How to Choose a Clearing Firm for Your Broker-Dealer

Key Takeaways

A clearing firm is a broker-dealer that handles settlement, custody, recordkeeping, and other back-office functions that allow securities transactions to be completed.

Most new broker-dealers choose an introducing model, where a third-party clearing firm performs clearing and custody functions while the broker focuses on client relationships and supervision.

Choosing a clearing firm requires evaluating regulatory history, financial stability, technology, supported products, pricing, reporting capabilities, and long-term business fit.

Outsourcing clearing functions does not transfer your compliance responsibilities, as introducing broker-dealers remain responsible for supervising outsourced activities and maintaining effective compliance programs.

Clearing agreements define how responsibilities are divided between the introducing broker and the clearing firm, making them a critical part of your supervisory and compliance framework.

Switching clearing firms can be costly and operationally disruptive, so selecting the right partner early is an important strategic decision for a growing broker-dealer.

Choosing a clearing firm is one of the most consequential decisions a broker-dealer makes. It affects your ability to launch, scale, and mitigate regulatory risks. For fintech startups, the choice can shape your entire operational model.

This article breaks down what clearing firms do, how they’re regulated, and the models available to broker-dealers. We’ll walk through key evaluation criteria so you can make an informed decision. You’ll also find compliance considerations, common misconceptions, and questions to ask before signing with a clearing partner.

InnReg supports fintech broker-dealers with vendor due diligence, clearing firm reviews, and end-to-end compliance operations. If your firm needs help structuring or managing a clearing relationship, reach out to our team.

What Is a Clearing Firm?

A clearing firm is the entity that handles the back-office mechanics of a securities transaction, such as settlement, custody, and recordkeeping. While introducing broker-dealers focus on client relationships and trade execution, clearing firms sit behind the scenes, allowing assets and funds to move correctly after a trade is placed.

In a typical clearing arrangement, the clearing firm is responsible for functions like:

Maintaining customer accounts

Sending trade confirmations and statements

Safeguarding client assets

Extending margin credit

Facilitating compliance with custody rules

Clearing firms are themselves registered broker-dealers, subject to heightened net capital and operational requirements because they carry customer funds and securities. For most startups, working with a clearing firm becomes essential because self-clearing requires significant infrastructure and capital.

Clearing Relationship Models

Broker-dealers don’t all handle post-trade operations the same way. Your approach depends on your business model, risk appetite, and regulatory strategy. There are two primary clearing models: introducing broker-dealer and self-clearing broker-dealer.

Each has its own requirements, costs, and implications for compliance. Understanding which model fits your firm’s goals is foundational to choosing the right clearing partner:

Introducing Broker-Dealer Model

An introducing broker-dealer works directly with clients but outsources clearing, custody, and settlement to a third-party clearing firm. This model is especially common among early- and growth-stage broker-dealers in the fintech space.

The clearing firm takes on back-office responsibilities such as:

Safeguarding customer funds and securities

Issuing trade confirmations and account statements

Settling trades and transferring assets

Providing books and records for customer accounts

Meanwhile, the introducing broker handles:

Customer onboarding and KYC

Order entry and routing

Client communication and servicing

Supervising associated persons and business conduct

This model is popular for a reason. It lowers the barrier to entry for new broker-dealers, with less capital tied up in back-office infrastructure. The tradeoff is that you're now managing a critical vendor relationship, not just an internal function. The clearing agreement needs to spell out who owns what, and your compliance program has to reflect that split, not just acknowledge it.

Self-Clearing Broker-Dealer Model

A self-clearing broker-dealer handles the full lifecycle of a trade in-house. Unlike introducing brokers, these firms don’t rely on a clearing partner. They interact directly with clearinghouses and must build the infrastructure to support those operations.

This model comes with high regulatory and operational demands. To become self-clearing, a firm must:

Register with the SEC and FINRA as a carrying broker

Join clearing organizations like the Depository Trust & Clearing Corporation (DTCC)

Maintain significantly higher net capital levels (per Rule 15c3-1)

Develop internal systems for custody, reconciliation, trade reporting, and reserve computations

Set up operational redundancies and business continuity plans

Most startups avoid self-clearing due to the cost, risk, and time required to get approval. However, some firms pursue it for long-term control, margin opportunities, or unique business models. It’s a strategic decision that typically makes sense only at scale.

