What Is the SEC Net Capital Rule? SEC Rule 15c3-1 Explained

Key Takeaways

The SEC’s net capital rule is designed to require broker-dealers to maintain enough liquid regulatory capital to meet their obligations and protect customers and counterparties.

Net capital is generally calculated by starting with net worth, deducting non-allowable assets, and applying prescribed haircuts to certain securities positions.

Minimum net capital requirements vary depending on the broker-dealer’s business activities and may be based on a fixed minimum, the aggregate indebtedness ratio, or the alternative method.

If a firm’s capital declines toward deficiency levels, it may need to notify regulators promptly and could face operational restrictions.

Broker-dealers typically monitor net capital on an ongoing basis, often daily, and report capital information to regulators through FOCUS filings.

Broker-dealers cannot operate without sufficient regulatory capital. US securities law requires these firms to maintain financial resources that allow them to meet obligations to customers and counterparties, even during periods of market stress.

One of the central requirements in that framework is the SEC Net Capital Rule, formally known as Rule 15c3-1 under the Securities Exchange Act of 1934. The rule establishes minimum capital thresholds and prescribes how broker-dealers must calculate their regulatory capital. It also sets restrictions and reporting requirements when capital levels approach regulatory limits.

This article explains how the SEC Net Capital Rule works in practice. We’ll cover how net capital is defined, how minimum requirements are determined, and how broker-dealers calculate and monitor their capital. We’ll also look at common compliance challenges and areas that often create confusion for fintech founders, lawyers, and compliance teams.

At InnReg, we help broker-dealers build and manage practical compliance programs. Our team supports firms with registration, regulatory capital oversight, policies and procedures, and ongoing compliance operations. Contact us to learn more.

What Is the SEC Net Capital Rule (Rule 15c3-1)?

The SEC Net Capital Rule (Rule 15c3-1) is a financial responsibility rule that requires broker-dealers to maintain a minimum amount of liquid capital. It’s part of the SEC’s framework for protecting customers and reducing the risk that a broker-dealer fails while holding obligations to clients or counterparties.

The rule focuses on liquidity, not just balance sheet strength. Broker-dealers must maintain net capital that can be readily converted into cash, rather than relying on illiquid assets or long-term investments. This is why the rule requires firms to deduct certain assets and apply risk-based adjustments when calculating regulatory capital.

In practice, the SEC Net Capital Rule is one of the core financial controls governing broker-dealers. Rule 15c3-1 applies to most SEC-registered broker-dealers, but the requirements vary depending on the firm’s business model:

Introducing broker-dealers (no custody): Lower capital thresholds because the firm does not hold customer funds or securities.

Broker-dealers that carry customer accounts: Higher capital requirements due to increased operational and custody risks.

Clearing or carrying firms: The highest capital requirements because these firms hold customer assets and process transactions.

The rule also imposes operational discipline. Firms must monitor net capital continuously and report capital levels through regulatory filings such as FOCUS reports. If capital levels fall close to regulatory thresholds, early warning provisions trigger notification and operational restrictions.

How Net Capital Is Defined Under Rule 15c3-1

Under the SEC Net Capital Rule, “net capital” is not the same as the equity shown on a broker-dealer’s balance sheet. Rule 15c3-1 uses a regulatory capital calculation designed to measure how much liquid financial capacity a broker-dealer actually has.

The calculation begins with the firm’s net worth but then applies a series of regulatory adjustments. Certain assets are excluded because they cannot easily be converted into cash, while securities positions are reduced using risk-based deductions. As a result, regulatory net capital is typically lower than the firm’s accounting equity.

The sections below explain how each of the components works and how they affect a broker-dealer’s regulatory capital:

Net Worth vs. Net Capital

Net worth is the starting point for calculating regulatory capital under Rule 15c3-1. It represents the firm’s shareholders’ equity as shown on the broker-dealer’s balance sheet, calculated as total assets minus total liabilities.

However, the SEC Net Capital Rule does not rely on accounting equity alone. The rule requires broker-dealers to adjust net worth to reflect liquidity and market risk. These adjustments produce regulatory net capital, which is the amount regulators use to evaluate whether a firm meets its minimum capital requirements.

Several deductions are applied during this process. For example, certain illiquid assets are removed from the calculation, and securities positions may be reduced through risk-based haircuts. These adjustments recognize that not all balance sheet assets can be quickly converted into cash.

Because of these adjustments, regulatory net capital is usually lower than net worth, and firms must monitor this figure closely when assessing their capital position under the SEC Net Capital Rule.

