What Is Algorithmic Trading in Financial Markets?

Algorithmic trading plays a central role in how modern financial markets operate. In fact, today, algorithmic trading underpins large parts of equities, derivatives, and digital asset markets.

For fintech companies, algorithmic trading affects product design, regulatory classification, licensing requirements, market access controls, and ongoing compliance obligations. Decisions about how algorithms are built, tested, and deployed can determine whether a business model is viable under US securities or commodities law.

This article explains what algorithmic trading is, who uses it, and how it works from a technology and strategy angle. It also focuses on the regulatory and compliance considerations you might need to understand around this.

At InnReg, we help fintech founders understand how algorithmic trading impacts registration, supervision, and regulatory risk. We support firms from early regulatory analysis through ongoing compliance operations.

What Is Algorithmic Trading?

Algorithmic trading is the use of computer programs to execute trades based on predefined rules. Those rules can reference price movements, timing, volume, market data, or combinations of multiple inputs. Once deployed, the system places orders automatically without manual intervention on each trade.

At a basic level, algorithmic trading replaces human execution with rule-based logic. The algorithm monitors the market, evaluates conditions, and submits orders when its criteria are met. The complexity can vary widely from simple execution rules to highly sophisticated models operating across multiple venues.

In financial markets, algorithmic trading is used to improve execution consistency, manage large order flow, and respond to market conditions at speeds that manual processes cannot realistically match.

