Broker-Dealer Registration Exemptions in the US

Broker-dealer registration exemptions are often the first thing founders and legal teams look for when a fintech business model starts touching securities activity. The reason is simple. Full broker-dealer registration comes with significant operational, supervisory, and cost implications, and not every activity triggers that obligation.

This article breaks down how broker-dealer registration exemptions work in the US, where they apply, and where they tend to fail. It also covers how the SEC analyzes broker activity, the most commonly relied-upon exemptions, and the boundaries that matter during exams and enforcement reviews.

At InnReg, we help broker-dealers and fintech companies evaluate whether broker-dealer registration exemptions apply to their business models. From assessing activity, compensation, and platform design to supporting registration when exemptions no longer fit, our team provides practical regulatory guidance.

What Is a Broker-Dealer and Why Is Registration Required?

A broker-dealer is a person or firm that helps facilitate securities transactions for others or for its own account.

This can include raising capital, introducing buyers and sellers, or earning transaction-based compensation tied to a deal’s success. These activities often show up early in fintech business models, sometimes before teams realize they carry regulatory weight.

That’s where registration comes in. By registering, a firm agrees to operate under SEC and FINRA oversight aimed at protecting investors. This oversight brings supervision, recordkeeping, and conduct rules that affect daily operations.

Want to understand how registered broker-dealers are structured? Learn how fully disclosed, omnibus, and self-clearing models differ →

