Regulation S-P: A Complete Guide For Broker-Dealer Compliance

Regulation S-P is the cornerstone of privacy and data protection rules for broker-dealers and investment advisors in the United States. It defines how firms must handle, protect, and potentially disclose customer financial information, which is a responsibility that has grown more complex as technology reshapes the way financial services operate.

For broker-dealers, the regulation is now more about maintaining client trust and managing risk in a data-driven marketplace. In 2026, new amendments will take full effect, expanding these obligations. These updates significantly raise the bar for data security and operational readiness across the industry.

This guide explains what Regulation S-P covers, how it applies to broker-dealers, and what steps firms should take to meet both existing and upcoming requirements. You’ll find practical insights into compliance challenges, recent enforcement trends, and strategies that help financial institutions stay aligned with regulators while continuing to innovate.

At InnReg, we help broker-dealers and investment advisors build and operate Regulation S-P privacy and data security programs, including safeguards, incident response, and vendor oversight aligned. Contact us to learn more.

What is Regulation S-P?

Regulation S-P is a privacy and data protection rule issued by the Securities and Exchange Commission (SEC) under the Gramm-Leach-Bliley Act. It requires financial institutions to protect the nonpublic personal information (NPI) of their customers and explain how that information is shared and safeguarded.

The regulation applies to both traditional and tech-driven financial firms and touches nearly every operational layer, including:

Onboarding

Data storage

Marketing

Vendor relationships

At its core, Regulation S-P gives firms the flexibility to use technology and data to serve clients efficiently, but it also sets boundaries on how far that data can travel outside secure systems. In practice, this means broker-dealers must not only have written policies but also demonstrate that those policies work in real-world operations.

Who Must Comply

Regulation S-P applies broadly to SEC-registered broker-dealers, investment advisors, and investment companies. It also covers transfer agents and certain other financial intermediaries handling client data.

The rule applies regardless of a firm’s size or business model. Whether a startup operates a mobile trading platform or a large broker-dealer manages traditional accounts, the same privacy standards apply.

Importantly, the regulation differentiates between consumers and customers:

Consumer | Customer |

|---|---|

Obtains a financial product or service for personal use | Ongoing relationship between consumer and the firm, such as a brokerage account |

This distinction matters because customer relationships trigger broader notice and safeguard obligations. Many fintech startups underestimate this requirement when designing automated onboarding flows. Integrating compliance steps like delivering privacy notices and tracking consent into digital account setups can help avoid early missteps.

