Washington Money Transmitter License: Checklist and Requirements

If your business moves money on behalf of others and your customers are located in Washington, there is a good chance you need a Washington money transmitter license.

That includes fintechs handling digital payments, remittances, wallets, or crypto, even if you're not based in Washington. Operating without the proper license can result in enforcement action, fines, or forced shutdowns.

This article breaks down the checklist and requirements for getting and maintaining a money transmitter license in Washington. It covers who needs one, what the application process looks like, what regulators expect from your compliance program, and where fintechs often experience issues.

At InnReg, we help money transmitters and fintechs obtain and manage state licenses, including Washington MTLs. Our team supports registration, regulatory documentation, and post-licensing compliance operations for complex business models.

Who Needs a Washington Money Transmitter License?

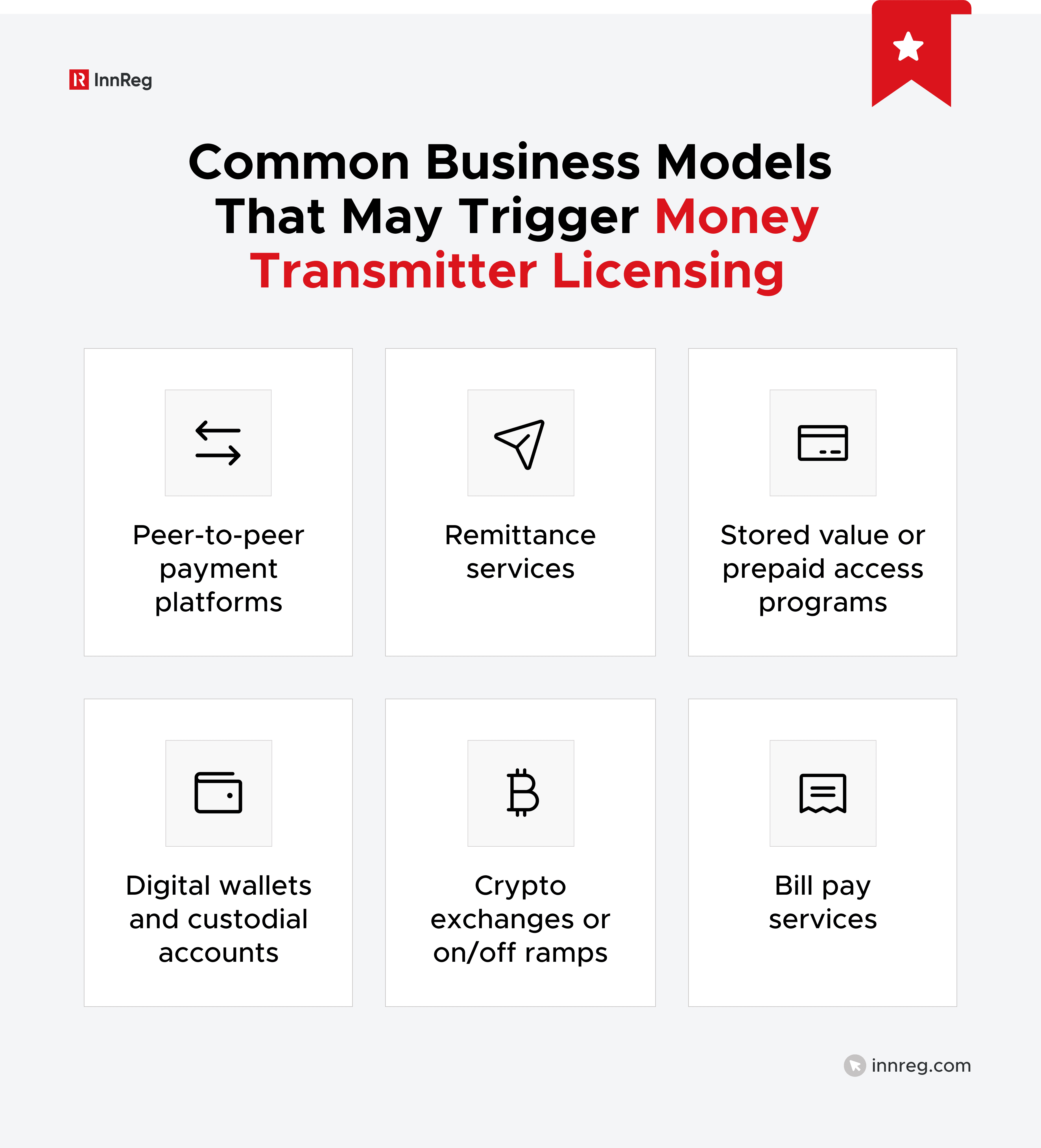

Washington takes a broad view of what qualifies as money transmission. If your product touches customer funds in transit, even briefly, you may need a license.