Fully Disclosed Clearing Arrangements

In a fully disclosed clearing arrangement, the clearing firm opens and maintains individual customer accounts under the name of the introducing broker. Each client is visible to the clearing firm, and account-level details are shared between both parties.

This is the most common arrangement for new broker-dealers, especially those in fintech. It simplifies custody and reporting, reduces operational complexity, and clearly assigns compliance duties across both firms.

Some of the key features of fully disclosed arrangements are as follows:

Each customer account is opened and custodied at the clearing firm

The introducing broker handles KYC, onboarding, and customer communication

The clearing firm handles settlement, custody, statements, and confirms

The clearing agreement spells out regulatory responsibilities between parties

This model supports most retail-focused use cases, including equities, options, and fractional shares. However, if your product mix includes emerging or non-standard asset classes, you’ll need to confirm that your clearing partner can support those at the account level.

Omnibus Clearing Arrangements

In an omnibus clearing arrangement, the clearing firm holds a single account for the introducing broker, and customer-level details are maintained solely by the introducing firm. The clearing firm sees one pooled account, not individual client records.

This setup gives the introducing broker more control but also increases its regulatory burden. Because customer records and supervisory data live in-house, the firm is responsible for a significantly larger portion of compliance obligations, including trade surveillance, reconciliation, and records requirements.

At the same time, certain responsibilities (such as custody and clearing functions) remain with the clearing firm based on the clearing agreement and regulatory framework.

Here are some of the key characteristics of an omnibus arrangement:

The clearing firm holds one omnibus account in the name of the introducing broker

The introducing firm maintains all individual customer records internally

The firm must build and maintain internal systems for customer-level trade and position tracking

Regulatory expectations increase, particularly around financial controls and books and records

Omnibus relationships are more common among firms with mature infrastructure or unique operating needs. Most fintech startups avoid this model for its capital intensity and compliance complexity, but it may suit firms seeking tighter control or pursuing certain institutional strategies.

Regulatory Framework Governing Clearing Firms

Clearing firms operate in one of the most highly regulated segments of the financial system. As registered broker-dealers that custody customer assets and settle trades, they fall under a dense layer of federal securities laws and self-regulatory organization (SRO) rules.

Here are the main regulatory frameworks that govern clearing firms:

See also:

SEC

The Securities and Exchange Commission (SEC) is the primary federal regulator overseeing clearing firms. Any broker-dealer that carries customer accounts must register with the SEC and comply with its financial responsibility rules.

Key SEC rules relevant to clearing firms include:

Rule 15c3-1 (Net Capital Rule): Requires clearing firms to maintain higher levels of net capital than introducing brokers. The amount depends on activity level, customer balances, and margin exposure.

Rule 15c3-3 (Customer Protection Rule): Requires clearing firms to safeguard customer funds and securities by maintaining segregated accounts and computing reserve requirements.

Books and Records Rules (e.g., Rule 17a-3, 17a-4): Set standards for how clearing firms maintain trade confirmations, account statements, and internal supervisory records.

These rules are designed to protect customers and reduce systemic risk. For an introducing broker, understanding how your clearing partner meets these requirements is part of vendor oversight.

Need help with broker-dealer compliance?

Fill out the form below and our experts will get back to you.

FINRA

The Financial Industry Regulatory Authority (FINRA) is the SRO that oversees day-to-day compliance for broker-dealers, including clearing firms. While the SEC sets the high-level rules, FINRA enforces them through supervision, exams, and disciplinary actions.

FINRA’s oversight of clearing firms focuses on:

Supervision and controls: Firms must have written supervisory procedures (WSPs) that reflect how clearing functions are carried out and monitored.

Clearing agreements: Under FINRA Rule 4311, introducing and clearing firms must sign an agreement that allocates responsibilities and provides disclosures to customers.

Vendor oversight: Introducing brokers are expected to monitor their clearing firms as critical vendors. FINRA may request documentation showing your due diligence and ongoing supervision.