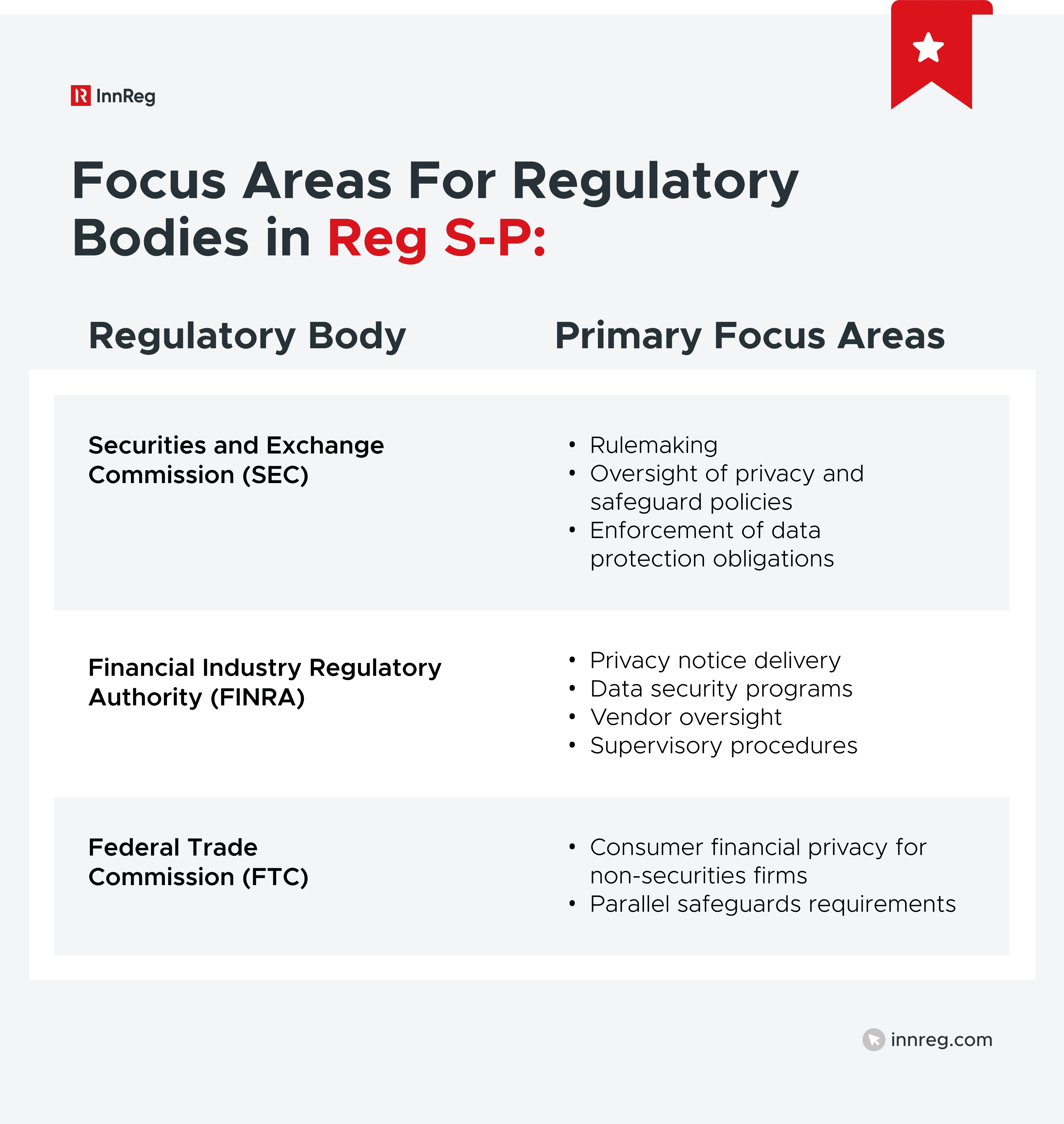

Key Regulators and Enforcement Bodies

Three main key regulatory bodies focus on Regulation S-P. Here is an overview of the bodies and their role in Regulation S-P:

Securities and Exchange Commission (SEC): Primary authority overseeing Regulation S-P for broker-dealers, investment advisors, and investment companies

Financial Industry Regulatory Authority (FINRA): Enforces Regulation S-P compliance among member broker-dealers through examinations and enforcement actions

Federal Trade Commission (FTC): Oversees similar privacy standards under the Gramm-Leach-Bliley Act for non-SEC-regulated financial institutions

In recent years, regulators have emphasized that written policies are not enough. Firms must demonstrate operational compliance, showing that safeguards are active, tested, and monitored. That shift reflects a broader trend: compliance is no longer just about documentation, but about execution.

Core Requirements Under Regulation S-P

Regulation S-P establishes a framework that governs how financial institutions handle customer information from collection to disposal. Broker-dealers must meet three central obligations:

Providing clear privacy notices

Implementing written safeguards to protect data

Disposing of customer information securely when it’s no longer needed.

Each requirement ties directly to protecting client trust and limiting exposure to regulatory and reputational risks.

Privacy Notices

Every broker-dealer must provide customers with a clear and conspicuous privacy notice explaining how their personal financial information is collected, used, and shared.

This notice must be given at the start of the relationship and delivered annually, unless the firm qualifies for the limited annual notice exemption.

A compliant privacy notice should include:

Categories of information collected from customers

How that information is used and shared, including whether it is shared with nonaffiliated third parties

The customer’s right to opt out of certain information-sharing practices

Details on the firm’s data protection measures

For fintech firms with automated onboarding or digital account opening processes, integrating privacy notice delivery and opt-out options directly into the user interface is essential. The SEC and FINRA closely review the timing of these disclosures during examinations, particularly when they’re embedded in mobile or web platforms.

The Safeguards Rule

Regulation S-P’s Safeguards Rule requires broker-dealers to adopt written policies and procedures designed to protect customer records and information. These policies should address administrative, technical, and physical controls that reduce the risk of unauthorized access or data loss.

Common elements of an adequate safeguards program include:

Access controls based on job function and data sensitivity

Encryption for sensitive information at rest and in transit

Employee training on data protection and phishing awareness

Vendor due diligence and ongoing oversight

Incident response planning and breach escalation procedures

Regulators expect these programs to reflect actual business operations, not generic templates. During recent SEC and FINRA exams, firms were cited for outdated safeguard policies that had never been implemented or tested.