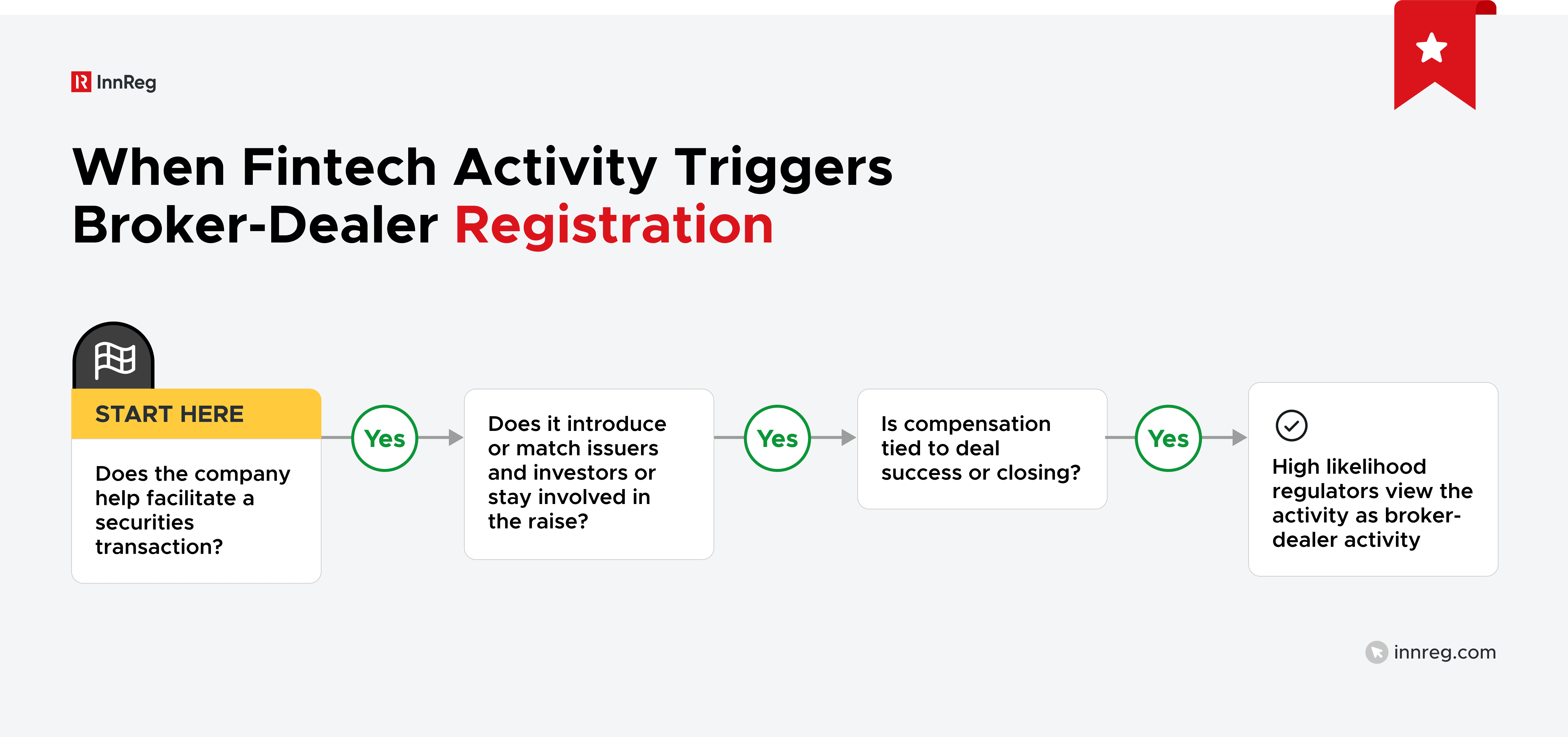

What the SEC Considers “Broker” Activity

The Securities and Exchange Commission (SEC) looks at what a business actually does, not how it describes itself. Titles, disclaimers, or marketing language don’t carry much weight if the underlying activity looks like brokerage.

Regulators evaluate a consistent set of factors, and no single one controls the outcome. As more of these elements appear together, the likelihood that registration is required increases.

Key factors include:

Involvement in securities transactions, even without handling funds or securities

Introducing or matching buyers and sellers in connection with an investment

Transaction-based compensation, such as commissions, success fees, or payments tied to a deal closing

Ongoing participation in the deal process, including support with negotiations or structuring

When these factors start to overlap, regulators are much more likely to view the activity as broker-dealer activity rather than a passive or administrative role.

How Common Fintech Roles Trigger Registration

Many fintech companies don’t think of themselves as broker-dealers, but certain roles can pull them into that category. The risk usually comes from what the company is helping to facilitate, not from what it calls itself.

Take a platform that helps startups raise capital. If the team actively connects issuers with investors, stays involved throughout the raise, and gets paid when the deal closes, that combination raises red flags. The same goes for consultants or advisors who introduce parties and receive transaction-based compensation.

Another common example is marketplace-style platforms. A company may see itself as a neutral technology provider, but if it curates deals, negotiates terms, or nudges parties toward a transaction, regulators may see a more active role.

The more a fintech influences who transacts and how, the harder it is to stay outside broker-dealer rules.

When a Business Is Considered “In the Business” of Brokerage

The SEC doesn’t expect every one-off introduction to trigger broker-dealer registration. What matters is whether a company is regularly engaged in brokerage activity as part of its business model.

Frequency and intent both play a role. If a firm consistently brings parties together for securities transactions and expects to be paid for it, regulators are more likely to view it as being in the business of brokerage.

This is especially true when the activity is marketed as a service or baked into the product offering. Doing something once is different from building a repeatable process around it.

For example, a founder who casually introduces two contacts to help with a single raise is unlikely to raise concerns. But a platform that promotes its ability to connect issuers and investors and does so across multiple deals starts to look very different.

At that point, brokerage isn’t incidental; it’s part of the business.

This distinction matters because exemptions often depend on how active and ongoing the activity is.

Overview of Broker-Dealer Registration Exemptions

Broker-dealer registration exemptions exist because not every securities-related activity requires full registration. They are narrow, fact-specific, and often misunderstood.

The sections below explain the exemptions fintechs most often rely on and where teams commonly misapply them.

Issuer Exemption

The issuer exemption applies when a company raises capital for itself, rather than for someone else.

If a business is selling its own securities and not acting on behalf of other issuers, it may fall outside broker-dealer registration requirements. This exemption is commonly relied on by startups during early fundraising rounds.

The key limitation is compensation. Founders, employees, or officers can’t receive transaction-based compensation for selling the company’s securities unless they’re registered. Salaries and equity awards are generally acceptable, but success fees tied to the amount raised are a problem. Therefore, how people are paid matters just as much as what they’re doing.

For example, a startup CEO pitching investors as part of a seed round is usually fine. If that same company hires a consultant who’s paid a percentage of funds raised, the exemption likely falls apart.

M&A Broker Exemption

The M&A broker exemption covers certain intermediaries involved in the sale of privately held companies. It allows an unregistered broker to help facilitate an acquisition, as long as the transaction meets specific conditions set by the SEC.

This exemption is limited to deals involving operating businesses, not passive investments. The buyer must gain control of the company, and the transaction can’t involve a public offering. It also restricts how funds are handled and who the broker can represent.

For example, an advisor helping sell a closely held software company to a strategic buyer may qualify under this exemption. If that same advisor starts arranging minority investments or capital raises, the exemption no longer applies.

