FINRA on AI: Compliance Implications for Broker-Dealers

The rapid adoption of artificial intelligence in financial services is reshaping how broker-dealers operate, engage clients, and manage risk.

In response, FINRA AI guidance has emerged as a foundational reference for understanding where and how AI is being deployed across the securities industry. While some firms are cautiously experimenting, others are building dedicated AI teams and tools to drive scale and efficiency.

This article breaks down FINRA’s high-level overview of AI applications, drawn from its direct conversations with industry participants. We will cover how broker-dealers use AI in customer communications, investment processes, and operational functions such as compliance, surveillance, and cybersecurity.

At InnReg, we help broker-dealers align AI innovation with FINRA regulatory expectations. From registration to day-to-day compliance operations, our consultants support the full lifecycle of your compliance program.

FINRA: AI Applications in the Securities Industry

Financial Industry Regulatory Authority’s (FINRA) guidance on AI does not serve as a rulebook or endorsement. Instead, it offers a high-level snapshot of how broker-dealers are currently exploring artificial intelligence across core functions. The aim is to help market participants identify relevant use cases and understand potential regulatory implications.

The publication groups AI use into three primary areas: customer communications, investment processes, and operational functions.

FINRA points to a range of technologies already in motion, from virtual assistants and tailored content engines to tools that help detect compliance risks or evaluate credit exposure. Regardless of how efficient these systems become, firms are still expected to meet their full regulatory responsibilities.

For fintechs, FINRA guidance highlights how traditional and tech-forward broker-dealers alike are balancing innovation with compliance.

How FINRA Views AI: Guidance, Not Endorsement

FINRA is not setting rules for AI. Its current position is more observational than directive. The regulator’s commentary is intended to inform the industry of emerging trends and to caution firms about the potential risks associated with adoption. FINRA’s AI guidance serves as a reference point, not a regulatory framework.

This distinction matters. While the publication highlights many of the tools firms are exploring, like natural language processing, machine learning, and behavioral targeting, it stops short of validating their use.

FINRA does expect firms to conduct their own legal and operational analyses before deploying any AI-driven system. That includes weighing potential benefits against potential compliance, supervisory, and reputational risks.

For fintechs, this places responsibility squarely on internal teams (or outsourced partners) to determine where existing rules still apply. There is no AI carve-out for supervision, communications, or investor protection. Even the most advanced system does not replace the need for a compliance function that’s tuned into the risks and ready to act when something goes wrong.

FINRA on AI for Customer Communications in Broker-Dealer Firms

AI is showing up first where broker-dealers interact with clients: customer service, email handling, and outbound messaging.

FINRA acknowledges the appeal but cautions against complacency. These tools are still subject to the same advertising, supervision, and recordkeeping rules that apply to any broker-dealer communication, including FINRA Rule 2210, which governs how firms present information to the public.

We will break down each use case below, starting with:

Virtual Assistants and Chatbots in Client Service

Many broker-dealers are now deploying AI-powered chat systems to handle common client requests. These virtual assistants can field routine questions (checking balances, verifying recent trades, resetting passwords, and similar) without needing a human rep. They are often available 24/7 through web, mobile, or voice platforms.

Some firms are experimenting with voice-activated systems that integrate with tools such as Alexa or Google Assistant. Others use AI-based IVR systems in call centers to either answer basic questions directly or route callers to the right human rep based on intent.

While the operational benefits are clear, the compliance burden remains. Chatbot responses are still considered communications under FINRA rules. That means they are subject to review, supervision, and recordkeeping requirements.

Firms must validate both the content and the underlying logic: what the bot says and why it says it.

This matters most when the chatbot touches regulated topics. For example, if an interaction recommends a product or indicates suitability, it must meet the same standards as an interaction with a human advisor. It’s not enough to disclaim that “this is an AI tool.” Oversight responsibility remains with the firm.

Email Handling and Internal Inquiry Triage

AI is increasingly used to categorize and route incoming emails from clients and internal teams.

The software reviews the sender, the subject line, and the email body to determine the required action. It might respond to simple requests on its own or escalate more complex issues to the appropriate team member.