Customer complaints and operational issues: Clearing firms must track and respond to service issues, errors, and reportable events, especially when acting on behalf of correspondents.

For introducing brokers, FINRA exams often include questions about the clearing arrangement, i.e., how it’s structured, how it’s supervised, and how responsibilities are divided. Clear documentation and strong coordination with your clearing firm can reduce friction during reviews.

Not sure what FINRA is? Read here to learn about this US broker-dealer regulator →

Clearing Agreements

A clearing agreement is the contract between the introducing broker and the clearing firm. It formally defines who is responsible for what across regulatory, operational, and customer-facing functions.

Under FINRA Rule 4311, the agreement must:

Specify the functions each party performs (e.g., account opening, order handling, margin extension)

Assign responsibility for regulatory compliance across those functions

Require the clearing firm to notify FINRA and the introducing firm of any material issues

Be disclosed to customers in writing, highlighting the roles of each party

The agreement becomes a core part of your supervisory system. Regulators expect your WSPs to align with how responsibilities are split in the clearing contract. For example, if the clearing firm handles trade confirmations but you handle account approvals, your procedures should reflect that.

Before signing, firms should carefully review clearing agreements for terms around:

Termination clauses

Service-level expectations

Indemnification provisions

Dispute resolution

Data access and record retention

These agreements are not boilerplate. Every clause affects how your compliance program must operate, and they often require legal and compliance review.

Compliance Responsibilities in a Clearing Relationship

Just because your clearing firm handles custody and settlement doesn’t mean your compliance obligations shrink. In a clearing relationship, compliance duties are split but not offloaded. Regulators expect introducing brokers to maintain full supervisory control over their business, even when key functions are outsourced.

Typical areas where responsibilities are divided:

Account opening and KYC: Usually handled by the introducing broker

CIP (Customer Identification Program): Often performed by the introducing firm under FinCEN guidance

AML monitoring: Both parties share obligations; the clearing firm may monitor for transaction anomalies, but your firm must track customer behavior and file suspicious activity reports (SARs)

Trade confirmations and statements: Sent by the clearing firm

Books and records: Maintained by both parties, depending on who performs each function

Customer complaints: Introducing brokers are expected to log and respond, even if the issue involves a clearing error

Your written supervisory procedures (WSPs) should map clearly to these roles. Examiners will ask how you supervise functions that involve customer contact, funds, or trading activity, regardless of whether a clearing firm is involved.

Factors to Consider When Choosing a Clearing Firm

Choosing a clearing firm is a foundational infrastructure call. Your clearing partner affects operations, compliance, customer experience, and long-term scalability.

The sections below outline the key factors to evaluate when comparing clearing firms:

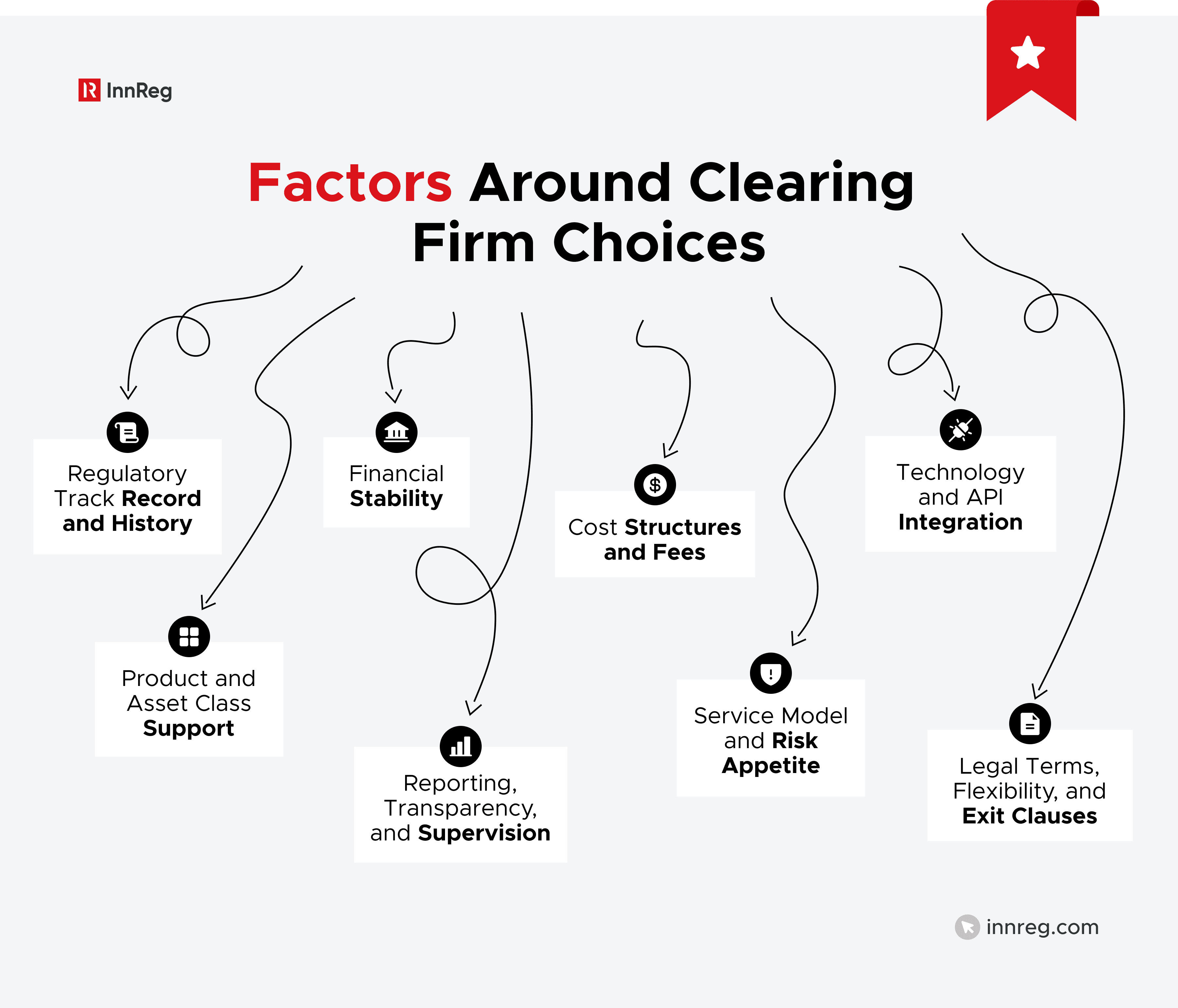

Regulatory Track Record and Enforcement History

Clearing firms carry direct regulatory exposure due to their custody and settlement roles. A firm’s disciplinary history says a lot about how it handles risk, supervision, and client protection. You don’t want surprises during a FINRA exam because of your vendor’s track record.

When evaluating a clearing firm, review:

FINRA BrokerCheck reports for enforcement actions, fines, or ongoing investigations

Any recent SEC, CFTC, or SRO actions involving operational failures or supervisory breakdowns

Patterns of repeat violations in areas like customer asset protection or AML oversight

The firm’s responsiveness to past issues; have they remediated effectively?

A firm doesn’t have to be spotless to be a viable partner, but persistent issues in critical areas (like books and records or capital compliance) are red flags. Strong due diligence up front protects your firm later.

Learn how to research brokers and firms via FINRA BrokerCheck →

Financial Stability and Capital Requirements

Your clearing firm will be the custodian of client funds and securities. That means its financial health directly impacts your operational and reputational risk. Regulators also expect you to monitor your clearing partner's stability as part of your vendor oversight program.

Key areas to assess:

Net capital levels under Rule 15c3-1 and how comfortably they exceed the minimum

Whether the firm is part of a larger financial institution or a standalone

Availability of audited financials or summaries of financial condition

Any history of capital deficiencies or close calls flagged by regulators

Capital shortfalls at a clearing firm can trigger operational restrictions or regulatory intervention. If you're launching or scaling a broker-dealer, you're better off with a partner that has a buffer.

See also:

Cost Structure, Fee Models, and Clearing Deposits

Clearing costs have a way of sneaking up on you, especially in the early days when every dollar is doing real work. What looks manageable at first can start to chip away at your margins faster than expected.