Intrastate Exemption

The intrastate exemption is built around a simple idea. If securities activity stays entirely within one state, federal registration may not be required. Both the issuer and the investors must be residents of the same state, and the offering can’t spill across state lines.

This exemption is harder to use than it sounds. Marketing, communications, and even a single out-of-state investor can break it. Online platforms face added risk since websites, emails, and digital ads often reach users nationwide.

For example, a local business raising funds only from in-state investors through private, state-limited outreach may qualify. If that same business promotes the offering online without restricting access by location, it likely won’t.

Teams considering this exemption need to think carefully about distribution, technology, and investor access before relying on it.

JOBS Act Platform Exemption

The JOBS Act created a limited path for certain online platforms to operate without registering as broker-dealers. This exemption is most commonly associated with crowdfunding and capital-raising portals, but it comes with strict boundaries.

Platforms relying on this exemption can host offerings and provide standardized information, but their role must stay passive. They can’t offer investment advice, negotiate terms, or receive transaction-based compensation outside what the rules allow.

Once a platform starts steering investors or shaping deals, the exemption can break down quickly.

For example, a crowdfunding platform that displays issuer information and facilitates investor access may qualify. If that same platform highlights specific offerings as “better” or helps issuers choose investors behind the scenes, it may cross the line.

Foreign Broker-Dealer Exemption

The foreign broker-dealer exemption applies to non-US firms that engage with US investors in limited ways. It allows certain cross-border activity without full US broker-dealer registration, as long as specific conditions are met.

The exemption focuses on who the clients are and where the activity takes place. In many cases, US investors must initiate the contact, or the activity must involve large institutional investors.

Retail solicitation in the US is usually off limits. The more direct the outreach to US investors, the harder this exemption is to rely on.

For example, a foreign broker responding to unsolicited interest from a US institutional investor may qualify. If that same firm starts marketing directly to US retail investors, registration concerns surface quickly.

This exemption can be helpful, but only when cross-border activity is carefully controlled and documented.

Learn more about reverse solicitation in financial services →

See also:

Finder No-Action Relief

Finder no-action relief comes from SEC guidance, not a formal rule. It gives limited comfort to individuals who make introductions between issuers and investors, as long as their role stays narrow and well defined.

The relief is split into tiers.

At the most basic level, a finder can introduce parties and share contact information. More involvement is sometimes allowed, but only if the finder avoids advising on the deal, negotiating terms, or handling funds. Compensation is tightly restricted and often capped, which catches many people by surprise.

For example, an individual who introduces a startup to accredited investors and receives a small, fixed fee may fit within the relief. If that person starts promoting the offering or gets paid based on how much capital is raised, the protection likely disappears.

Need help with broker-dealer compliance?

Fill out the form below and our experts will get back to you.

What Broker-Dealer Registration Exemptions Actually Do

Broker-dealer registration exemptions don’t remove regulation. They limit when full registration is required based on the nature of the activity and how restricted the role is. Understanding these limits helps teams avoid assuming an exemption provides broader coverage than it actually does.

What an Exemption Allows You to Avoid

A broker-dealer registration exemption can narrow a company’s regulatory footprint, but it does not eliminate regulatory oversight. The main relief is avoiding full broker-dealer registration and FINRA membership, which often drive the highest costs and staffing demands.

When an exemption applies, a business may avoid:

Registering as a broker-dealer with the SEC

Becoming a FINRA member and complying with FINRA supervision rules

Hiring licensed principals and registered representatives

Building a complete broker-dealer supervisory and compliance infrastructure

These carve-outs can be meaningful, especially for early-stage teams. At the same time, anti-fraud rules and other applicable regulations still apply, so exemptions work best when they’re paired with clear internal controls and ongoing monitoring.

Who Typically Qualifies for Exemptions

Broker-dealer registration exemptions are usually designed for limited, clearly defined roles, not full-service intermediaries. Companies that qualify often have a narrow scope of involvement and avoid activities tied closely to closing transactions.

Common examples include:

Founders raising capital for their own companies

Advisors involved in a single M&A transaction

Platforms that provide passive tools without steering investors

In these cases, the business stays close to information sharing rather than deal execution. The less influence a company has over the transaction, the more likely an exemption fits.

Why Exemptions Exist in the First Place

Broker-dealer registration exemptions exist because not every securities-related activity carries the same level of risk. Some transactions are limited in scope, involve sophisticated parties, or don’t raise the same investor protection concerns as traditional brokerage.