Algorithmic Trading vs. Manual Trading

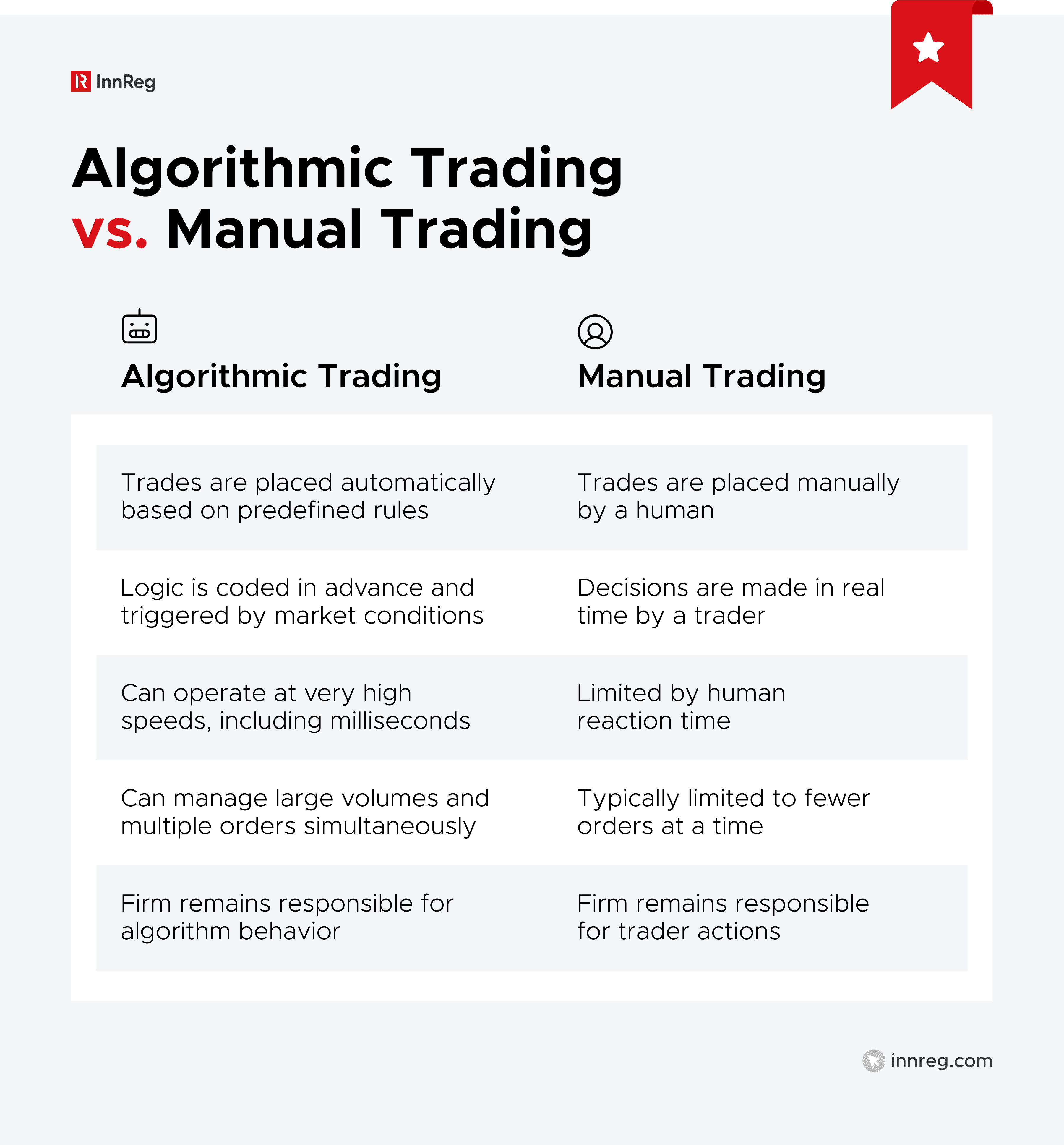

Manual trading relies on a human making decisions and placing orders directly. Algorithmic trading shifts that decision-making into software, with humans setting the rules and oversight framework rather than executing each trade.

Key differences include:

Decision execution: Manual trading depends on human judgment in real time. Algorithmic trading, on the other hand, executes based on predefined logic once conditions are met.

Speed and scale: Algorithms can react to market data and submit orders in milliseconds, and can manage large volumes simultaneously.

Consistency: Algorithms apply the same logic every time, while manual trading is influenced by discretion and judgment.

From a compliance perspective, the distinction matters. Algorithmic trading does not remove human responsibility. Firms remain accountable for how their algorithms behave, how they are supervised, and whether they comply with market rules and regulatory expectations.

Is Algorithmic Trading Legal?

Yes, algorithmic trading is legal in the US. No rule prohibits the use of algorithms to place or execute trades. However, fintechs should see whether the activity complies with applicable securities or commodities laws.

Regulators treat algorithmic trading as another method of market participation. The same core obligations apply as with manual trading, including:

Prohibitions on market manipulation

Requirements around supervision

Expectations for risk controls

When an algorithm violates those rules, regulators look to the firm and its supervisors, not the software itself. That said, algorithmic trading can trigger additional regulatory scrutiny. This is because automated systems can generate high-order volumes, interact with multiple venues, and amplify errors quickly.

Whether algorithmic trading is legal for a particular business model depends on several factors, including:

The asset classes traded, such as securities, futures, or digital assets

Whether trading is proprietary or done on behalf of clients

How the algorithm interacts with markets and trading venues

Whether the activity requires registration as a broker-dealer, advisor, or commodities registrant

And for fintechs, the answer is rarely ever yes or no. The more relevant question is often how algorithmic trading fits into existing regulatory categories and what obligations follow from that classification.