Activities That Trigger Licensing

If your company receives money or its equivalent for transmission on behalf of customers located in Washington, you likely fall under the state’s money transmitter licensing law.

The key trigger is whether your business handles funds on behalf of others (even temporarily). That includes both fiat and virtual currencies. Washington’s Department of Financial Institutions (DFI) treats crypto like any other form of monetary value for licensing purposes.

Applicability to Fintech and Crypto Businesses

In Washington, crypto is not a gray area and is included in money transmission rules. Services like digital asset custody, crypto-to-fiat conversions, and custodial wallets (where the provider controls private keys or has the ability to move user funds) fall under the same umbrella. That includes newer models mixing crypto with financial rewards or prepaid programs. Non-custodial wallet software that does not control user assets is generally treated differently.

Even short handling times do not exempt you. If your product takes custody of or has control over money or crypto on behalf of someone else, you are probably on the hook for a license.

Common Exemptions and Gray Areas

Washington does not draw a sharp line between crypto and fiat when it comes to money transmission. If you are helping users store, transfer, or cash out digital assets, you are probably operating in a regulated space.

This applies even to business models that do not look like traditional remittance, such as crypto-funded incentives or payment-plus-investing apps.

It’s not about how long you hold the funds. If value flows through your system, that may be all it takes to trigger licensing requirements.

Key Regulators and Legal Framework

The licensing process involves multiple layers: state oversight, federal obligations, and a shared digital filing system:

Washington DFI and Relevant State Laws

The Washington State Department of Financial Institutions (DFI) is the state agency that regulates money transmitters in Washington.

If you're applying for a license or already hold one, DFI is your primary point of contact. The agency oversees applications, conducts examinations, and handles enforcement.

Washington’s licensing process is built on RCW 19.230, known as the Uniform Money Services Act. That law defines what qualifies as money transmission and outlines the net worth, bonding, and reporting requirements.

Additional rules appear in WAC 208-690, which covers operational expectations like cybersecurity, recordkeeping, and business continuity.

NMLS and Federal MSB Registration

The application process starts in the Nationwide Multistate Licensing System (NMLS), a platform many state regulators use to handle licensing logistics. You will use it to submit your company and control person forms, upload compliance documentation, and track status updates.

In parallel, your business must be registered with the Financial Crimes Enforcement Network (FinCEN) as a Money Services Business. Washington treats federal registration as a required step; your state application won’t move forward without it.

See also:

Interaction with FinCEN, BSA, and OFAC Rules

Beyond state laws, Washington money transmitters must follow federal standards under the Bank Secrecy Act (BSA). That includes developing an Anti-Money Laundering (AML) compliance program, conducting ongoing transaction monitoring, and filing reports like SARs and CTRs when applicable.

See how InnReg helps fintech with AML compliance →

Office of Foreign Assets Control (OFAC) compliance also applies. Transmitters must avoid facilitating transactions involving sanctioned individuals or jurisdictions.

For startups operating internationally or with crypto components, this layer of compliance often adds operational complexity. This is especially true when it comes to vendor risk management and onboarding processes.

Component | Role and Requirements |

|---|---|

Washington DFI | Primary regulator for money transmitters in Washington. Oversees applications, licensing, exams, and enforcement. |

RCW 19.230 & WAC 208-690 | Defines money transmission activities, capital and bonding standards, and sets operational rules (e.g., cybersecurity, continuity, recordkeeping). |

NMLS | Portal for submitting and managing state license applications. Used for MU1, MU2 forms, document uploads, and communication with DFI. |

FinCEN (Federal MSB Registration) | Required federal registration for all money transmitters. Proof of MSB status must be included in the Washington license application. |

Bank Secrecy Act (BSA) | Requires an AML compliance program, ongoing monitoring, and filings such as SARs and CTRs. Applies in parallel with state licensing. |

OFAC Compliance | Businesses must block or avoid transactions involving sanctioned entities or jurisdictions. Critical for firms handling cross-border or crypto transactions. |

Need help with money transmitter compliance?

