SEC Crypto Guidance: What Fintechs Need to Know in 2026

The Securities and Exchange Commission (SEC) initially released FAQs on crypto asset activities (December 17, 2025), offering clarity on how existing securities regulations apply to digital assets and distributed ledger technology. More recently, in March 2026, the SEC expanded on this guidance through a formal interpretation addressing how federal securities laws apply to different types of crypto assets and related activities.

Together, these developments provide a more structured view of how regulated firms can engage in crypto-related activities without stepping outside established regulatory frameworks. While the FAQs focused on how existing rules apply across custody, trading, settlement, and recordkeeping, the 2026 interpretation goes further by introducing a clearer framework for classifying crypto assets and evaluating when securities laws apply.

For fintechs, the value now lies not only in understanding how the SEC interprets existing rules in crypto-specific contexts, but also in how asset classification and business models influence regulatory treatment. This includes greater clarity around which activities fall within securities laws and how regulatory expectations may evolve as products develop.

This article breaks down the SEC’s guidance by activity and business type, highlights which firms are most affected, outlines key compliance considerations, and explains how fintechs should approach structuring crypto-enabled products and services in light of the SEC’s evolving position.

At InnReg, we help fintechs navigate crypto-related regulatory compliance. From registration and licensing to building and managing day-to-day compliance programs, our team supports broker-dealers, ATSs, and other regulated firms operating at the intersection of crypto and traditional securities.

Crypto Asset Activities Covered by the SEC’s Statements

The SEC FAQs related to crypto and distributed ledger technologies primarily focused on how specific crypto asset activities fit within existing securities regulatory frameworks. More recent SEC guidance expands on this approach by introducing a clearer structure for how crypto assets themselves are evaluated, including formal categories and more defined boundaries between securities and non-securities.

Together, the SEC’s statements reflect a combined activity-based and asset-based approach. In practice, this means regulatory analysis now depends both on what a firm is doing (e.g., custody, trading, settlement) and what type of crypto asset is involved.

The SEC’s guidance continues to focus on the following activity areas:

Broker-Dealer Custody and Financial Responsibility: How the Customer Protection Rule, the Net Capital Rule, and custody concepts apply when broker-dealers engage with crypto assets.

Crypto Asset Trading on ATSs and Exchanges: Conditions under which regulated trading venues may facilitate trading involving crypto asset securities, including security and non-security crypto pairs.

Transfer Agent Functions Using DLT: When transfer agent registration is required, and how blockchain technology may be used as an official recordkeeping system.

Clearing, Settlement, and Recordkeeping: How existing clearance, settlement, and books-and-records obligations apply to crypto asset transactions conducted by regulated firms.

Crypto Exchange-Traded Products (ETPs): Application of Regulation M and existing no-action relief to ETPs referencing crypto assets.

Taken together, these areas reflect how the SEC is integrating crypto into the existing market structure while also introducing a more defined framework for evaluating crypto assets themselves.

The regulatory approach now combines activity-based analysis with clearer asset classification, helping distinguish when crypto assets fall within securities laws and when they do not. In parallel, coordination with the Commodity Futures Trading Commission (CFTC) further clarifies jurisdictional boundaries between securities and commodities.

For fintechs developing crypto-related products, this reinforces the need to align both business models and asset design with evolving regulatory expectations from the outset.

Learn how InnReg helps fintechs develop regulatory and product strategies →

SEC Views on Crypto Asset Activities by Business Type

The SEC FAQs evaluate crypto activity based on the type of regulated firm involved, rather than creating new crypto-specific categories. That distinction is important. Regulatory expectations depend on who is operating the business and what role they play, even when similar technology is used.

More recent SEC guidance adds another layer to this analysis. Regulatory obligations now depend not only on the type of firm involved, but also on how the underlying crypto asset is classified and whether it is subject to an investment contract. As a result, firms offering similar products may face different regulatory expectations depending on both their role and the characteristics of the assets they handle.

Business Type | Primary Crypto Activities Addressed | Key Regulatory Focus |

|---|---|---|

Broker-Dealers | Custody, customer protection, net capital, SIPC exposure | |

Transfer Agents | Ownership records, issuance, and transfers using DLT | |

ATSs and Exchanges | Trading, pairs trading, disclosure, and settlement | |

ETP Sponsors and Participants | Issuance and trading of crypto-linked products | Regulation M, anti-fraud rules |

1. Broker-Dealer and Crypto Asset Activities

Broker-dealers are the most directly impacted by the SEC FAQs on crypto asset activities.