Regulators use exemptions to strike a balance. They allow capital formation and business transactions to move forward without forcing every participant into a full broker-dealer framework.

This is especially important for startups, founders, and one-off transactions that would struggle with the cost and complexity of registration.

For example, a founder raising money for their own company or an advisor helping sell a privately held business presents a different risk profile than a firm regularly matching investors and issuers.

How to Tell If an Exemption Applies to You

Determining whether an exemption applies isn’t about labels or intentions. It comes down to facts, behavior, and your role in the transaction.

How Compensation Factors Into the Analysis

How you get paid is one of the first things regulators look at. Transaction-based compensation is a strong signal of broker activity, especially when payment depends on whether a deal closes.

Fixed fees, salaries, and equity awards are generally lower risk because they aren’t tied to the outcome of a securities transaction. By contrast, success fees, percentages of capital raised, or commissions quickly raise concerns. Even small payments can matter if they’re structured around deal completion.

See also:

How Many Deals Is “Too Many?”

There’s no bright-line rule for how many transactions trigger broker-dealer concerns. What matters more than the number of deals is whether deal activity looks ongoing and expected, rather than occasional and incidental.

A single, isolated transaction may fit within an exemption. Repeating the same activity across multiple deals starts to look like a business model. The risk increases if the company markets its role, builds processes around deal facilitation, or expects to earn compensation each time.

