Vendor Management Policy: A Guide for Regulated Companies

Key Takeaways

Outsourcing a function to a vendor does not transfer the firm’s underlying compliance responsibility.

A strong vendor management framework typically includes risk tiering, due diligence, contract standards, ongoing monitoring, and exit planning.

Vendor relationships can create operational, cybersecurity, compliance, business continuity, and concentration risks.

Critical or high-risk vendors generally require more detailed diligence, stronger controls, and closer ongoing monitoring.

An effective policy should be supported by practical workflows for onboarding, periodic reassessment, escalation, and ongoing updates.

Financial companies rely on a growing network of service providers. Cloud platforms, payment processors, KYC vendors, cybersecurity firms, trading infrastructure providers, and data analytics platforms often sit at the center of daily operations. For regulated entities, this makes a vendor management policy a core part of the compliance framework, not just an operational document.

Regulators across the US expect firms to maintain oversight of third parties that support regulated activities. Outsourcing technology, compliance tasks, or operational functions does not transfer regulatory responsibility. Broker-dealers, RIAs, and fintech companies are still accountable for how vendors handle sensitive data, support customer-facing systems, and affect regulatory obligations.

This article explains what a vendor management policy is and why regulators focus on vendor oversight. It also walks through the risks regulators expect firms to address, the components commonly included in a vendor management policy, and practical steps companies can take to build and operationalize one.

At InnReg, we support fintechs and regulated financial firms with vendor management policy development and broader compliance program design. Our team helps clients build workable processes for vendor due diligence, monitoring, and internal oversight. Contact us to learn more.

What Is a Vendor Management Policy?

A vendor management policy is a formal document that defines how a regulated company selects, evaluates, monitors, and oversees third-party service providers. In financial services, these policies help structure how firms manage operational, regulatory, and data risks introduced by external vendors.

Many financial institutions depend on vendors for critical functions. These may include:

Payment processing

Customer onboarding tools

Trading systems

Cybersecurity infrastructure

Cloud hosting

A vendor management policy establishes the governance framework for those relationships, outlining how vendors are approved, how risks are assessed, and how performance is monitored over time.

Regulators across the US expect firms to maintain visibility into third-party relationships that affect regulated activities. As a result, vendor management policies typically address areas such as due diligence, contractual safeguards, ongoing monitoring, and escalation procedures.

For fintech companies and regulated financial firms, the policy often acts as the foundation of a broader vendor risk management program, supported by procedures, risk assessments, and internal oversight workflows.

Vendor Management vs. Procurement Management

Vendor management and procurement are closely related, but they serve different functions within regulated companies. Procurement typically focuses on sourcing vendors, negotiating contracts, and managing purchasing processes. Vendor management, by contrast, focuses on ongoing oversight of third-party relationships and the risks they introduce.

In financial services, the distinction matters because regulators expect firms to supervise vendors that support regulated activities. Procurement may handle vendor selection and contracting, but a vendor management policy governs how those vendors are reviewed, monitored, and evaluated from a compliance and risk perspective.

The difference becomes clearer when comparing typical responsibilities:

Procurement Function | Vendor Management Function |

|---|---|

Vendor sourcing and RFP processes | Vendor risk assessment |

Contract negotiation and pricing | Regulatory and compliance oversight |

Purchase approvals | Ongoing monitoring and performance reviews |

Vendor onboarding logistics | Incident reporting and escalation |

For regulated firms, vendor management often sits within compliance, risk management, or a cross-functional governance process involving legal, security, and operations. Procurement may initiate the relationship, but vendor oversight continues throughout the lifecycle of the vendor relationship.

Regulatory Expectations for Vendor Oversight

Financial regulators consistently emphasize that outsourcing services does not remove a firm’s regulatory responsibilities. Several regulatory bodies have published guidance addressing third-party and vendor risk management. The expectations vary slightly by sector but follow similar principles:

SEC Expectations for Investment Advisors

Investment advisors frequently rely on third-party providers for services such as compliance tools and cybersecurity infrastructure. While these vendors support daily operations, the SEC expects advisors to maintain oversight of service providers that affect regulated activities.

Several SEC rules and guidance documents address vendor oversight indirectly through broader compliance obligations.

For example, the Compliance Rule under the Investment Advisers Act (Rule 206(4)-7) requires registered investment advisors to adopt written policies and procedures reasonably designed to address operational and compliance risks. Vendor relationships that affect client data, trading, reporting, or recordkeeping typically fall within this scope.

The SEC has also emphasized vendor oversight in areas such as cybersecurity, operational resilience, and safeguarding client information. As a result, advisors often include vendor-related controls in their compliance frameworks, such as:

Risk assessments before onboarding a vendor

Reviews of vendor cybersecurity practices

Contract provisions addressing confidentiality and data protection

Ongoing monitoring of vendor performance and security practices

During examinations, the SEC may review documentation showing how vendors were evaluated and approved. A vendor management policy helps advisors document their oversight process and demonstrate that vendor risks are considered within the broader compliance program.