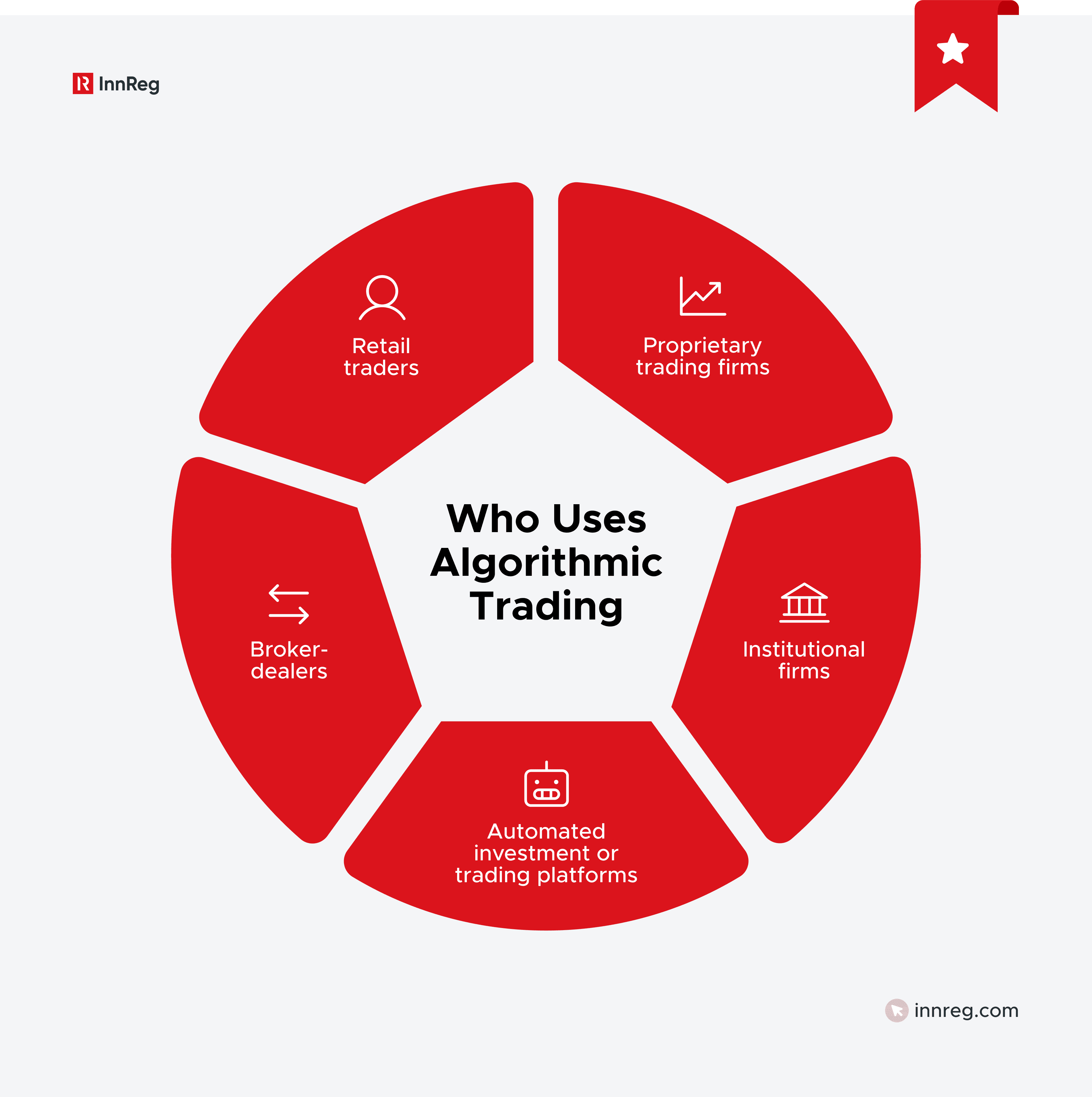

Who Uses Algorithmic Trading Today?

Algorithmic trading is no longer limited to a narrow group of quantitative hedge funds. It’s used across the financial markets by firms with very different goals, structures, and regulatory profiles.

Here are the common users of algorithmic trading:

Institutional Firms and Proprietary Trading Firms

Large institutional firms were early adopters of algorithmic trading and remain heavy users today. This includes banks, hedge funds, asset managers, and proprietary trading firms trading their own capital.

These firms use algorithmic trading to manage execution risk, handle large order sizes, and interact with fragmented markets. Strategies often focus on execution quality, liquidity provision, or short-term pricing inefficiencies. From a regulatory standpoint, these firms are typically already registered and supervised, which shifts the focus toward internal controls, supervision, and market conduct.

Regulators tend to scrutinize these firms closely due to trading volume, market impact, and the potential for systemic effects if algorithms malfunction.

Fintech Platforms and Trading Technology Providers

Fintech companies increasingly build products that rely on algorithmic trading, even if trading is not their core business. Examples include automated investing platforms, embedded trading features, and execution tools offered through APIs.

In these cases, algorithmic trading can affect how the platform is classified. Depending on the design, a fintech may be viewed as a broker-dealer, an advisor, a trading venue, or a technology provider supporting regulated activity. The distinction is rarely obvious from a product description alone.