That’s why it’s worth slowing down before you commit. Take the time to really understand how the clearing firm prices its services. The headline fee is just the cover page. The real story is in how those costs play out based on how you’ll use the platform day to day.

Key elements to review:

Per-ticket or per-share fees for equities, options, and other asset classes

Monthly minimums or platform fees; some firms charge minimum clearing revenue regardless of activity

Initial and ongoing clearing deposits, often based on projected volume or margin exposure

Charges for ancillary services like Automated Customer Account Transfer Service (ACATS transfers), confirmations, or regulatory reporting

Revenue-sharing structures, such as interest on idle cash or payment for order flow

Run a model based on your projected trade volume and customer base. What looks affordable on paper may not scale with your business. If you're planning for fractional shares, high-volume trading, or non-standard assets, make sure pricing supports that model without hidden friction.

Technology, API Access, and Workflow Integration

For fintech broker-dealers, technology compatibility can be just as important as cost or reputation. The clearing firm’s systems will sit at the core of your trade processing, customer data, and compliance workflows.

Evaluate:

Availability of modern APIs for account creation, trade execution, funding, and reporting

Real-time vs. batch data access

Ability to integrate with your CRM, back-office systems, and compliance tools

Support for digital account onboarding and automated workflows

The more automated and accessible the platform, the less manual reconciliation you’ll need. If your model depends on real-time data or a custom client experience, choose a clearing firm that doesn’t box you into legacy systems.

Product and Asset Class Support

Not every clearing firm supports every product type. Before committing, confirm whether your current and future offerings are viable on their platform.

Key questions to ask:

Do they support fractional shares, options, margin, or extended hours trading?

Can they integrate with a crypto custodian or alternative asset provider if needed?

Are retirement accounts, trust accounts, or international securities supported?

What limitations exist on trading volume, ticket size, or product scope?

Your clearing firm should match your current roadmap and not block future growth. If they can’t support what you plan to build next year, you’ll be switching providers faster than expected, and that’s rarely cheap or simple.

Reporting, Transparency, and Supervision

Strong reporting and access to clean data are essential for compliance and operational oversight. If your clearing partner doesn’t give you visibility, your supervisory program suffers.

Ask about:

Real-time access to customer positions, cash balances, and trade data

Standard reports available for surveillance, reconciliation, and exception tracking

Tools or dashboards for compliance monitoring

Error handling and issue escalation workflows

Clear, consistent data feeds into your WSPs, AML program, and audit trail. Without it, regulatory exposure increases, particularly during exams or investigations. Transparency isn’t a feature. It’s a requirement.

Service Model and Risk Appetite

A clearing firm is a critical partner. How they handle service, communication, and risk directly impacts your daily operations. This matters even more if your firm is innovating outside traditional boundaries.

When assessing the service model, consider:

Will you have a dedicated relationship manager or a rotating support queue?

Do they provide 24/7 support or only standard business hours?

How do they handle escalations, outages, or trade breaks?

What’s their risk appetite for supporting new or complex products?

Fintech firms often face resistance from traditional clearers. Some won’t support fractional trading, crypto integration, or unusual order flows. Others will, but only with strict volume caps or custom controls.

Legal Terms, Flexibility, and Exit Clauses

Clearing relationships are long-term by nature, but that doesn’t mean you should lock yourself in. Review contract terms with an eye toward flexibility, transparency, and risk allocation. Focus on:

Termination clauses: Are there penalties or long notice periods?

Exclusivity: Are you required to route all trades or products through them?

Dispute resolution: Arbitration only? Jurisdictional limits?

Indemnification and liability: Who’s on the hook if something breaks?

Data ownership and access: Do you retain full access to customer records if you leave?

Switching clearing firms is operationally and legally complex. Choose a provider that gives you room to grow and a way out if your strategy changes.

How Clearing Firm Choice Impacts Your Compliance Program

Your clearing firm directly affects how your compliance program is structured, supervised, and examined. The way responsibilities are allocated between your firm and the clearing firm defines how your internal controls need to operate.