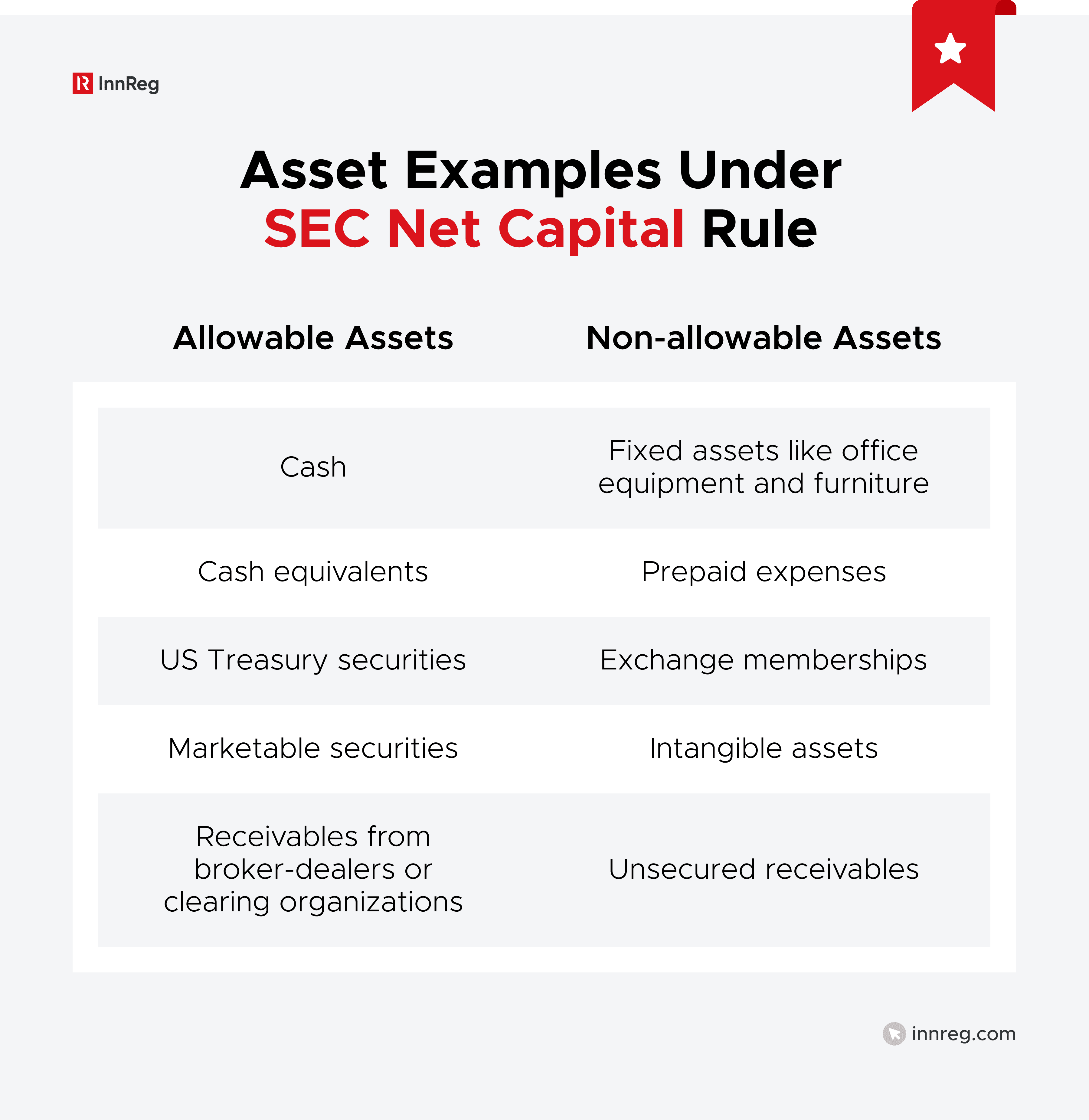

Allowable Assets vs. Non-Allowable Assets

Under the SEC Net Capital Rule, not all assets on a broker-dealer’s balance sheet count toward regulatory capital. Rule 15c3-1 distinguishes between allowable assets, which can be included in the net capital calculation, and non-allowable assets, which must be deducted entirely.

The rule focuses on liquidity. Regulators want to know what resources a firm could realistically convert into cash within a short period of time. Assets that cannot be quickly liquidated are removed from the calculation.

Allowable assets generally include items that can readily support a firm’s financial obligations. In contrast, non-allowable assets are deducted from net worth when calculating regulatory net capital because they may not be accessible during a financial stress event.

Here are a few key examples of both types of assets:

Regulatory Haircuts

Another key adjustment under Rule 15c3-1 is the use of regulatory haircuts, which are deductions applied to securities positions when calculating net capital. These reductions reflect the potential market risk associated with holding those securities.

Even highly liquid securities can fluctuate in value. For this reason, the SEC Net Capital Rule requires broker-dealers to reduce the reported value of securities positions by a specified percentage when calculating regulatory capital. The deduction represents a buffer against short-term price volatility.

Haircut percentages vary depending on the type of security and its risk profile. We’ll define regulatory haircuts later in this article.

Who Must Comply With the SEC Net Capital Rule

Any firm that executes securities transactions for customers or for its own account generally falls within the scope of Rule 15c3-1. The sections below explain how the SEC Net Capital Rule applies across different broker-dealer business models.

Broker-Dealers

The SEC Net Capital Rule primarily applies to registered broker-dealers, which are firms that buy and sell securities either for customers or for their own accounts. These firms must maintain regulatory capital at all times as a condition of operating in the US securities markets.

The exact capital requirement depends on the firm’s activities and operational structure. Broker-dealers that take on more operational or market risk typically face higher net capital requirements under Rule 15c3-1.

Activities that often increase capital requirements include:

Holding customer funds or securities

Carrying customer accounts

Clearing and settling trades

Maintaining proprietary trading positions

Operating market-making activities

Regulators expect broker-dealers to monitor their capital position continuously. If a firm’s net capital approaches regulatory thresholds, it may need to notify regulators and limit certain activities until capital levels recover.