Note: This is where fintech-specific regulatory analysis matters. Small design choices around discretion, order routing, or automation can materially change a firm’s regulatory obligations.

Retail and API-Driven Algorithmic Trading

Retail traders increasingly access algorithmic trading through broker APIs, third-party tools, or no-code strategy builders. While the trading volume per user may be smaller, the aggregate activity can still be significant.

Retail-facing algorithmic trading raises different concerns. These include:

Customer disclosures

Suitability

Supervision of automated strategies

Controls around misuse or abusive trading patterns.

Even when algorithms are built by end users, platforms and brokers retain compliance responsibilities. For fintechs enabling this activity, the risk often lies less in the strategy itself and more in how the product is governed, monitored, and supported from a compliance perspective.

See also:

The Technology Behind Algorithmic Trading Systems

Algorithmic trading systems rely on a layered technology stack that connects market data, decision logic, and execution infrastructure. The design of this stack directly affects trading behavior, risk exposure, and regulatory obligations.

While strategies get most of the attention, regulators often focus on the underlying systems of how data is sourced, how orders are generated, and how failures are handled.

Here is a breakdown of the technology used:

Need help with RIA compliance?

Fill out the form below and our experts will get back to you.

Data Feeds, Latency, and Execution Infrastructure

Market data sits at the center of everything in algorithmic trading. Algorithms pull in real-time and historical feeds to assess conditions and decide when to trade. Those feeds might come straight from exchanges or through third-party data vendors.

Speed matters. A lot. Faster systems can react before slower ones, which is the whole point of low-latency infrastructure. But that speed comes with operational risk.

Low-latency infrastructure increases the need for robust controls, throttles, and kill-switch mechanisms, especially when you're trading across multiple venues at once.

Execution infrastructure connects the algorithm to exchanges, brokers, or liquidity providers. This layer must handle order routing, acknowledgments, rejections, and error states. From a compliance standpoint, failures here can lead to erroneous orders, duplicate trades, or market disruptions.

Use of AI and Machine Learning in Algorithmic Trading

Some algorithmic trading systems use machine learning or AI to refine their strategies as new data comes in. These models might tweak parameters, shift how they weight certain signals, or change execution behavior over time without anyone manually updating the code.

That flexibility creates real compliance challenges. AI-driven trading is harder to explain, harder to test, and harder to supervise, particularly when the model's decision logic isn't fully visible even to the people who built it.

Regulators still expect firms to understand and document how these models behave, even when the model keeps learning and changing.

For fintechs, the question isn't whether using AI is allowed. It's whether your supervision, testing, and governance frameworks can actually keep up with a system that doesn't stay static.

Learn more about AI compliance in our guide →

Limits of Backtesting and Model Assumptions

Backtesting is a standard part of algorithm development. It involves testing a strategy against historical data to evaluate how it would have performed under past market conditions.

However, backtesting has limits. Historical data cannot fully capture future market behavior, liquidity conditions, or structural changes. Overreliance on backtesting can obscure real-world risks, particularly in stressed or unusual market environments.

Backtesting should be ideally complemented by forward-looking testing, scenario analysis, and ongoing performance monitoring once the algorithm is live.

Common Algorithmic Trading Strategies

Algorithmic trading strategies define how and when an algorithm places trades. The strategy determines the data inputs, decision rules, execution logic, and risk profile. Below are the most common categories used across financial markets today:

Trend-Following and Signal-Based Strategies

Trend-following strategies place trades based on predefined signals. These signals may come from price movements, technical indicators, or statistical thresholds.

The logic is straightforward. When the signal is triggered, the algorithm executes according to preset rules. These strategies are widely used because they are relatively easy to test and explain, but they can still generate rapid order flow in volatile markets.

Note: From a risk standpoint, signal-based strategies can perform poorly when markets shift regimes or move sideways for extended periods.

Arbitrage and Market-Making Strategies

Arbitrage strategies attempt to exploit price differences across venues, instruments, or related assets. Market-making strategies focus on providing liquidity by continuously quoting buy and sell prices.

These strategies often involve high message rates and frequent order updates. Because of their interaction with market structure, regulators closely monitor arbitrage and market-making algorithms for disruptive behavior, self-trading, or manipulative patterns.

