Series 7 License: What It Covers and Who Needs It

The Series 7 license is a foundational requirement for anyone looking to sell securities in the US. This FINRA license is a regulatory milestone that applies to brokers working at traditional firms, fintech startups, and other types of broker-dealers.

If your business involves facilitating trades or offering access to securities, someone on your team likely needs this license, or you need a clear plan for outsourcing that function. But the Series 7 isn’t just a box to check. It determines what your representatives can legally do, which regulators you’ll answer to, and how your compliance program needs to be structured.

Many founders misunderstand where this license applies, assume it’s optional in early stages, or overlook the ongoing obligations tied to it. This article breaks down exactly what the Series 7 covers, who needs it, how to obtain it, and what pitfalls fintech teams often face.

At InnReg, we support broker-dealers and fintechs with licensing and compliance operations. From Series 7 registration and related FINRA requirements to building supervisory procedures and ongoing compliance support, our team helps firms structure their compliance programs. Contact us to learn more.

What Is the Series 7 License?

Formally known as the General Securities Representative license, the Series 7 license qualifies individuals to sell a broad range of securities products in the United States. In fact, it's required for most brokerage roles involving direct client interaction or execution of trades.

The Series 7 is not a standalone certification. To acquire it, individuals must also pass the Securities Industry Essentials (SIE) exam and be sponsored by a FINRA-member firm. Once registered, a Series 7 representative is subject to FINRA rules, ongoing reporting obligations, and continuing education requirements.

Regulatory Bodies Behind the Series 7

The Series 7 license is administered by the Financial Industry Regulatory Authority (FINRA). FINRA is a self-regulatory organization overseen by the US Securities and Exchange Commission (SEC).

While FINRA handles the exam and licensing process, it operates under the SEC’s authority and enforces federal securities laws within its jurisdiction, making these two different entities with differing responsibilities.

For state-level requirements, the North American Securities Administrators Association (NASAA) plays a role. NASAA develops the Series 63, 65, and 66 exams that are often required in conjunction with the Series 7, depending on your business model and where your clients are located.

Here’s how responsibility breaks down:

Regulator | Role in Series 7 Licensing |

|---|---|

FINRA | Develops and administers the Series 7 exam; licenses registered representatives; enforces rules for broker-dealers |

SEC | Provides federal oversight of FINRA and the securities markets; enforces broader securities laws |

NASAA | Oversees state-level securities regulation; sets content for exams like Series 63 that often accompany Series 7 |

For fintech firms operating across jurisdictions, understanding these regulatory boundaries is critical.

What the Series 7 Exam Covers

The Series 7 exam tests whether a candidate is qualified to work as a general securities representative. That includes not just product knowledge, but also regulatory procedures, ethics, and customer account handling. The scope is broad because the license grants wide authority over securities sales.

FINRA organizes the exam into four functional areas:

Seeking business for the broker-dealer from customers and potential customers

Opening accounts after obtaining and evaluating the customer's financial profile and investment objectives

Providing customers with information about investments, making recommendations, transferring assets, and maintaining records

Obtaining and verifying customer purchase and sales instructions; processing transactions

The third section is focused on customer interaction and investment recommendations, making up nearly three-quarters of the exam.

Candidates must also pass the Securities Industry Essentials (SIE) exam separately, which covers foundational knowledge across product types, market structure, and prohibited practices. The SIE can be taken without firm sponsorship, but the Series 7 requires it.

A licensed individual must be able to explain products, take orders, and comply with FINRA’s standards, especially around suitability and Regulation Best Interest. Here’s an overview of the Series 7 exam format:

Who Needs the Series 7 (and Who Doesn’t)

The Series 7 license is required for individuals who solicit, execute, or are compensated for securities transactions on behalf of a broker-dealer. If someone is engaging directly with clients to recommend or process trades in stocks, bonds, ETFs, mutual funds, or options, they need this license.