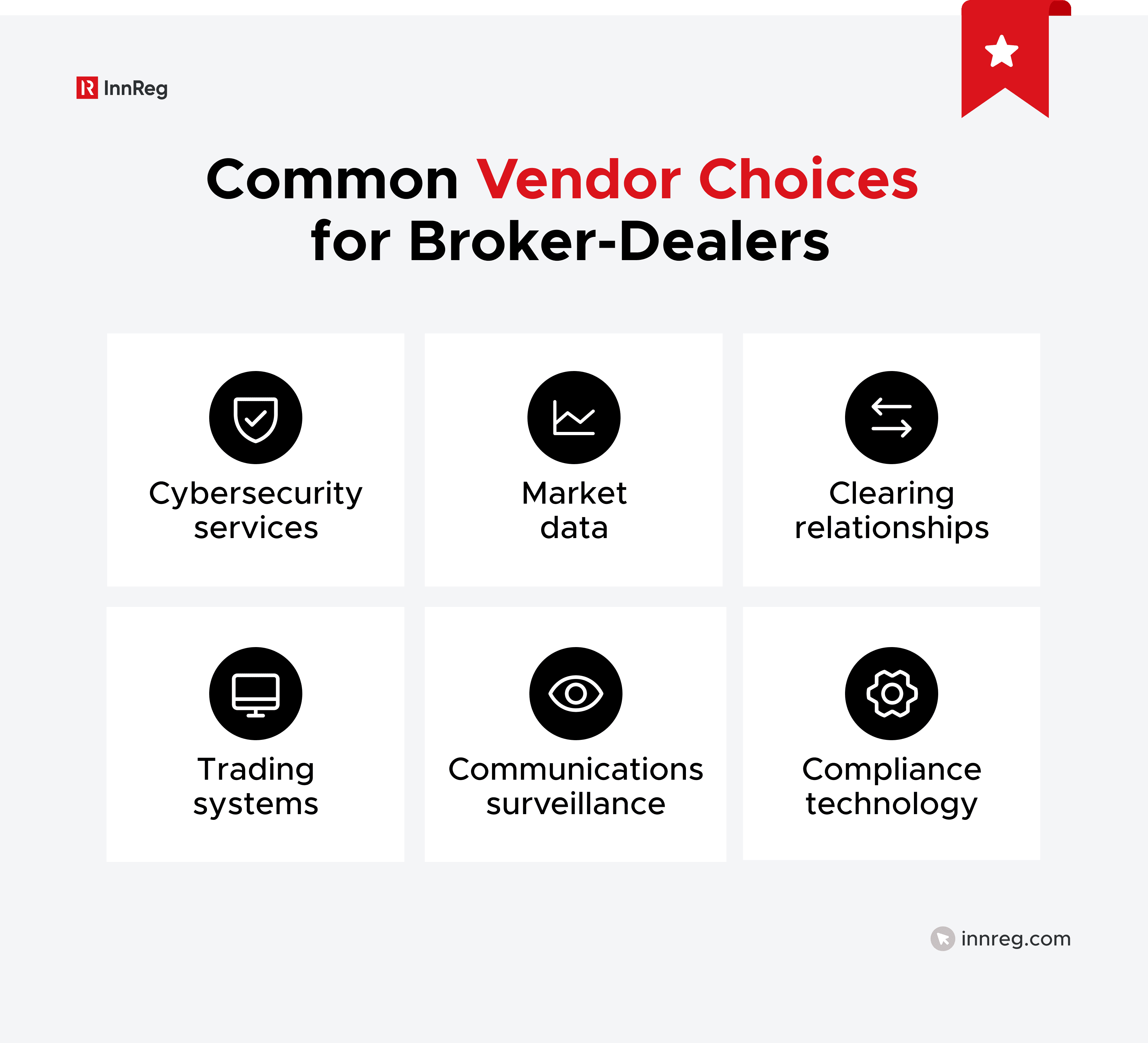

FINRA Requirements for Broker-Dealers

Broker-dealers regularly use vendors for various systems. While these vendors support operational functions, FINRA holds broker-dealers responsible for the supervision of activities tied to their regulatory obligations.

FINRA has repeatedly emphasized that outsourcing does not remove supervisory responsibility. Regulatory Notice 05-48 states that broker-dealers remain responsible for functions performed by third-party service providers, particularly when those functions affect compliance with securities laws or FINRA rules.

As a result, broker-dealers typically incorporate vendor oversight into their supervisory framework. A vendor management policy often connects to the firm’s broader supervisory procedures and risk management processes.

Common vendor oversight practices in broker-dealer environments include:

Pre-engagement vendor due diligence

Risk classification of vendors based on their role in regulated activities

Contract provisions addressing compliance obligations and regulatory access

Ongoing monitoring of vendor performance and security practices

FINRA examinations often review how firms supervise vendors that support trading operations, recordkeeping, cybersecurity, and communications monitoring. Documented vendor oversight processes help demonstrate that third-party relationships are reviewed within the firm’s supervisory structure.

Banking Regulator Guidance on Third-Party Risk

Banking regulators have developed some of the most detailed expectations around vendor oversight. Institutions supervised by the OCC, the Federal Reserve, and the FDIC must follow structured third-party risk management frameworks that cover the entire vendor lifecycle.

In 2023, US banking regulators issued Interagency Guidance on Third-Party Relationships: Risk Management, which consolidates prior expectations into a single framework. The guidance applies to banks and banking organizations, but it has influenced vendor management practices across fintech partnerships and regulated financial firms.

