Buy Now Pay Later Model Explained (Pros + Cons)

Buy Now Pay Later (BNPL) has moved from a niche checkout option to a core payment and credit feature across ecommerce, fintech platforms, and consumer finance products.

What started as a simple pay-in-four alternative to credit cards is now a regulated financial product drawing attention from federal and state regulators, banks, and compliance teams.

This article explains what Buy Now Pay Later is, how the model works in practice, and who regulates it, with a specific focus on fintech business models.

At InnReg, we help fintechs build BNPL and other credit-driven products by providing licensing, compliance program development, and ongoing regulatory support. Contact us to learn more.

What Buy Now Pay Later Means in Today’s Fintech Landscape

Buy Now Pay Later is no longer just a checkout feature layered onto ecommerce. BNPL today effectively functions as a form of short-term consumer credit, embedded directly into payments, lending, and platform-based financial products.

It influences how consumers borrow, how merchants sell, and how fintechs structure regulated offerings.

As the adoption has expanded across retail, travel, marketplaces, and embedded finance platforms, Buy Now Pay Later models have become increasingly relevant. With the increase in consumer volume, regulators began to evaluate BNPL using the same lens applied to other credit products, and these models now sit at the intersection of payments, lending, and consumer protection, rather than outside of regulation altogether.

For fintechs, this shift influences the licensing strategy, disclosure obligations, underwriting practices, data reporting, and ongoing compliance operations. Understanding where BNPL fits today is the starting point for deciding whether, and how, to offer it responsibly.