See also:

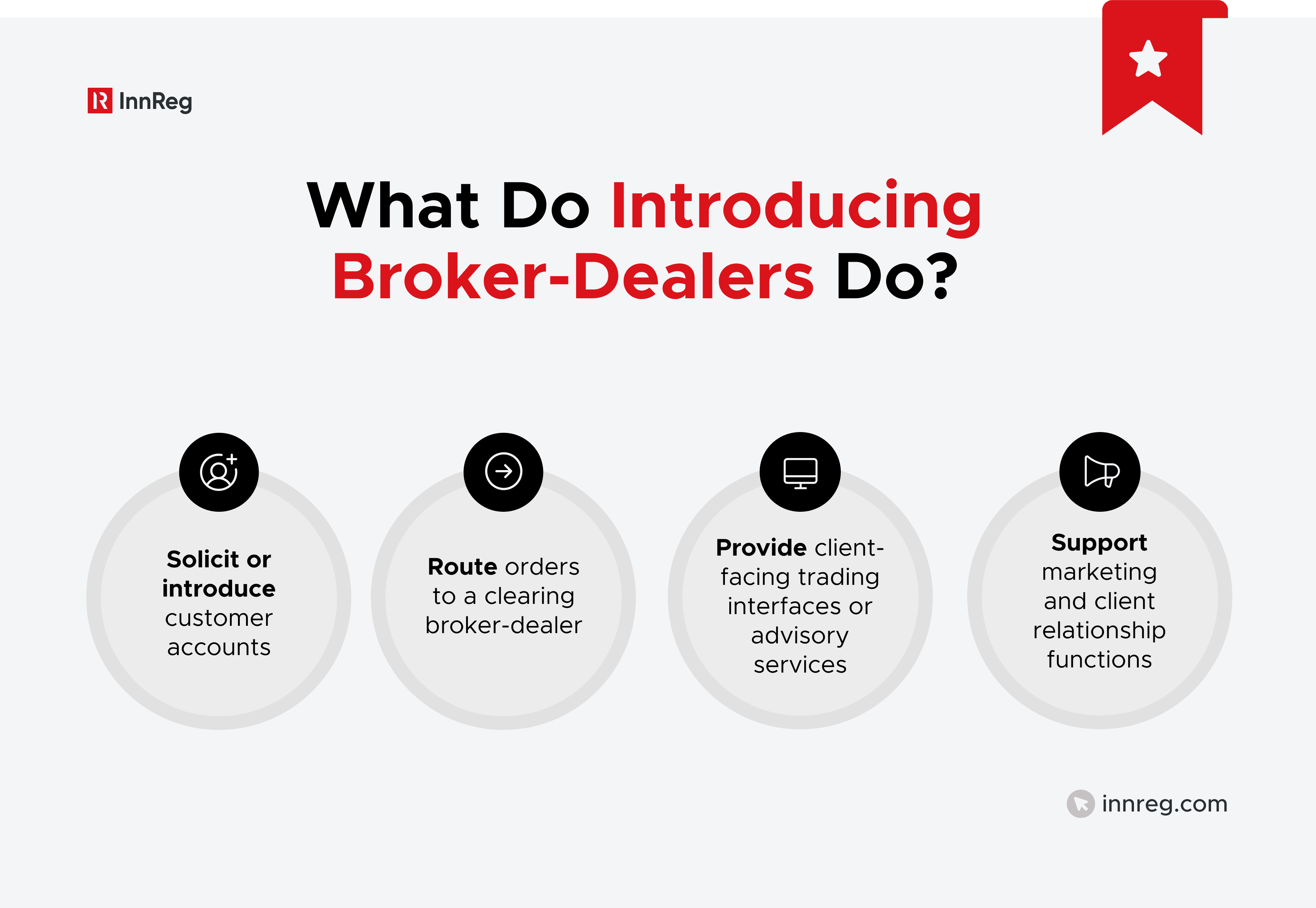

Limited-Purpose and Introducing Broker-Dealers

Some broker-dealers operate with a more limited role in the securities transaction process. These firms are often referred to as introducing broker-dealers, meaning they introduce customer accounts to another broker-dealer that performs clearing, custody, and settlement functions.

Because these firms do not hold customer assets or carry customer accounts, their regulatory risk profile is lower. As a result, the SEC Net Capital Rule generally imposes lower minimum capital requirements on limited-purpose broker-dealers.

Typical activities of introducing broker-dealers include:

The clearing broker-dealer handles operational functions such as custody of funds and securities, settlement of trades, and margin processing.

Even with this limited role, introducing broker-dealers must still comply with Rule 15c3-1. They are required to maintain minimum net capital levels and monitor their regulatory capital position on an ongoing basis.

Need help with broker-dealer compliance?

Fill out the form below and our experts will get back to you.

Clearing Broker-Dealers and Firms That Hold Customer Assets

Clearing broker-dealers play a central role in the securities transaction process. These firms handle trade settlement, custody of customer assets, and recordkeeping for customer accounts. Because of these responsibilities, clearing and carrying firms face the highest capital expectations under the SEC Net Capital Rule.

When a broker-dealer holds customer funds or securities, regulators view the operational and financial risks as significantly higher. A failure at this level could directly affect customer assets. As a result, Rule 15c3-1 requires clearing firms to maintain substantially larger net capital buffers compared to introducing broker-dealers.

Clearing and carrying firms typically perform functions such as:

Holding customer cash and securities in custody

Settling securities transactions

Maintaining margin accounts

Processing corporate actions and account transfers

Keeping detailed customer account records

These firms also operate under additional regulatory obligations. For example, many must comply with the SEC Customer Protection Rule (Rule 15c3-3), which governs how customer funds and securities must be safeguarded.

Key Regulators Overseeing the SEC Net Capital Rule

Several regulators oversee compliance with the SEC Net Capital Rule, each with a different role in supervision, examinations, and enforcement. While the rule itself is issued by the SEC, broker-dealers typically interact more frequently with their self-regulatory organization during day-to-day supervision.