On the client-facing side, this can mean faster responses to routine questions, such as account updates or document submissions. Internally, firms are using similar models to streamline help desk functions, improving resolution times for operational or technical issues.

From a compliance standpoint, the key issue is supervision. Any auto-generated reply or triaged message falls under FINRA’s communications rules. Even if the response is templated or generated by machine logic, firms must still review it for accuracy, fairness, and alignment with regulatory obligations.

Firms should have a documented process for testing, approving, and monitoring these workflows. If AI is shaping the content or routing regulated communications, it becomes part of the supervisory system and needs to be treated accordingly.

AI-Driven Outreach and Behavioral Targeting

Firms are using tools that analyze client behavior across digital channels, enabling them to understand which content gets attention and how users navigate the site or app, and to craft more relevant follow-ups.

Some firms are also exploring how AI can predict when a client may be interested in a new service, based on patterns seen in similar accounts. This level of customization is driving higher engagement and is often integrated across email, push notifications, and the firm’s logged-in experience.

Highly tailored communications, while effective, carry additional scrutiny. If the message promotes a product or directs the client to take a specific action, it may trigger compliance reviews under existing FINRA rules.

Firms using AI for targeting should document how it selects content, what business rules drive the logic, and who reviews the materials. The systems may be automated, but compliance still needs visibility and control.

Customer Communication Risks Under FINRA AI Guidelines

FINRA consistently reminds firms that using AI tools does not reduce regulatory obligations. Whether it’s a chatbot, automated email, or behavior-triggered outreach, the standard for review remains the same.

If the content is promotional or perceived as influencing investment decisions, it may be subject to FINRA Rule 2210. If the communication includes any recommendation, it may trigger additional requirements under Reg BI or other suitability standards, depending on the client profile.

Using AI agents also introduces operational risks. Poor oversight can lead to inconsistent messaging, incorrect disclosures, or exposure of sensitive data.

Firms need to remember that any AI tool deployed for client communications is part of a supervised process with audit trails, clear documentation, and compliance input built in.

See also:

Agentic AI and Autonomy Risks

Recent FINRA commentary has highlighted the rise of AI agents (tools that operate independently to plan, decide, and act).

These systems introduce new regulatory concerns, especially when they act outside their intended scope, lack transparency, or trigger actions without human sign-off.

Firms using such agentic AI must reevaluate their supervision frameworks to account for elevated autonomy and reasoning complexity.

Tool | Common Use Cases | Key Regulatory Considerations |

|---|---|---|

Virtual Assistants/ Chatbots | Handling routine client requests (balances, trade confirmations, password resets); some voice-integrated tools. | Responses count as communications under FINRA rules. Firms must supervise, log, and test, especially if suggesting products. |

Email Triage and Internal Inquiry Handling | Auto-routing client emails; resolving low-complexity service tickets; internal ops/helpdesk automation. | Machine-generated replies must be reviewed for compliance. Supervision and audit trails are essential. |

Behavioral Targeting and Outreach Engines | Content personalization, action nudges during onboarding; product suggestions based on site behavior. | Tailored outreach may trigger Reg BI or Rule 2210 scrutiny. Documentation of logic and review processes is required. |

AI Agent Autonomy Risks | Emerging use of agentic AI for initiating actions across workflows without manual input. | FINRA flags risks around scope drift, lack of explainability, and reinforcement learning. Firms must embed oversight and scope limits. |

Need help with broker-dealer compliance?

Fill out the form below and our experts will get back to you.

FINRA on the Use of AI in Investment Processes

FINRA highlights how broker-dealers are incorporating AI into the investment process, from account-level insights to market execution. Applications include real-time profiling, predictive research, trade routing, and portfolio optimization.

The sections that follow break down each of these areas, focusing on where regulatory expectations still apply and where firms should exercise caution.

Real-Time Brokerage Account Management Tools

Broker-dealers are building dashboards that go beyond static reports. They show live account activity, flag anomalies, and sometimes push alerts based on market or client behavior.