Maintaining accurate, operationally aligned procedures is now a fundamental compliance expectation.

Secure Disposal of Customer Information

The Disposal Rule, a component of Regulation S-P, requires firms to securely dispose of customer and consumer report information once it’s no longer needed for business or regulatory purposes.

Acceptable disposal methods include:

Shredding or pulverizing paper records

Permanently deleting or wiping digital files from storage devices

Using certified vendors for the destruction of electronic media

Recent enforcement actions have shown that improper disposal, such as reselling servers with unencrypted data, can lead to significant penalties. Secure disposal is not optional but instead a regulatory requirement that helps protect customers from identity theft and firms from costly investigations.

See also:

Regulation S-P Updates and 2026 Implementation

The 2026 Regulation S-P amendments represent the most significant overhaul of the rule since it was first introduced. These updates expand the definition of customer information, modernize cybersecurity expectations, and introduce new obligations for broker-dealers to detect, respond to, and report data breaches.

By late 2025 and mid-2026, all covered firms will need to demonstrate operational readiness under these standards.

Need help with broker-dealer compliance?

Fill out the form below and our experts will get back to you.

Key Changes Taking Effect in 2026 for Broker-Dealers

The 2026 amendments strengthen Regulation S-P in four main areas:

Incident response programs must be written, tested, and integrated into each firm’s safeguards framework.

Breach notification obligations require prompt communication to affected customers.

Vendor oversight becomes a formal compliance responsibility, not a best practice.

Recordkeeping and documentation requirements expand to cover all privacy and data security activities.

These changes reflect regulators’ focus on accountability and transparency. Broker-dealers must now show that they can detect security incidents quickly, contain them effectively, and document every step of their response.