The guidance outlines several stages of vendor oversight that regulators expect institutions to address:

Risk assessment before engaging a vendor

Due diligence and vendor selection

Contract negotiation and risk allocation

Ongoing monitoring and performance review

Termination planning and contingency preparation

While fintech companies are not always directly supervised by banking regulators, many operate through bank partnerships or rely on bank infrastructure. In those situations, bank partners often expect fintechs to follow vendor management practices aligned with banking third-party risk frameworks.

State Regulatory Expectations for Money Transmitters and Fintechs

Money transmitters and other state-licensed fintech companies often rely on vendors for payment processing, transaction monitoring, identity verification, fraud detection, and cloud infrastructure. Even when these functions are outsourced, state regulators still expect licensed entities to maintain oversight of vendors that support regulated activities.

Most state regulators address vendor oversight through money transmission laws, supervisory expectations, and examination procedures.

During examinations, regulators commonly review how firms evaluate vendors that handle customer funds, sensitive data, or transaction processing. A vendor management policy helps demonstrate that the company has a structured process for assessing and monitoring these third-party relationships.

Key Risks a Vendor Management Policy Should Address

A vendor management policy is designed to help regulated companies identify and manage risks introduced by third-party service providers. Vendors often have access to sensitive systems, customer data, and operational infrastructure.

If those vendors experience failures, security incidents, or compliance issues, the regulated firm remains accountable. For that reason, vendor oversight frameworks typically categorize vendor risk across several areas:

See also:

Operational Risk

Operational risk arises when vendor failures disrupt business activities or core systems. This can include outages, processing errors, infrastructure failures, or service interruptions.

Financial firms often depend on vendors for functions such as payment processing, trade execution systems, transaction monitoring platforms, or compliance software. If a critical vendor experiences downtime, the firm’s ability to operate or serve customers may be affected.

Vendor management policies typically address operational risk through:

Vendor risk classification frameworks

Service level expectations in contracts

Performance monitoring and incident reporting

Contingency planning for critical vendors

These controls help firms understand how vendor disruptions could affect daily operations.

Need help with fintech compliance?

Fill out the form below and our experts will get back to you.

Business Continuity Risk

Vendor disruptions can affect a firm’s ability to continue operations during system outages, cyber incidents, or infrastructure failures. Regulators expect firms to consider how vendor dependencies affect business continuity planning.

A vendor management policy typically addresses whether critical vendors maintain business continuity and disaster recovery capabilities. This is particularly important for vendors supporting transaction processing, trading systems, or customer account access.

Firms often review vendor documentation covering disaster recovery infrastructure, backup, and redundancy practices. The documentation should also cover recovery time objectives as well as incident response coordination.

Understanding these capabilities helps firms evaluate how vendor disruptions may affect operational resilience.

Data Security and Cybersecurity Risk

Many vendors process or store sensitive financial information, including customer data, transaction records, and internal systems data. This creates cybersecurity exposure that regulators expect firms to evaluate before onboarding vendors.

A vendor management policy often requires security reviews for vendors that access confidential information or critical systems. These reviews may include security questionnaires, assessments of data handling practices, and reviews of independent security reports.

Common cybersecurity review areas include:

Data encryption practices

Access controls and authentication methods

Incident response procedures

Security certifications or audit reports

Cybersecurity oversight has become a central focus for regulators. Vendors with access to financial data or infrastructure typically receive heightened scrutiny.