Much of the guidance focuses on how existing broker-dealer rules apply when crypto assets are introduced into custody, trading, or balance sheet activities.

More recent SEC guidance builds on this by clarifying how crypto assets should be classified and when securities laws apply, adding an additional layer to how broker-dealers evaluate their obligations.

The SEC’s position is evolutionary, not experimental. Longstanding financial responsibility rules remain the starting point.

Learn how InnReg supports broker-dealers →

Customer Protection Rule and Crypto Assets

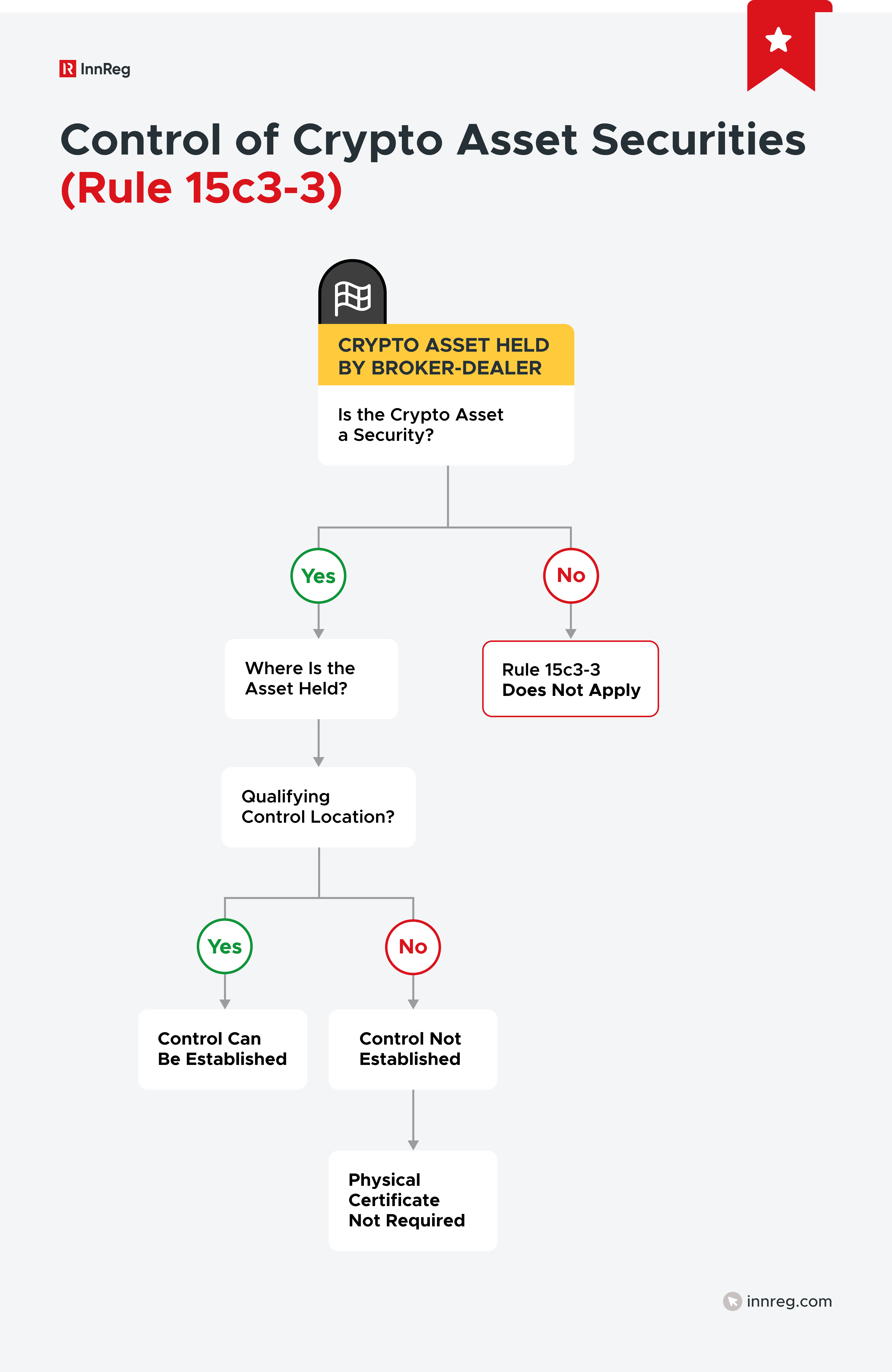

The SEC clarifies that Exchange Act Rule 15c3-3 applies only to securities. Crypto assets that are not securities are outside the scope of the Customer Protection Rule, even if they are held by a broker-dealer.

