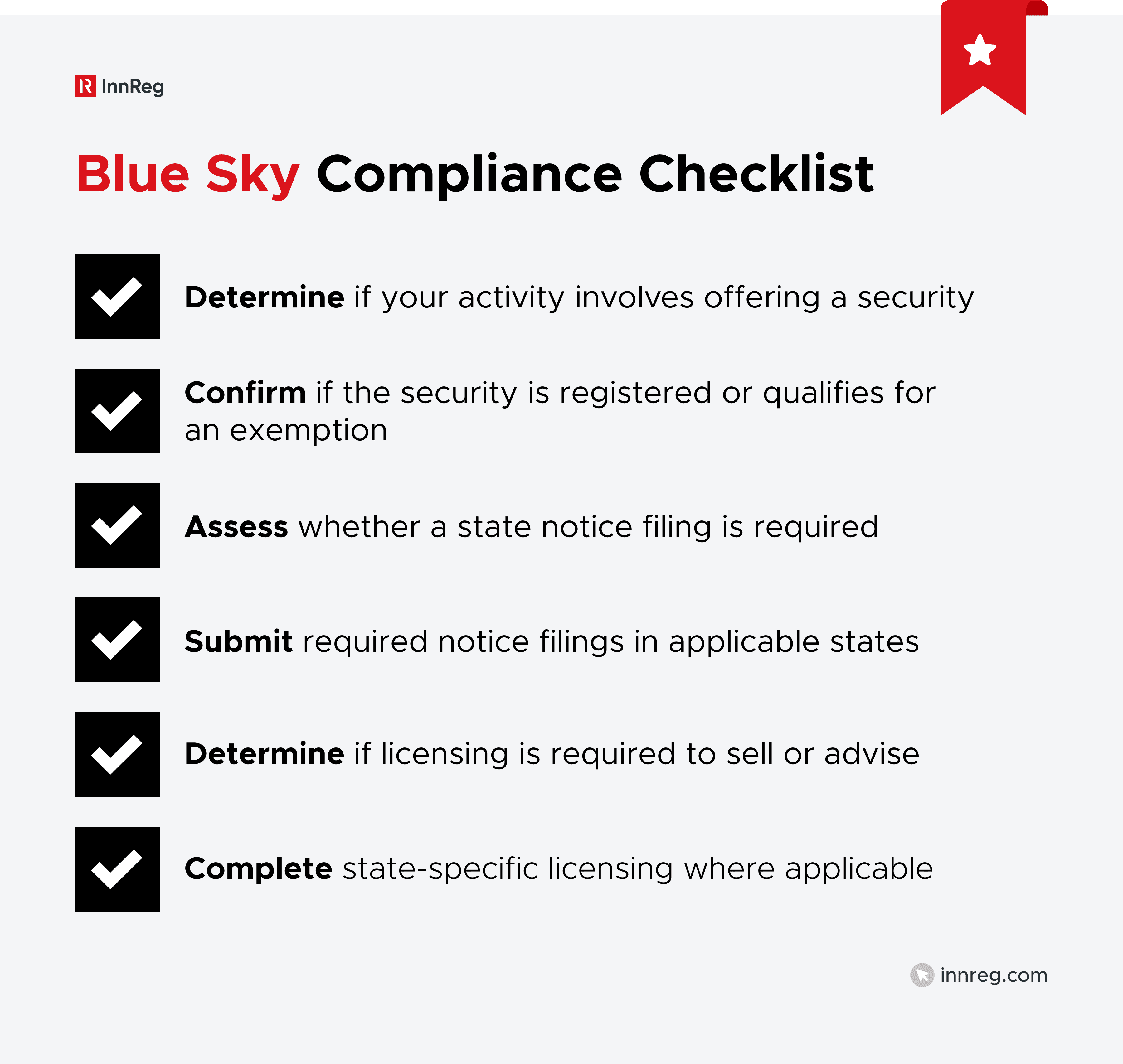

Key Compliance Obligations Under Blue Sky Laws

Blue sky laws generally fall into three categories: registration of securities, licensing of individuals or firms, and anti-fraud compliance. The specific requirements vary by state, but these are the core areas most fintech teams need to address.

