Equal Credit Opportunity Act: A Practical Guide for Fintechs

The Equal Credit Opportunity Act (ECOA) is one of the most important US laws shaping fair lending practices.

For lenders building innovative credit products, understanding ECOA is not optional. It directly governs how they market, underwrite, and service credit, whether they are offering consumer loans, small business financing, or buy-now-pay-later programs.

This article explains the purpose of the law, the types of transactions it covers, and the obligations it imposes on financial institutions.

At InnReg, we help lenders and fintechs develop and operate ECOA and fair lending compliance programs, from policies and underwriting governance to adverse action workflows and bank-partner oversight. Contact us to learn more.

What Is the Equal Credit Opportunity Act?

The Equal Credit Opportunity Act was passed in 1974 as part of the Consumer Credit Protection Act. Its purpose is to prohibit discrimination in any aspect of a credit transaction. Before ECOA, it was common for women to be denied credit unless a husband or male relative co-signed. Similar barriers existed for applicants based on race, age, or source of income.

ECOA established a set of protected classes and requires lenders to evaluate applications based on creditworthiness rather than personal characteristics. The law is implemented through Regulation B, which provides detailed rules for compliance. Over time, ECOA has been updated to reflect broader definitions of discrimination, including protections related to sexual orientation and gender identity.

For fintech firms, ECOA shapes how products are built and offered. Whether developing a machine-learning underwriting model, structuring a buy-now-pay-later service, or lending to small businesses, compliance with ECOA determines what data can be used, how decisions are explained, and how applicants are treated throughout the process.

Learn about Fair Lending Act compliance →

Who and What the Equal Credit Opportunity Act Covers

The Equal Credit Opportunity Act’s scope is intentionally broad and covers nearly every form of credit, applying to a wide range of lenders and businesses:

Types of Credit Transactions Included

ECOA covers any extension of credit, whether personal, business, secured, or unsecured. This includes consumer loans, credit cards, auto and student loans, mortgages, lines of credit, small business loans, and buy-now-pay-later products. In short, if your company is deciding whether to extend credit, ECOA applies.

InnReg helps fintechs expand their operations by providing lender licence services →

For fintechs, this scope matters, as many innovative products blur traditional category boundaries. A cash-advance app, a digital line of credit, or a merchant financing product all fall under ECOA’s rules if they involve repayment terms and credit risk.

Institutions and Businesses Subject to ECOA

The law applies to any “creditor,” meaning any person or business that regularly participates in credit decisions. This includes banks, credit unions, online lenders, retail companies offering financing, and fintech platforms involved in underwriting or setting credit terms.

For fintechs that partner with banks, both the bank and the fintech can fall under ECOA. The bank is typically the lender of record, but regulators also expect fintech partners to meet compliance obligations when they influence marketing, eligibility, or pricing.

InnReg provides consulting services to help digital banks →

ECOA vs. Related Laws (Fair Housing Act, UDAAP)

ECOA often works in tandem with other laws. The Fair Housing Act prohibits discrimination in housing-related lending, including mortgages and home equity loans, and provides additional protections for individuals with disabilities and those with familial status. ECOA and FHA are commonly enforced together in mortgage cases.

The UDAAP standard (Unfair, Deceptive, or Abusive Acts or Practices) is broader. The CFPB has argued that certain discriminatory practices can be pursued under UDAAP, even outside of ECOA.

While courts are still debating the extent of that authority, fintech firms should view fair treatment not just as an ECOA obligation, but as part of a larger consumer protection framework.

Learn about Regulation Z (Truth in Lending) →

Protected Classes Under the Equal Credit Opportunity Act

At its core, ECOA is about preventing discrimination in credit decisions. To prevent discrimination in credit decisions, ECOA defines specific protected classes that lenders must not use as a basis for approval, denial, or terms of credit.

Under ECOA, creditors cannot discriminate against an applicant based on:

Race or color

Religion

National origin

Sex, including gender identity and sexual orientation

Marital status

Age (provided the applicant can legally contract)

Receipt of income from public assistance programs

Exercising rights under the Consumer Credit Protection Act

These protections apply in any aspect of a credit transaction, from marketing to application, underwriting, pricing, servicing, and collections.