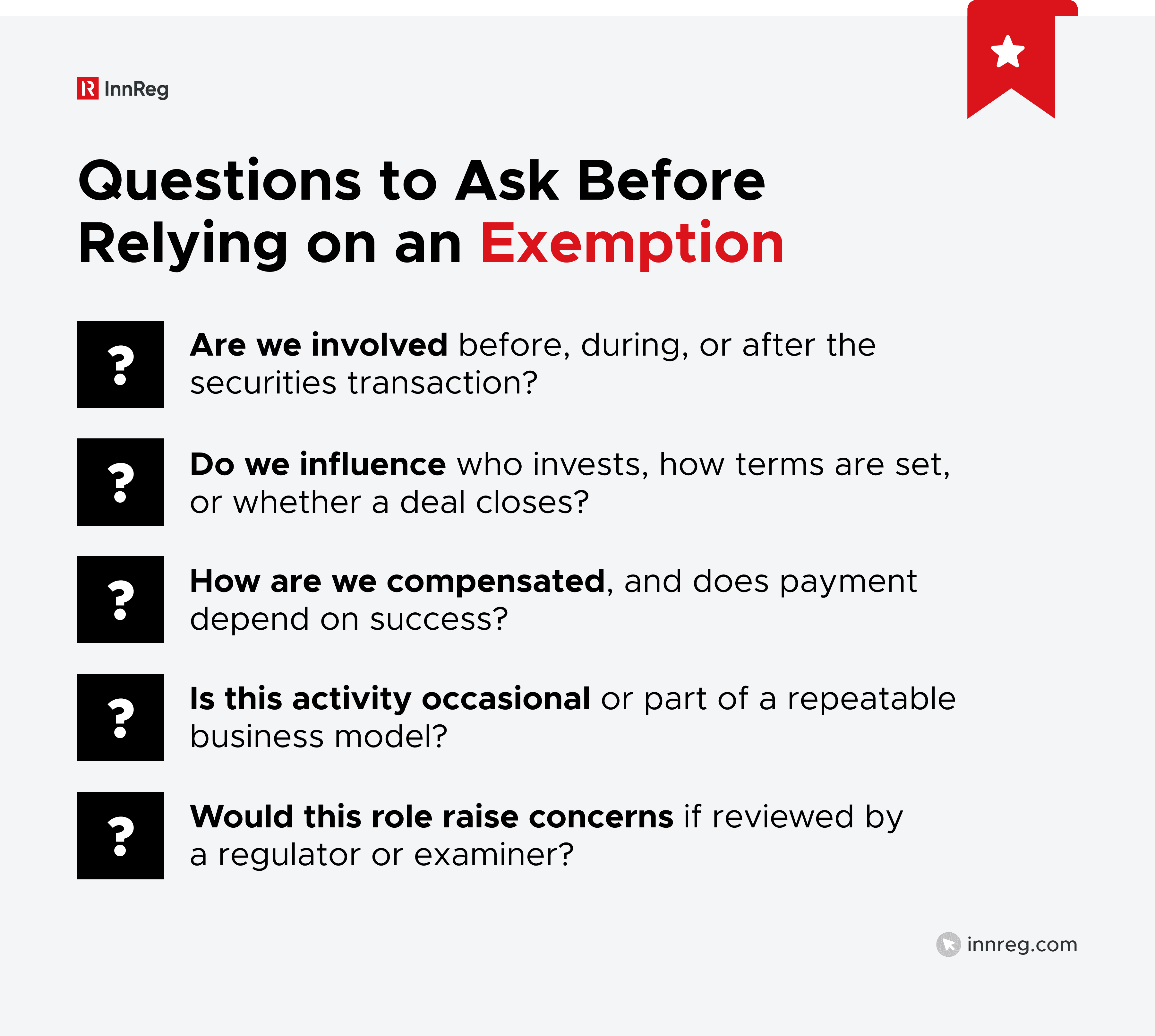

Questions Founders and Legal Teams Should Ask Themselves

Before relying on a broker-dealer exemption, it helps to step back and ask practical questions. Small details around role, involvement, and compensation often matter more than intent.

We put together the visual checklist below to summarize the key questions founders and legal teams should ask when assessing broker-dealer exemption risk.

If you answer “yes” to most of these questions, it becomes harder to rely on a broker-dealer exemption.

For example, a platform that only provides information may answer “no” to most of these questions. But a business earning success-based fees across multiple deals would likely answer “yes.” Walking through these questions early helps teams identify risk while there’s still room to adjust.

How State Laws Affect the Use of Exemptions

Federal exemptions don’t operate in isolation. State securities laws can still apply, even when an activity fits within a federal exception.

Why a Federal Exemption Doesn’t Preempt State Rules

A federal broker-dealer exemption doesn’t automatically override state securities laws. States can still require registration, notice filings, or their own exemptions, even when federal relief applies.

State regulators focus on protecting investors within their borders. If an issuer, investor, or intermediary is located in a particular state, that state’s rules may come into play. This often applies to M&A transactions and private offerings that involve parties in multiple states.

Which States Adopted NASAA’s M&A Broker Exemption

States haven’t taken a uniform approach to the M&A broker exemption. Many have adopted versions of the North American Securities Administrators Association (NASAA) model rule, but the scope and conditions vary, which makes state-by-state review important.

Exemption Approach | States |

|---|---|

Statutory M&A Broker Exemption | Alaska, Arkansas, Colorado, Florida, Illinois, Iowa, Michigan, Mississippi, Montana, Nebraska, Oklahoma, Pennsylvania, South Carolina, South Dakota, Tennessee, Texas, Utah, Vermont |

M&A Broker Relief via Regulatory Guidance | Georgia, Maryland |

Washington is often discussed in this context, too, but it’s generally treated separately because it’s described as having other fact-specific exemptions rather than a clear M&A broker carveout.

Because adoption and interpretation differ, teams should always confirm how each relevant state applies the exemption before relying on it.

Where to Look for Additional Registration Triggers

Even when an exemption seems to apply, other parts of the business can still create registration risk. Registration issues often come from activities outside the core transaction, not the deal itself.

Common areas to review include marketing language, sales practices, and compensation structures. For example, a platform may qualify for an exemption based on how it structures transactions. However, claims on its website about “connecting investors” or highlighting fundraising success can change how regulators view the role.

Side arrangements can also matter. Referral fees, success-based bonuses, or informal introductions handled by sales teams may introduce broker-dealer activity without anyone realizing it. Looking beyond the transaction helps teams catch these issues early, while there’s still time to adjust.

How Fintechs Can Use or Avoid Exemptions Strategically

Fitting within an exemption often comes down to design choices. How a platform operates and how deals are structured can make or break exemption eligibility. Small adjustments early can reduce regulatory risk later.

See also:

When to Use an Exemption Versus Registering

Choosing between an exemption and registration is a business decision, not just a legal one. Exemptions work best for limited, short-term, or narrowly defined activities, while registration makes more sense when securities involvement is core to the model.

An exemption may be the right fit if the activity is occasional, tightly scoped, and easy to contain. For example, a founder raising capital for a single company or an advisor working on one private sale may be able to operate comfortably within an exemption. The tradeoff is flexibility, since exemptions limit how involved you can be and how you get paid.

Registration starts to make more sense when deal activity is repeatable or central to revenue. A platform that expects to facilitate transactions at scale may find that exemptions slow growth or create constant edge cases. In those situations, registering early can provide clarity, even if it comes with a higher upfront cost and operational effort.