Fill out the form below and our experts will get back to you.

Pre-Application Checklist for a Money Transmitter License in Washington

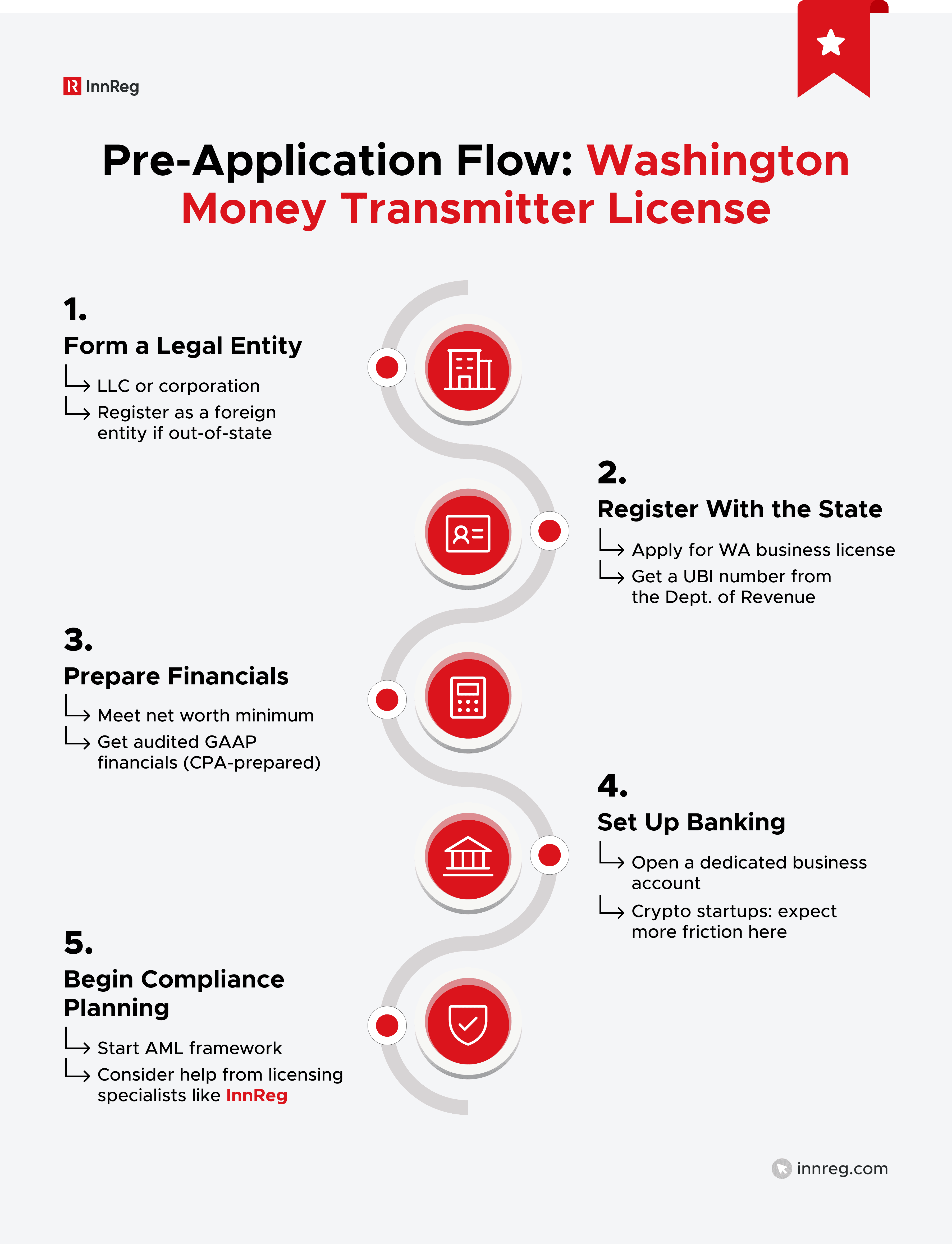

Before applying through NMLS, your company should be fully set up. Legal structure, financials, and core compliance elements are all in place. Washington expects applicants to be prepared, not to figure it out during review.