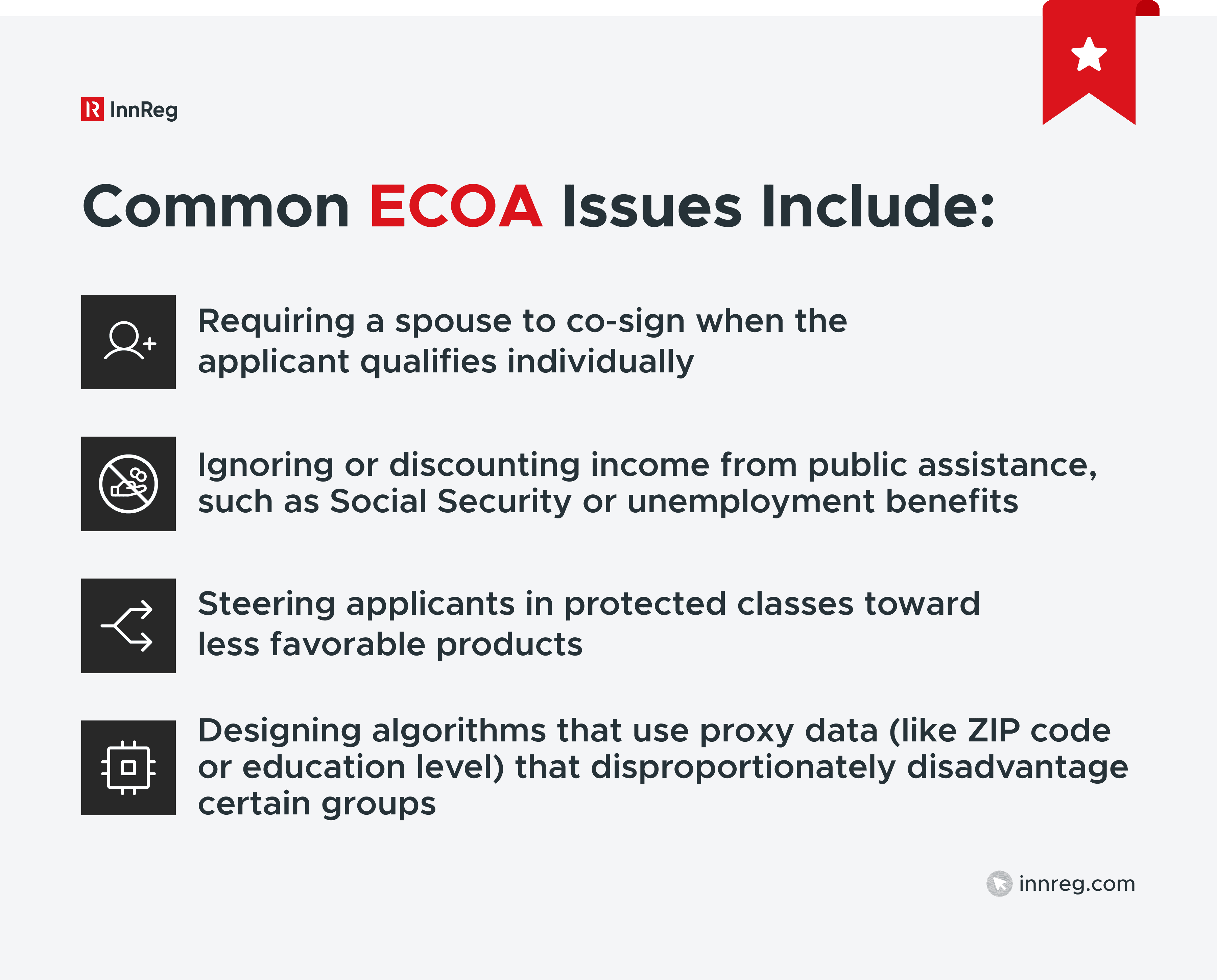

Some violations are obvious, such as denying a loan because of an applicant’s race. Others are more subtle.

For fintechs using machine learning, the risk often lies in indirect forms of discrimination. Building compliance checks into product workflows helps mitigate the exposure to enforcement actions.

Key Requirements Under ECOA (Regulation B)

ECOA’s broad prohibition on discrimination is implemented through Regulation B. The requirements of this regulation influence how fintech companies process applications, communicate decisions, and maintain records:

See also:

Timely Decision and Notice Obligations

Creditors must act on completed applications promptly.

In most cases, applicants must be notified of a decision within 30 days. The notice can be an approval, a denial, or a request for additional information.