Here’s a detailed list of roles where the Series 7 is typically required:

Retail brokers and financial advisors employed by broker-dealers

Institutional sales reps handling large-scale securities transactions

Fintech product specialists who recommend or facilitate stock, bond, or ETF purchases for users

Customer-facing roles at fintechs or broker-dealers who help clients with investment decisions or execute orders

Registered reps who sell complex securities products such as options, structured notes, REITs, or private placements

Inside sales or relationship managers who are paid based on securities-related activity

Client-facing representatives at digital advisory firms who recommend securities, place trades, or take trading instructions, especially in hybrid broker-dealer/RIA models

The rule of thumb: if a person is recommending a security, taking trade instructions, or getting paid in connection with securities sales, they need to be licensed. That licensing most often starts with the Series 7.

By contrast, here are roles that typically don’t require Series 7:

Back-office professionals (e.g., operations, clearing, settlements) who don’t interact with clients or handle trades

Marketing or communications staff, unless they make product recommendations or solicit trades

Software engineers, UX designers, and product managers, unless they directly facilitate or solicit securities transactions

Investment advisor representatives (IARs) who only provide advisory services and do not sell securities (typically need Series 65 or Series 66 instead)

Legal counsel (though they may need to understand licensing rules, they don’t need Series 7 unless performing rep functions)

Remember, the license is tied to activity, not job title. If the activity triggers broker-dealer status under SEC and FINRA rules, the Series 7 becomes non-negotiable.

What You Can and Can’t Do With a Series 7 License

A Series 7 license is the most comprehensive license for general securities sales and is often considered the baseline for working at a broker-dealer.

With a Series 7 license, you can:

Solicit and execute trades in individual stocks and bonds

Sell mutual funds, ETFs, and closed-end funds

Offer options and other derivatives

Solicit municipal and government securities

Market and sell direct participation programs (DPPs)

Engage in private placements of securities

Interact directly with retail and institutional clients about investment recommendations

Open new customer accounts and manage account maintenance

This level of authority allows firms to provide full-service brokerage offerings. That includes handling trades, discussing strategy, and managing complex investment portfolios.

However, the Series 7 does not cover everything. You cannot:

Sell commodities or futures contracts (requires a Series 3 license)

Provide fee-based investment advice without additional licensing (typically Series 65 or Series 66)

Supervise other representatives or act as a principal (requires Series 24)

Sell life insurance or annuities unless licensed under state insurance regulations

Sell real estate, unless separately licensed by a state real estate board

For fintech companies, these distinctions matter. Your compliance obligations may be split across multiple regulatory frameworks, and for many firms, the Series 7 is an early and significant licensing step for the securities side.

How to Get the Series 7 License

The process of getting a Series 7 license is structured around regulatory approvals, firm sponsorship, and prerequisite exams. For founders or compliance teams planning ahead, knowing the complete path helps avoid delays or rework.

Here’s how the process typically unfolds:

Step 1: Get Hired or Sponsored by a FINRA-Member Firm

You can’t register for the Series 7 exam on your own. FINRA requires candidates to be associated with a member firm, which submits Form U4 (Uniform Application for Securities Industry Registration) on behalf of the individual. This step formally initiates your application for registration and triggers a background check.

See also:

Step 2: Pass the Securities Industry Essentials (SIE) Exam

Before you can take the Series 7, you need to pass the SIE exam. This is a 75-question test covering foundational securities knowledge: product types, markets, regulatory bodies, and prohibited practices.

You don’t need firm sponsorship to take the SIE, so many candidates complete it in advance to boost their employability. Furthermore, your SIE results remain valid for four years.

The Sponsorship Requirement

To take the Series 7 exam, candidates must be sponsored by a FINRA-member firm. This is a regulatory requirement since FINRA does not allow individuals to register for the exam on their own.

The sponsoring firm submits Form U4, which starts the registration process and triggers a background check. Until that form is filed and approved, the candidate can’t schedule the Series 7 exam, regardless of whether they’ve already passed the SIE.

This applies to full-time employees, contractors, and anyone performing registered representative functions. The license isn’t independent, and it’s tied to the firm. If a registered individual leaves the firm, the license becomes inactive and must be reactivated through a new sponsor.