Entity and Business Registration

You will need a properly formed legal entity, typically a corporation or LLC. If the business is not based in Washington, you must also register as a foreign entity with the Secretary of State and obtain a certificate of authority.

On top of that, you will need a Washington business license and a Unified Business Identifier (UBI) number. These are issued by the Department of Revenue through the Business Licensing Service and are required for most financial activities in the state.

Financial Prep

Washington imposes a minimum net worth requirement based on projected transaction volume. Most startups will start with the $10,000 minimum, but it scales with business size and can reach as high as $3 million.

If your platform holds crypto wallets for users, the minimum jumps to $100,000.

You will also need audited financial statements prepared under Generally Accepted Accounting Principles (GAAP).

For newer companies, this might mean engaging a Certified Public Accountant (CPA) to audit your opening balance sheet. Many applications are delayed simply because founders underestimate this step.

Banking Setup and Early Compliance Planning

DFI requires applicants to maintain a dedicated business bank account. That means finding a bank willing to work with your model, often a pain point for early-stage fintechs, especially those dealing with crypto.

This is where a practical compliance consultant, such as InnReg, can step in. We help fintech teams navigate early banking roadblocks, prepare AML documentation, and build the operational controls needed for licensing.

See how InnReg helps fitechs obtain a Money Transmitter Licence →

Washington Money Transmitter License Application Requirements

Once your foundational setup is in place, the actual application process moves through NMLS, with Washington DFI reviewing and approving the submission. The state does not just assess paperwork. It evaluates whether your business is ready to handle regulated financial activity responsibly.

Core NMLS Components (MU1, MU2, etc.)

The application begins with the MU1 form, which captures your company’s legal structure, business model, ownership, and control persons. Each person with significant ownership or decision-making authority also completes an MU2 form.

These forms include personal disclosures, fingerprints, credit checks, and background information. Washington reviews this data closely, especially if any individual has a regulatory, legal, or financial history.

See also:

Required Documents and Supporting Materials

Washington DFI expects a full set of supporting materials to be submitted through NMLS. These documents give regulators a clearer picture of your business model, financial position, and compliance readiness.

They also help DFI assess whether your operations align with the obligations that come with holding a license.

Not everything has to be uploaded on day one, but core documents should be in place. Regulators may ask for additional items during the review, and some of the most frequent issues are cluttered and incomplete submissions.

Key items include:

Audited financial statements (current and prepared under GAAP by a CPA)

Organizational charts showing the full ownership structure and management team

A business plan that outlines your products, customer segments, operational model, and risk framework

A flow of funds diagram for each transaction type, showing how money or value moves through your system

Sample receipts, terms of service, or other customer-facing documents

Your internal compliance policies, including AML and cybersecurity documentation (DFI may not require full uploads, but you must confirm they are in place)

Note: Keep your files clean and well-labeled (PDF format is standard). Expect follow-up questions if anything looks incomplete or unclear.

Designating a Responsible Individual

You will also need to name a Responsible Individual: a W-2 employee who will oversee licensed activity in Washington. This person must be legally authorized to work in the US and have relevant experience. Be prepared to submit a résumé and their 10-year work history as part of the application.

Regulators will refer to this person for licensing matters, compliance issues, exams, and communications.

While not always titled this way internally, the Responsible Individual is often a Head of Compliance, Chief Compliance Officer, or a Senior Operations or Legal Manager, depending on the company’s size and structure.