Here is how clearing relationships intersect with key compliance areas:

See also:

Supervision Models

Your clearing arrangement affects how you design and document your supervisory structure. FINRA expects introducing broker-dealers to maintain full supervisory responsibility, even when functions are outsourced to a clearing firm.

That means your WSPs must:

Reflect who performs each function (e.g., account opening, margin review, trade review)

Include processes to oversee any functions performed by the clearing firm

Identify escalation paths and internal points of contact

A mismatch between your WSPs and the clearing agreement is a red flag during exams. Supervisory gaps, like assuming the clearing firm is monitoring trades when they aren’t, can expose you to enforcement. You don’t have to control everything, but you do have to supervise it.

AML Coordination

Anti-money laundering responsibilities are shared in most clearing relationships. Even if the clearing firm monitors for certain transaction patterns, your firm remains on the hook for customer-level risk.

Typical AML role splits:

Customer Identification Program (CIP): Often handled by the introducing broker

Ongoing monitoring: The clearing firm may flag unusual activity (e.g., high-volume withdrawals), but your team must review and act

SAR filings: Both firms may file suspicious activity reports independently, depending on who detects the issue

AML procedures: Should document coordination points and clearly define what gets escalated and by whom

Regulators expect both firms to maintain standalone AML programs, even when certain functions overlap. Weak coordination or unclear expectations can lead to missed red flags or duplicative filings.

Customer Protection Rules

Clearing firms are directly subject to SEC Rule 15c3-3, which governs how customer funds and securities must be protected. But introducing firms aren't off the hook.

Here's how responsibility typically breaks down:

Clearing Firm | Maintains reserve bank accounts, segregates fully paid securities, and performs reserve calculations |

|---|---|

Introducing Broker | Must understand how the clearing firm performs these functions and monitor client-facing activity (e.g., disbursement patterns, restricted security movement) |

You’re expected to oversee how your clearing partner safeguards customer assets. That means asking questions, reviewing their processes, and incorporating those dependencies into your supervisory program.

Reporting Dependencies

Much of your reporting and disclosure activity depends on what your clearing firm provides. If data is delayed, incomplete, or inaccurate, your compliance program suffers.

Here are some important examples of critical reporting functions:

Trade confirmations and statements: Generated by the clearing firm, but your firm is still responsible for reviewing them

Exception reporting and error tracking: Some firms provide dashboards or automated alerts, while others don't

Regulatory filings: If your firm relies on the clearing firm for data used in regulatory reports (e.g., FOCUS reports), that dependency should be documented

Surveillance reports: Review how the firm supports AML, suitability, and trading activity oversight

Your ability to supervise depends on timely access to accurate information.

Exam Outcomes

Your clearing arrangement will come under scrutiny during regulatory exams. FINRA and the SEC routinely assess how introducing brokers manage outsourced functions and whether the clearing firm relationship introduces compliance risk.

Expect examiners to ask:

Who performs key functions, and how is that documented?

How does your firm supervise what the clearing firm does on your behalf?

Are roles clearly outlined in your clearing agreement and WSPs?

How do you monitor the clearing firm’s performance, financial health, and incident history?

Gaps in oversight or unclear ownership often lead to exam findings. Even if your clearing firm handles a function well, you’re still expected to know how it’s done and have a process to oversee it.

Special Considerations for Fintech Broker-Dealers

Fintech broker-dealers face a unique mix of operational complexity and regulatory scrutiny. From unconventional product structures to nonstandard onboarding flows, not every clearing firm is built to support these models effectively.

Consider these specifically for fintech broker-dealers:

Product fit: Does the clearing firm support fractional shares, embedded investing, or hybrid custody models?

Tech compatibility: Can their APIs integrate with your platform? Do they support automated workflows?

Risk tolerance: Are they comfortable with your innovation, or are they going to block or delay launches?

Speed to market: Some clearing firms are optimized for large institutions, not for fast-moving startups.

InnReg often works with fintechs to evaluate and manage these relationships, especially when the business model doesn’t fit neatly into legacy processes. A practical, tech-neutral, and compliance-driven approach can help fintechs avoid slowdowns tied to the wrong clearing partner.