Broker-dealers are subject to both SEC oversight and ongoing supervision by FINRA or another self-regulatory organization, along with additional requirements tied to customer protection rules. Learn how these regulators fit into the broader SEC Net Capital Rule:

The Role of the SEC

The Securities and Exchange Commission (SEC) is the primary regulator responsible for establishing and enforcing the SEC Net Capital Rule. Rule 15c3-1 was adopted under the Securities Exchange Act of 1934 as part of the SEC’s financial responsibility rules for broker-dealers.

The SEC’s responsibilities include:

Drafting and amending Rule 15c3-1

Publishing interpretive guidance and regulatory releases

Conducting examinations and investigations

Bringing enforcement actions when firms violate capital requirements

The SEC sets the regulatory framework that broker-dealers must follow. FINRA and other self-regulatory organizations typically oversee day-to-day supervision and examinations, but the SEC maintains ultimate authority over the Rule.

The Role of FINRA

Most broker-dealers are members of the Financial Industry Regulatory Authority (FINRA), which acts as the primary self-regulatory organization supervising broker-dealer operations.

FINRA’s responsibilities related to the SEC Net Capital Rule are:

Examining broker-dealers for compliance with Rule 15c3-1

Reviewing capital calculations during routine and targeted exams

Monitoring regulatory filings such as FOCUS reports

Investigating potential capital deficiencies

In practice, broker-dealers interact with FINRA more frequently than with the SEC. FINRA examinations often review how firms calculate net capital, classify assets, and apply regulatory haircuts.

Curious to read FINRA rules that might impact your broker-dealer model? Read our collection here →

Interaction With the Customer Protection Rule (15c3-3)

The SEC Net Capital Rule operates alongside the Customer Protection Rule (Rule 15c3-3), which governs how broker-dealers safeguard customer funds and securities.

While Rule 15c3-1 focuses on the financial condition of the broker-dealer, Rule 15c3-3 focuses on protecting customer property. Many broker-dealers, especially those that carry customer accounts, must comply with both rules simultaneously. Here are some of the common interactions between the two rules:

Customer Protection Rule | SEC Net Capital Rule |

|---|---|

Reserve account requirements for customer funds | |

Segregation of customer securities | |

Operational controls for custody and settlement | |

Because of this relationship, firms that hold customer assets often face both higher net capital requirements and additional operational safeguards under Rule 15c3-3.

SIPC Considerations

The Securities Investor Protection Corporation (SIPC) plays a different role in the regulatory framework. SIPC is not a regulator, but it provides limited protection to customers if a broker-dealer fails financially.

If a broker-dealer becomes insolvent, SIPC may initiate a liquidation proceeding to return customer securities and cash. The presence of SIPC does not replace the SEC Net Capital Rule. Instead, the rule is designed to reduce the likelihood that a broker-dealer reaches the point of insolvency in the first place.

Broker-dealers that are SIPC members must also follow certain financial reporting and operational requirements tied to SIPC oversight.

See also:

Minimum Net Capital Requirements Under the Rule

Rule 15c3-1 does not impose a single capital requirement for all broker-dealers. Instead, the SEC Net Capital Rule sets different minimum thresholds depending on the firm’s business activities and risk profile.

The rule combines fixed minimum dollar requirements with ratio-based capital tests. Broker-dealers must maintain net capital above the applicable threshold at all times or risk being restricted from conducting securities business until the deficiency is resolved.

Let’s look at the fine print around the minimum net capital requirements of the SEC Net Capital Rule:

Fixed Dollar Minimums by Broker-Dealer Activity

Rule 15c3-1 establishes baseline capital requirements tied to the services a broker-dealer provides. The goal is to align minimum capital levels with operational and financial risk.

Firms that do not hold customer assets generally face lower requirements. Broker-dealers that carry customer accounts, maintain proprietary positions, or clear trades must maintain significantly higher capital levels.

The typical examples can look like this:

Broker-Dealer Activity | Typical Minimum Net Capital Requirement |

|---|---|

Introducing broker (no custody) | Lower fixed dollar threshold |

Broker-dealer with customer accounts | Higher fixed requirement |

Clearing or carrying firm | Significantly higher requirement |

These thresholds represent baseline requirements. Firms must still calculate their regulatory net capital under Rule 15c3-1 and verify that the result exceeds the applicable minimum.

The Aggregate Indebtedness Standard

Many broker-dealers calculate their capital requirement using the Aggregate Indebtedness (AI) standard, which compares a firm’s liabilities to its net capital.

Under this method, a broker-dealer’s aggregate indebtedness cannot exceed 15 times its net capital. For broker-dealers in their first 12 months of operation, the ratio is more restrictive and cannot exceed eight times net capital. In other words, the firm must maintain sufficient regulatory capital relative to the amount of liabilities on its balance sheet.

Aggregate indebtedness generally includes obligations such as:

Payables to customers

Payables to broker-dealers

Short-term liabilities tied to trading activity

This ratio-based test acts as a financial constraint on leverage. If a firm’s liabilities grow too large relative to its net capital, it may fall out of compliance even if it meets the fixed dollar minimum requirement.

The Alternative Net Capital Standard

Some broker-dealers, particularly firms that carry customer accounts, operate under the Alternative Net Capital Standard instead of the aggregate indebtedness test.

Under this approach, the firm must maintain net capital equal to at least 2% of aggregate debit items, which are calculated under the SEC Customer Protection Rule reserve formula.

This method is commonly used by clearing firms and broker-dealers that maintain margin accounts. Because these firms handle significant customer balances, regulators require a capital measure tied to the size of those balances.