See how InnReg helps fintechs by providing outsourced Chief Compliance Officer services →

Component | What It Covers | Why It Matters |

|---|---|---|

NMLS Core Forms | Company (MU1) and control person (MU2) forms, including disclosures, fingerprints, and credit checks | Establishes business structure and individual qualifications; reviewed closely by DFI |

Audited Financial Statements | GAAP-compliant, CPA-prepared statements | Demonstrates financial readiness; required to meet net worth thresholds |

Organizational Charts | Ownership and management structure | Clarifies control and internal oversight |

Business Plan | Overview of products, target market, risk strategy, and operating model | Helps DFI assess the nature and risk of your business |

Flow of Funds Diagram | Visual of how money/value moves through each product or transaction type | Used to determine if transmission activity is occurring and how it's managed |

Sample Customer Documents | Receipts, terms of service, or other user-facing communications | Shows how consumers are informed and protected |

Compliance Policies | AML, cybersecurity, and other internal procedures | Indicates regulatory awareness and preparedness |

Responsible Individual | W-2 employee with authority over WA-licensed activity; résumé and 10-year work history required | Acts as the regulator’s main point of contact and accountability post-licensing |

Net Worth and Surety Bond Explained

Washington ties both net worth and bonding requirements to your projected transaction volume. These are the financial controls designed to reduce risk for consumers and the state.

Minimums and Calculation Method

The baseline net worth requirement in Washington is $10,000. But it does not stop there. For every additional $1 million in transmission volume you expect to process, another $10,000 is added (or a fraction thereof). The maximum required amount tops out at $3 million.

The formula is:

$10,000 for the first $1 million in volume

An additional $10,000 for each additional $1 million (or fraction thereof)

Capped at a maximum of $3 million

Your audited financial statements must demonstrate that your business meets this threshold. If your actual volume exceeds projections, Washington may require you to increase your capital later on.

The surety bond follows a similar volume-based scaling structure, starting at $10,000 and scaling with volume, capped at $550,000. The bond protects customers and the state if your company fails to meet its obligations.

Crypto-Specific Thresholds

The moment your business takes on crypto custody, the rules change. The state sets a $100,000 minimum net worth for businesses that hold digital assets, and that applies even if your transaction volume is low.

Even if you use a third-party custodian, DFI might still treat you as holding control, depending on how your service is structured. It’s smart to take a close look at your flow of funds and how your platform operates before applying.

Projected Volume | Net Worth Required | Surety Bond Required |

|---|---|---|

$0 - $1 million | $10,000 | $10,000 |

$5 million | $50,000 | $50,000 |

$10 million | $100,000 | $100,000 |

$50 million | $500,000 | $500,000 |

Over $55 million | $3 million (cap) | $550,000 (cap) |

Any amount w/crypto custody | $100,000 (minimum) | Based on volume (same scale) |

Flow of Funds and Sample Docs for Your Money Transmitter License in Washington

DFI expects more than a description of how your product works; it wants to see how money actually moves. That’s where flow of funds documentation comes in.

This section of your application helps regulators understand risk points, third-party involvement, and whether your structure complies with Washington’s requirements.

What Your Flow of Funds Diagram Should Show

Your diagram should clearly illustrate every movement of funds or monetary value, from the moment a customer initiates a transaction to final settlement.

That includes:

All counterparties and intermediaries (banks, processors, custodians)

The direction of each transfer: who sends what, and to whom

Where funds are held temporarily (if at all)

The timing and order of each step

How your system handles cancellations or failed transactions

DFI looks closely at these diagrams to understand how much control your company has over the movement of funds, especially if crypto is part of your offering. If your platform initiates or directs the flow of money, even indirectly through an API, that could change how the state treats your activity.

Note: Use clear, plain labels in your flow chart. Assume the regulator isn’t familiar with your infrastructure.

See also:

Sample Receipts, Agreements, and Disclosures

Alongside your flow diagram, DFI may request or require sample versions of customer-facing materials. Your user materials tell DFI how clearly you communicate with customers.

Be ready to submit:

Receipts

Terms of service

Disclosures on fees, delays, or limits

Error resolution policies

Risk disclaimers

The materials you provide need to match how your platform actually works. If they do not, reviewers will likely push back.

Post-Licensing: Ongoing Compliance Requirements

After your fintech is approved, you are expected to maintain strong controls, stay current with filings, and keep regulators informed of any material changes.