How the Buy Now Pay Later Model Works

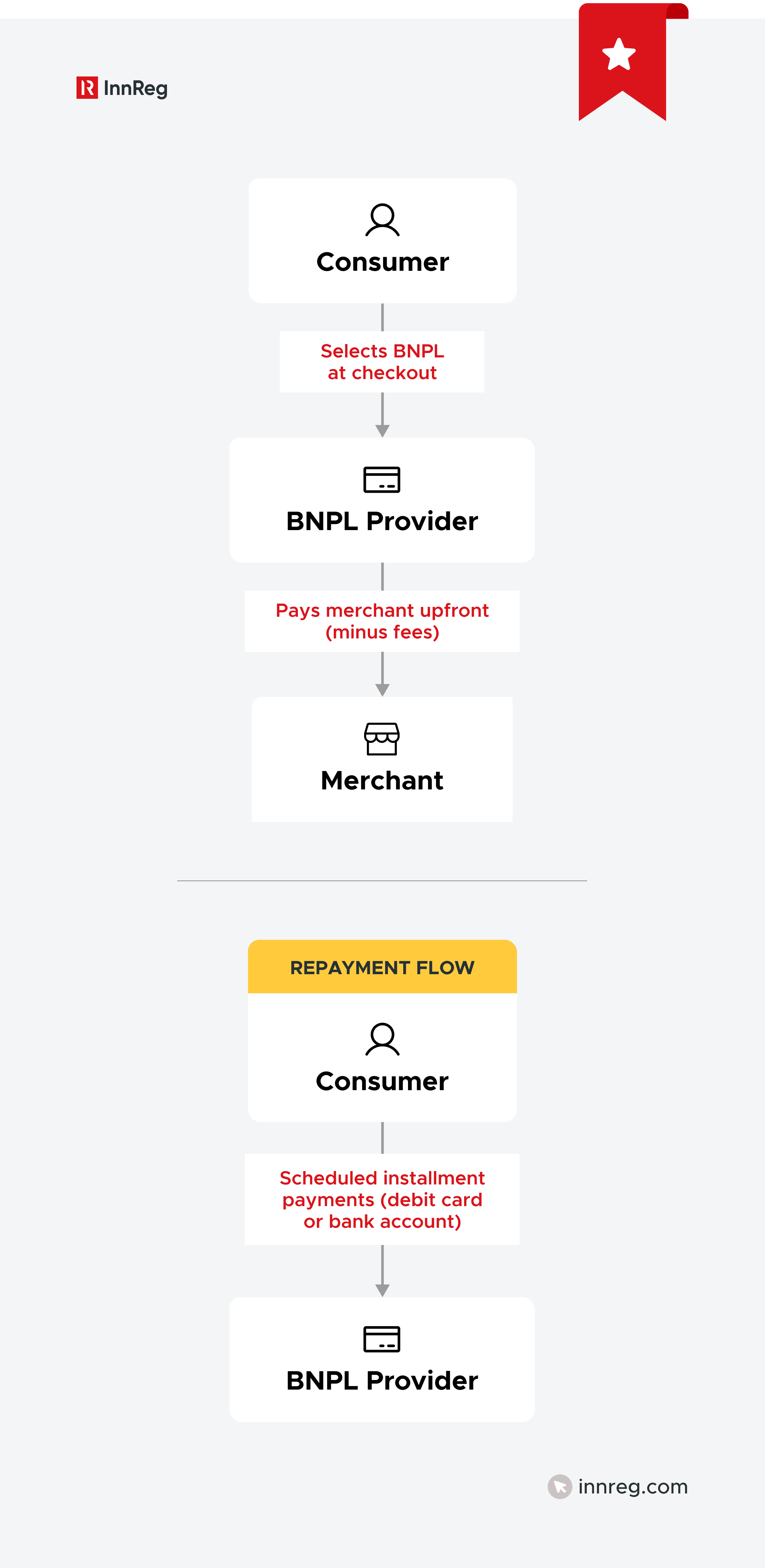

So, what is Buy Now Pay Later? The Buy Now Pay Later model allows a consumer to complete a purchase immediately and repay it over a short period through scheduled installments.

Understanding how BNPL works is essential as product design choices directly affect regulatory treatment, operational complexity, and ongoing compliance responsibilities.

Core Mechanics of BNPL

In its most usual form, Buy Now Pay Later works as a point-of-sale credit arrangement that is embedded into a merchant’s checkout flow.

The basic mechanics usually include:

The BNPL provider pays the merchant upfront, minus a fee.

The consumer repays the BNPL provider in installments.

Payments are typically automated via debit card or bank account.

Approval decisions are made in real time, often using alternative data and soft credit checks rather than traditional underwriting. This speed is a defining feature, but it also introduces risk that regulators increasingly scrutinize.

Pay-in-Four vs. Longer-Term BNPL Loans

The regulatory and operational profile of a Buy Now Pay Later product depends on loan duration, repayment structure, and pricing.

Two of the most common are:

Pay-in-four BNPL, which typically involves four equal installments, with the first payment due at checkout and the remaining payments spread over a short window, often 6–8 weeks. These products usually do not charge stated interest and rely instead on merchant fees. Historically, this structure has received lighter regulatory treatment, largely because it falls outside certain federal credit thresholds.

Longer-term BNPL loans look more like traditional installment credit. Repayment occurs monthly over several months, and interest or additional fees are more common. Because of these features, longer-term BNPL products are often treated as consumer loans under state lending laws and federal disclosure regimes, triggering licensing, underwriting, and ongoing compliance requirements.

This distinction matters in practice as longer-term BNPL products frequently fall squarely within existing consumer credit frameworks at both the state and federal levels. At the same time, pay-in-four models increasingly attract scrutiny as regulators reassess where they fit within modern credit regulation.

Pay-In-Four BNPL | Longer-Term BNPL | |

|---|---|---|

Repayment Term | 6-8 weeks | Several months |

Installments | Four equal payments | Monthly installments |

Interest | Typically none stated | Interest and/or fees are common |

Primary Revenue | Merchant discount fees | Interest, fees, card economics |

Underwriting | Light, real-time decisioning | More traditional credit review |

Regulatory Treatment | Historically lighter treatment | Treated as consumer lending |

Compliance Impact | Increasing scrutiny | Licensing, disclosures, ATR, ongoing supervision required |

How BNPL Providers Make Money

Short-term BNPL products are usually structured without interest income. In short-term models (such as pay-in-four), revenue is generated through merchant discount fees.

Additional economic issues arise in card-based BNPL models due to longer-term payment structures, which create interchange or card programs. These programs may create regulatory complexity, especially when multiple entities are involved.

In terms of compliance, regulators require full disclosure of all fees associated with an agreement. Not charging interest doesn’t mean lenders don’t have to be transparent about other fees. Regulators expect consumers to understand when and why charges will be incurred.

Where BNPL Fits in the Broader Credit Ecosystem

Buy Now Pay Later sits between traditional payments and consumer lending. It’s not a revolving credit product like a credit card, and it’s not a one-time installment loan originated outside the point of sale. BNPL is embedded credit, offered at checkout, and tied directly to a specific transaction.

Unlike credit cards, BNPL loans have a set repayment timeline and no ongoing line of credit. Once the loan is originated, repayment terms are locked in. There’s typically no minimum payment flexibility and no ability to carry a balance forward. While this structure limits the potential for duration risk (the possibility that consumers will be able to continue borrowing), it does increase short-term repayment pressure on the consumer.