Small configuration errors in these strategies can lead to outsized exposure in short periods of time.

High-Frequency Trading as a Subset of Algorithmic Trading

High-frequency trading, or HFT, is a specialized subset of algorithmic trading. It is characterized by very low latency, high order volume, and short holding periods.

Not all algorithmic trading is high-frequency trading. However, HFT strategies tend to attract heightened regulatory scrutiny due to their speed, scale, and potential market impact.

Firms operating in this space typically face stricter expectations around testing, controls, and real-time monitoring.

Portfolio Rebalancing and Execution Algorithms

Execution algorithms are designed to manage how trades are carried out, rather than what is traded. Examples include:

Volume-weighted average price (VWAP)

Time-weighted average price (TWAP)

Rebalancing algorithms used by asset managers and automated investment platforms.

These strategies aim to reduce market impact and execution risk. They are common in fintech products that automate investing or portfolio management, including robo-advisory platforms.

Key US Regulators Overseeing Algorithmic Trading

Algorithmic trading in the US is regulated through existing securities and commodities frameworks. There is no single regulator dedicated only to algorithmic trading. Instead, oversight depends on the markets traded, the instruments involved, and the role the firm plays.

Understanding which regulator has jurisdiction is a foundational compliance step. For many fintechs, multiple regulators may be relevant at the same time:

SEC Oversight

The Securities and Exchange Commission (SEC) oversees algorithmic trading activity in securities markets, including equities, options, and certain digital asset products that qualify as securities.

The SEC focuses on market integrity, investor protection, and orderly markets. In the context of algorithmic trading, this includes

Scrutiny of market manipulation

Disclosure obligations

Failures to supervise automated systems

When algorithmic trading involves securities, the SEC ultimately sets the regulatory tone, even when day-to-day supervision is delegated to self-regulatory organizations.

The SEC also oversees exchanges and alternative trading systems, which means platform design and order handling logic can fall within its scope.

See also:

FINRA Rules and Supervision

FINRA is responsible for supervising broker-dealers engaged in algorithmic trading. This includes firms that execute trades for clients, provide market access, or operate trading platforms tied to securities markets.

FINRA places strong emphasis on supervision, testing, and governance of algorithmic trading systems. It expects firms to:

Understand how their algorithms operate

Monitor them on an ongoing basis

Maintain controls that address trading errors and abusive patterns.

FINRA enforcement actions often focus on breakdowns in supervision rather than the trading strategy itself. FINRA rules frequently drive day-to-day compliance obligations for fintechs operating as or alongside broker-dealers.

CFTC Regulation

The Commodity Futures Trading Commission (CFTC) regulates algorithmic trading in futures, options on futures, and swaps markets. This includes many high-speed and quantitative trading strategies.

The CFTC’s focus areas include disruptive trading practices, spoofing, and market stability. While the CFTC has taken a principles-based approach to algorithmic trading rules, it has been active in enforcement. Algorithmic trading misconduct in derivatives markets has resulted in significant civil and criminal penalties.

For firms trading both securities and derivatives, coordination across the SEC, FINRA, and CFTC requirements becomes a practical necessity rather than a theoretical concern.

Core Regulatory Requirements for Algorithmic Trading Firms

Algorithmic trading does not create a separate regulatory regime, but it does shape how existing rules apply. Firms are regulated based on what they do, not the fact that trading is automated.

The core requirements typically fall into registration, market access controls, and ongoing supervision:

Registration and Licensing Considerations

Whether algorithmic trading triggers registration depends on the business model. Firms trading their own capital face a different analysis than those trading for clients or providing trading functionality to third parties.

Common regulatory questions include:

Is the firm acting as a broker-dealer by routing or executing client orders?

Does the platform exercise discretion that could trigger advisor registration?

Are derivatives involved, requiring CFTC or NFA registration?

Algorithmic trading frequently accelerates registration timelines because automation reduces the line between technology provider and regulated intermediary.

Market Access Rules and Pre-Trade Risk Controls

Firms with direct or indirect market access are expected to implement controls that prevent erroneous or disruptive orders. This applies regardless of whether orders originate from humans or algorithms.