Need help with broker-dealer compliance?

Fill out the form below and our experts will get back to you.

Step 3: Prepare for the Series 7 Exam

The Series 7 is detailed and product-heavy. Many candidates use commercial prep courses, practice exams, or in-house training programs.

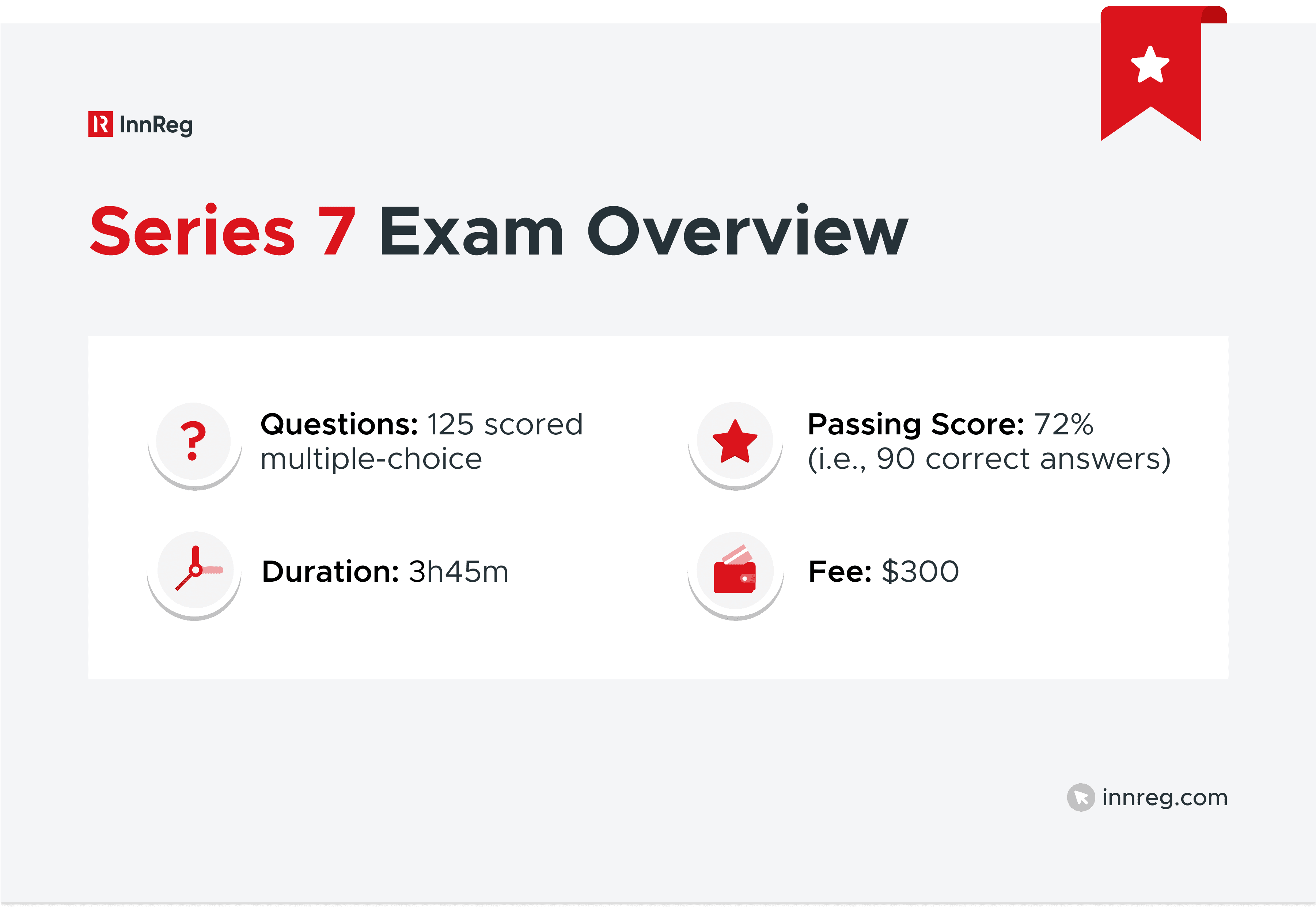

Format: 125 multiple-choice questions

Duration: 3 hours, 45 minutes

Passing score: 72%

Exam fee: $300

Step 4: Take the Series 7 Exam Through FINRA’s Platform

Once your sponsoring firm files Form U4 and you're approved, you’ll receive instructions to schedule the exam through Prometric (FINRA’s test administrator). You can take it at a testing center, or in limited circumstances, online.