For crypto assets that are securities, the rule applies as it would for any other security. This distinction is critical for firms offering mixed asset products. Misclassifying assets at the custody level can lead to incorrect reserve calculations and flawed account structures.

With the SEC’s more defined framework for evaluating crypto assets, firms are better positioned to assess whether a particular asset falls within the scope of securities rules, but classification still requires careful, fact-specific analysis.

Establishing Control of Crypto Asset Securities

The SEC FAQs state that a broker-dealer can establish control of a crypto asset security under Rule 15c3-3(c) even if the security is not issued in certificated form.

What matters is where and how the asset is held, not whether a physical certificate exists.

This clarification removes a long-standing point of uncertainty for digital-only securities. It also places more weight on how custody arrangements are structured, documented, and supervised.

The SPBD Statement and Its Role After the SEC FAQs

The 2020 Special Purpose Broker-Dealer statement provided a temporary enforcement position for firms seeking to custody digital asset securities. The SEC FAQs make clear that compliance with the SPBD framework is not mandatory.

Broker-dealers may instead rely on traditional Rule 15c3-3 control concepts, provided they can meet the rule’s requirements. For many firms, this opens alternative paths to custody that are better aligned with existing operations and examiner expectations.

At the same time, firms must consider how asset classification and evolving interpretations of securities status may affect whether SPBD-like structures are necessary in the first place.

Net Capital Treatment for Crypto Positions

When a broker-dealer takes a proprietary position in crypto assets, that exposure must be included in its net capital computation. The SEC FAQs make clear that crypto positions are not carved out from existing capital rules simply because they involve digital assets.

The SEC staff indicates it will not object if bitcoin and ether are treated as readily marketable assets when applying net capital haircuts. This aligns their treatment with certain commodities for purposes of Rule 15c3-1.

More recent SEC guidance further reinforces this approach by treating certain widely traded crypto assets as non-securities based on their characteristics, which has direct implications for how firms assess capital treatment.

For broker-dealers participating in crypto ETP activity, this clarification reduces uncertainty around capital treatment. It also affects firms that facilitate crypto transactions using their own balance sheet.

Other crypto assets may still be subject to higher haircuts. Liquidity, price volatility, and market depth remain relevant factors when determining capital impact.

See also:

SIPC Protection and Insolvency Exposure

SIPC coverage is limited to securities as defined under SIPA. Crypto assets that do not meet that definition fall outside SIPC protection, and even crypto asset securities are only covered when they are registered under the Securities Act.

This distinction has direct consequences for fintechs. Disclosures, customer agreements, and contingency planning need to reflect how crypto assets would be treated if a broker-dealer enters liquidation.

As the SEC provides more clarity on which crypto assets are not securities, firms should ensure that customer disclosures accurately reflect the limits of SIPC protection across different asset types.

As a result, many broker-dealers rely on structural and contractual approaches to address potential exposure.

Learn how InnReg helps broker-dealers map and address exposures →

Need help with fintech compliance?

Fill out the form below and our experts will get back to you.

2. Transfer Agents and Distributed Ledger Technology

The SEC FAQs on crypto and ledger technologies also address how transfer agent requirements apply when securities are issued, recorded, or transferred using distributed ledger technology. While this affects a narrower set of firms than the broker-dealer guidance, the implications are significant for fintechs involved in tokenized securities or blockchain-based cap tables.

More recent SEC guidance reinforces this analysis by explicitly recognizing certain blockchain-based instruments as digital securities, clarifying when traditional transfer agent requirements apply in tokenized environments.

When Crypto Transfer Agents Must Register

A firm’s obligation to register as a transfer agent depends on what it’s doing and which securities are involved. Registration is triggered when a firm carries out transfer agent functions for securities subject to Exchange Act Section 12.

Those functions can include keeping official ownership records, processing changes in ownership, monitoring issuances, or handling exchanges and conversions. In many structures, these responsibilities are split across multiple providers, and each party needs to evaluate its own regulatory position.

As the SEC provides clearer distinctions between digital securities and non-security crypto assets, firms must assess whether the underlying instrument falls within the scope of transfer agent regulation before determining registration obligations.

Using Blockchain as the Official Securityholder Record

The SEC FAQs clarify that a registered transfer agent may use distributed ledger technology as its official master securityholder file, provided all existing regulatory requirements are met. The use of blockchain does not eliminate recordkeeping, reporting, or examination obligations.