In practice, firms that use the alternative method must:

Calculate net capital under Rule 15c3-1

Calculate aggregate debit items under Rule 15c3-3

Maintain regulatory capital above the required percentage threshold

For firms operating under this framework, changes in customer balances or margin activity can directly affect net capital requirements.

How the SEC Net Capital Rule Calculation Works

Calculating regulatory capital under Rule 15c3-1 involves several structured adjustments to a broker-dealer’s balance sheet. Most firms calculate net capital through a sequence of steps defined in the SEC Net Capital Rule.

Each step below removes or adjusts elements that could distort the firm’s true liquidity position.

Step 1: Start With Net Worth

The net capital calculation begins with the firm’s net worth, which represents total assets minus total liabilities on the broker-dealer’s balance sheet. This figure is typically derived from the firm’s financial statements and serves as the starting point for the regulatory calculation.

However, accounting equity alone does not provide an accurate picture of regulatory liquidity. Several adjustments must be made before the firm can determine its net capital under Rule 15c3-1.

Step 2: Deduct Non-Allowable Assets

The next step removes assets that regulators consider illiquid or inaccessible during a financial stress event. These are known as non-allowable assets and must be deducted entirely from the calculation.

Common examples include:

Fixed assets such as office equipment and furniture

Prepaid expenses

Intangible assets such as goodwill

Certain unsecured receivables

After these deductions are applied, the firm continues the calculation by applying additional regulatory adjustments before arriving at tentative net capital.

Step 3: Apply Securities Haircuts

The next adjustment applies regulatory haircuts to securities positions held by the broker-dealer. These deductions reflect the potential market risk associated with holding financial instruments that could decline in value.

Haircuts vary depending on the type of security, its liquidity, and its volatility. For example, Treasury securities typically receive smaller deductions, while equities or concentrated positions receive larger reductions.

This step reduces the value of the firm’s trading inventory for regulatory purposes, which helps regulators account for market volatility.

Step 4: Determine Tentative Net Capital

After applying non-allowable asset deductions and securities haircuts, the firm arrives at its tentative net capital, which is an intermediate measure used before applying any additional required charges or deductions under Rule 15c3-1.

At this stage, the calculation reflects a liquidity-focused view of the firm’s financial position. The remaining figure is used to determine whether the broker-dealer satisfies its regulatory capital obligations.

Step 5: Compare With Required Minimum

The final step is to compare the calculated net capital against the minimum requirement established under Rule 15c3-1.

A broker-dealer must maintain regulatory capital above the highest applicable requirement, which may include:

Fixed dollar minimum thresholds

The Aggregate Indebtedness Ratio Test

The Alternative Net Capital standard

If a firm’s net capital falls below the required threshold, it may face operational restrictions and must take steps to restore compliance. Continuous monitoring is, therefore, a core operational responsibility for broker-dealers operating under the SEC Net Capital Rule.

Haircuts and Risk Adjustments in Rule 15c3-1

Haircuts are one of the most important adjustments in the SEC Net Capital Rule calculation. They reduce the value of securities positions to reflect potential market volatility. The goal is to account for the risk that a position could lose value before it can be liquidated.

Under Rule 15c3-1, broker-dealers must apply standardized percentage deductions to many types of securities. These reductions are built into the regulatory capital calculation and apply even if the securities are highly liquid.

The haircut framework allows regulators to estimate how much capital would remain if market conditions deteriorate. The section below helps broker-dealers understand the standards and charges surrounding these adjustments:

Standard Haircuts for Common Securities

The SEC Net Capital Rule establishes baseline haircut percentages for many commonly held securities. These deductions vary depending on liquidity, maturity, and historical volatility.

Below are simplified examples of typical haircut ranges used in regulatory calculations:

Security Type | Typical Haircut | Reason for Deduction |

|---|---|---|

US Treasury securities (short maturity) | ~0%-1% | Very high liquidity and low credit risk |

US Treasury securities (longer maturity) | ~1%-6% | Greater interest rate sensitivity |

US agency securities | ~2%-6% | Slightly higher credit and liquidity risk |

Investment-grade corporate bonds | ~6% | Credit and market risk |

Listed equity securities | ~15% | Higher price volatility |

These deductions can materially reduce regulatory capital. Broker-dealers with significant inventory positions must account for haircuts when evaluating their capital buffer.

Concentration Charges

Standard haircuts may increase when a broker-dealer holds large or concentrated positions in a single security or issuer. Concentration risk can make it more difficult for a firm to liquidate positions without affecting market prices.

Rule 15c3-1 addresses this through additional deductions when positions exceed certain concentration thresholds. The larger the exposure relative to the firm’s capital, the greater the potential adjustment.

These concentration charges recognize that liquidity risk increases when positions are heavily concentrated in a limited number of securities.

Treatment of Proprietary Positions

Broker-dealers that engage in proprietary trading must also account for haircut adjustments across their trading inventory. All proprietary securities positions are subject to the haircut framework under the SEC Net Capital Rule.

This means capital requirements can fluctuate with changes in trading activity or market prices. A firm that expands proprietary trading activity may see its regulatory capital decline due to increased haircut deductions.

For fintech broker-dealers or platforms exploring proprietary trading strategies, these capital impacts often become an important factor in business model design and ongoing capital planning.

Early Warning Levels and Capital Deficiency

Rule 15c3-1 not only sets minimum capital thresholds. It also includes early warning provisions that trigger regulatory notifications before a firm actually falls below its required capital level. These mechanisms allow regulators to monitor firms that may be approaching financial stress.