For fintechs managing high application volumes, automated workflows can help in tracking dates and trigger responses without delay.

Need help with lender compliance?

Fill out the form below and our experts will get back to you.

Adverse Action Notices: What They Must Include

When a creditor denies an application or approves it with less favorable terms, they must provide an adverse action notice.

This notice must:

Be in writing or in a compliant electronic format

Clearly state the principal reasons for the decision

Inform the applicant of their right to request additional information

Generic or vague reasons, such as “credit criteria not met,” are insufficient. For fintechs relying on algorithms, this requirement creates pressure to build models that can output understandable reason codes for each decision.

Information Lenders Can and Cannot Request

ECOA limits the kind of information a creditor can ask during the application process.

Permitted vs. Prohibited Questions Under Regulation B | ||

|---|---|---|

Permitted: | Prohibited: | Caution: |

Marital status (only as married, unmarried, or separated). Age in the context of verifying legal capacity for a contract. | Details about religion, race, or spouse, unless required by law (such as in community property states or for joint credit). | Requesting demographic data in contexts outside of legal exceptions can create risk. |

Fintechs designing onboarding flows should carefully audit application forms to avoid collecting restricted data.

Recordkeeping and Monitoring Obligations

Regulation B requires creditors to retain application records for 25 months for consumer credit and 12 months for business credit.

These records include applications, communications, credit reports, and adverse action notices.

For fintechs, digital storage and audit trails are the norm. The key is to maintain organized systems that allow quick retrieval during a regulatory examination.

Special Purpose Credit Programs (SPCPs)

ECOA allows creditors to establish special-purpose credit programs that extend credit to groups who have historically faced disadvantages (for example, minority-owned businesses).

These programs must meet specific criteria:

A written plan describing the program and its objectives

A demonstration of need in the target community

Compliance with regulatory standards to avoid misuse

For fintechs focused on financial inclusion, SPCPs can be a compliant way to design products that expand access to underserved groups.

ECOA Regulators and Enforcement

Several federal agencies enforce the Equal Credit Opportunity Act, each responsible for different types of institutions:

Consumer Financial Protection Bureau (CFPB): Writes and enforces Regulation B. Oversees large banks and many non-bank lenders, including fintechs.

Department of Justice (DOJ): Pursues cases where a pattern or practice of discrimination is found. Often works with CFPB or banking regulators.

Office of the Comptroller of the Currency (OCC): Supervises national banks and their fintech partnerships.

Federal Deposit Insurance Corporation (FDIC): Oversees state-chartered banks that are not members of the Federal Reserve System.

Federal Reserve Board (FRB): Regulates state-chartered banks that are members of the Federal Reserve System.

Federal Trade Commission (FTC): Enforces ECOA against non-bank creditors under its jurisdiction.

State regulators and attorneys general: Enforce state-level fair lending laws, which often mirror or expand on ECOA.

How Examinations and Referrals Work

Banking regulators conduct periodic fair lending exams, reviewing loan files, policies, and data to detect discrimination. If they find evidence of discrimination, they must refer the matter to the DOJ.

For fintechs working with banks, examiners may scrutinize both the bank and the fintech’s role in underwriting, marketing, or servicing.

Non-bank lenders can also face direct CFPB exams. The agency reviews compliance management systems, adverse action notices, and statistical evidence of disparities. The FTC and state authorities can initiate investigations based on consumer complaints or market practices.

See also:

Penalties and Enforcement Actions

ECOA violations carry significant consequences. Agencies may impose civil money penalties, require restitution to harmed applicants, and mandate changes in business practices. The DOJ can file lawsuits seeking monetary damages and injunctive relief.

For fintechs, the most disruptive outcome is often operational. Regulators can order suspension of lending activities, impose consent orders with ongoing reporting obligations, or require partnerships to be restructured.

Reputational damage can also affect growth, investor confidence, and customer trust.

Common Compliance Challenges for Fintech Companies

Equal Credit Opportunity Act compliance rarely breaks down to a single rule or disclosure. For fintechs, the difficulty comes from aligning rapid innovation with regulatory boundaries. Fast product launches, technology-driven models, and the use of alternative data can open up compliance gaps if oversight is not embedded early.

Algorithmic Bias and AI Underwriting

Machine learning models can improve credit access but also introduce bias. Variables such as ZIP code, education, or spending patterns may act as proxies for protected characteristics.