In practice, this often results in hybrid recordkeeping models. Transaction data such as wallet addresses, balances, and transaction history may be maintained on-chain, while investor identity and other sensitive information remain off-chain within proprietary systems.

What matters to the SEC is that records remain accurate, secure, readily accessible, and reproducible in a usable format. The technology choice is secondary to the firm’s ability to meet those standards on an ongoing basis.

For fintechs building infrastructure around tokenized securities, this guidance suggests that blockchain-based systems may be used in ways that align with existing regulatory requirements. It also reinforces the need for clear governance, controls, and accountability around who maintains the official books and records.

3. ATSs, Exchanges, and Crypto Asset Trading

The SEC FAQs related to crypto and ledger technologies address how crypto asset trading can occur on regulated venues. The SEC’s position allows for crypto trading within existing market structure rules, rather than carving out a separate framework.

More recent SEC guidance builds on this by clarifying how different types of crypto assets are classified and when trading activity may fall within securities laws, which directly affects how ATSs and exchanges evaluate listing and trading decisions.

Pairs Trading Under the SEC FAQs

According to the SEC FAQs, federal securities laws do not, by themselves, prevent regulated trading venues from offering pairs that include both crypto-asset securities and non-security crypto assets. This covers trading models that do not involve an intermediate fiat leg.

The SEC’s position does not remove existing obligations. Exchanges and ATSs must continue to comply with applicable market structure rules, including those related to disclosures and transaction reporting.

With clearer distinctions between security and non-security crypto assets, firms are better positioned to determine which trading pairs fall within securities regulation, although classification remains a key threshold analysis.

As a result, firms typically need to address these requirements before rolling out pairs trading functionality.

