Top 7 Tokenization Models to Watch Out For in 2026

Tokenization models are becoming a practical design choice for fintechs that want to move faster, reach new markets, or repackage existing financial products using blockchain infrastructure.

By 2026, many of these models will no longer sit at the edge of experimentation. They will operate inside regulated financial systems, alongside broker-dealers, payment firms, investment advisors, and banks.

This article breaks down seven tokenization models to watch in 2026, with a focus on how they’re actually implemented, how regulators view them, and where compliance challenges tend to surface. The guide offers operational guidance to help you understand which models are viable, which are high-risk, and what it takes to operate them responsibly.

At InnReg, we support fintechs pursuing tokenization models that touch broker-dealer, RIA, and money transmission requirements. Our team helps with licensing, regulatory positioning, and compliance program buildout and operations. Contact us to learn more.

What Tokenization Models Mean in Financial Services

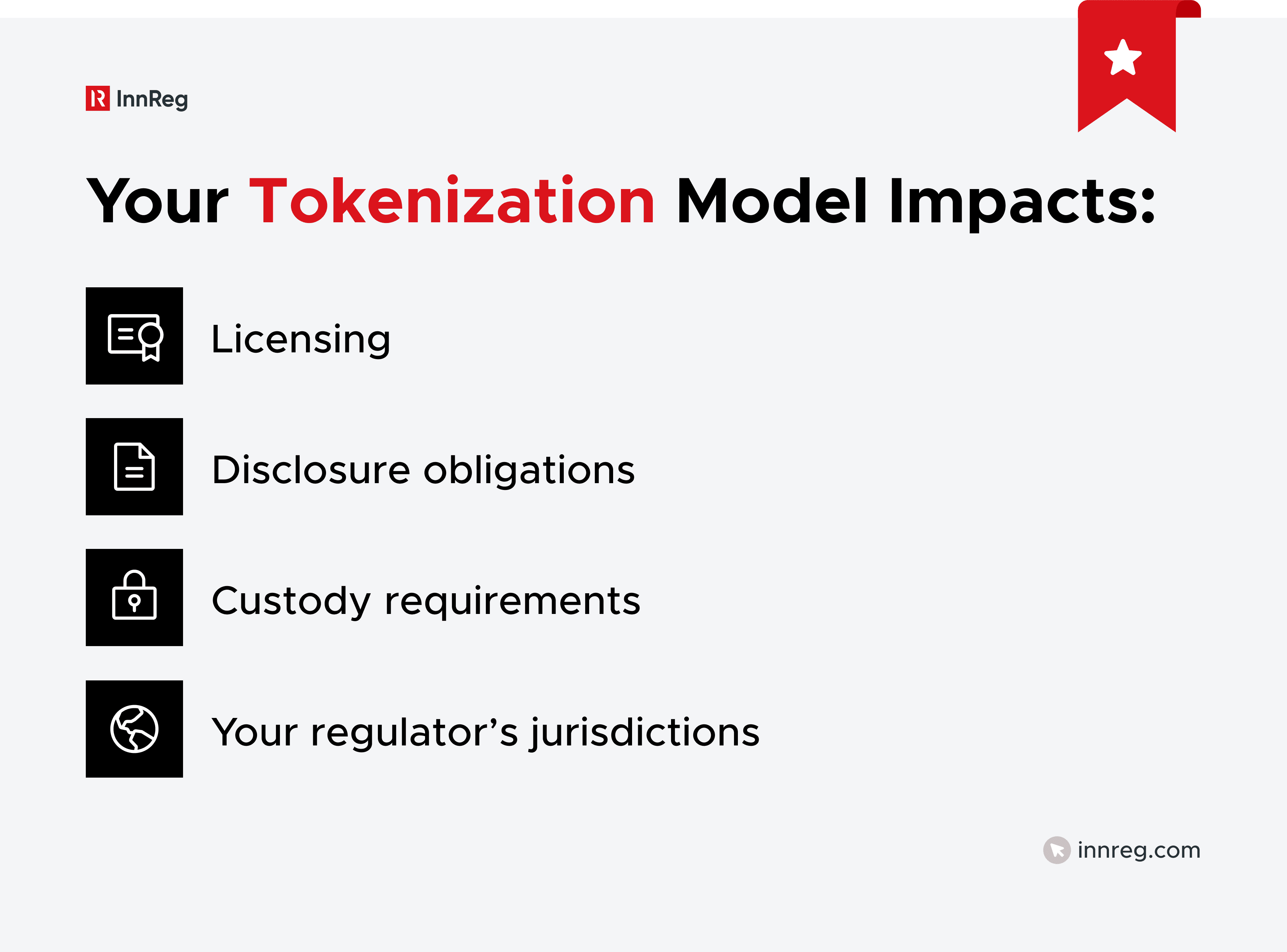

In financial services, tokenization models describe how ownership, value, or rights are represented, transferred, and governed using tokens. The model determines what the token actually represents, how it's issued, who can hold or trade it, and which regulatory frameworks apply.

