Registered Representative: What Is It and How Is It Regulated?

Key Takeaways

A registered representative is a licensed individual who can solicit, recommend, and execute securities transactions on behalf of a broker-dealer.

You generally need to become a registered representative if your role involves discussing investments, handling securities transactions, or being compensated based on securities-related activity.

Becoming a registered representative requires sponsorship by a FINRA-member broker-dealer, passing the required qualification exams, and completing FINRA and state registration.

Registered representatives are regulated by FINRA, the SEC, and state securities regulators, and must comply with ongoing supervision, recordkeeping, disclosure, and continuing education requirements.

Registered representatives and investment advisor representatives serve different regulatory functions, follow different standards, and may require different licenses, even when operating within the same firm.

Fintech companies often encounter registration issues when unlicensed employees discuss investment products, receive transaction-based compensation, or support securities activities without proper supervision and licensing.

The term registered representative carries specific regulatory meaning in financial services, especially for broker-dealers, hybrid fintechs, and firms offering investment-related products.

If your business involves soliciting or executing securities transactions, understanding what this role entails is not optional. It is central to staying on the right side of regulators like FINRA and the SEC.

This article breaks down what a registered representative is, when your company needs one, and how to navigate the licensing and compliance landscape that surrounds the role.

At InnReg, we help fintech companies and broker-dealers navigate registered representative licensing and compliance. From sponsorship structures to ongoing supervision, our team supports firms building investment features into innovative products.

What Is a Registered Representative?

A registered representative is an individual licensed to engage in securities transactions on behalf of a broker-dealer. This includes recommending, soliciting, or executing securities such as stocks, bonds, and mutual funds for retail or institutional clients.

To operate in this capacity, the individual must be registered with the Financial Industry Regulatory Authority (FINRA) through a broker-dealer and must pass the required qualification exams. These include general industry exams as well as exams specific to the products or functions the individual will handle.

Registered representatives are also subject to regulatory oversight from the Securities and Exchange Commission (SEC), state regulators, and the broker-dealer’s internal supervisory structure.

In the fintech space, this role often extends beyond traditional sales or trading. A registered representative may support in-app financial services, review flagged transactions, or interact with customers through digital channels. Regardless of how the service is delivered, the regulatory responsibilities remain the same.

Who Needs to Be a Registered Representative?

Any individual who engages in the solicitation or execution of securities transactions on behalf of a broker-dealer must register as a registered representative. This requirement applies whether the person is advising a client, placing a trade, or supervising others doing so.

This is not about job titles. It comes down to what someone actually does. If a team member discusses investments with clients, helps process trades, or gets paid based on transactions, they meet the regulatory definition of a registered representative.

These registration requirements apply across the board. Whether the firm is a traditional broker-dealer or a fintech platform offering embedded securities, the same rules apply. Even a founder or executive may need to register if they are involved in pitching investment features or handling early client interactions.