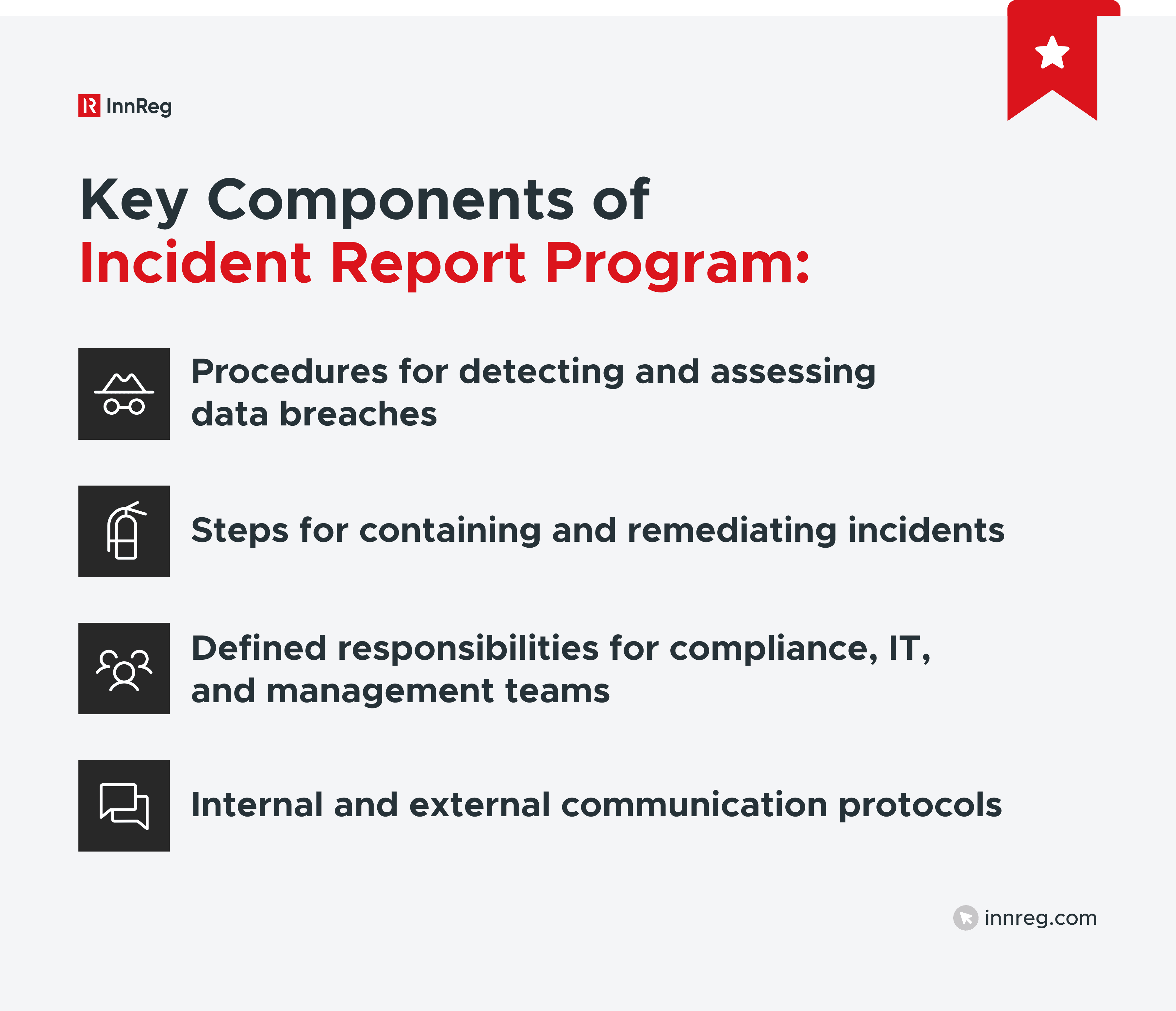

Mandatory Incident Response and Breach Notification Programs

Under the 2026 rules, every broker-dealer must maintain a written incident response program that outlines how it will identify, investigate, and recover from unauthorized access to customer information.

If sensitive customer information is compromised, firms must notify affected individuals as soon as practicable, and no later than 30 days after becoming aware of the incident.

The notice must describe the nature of the breach, the information involved, what customers can do to protect themselves, and information to assist affected individuals.

Also required is the date of the incident, the estimated date of the incident, or the range in which the incident occurred, if reasonably possible to determine. Firms should also maintain detailed records of how each breach was managed, as regulators will review these during examinations.

Vendor Oversight and Third-Party Breach Reporting

The 2026 amendments make vendor oversight a formal requirement under Regulation S-P. Broker-dealers must take reasonable steps to confirm that third-party service providers handling customer data maintain appropriate safeguards.

When engaging vendors/service providers, firms must conduct oversight of each entity to ensure they take appropriate measures to:

Protect against incidents related to customer information.

Provide notification to the broker-dealer within 72 hours of discovery of a breach in security resulting in unauthorized access to customer information.

Permit the broker-dealer to review the vendor’s security practices upon request.

This change is especially relevant for fintech firms that depend heavily on cloud platforms, data analytics partners, and outsourced software developers. Regulators will hold the broker-dealer responsible for lapses by its vendors, even when data exposure originates outside the firm’s direct control.

New Recordkeeping and Documentation Standards for 2026

Recordkeeping obligations now extend to all areas of a firm’s privacy and information security program. Broker-dealers must maintain:

Copies of written policies, procedures, and incident response plans

Records of all privacy notices and opt-out communications

Documentation of staff training sessions related to data protection

Logs of vendor due diligence and breach response activities

Accurate, well-organized records will serve as evidence of compliance during SEC and FINRA examinations. Firms that cannot produce documentation quickly are likely to draw closer regulatory scrutiny.

Implementation Timeline and Transition Plan for Large vs. Small Firms

The SEC has set two key compliance dates:

Large firms | Small firms |

|---|---|

December 31, 2025 | June 3, 2026 |

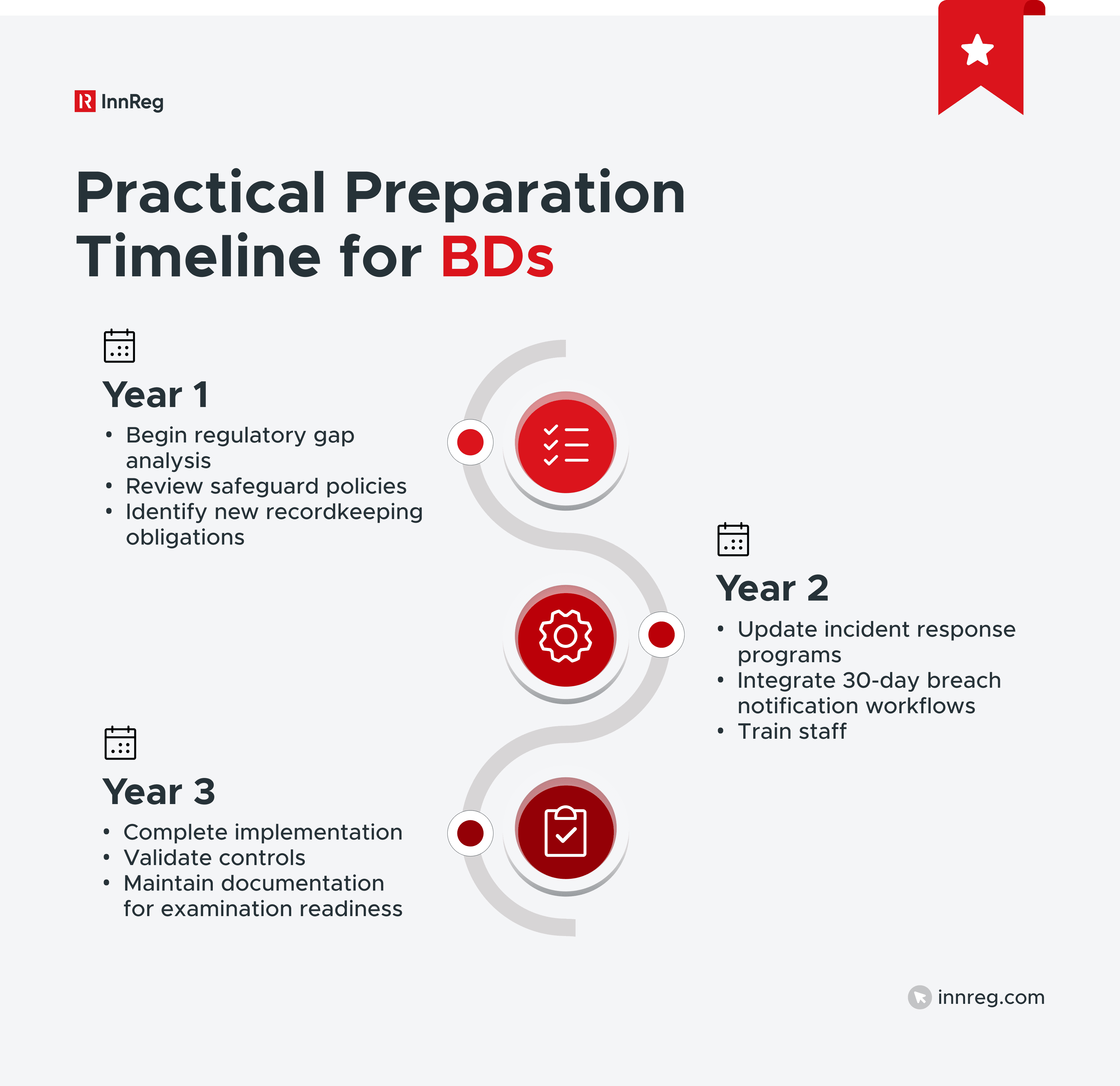

To meet these deadlines effectively, broker-dealers should follow a structured transition plan:

Q4 2024-Q2 2025: Conduct a Regulation S-P gap analysis and identify all required updates to systems, vendor contracts, and internal policies.

Q3-Q4 2025: Finalize and test new policies, incident response plans, and breach notification templates. Large firms must be fully compliant by December 31, 2025.

2026 onward: Fully operationalize reporting workflows, maintain documentation, and provide refresher training for all staff.

For fast-growing fintech firms, working with experienced compliance partners can simplify this transition. InnReg helps firms operationalize these complex updates efficiently. We can combine regulatory expertise, fintech understanding, and a practical, process-driven approach to implementation.

Regulation S-P Compliance Deadlines

The updated Regulation S-P compliance deadlines mark a clear timeline for when firms must implement the new privacy, cybersecurity, and recordkeeping standards. The SEC’s phased approach gives larger firms an earlier deadline, followed by smaller entities six months later:

December 31, 2025: Deadline for large broker-dealers, transfer agents and investment companies.

June 3, 2026: Deadline for small broker-dealers and investment advisors.

For most broker-dealers, this transition means more than meeting a single date. It involves preparing systems, training staff, updating vendor contracts, and verifying that new breach response procedures are operational by the effective date.

See also:

Common Compliance Challenges for Broker-Dealers

Regulation S-P compliance often breaks down not because of unclear rules, but because of operational gaps. For broker-dealers, these are the most common challenges regulators continue to flag:

Missed or Incomplete Privacy Notices

Some firms still fail to provide the required privacy notices at account opening or during annual reviews. In others, the notices exist but lack the disclosures Regulation S-P requires.