The goal is preventative supervision. If a broker-dealer’s capital begins to decline, regulators want to be notified early so they can evaluate the firm’s financial condition. For compliance teams, monitoring these thresholds is just as important as meeting the minimum capital requirement itself:

Early Warning Thresholds

Under the SEC Net Capital Rule, broker-dealers must notify regulators when their net capital falls below certain early warning levels, even if the firm is still technically in compliance.

These notification thresholds vary depending on the firm’s regulatory capital method and minimum capital requirement. Early warning triggers are designed to alert regulators when a firm’s capital cushion begins to narrow.

When an early warning threshold is triggered, firms are typically required to:

Notify their designated examining authority, often FINRA

Provide updated financial information if requested

Monitor capital levels more closely until the situation stabilizes

Early warnings do not automatically mean the firm is out of compliance. However, they signal that the broker-dealer’s capital buffer is becoming limited.

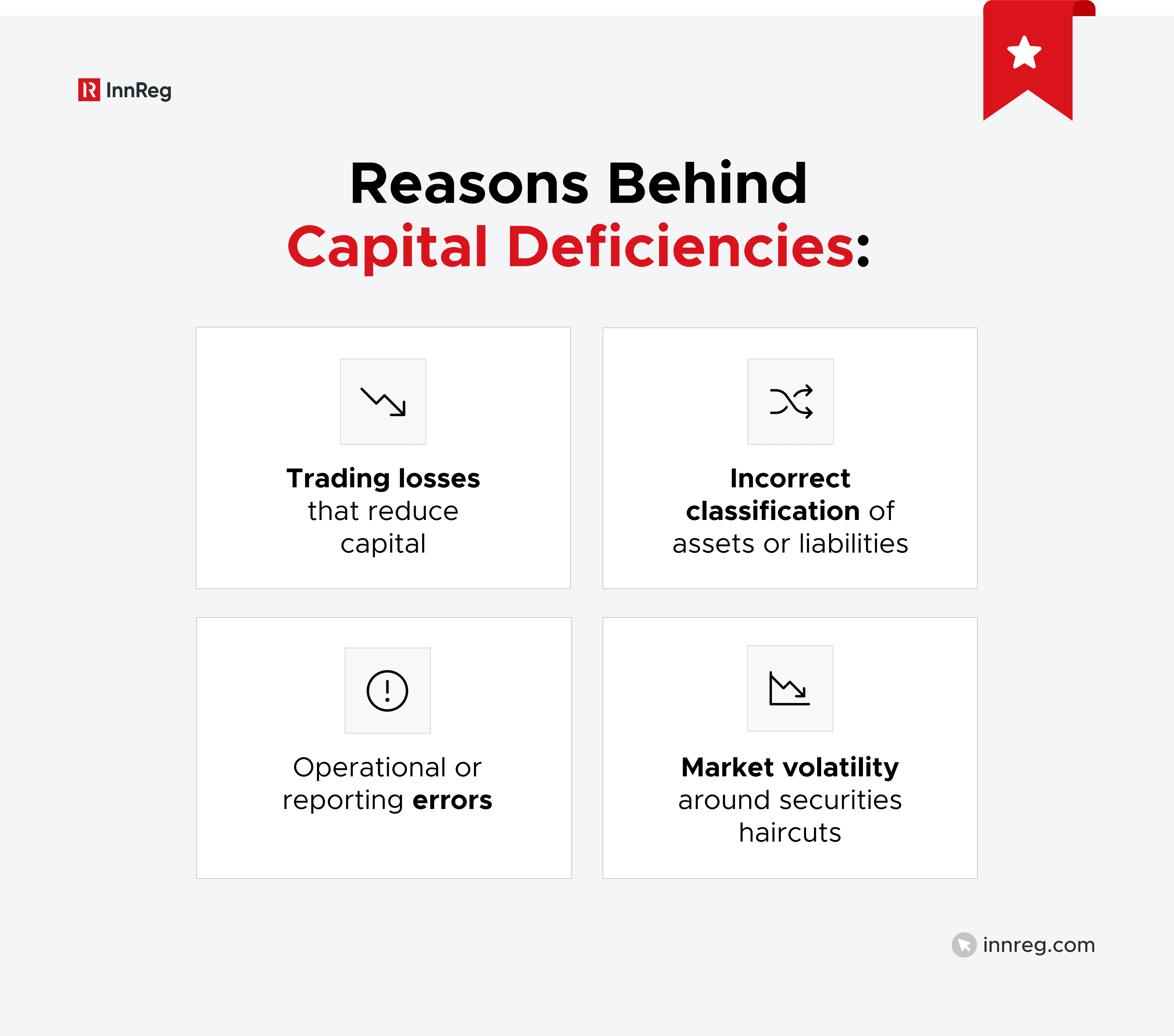

Capital Deficiency Triggers

A net capital deficiency occurs when a broker-dealer’s regulatory capital falls below the minimum requirement established under Rule 15c3-1.

When this happens, the firm must immediately notify its regulators and take steps to restore compliance. This situation is treated as a serious regulatory event because the firm no longer meets the financial responsibility standards required to operate as a broker-dealer.

Restrictions When Capital Falls Below Required Levels

If a broker-dealer falls below its required net capital level, regulators may impose operational restrictions until the deficiency is resolved.

Common restrictions may include:

Limiting or suspending certain trading activities

Restricting withdrawals or distributions of capital

Requiring additional financial reporting

Supervisory review by regulators

In severe cases, regulators may require the firm to wind down operations or transfer customer accounts to another broker-dealer.

Because of these consequences, most broker-dealers implement internal monitoring procedures that track regulatory capital daily and escalate issues well before early warning thresholds are reached.