This distinction matters because regulators don’t regulate “tokens” in the abstract. They regulate securities, payments, commodities, deposits, and financial contracts, regardless of whether those instruments are recorded on a blockchain or in a traditional database.

A well-designed tokenization model aligns the technology with an existing legal category rather than trying to bypass it. However, a wrong tokenization model often leads to product delays, forced restructures, and stalled approvals down the road.

Explore what tokenization means in fintech here →

Tokenization vs. Payment and Data Tokenization

The term tokenization is often used loosely, which creates confusion during product design and regulatory discussions. In financial services, there is a critical difference between asset tokenization and payment or data tokenization.

Asset tokenization involves representing ownership, economic rights, or claims using tokens. These tokens may reflect securities, commodities, real-world assets, or contractual rights. That’s the focus of this article, and where regulatory scrutiny is highest.

Payment and data tokenization serve a different purpose. They replace sensitive information, such as card numbers or bank details, with non-sensitive tokens for security and fraud reduction.

Here’s a table to highlight the differences between the two for a clear distinction:

Dimension | Asset Tokenization | Payment and Data Tokenization |

|---|---|---|

Primary purpose | Represents ownership, economic rights, or legal claims | Protects sensitive information by replacing it with non-sensitive tokens |

What is tokenized | Securities, real-world assets, commodities, contractual rights | Card numbers, bank details, personal or transaction data |

Regulatory focus | Economic substance and investor or user rights | Data security, fraud prevention, and payments compliance |

Typical regulators involved | Securities regulators, commodities regulators, banking supervisors | Payments regulators, data protection authorities |

Common compliance risk | Misclassifying regulated financial activity as “just a token” | Failing to meet security or data protection standards |

Many compliance issues arise when teams conflate these concepts. Treating an asset token like a security token one day and a payments token the next often triggers regulatory pushback.

This is where a practical compliance lens matters. At InnReg, we know that teams working on tokenization models typically need help mapping product features to existing regulatory categories early, before development hardens assumptions that are difficult to unwind later.

7 Tokenization Models to Watch in 2026

Not all tokenization models are equally viable from a regulatory or operational standpoint. Some are becoming easier to deploy as regulators gain familiarity with them. Others remain high-friction and require careful structuring to avoid enforcement or licensing issues.

The models outlined below reflect where regulatory attention, market adoption, and product experimentation are converging. They also reflect where fintech teams most often underestimate compliance complexity. The goal is not to rank these models by popularity, but by relevance and risk heading into 2026.

As you read through each model, keep three questions in mind:

What does the token legally represent?

Which regulators are likely to assert jurisdiction?

How much ongoing compliance work does the model create after launch?

Here are the seven tokenization models to watch out for this year:

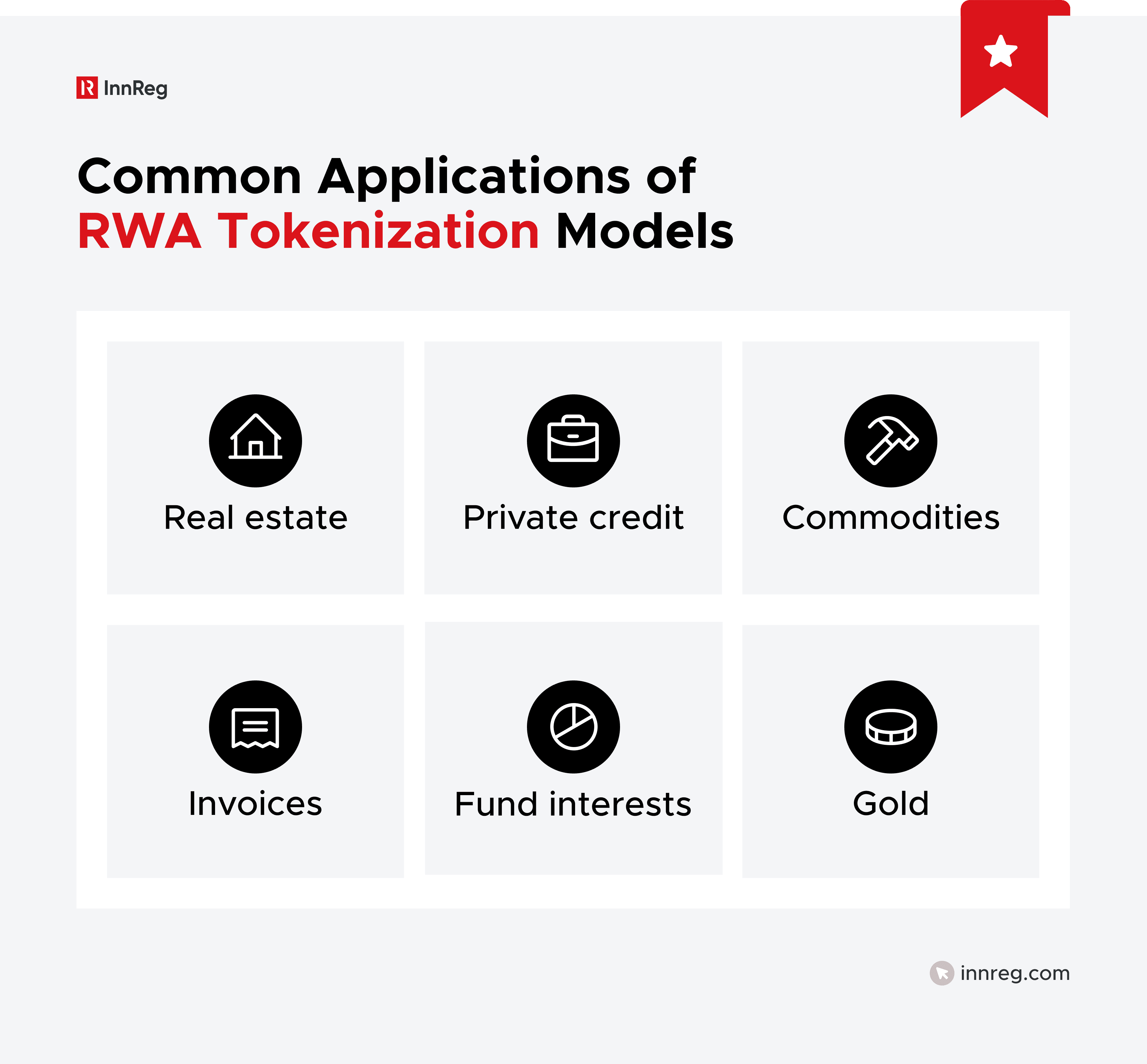

1. Real-World Asset (RWA) Tokenization Models

Real-world asset tokenization models represent off-chain assets through on-chain tokens. The token typically reflects an ownership interest, an economic claim, or a contractual right tied to a physical or legally recognized asset.

RWA tokenization spans a wide range of asset classes, but not all behave the same from a compliance perspective. Each asset type pulls different regulatory threads. For example, a tokenized loan looks very different, legally, from a tokenized warehouse receipt for gold.

Despite the different asset classes, most RWA tokenization models rely on a legal wrapper that holds the underlying asset. The token doesn't usually hold the asset directly. Instead, it represents an interest in an entity or agreement that owns the asset. The typical structures include:

A special-purpose vehicle holding the asset

A trust or custodial arrangement

A contractual claim on cash flows or redemption value

From a regulatory standpoint, most RWA tokenization models fall under existing securities or commodities frameworks. Fractional ownership, pooled vehicles, and profit expectations frequently trigger securities laws.

Regulators focus on economic substance, which means teams must resolve classification, licensing, and distribution questions early, before product decisions become locked in.

2. Tokenized Securities Models (Equity and Debt)

Tokenized securities models involve issuing or representing traditional securities using tokens, rather than paper certificates or standard book-entry records. The underlying instruments are familiar. Equity, debt, and fund interests remain securities under existing law, regardless of the technology used to record ownership.

These models are among the most mature from a regulatory standpoint. Securities regulators already have clear authority, and many requirements are well understood. The complexity comes from fitting tokenized issuance, custody, and trading into established market structure rules.

In practice, tokenized securities are often used for:

Private company equity

Corporate or structured debt

Fund shares or interests

Tokenization changes the infrastructure, not the legal nature of the instrument. Issuers still need to rely on registration or valid exemptions, and intermediaries must be properly licensed.

Operationally, these models require tight coordination between legal documentation and technical implementation. Transfer restrictions, investor eligibility, and record-keeping obligations must be reflected in how tokens are issued and moved.

Learn more about the regulations surrounding tokenized securities in this guide →

Native vs. Wrapped Tokenized Securities

There are two common approaches to structuring tokenized securities, and the distinction matters for compliance and operations.