Registration of Securities

In most states, companies offering securities must either register those offerings or qualify for an exemption. This requirement applies based on where investors are located, not where the company is formed or operates.

States may ask for offering documents, disclosures, consent to service, and filing fees. In some cases, regulators scrutinize the deal itself, not just what is disclosed, but whether the terms are considered reasonable for investors.

Even when a company relies on a federal exemption like Regulation D, most states still require notice filings. Failing to complete these filings on time can cause penalties or, sometimes, a right of rescission for investors.

See also:

Licensing of Brokers, Agents, and Advisors

In most states, anyone selling securities or providing investment advice must be licensed where the investor lives. That includes broker-dealers, advisors, and the individuals working under them.

Licensing typically involves state registration, disclosure filings, and passing relevant exams, most commonly the Series 63. In states that don’t recognize certain federal exemptions or rely heavily on local oversight, the licensing burden can increase quickly.

Unlicensed activity is a common enforcement trigger. Someone who solicits investment without proper registration, even informally or as a contractor, can create legal exposure for the company and halt fundraising efforts.

Need help with broker-dealer compliance?

Fill out the form below and our experts will get back to you.

Anti-Fraud Provisions and Disclosure Requirements

All states include anti-fraud provisions in their blue sky laws. These rules target false claims, material omissions, and other deceptive practices that could mislead investors.

Even if a company qualifies for an exemption from registration or licensing, anti-fraud obligations still apply. Marketing materials, pitch decks, offering memos, and investor communications must reflect the actual risks, structure, and status of the business or product being offered.

Some states, like New York, can initiate an enforcement case without proving intent to mislead. That makes accurate, measured communication a core part of any compliance strategy, especially for fintech teams launching innovative or hybrid investment models.

How Federal Laws Interact with Blue Sky Laws

While federal securities laws pre-empt some state requirements, blue sky laws still apply in many key areas. For most fintech companies, compliance involves navigating both federal and state regulatory systems simultaneously.

“Covered Securities” and NSMIA Preemption

In 1996, Congress passed the National Securities Markets Improvement Act (NSMIA) to reduce regulatory overlap between federal and state law. The law created a category of “covered securities” that are exempt from state-level registration requirements.

Covered securities include:

Securities listed on national exchanges (like NYSE or Nasdaq)

Offerings made under Rule 506(b) or 506(c) of Regulation D

Certain offerings under Regulation A (Tier 2 only)

Securities sold to qualified purchasers

If an offering falls into one of these categories, states cannot require full registration. However, they can still require notice filings and fees, especially for Regulation D offerings. Many founders miss this distinction, assuming that “pre-emption” means no state involvement at all.

In practice, NSMIA simplifies multi-state fundraising but does not remove the need to interact with state regulators. Timing and documentation still matter.

Notice Filings: Still Required in Most States

Even when a company qualifies for a federal exemption, most states still require a notice filing. This typically involves submitting a copy of the federal Form D, paying a filing fee, and completing a short state-specific form.

Typically, the notice must be filed within 15 days of the first sale to an investor in that state. Some states require it even earlier. Others impose penalties for late filings or failure to submit altogether.

This is one of the most common compliance oversights in startup fundraising. Skipping a state notice can lead to fines or investor rescission rights, even if the broader exemption under Regulation D is valid.

Fintech companies raising funds from investors across multiple states often manage this process using a compliance calendar or an outsourced partner.

Crypto, Digital Assets, and Blue Sky Enforcement

Many states have taken the position that certain digital assets qualify as securities, even when marketed as utility tokens or nontraditional financial instruments. That brings them within the scope of blue sky laws.

State regulators have not waited for federal agencies to act. Some have already taken enforcement steps against token projects and crypto lenders, pointing to unregistered offerings or questionable marketing practices, even in areas where federal rules are still evolving.

For fintech teams working with digital assets, the state-level risk is real. If a product resembles an investment or carries return expectations, states may treat it as a security and demand compliance.