How to Become a Registered Representative

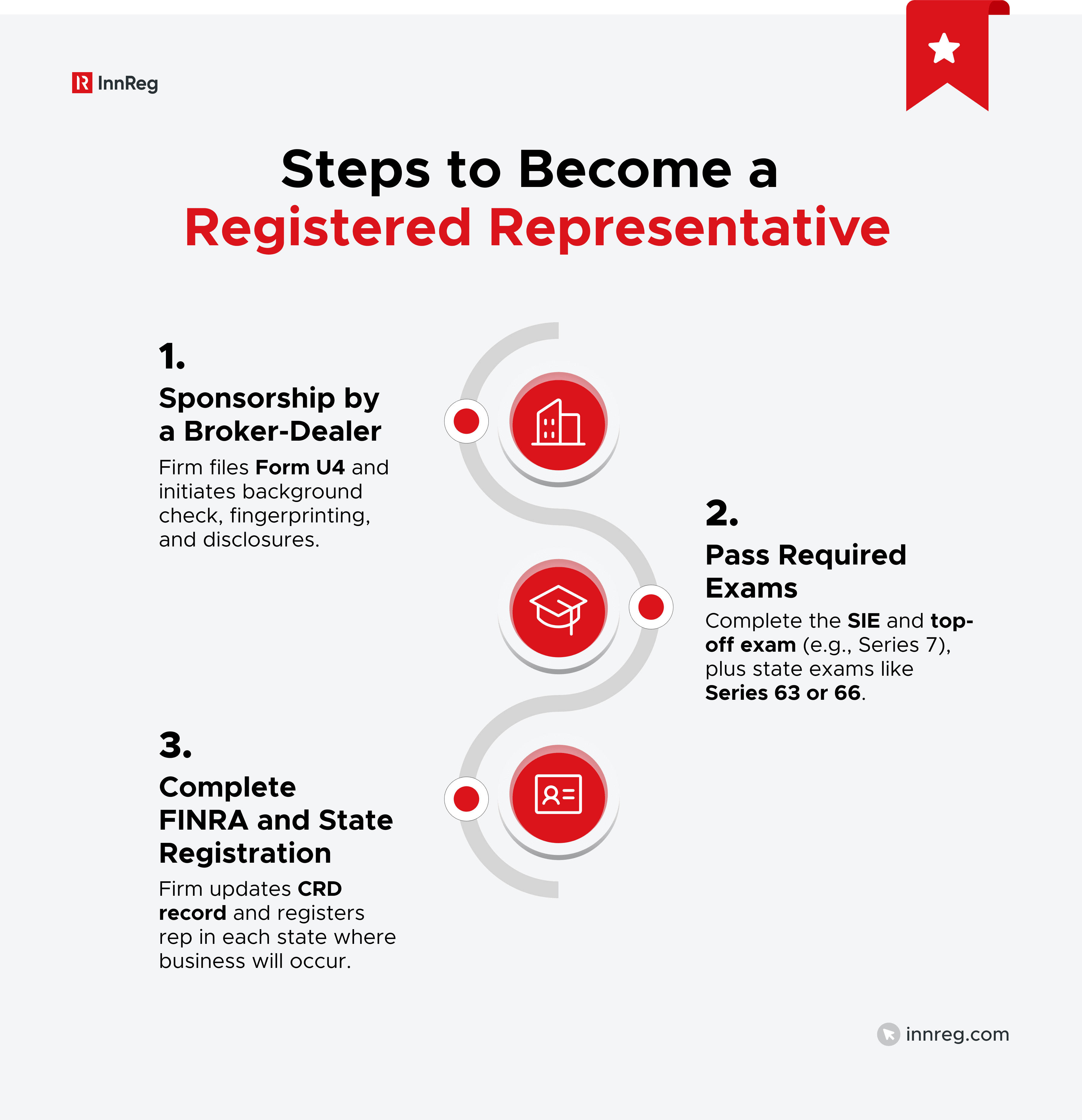

Becoming a registered representative is a regulated process that involves sponsorship, exams, and approvals at both the federal and state levels. It is not a license you can hold independently. You must be affiliated with a FINRA-member broker-dealer to begin the process.

The path typically follows three stages:

1. Sponsorship by a Broker-Dealer | 2. Required Exams and Licenses | 3. FINRA and State Registration Process |

|---|---|---|

Firm files Form U4; background check, fingerprinting, disclosures; CRD profile created | Pass SIE + Series 7 or other top-off exam; possibly Series 63/65/66 based on role | Firm associates license in CRD; register with each applicable state |

1. Sponsorship by a Broker-Dealer

The first step to becoming a registered representative is sponsorship by a FINRA-member broker-dealer. You cannot apply directly as an individual. A firm must initiate the process by filing Form U4 (Uniform Application for Securities Industry Registration) on your behalf.

This filing includes personal and professional disclosures, fingerprinting, and a background check. It triggers your profile in FINRA’s Central Registration Depository (CRD) system. Any disciplinary history, criminal record, or financial disclosure, such as bankruptcies or liens, must be reported and may impact approval.

In startup environments, it is common for early employees or founders to become registered representatives. In those cases, the startup itself must be an approved broker-dealer and designate a supervisory structure. This includes having qualified principals in place, not just representatives.

2. Required Exams and Licenses

Once sponsored, the individual must pass specific qualification exams administered by FINRA or, in some cases, NASAA. These exams validate knowledge of products, industry rules, and applicable regulations.

Most registered representatives begin with the Securities Industry Essentials (SIE) exam, followed by a representative-level “top-off” exam. The most common combination is the SIE plus the Series 7, which qualifies individuals as General Securities Representatives. If the role is narrower, such as selling only mutual funds or variable annuities, then the Series 6 may be more appropriate.

In most states, a separate state law exam, such as the Series 63 or Series 66, is also required to conduct business with residents of that jurisdiction. These state-level exams are often required in addition to FINRA licenses.