This tech helps clients stay informed. However, if it pushes a decision, it becomes a regulatory issue. The messaging, triggers, and tone matter.

Anything that appears to be a suggestion could fall under FINRA scrutiny or even trigger a Reg BI review.

Learn more about Reg BI →

AI-Powered Customer Profiling and Suggestion Engines

Some firms are building client profiles using more than just account data. They are factoring in how people trade, what they read, and how they move through digital channels. Based on that, the system may surface next steps like a product prompt or a portfolio nudge.

The more tailored the output, the more scrutiny it draws. As a general rule, if it feels like advice, it may fall under Reg BI or FINRA communication rules.

The key question is not whether a human wrote the message. It is whether the message influences action. If the answer is yes, it is part of the firm’s regulatory footprint.

AI for Customized Research and Sentiment Insights

Some firms are using software to scan news, earnings calls, and online posts for signals. It saves time, but if the output reaches clients, it’s a compliance matter.

What to watch:

Where the data comes from

How the system decides what’s important

Who sees the results, and in what form

If it reads like advice, it’s treated like advice.

Portfolio Management: Pattern Recognition and Alternative Data

Firms are increasingly using AI tools to identify trading signals based on how clients behave, how markets move, and what is happening outside traditional financial data streams.

In some firms, models look for patterns across positions or peer accounts to flag possible adjustments. Others pull in non-market inputs (e.g., weather shifts, traffic flows, retail foot traffic) to anticipate opportunities or risks before they show up in earnings reports.

The idea is to give advisors or clients an edge in lead time. But once these tools inform decisions or influence strategy, they fall under the same scrutiny as any other part of the investment process.

If a model’s output nudges a portfolio rebalance or prompts a conversation with a client, that interaction needs to meet the firm’s regulatory standards.

FINRA does not prohibit this kind of innovation, but it does expect controls. That means firms should be clear on how the models work, where the data comes from, and whether anyone has reviewed how those insights reach an end user.

The more impact the tool has on outcomes, the more it becomes part of the firm’s regulatory footprint.

Trading Optimization: Execution, Pricing, and Allocation

AI tools are quietly influencing trade execution. They help decide when to act, what price to aim for, and how orders are split across markets. Some respond to real-time shifts in liquidity or pricing. Others use past trade data to avoid slippage or select a strategy that may lead to better outcomes.

Even if the system works in the background, its impact is front and center. If it changes how trades are priced or routed, it becomes part of the compliance conversation. That is especially true when algorithms operate faster than human input. In those cases, the design of the process and its monitoring takes on added weight.

See also:

Risk Scenarios and FINRA AI Oversight Expectations

As firms add AI into portfolio decision-making, FINRA is looking closely at how these systems impact oversight. If a model flags risk or triggers an allocation shift, that action is subject to the same rules as any other investment decision.

The challenge is that these tools don’t always work in isolation. A missed signal or misaligned trigger can affect outcomes quickly, especially if the tool operates without review.

In FINRA’s view, any model that influences decisions needs to be part of the firm's supervisory framework with controls, records, and accountability in place.

AI Application | Common Use Cases | Key Regulatory Considerations |

|---|---|---|

Real-Time Brokerage Account Management | Live dashboards, behavioral alerts, anomaly detection | If alerts influence decisions, they may trigger Reg BI or communications rules. Oversight is required. |

Customer Profiling and Suggestion Engines | Dynamic client segmentation, behavioral scoring, next-best-action prompts, and personalized product or portfolio suggestions | Personalized outputs that resemble advice are subject to Reg BI. Firms must validate logic and maintain oversight. |

Customized Research and Sentiment Insights | AI-generated news analysis, sentiment scoring from earnings calls, or public content | If insights are shared with clients, they count as communications and must meet compliance standards. |

Portfolio Management via Pattern Recognition | Trading signal identification, peer comparison, non-traditional data (e.g., traffic, weather) | When used to guide portfolio strategy, outputs must be documented, supervised, and justified under compliance rules. |

Trade Execution Optimization | Timing trades, price targeting, and order routing across venues | Even if used behind the scenes, execution models fall under supervision and review, especially if decisions bypass human input. |

AI-Triggered Risk Adjustments | Allocation changes, exposure alerts, automated rebalancing | Any model influencing investment actions must be embedded within the firm’s supervisory framework, with clear accountability. |

Operational Use of AI in Compliance and Risk

Broker-dealers are applying AI to core risk and compliance functions, from surveillance and onboarding to marketing reviews and transaction monitoring. These tools may reduce manual work, but they do not reduce regulatory responsibility.