Here are the key differences between native vs. wrapped tokenized securities:

Native Tokenized Securities | Wrapped Tokenized Securities |

|---|---|

Treated as the security | Represents an interest in a traditional security held off-chain |

On-chain ledger serves as the primary record | Off-chain registry or custodian remains the source of truth |

Issued directly on blockchain infrastructure | Issued by an intermediary holding the underlying security |

Often requires deeper coordination with regulators, transfer agents, and custodians | Often easier to deploy within existing regulatory and operational frameworks |

Custody is structured around digital asset custody rules and wallet-based controls | Custody follows traditional securities custody and recordkeeping practices |

More frequently seen in pilot programs and bespoke private market structures | More frequently used for private placements and transitional tokenization models |

Choosing between native and wrapped structures affects custody, supervision, and secondary trading options. The decision should be driven by regulatory constraints and operational readiness, not just technical preference.

3. Stablecoin and Asset-Backed Tokenization Models

Stablecoin and asset-backed tokenization models are designed to maintain a stable or asset-linked value, rather than expose holders to price volatility. These models are commonly used for payments, settlement, treasury operations, and as infrastructure layers within larger tokenized ecosystems.

Unlike speculative crypto assets, these tokenization models derive their value from reserves held off-chain or from clearly defined assets. That design choice brings them squarely into the scope of financial regulation.

Read more about the GENIUS Act and how it impacts stablecoins here →

Fiat-Backed vs. Commodity-Backed Structures

Fiat-backed tokens are typically pegged to currencies such as the US dollar or euro. Their value depends on the issuer’s ability to maintain adequate reserves and honor redemption obligations.

Commodity-backed tokens are linked to assets like gold, energy products, or other tangible commodities. In these models, token holders usually have a contractual claim tied to the underlying asset rather than direct ownership.

Here’s how they differ:

Fiat-backed models prioritize liquidity and payment use cases.

Commodity-backed models often emphasize store-of-value or hedging.

Regulatory treatment varies based on redemption rights and structure.

The backing asset and redemption mechanics drive regulatory classification, not the label applied to the token.

Reserve, Custody, and Disclosure Requirements

From a compliance perspective, reserve-backed tokenization models introduce ongoing operational obligations. Regulators focus heavily on how reserves are held, who controls them, and how accurately they are disclosed.

Common regulatory expectations include:

Clear reserve composition and segregation

Independent verification or attestations

Defined redemption processes and timelines

Failures in this area have driven enforcement actions and heightened supervisory attention. For fintech teams, this means stablecoin and asset-backed tokenization models require continuous compliance oversight, not periodic check-ins.

These models often attract early regulatory interest due to their potential scale and systemic impact. Teams pursuing them typically need mature compliance processes and the ability to respond quickly to supervisory requests, particularly as rules continue to evolve across jurisdictions.

4. NFT-Based Tokenization Models Beyond Collectibles

NFT-based tokenization models are no longer limited to digital art or collectibles. In fintech and adjacent financial products, NFTs are increasingly used to represent access rights, memberships, credentials, or participation in broader ecosystems.

Regulatory exposure depends less on the NFT format and more on how the token is structured and marketed. NFTs that function like investment products may fall under securities laws, even if they are labeled as collectibles.

NFT models generally fall into two broad categories from a compliance perspective:

Lower Regulatory Risk NFTs | Higher Regulatory Risk NFTs |

|---|---|

Used for access, identity, or consumption | Sold primarily to fund development or operations |

No promise or implication of financial return | Marketed with profit or appreciation narratives |

Limited or utility-driven transferability | Designed for active secondary market trading |

Value tied to use, not issuer performance | Value tied to issuer or platform success |

From an operational standpoint, NFT models also raise questions around transferability, royalty enforcement, and platform control. Compliance teams should assess whether NFTs can be freely traded, whether pricing signals imply speculative value, and how communications frame the purpose of the token.

NFT-based tokenization models can work within regulated environments, but only when economic rights, marketing language, and platform behavior are carefully aligned. Teams that treat NFTs as exempt by default often discover regulatory exposure late in the product lifecycle, when changes are costly to implement.

