RIA Innovation in 2026: The Trends Redefining Investment Advisors

RIA firms today face a steady stream of innovation across technology, client expectations, and regulations.

Staying ahead means understanding how these shifts are shaping the next generation of advisory models, and where meaningful change is already happening.

This article breaks down the most important developments defining the future of registered investment advisors, from AI-native workflows to tokenized liquidity solutions, and from embedded advice to real-time compliance systems.

At InnReg, we help RIAs navigate complex regulatory changes and build practical compliance programs. From registration and licensing to operational oversight, our team specializes in working with innovative, fast-moving firms.

The New RIA Business Models Emerging in 2026

RIA models are not simply improving at the margins. They are undergoing a structural evolution. The firms gaining traction today are not defined by marketing trends or surface-level design. They are distinguished by real changes in how advice is delivered, governed, and monetized.

The sections below outline seven of the most relevant RIA business model innovations, with a focus on what they are and why they matter:

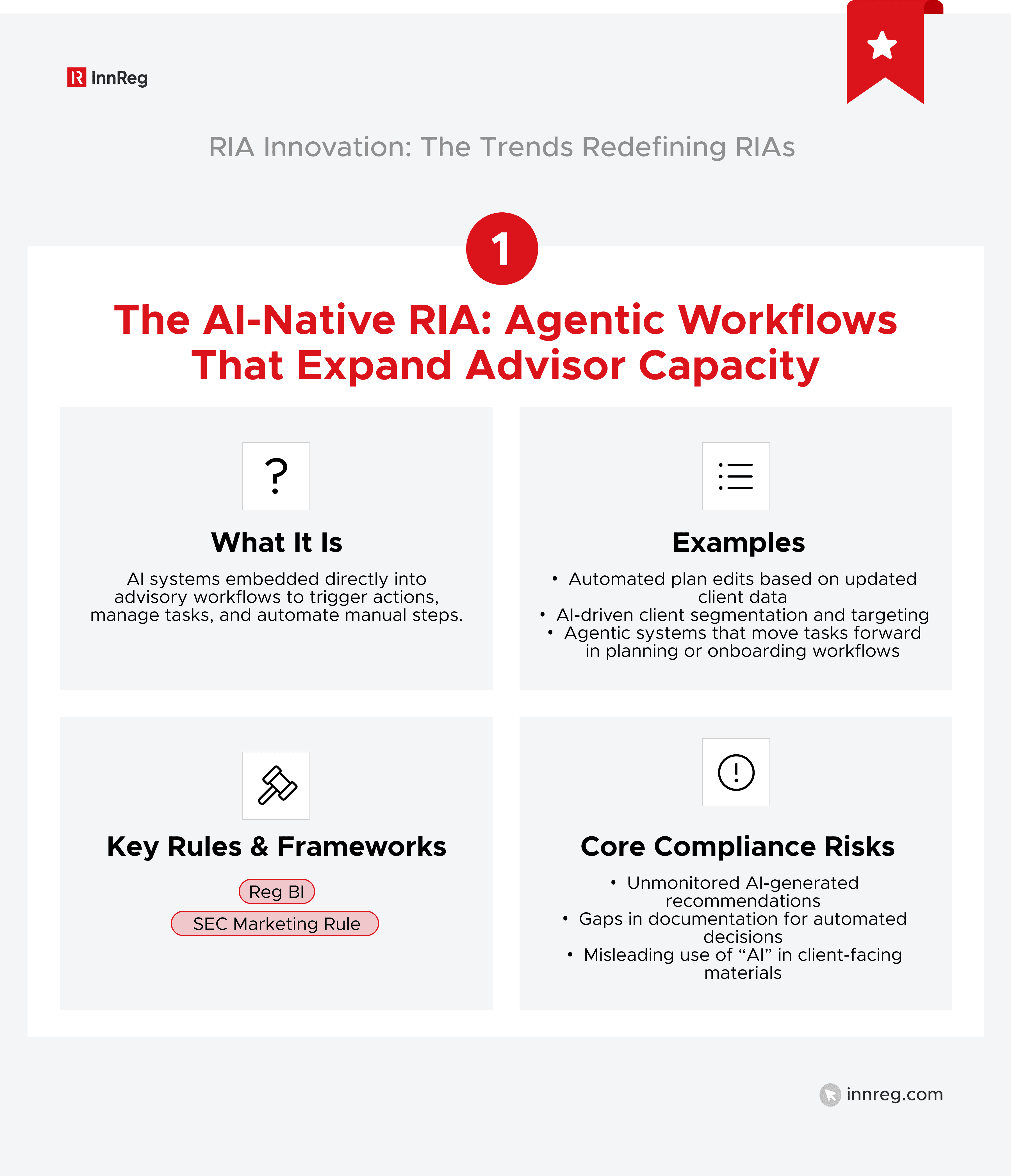

1. The AI-Native RIA: Agentic Workflows That Expand Advisor Capacity

In the past, AI tools were used around the edges: writing messages, pulling summaries, or managing reminders. That has changed.

Today’s agentic systems are being placed directly inside the business logic. They trigger actions, move tasks forward, and handle repetitive steps that previously tied up associate advisors.

AI adoption is affecting more than just tools. It is actively changing the team structure. Work that once required staff involvement, such as plan edits or internal routing, is now automated in many cases. Firms are adapting by rethinking associate roles, shifting focus toward oversight and exception handling.

This shift brings compliance into sharper focus. Tools that generate advice, automate client communications, or flag financial risks still require oversight.

Based on InnReg’s experience of working with 100+ fintechs, Regly’s Marketing Compliance module helps RIAs review and flag potential risks using AI-powered tools →