Step 5: Maintain Active Registration

After passing, your Series 7 registration becomes active as long as you remain associated with your sponsoring firm. If you leave, that registration ends, and a multi-year reactivation window begins. Beyond that, you’ll need to retake the exam unless you qualify for a waiver.

It’s very common for early-stage fintechs without in-house licensed personnel to work with outsourced compliance partners. InnReg works with fintech firms navigating these exact scenarios from scratch. For companies moving fast or testing new models, outsourcing this function can help mitigate regulatory risks and help avoid early missteps.

Series 7 vs. Other Securities Licenses

The Series 7 license is broad, but it doesn’t cover everything. Depending on your business model and the types of services you offer, other licenses may also be required. Understanding how Series 7 compares to related registrations helps prevent gaps in coverage and avoid regulatory risk.

Series 7 vs. Series 63, 65, and 66

Often, professionals are confused between the Series 7 license and Series 63, 65, and 66. Here’s a clear difference between these securities licenses:

License | Purpose | Common Use Cases |

|---|---|---|

Series 7 | Authorizes the sale of most securities | Required for registered reps at broker-dealers |

Series 63 | Covers state-level securities law | Required by most states to solicit clients |

Series 65 | Allows giving investment advice for a fee | Required for investment advisor representatives (IARs) |

Series 66 | Combines 63 and 65 for Series 7 holders | Used by dual registrants working as both reps and advisors |

Series 7 vs. Series 24 (Supervisor-Level Licensing)

The Series 7 is for representatives. If someone supervises representatives or is responsible for compliance oversight at a broker-dealer, they’ll need a principal-level license, which is typically the Series 24. Series 24 is required for:

Chief Compliance Officers for broker-dealers

Supervising sales and trading activities

Approving new accounts

Overseeing advertising and marketing

Managing regulatory reporting obligations

Fintechs building or acquiring a broker-dealer must account for these supervisory roles in their org charts and compliance plans.

See also:

When You Need More Than One License

Multi-product firms, hybrid BD/RIA models, and firms operating across multiple states often require reps to hold more than one license. For example:

A rep recommending mutual funds in all 50 states may need Series 7 and 63

A hybrid advisor rep giving portfolio advice and selling securities may need Series 7 and 66

A supervisor overseeing other reps will need Series 7 and 24

Licensing in the US isn’t modular by accident and instead reflects the layered nature of the country’s securities regulation. Matching the right credentials to the right roles is part of building a defensible compliance structure.

Common Compliance Challenges Tied to Series 7

Even when a company understands that the Series 7 is required, execution often breaks down in the details. Gaps in licensing, oversight, or registration can expose firms to enforcement risk, especially in fast-moving fintech environments.

Below are the most common compliance challenges related to the Series 7 license:

Registration Gaps and Lapsed Licenses

A Series 7 license is only active while the rep is associated with a FINRA-member firm. If that association ends, the license becomes inactive. The rep has two years to affiliate with a new firm before needing to retake the exam, or up to five years if participating in the MQP program.

This becomes a risk in cases of turnover, restructuring, or using contractors without clear registration paths. Many early-stage teams don’t realize that a rep’s license may have lapsed until it’s already a compliance issue.

Hiring and Supervision Issues

Some firms mistakenly assume hiring someone with Series 7 credentials is enough. It’s not. The rep still needs to be formally registered under your firm and supervised according to FINRA rules.

Supervision must be documented, not just implied. This includes assigning a qualified principal (often Series 24), setting up written supervisory procedures, and using systems to track activity and approvals. Without this structure, even licensed reps can’t legally operate.