Surveillance and Monitoring Beyond Rules-Based Systems

Some broker-dealers are using machine learning to flag unusual activity across accounts, reps, and systems. These models learn from past behavior and can spot changes that pre-set rules might miss, such as subtle shifts in trade timing or communication patterns.

The appeal is speed and scale. A well-trained model can review thousands of data points and flag potential issues faster than a traditional rules engine. But this doesn’t mean firms can take a hands-off approach.

If a model is driving alerts, the logic must be documented, reviewed, and explainable. FINRA expects firms to know how the system works, what triggers alerts, and how false positives or blind spots are managed. Just because a system is adaptive does not exempt it from supervision.

AI for KYC, AML, and Financial Crime Prevention

Some firms are now using advanced software to help with tasks like verifying client identities, checking transactions, and assigning risk levels. These systems can compare customer data to watchlists, scan for unusual activity, and spot irregularities across multiple accounts.

The benefit is scale. AI models can catch patterns that are easy to miss, such as layering, structuring, or subtle changes in behavior that might indicate suspicious activity.

But use does not remove responsibility. If AI plays a role in onboarding or AML review, its logic and outputs are subject to regulatory oversight. That includes how risk scores are assigned, when alerts are triggered, and who reviews escalations. Firms must be ready to explain decisions driven by machine logic just as clearly as those made by humans.

Designed based on InnReg’s experience of working with 100+ fintech, Regly FinCrime provides a comprehensive set of tools, including KYC/KYB and AML modules →

AI in Marketing Reviews

Firms use AI to streamline how they review marketing content, including web pages, email campaigns, social posts, and investor-facing documents.

These systems can flag common issues: missing disclosures, outdated language, or improper formatting. Some are trained on past approvals to help predict whether a piece will pass internal or regulatory review.

However, it is important to remember that marketing compliance still requires a human checkpoint. AI can assist, not replace. If content goes live, the firm is responsible for what it says and how it is interpreted.

FINRA Rule 2210 still applies. Tools used in review processes must be auditable, with documented logic and a clear chain of approval. Whether in a headline or a footnote, firms need to show how the messaging was vetted and by whom.

Learn how Regly uses AI to flag potential risks and streamline marketing approval processes →

Regulatory Intelligence Management and Machine-Readable Rules

Some broker-dealers are experimenting with AI tools that monitor regulatory updates and translate them into structured outputs. The goal is to reduce lag time between a rule change and internal action. These systems scan notices, enforcement actions, and rule proposals, surfacing what’s relevant based on the firm’s activities and product lines.

But building something reliable in-house is complex. It requires constant tuning, ongoing source validation, and the ability to link updates to practical workflows.

At InnReg, we have developed an internal system that automates much of this work. We connect directly with dozens of regulators and vetted third-party sources. Every month, AI processes thousands of updates, helping our consultants identify, prioritize, and flag what matters for each client.

This is not just a dashboard; it is a part of our hands-on compliance support. When you work with InnReg, our intelligence becomes part of your compliance program.

AI in Liquidity, Credit, and Cash Risk Assessment

Some firms are using AI to strengthen how they assess funding needs, credit exposure, and payment flows.

These tools pull data from multiple systems to spot pressure points in real time, such as when a counterparty’s activity pattern changes or when cash buffers dip below risk thresholds.

The technology may help identify issues earlier than manual checks, but the rules have not changed. If a model is influencing capital decisions, firms are expected to understand how it works, what triggers its alerts, and how outputs are reviewed.

See also:

Bias and Fairness Concerns in AI-Driven Credit Models

Credit models that rely on AI can surface hidden patterns. However, they can also introduce hidden bias. Variables that seem neutral on paper may correlate with sensitive characteristics like race, age, or income bracket, raising potential red flags around fairness.