Typical controls include:

Order size and price limits

Message rate and exposure thresholds

Automated kill switches and trading halts

Regulators view pre-trade controls as a baseline expectation, particularly for high-volume or low-latency trading environments.

Supervision, Testing, and Governance Expectations

Supervision does not end once an algorithm is deployed. Firms are expected to understand how their algorithms operate, how changes are approved, and how performance is monitored.

This usually involves:

Documented testing before deployment and after material changes

Ongoing monitoring for errors, abnormal behavior, and compliance risks

Clear ownership across engineering, trading, and compliance teams

From a regulatory perspective, algorithmic trading failures are often framed as governance failures. The lesson learned is that regulators tend to focus on oversight first, not sophistication.

Common Compliance Challenges in Algorithmic Trading

Algorithmic trading combines operational, market, and regulatory risks into software. When problems occur, they often surface quickly and at scale. Here are some of the most common compliance challenges you might encounter as you engage in algorithmic trading:

Managing Algorithm Risk and Trading Errors

Automated systems can generate large numbers of orders in very short periods of time. A logic error, data issue, or infrastructure failure can result in unintended trades or market exposure.

Some of these common risk points are:

Inadequate testing before deployment or after code changes

Poor handling of edge cases and extreme market conditions

Delayed detection of abnormal trading behavior

Unintentional failures are not exempt from scrutiny. Regulators expect firms to anticipate these risks and design controls accordingly.

Preventing Market Manipulation and Abusive Trading

Algorithmic trading systems can accidentally produce activity that looks a lot like market manipulation. When a firm's order cancellation rates spike, or when orders come in faster than any human could submit them, or when trades end up crossing between the firm's own accounts, regulators start asking questions.

Key areas of focus include:

Spoofing and layering risks, where orders are placed with no intention of execution to move prices.

Self-trading and wash trade patterns, where a firm ends up on both sides of the same transaction.

Momentum ignition and quote stuffing, where the goal appears to be disrupting normal market function.

What makes enforcement tricky here is that regulators often work backward from results. If the trading pattern looks manipulative, the burden shifts to the firm to show it wasn't. That means firms need active surveillance to catch these patterns before they become a problem and to step in when something looks off.

Monitoring, Surveillance, and Audit Trail Obligations

Ongoing monitoring is a core requirement, not an optional enhancement. Firms must be able to reconstruct what an algorithm did, why it did it, and who approved it.

This typically requires:

Real-time or near-real-time trade surveillance

Detailed logs of algorithm logic, changes, and deployments

Retention of order and execution data for regulatory review

In algorithmic trading, documentation and audit trails are as important as the strategy itself. Gaps here are a common source of regulatory findings.

See also:

Frequent Misconceptions About Algorithmic Trading

Algorithmic trading is often discussed in simplified terms. That creates misunderstandings that can lead to poor regulatory decisions or misplaced risk assumptions. Below are misconceptions that commonly surface in fintech and trading businesses.

Algorithmic Trading vs. High-Frequency Trading

Algorithmic trading and high-frequency trading are not interchangeable. All high-frequency trading is algorithmic, but most algorithmic trading is not high-frequency.

High-frequency trading involves very low latency, high order volumes, and short holding periods. Most algorithmic trading strategies operate at much lower speeds and volumes, including execution algorithms and portfolio rebalancing tools.

Confusing the two can lead firms to either underestimate their obligations or overbuild controls that don’t match their actual risk profile.

Responsibility for Algorithm Decisions

A common misconception is that responsibility shifts to the algorithm once it’s live. That’s not how regulators view it.

The algorithm might be doing the trading, but the firm is still on the hook for everything that the algorithm does. That accountability runs through the entire lifecycle, from how it's built and tested to how it's rolled out and watched over.

Engineering, trading desks, and compliance all share pieces of that responsibility. Letting a machine make decisions doesn't mean anyone gets to step back from supervising those decisions.

When something goes wrong, regulators aren't going to dig through your source code looking for bugs. They're going to ask about your governance structure. Who had oversight? What controls were in place? When the issue surfaced, how did it get escalated and addressed? Those are the questions that matter in an enforcement context.