Common causes include:

No automated trigger in digital onboarding workflows

Lack of a centralized record of customer notice delivery

Overreliance on outdated templates that don’t reflect actual data-sharing practices

Failing to issue or document privacy notices is one of the easiest red flags for regulators to identify. Firms should incorporate notice delivery and acknowledgment into client onboarding systems and maintain evidence of each interaction.

Outdated or Generic Safeguard Policies

The Safeguards Rule requires written, risk-based data protection programs. Yet many broker-dealers still use static templates that don’t match their actual operations.

Key warning signs include:

Generic policies that don’t reference current technology or vendor setups

Procedures that exist on paper but aren’t applied in daily workflows

No record of periodic reviews or testing of controls

Regulators expect active, tested safeguards that reflect a firm’s technology stack and threat landscape. This includes revisiting policies whenever a new system, vendor, or product feature is introduced.

Weak Encryption and Device Controls

In a mobile-first environment, sensitive client data often moves between multiple platforms and devices. Weak encryption or lax device policies can lead to unnecessary exposure.

Some of the most common signs of weak encryption and device controls are as follows:

Employees are using personal devices without security controls

Lack of data encryption for stored or transmitted information

Inadequate monitoring of who accesses client files or downloads reports

Updating access controls and enforcing device management policies is now considered a baseline compliance standard.

Gaps in Employee Training and Access Management

Even strong policies fail without proper training. Employees often become the weak link when they don’t understand phishing risks, data-handling procedures, or breach escalation steps.

Firms should:

Conduct data security and privacy training at least annually

Tailor content for different roles (operations, technology, compliance)

Maintain attendance logs and quiz results as part of recordkeeping

Training is both a compliance and cultural priority. The most effective programs make privacy part of daily behavior rather than a yearly requirement.