FINRA does not prescribe how firms should test for bias, but it expects them to recognize and mitigate the risk. That includes running back-tests, stress tests, and independent audits, especially when models affect customer onboarding, credit approval, or rate setting.

FINRA also warns that general-purpose systems may lack the financial domain expertise needed to operate reliably in regulated contexts. (FINRA, Emerging Trend in GenA) Without proper training on industry-specific data, an AI model may produce outputs that appear logical but are contextually or legally inaccurate.

Firms must assess whether the model has the domain-specific training required for financial contexts. Outputs that sound plausible to a layperson may still fall short of fairness, suitability, or disclosure standards.

Cybersecurity and Insider Threat Detection with AI

AI tools are being applied in cybersecurity to monitor digital activity for signs of unauthorized access, data misuse, or insider threats. These tools can flag anomalies across login behavior, file access, and system usage that traditional rules may overlook.

But like other surveillance systems, they require structure and oversight.

Firms should be able to explain how the tools work, how data is stored, and what happens when a flag is triggered. If employee activity is being monitored, transparency and proper policy disclosures are key.

AI for Document Review and Contract Intelligence

AI can speed up the review of legal documents by extracting key terms, identifying risk clauses, and flagging gaps or inconsistencies. Some broker-dealers are using these tools to scan vendor agreements, client contracts, or product disclosures.

The value is in surfacing issues faster. But anything that affects disclosures, obligations, or client agreements must still be reviewed by a qualified professional.

Compliance Responsibilities Under FINRA AI Use

AI Does Not Reduce Regulatory Obligations

Replacing manual processes with automated ones does not reduce oversight requirements.

If a system helps decide when to reach out to a client, recommend a product, or monitor risk, its outputs are subject to the same scrutiny as any human-led activity.

That includes maintaining full documentation, applying suitability standards, and ensuring proper recordkeeping. Automation changes speed and scale, but not responsibility.