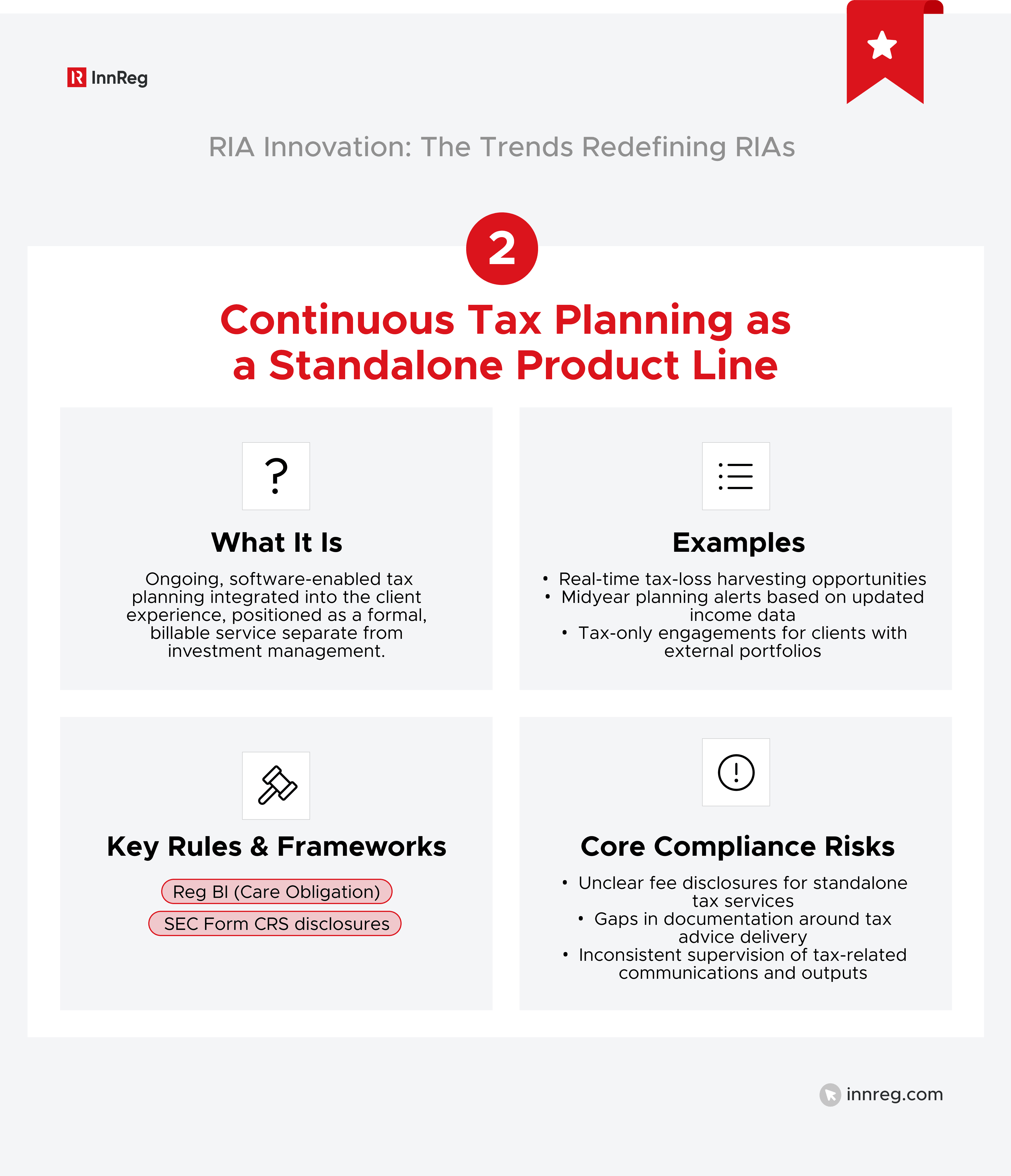

2. Continuous Tax Planning as a Standalone Product Line

Real-time tax work is turning into a formal service line inside modern RIA firms.

What used to be handled once a year is now baked into the regular client experience. Tools are pulling live tax data, spotting planning opportunities midyear, and supporting actions.

Firms are beginning to charge for this directly, offering tax-only services or packaging it separately from investment management.

It opens the door to working with clients who value tax guidance but are not ready to move their investments, while at the same time requiring additional structure inside the RIA. Tasks related to documentation, handoffs, etc., need clear ownership.

Developed based on InnRegs 10+ years of industry experience, Regly Compliance helps RIAs centralize data and manage ownership →