As BNPL models align with traditional lending models more and more, regulators are increasingly treating it as credit rather than a payment feature. Solutions are often evaluated alongside installment loans, cards, and other financing products, particularly where underwriting, disclosures, and consumer protections are concerned.

Note: For fintechs, this means BNPL should be designed and governed as part of the broader credit and risk strategy, not as a standalone checkout feature.

4 Examples of Buy Now Pay Later Models

Buy Now Pay Later does not follow a single standard structure. The way BNPL is embedded, funded, and serviced varies by product and platform, and those differences matter from both an operational and regulatory standpoint.

Below are the most common BNPL models, illustrated through well-known market participants:

1. Klarna and Afterpay: Checkout-Based Pay-in-Four BNPL

Companies like Klarna and Afterpay built their core products around short-term, pay-in-four installment plans offered directly at checkout.

The BNPL provider integrates with the merchant, pays the merchant upfront, and collects four scheduled payments from the consumer over a short window.

These models typically do not charge stated interest and rely heavily on merchant fees. Historically, this structure attracted lighter regulatory treatment, though it is now under closer review as usage and repeat borrowing increase.

2. Affirm: Longer-Term Installment BNPL

Affirm is commonly cited as an example of BNPL that closely resembles traditional installment lending. While it also offers short-term options, many Affirm loans extend over several months and may include interest or financing charges.

Because of these features, Affirm’s products are more frequently treated as consumer loans under state and federal law, triggering licensing, disclosure, and underwriting obligations similar to those applied to other installment lenders.

3. PayPal Pay Later: BNPL Inside a Payments Platform

PayPal Pay Later functions as an embedded feature within PayPal’s core payments product. Consumers select installment options during checkout or directly within their PayPal account, without needing to engage with a separate BNPL provider.

Because repayment is tied to existing PayPal credentials, the user experience remains closely connected to the broader PayPal platform. This creates a tighter link between payments and credit than in traditional checkout-based BNPL models.

From a compliance standpoint, this means the BNPL offering is reviewed alongside PayPal’s other regulated activities, rather than being assessed as a standalone financing product.

4. Apple Pay Later: Card-Linked and Ecosystem-Based BNPL

Apple Pay Later offers installment payments tied to Apple Pay transactions, with repayments managed through the user’s Apple Wallet. While the consumer experience feels simple, the underlying structure involves card networks, issuing banks, and platform-level controls.

This approach highlights how BNPL can sit inside a larger ecosystem, increasing coordination requirements among partners and expanding the scope of compliance oversight.

See also:

Pros of Buy Now Pay Later for Consumers and Businesses

The Buy Now Pay Later model gained traction because it addressed practical issues on both sides of a transaction. They lower the upfront cost of a purchase while at the same time reducing checkout friction and thus benefiting the sellers.