Common Misconceptions About Clearing Firms

Clearing firms are often misunderstood by first-time founders or early compliance hires. Assumptions about what a clearing firm does (or doesn’t do) can lead to risk exposure or operational friction.

Common misconceptions include:

The clearing firm handles compliance: A clearing firm will support parts of the operation. They might handle things like generating statements or flagging unusual trading activity. But the core responsibilities stay with you. You still own supervision, your written supervisory procedures, AML monitoring, and regulatory filings.

All clearing firms offer the same services: They don’t. Some firms specialize in supporting digital onboarding, fractional shares, or alternative assets, while others don’t support these at all. Differences in API access, service models, and asset class coverage can significantly impact your ability to launch or grow.

We can always switch later: Technically, yes, but clearing transitions are highly disruptive. They involve transferring customer accounts, repapering disclosures, re-integrating systems, and coordinating with regulators. Switching midstream often costs more in both time and credibility than choosing the right fit from the start.

If something goes wrong, it’s on them: Regulators expect introducing firms to supervise all functions touching their business, even if outsourced. If a clearing firm mishandles a customer transfer or fails to escalate a red flag, your firm may still be held responsible for the outcome. Contracting out does not absolve you of oversight duties.

Understanding the real scope and limits of your clearing partner helps you avoid missteps in vendor management, compliance oversight, and business planning.

Clearing Firm Selection Checklist

Use this checklist to guide your clearing firm evaluation process. Each item helps assess regulatory alignment, operational fit, and long-term viability.