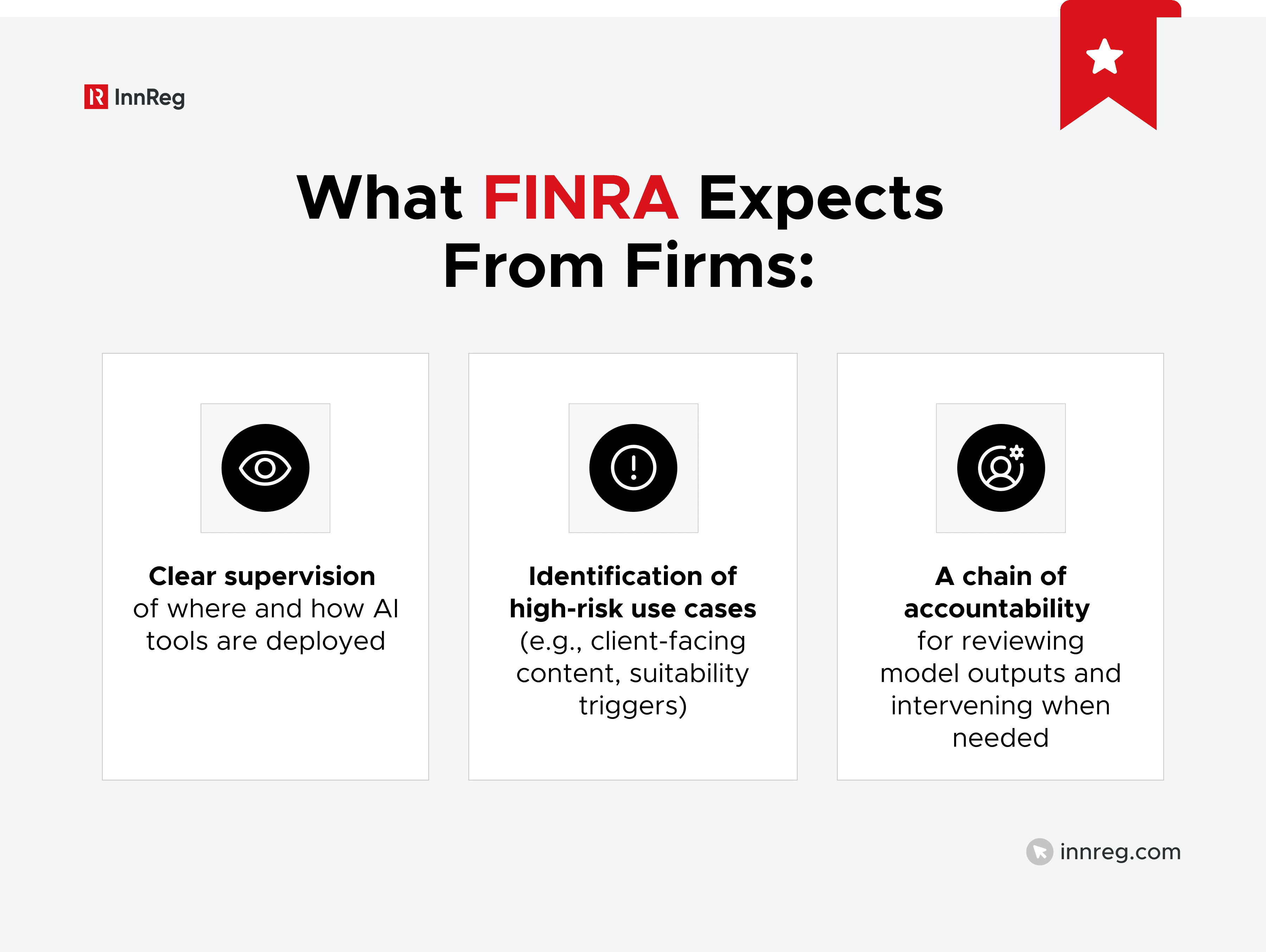

What FINRA Expects in Supervision and Model Oversight

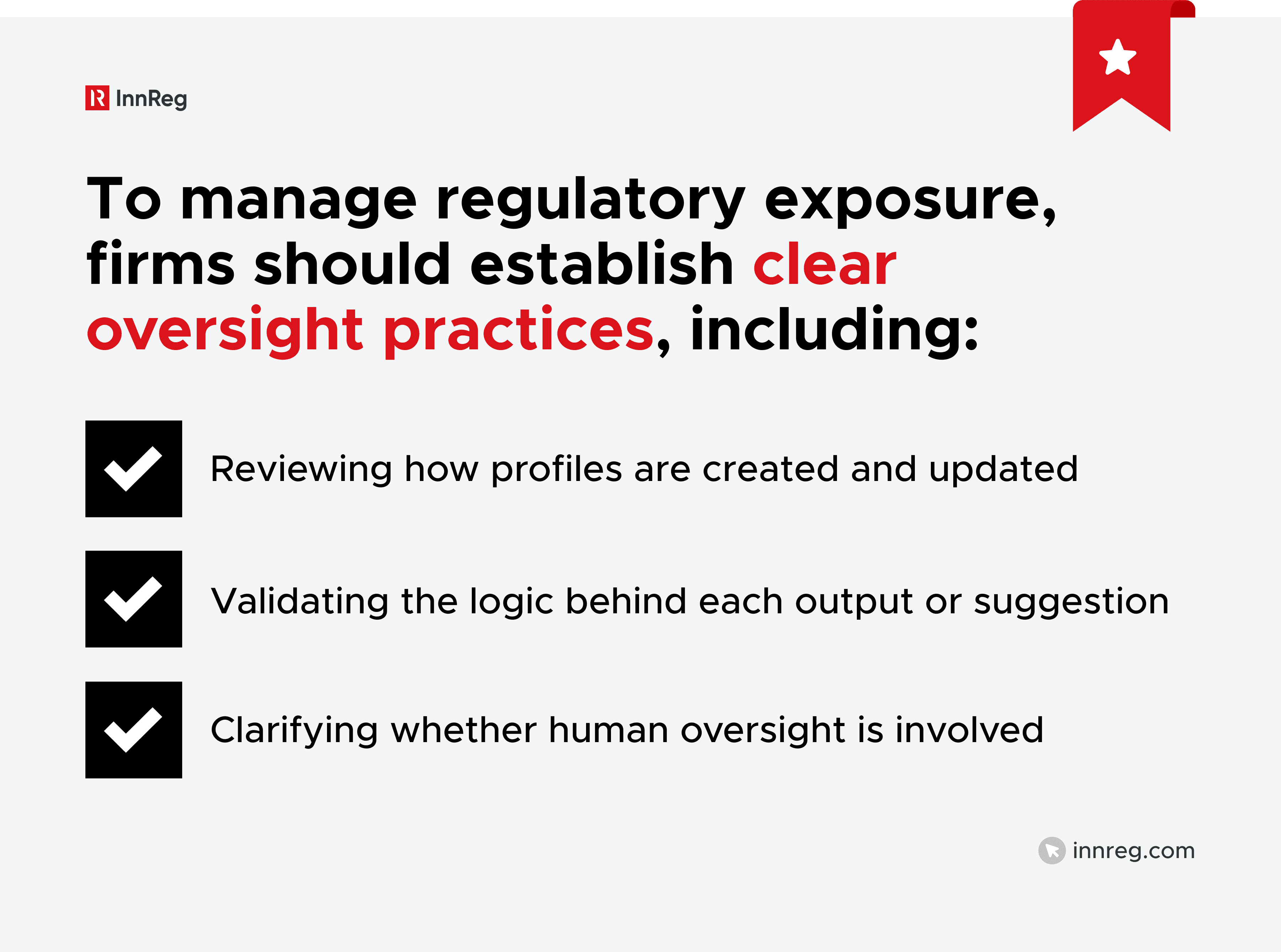

FINRA expects broker-dealers to integrate AI oversight into their existing compliance frameworks. Firms must treat AI systems as part of their supervisory architecture, not separate from it. This includes understanding where and how models are used, what logic drives them, and how their outputs are reviewed.

AI systems that operate with open-ended tasks or reinforcement-driven learning may optimize for goals misaligned with investor or firm interests.

FINRA explicitly flags this risk and expects firms to embed controls that address not just what the agent does, but why (FINRA, Emerging Trend in GenA). That means audit trails, scope constraints, and human validation checkpoints become even more critical when autonomy increases.

As models move from narrow logic to multi-step planning or task execution, governance must keep pace. Firms should be ready to explain not just outcomes, but the decision path behind them.

Data Quality, Documentation, and Explainability Standards

A system is only as reliable as the data that feeds it. FINRA places serious weight on data quality and transparency.

That means firms must know where their inputs come from, how the model was trained, and what logic it follows.