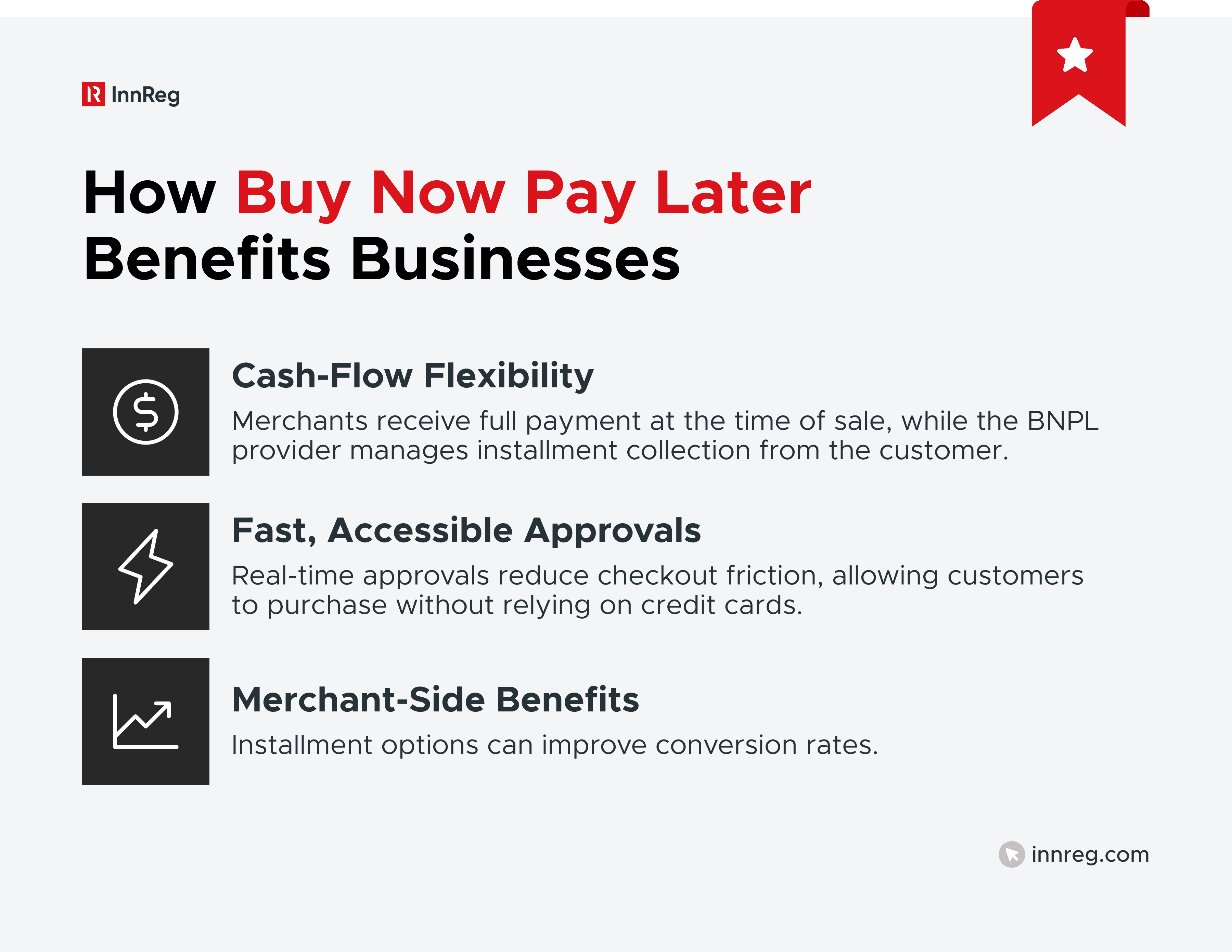

Cash-Flow Flexibility

BNPL enables customers to divide a payment over a usually short period instead of being paid in full at checkout. This can make higher-priced items easier to manage within normal income and budgeting cycles.

For merchants, BNPL changes payment timing without requiring them to offer credit directly. The merchant is paid at the time of sale, while the BNPL provider takes on responsibility for collecting installment payments from the customer.

This structure streamlines the checkout experiences without tying up merchant capital. It allows businesses to support flexible payment options while keeping their cash flow and operational model largely unchanged.

Fast, Accessible Approvals

BNPL approvals usually happen directly at checkout, with decisions made in real time. Many providers rely on soft credit checks or limited data signals, which lowers the bar compared to traditional credit products.

As a result, more customers can complete a purchase. Shoppers who do not qualify for or prefer not to use a credit card can still move forward, which often leads to higher approval rates at checkout.

Merchant-Side Benefits

Merchants adopt Buy Now Pay Later models to reduce cart abandonment and give customers more flexibility at the point of purchase. Breaking a larger price into installments can make a transaction feel more accessible, which may improve conversion rates and, in some cases, increase average order value.

At the same time, BNPL shifts credit and repayment responsibilities away from the merchant as the provider handles installment collection, servicing, and related credit functions. This effectively allows merchants to offer financing without operating their own lending or compliance infrastructure.

This approach supports flexible payment options while keeping merchant operations focused on sales, fulfillment, and customer experience rather than credit administration.

—

When used intentionally, BNPL can function as a targeted financing tool rather than a substitute for revolving credit, offering value to both sides of the transaction without long-term debt accumulation.

Need help with lender compliance?

Fill out the form below and our experts will get back to you.

Cons of Buy Now Pay Later and Emerging Risks

Buy Now Pay Later simplifies purchasing, but it also introduces risks that become more visible as usage increases. Many of these issues are tied to volume, repeat usage, and how BNPL fits into a consumer’s broader financial picture.

Common risks associated with BNPL include:

Consumers taking on multiple installment loans simultaneously

Late or failed payment fees and potential overdrafts

Inconsistent protections around disputes and refunds

Added operational complexity

While individual BNPL transactions may be small, overlapping repayment schedules can create consumer stress that surfaces through increased complaints, disputes, and support requests.