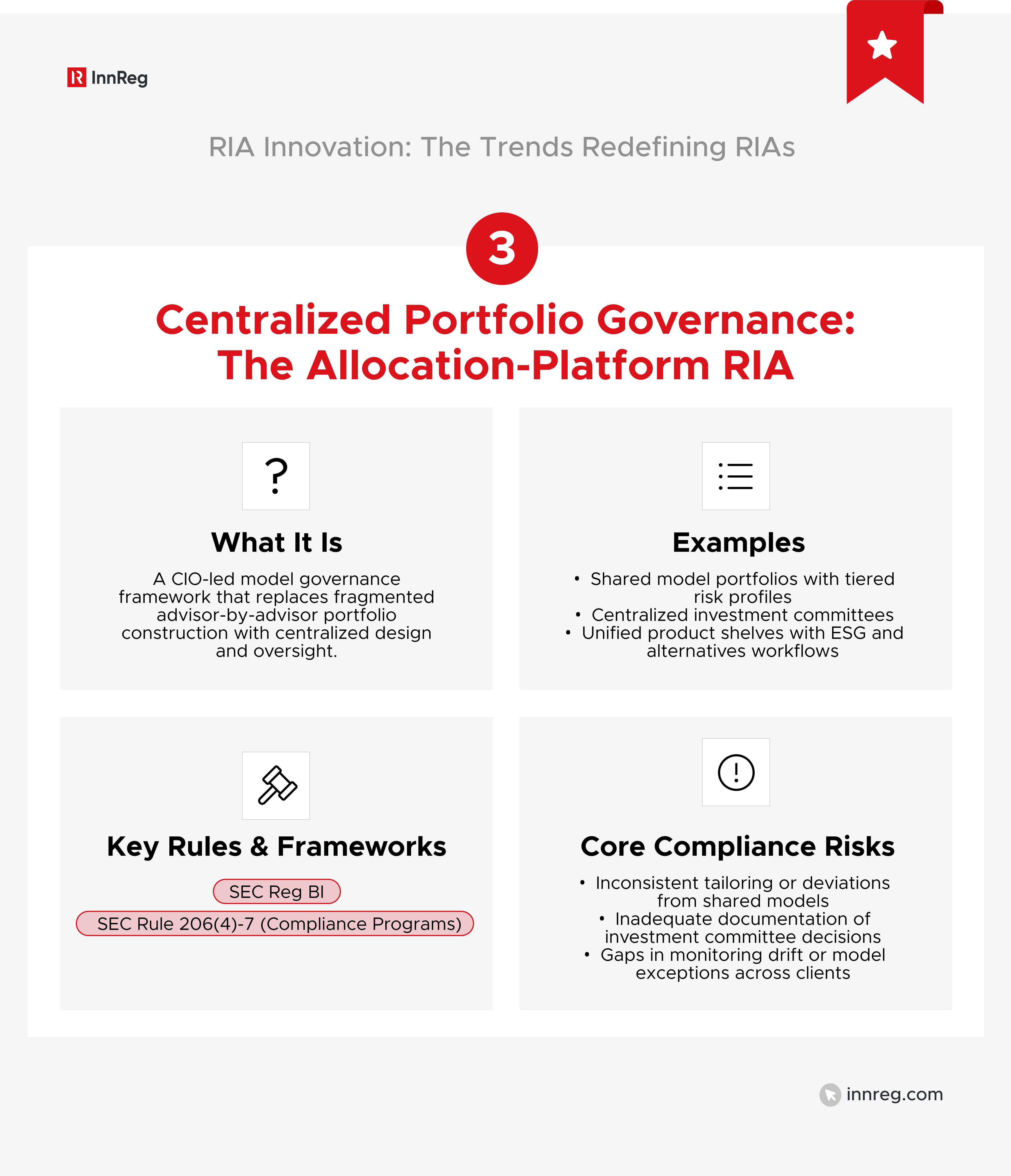

3. The Allocation-Platform RIA (CIO-Led, Centralized Portfolio Governance)

RIAs are moving away from fragmented investment decision-making toward centralized governance and shared models.

In many firms, every advisor has historically built portfolios independently. That approach is starting to shift. More RIAs are now organizing around a centralized investment committee, led by a CIO or similar role, that owns portfolio design and model governance.

This platform structure allows firms to define investment philosophy once, then apply it consistently across all clients. Advisors still tailor based on client goals, but the base framework, risk tiers, asset mixes, and product shelves are shared.

For fast-growing firms, this solves multiple problems at once. It reduces operational risk, simplifies compliance, and makes it easier to roll out updates across hundreds or thousands of accounts. It also makes due diligence more repeatable, especially in areas such as ESG screening and alternative assets.

Oversight becomes more manageable, too. Centralized portfolios are easier to monitor, document, and audit.

For RIAs working with InnReg, we have helped build supervisory processes around these platforms, making it easier to track drift, flag exceptions, and maintain model discipline without slowing down the advisory workflow.

4. Private Markets Operations as a Core Capability, Not an Alternative Add-On

Previously, private fund exposure was ad hoc and sourced at the advisor’s discretion, meaning that it was usually dealt with on a case-by-case basis. However, as these assets increasingly move into the core portfolio, RIAs are under pressure to standardize how they manage and supervise them.

For this reason, an increasing number of RIAs are now establishing repeatable workflows for sourcing, onboarding, and performance tracking. Formats such as interval funds and semi-liquid structures are becoming more common because they make it easier for investors to plan around investor access.

This is an operational shift. RIAs are adopting tools to model cash flows, manage lockup periods, and integrate private holdings into sleeve-based portfolios. That keeps illiquid exposure aligned with broader goals without swamping advisor bandwidth.

Supervision has to keep pace. As these assets move from edge cases to the mainstream, review, documentation, and exception-tracking processes must scale accordingly, especially as regulators monitor how retail investors are exposed to private markets.