It is not enough to say that a tool works. The underlying process needs to be clear, documented, and explainable. If a regulator wants to know why the system flagged something or made a decision, the firm needs a plain-language answer.

—

FINRA’s AI guidance reaffirms that existing standards apply, regardless of how tasks are automated. Whether an AI tool sends a message or routes a trade, firms remain responsible for the outcome.

Regulators now look beyond function to governance and transparency.

Firms must know how each tool works, what triggers it, and how it’s supervised. "Black box" logic won’t hold up in an exam.

Those who embed AI within their compliance program, not around it, will move faster and stay protected. At InnReg, we help firms do exactly that.

Kushal Abeywickrama is the Chief Operating Officer at InnReg with over 10 years of experience in broker-dealer compliance, supervision, and regulatory operations across FINRA-regulated firms. He holds Series 7, 24, 4, 63, and 57 FINRA licenses and has previously held roles at HSBC and BlackSwan Technologies.

How Can InnReg Help?

InnReg is a global regulatory compliance and operations consulting team serving financial services companies since 2013.

We are especially effective at launching and scaling fintechs with innovative compliance strategies and delivering cost-effective managed services, assisted by proprietary regtech solutions.

If you need help with broker-dealer compliance, reach out to our regulatory experts today:

Related Articles

Featured LinkedIn Posts