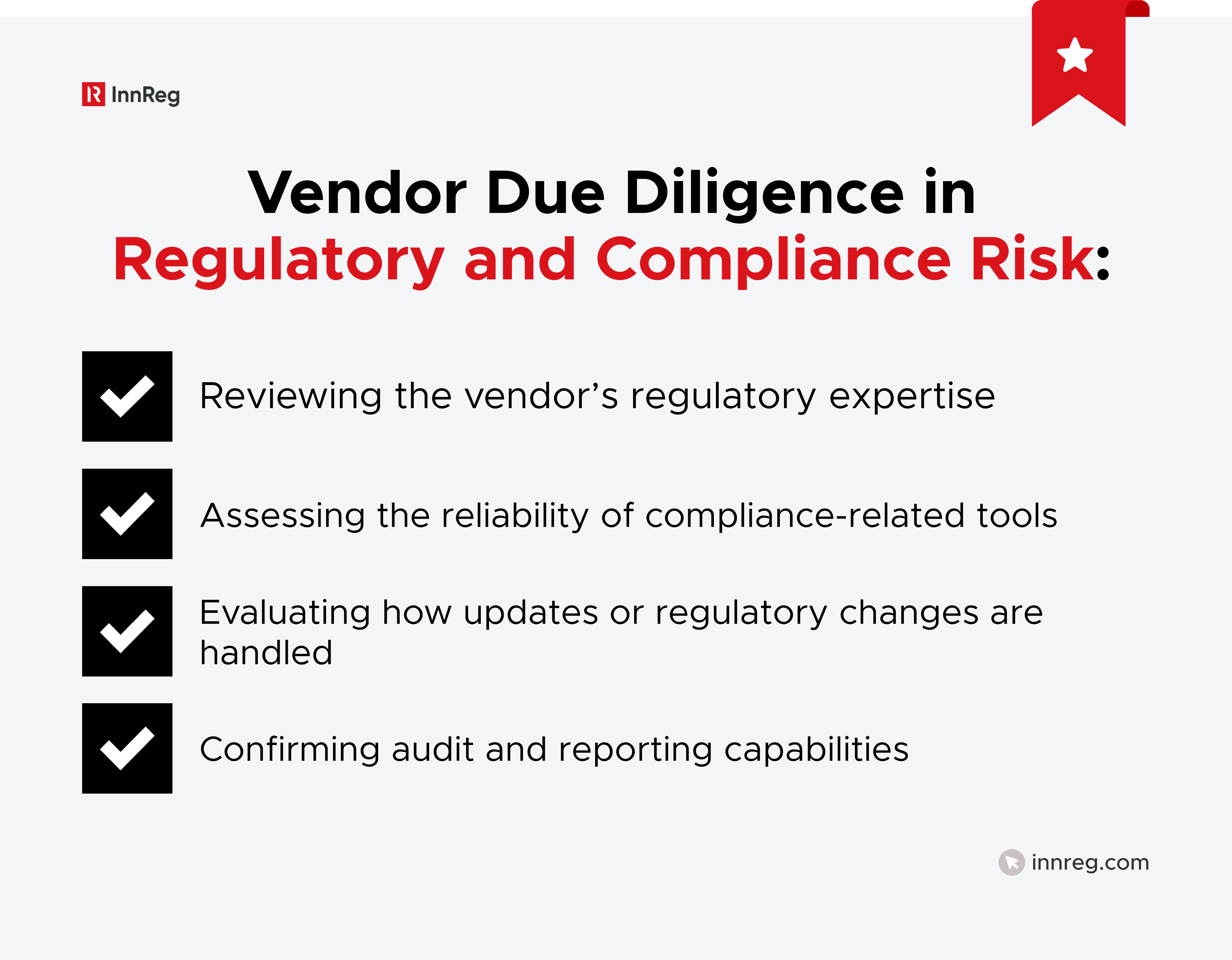

Regulatory and Compliance Risk

Some vendors directly support activities that fall under regulatory requirements. Examples include transaction monitoring systems, communications surveillance tools, regulatory reporting platforms, and compliance software.

If these vendors malfunction or operate incorrectly, the regulated firm may face compliance failures. A vendor management policy helps firms evaluate whether vendors can support regulatory obligations and maintain appropriate controls. These reviews help firms understand whether a vendor’s services align with regulatory expectations.

Concentration and Critical Vendor Risk

Some firms rely heavily on a small number of vendors for essential services. While this can improve efficiency, it also creates concentration risk.

For example, many fintech companies rely on a single cloud infrastructure provider or a single payment processing platform. When a firm depends heavily on one vendor for core operations, disruptions can have widespread operational impact.

Vendor management policies often address concentration risk by:

Identifying critical vendors

Assessing dependency levels across vendors

Evaluating alternative providers or backup systems

Monitoring vendor financial stability and operational resilience

Recognizing concentration risk helps firms understand how vendor dependencies may affect long-term operational stability. Platforms like Regly can help firms map vendor risks across operational, cybersecurity, and compliance domains, making these exposures easier to track and manage.

Core Components of a Vendor Management Policy

A vendor management policy typically defines the governance structure for how a company evaluates, approves, and oversees third-party service providers. Regulators generally expect firms to document these controls clearly and apply them consistently across vendor relationships.

These components help firms document how vendor risks are identified and managed throughout the vendor lifecycle:

Vendor Risk Classification

Not every vendor requires the same level of oversight. A vendor providing internal office tools presents a different risk profile than a vendor handling payments or customer data.

For that reason, vendor management policies typically classify vendors into risk tiers. This classification determines the depth of due diligence and the level of ongoing monitoring required.

Firms often evaluate factors such as:

Whether the vendor accesses customer information

Whether the vendor supports regulated activities

The operational dependency on the vendor

Integration with core systems

A cloud provider hosting customer accounts, for example, would typically fall into a higher-risk tier than a scheduling software vendor.

Vendor Due Diligence

Before onboarding a vendor, firms generally conduct due diligence to understand the vendor’s operations, security practices, and financial stability.

Vendor due diligence allows firms to identify potential risks before entering a contractual relationship. In practice, this often involves collecting documentation, reviewing operational controls, and evaluating the vendor’s ability to support regulated activities.

Typical due diligence reviews examine areas such as operational capabilities, corporate structure, security controls, and independent audit reports. Some firms also review the vendor’s regulatory experience when the service supports compliance-related functions.

Contract and Legal Requirements

Vendor contracts establish the legal structure of the relationship. They allocate responsibilities between the firm and the vendor and define how risks are handled.

Most vendor management policies require certain provisions in vendor agreements. These contract provisions give firms oversight rights and define expectations around confidentiality, performance, and regulatory access.

Contracts supporting regulated services commonly address confidentiality and protection of customer information as well as performance standards and service expectations. Oftentimes, they also address the right to audit vendor activities as necessary.

These terms help clarify how vendor obligations are handled during the relationship.

Information Security and Data Protection Controls

Vendors frequently process sensitive financial information. Because of this, cybersecurity oversight is a central part of vendor risk management.

A vendor management policy often requires security reviews for vendors that access confidential data or critical systems. These reviews help firms understand how vendors manage cybersecurity risk.

Security assessments may evaluate data encryption practices, access management controls, and incident response procedures. Firms may also review independent security certifications or audit reports when they are available.

The goal is to understand how vendor security practices align with the firm’s own risk management framework.