See also:

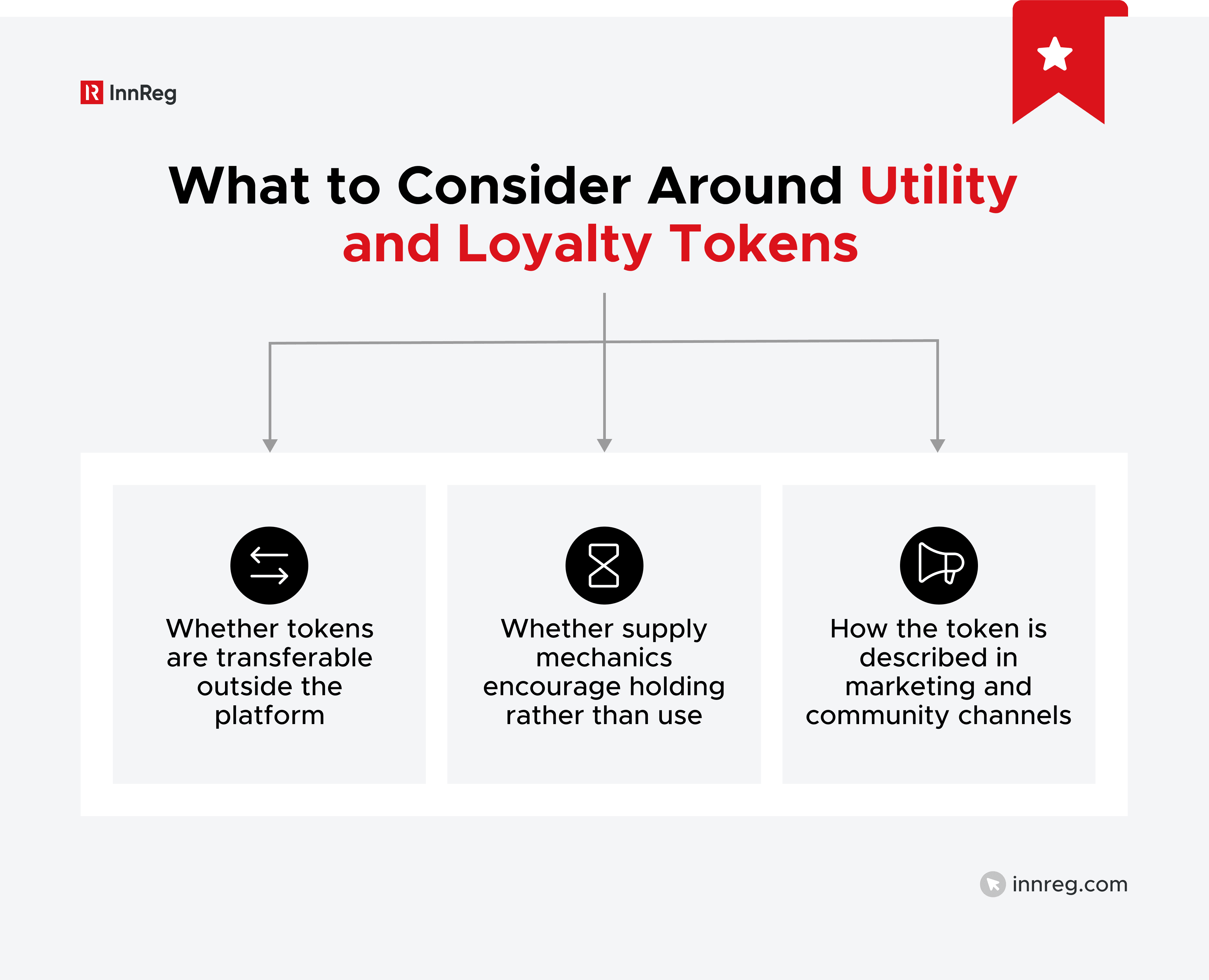

5. Utility and Loyalty Tokenization Models

Utility and loyalty tokenization models are designed to support product usage rather than capital formation. The token functions as a tool inside a defined ecosystem, not as a claim on profits, assets, or issuer performance.

These models are commonly used for access, discounts, rewards, or feature enablement. When structured carefully, they can operate with lower regulatory exposure than investment-oriented tokenization models.

The line becomes blurry when tokens begin to trade, appreciate, or function outside their intended use case.

Common utility and loyalty use cases include:

Platform access or feature unlocks

Usage credits or service consumption

Rewards and customer loyalty programs

The token’s value should be tied to consumption, not expectation. Once pricing, messaging, or transferability suggest upside, regulatory risk increases.

From a compliance perspective, the biggest risk is drift. A token launched as a utility instrument can evolve into a speculative asset if secondary markets emerge or if incentives change over time.

Utility and loyalty tokenization models often fail due to weak operational controls rather than regulatory intent. Clear usage rules, controlled transferability, and disciplined communications help keep these models aligned with their original purpose.

Need help with fintech compliance?