Learn how InnReg helps RIAs establish clear supervision processes →

5. Tokenized Cash and Next-Generation Liquidity Design

Tokenized money market funds and real-world asset wrappers are increasingly playing a role in advisory portfolios.

These are regulated, short-duration instruments issued by well-known fund managers. The appeal is operational, as RIAs use them to speed up settlement, improve collateral flexibility, and offer intraday liquidity in ways traditional products cannot.

This design is especially useful for RIAs working across multiple custodians, platforms, or jurisdictions: a tokenized wrapper allows the same asset to settle faster or be used more efficiently across different systems. That reduces wait times and manual intervention.

Advisory teams do not need to build custom tech to adopt this, as most tokenized cash products work through standard fund infrastructure and are available through approved channels. However, they do require careful review of custody models, control processes, and disclosures.

Read our article to learn more about tokenization →

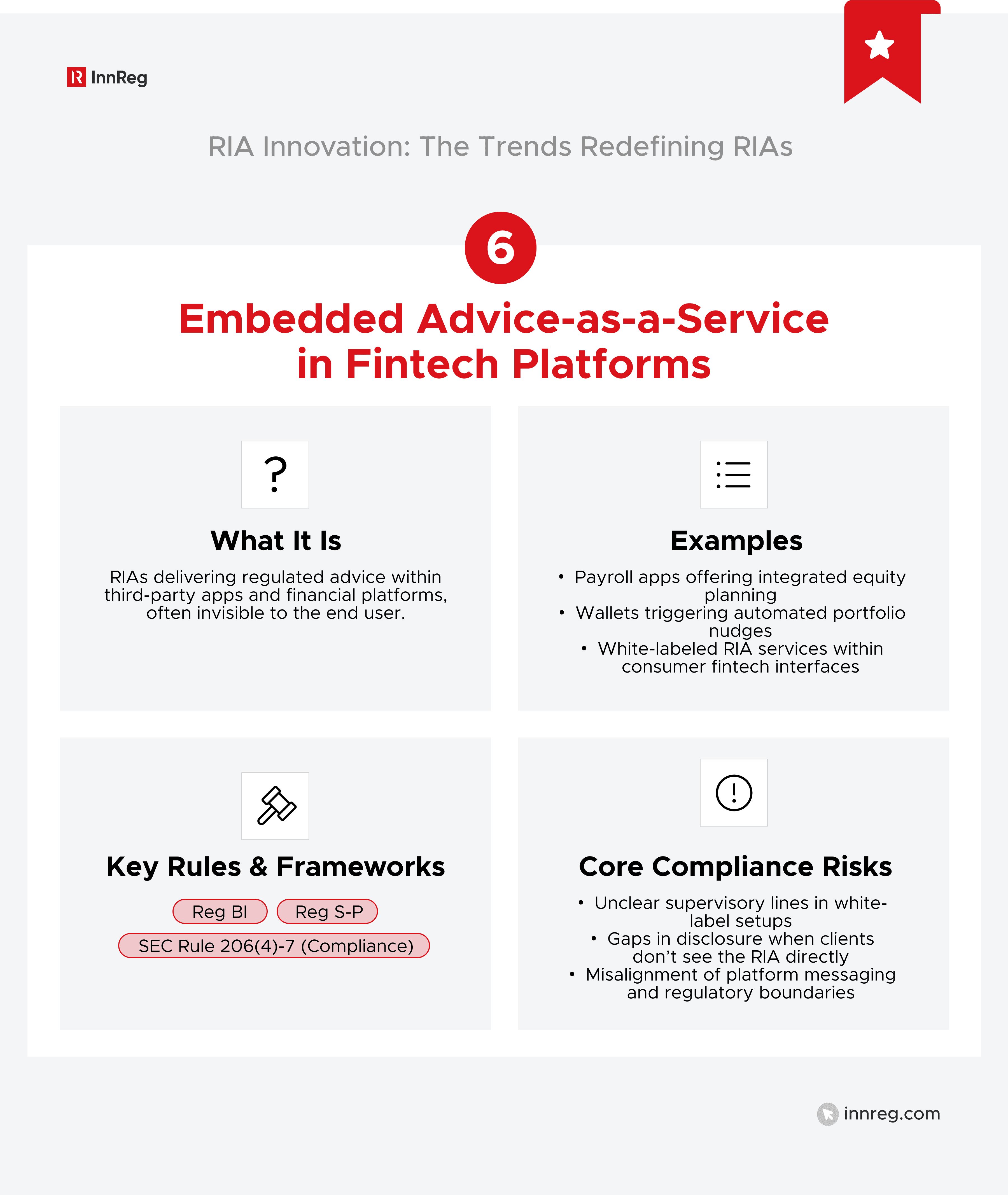

6. Embedded Advice and Advice-as-a-Service Inside Fintech Ecosystems

RIAs are increasingly serving as the regulated advice layer within other platforms, not just their own storefronts. This means that an increasing number of RIAs are offering their services to already existing financial platforms and their user bases.

Fintech products are integrating wealth management services directly into their ecosystems, whether through a payroll app that offers equity planning or a wallet that provides portfolio nudges. In these models, the RIA is invisible to the end client but critical to the product experience.

This approach flips the traditional model. Instead of building a brand and acquiring clients directly, RIAs are embedded into third-party platforms where distribution, data, and user engagement already exist. Advice becomes a service, not a destination.

This setup significantly changes the operation model: instead of attempting to attract clients directly, when relying on these models, RIAs now need to integrate within an existing ecosystem.

This, however, brings new challenges. When the advice is embedded, RIAs need to rethink disclosures, supervision, and communications. This holds especially true when working with white-label and API-based models.

See also:

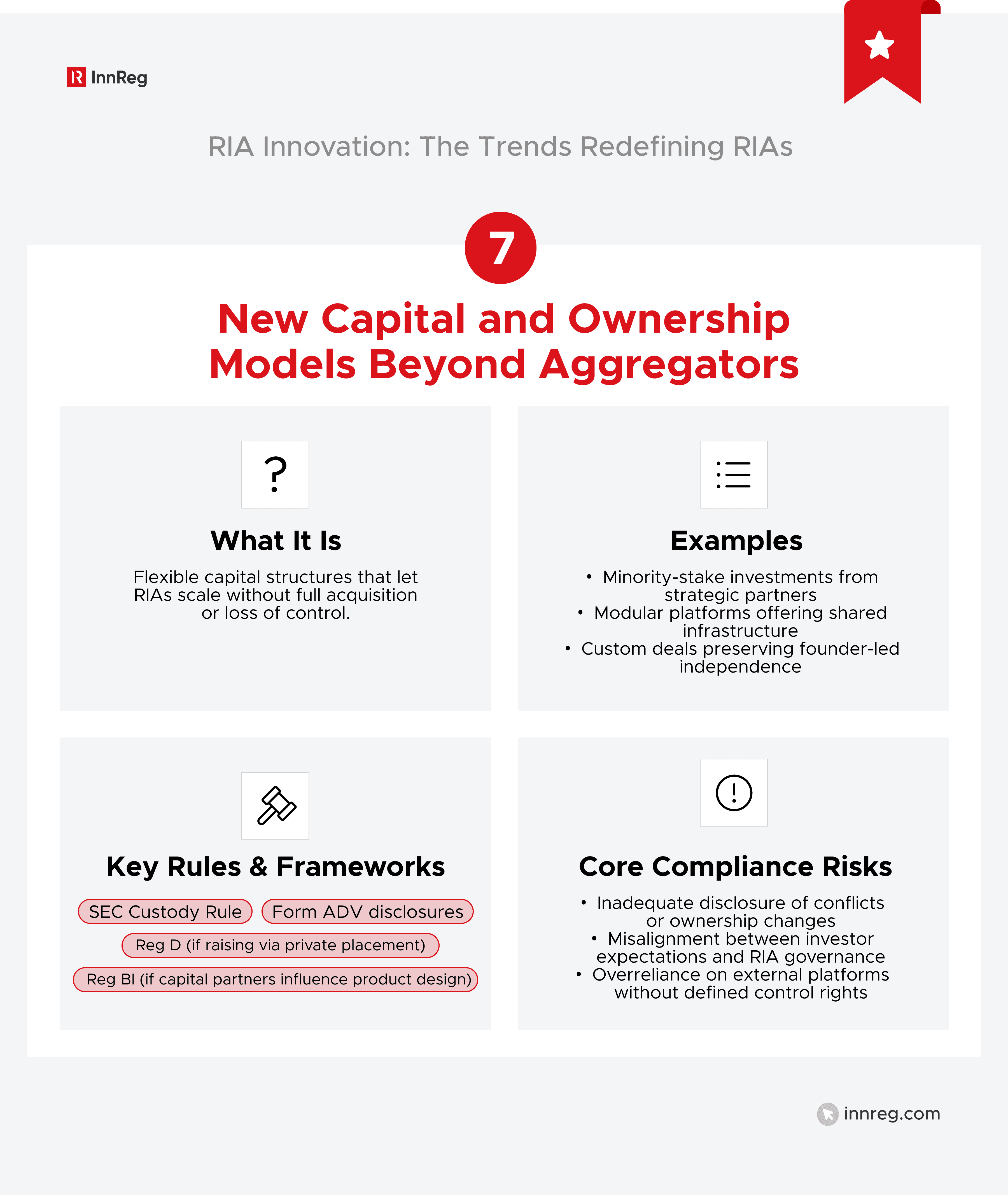

7. New Capital and Ownership Models Beyond the Aggregator Playbook

Firms are moving away from all-or-nothing roll-ups. They want capital without giving up control.

Many RIAs no longer view full acquisition by a mega-platform as the only way to scale. Instead, they are exploring minority-stake partnerships, modular platforms, and customized support structures that let them grow on their own terms.

The primary appeal of these models is the flexibility they provide. For example, a firm might sell 30% to gain growth capital and infrastructure support, without handing over decision-making.

This shift is reshaping the advisor landscape. There is more variety in how firms partner, raise capital, and build long-term enterprise value, especially among founder-led RIAs that want to keep their identity while benefiting from shared resources.

Innovation | Impact |

|---|---|

AI-Native RIA | AI agents trigger tasks, increase capacity, and consequently reshape team structures. |

Continuous Tax Planning | Tax services are increasingly offered as a standalone, year-round product. |

Allocation-Platform RIA | Centralized portfolio design and oversight through CIO-led governance. |

Private Markets as Core Capability | Standardized workflows and tools for managing private assets. |

Tokenized Cash and Liquidity Design | Faster settlement and flexibility through regulated digital wrappers. |

Embedded Advice-as-a-Service | RIAs integrated into fintech platforms, enabling white-label delivery. |

New Capital and Ownership Models | Minority-stake and modular models replace full acquisitions. |

Need help with RIA compliance?

Fill out the form below and our experts will get back to you.

2026 RIA Trends Fintechs Should Watch

Not every shift is client-facing. That does not make it less important. As regulations tighten and infrastructure matures, RIAs are rebuilding the core mechanics of how they operate.

1. API-First Custody and the Custody Stack Wars

Custodians are no longer just account holders. They are becoming infrastructure providers. Modern platforms are exposing core functions like onboarding, ACATS transfers, holdings access, and document delivery through publicly documented APIs.

This shift matters because it allows RIAs to build differentiated client experiences on top of custody layers. Rather than being locked into prebuilt portals, firms can integrate planning tools, performance views, and reporting dashboards directly into the custodial flow.

This unlocks new partnership models for fintech teams. As custody is becoming composable, firms can now plug regulated assets into broader ecosystems, wallets, apps, and CRMs, with mitigated risk of losing data visibility or compliance control.

2. The “Unified Client Brain:” Data Foundations as Strategy

Modern RIAs are increasingly treating data as a strategic asset.