See also:

Reporting and Monitoring Requirements

Compliance with the SEC Net Capital Rule is not limited to calculating capital periodically. Broker-dealers must monitor their regulatory capital continuously and report financial information to regulators on a regular basis.

In practice, most broker-dealers integrate net capital monitoring into their daily financial and compliance processes:

FOCUS Reports and Regulatory Filings

Broker-dealers must report their financial condition through FOCUS reports (Financial and Operational Combined Uniform Single Reports). These filings provide regulators with detailed information about a firm’s balance sheet, capital calculations, and operational activities.

FOCUS reports typically include:

Net capital calculations under Rule 15c3-1

Balance sheet and income statement information

Aggregate indebtedness and other regulatory ratios

Operational data related to the firm’s business activities

Most firms file FOCUS reports monthly or quarterly, depending on their regulatory classification. Regulators review these reports to monitor compliance with the SEC Net Capital Rule and other financial responsibility requirements.

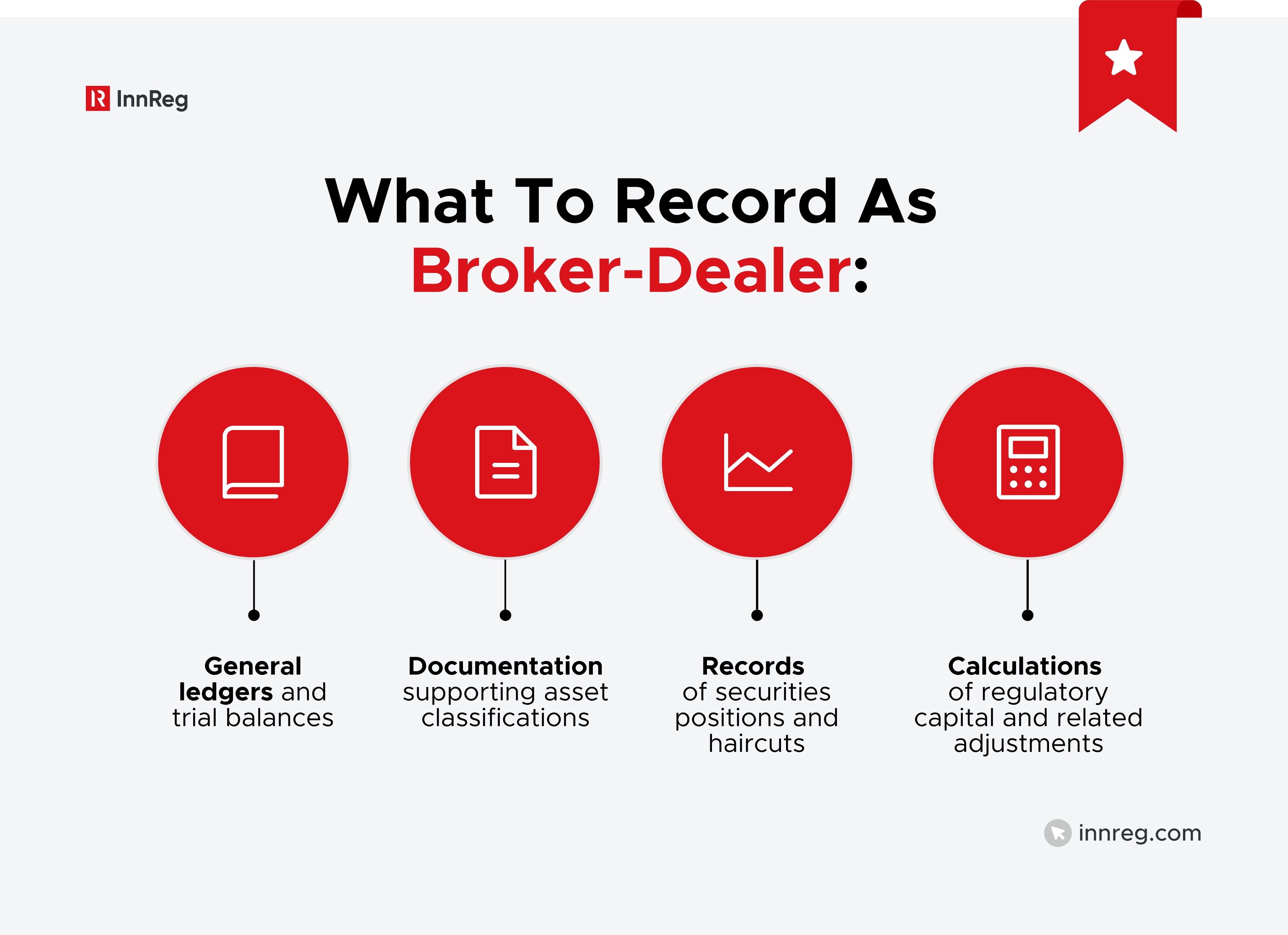

Books and Records Requirements

Broker-dealers must also maintain detailed financial records that support their net capital calculations. The SEC’s Broker-Dealer Books and Records Rules mandate this requirement. These records allow regulators and examiners to verify how a firm calculates its net capital position.

Daily and Monthly Net Capital Monitoring

Although formal filings occur periodically, most broker-dealers monitor net capital on a daily or near-daily basis. Market movements, trading activity, or operational changes can affect capital levels quickly.

Firms typically implement internal monitoring processes that include:

Daily or weekly net capital calculations

Alerts when capital approaches early warning thresholds

Internal escalation procedures for capital changes

For fintech broker-dealers operating in fast-moving trading environments, this monitoring process often becomes part of the firm’s operational infrastructure. Compliance, finance, and operations teams typically coordinate to track capital levels and respond to changes in real time.