Ongoing Vendor Monitoring

Vendor oversight does not end after the contract is signed. Firms are expected to review vendor performance and risk exposure throughout the relationship.

Ongoing monitoring allows firms to identify changes in vendor risk, operational issues, or emerging security concerns. The depth of monitoring usually depends on the vendor’s risk classification.

Examples of monitoring activities include reviewing vendor performance metrics, requesting updated security documentation, or reassessing vendor risk periodically. Some firms also track vendor incidents and service interruptions over time.

Incident Reporting and Escalation

Vendor-related incidents can affect regulatory compliance, system availability, or customer data protection. For that reason, vendor management policies often define procedures for reporting and escalating vendor issues.

A vendor management policy typically outlines how vendor incidents are reported internally and how the firm responds to operational or security issues involving vendors.

These procedures may address:

Vendor service outages

Security incidents or data breaches

Compliance failures involving vendor services

Communication protocols with internal teams and regulators

Clear escalation procedures help firms respond to vendor issues in a structured and documented manner.

Vendor Termination and Exit Planning

Vendor relationships eventually change. A firm may replace a vendor due to cost, performance issues, or strategic decisions.

For this reason, vendor management policies often include procedures for terminating vendor relationships and transitioning services. Exit planning helps firms avoid operational disruptions and protect sensitive data.

Termination processes may involve revoking system access, transferring data to a new vendor, and documenting how the transition was managed. For critical vendors, firms sometimes maintain contingency plans that allow operations to continue if a vendor relationship ends unexpectedly.

Vendor Due Diligence: What Regulators Expect

Vendor due diligence is one of the most closely reviewed elements of a vendor management policy. Regulators expect firms to evaluate third-party providers before onboarding them, particularly when those vendors support regulated activities or handle sensitive information.

In practice, vendor due diligence helps firms understand the operational, financial, and compliance risks associated with a vendor relationship. The depth of this review usually depends on the vendor’s risk classification and the services being provided.

While approaches vary across firms, regulators generally expect due diligence to cover several core areas:

Pre-Engagement Risk Assessment

Before engaging a vendor, firms typically conduct a risk assessment to determine how the vendor could affect operations, regulatory obligations, and data security.

A pre-engagement risk assessment helps determine whether the vendor should be classified as low, moderate, or high risk. This classification then guides the depth of due diligence required before onboarding.

Factors commonly considered during this stage include:

Whether the vendor handles customer or financial data

Whether the vendor supports regulated activities

Integration with core infrastructure or operational systems

The firm’s dependency on the vendor’s services

This early assessment allows firms to allocate review resources appropriately.

Operational and Financial Review

Operational stability is an important consideration when evaluating vendors that support critical business functions.

Firms often review the vendor’s organizational structure, financial stability, and operational capabilities. Understanding the vendor’s ability to deliver services over time is an important part of vendor risk evaluation.

This review may include evaluating corporate structure, reviewing financial statements when available, and assessing whether the vendor has sufficient personnel and infrastructure to support the service being provided.

For newer fintech vendors, firms may also consider factors such as funding stability or reliance on external infrastructure providers.

Security and Data Protection Assessment

Vendors that access internal systems or customer information require additional security review. Data breaches or cybersecurity failures involving vendors can create regulatory exposure for the regulated firm.

A vendor management policy typically requires security assessments for vendors with access to sensitive data or critical systems. These assessments help firms understand how vendors protect data and manage cybersecurity risks.

Security reviews may include examining:

Data storage and encryption practices

Access control and authentication policies

Incident response procedures

Independent security certifications or audit reports

The depth of these reviews often increases for vendors supporting customer-facing infrastructure.

Regulatory and Compliance Background Checks

Some vendors support functions tied directly to regulatory obligations. Examples include transaction monitoring platforms, communications surveillance systems, regulatory reporting tools, and compliance software.

For these vendors, firms often conduct background checks to evaluate regulatory experience, past enforcement history, or compliance-related issues.

This may involve reviewing public enforcement records, evaluating the vendor’s regulatory expertise, or assessing whether the vendor has experience supporting regulated financial firms.

These reviews help firms understand whether a vendor’s services align with regulatory expectations and industry practices. Many firms use Regly to streamline due diligence workflows, collect vendor documentation, and maintain centralized records for audits.

See also:

Contract Requirements for Vendor Relationships

Vendor contracts define the legal and operational structure of the relationship between a firm and its service providers. For regulated companies, these agreements often include provisions that address compliance obligations, data protection, and operational oversight.

Regulators frequently review vendor contracts during examinations, particularly when vendors support regulated activities or handle sensitive customer information. Here are the contract requirements set by regulatory bodies:

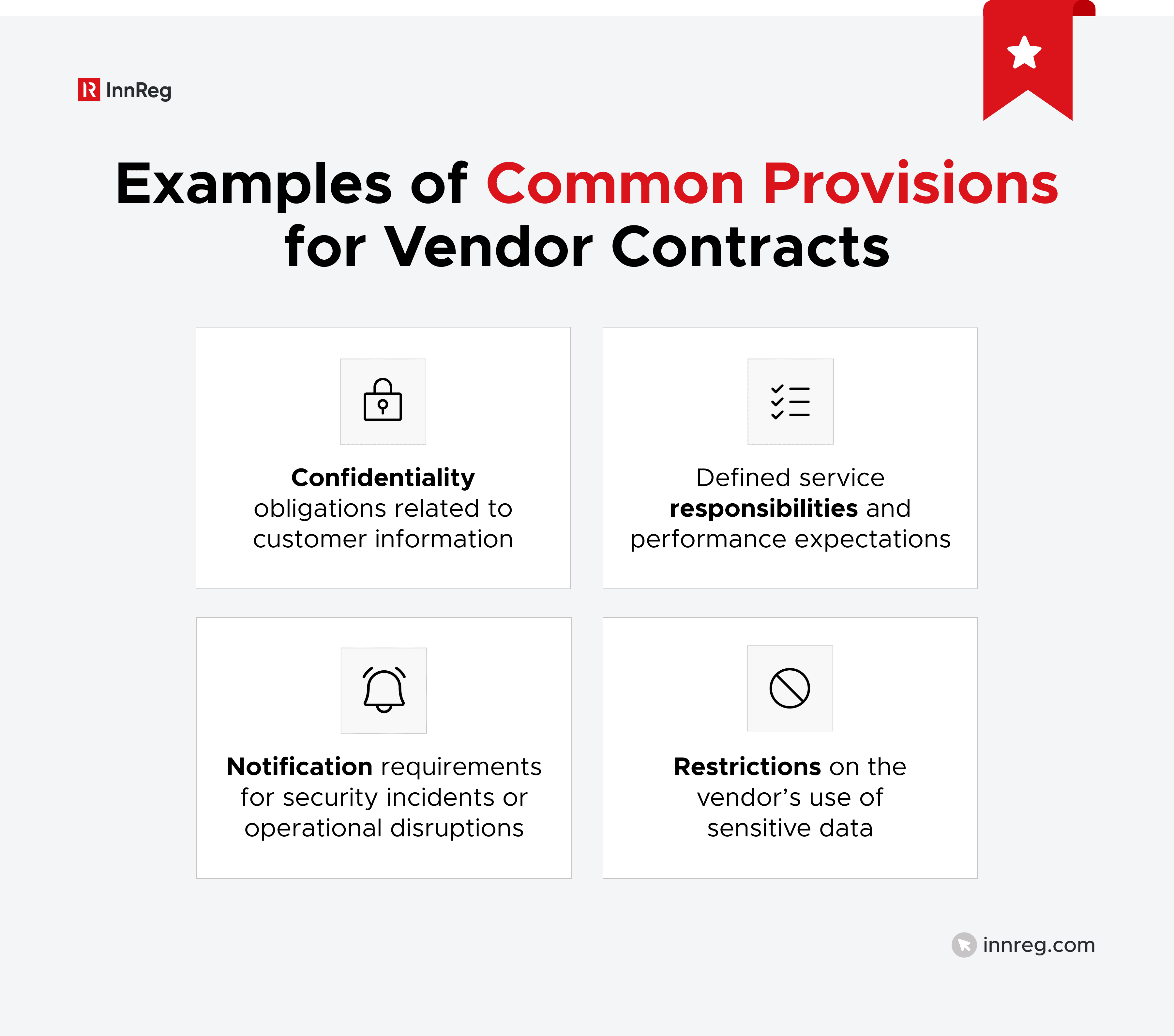

Required Contract Provisions

Vendor agreements often include several baseline provisions that address confidentiality, performance expectations, and operational responsibilities.

While specific language varies across organizations, regulated firms commonly include contractual clauses covering data protection, service obligations, and incident reporting. These provisions help clarify how vendors are expected to operate within the relationship.

Audit Rights and Regulatory Access

Financial regulators may request access to records or information maintained by vendors that support regulated activities. Contracts, therefore, often include provisions allowing firms to review vendor practices when necessary.

Audit rights allow the firm to review vendor controls, documentation, and operational practices when risks or regulatory questions arise.

In some cases, regulators may also require firms to demonstrate that vendors will cooperate with regulatory inquiries. Contract language addressing regulatory access helps support that oversight.

Data Protection and Confidentiality Clauses

Vendors frequently process customer data, financial records, and internal system information. Contracts, therefore, typically contain provisions addressing how that data is handled and protected.

These clauses often define how vendors store, transmit, and protect sensitive information. Data protection provisions help document the vendor’s responsibilities for safeguarding confidential data.

Contracts may also address incident reporting timelines and expectations for responding to security events involving sensitive information.

Subcontractor and Fourth-Party Oversight

Many vendors rely on their own subcontractors or infrastructure providers. Cloud hosting platforms, data processors, and software vendors frequently depend on other service providers behind the scenes.

Because of this, vendor contracts often address how vendors manage subcontractors that support the services being provided.

These provisions may require vendors to disclose critical subcontractors or obtain approval before engaging additional service providers. Firms may also request visibility into how subcontractors handle sensitive data or operational processes.

Addressing subcontractor oversight helps firms understand risks that may arise beyond the immediate vendor relationship.

Ongoing Monitoring of Vendors

Vendor oversight does not end once a contract is signed. Regulators expect firms to monitor vendor performance and risk exposure throughout the lifecycle of the relationship.

The level of monitoring usually depends on the vendor’s risk classification. These are the types of monitoring your firm must engage in:

Performance Monitoring

Performance monitoring refers to evaluating whether a vendor is delivering services according to contractual expectations and operational requirements.