Client information, once spread across systems, is being pulled into centralized data layers. These include CRM notes, planning details, custodial records, and message history.

Firms that do this well reduce internal friction and scale faster. Compliance, operations, and planning use the same client data, which decreases data siloing and enables RIAs to run more efficiently and scale faster.

For fintech teams, this reinforces the value of strong integration points and well-structured APIs. RIAs don’t just need tools; they need tools that talk to each other.

3. Real-Time Compliance Architecture Embedded in Advisory Workflows

Compliance is becoming a live part of the advisory process.

Modern RIAs are adopting tools that embed controls into everyday workflows. That includes automated marketing review, AI-based communication flagging, pre-trade oversight, and vendor monitoring, all triggered in real time, not in post-event audits.

Based on InnReg’s experience of working with 100+ fintechs, Regly Compliance provides AI-powered marketing and communications reviews, and a vendor management module →

In addition to reducing delays and strengthening consistency, this shift helps compliance officers spot gaps earlier and spend less time chasing down documentation. When rules are built into the process, not layered on top, advisory teams can operate more efficiently.

4. Privacy and Incident Response as Table Stakes (Reg S-P’s 30-Day Clock)

RIAs are being pushed to treat data protection and incident response as live operations, not paperwork exercises.

The SEC’s Reg S-P amendments impose a 30-day breach notification clock and stronger expectations around vendor oversight. That means RIAs must be able to detect, contain, and disclose incidents fast with clear logs, procedures, and role ownership.

It is not just about having a policy binder. RIAs now need working infrastructure: audit trails, incident playbooks, vendor monitoring dashboards, and integrated notification workflows. Without them, firms risk both regulatory exposure and reputational harm.

Read our guide to learn more about Reg S-P →

5. Adviser AML: The Deadline Moved, But the Direction Didn’t

Although the AML rule for RIAs is not yet in effect, its impact is already being felt.

FinCEN pushed the compliance date to 2028, but many are using the extra time to strengthen their AML programs. This is especially true for those handling direct accounts or complex flows involving private funds and digital assets.

This is not only about preparing for the future rule, but also about aligning with bank-level expectations when dealing with transfers, private assets, or tokenized products. As a consequence, the risk-based customer due diligence, suspicious activity monitoring, and ownership screening are becoming part of the baseline.

Fintech RIAs are especially exposed. The more automation or embedded flows you use, the more intentional your AML controls need to be.

See also:

6. The New SEC Posture on AI

The SEC may have pulled back on proposed AI-specific rules, but that does not mean enforcement has slowed down.

Firms using AI in client-facing contexts, especially for recommendations or personalization, are being asked tough questions about transparency, oversight, and testing.

RIAs cannot treat AI as a black box. They need to document how outputs are generated, how they are reviewed, and where human judgment fits in. Controls around model drift, hallucination, and bias are becoming standard parts of the compliance conversation.

The direction is clear: innovation must stand up to existing rules and exams, not just product demos.

Why These RIA Trends Matter Now

RIA business models are shifting in ways that affect strategy, structure, and risk. What was once incremental, adding tech and optimizing workflows, is now foundational. AI systems are making decisions, compliance is embedded, and custody is infrastructure. These are not back-office changes. They reshape how firms grow, supervise, and compete.

Founders and executives who wait risk falling behind platforms that already run faster, cleaner, and with better unit economics.

Tarik is a Principal Compliance Consultant at InnReg with over 5 years of experience advising fintech clients across broker-dealer, RIA, and money transmitter verticals. He holds FINRA Series 3, 7, 24, 57, 63, 79, and 99 licenses, with expertise in regulatory strategy, supervisory systems, and compliance roadmap implementation.

How Can InnReg Help?

InnReg is a global regulatory compliance and operations consulting team serving financial services companies since 2013.

We are especially effective at launching and scaling fintechs with innovative compliance strategies and delivering cost-effective managed services, assisted by proprietary regtech solutions.

If you need help with RIA compliance, reach out to our regulatory experts today:

Related Articles

Featured LinkedIn Posts