Areas of Confusion Around Rule 15c3-1

Even experienced founders and compliance teams sometimes misinterpret how the SEC Net Capital Rule works in practice. The rule is technical, and several concepts used in the calculation are often confused with more familiar financial metrics.

Let’s clarify the top two confusions around the SEC Net Capital Rule:

Net Capital vs. Liquidity

Net capital is closely related to liquidity, but the two concepts are not identical. Liquidity generally refers to how quickly a firm can convert assets into cash to meet obligations.

Regulatory net capital focuses on the same principle but applies specific deductions and adjustments required by Rule 15c3-1. Assets that appear liquid in normal accounting may still be excluded from the regulatory capital calculation.

Liquidity | Net Capital |

|---|---|

Ability to convert assets into cash quickly | Regulatory capital calculated under Rule 15c3-1 |

General financial measure used across industries | Used by regulators to evaluate broker-dealer financial stability |

Broad assessment of cash availability | Certain assets must be deducted as non-allowable |

Not a formal regulatory metric | Key compliance metric under the SEC Net Capital Rule |

Net Capital vs. Minimum Equity

Another common point of confusion involves the difference between regulatory net capital and a firm’s accounting equity.

Equity reflects the firm’s total assets minus liabilities under standard accounting rules. Net capital, however, adjusts this figure to account for liquidity and market risk.

Equity | Net Capital |

|---|---|

Total assets minus liabilities | Adjusted regulatory capital after deductions and haircuts |

Reported on the balance sheet | Calculated using Rule 15c3-1 methodology |

Includes all balance sheet assets | Non-allowable assets are removed |

General financial measure | Determines compliance with SEC Net Capital Rule requirements |

Because of these adjustments, a broker-dealer may report substantial equity while still operating close to its regulatory capital threshold. For firms subject to Rule 15c3-1, net capital becomes the critical measure regulators monitor when evaluating financial responsibility.

Practical Steps for Managing SEC Net Capital Rule Compliance

Maintaining compliance with the SEC Net Capital Rule requires more than performing periodic calculations. Broker-dealers must integrate capital monitoring into daily financial operations and internal controls.

For many firms, net capital management becomes a coordinated effort between finance, compliance, and operations teams. Systems, workflows, and escalation procedures all play a role in keeping regulatory capital within acceptable levels.

The following practices are commonly used to manage Rule 15c3-1 compliance:

Establishing Net Capital Monitoring Procedures

Most broker-dealers implement structured procedures for calculating and monitoring regulatory capital. Daily or near-daily net capital calculations are common, particularly for firms with active trading operations.

These monitoring processes typically include:

Regular net capital calculations using updated financial data

Monitoring for early warning thresholds under Rule 15c3-1

Reviews of asset classifications and securities haircuts

Internal reporting of capital levels to management

Firms with proprietary trading activity or volatile balance sheets often monitor capital more frequently.

Internal Controls and Escalation Policies

Internal controls help firms respond quickly when capital levels change. These controls define how capital is calculated, who reviews the calculations, and what actions are taken when thresholds are approached. These processes help firms identify issues early and prevent unexpected capital deficiencies.

Working With Compliance and Finance Teams

Net capital compliance typically requires close coordination between multiple teams. Finance teams manage balance sheet data, while compliance teams interpret regulatory requirements and monitor reporting obligations.

This can create challenges when the business is growing quickly or when new features change the firm’s capital profile. Launching new trading capabilities, introducing custody features, or changing clearing arrangements can all affect net capital requirements.

This is where many firms rely on specialized compliance partners. InnReg frequently operates as an outsourced compliance department or as an extension of internal teams, helping broker-dealers manage the operational side of regulatory capital.

Working with InnReg means getting help to:

Implement structured processes for net capital monitoring

Review capital calculations and asset classifications

Coordinate compliance reporting and regulatory filings

Evaluate how new business models affect capital requirements

Because InnReg focuses on fintech broker-dealers and other innovative financial firms, the team is often involved when companies launch new brokerage models or integrate new trading features. The goal is practical implementation.

In many cases, this approach allows firms to access a broader compliance team without building a full internal department, while maintaining structured oversight of Rule 15c3-1 requirements.

Talk to one of our experts today →

—

The SEC Net Capital Rule (Rule 15c3-1) is one of the core financial responsibility requirements governing US broker-dealers. It requires firms to maintain a minimum level of liquid regulatory capital and to calculate that capital using a structured methodology that accounts for asset liquidity and market risk.

For fintech broker-dealers, these requirements often become an important design constraint. Decisions around custody, clearing arrangements, trading activity, and proprietary positions can directly affect capital requirements under Rule 15c3-1.

For firms navigating these issues, specialized regulatory expertise can make a meaningful difference. InnReg works with broker-dealers, fintech platforms, and other regulated financial firms to design and operate practical compliance programs, including support for broker-dealer registration, regulatory capital monitoring, and ongoing compliance operations.

Bruno is a Principal Compliance Officer at InnReg advising fintech clients across broker-dealer, RIA, and money transmitter verticals. He brings prior experience at Santander Brasil and Passfolio, with expertise in regulatory strategy, supervisory systems, and compliance execution. He holds FINRA Series 4, 7, 24, 63, and 99 licenses.

How Can InnReg Help?

InnReg is a global regulatory compliance and operations consulting team serving financial services companies since 2013.

We are especially effective at launching and scaling fintechs with innovative compliance strategies and delivering cost-effective managed services, assisted by proprietary regtech solutions.

If you need help with broker-dealer compliance, reach out to our regulatory experts today:

Related Articles

Featured LinkedIn Posts