Navigating State vs. Federal Requirements

A rep holding Series 7 can’t solicit business in most states without also passing Series 63 (or 66). This often catches firms off guard, especially those offering products nationally.

Failing to meet state-level requirements can result in regulatory findings or forced rollbacks of business operations. It’s a straightforward fix, but only if addressed early.

Misjudging Licensing Requirements

Fintech teams frequently underestimate the regulatory impact of new features. Adding stock rewards, gamified investing, or embedded brokerage functionality may trigger activity that requires Series 7 licensed reps, even if the product isn’t pitched as “traditional investing.”

Licensing isn’t about how you describe the feature. It’s about how regulators view the underlying activity.

Confusing Advisory and Brokerage Roles

Series 7 allows for the sale of securities, but not fee-based advisory services. That’s covered by Series 65 or 66, under a different regulatory framework. Teams combining these functions often need reps with multiple licenses and a clear understanding of their roles.

Treating brokerage and advisory as interchangeable can lead to incorrect licensing, improper disclosures, or supervision gaps.

Underestimating Ongoing Regulatory Obligations

Licensing isn’t a one-time event. FINRA requires registered reps to complete continuing education, disclose status changes, and comply with regular audits and supervisory reviews.

Outsourced compliance partners, like InnReg, often support firms in building systems that handle these tasks reliably and promptly, especially when internal bandwidth is limited or nonexistent.

What Causes a Series 7 License to Become Inactive?

Holding a Series 7 license doesn’t mean it’s valid indefinitely. As mentioned, the license stays active only while the individual is registered with a FINRA-member firm. Once that affiliation ends, the clock starts ticking.

Here are the main reasons a Series 7 license becomes inactive:

Leaving a FINRA-member firm: When a representative leaves their sponsoring firm, the firm files Form U5 to terminate the registration. The license becomes inactive immediately upon termination.

Exceeding the two-year reactivation window: If the individual isn’t re-registered with another FINRA-member firm within two years of termination, the license expires, and the exam must be retaken. Note: if participating in the MQP program, the window can be extended to five years.

Missing continuing education (CE) requirements: FINRA requires annual CE. Missing deadlines results in an inactive license until the rep completes the training. Extended noncompliance can lead to additional consequences.

Disciplinary actions: FINRA or SEC sanctions, including suspensions or bars, can deactivate or permanently revoke a license, depending on the severity of the violation.

Incomplete or outdated Form U4 information: Failing to update key details like address, employment, or disclosure items can trigger regulatory review or put the license on administrative hold.

For fintech teams, especially those working with distributed or outsourced reps, tracking license status is a necessary part of your compliance function.

——

The Series 7 license is a regulatory gatekeeper for anyone involved in selling or recommending securities in the US. Someone in your operation must hold this license if your business involves brokerage, embedded trading, or building investment features into a fintech product.

But understanding who needs it, when, and how to manage it is where things often break down. Licensing is tied to activity, not titles. It’s governed by multiple regulators. And it requires ongoing supervision, continuing education, and up-to-date registration data.

For fintech teams moving quickly, it’s worth thinking about licensing before launch, before onboarding reps, and definitely before offering investment products. Whether you build the capability in-house or outsource it with consultants like InnReg, addressing this early is a foundational part of your compliance strategy.

Bruno is a Principal Compliance Officer at InnReg advising fintech clients across broker-dealer, RIA, and money transmitter verticals. He brings prior experience at Santander Brasil and Passfolio, with expertise in regulatory strategy, supervisory systems, and compliance execution. He holds FINRA Series 4, 7, 24, 63, and 99 licenses.

How Can InnReg Help?

InnReg is a global regulatory compliance and operations consulting team serving financial services companies since 2013.

We are especially effective at launching and scaling fintechs with innovative compliance strategies and delivering cost-effective managed services, assisted by proprietary regtech solutions.

If you need help with broker-dealer compliance, reach out to our regulatory experts today:

Related Articles

Featured LinkedIn Posts