Fill out the form below and our experts will get back to you.

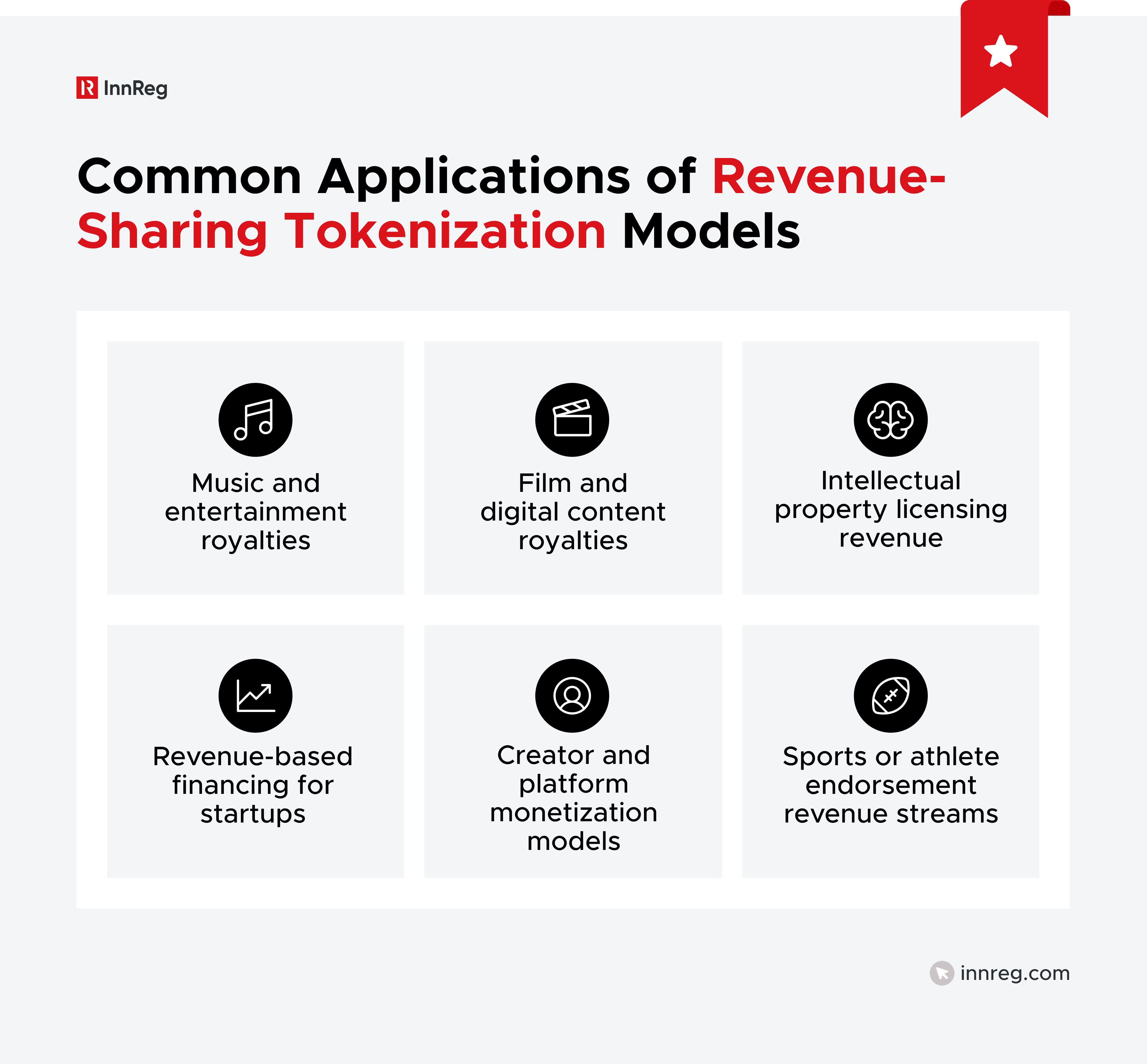

6. Revenue-Sharing and Royalty Tokenization Models

Revenue-sharing and royalty tokenization models allocate a contractual right to future cash flows generated by a business, asset, or project. Instead of ownership or repayment, token holders receive a portion of revenue, royalties, or other defined income streams.

These tokenization models are often used in media, IP-backed businesses, private ventures, and alternative financing structures. They appeal to founders looking for non-dilutive capital and to participants seeking exposure to performance-based returns.

From a regulatory perspective, these models are rarely neutral. Revenue participation almost always introduces securities law considerations, regardless of how the token is labeled.