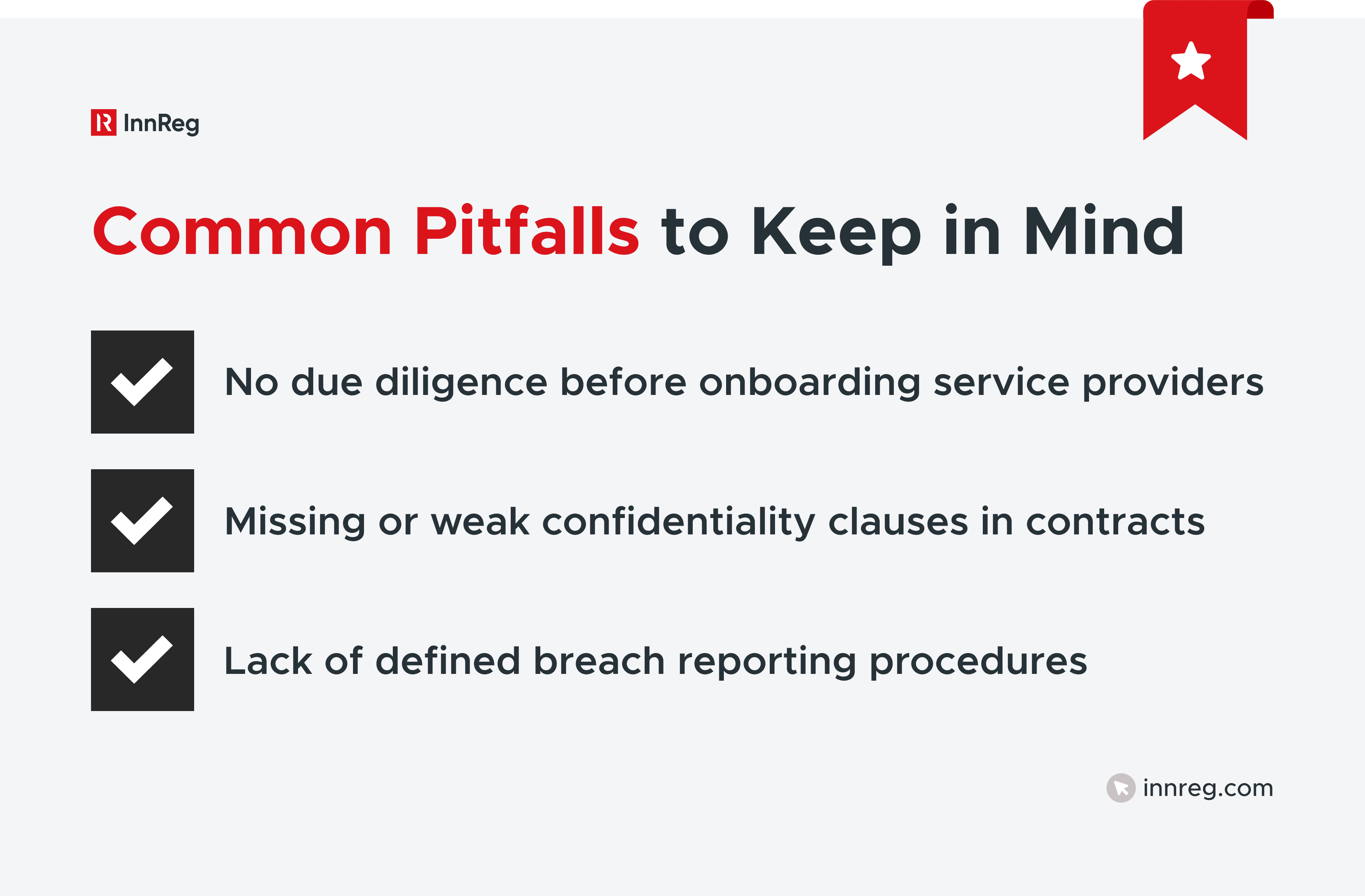

Vendor Oversight and Contract Deficiencies

Many fintech broker-dealers rely heavily on third-party technology providers. But vendor oversight is often reactive rather than proactive.

Under the 2026 rules, broker-dealers are directly accountable for vendor data incidents. Conducting vendor risk assessments and maintaining contractual controls are now integral to ongoing Regulation S-P compliance.

Incident Response Planning Pitfalls

Some firms have incident response plans, but few test them regularly. Others treat data breach management as an IT issue, not a cross-departmental responsibility.

An effective plan should:

Define response roles across compliance, IT, and legal

Include escalation steps and communication protocols

Be tested through periodic simulations or tabletop exercises

The 30-day breach notification requirement makes timing critical. Firms that haven’t rehearsed their procedures risk delayed responses and heightened regulatory exposure.

Misconceptions About Regulation S-P

Regulation S-P has been in place for over two decades, but misconceptions continue to create compliance gaps. Many misunderstandings arise from assuming the rule is static or only applies to traditional firms.

The 2026 updates make it even more critical to separate fact from assumption. Here are the three misconceptions to correct:

Belief that Outsourcing Shifts Responsibility

Some firms assume that outsourcing compliance or IT functions transfers the regulatory burden to a third party. It does not. The broker-dealer remains fully responsible for Regulation S-P compliance, even when vendors or consultants are handling tasks.

This misconception often surfaces in vendor management. A service provider may handle data securely, but without written contracts outlining breach reporting timelines and security expectations, the firm still faces exposure.

The 2026 amendments explicitly reinforce that responsibility cannot be outsourced; it must be governed, monitored, and documented.

Outsourced compliance partners, such as InnReg, can provide operational support and specialized expertise, but they act as an extension of the firm’s compliance team, not as a substitute for regulatory accountability.

“We Don’t Share Data, so Reg S-P Doesn’t Apply”

This is one of the most common misconceptions. Even if a broker-dealer does not share customer information with outside parties, it is still required to:

Provide an initial privacy notice when the relationship begins

Maintain written policies to safeguard customer data

Protect against unauthorized access or loss

Regulation S-P applies to how information is stored, accessed, and protected, not just how it’s shared. Fintech founders who assume they are exempt because they “don’t share data” often miss core requirements related to safeguards, disposal, and breach response.

Confusion Between Consumer and Customer Obligations

Another area of confusion lies in the distinction between consumers and customers. A consumer might use a service once, while a customer maintains an ongoing account or relationship.

Broker-dealers must provide full privacy and safeguard protections to both, but customers receive additional ongoing notice and security obligations. Failing to identify which category an individual belongs to can result in missed notices or incomplete records.

This is especially relevant for fintech platforms that blur the line between single-use users and active account holders.

Practical Compliance Steps for Broker-Dealers

As previously mentioned, Regulation S-P compliance is an ongoing operational process, not a one-time filing or certification. For broker-dealers, the most effective programs integrate privacy and data protection controls into everyday business operations.

The following steps outline how to build a strong, practical framework that meets both current and 2026 requirements:

Building Effective Privacy Notices

Privacy notices are the foundation of Regulation S-P. They communicate transparency and demonstrate that a firm understands its data-handling responsibilities.