Firms typically track vendor performance using service metrics defined in contracts or service level agreements. Performance monitoring helps identify recurring service issues, outages, or operational disruptions that could affect business activities.

Examples of performance monitoring activities include reviewing system uptime, evaluating support response times, and tracking service reliability. Over time, these reviews help firms determine whether the vendor continues to meet operational expectations.

Compliance Monitoring

Compliance monitoring refers to reviewing whether vendor services continue to support the firm’s regulatory obligations and compliance processes.

Some vendors directly support regulatory functions such as transaction monitoring, communications surveillance, regulatory reporting, or compliance software. Compliance monitoring helps firms identify whether vendor systems continue to function properly within the regulatory framework.

Firms may review vendor updates to compliance features, assess how regulatory changes are implemented within vendor platforms, or document how vendor services support regulatory requirements.

Security and Data Protection Reviews

Security and data protection reviews refer to periodic assessments of how vendors manage cybersecurity risks and protect sensitive information.

Vendors with access to internal systems or customer data can create cybersecurity exposure for regulated firms. Security reviews help firms evaluate whether vendor security practices remain aligned with the firm’s risk management expectations.

These reviews may involve updated security questionnaires, review of security certifications, or evaluation of vendor incident history.

Periodic Vendor Risk Reassessments

Vendor risk reassessments refer to the periodic reevaluation of a vendor’s risk classification as the relationship evolves.

Vendor risk can change over time. A vendor initially classified as moderate risk may become critical as the firm relies more heavily on its services. Periodic reassessments allow firms to update vendor risk classifications and adjust oversight requirements accordingly.

During reassessments, firms may evaluate changes in vendor system access, operational dependency, regulatory exposure, or vendor organizational developments.

Critical and High-Risk Vendors

Not all vendors introduce the same level of risk. Some vendors support core infrastructure, process sensitive financial data, or perform functions tied directly to regulatory obligations. These vendors are typically classified as critical or high risk within a vendor management policy.

A vendor is usually considered critical when its failure could significantly disrupt operations, customer access, or regulatory compliance. High-risk vendors may also require elevated oversight when they have access to sensitive systems or customer data.

Risk classification helps firms determine the level of due diligence, monitoring, and governance applied to each vendor relationship.

Most vendor management frameworks organize vendors into risk tiers based on operational impact, data access, and regulatory exposure:

Vendor Risk Tier | Description | Examples | Typical Oversight Level |

|---|---|---|---|

Critical Vendor | Vendors whose services are essential to business operations or regulated activities | Cloud infrastructure providers, payment processors, CRM systems, clearing firms, trading platforms | Enhanced due diligence, executive oversight, frequent monitoring |

High-Risk Vendor | Vendors with access to sensitive data, financial systems, or regulated processes | KYC providers, transaction monitoring platforms, cybersecurity vendors | Detailed due diligence, periodic security reviews, ongoing performance monitoring |

Moderate-Risk Vendor | Vendors with limited system access or operational impact but still connected to business systems | Analytics platforms, internal compliance tools | Standard due diligence and periodic monitoring |

Low-Risk Vendor | Vendors with minimal access to sensitive data or operational systems | Scheduling tools, office productivity software, internal collaboration tools | Basic onboarding review and limited monitoring |

For fintech companies, vendor concentration often increases risk exposure. Many firms rely on a small number of vendors for cloud infrastructure, payments infrastructure, or compliance systems. Identifying critical vendors early allows firms to prioritize oversight and document how key operational dependencies are managed.

See also:

How to Build a Vendor Management Policy

Building a vendor management policy requires more than documenting vendor relationships. Firms need a structured process for evaluating vendors, assigning risk levels, and monitoring those relationships over time.

Below is a practical framework many regulated firms use when developing a vendor management policy:

Step 1: Define Vendor Risk Tiers

The first step is establishing a vendor risk classification framework. Not all vendors present the same level of operational or regulatory risk, so firms typically group vendors into categories such as critical, high, moderate, or low risk.

Risk tiers determine how much due diligence and monitoring a vendor receives. Vendors supporting regulated activities, handling customer data, or operating core infrastructure typically fall into higher risk tiers.

Step 2: Establish Due Diligence Standards

Once risk tiers are defined, firms typically establish standardized due diligence requirements for each category. Higher-risk vendors usually require deeper operational, financial, and security reviews.

Due diligence standards help create consistency in how vendors are evaluated before onboarding. These reviews may include reviewing security practices, financial stability, operational capabilities, and regulatory experience.

Documenting these standards helps firms demonstrate that vendor relationships are evaluated in a structured way.

Step 3: Implement Vendor Onboarding Procedures

Vendor onboarding procedures define how vendors are approved and integrated into the firm’s operational environment. This process typically includes internal approvals, documentation reviews, and contract validation.

Vendor onboarding procedures connect the vendor management policy to operational workflows. They help ensure that due diligence, risk classification, and contract requirements are completed before a vendor begins providing services.

Some firms also require compliance or risk management review for vendors classified as critical or high risk.

Step 4: Create Monitoring and Review Workflows

Vendor oversight continues after onboarding. Firms typically establish monitoring workflows that track vendor performance, operational reliability, and changes in vendor risk.

Monitoring workflows helps maintain visibility into vendor performance and risk exposure over time. These processes may include periodic vendor reviews, updated security assessments, or performance evaluations.