These outcomes are a key reason regulators evaluate BNPL providers using the same standards applied to other consumer credit products, rather than treating BNPL as a simple payment feature.

Compliance Challenges Fintech Teams Should Anticipate

As BNPL is at the intersection of lending, payments, and consumer protection, fintechs often face regulatory obligations that were not initially obvious during product design.

The challenges below tend to surface as usage grows, regulators engage, or expansion into new states or markets begins:

Compliance Area | Why It Matters |

|---|---|

Licensing Obligations | BNPL products can trigger state lending or financing laws based on structure, fees, repayment length, and funding model, even when marketed as interest-free |

Ability-to-Repay Expectations | Regulators increasingly expect BNPL providers to consider repayment capacity, particularly as products move beyond short pay-in-four models or scale in volume. |

Credit Reporting | As BNPL data is reported more frequently, providers must comply with accuracy, correction, and dispute requirements under credit reporting laws |

Dispute Handling and Refunds | Returns and billing disputes are operationally complex and closely scrutinized, especially when consumers continue making payments during unresolved issues |

Data Accuracy and Fair Lending | Automated decisioning requires ongoing oversight to avoid data quality issues, inconsistent outcomes, or fair lending concerns as programs scale |

Fraud and Vendor Oversight | Real-time approvals and third-party integrations increase exposure to fraud and operational risk, particularly at system and vendor integration points |

Licensing Obligations and Gray Areas

Fintechs sometimes assume that short-term or no-interest products fall outside traditional licensing regimes. However, licensing requirements can apply earlier than initially expected, especially as volume grows or as the product evolves.

Operating without the appropriate licenses can result in regulatory inquiries, remediation efforts, or required changes to the product’s structure, all of which can disrupt growth and increase compliance costs.

Ability-to-Repay Requirements

As Buy Now Pay Later products continue to evolve, regulators are paying closer attention to whether consumers have the ability to repay their obligations. This scrutiny becomes more pronounced as BNPL offerings move beyond short pay-in-four structures and into longer repayment periods or higher purchase amounts.

Importantly, this expectation is not limited to large loans. Even relatively small BNPL transactions can raise concerns when consumers hold multiple installment plans at the same time or show signs of repayment stress.

For fintechs, this creates a real tradeoff. Fast approvals remain central to the BNPL experience. However, decisioning must still be grounded in defensible underwriting practices, as insufficient consideration of repayment capacity has become an increasingly common regulatory concern.

Credit Reporting Considerations

Historically, many BNPL providers avoided credit reporting.

That approach is changing. As BNPL data becomes more integrated into credit reporting systems, providers must comply with accuracy, dispute handling, and correction requirements.

Once BNPL activity is reported, it becomes subject to the same expectations as other credit data, including consumer rights under applicable reporting laws.

Dispute Handling, Refunds, and Error Resolution

Returns and disputes tend to be more complicated in Buy Now Pay Later models than in traditional card payments. In many cases, consumers are still required to make scheduled payments while a return or dispute is being reviewed, which can quickly lead to frustration if expectations are not clear.

The way these situations are handled matters. When timelines are vague or responsibilities between the BNPL provider and the merchant are not clearly defined, complaints tend to rise, and support teams feel the strain.

Regulators pay close attention to how BNPL providers handle disputes. Billing customers while returns or errors are still unresolved, especially without clear communication, is a common source of regulatory concern.

Data Accuracy and Fair Lending Implications

As BNPL programs grow, providers take on greater responsibility for the quality and integrity of their data. Errors in inputs, reporting, or model assumptions can create downstream issues that are difficult to unwind.

Automated decisioning plays a central role in BNPL approvals, but it requires oversight. Even well-designed systems can drift if performance is not monitored and adjusted over time.

Regulators increasingly ask how BNPL providers test for consistency, identify anomalies, and explain decision outcomes. Transparency and repeatability are recurring themes in these discussions.

Fraud, Operational Risk, and Vendor Oversight

BNPL products depend heavily on real-time decisioning and multiple third-party integrations. That speed is part of the appeal, but it also increases exposure to fraud, identity misuse, and breakdowns in day-to-day operations when controls are not well aligned.

In many cases, the risk does not come from the product logic itself but from how different systems interact. Processors, card programs, data vendors, and banking partners are all involved in moving a BNPL transaction from approval to repayment, and issues tend to arise when roles are not clearly defined or when monitoring is uneven.