Category | Requirement |

|---|---|

Annual Renewal and Assessment | Submit updated financials, transmission volume reports, ownership/business model changes, and compliance attestations. The deadline for report filings is typically March 1. |

AML Program | Maintain a named AML lead, working transaction monitoring tools, documented CDD/EDD procedures, and a SAR reporting process tailored to your risk model. |

Cybersecurity and Recordkeeping | Implement security controls and retain customer records, transaction logs, and audit trails for at least 5 years. |

Examinations | Expect periodic reviews by DFI, which may be document-based or onsite. |

Agent Oversight | Disclose all agents in NMLS, submit quarterly reports, and supervise compliance. Licensee remains fully accountable for agent conduct. |

Annual Renewal and Assessment Filings

Each year, money transmitters in Washington must renew their license and report key updates. DFI uses this to keep tabs on how your business has grown or changed.

You will need to submit:

Updated financial statements

A report of transmission volumes

Any changes to ownership or business model

Updated compliance attestations

License renewals are processed through the NMLS annual renewal cycle (typically November through December), and annual reports, including transmission volume data, are generally due by March 1. Late filings can result in penalties or suspension. Keep in mind: DFI uses this review to re-evaluate your risk profile.

AML, Cybersecurity, and Recordkeeping Obligations

After approval, regulators expect you to be operating with a working AML framework.

You will need to have:

A named individual responsible for AML oversight

Tools to flag and review unusual transactions

A working process for CDD and EDD

Clear steps for when and how to file SARs

Washington also expects you to maintain strong cybersecurity practices and retain records for at least five years, including transaction logs, customer communications, and audit trails. These requirements are enforced through periodic exams, which can be document-based or onsite.Learn how InnReg helps fintechs with cybersecurity program development →

Managing Agents and Authorized Delegates

If your business uses third-party agents or payment facilitators (white-labeled or otherwise), Washington expects more than a basic disclosure.

You will need to document all authorized delegates in your NMLS filings and submit a report every quarter. Beyond that, regulators want to see that you’re actively supervising those agents.

You are still on the hook for their actions. If one of them mishandles funds or violates compliance rules, your license is what’s at risk.

—

Securing a Washington money transmitter license is a milestone, not a finish line.

The process requires planning, structure, and documentation well beyond just filling out forms. And once licensed, staying compliant means keeping systems updated, supervising third parties, and responding promptly to regulatory requests.

Products that handle funds, especially in fintech or crypto, will likely need to meet these regulatory requirements. Tackling them before launch or scale saves time and limits risk.

Frequently Asked Questions

What is the money transmitter law in Washington state?

Washington’s money transmitter law falls under the Uniform Money Services Act (RCW 19.230). It regulates businesses that receive money or digital value for transmission to another person or location. The law is enforced by the Washington State Department of Financial Institutions (DFI).

What qualifies as a money transmitter?

A business qualifies as a money transmitter if it handles funds, fiat or crypto, on behalf of others. This includes moving money between parties, storing value temporarily, or converting currencies. Even brief control of customer funds can trigger licensing requirements.

Do you need a business license to sell in Washington state?

Yes. Most businesses selling products or services in Washington need a state business license and a Unified Business Identifier (UBI) number. The Department of Revenue issues these through the Business Licensing Service.

What is the difference between a money transmitter and a payment processor?

Money transmitters directly handle and transfer funds on behalf of customers. Payment processors, by comparison, usually just help facilitate the transaction without taking control of the money. But in Washington, that line can blur. Processors that route or hold funds, even momentarily, might fall under licensing rules.

How long does it take to acquire a money transmitter license in Washington?

It typically takes 3-6 months to get a Washington money transmitter license, though timelines vary. Delays often stem from incomplete filings or missing financial documentation.

InnReg was founded in 2013 by Francesco Matteini, former Chief Compliance Officer who helped launch and scale some of the most innovative digital broker-dealers over the last two decades. He built compliance programs to support the first zero-commission broker and the first BD-sponsored investor social network. Since its founding, InnReg has attracted highly experienced fintech consultants with long careers in compliance, risk management, and a deep understanding of the fintech industry.

How Can InnReg Help?

InnReg is a global regulatory compliance and operations consulting team serving financial services companies since 2013.

We are especially effective at launching and scaling fintechs with innovative compliance strategies and delivering cost-effective managed services, assisted by proprietary regtech solutions.

If you need help with money transmitter compliance, reach out to our regulatory experts today:

Related Articles

Featured LinkedIn Posts