Profitability vs. Regulatory Risk

Firms often market algorithmic trading by claiming that itimproves performance or efficiency. That framing can obscure regulatory risk.

Even strategies that appear operationally sound can create compliance exposure if they interact poorly with market rules or platform design. Profitability does not offset regulatory obligations, and regulators do not evaluate strategies based on financial outcomes.

For fintechs, the key question is not whether an algorithm works, but whether it operates within the firm’s regulatory perimeter.

How Compliance Firms Support Algorithmic Trading Businesses

Most fintech teams aren't built to handle the regulatory side of algorithmic trading on their own. It's not a knock on capability. It's just that the compliance demands in this space are dense, fast-moving, and easy to get wrong.

And the problems usually don't show up during development. They surface after launch, when a regulator reviews your trading patterns or a partner bank asks questions you weren't expecting.

That's the point where specialized compliance support stops being a nice-to-have and starts being a practical necessity. For fintechs that are scaling quickly, the most useful compliance partners don't operate like gatekeepers or auditors showing up at the end of a project. They embed alongside your team, helping you make decisions in real time instead of flagging issues after the fact.

Registration and Regulatory Strategy

One of the earliest challenges is determining how algorithmic trading fits into existing regulatory categories. Small design decisions around discretion, order routing, or automation can change whether a firm is viewed as a broker-dealer, advisor, commodities registrant, or technology provider.

This is where compliance expertise pays off early. The work involves translating your actual business model into the right regulatory framework, not over-registering just to be safe, but getting it right from the start so you're not unwinding decisions later.

That means thinking through regulator engagement, realistic licensing timelines, and jurisdictional questions when your product operates across multiple markets.

InnReg works with fintechs at this stage regularly, especially when the product doesn't fit neatly into traditional regulatory buckets. Innovative trading platforms often don't, and sorting that out early saves significant time and cost down the line.

Compliance Program Design for Algorithmic Trading

Once registration questions are addressed, firms need controls that match how algorithmic trading actually operates. Generic compliance templates rarely account for automated decision-making, low-latency execution, or rapid iteration cycles.

Effective programs typically cover:

Algorithm testing, change management, and approvals

Pre-trade and post-trade risk controls

Surveillance tailored to automated trading behavior

Compliance design needs to reflect how engineers build and deploy systems, not how regulators describe them in the abstract.

Ongoing Oversight and Operational Support

Algorithmic trading compliance is not static. Strategies evolve, code changes, and markets behave unpredictably. Ongoing oversight is where many firms struggle, especially as trading volume scales.

Outsourced compliance teams can take ownership of monitoring, documentation, regulatory interactions, and internal coordination. For many fintechs, this model is more practical and cost-effective than hiring a single in-house compliance officer, particularly when algorithmic trading spans multiple regulatory regimes.

InnReg often operates in this capacity, integrating into client workflows and systems while maintaining independent compliance oversight aligned with fast-moving product teams.

—

Algorithmic trading can support innovation, but it also introduces regulatory and operational complexity that needs to be addressed early. How algorithms are designed, deployed, and supervised directly affects licensing, compliance obligations, and long-term viability.

InnReg works with fintechs using algorithmic trading across securities, derivatives, and hybrid products. We support registration, compliance program design, and day-to-day oversight, often acting as an outsourced compliance function.

If you are building or scaling an algorithmic trading product, contact InnReg to discuss a practical, regulator-informed approach.

InnReg was founded in 2013 by Francesco Matteini, former Chief Compliance Officer who helped launch and scale some of the most innovative digital broker-dealers over the last two decades. He built compliance programs to support the first zero-commission broker and the first BD-sponsored investor social network. Since its founding, InnReg has attracted highly experienced fintech consultants with long careers in compliance, risk management, and a deep understanding of the fintech industry.

How Can InnReg Help?

InnReg is a global regulatory compliance and operations consulting team serving financial services companies since 2013.

We are especially effective at launching and scaling fintechs with innovative compliance strategies and delivering cost-effective managed services, assisted by proprietary regtech solutions.

If you need help with RIA compliance, reach out to our regulatory experts today:

Related Articles

Featured LinkedIn Posts