This is why vendor oversight and clear controls are so important. Compliance problems often show up at integration points, where gaps in ownership, testing, or escalation processes may not be obvious until they result in customer impact or regulatory attention.

See how InnReg helps fintechs by providing vendor risk management services →

BNPL vs. Other Credit Options: A Practical Comparison

Buy Now Pay Later is often grouped with credit cards and installment loans. But each option works differently in practice, especially regarding repayment structure, regulatory treatment, and operational impact.

Feature | BNPL | Credit Cards | Personal Loans | Store Financing |

|---|---|---|---|---|

Point of Use | Embedded at checkout | Broad, reusable | Outside checkout | Merchant-specific |

Repayment Structure | Fixed installments | Revolving balance | Fixed installments | Fixed installments |

Interest | Often none for short-term | Typically variable | Usually fixed | Often promotional |

Credit Line | No revolving line | Yes | No | No |

Approval Timing | Real-time at checkout | Pre-approved or applied | Application-based | At point of sale |

Underwriting Depth | Light to moderate | Moderate to extensive | Extensive | Moderate |

Consumer Protections | Evolving, not uniform | Well-established | Established | Varies by program |

Regulatory Treatment | Increasingly treated as credit | Fully regulated credit | Fully regulated credit | Fully regulated credit |

What sets BNPL apart is how closely it’s tied to the transaction itself. The product is embedded at checkout and blends payment functionality with short-term financing, which reduces friction for both consumers and merchants.

That same structure also explains why regulators are paying closer attention. As BNPL offerings expand beyond short, no-interest models, they’re increasingly evaluated alongside more traditional credit products.

As such, fintech should view BNPL not as a lighter form of credit, but part of the broader credit landscape, with its own set of tradeoffs around user experience, compliance requirements, and risk management.

Key Regulators Overseeing BNPL Models in the US

Buy Now Pay Later products do not sit under a single regulator. Oversight is split between federal and state authorities, depending on how the product is structured, funded, and used by consumers.

Key regulators overseeing BNPL providers are:

Consumer Financial Protection Bureau (CFPB): Oversees BNPL from a consumer protection perspective, with a focus on disclosures, fees, dispute handling, and unfair or deceptive practices.

Federal Trade Commission (FTC): Regulates BNPL marketing and consumer-facing representations, especially where disclosures or data use may raise consumer protection concerns.

Office of the Comptroller of the Currency (OCC): Applies when BNPL involves national banks or bank partnerships, with expectations around underwriting, risk management, and third-party oversight.

State regulators: Enforce state lending and financing laws, often requiring licensing and consumer protections regardless of whether BNPL products charge interest. California and New York have been especially active, requiring licenses and imposing consumer protection requirements.

Regulatory Developments Shaping BNPL

Regulatory expectations around Buy Now Pay Later have shifted quickly over the past few years. What was once treated as a lightly regulated payment alternative is now increasingly assessed as a credit product, particularly as BNPL usage and consumer exposure have grown.

CFPB’s Interpretive Rule and its Withdrawal

The CFPB signaled heightened scrutiny of BNPL when it issued interpretive guidance suggesting certain products should be treated similarly to credit cards under existing consumer protection rules.

The focus was on dispute rights, billing practices, and fee transparency.

While that guidance was later withdrawn, the underlying concerns did not disappear. The CFPB has made clear it continues to monitor BNPL through its general consumer protection authority, including unfair or deceptive practices.

OCC Guidance for Bank-Offered BNPL

The OCC has addressed BNPL primarily through its supervision of banks and bank partnerships and issued guidance outlining expectations for underwriting practices, risk management, and third-party oversight when banks are involved in BNPL programs.

For fintechs operating through bank partnerships, the message is clear. BNPL offerings are expected to meet the same safety, soundness, and compliance standards that apply to other bank-supported credit products, regardless of how the product is marketed.

See also:

New York’s BNPL Licensing Law

New York has taken one of the most direct regulatory approaches to BNPL. The state enacted legislation that requires Buy Now Pay Later providers to be licensed by the New York Department of Financial Services.

The scope of this law is part of a larger trend of states filling gaps left by the federal government where there was less direction. BNPL will fall under a regulated environment with more structure than most credit products.

California’s Licensing Approach

In California, many Buy Now Pay Later plans are considered loans subject to the California Financing Law (CFL) and, therefore, providers must be licensed as lenders. State enforcement actions and public guidance from the California Department of Financial Protection and Innovation (DFPI) confirm this interpretation and the need for CFL licensure.