If the model consistently produces disparate outcomes for certain groups, regulators may see this as discrimination.

To mitigate risk, fintechs need testing frameworks that identify and document potential bias, along with clear documentation of how credit decisions are made.

Use of Alternative Data and Proxies

Fintech lenders often turn to alternative data to reach applicants with little or no credit history.

Although this approach broadens access, it can also create compliance concerns. If the used data correlates with protected traits, the regulator could interpret it as discriminatory.

Fintechs may mitigate risk by limiting inputs to those linked to repayment and by reviewing models for disparate outcomes on a regular basis.

Bank-Fintech Partnership Oversight

Partnership models extend ECOA responsibilities to both banks and their fintech partners. Even if the bank is the lender of record, regulators expect fintechs to follow fair lending standards when influencing eligibility, pricing, or customer outreach.

This requires joint compliance frameworks, regular reporting, and transparent contractual allocation of responsibilities. Weak oversight can expose both parties to enforcement risk.

Learn about FDIC bank consent orders →

Digital Redlining in Marketing

Targeted advertising can create unequal reach across audiences. Algorithms that prioritize wealthier neighborhoods, for instance, may reduce exposure in minority communities. Regulators view this as a modern form of redlining.

Fintechs should monitor ad targeting strategies, track distribution data, and verify that campaigns reach diverse audiences.

Business Credit Applications and Misconceptions

ECOA covers both consumer and business credit. Some fintech founders assume small business lending is exempt, but that is incorrect. Business loan applicants have the same rights to fair treatment and adverse action notices as individual consumers.

Failing to provide proper notices or applying inconsistent criteria between business applicants can expose fintech lenders to regulatory findings.

Key Takeaways for Fintechs

The following practices can help fintech firms translate ECOA’s legal requirements into operational steps that fit fast-moving business models:

Building ECOA Compliance Into Product Design: Credit products should be designed with fair lending considerations from the start. This means involving compliance teams early when selecting eligibility criteria, structuring workflows, and planning customer communications. Addressing ECOA at the design stage reduces the need for costly changes later.

Monitoring and Testing Algorithms for Bias: Machine learning models and alternative data must be evaluated regularly by comparing approval and pricing outcomes across different demographic groups. Fintech teams should document why each data input was selected and how it relates to credit risk, so there is a clear rationale behind every decision variable.

Managing Adverse Action Workflows at Scale: High application volumes can put pressure on compliance operations. Automating adverse action notices can be highly useful, especially when systems are designed to produce clear and accurate reason codes. Keeping logs of each notice also makes it much easier to retrieve records during audits.

Coordinating With Partner Banks on ECOA Duties: In fintech-bank partnerships, ECOA duties need to be clearly established: contracts should specify who is responsible for tasks such as sending notices and maintaining monitoring records. Regular check-ins between partners reduce misunderstandings and support consistent compliance practices.

Leveraging Outsourcing or Expert Partners for Compliance Programs: As not every fintech has the internal capacity to manage complex fair lending requirements, outsourcing compliance functions can provide access to specialized expertise, proven workflows, and cost-effective resources.

InnReg helps fintech offering bank-like and digital banking services →

—

For fintech companies, ECOA is not only a legal requirement but also a framework for building responsible, scalable lending products.

By defining protected classes, requiring transparent decision-making, and assigning oversight to multiple regulators, ECOA sets the standard for fair access to credit.

Compliance with ECOA comes down to daily operations: fintechs need to design products with fair lending in mind, maintain accurate records, and manage notices and workflows efficiently.

InnReg was founded in 2013 by Francesco Matteini, former Chief Compliance Officer who helped launch and scale some of the most innovative digital broker-dealers over the last two decades. He built compliance programs to support the first zero-commission broker and the first BD-sponsored investor social network. Since its founding, InnReg has attracted highly experienced fintech consultants with long careers in compliance, risk management, and a deep understanding of the fintech industry.

How Can InnReg Help?

InnReg is a global regulatory compliance and operations consulting team serving financial services companies since 2013.

We are especially effective at launching and scaling fintechs with innovative compliance strategies and delivering cost-effective managed services, assisted by proprietary regtech solutions.

If you need help with lender compliance, reach out to our regulatory experts today:

Related Articles

Featured LinkedIn Posts