The defining feature is economic dependence. Token holders rely on the issuer’s ongoing efforts to generate revenue.

Disclosure, Structuring, and Ongoing Obligations

Revenue-sharing tokenization models require careful structuring to clearly define rights, risks, and limitations. Ambiguity in these areas is a common source of regulatory and investor disputes.

Key compliance considerations include:

How revenue is calculated and distributed

What happens if revenue declines or stops

Whether tokens are transferable or tradable

Disclosure obligations tend to be ongoing, not one-time. Many structures require periodic reporting, clear payout mechanics, and restrictions on who can participate.

Operationally, these models create long-term compliance ownership. Payments must be tracked, reconciled, and communicated accurately. Secondary trading, if permitted, introduces additional supervision and recordkeeping requirements.

Revenue-sharing and royalty tokenization models can be effective financing tools, but only when teams are prepared to manage them as regulated financial products rather than lightweight token features.

7. Central Bank and Institutional Tokenization Models

Central bank and institutional tokenization models focus on tokenizing money, settlement assets, or financial infrastructure at the system level, rather than individual products. These models are typically driven by:

Central banks

Regulated financial institutions

Market infrastructure providers

The objective is not product innovation, but operational efficiency, settlement resilience, and regulatory control. As a result, these tokenization models sit firmly inside existing supervisory frameworks and tend to evolve slowly.

For fintechs, the relevance is indirect but important. These models shape how payments, custody, and settlement may function over time, and they influence what regulators expect from market participants.

Institutional tokenization models are compliance-led by design, with rules embedded at the infrastructure level rather than enforced after the fact.

Wholesale vs. Retail Tokenization Initiatives

Most central bank tokenization efforts fall into one of two categories: wholesale and retail tokenization. Here is what makes them both different:

Wholesale Tokenization Initiatives | Retail Tokenization Initiatives |

|---|---|

Designed for interbank settlement and market infrastructure | Designed for consumer and business payments |

Used for securities clearing, cross-border payments, and liquidity management | Used for everyday payment use cases |

Access is limited to regulated financial institutions | Access provided through banks or licensed intermediaries |

Focused on reducing settlement risk and operational friction | Focused on payment efficiency, inclusion, and control |

Operate fully within existing supervisory frameworks | Introduce additional consumer protection and AML considerations |

For fintechs, participation usually comes through integration rather than issuance. Firms may be required to support new settlement rails, custody standards, or reporting requirements as these initiatives mature.

Central bank and institutional tokenization models are unlikely to offer fast paths to market. However, they set the baseline for how regulated tokenized finance will operate, and ignoring them can create long-term operational blind spots.

Learn how to comply with AML guidelines around your tokenization model here →

Comparing Tokenization Models by Regulatory Exposure

Not all tokenization models attract the same level of regulatory scrutiny. Exposure depends on what the token represents, who can access it, and how value is created or distributed. Comparing models side by side helps teams anticipate licensing needs, approval timelines, and ongoing compliance efforts.

Below is a practical comparison focused on regulatory exposure rather than technical design.

Tokenization Model | Typical Regulatory Classification | Primary Regulators Involved | Relative Compliance Burden |

|---|---|---|---|

Real-World Asset (RWA) | Securities or commodities, depending on structure | Securities regulators, commodities regulators | High |

Tokenized Securities | Securities | Securities regulators, broker-dealer supervisors | High |

Stablecoin and Asset-Backed | Payments, e-money, or commodities | Payment regulators, banking supervisors | Medium to High |

NFT-Based (Beyond Collectibles) | Case-by-case; often securities when investment-like | Securities regulators, consumer protection agencies | Medium |

Utility and Loyalty | Consumer or payments-related when well-contained | Payment regulators, consumer protection agencies | Low to Medium |

Revenue-Sharing and Royalty | Securities | Securities regulators | High |

Central Bank and Institutional | Monetary and financial infrastructure | Central banks, banking regulators | Institution-led |

Regulatory exposure increases when tokens involve profit expectations, pooled assets, or broad distribution. Models tied to system infrastructure or pure consumption tend to face more predictable oversight.

For fintech teams and RIAs, this comparison is most useful early in product design. It clarifies which models are likely to require licenses, exemptions, or supervisory engagement, and which allow more operational flexibility.

Common Misconceptions About Tokenization Models

Misunderstandings around tokenization models are a frequent source of regulatory risk. Many issues don’t stem from novel rules, but from applying old assumptions to new infrastructure.

The misconceptions below appear repeatedly across fintech products, regardless of asset class or jurisdiction.