Global Regulatory Trends Influencing BNPL

Buy Now Pay Later is facing more scrutiny worldwide, not just in the US. Regulators in several major markets are moving to bring BNPL under existing consumer credit rules, removing exemptions that once allowed these products to operate with relatively limited oversight.

UK Approach and Upcoming FCA Authorization

In the UK, BNPL products were historically exempt from consumer credit regulation.

However, in May 2025, the UK government published the Financial Services and Markets Act 2000 (Regulated Activities etc.) (Amendment) Order 2025.

This act brings previously exempt BNPL products into the UK’s financial services regulatory regime and sets the stage for FCA regulation. Under this framework, BNPL lenders will require authorization by the Financial Conduct Authority (FCA) starting around mid-2026.

EU Consumer Credit Directive (CCD2)

The European Union has taken a similar path through the revised Consumer Credit Directive (CCD2), adopted in 2023. CCD2 expands the scope of regulated credit to include short-term, low-value, and interest-free products that were previously out of scope.

Once implemented by member states, BNPL providers will face standardized disclosure requirements, creditworthiness assessments, and consumer rights obligations. This change significantly reduces regulatory arbitrage across EU markets.

Observations from Australia and Canada

Australia has moved to regulate BNPL through tailored credit frameworks that introduce suitability and affordability checks without fully applying traditional credit licensing in all cases. The focus has been on preventing consumer harm while preserving product flexibility.

Canada has taken a more incremental approach, relying largely on existing consumer protection and lending laws at the provincial level. Even so, regulatory scrutiny is increasing as BNPL usage grows, particularly around disclosures and fee practices.

How to Build BNPL Compliance Into Your Product

Launching a Buy Now Pay Later product is not just a product decision, as the compliance choices shape how the product operates, scales, and withstands regulatory scrutiny.