State-by-State Variability

Navigating blue sky laws means dealing with a different rulebook in every state. Some states define securities more broadly. Others have unique filing systems, fee schedules, or review timelines that don’t match federal processes or each other.

In a few states, regulators go beyond reviewing disclosures and look at whether the offering itself is fair. Others take a lighter touch, focusing more on whether the information provided is accurate and not misleading.

For fintech teams working across state lines, this lack of consistency adds operational complexity. What works in one jurisdiction might raise questions or trigger a review in another. Staying ahead of those differences is critical to keeping growth on track.

See also:

Blue Sky Notice Filing Requirements by State

Because filing obligations vary so widely, it’s useful to compare how a few key states handle notice requirements for Rule 506 offerings:

State | Notice Filing Required? | Form | Filing Deadline | Estimated Fee |

|---|---|---|---|---|

California | Yes | Form D + State Form | Within 15 days of sale | $300 |

New York | Yes (special process) | Form D + State Form | Within 15 days of sale | $1,200 |

Texas | Yes | Form D | Within 15 days of sale | $250 |

Florida | Yes | Form D | Within 15 days of sale | $250 |

Illinois | Yes | Form D + U-2 Form | Within 15 days of sale | $300 |

Note that this is only a snapshot. Many other states have similar, but slightly different, rules. Some accept electronic filings through NASAA’s EFD system, while others require direct mail or separate portals.

For fintech companies fundraising nationally, tracking each state’s filing requirements, fees, and deadlines is not optional. Teams often manage this with internal tracking systems or outsource the work to a compliance partner with multi-state experience.

InnReg provides outsourced compliance services, helping fintech develop an effective regulatory strategy →

Common Blue Sky Compliance Challenges for Fintechs

Blue sky compliance problems often show up in the same few places. These issues are avoidable, but only if founders understand how state rules interact with product design and capital strategy.

The most common compliance challenges include:

Multi-state fundraising without tracking state-specific filings: Each new investor can create a new jurisdictional trigger. Filing rules vary by state, and deadlines are easy to miss mid-round.

Relying on unregistered brokers or finders: Paying contractors or advisors to help raise funds without proper licensing can violate state laws, even if they don’t call themselves brokers.

Overlooking state filing deadlines: Relying on a federal exemption like Rule 506 doesn’t remove state obligations. Most states still expect a notice filing, often within a specific window after the first sale.

Misjudging how states view digital assets: Teams building around tokens or synthetic products sometimes assume they are outside securities law. But when those offerings look like investments or promise returns, state regulators may step in, regardless of how the product is labeled.

Treating one-size-fits-all compliance as sufficient: What satisfies regulators in one state may not be enough in another. Some perform merit review; others expect upfront licensing.

—

For fintech teams moving fast across products, users, and states, blue sky laws are a structural part of compliance.

These state-level rules actively shape how offerings can be structured, marketed, and sold, especially when the product touches investment or advisory functions.

Ignoring state obligations can jeopardize investor confidence and halt fundraising activity. From early-stage capital raises to novel digital asset launches, blue sky compliance is a live issue, not a historical one.

As such, fintechs should track where their users are, know where their investors live, and build filing and licensing workflows that scale. Whether handled in-house or with external support, staying ahead of state-specific triggers is what keeps products moving and deals on track.

Tarik is a Principal Compliance Consultant at InnReg with over 5 years of experience advising fintech clients across broker-dealer, RIA, and money transmitter verticals. He holds FINRA Series 3, 7, 24, 57, 63, 79, and 99 licenses, with expertise in regulatory strategy, supervisory systems, and compliance roadmap implementation.

How Can InnReg Help?

InnReg is a global regulatory compliance and operations consulting team serving financial services companies since 2013.

We are especially effective at launching and scaling fintechs with innovative compliance strategies and delivering cost-effective managed services, assisted by proprietary regtech solutions.

If you need help with broker-dealer compliance, reach out to our regulatory experts today:

Related Articles

Featured LinkedIn Posts