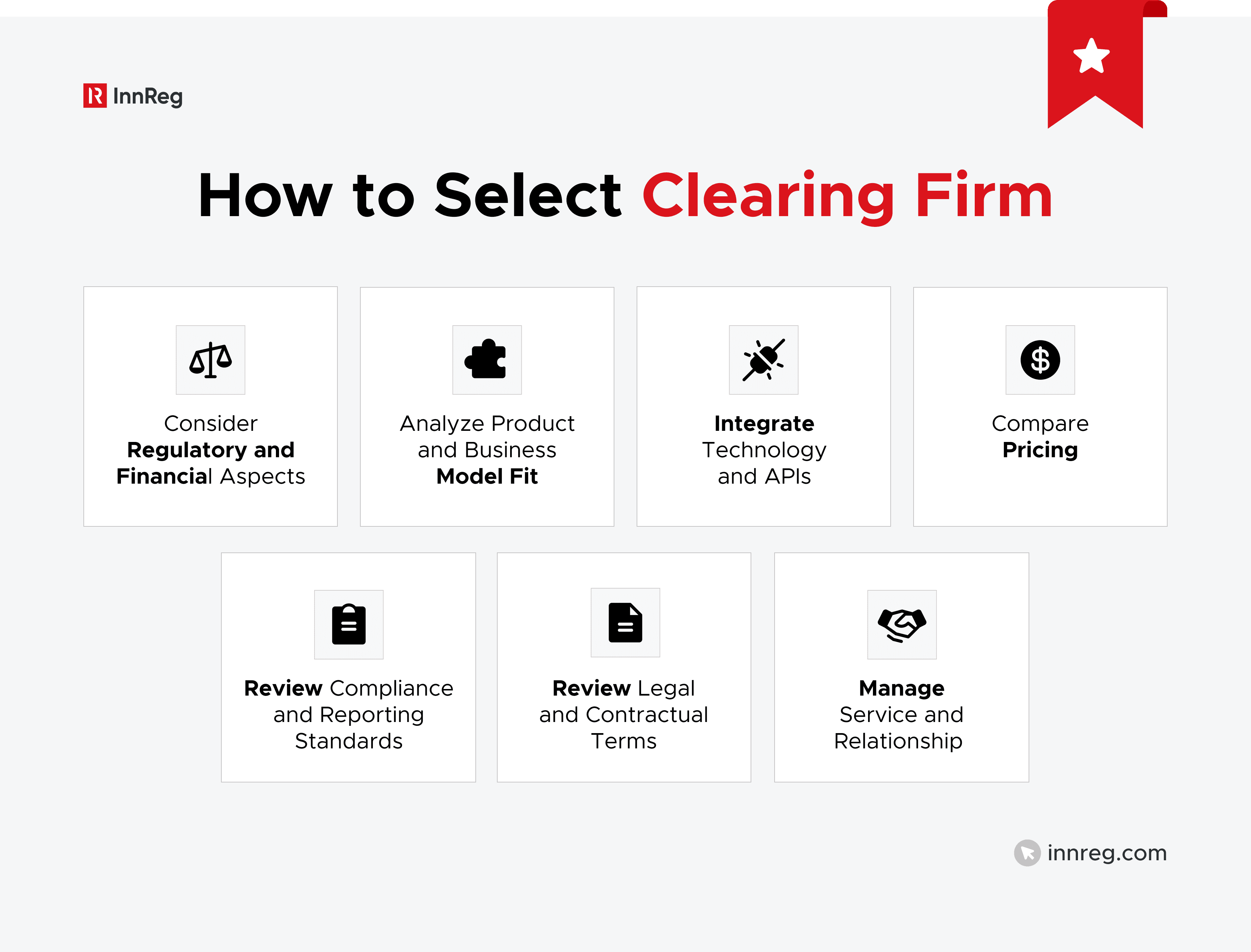

Regulatory and Financial Considerations

Reviewed FINRA BrokerCheck and SEC filings for enforcement history

Confirmed firm is registered as a carrying broker-dealer

Verified capital levels exceed minimum net capital requirements

Requested audited financial statements or capital summary

Evaluated parent company backing or institutional affiliation

Product and Business Model Fit

Supports all required asset classes (e.g., equities, options, fractional shares)

Accommodates current and planned account types (e.g., IRAs, trusts, entities)

Offers flexibility for embedded or alternative product models

Can integrate with crypto custody partners, if applicable

Technology and Integration

Provides modern APIs for account onboarding, trading, and reporting

Offers real-time or near-real-time data access

Compatible with your CRM, compliance tools, and internal systems

Supports automated onboarding and operational workflows

Pricing and Economics

Transparent fee schedule (per-ticket, per-share, monthly minimums)

Clearing deposit requirements reviewed and budgeted

No unexpected platform or data access fees

Aligned with any revenue-sharing arrangements (e.g., interest, PFOF)

Compliance and Reporting

Responsibilities are clearly defined in the draft clearing agreement

WSPs and AML procedures can map to shared workflows

Provides exception reports, surveillance tools, or dashboards

Exam history or references confirm a strong compliance culture

Legal and Contractual Terms

Reviewed termination clauses and exit penalties

No unreasonable exclusivity or routing restrictions

Data ownership and access are addressed in the contract

Dispute resolution terms are acceptable

Service and Relationship Management

A dedicated relationship manager or an assigned team

Support model meets business hours and escalation needs

Demonstrated willingness to support fintech models

References confirmed service responsiveness and issue resolution

Tip: Keep a record of how each firm stacks up against these items during due diligence. It’s helpful during internal reviews and shows regulators you approached vendor selection with intent and discipline.

—

Clearing firm selection is one of the first and most critical steps in launching a broker-dealer. The right partner can support your product roadmap and regulatory obligations. The wrong one can create friction, delays, or even regulatory exposure. At InnReg, we help fintech firms navigate this process with a compliance-first lens.

Our team has advised dozens of startups on structuring clearing relationships, vetting vendors, reviewing agreements, and aligning supervision and workflows. Whether you're applying for FINRA approval or reassessing your current clearing setup, we act as an extension of your compliance team. Speak to our experts if that interests you.

José is a Compliance Consultant with over 6 years of experience across Tier-1 financial institutions including KPMG, Deutsche Bank, ICBC, and Citco. He specializes in KYC/AML, transaction monitoring, forensic financial investigations, and emerging frameworks such as MiCA and DORA. He holds a Master's from SOAS University of London.

How Can InnReg Help?

InnReg is a global regulatory compliance and operations consulting team serving financial services companies since 2013.

We are especially effective at launching and scaling fintechs with innovative compliance strategies and delivering cost-effective managed services, assisted by proprietary regtech solutions.

If you need help with broker-dealer compliance, reach out to our regulatory experts today:

Related Articles

Featured LinkedIn Posts