Other FINRA-administered exams, such as the Series 79 for investment banking, may be required depending on the products or services offered. This license is specific to activities such as advising on or facilitating M&A transactions and cannot be substituted for general securities qualifications.

Some fintech firms choose to license certain individuals to engage in or supervise multiple functions, such as combining Series 7, 63, and Series 24 or adding advisory licenses like the Series 65, to support hybrid business models also engaging in investment advisory activity. This approach can reduce staffing requirements and improve operational flexibility in lean teams.

3. FINRA and State Registration Process

Once the required qualification exams are passed, FINRA automatically records the results in the individual’s Central Registration Depository (CRD) profile, allowing the individual to function in the newly qualified business lines.

In parallel, state registration is required in every jurisdiction where the representative will do business. Most states require passing the Series 63 or 66, along with meeting any local disclosure or fee requirements.

The registered representative cannot conduct any securities activities until both FINRA and the relevant state approvals are confirmed.

Firms must also monitor ongoing changes, such as an individual's address updates, legal actions, or outside business activities, and promptly update Form U4.

Registered Representative vs. Investment Advisor

The lines between registered representatives and investment advisors are often blurred in conversation, but these are two different roles from a regulatory standpoint. Each comes with its own set of rules, licenses, and compensation methods.

A registered representative is affiliated with a broker-dealer and typically earns commissions from securities transactions. Their activity is regulated by FINRA and the SEC, with obligations tied to suitability and Regulation Best Interest (Reg BI) when recommending securities to investors.

An investment advisor representative (IAR) works under a Registered Investment Advisor (RIA) and follows a fiduciary standard. Instead of commissions, IARs typically charge clients based on assets managed or offer flat-fee services. State licensing usually involves passing the Series 65 or a combination of the Series 66 and Series 7.

See how InnReg helps Registered Investment Advisors →

Many modern fintechs combine brokerage and advisory functions. In those cases, firms may be dual-registered, and personnel might hold both sets of licenses. However, the compliance standards differ, and activities must be clearly separated to avoid regulatory issues.

See also:

What a Registered Representative Can and Cannot Do

A registered representative works through a broker-dealer and is approved to handle securities transactions. That includes placing trades, talking clients through investment options, and managing tasks tied to their accounts.

They cannot act on their own. All activity must go through the firm that supervises them. They are not allowed to take custody of client funds, make performance guarantees, or give investment advice unless properly licensed to do so.

The scope of what they can do depends on their licenses and the firm’s setup. This is especially important in fintech, where some platforms combine different asset types. If a rep handles both crypto and securities, the lines need to be clearly drawn and documented.

Need help with broker-dealer compliance?

Fill out the form below and our experts will get back to you.

Regulatory Oversight: FINRA, SEC, and State Authorities

Registered representatives answer to several different regulators. FINRA, the SEC, and state securities agencies all play a role, and each brings its own set of rules:

FINRA handles exams, licensing, continuing education, and day-to-day conduct. It also writes and enforces rules for how broker-dealers and their reps operate.

The SEC sets broader federal standards, focusing on market integrity, fraud prevention, and disclosures. FINRA’s rulebook is shaped around those federal guidelines.

States require their own registration steps. Depending on where business is done, that may include extra filings, fees, or disclosures.

Firms need to keep all three in mind when building compliance programs. Overlooking one can create problems fast.

Compliance Responsibilities of a Registered Representative

Registered representatives must meet ongoing compliance obligations that extend beyond licensing. These include regulatory duties related to suitability, supervision, disclosures, and continuing education.

The key areas firms and individuals must manage on an ongoing basis are:

Compliance Area | Responsibilities |

|---|---|

Suitability and Reg BI | Recommendations must be suitable and in the client's best interest. Firms must implement processes that align with Reg BI, including client profiling, documentation, and conflict oversight. |

Supervision, Recordkeeping, and Disclosures | Firms are responsible for reviewing communications, monitoring rep activity, and archiving business-related correspondence. Reps must explain risks and costs clearly and use approved materials. |

Continuing Education and Form U4/U5 | Reps must complete annual CE (Regulatory and Firm Elements), keep Form U4 up to date, and Firms must ensure timely U5 filings upon termination or departure. |

Suitability and Regulation Best Interest (Reg BI)

Registered representatives must base product recommendations on suitability standards and, for retail clients, comply with Regulation Best Interest (Reg BI). This means not only understanding the client's investment profile, financial goals, and risk tolerance before making any recommendation, but also understanding the product being recommended, especially complex products.