“Tokenization Avoids Securities Law”

Tokenization doesn’t change the legal nature of a financial product. If a token represents an investment, regulators will typically treat it as a security, regardless of whether it’s issued on-chain or off-chain.

Common red flags include:

Fractional ownership in income-producing assets

Profit-sharing or revenue participation

Marketing that emphasizes financial upside

Calling a token “utility,” “digital,” or “community-based” doesn't alter the analysis. Regulators focus on substance and economic reality, not labels.

“Decentralization Removes Accountability”

Decentralization doesn't eliminate regulatory responsibility. Someone still designs the system, sets the rules, and benefits economically.

Regulators routinely look at:

Who controls issuance and upgrades

Who sets pricing or supply mechanics

Who profits from the system’s operation

If a party exercises meaningful control, accountability usually follows. Claims of decentralization rarely hold up when governance, incentives, or technical control are centralized in practice.

“Smart Contracts Replace Compliance Programs”

Smart contracts can automate certain rules, but they don’t replace governance, oversight, or regulatory judgment.

Limitations include:

Inability to interpret evolving regulatory guidance

Lack of discretion in edge cases or disputes

Dependence on off-chain data and controls

Compliance remains an ongoing operational function, even when enforcement logic is embedded in code. Regulators expect monitoring, documentation, and human accountability alongside technical controls.

These misconceptions often surface late, after product decisions are already embedded. Addressing them early helps teams avoid costly redesigns and regulatory friction as tokenization models mature.

How to Evaluate Tokenization Models Before Launch

Evaluating tokenization models early is one of the most effective ways to avoid regulatory friction later. Once technical architecture, incentives, and distribution assumptions are embedded, correcting course becomes slower and more expensive.

A structured evaluation helps teams align product design with regulatory reality before launch, rather than reacting to it afterward.

A Practical Pre-Launch Compliance Checklist

Before committing to a tokenization model, teams should pressure-test the design against a short set of core questions.

Key items to review include:

What legal rights the token represents

Whether holders expect profit or appreciation

How tokens are issued, transferred, and redeemed

Which licenses or exemptions may apply

If the answers are unclear, regulators will likely view the model as higher risk. Ambiguity almost always works against the issuer.

See also:

When to Engage Regulators and Supervisors

Not every tokenization model requires immediate regulatory engagement, but many benefit from it. Early conversations are most useful when a model sits close to regulated activity or relies on novel structures.

Engagement is often appropriate when:

Tokens resemble securities, deposits, or payment instruments

Cross-border distribution is planned

Regulated intermediaries are involved

These discussions are typically exploratory, not approval requests. Framing them correctly can prevent misalignment later.

Build vs. Partner vs. Outsource Compliance

Tokenization models vary widely in operational burden. Some can be managed with lean internal processes. Others require dedicated teams and continuous oversight.

Common approaches include:

Building in-house for mature, regulated organizations

Partnering with licensed entities for distribution or custody

Outsourcing compliance operations to specialized firms

Outsourcing can often be more cost-effective than hiring full-time compliance staff, particularly for early-stage or fast-moving fintechs. Firms like InnReg are typically engaged when teams need deep fintech-specific expertise without adding permanent headcount.

Choosing the right operating model is as important as choosing the tokenization model itself. Both decisions shape how scalable and defensible the product will be over time.

Final Thoughts

Tokenization models are moving out of experimental sandboxes and into regulated financial markets. By 2026, the question will no longer be whether tokenization is viable, but which models can operate sustainably within existing regulatory frameworks.

Across every model covered in this guide, the same pattern holds. Regulatory risk is driven by economic substance, not technology. Products that treat compliance as a design constraint early tend to move faster later. Products that treat it as a post-launch problem rarely do.

This is where experienced compliance support becomes critical. InnReg works with fintechs building and operating regulated tokenization models, from early structuring and licensing through ongoing program management. If you’re evaluating tokenization models or preparing to launch one in 2026, talk to an expert now.

Adriana is a Principal Consultant at InnReg with 8 years of compliance experience specializing in VASP licensing and regulatory frameworks across Europe and LATAM. She has held senior compliance roles at leading global crypto and financial institutions, including Gate.io, Binance, Santander Bank, and BNP Paribas, with deep expertise in KYC/AML operations, MiCA adaptation, and building compliance programs from the ground up.

How Can InnReg Help?

InnReg is a global regulatory compliance and operations consulting team serving financial services companies since 2013.

We are especially effective at launching and scaling fintechs with innovative compliance strategies and delivering cost-effective managed services, assisted by proprietary regtech solutions.

If you need help with compliance, reach out to our regulatory experts today:

Related Articles

Featured LinkedIn Posts