To strengthen your privacy notice program:

Review and update content annually to reflect current data-sharing practices

Maintain digital records of when and how each notice was delivered

Use clear, concise language that customers can easily understand

Include opt-out options in both electronic and paper forms

Firms operating digital platforms should incorporate notice delivery directly into account creation or onboarding screens. Automation can make compliance consistent and auditable, reducing the risk of missed disclosures.

Designing and Testing Safeguard Programs

Written safeguard policies are central to every compliance program. Broker-dealers should move beyond templates and focus on operational design.

Strong safeguard programs typically include:

Risk-based security controls tailored to the firm’s technology stack

Regular vulnerability assessments or penetration testing

Defined incident detection and escalation processes

Access control systems that restrict customer data to authorized personnel

Testing is critical. Firms should perform periodic reviews and document results to demonstrate that controls are effective in practice, not just on paper.

Implementing Vendor Oversight Controls

Vendor management has become one of the most scrutinized areas of Regulation S-P. Firms are now responsible for confirming that third parties protect customer data with the same rigor they do internally.

A strong oversight framework includes:

Conducting due diligence before onboarding vendors

Requiring written confidentiality and breach notification clauses

Maintaining a vendor inventory with documented risk ratings

Reviewing vendor cybersecurity reports or certifications annually

Regulators will look for written evidence that vendor oversight occurs regularly, not reactively. For fintech broker-dealers with multiple integrations, maintaining organized documentation is key to meeting this expectation.

Training And Monitoring Staff

Compliance programs are only as effective as the people running them. Training creates awareness and consistency across departments.

As a firm, one could conduct privacy and data protection training at onboarding and annually thereafter. You can also tailor sessions by role. For example, the training could focus on phishing prevention for staff and vendor management for compliance officers.

Maintaining attendance logs, quiz scores, and content updates are also part of required recordkeeping. Training is both a compliance requirement and a key control against human error. Building a privacy-aware culture helps reduce risk and reinforces accountability.

See also:

Developing and Practicing Incident Response Plans

Every broker-dealer must have a written and tested incident response plan. The 2026 updates make this a core compliance requirement, not just an IT function.

An effective plan should:

Define clear roles across compliance, IT, and management

Include a step-by-step breach escalation and notification process

Document communication channels with regulators and customers

Be tested through mock scenarios or tabletop exercises

Regular testing helps teams identify weak spots before a real incident occurs. Firms should also keep detailed logs of testing dates, participants, and findings for examiner review.

Using Technology to Strengthen Compliance

Technology can make compliance more reliable and measurable. Automated systems can track privacy notices, log access to customer data, and record incident response actions in real time.

Fintech broker-dealers, in particular, can benefit from cloud-based compliance dashboards, automated alerts for privacy notice deliveries, and secure platforms for compliance documentation storage.

InnReg can integrate with a client’s existing tools, such as Asana, Jira, or proprietary systems, to manage workflows efficiently. This tech-neutral, process-driven approach allows fast-moving teams to maintain regulatory discipline without slowing innovation.

—

Regulation S-P is a test of how effectively a firm manages client trust and operational risk. With the 2026 amendments, the SEC has made clear that written policies are no longer enough. Broker-dealers must demonstrate that their privacy, cybersecurity, and vendor oversight programs work in practice.

Preparing for these changes requires coordination across compliance, technology, and management teams. Firms that approach Regulation S-P proactively will be best positioned to operate confidently in this new regulatory environment.

For fintech broker-dealers, these challenges are amplified by the pace of innovation. That’s where InnReg can add value. Our team specializes in helping fast-moving financial firms build and manage compliance programs that align with both regulatory expectations and business objectives. With experience supporting over a hundred fintechs globally, we can bring the structure and insight needed to mitigate risks while continuing to innovate.

InnReg was founded in 2013 by Francesco Matteini, former Chief Compliance Officer who helped launch and scale some of the most innovative digital broker-dealers over the last two decades. He built compliance programs to support the first zero-commission broker and the first BD-sponsored investor social network. Since its founding, InnReg has attracted highly experienced fintech consultants with long careers in compliance, risk management, and a deep understanding of the fintech industry.

How Can InnReg Help?

InnReg is a global regulatory compliance and operations consulting team serving financial services companies since 2013.

We are especially effective at launching and scaling fintechs with innovative compliance strategies and delivering cost-effective managed services, assisted by proprietary regtech solutions.

If you need help with broker-dealer compliance, reach out to our regulatory experts today:

Related Articles

Featured LinkedIn Posts