The frequency of monitoring usually depends on the vendor’s risk tier and the services provided. Firms implementing these steps often rely on platforms like Regly to operationalize vendor management policies and ensure consistency across teams.

Step 5: Document Escalation and Remediation Processes

Even well-managed vendor relationships can experience operational issues, service disruptions, or security incidents. A vendor management policy should define how those situations are handled.

Escalation procedures document how vendor incidents are reported, reviewed, and addressed internally. This often involves coordination between compliance, information security, legal, and operational teams.

Clear escalation procedures also help firms document their response when regulators review vendor oversight practices.

Vendor Management Policy vs. Vendor Management Program

A vendor management policy and a vendor management program serve different purposes within a firm’s compliance framework. The policy defines the governance principles, while the program represents the operational processes used to apply those principles.

A vendor management policy establishes the rules and expectations for vendor oversight. It typically describes risk classification standards, due diligence requirements, monitoring expectations, and escalation procedures.

A vendor management program, on the other hand, refers to the day-to-day implementation of those requirements. The program includes the procedures, workflows, documentation, and internal controls used to manage vendor relationships in practice.

For example, the policy may state that vendors must undergo risk classification and due diligence before onboarding. The program defines how those reviews are conducted, who performs them, and how the results are documented.

Regulators often review both elements during examinations. They may request the written policy as well as evidence showing how vendor oversight processes are actually carried out.

Element | Vendor Management Policy | Vendor Management Program |

|---|---|---|

Purpose | Defines governance principles and oversight expectations | Implements vendor oversight in daily operations |

Content | Policy statements, risk framework, oversight requirements | Procedures, workflows, documentation, monitoring processes |

Scope | High-level governance document | Operational implementation across departments |

Regulatory review | Evaluates whether the firm has documented vendor oversight expectations | Evaluates whether those expectations are applied consistently |

When to Update a Vendor Management Policy

A vendor management policy should evolve as the firm’s operations, vendor ecosystem, and regulatory environment change. Static policies can quickly become outdated, especially for fintech companies that frequently adopt new technologies and infrastructure providers.

Most firms review their vendor management policy periodically to confirm that it reflects current operations and regulatory expectations. Updates may also occur when the firm introduces new products, expands vendor relationships, or changes how vendors support regulated activities.

Several common triggers often lead firms to revise their vendor management policy.

Regulatory Changes

Regulatory expectations around third-party risk management continue to evolve. New guidance, enforcement trends, or examination priorities may require firms to adjust how vendor oversight is documented.

Regulatory changes are one of the most common reasons firms update a vendor management policy. Updates may involve expanding due diligence requirements, adjusting risk classification standards, or documenting new oversight controls.

Firms that operate across multiple regulatory frameworks may review their policy whenever new regulatory guidance affects vendor oversight.

Using AI as a vendor? Read our guide on AI risk management here →

Vendor Incidents or Security Events

Operational disruptions, cybersecurity incidents, or compliance failures involving vendors often prompt policy reviews. These events can highlight gaps in vendor oversight procedures or escalation processes.

When incidents occur, firms often evaluate whether the vendor management policy addressed the risk appropriately. Policy updates may follow incidents that reveal weaknesses in monitoring, escalation, or vendor due diligence.

These reviews help firms refine oversight processes and strengthen vendor risk controls.

Major Operational Changes

Vendor risk profiles often change as companies grow. New products, system integrations, or infrastructure changes can increase reliance on certain vendors or introduce new vendor relationships.

Operational changes may require updates to vendor risk classifications, oversight procedures, or onboarding processes. For example, launching a new fintech product may introduce additional payment processors, identity verification vendors, or cloud infrastructure providers.

Updating the policy helps align vendor oversight practices with the firm’s evolving operations.

Periodic Compliance Reviews

Even without major operational changes, firms often review their vendor management policy on a scheduled basis. Annual or periodic compliance reviews allow firms to confirm that vendor oversight procedures remain current.

These reviews typically evaluate whether vendor risk classifications remain appropriate, whether due diligence standards remain relevant, and whether documentation practices align with regulatory expectations.

Periodic policy reviews help maintain alignment between the written vendor management policy and the firm’s actual vendor oversight practices.

—

Vendor relationships play a central role in modern financial services operations. A vendor management policy provides the framework firms use to evaluate and oversee third-party providers, helping document how operational, security, and regulatory risks are managed.

InnReg works with broker-dealers, RIAs, money transmitters, and fintech companies to build practical compliance programs, including vendor management policies and oversight processes. Our team often operates as an outsourced or embedded compliance function, supporting vendor risk management as part of a broader regulatory obligation.

Alek is a Compliance Consultant at InnReg delivering compliance solutions for fintech clients across broker-dealer, RIA, and money transmitter verticals. He holds FINRA Series 3, 7, and 24 licenses and brings prior experience in operations and compliance at Vest.app, with a strong foundation in financial markets and regulatory execution.

How Can InnReg Help?

InnReg is a global regulatory compliance and operations consulting team serving financial services companies since 2013.

We are especially effective at launching and scaling fintechs with innovative compliance strategies and delivering cost-effective managed services, assisted by proprietary regtech solutions.

If you need help with compliance, reach out to our regulatory experts today:

Related Articles

Featured LinkedIn Posts