Under Reg BI, recommendations must not only be suitable but also in the client’s best interest. This includes avoiding conflicts or disclosing them clearly, considering lower-cost alternatives when appropriate, and documenting the rationale behind recommendations.

Fintech firms offering securities to retail users must implement processes, automated or manual, that align with Reg BI. This includes compliance reviews of marketing materials, workflows for documenting client interactions, and supervisory systems that monitor representative activity.

Supervision, Recordkeeping, and Disclosures

Broker-dealers are responsible for supervising their registered representatives. That supervision includes reviewing communications before use, overseeing client interactions, and tracking trading activity as it happens.

Firms must also keep detailed records. Emails, chats, and other client-facing communications, if business-related, must be archived under FINRA and SEC rules.

Representatives must explain product features, risks, and costs in a way clients can understand. Leaving out key details or using language that has not been approved may raise compliance concerns.

Continuing Education and Form U4/U5 Obligations

Registered representatives must complete continuing education (CE) on an annual basis, as required by FINRA. This includes both the Regulatory Element, delivered through FINRA, and the Firm Element, which is assigned by the broker-dealer based on the rep’s role.

In addition to training, representatives are responsible for keeping their Form U4 up to date. Any changes to a representative’s status, like a new address, a regulatory event, or a side business, need to be reported without delay. If someone leaves the firm, the broker-dealer files a Form U5 that outlines the reason for the departure.

Missing a CE deadline or failing to keep records current can put a registration at risk. In fast-moving fintech teams, staying on top of these tasks often requires coordination between compliance, operations, and HR.

Common Compliance Challenges for Fintech Companies

Fintech companies building in the securities space often run into compliance hurdles when working with registered representatives.

These problems usually stem from rapid growth, mixed business models, or vague role boundaries:

Using Unregistered Salespeople: Paying unlicensed staff to refer clients or discuss investment features can trigger broker-dealer registration requirements. Compensation tied to transactions is a common red flag for regulators.

Misclassifying Roles or Titles: Calling someone an “advisor” or “consultant” without the right license can create problems. The title needs to match what the person is actually allowed to do.

Remote Supervision and Technology Integration: With distributed teams, it becomes harder to track day-to-day activity. Supervision tools need to be built for flexibility without losing control. Firms must adapt supervisory systems to cover off-site reps without weakening oversight.

Dual-Registration and Blurred Business Models: Fintech platforms that combine brokerage and advisory services often face confusion around which hat a representative is wearing. Activities must be clearly separated and tracked under the correct regulatory framework.

See also:

When Does Your Startup Actually Need a Registered Representative?

Not every fintech needs a registered representative on day one. But once your product involves soliciting or facilitating securities transactions, registration requirements come into play. This includes functions like promoting investment features, handling customer trades, or offering investment-related customer support.

If your platform allows users to trade stocks, purchase funds, or interact with any product considered a security, you are likely operating in broker-dealer territory. At that point, either someone on your team must become registered, or you need to partner with a firm that already has licensed reps in place.

—

The role of a registered representative is not just a formality. It is a regulated function with real legal and operational consequences. If your business touches securities, registration is often not optional.

Founders, legal teams, and compliance leads should factor this in when designing product features, onboarding flows, or compensation models. Missteps are rarely about bad intent. They usually come from underestimating how quickly a product crosses into regulated territory.

Bringing in expertise early, whether in-house or outsourced, can keep growth plans on track without creating avoidable risk. Clarity on registration needs is not just a legal box to check. It is part of building a business that can scale under scrutiny.

Tarik is a Principal Compliance Consultant at InnReg with over 5 years of experience advising fintech clients across broker-dealer, RIA, and money transmitter verticals. He holds FINRA Series 3, 7, 24, 57, 63, 79, and 99 licenses, with expertise in regulatory strategy, supervisory systems, and compliance roadmap implementation.

How Can InnReg Help?

InnReg is a global regulatory compliance and operations consulting team serving financial services companies since 2013.

We are especially effective at launching and scaling fintechs with innovative compliance strategies and delivering cost-effective managed services, assisted by proprietary regtech solutions.

If you need help with broker-dealer compliance, reach out to our regulatory experts today:

Related Articles

Featured LinkedIn Posts