How to Structure a Platform or Deal to Fit Within an Exemption

Staying within an exemption usually depends on how much control and influence a business has over a transaction. Platforms that remain passive and avoid steering transactions have a better chance of qualifying.

For platforms, this often means avoiding activities like recommending specific investments, negotiating terms, or pushing deals toward closing. For example, a marketplace that displays issuer profiles and lets investors reach out directly carries less risk than one that actively matches parties and manages the process.

Compensation design matters just as much. Fixed fees or subscriptions are usually safer than success-based payments. A platform charging issuers a flat listing fee may fit within an exemption, while one earning a percentage of funds raised likely won’t.

Clear boundaries around role, features, and payment help exemptions hold up over time.

Internal Compliance Measures That Make or Break the Strategy

Exemptions rely on consistent internal controls that keep activity within defined limits, even as the business grows.

This includes clear policies around marketing, compensation, and employee conduct. For example, sales teams should know what they can and can’t say about deals, and product teams should understand which features could create registration risk. Training and documentation help keep everyone aligned.

Many fintechs struggle here because no one owns the compliance function day to day. That scenario is why firms partner with InnReg.

InnReg often operates as an outsourced compliance department, bringing fintech-specific regulatory experience and practical controls without the cost of an entire in-house team. You focus on growth while we help mitigate regulatory risks.

—

Broker-dealer registration exemptions can be useful, but they’re narrow and fact-driven. Small differences in role, compensation, or frequency of activity can change the regulatory outcome, sometimes quickly.

For fintech founders and legal teams, the real value comes from understanding where exemptions fit into a broader regulatory strategy. In some cases, an exemption supports early-stage growth. In others, planning for registration sooner avoids friction later. The key is making that choice intentionally, with a clear view of how the business operates today and where it’s headed.

FAQs About Broker-Dealer Exemptions

Here are the questions founders and legal teams always ask about exemptions versus registration.

What is the issuer's exemption for broker-dealers?

The issuer’s exemption allows a company to sell its own securities without registering as a broker-dealer, as long as it’s raising capital for itself and not for others. Founders and employees can speak with investors as part of this process, but they can’t receive transaction-based compensation tied to the amount raised. Salaries and equity awards are typically acceptable, while success fees are not.

What securities are exempt from registration?

Some securities are exempt from registration based on how they’re offered or who they’re offered to. Common examples include private placements under Regulation D, intrastate offerings, and certain crowdfunding securities. These exemptions reduce registration requirements for the securities themselves, but they don’t automatically exempt the people or platforms involved from broker-dealer rules.

Does an issuer need to register as a broker-dealer?

An issuer doesn’t need to register as a broker-dealer when it’s selling its own securities, as long as it isn’t acting on behalf of others or paying transaction-based compensation. Founders and employees can raise capital for the company without registration, but bringing in third parties paid based on deal success can trigger broker-dealer requirements.

What is the M&A exemption for broker-dealers?

The M&A exemption allows certain intermediaries to help facilitate the sale of a privately held operating company without registering as a broker-dealer. It applies when the transaction results in a change of control and doesn’t involve a public offering. The exemption is limited and fact-specific, so it won’t cover capital raises or minority investment deals.

Who is exempt from registration under the Securities Act of 1933?

Certain issuers and transactions are exempt from registration under the Securities Act of 1933, such as private placements, intrastate offerings, and offerings to accredited investors. These exemptions apply to the securities being offered, not automatically to the people or firms involved in selling them, which is where broker-dealer registration questions often arise.

Are all US broker-dealers registered with FINRA?

Most US broker-dealers are registered with both the SEC and FINRA, since FINRA membership is required for firms that deal with the public. Some limited-purpose broker-dealers may register with the SEC without FINRA membership, but those cases are rare and depend on the firm’s activities.

Maria is a Compliance Consultant at InnReg delivering compliance solutions for fintech clients across broker-dealer, RIA, and money transmitter verticals. She brings prior experience at Finalis, Fenix Securities and PwC, with expertise in AML, CCO support, investment banking operations and securities compliance. She holds FINRA Series 14, 24, and 82 licenses and actively supports regulatory and compliance processes revolving broker-dealer activities.

How Can InnReg Help?

InnReg is a global regulatory compliance and operations consulting team serving financial services companies since 2013.

We are especially effective at launching and scaling fintechs with innovative compliance strategies and delivering cost-effective managed services, assisted by proprietary regtech solutions.

If you need help with broker-dealer compliance, reach out to our regulatory experts today:

Related Articles

Featured LinkedIn Posts