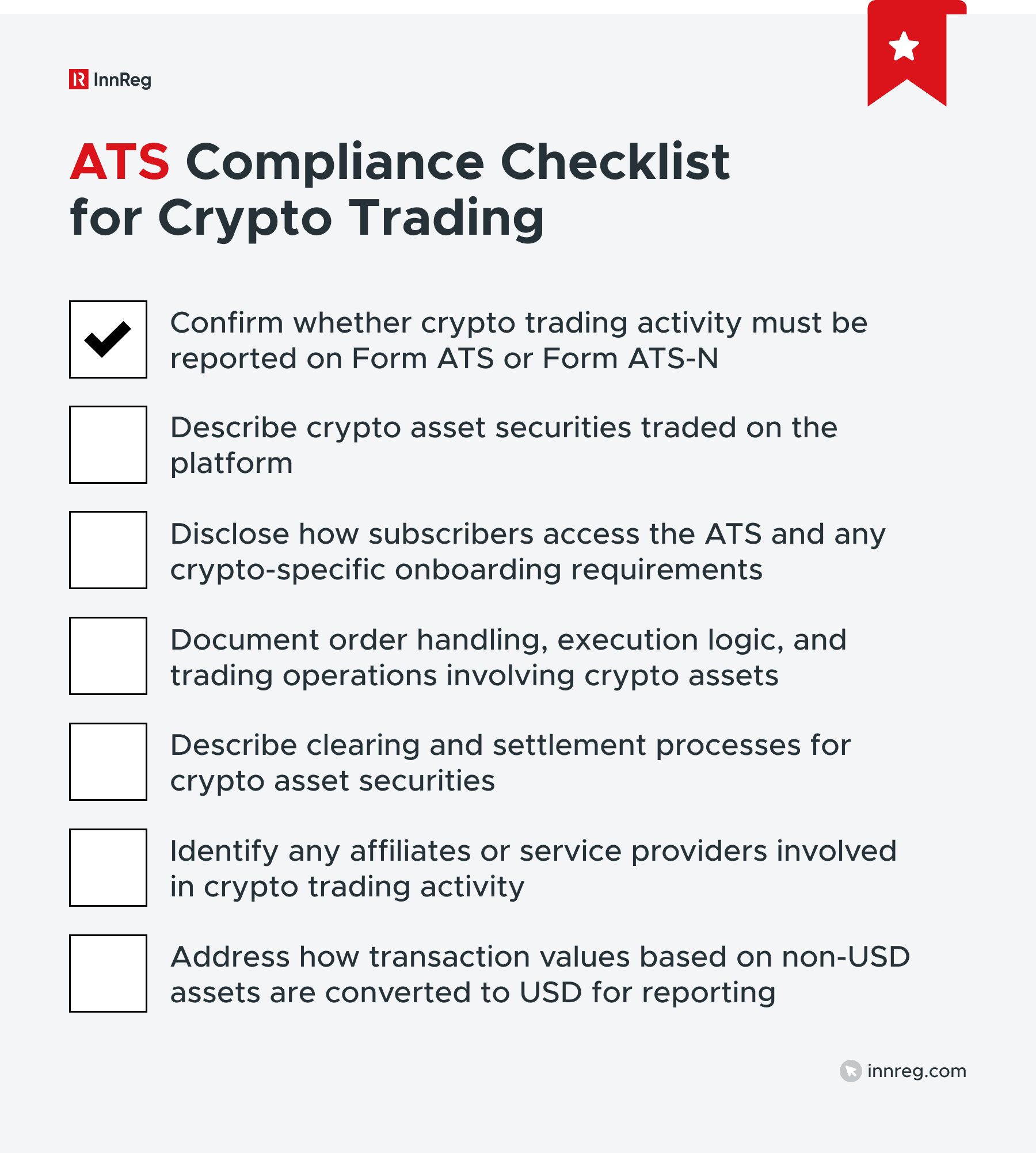

ATS Compliance for Crypto Trading

ATSs engaging in crypto asset trading remain subject to Regulation ATS. The SEC FAQs make clear that crypto-related trading activity must be accurately reflected in Form ATS or Form ATS-N filings, depending on the type of securities traded.

Required disclosures may cover trading operations, access criteria, order handling, clearing and settlement processes, and the role of affiliates. Where transaction values are based on non-USD assets, ATSs may convert values to USD using consistent and reasonable methods for reporting purposes.

Firms that treat crypto as an extension of existing trading activity, rather than a parallel business line, are often better positioned to meet these expectations.

Read our article to learn more about Regulation ATS →

See also:

Clearing and Settlement for Crypto Asset Securities

The SEC FAQs address whether an ATS operator that clears and settles crypto asset securities for its own customers must also register as a clearing agency. The staff’s view is that registration is not required when those activities fall within customary brokerage functions.

In practice, this means a broker-dealer that operates an ATS may handle settlement by recording debits and credits on its own books, as long as it is acting in its capacity as a broker-dealer. Performing these functions alone does not convert the firm into a clearing agency.

For fintech platforms, this distinction affects how much of the trading and settlement process can be handled internally without expanding the firm’s regulatory footprint.

However, firms should consider how changes in an asset’s classification or evolving interpretations of securities status may affect whether certain activities continue to fall within brokerage functions over time.

See how InnReg supports Alternative Trading Systems (ATS) →

4. Crypto Exchange-Traded Products (ETPs)

The SEC publication also touches on crypto exchange-traded products, an area where regulatory expectations have historically been less explicit. While the guidance is narrow, it provides useful context for how the SEC views crypto-linked products that trade on regulated exchanges.

Regulation M and Crypto ETPs

The SEC staff indicates it will not object to trading in shares of crypto ETPs when those transactions follow the same conditions previously outlined for commodity-based investment vehicles. In doing so, the SEC is aligning the treatment of crypto ETPs with other exchange-traded products that track commodity exposure.

This alignment is reinforced by the SEC’s view that certain crypto assets may be treated similarly to commodities based on their characteristics, which supports existing approaches to structuring crypto-linked ETPs.

That position is conditioned on the ETP being listed and traded on a national securities exchange pursuant to SEC-approved rules. It also assumes that participants are not engaging in conduct outside the scope of permitted distribution activity.

—

The SEC is no longer just explaining how rules apply to crypto. It’s defining how crypto assets are evaluated within the existing regulatory framework.

For fintechs, this raises the importance of getting both structure and classification right from the start. The firms that do this well will be better positioned to scale, adapt, and withstand regulatory scrutiny.

Adriana is a Principal Consultant at InnReg with 8 years of compliance experience specializing in VASP licensing and regulatory frameworks across Europe and LATAM. She has held senior compliance roles at leading global crypto and financial institutions, including Gate.io, Binance, Santander Bank, and BNP Paribas, with deep expertise in KYC/AML operations, MiCA adaptation, and building compliance programs from the ground up.

How Can InnReg Help?

InnReg is a global regulatory compliance and operations consulting team serving financial services companies since 2013.

We are especially effective at launching and scaling fintechs with innovative compliance strategies and delivering cost-effective managed services, assisted by proprietary regtech solutions.

If you need help with compliance, reach out to our regulatory experts today:

Related Articles

Featured LinkedIn Posts