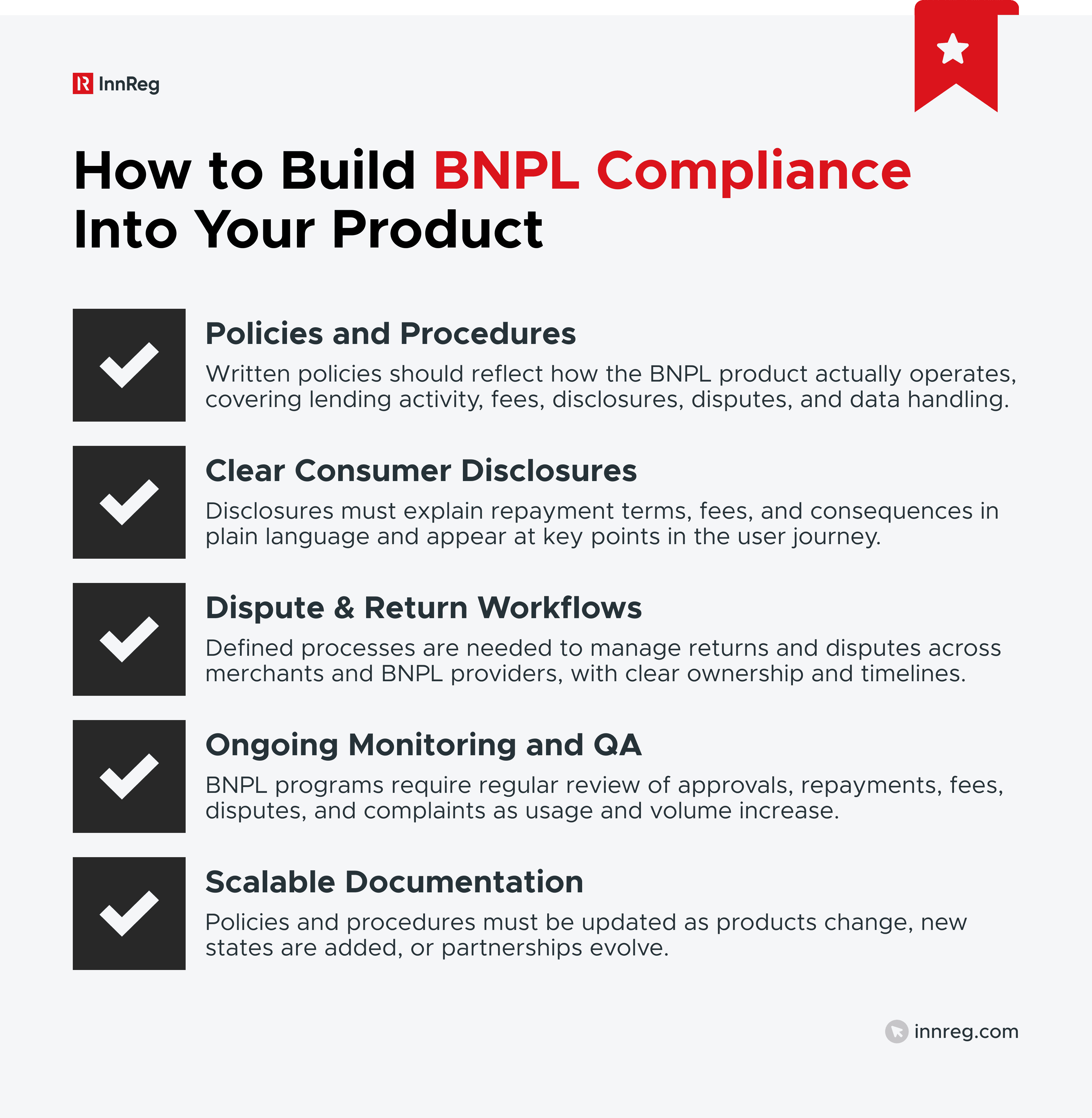

Core Policies and Procedures Needed

A BNPL program should be supported by policies that reflect how the product actually operates. That includes documenting how lending activity is handled, how fees are applied, how disclosures are presented, and how disputes and data are managed.

These policies are not just reference documents. They are meant to guide day-to-day decisions and provide consistency as the product scales.

If written policies do not match actual business operations, issues surface quickly. Misalignment is often flagged during regulatory reviews, partner diligence, or audits, and correcting it later can be time-consuming.

Learn how InnReg helps fintechs with compliance policies and procedures development →

Implementing Disclosures That Users Actually Understand

Disclosures are one of the most common friction points in BNPL programs. Regulators tend to look beyond whether terms technically exist and focus instead on whether users can realistically understand what they are agreeing to.

That means explaining repayment timing, fees, and potential consequences in plain language. Legal accuracy matters, but so does readability.

Where disclosures appear also matters. Checkout, account setup, and payment confirmation screens are the moments regulators expect clarity, not buried links or dense terms pages.

Handling Disputes and Returns

Returns and disputes need clear processes on both the BNPL and merchant side. Roles should be defined, timelines documented, and escalation paths understood by the teams involved.

When ownership is unclear, issues tend to surface quickly. Consumers are often left unsure who to contact or what to expect while payments continue.

This is an area regulators pay close attention to. Weak or inconsistent dispute handling is one of the fastest ways BNPL programs draw regulatory scrutiny.

Setting Ongoing Monitoring and QA

BNPL compliance does not end at launch. As volume grows, teams need ongoing monitoring of approvals, repayment behavior, fees, disputes, and complaints.

Regular reviews help surface issues early. Regulators expect to see evidence that programs are actively monitored, not just initially approved.

Scalable Documentation Practices

BNPL products change. New features, new states, and new partners all require updates to policies and procedures.

For many fintechs, maintaining that documentation internally becomes resource-intensive. In those cases, working with an external compliance team like InnReg can provide structure and continuity without the overhead of building a large in-house function.

See also:

—

Buy Now Pay Later has evolved into a regulated form of consumer credit that sits within the broader financial services ecosystem.

For fintechs, the opportunity is real, but so are the obligations. Product structure, disclosures, underwriting, and operational workflows all influence how BNPL is regulated and supervised.

BNPL should be treated as a credit product from day one, even when it looks simple on the surface. Teams that understand the tradeoffs, regulatory expectations, and operational risks are better positioned to scale without disruption.

Ani is a Senior Compliance Consultant with over 10 years of experience in legal and regulatory compliance across fintech, RegTech, and cross-border payments. She has held roles at Remote and EY, with expertise in AML, GDPR, financial crime, and EU regulatory frameworks. She holds CAMS and CIPP/E certifications.

How Can InnReg Help?

InnReg is a global regulatory compliance and operations consulting team serving financial services companies since 2013.

We are especially effective at launching and scaling fintechs with innovative compliance strategies and delivering cost-effective managed services, assisted by proprietary regtech solutions.

If you need help with lender compliance, reach out to our regulatory experts today:

Related Articles

Featured LinkedIn Posts