Crypto Innovation: Top 10 Crypto Business Models in 2026

Crypto innovation is moving into a new phase. The era of copying exchanges and launching meme tokens is over. In 2026, the crypto business models gaining traction are those with real economic infrastructure, strong compliance foundations, and clearer regulatory touchpoints.

This article outlines ten of the most innovative crypto business models shaping the current landscape. These aren’t recycled ideas with a new coat of branding. Each one reflects a shift in how blockchain is being used across financial services, infrastructure, and consumer products.

For fintech founders, compliance teams, and legal advisors, understanding how these models work is now core to building anything sustainable in crypto. Ready to find out more? Keep reading.

At InnReg, we help crypto and fintech companies navigate complex compliance challenges. Whether you're launching a new tokenized model, building compliance-native infrastructure, or integrating DeFi features, our team supports you from registration to daily program management. Contact us to explore how InnReg can support your growth.

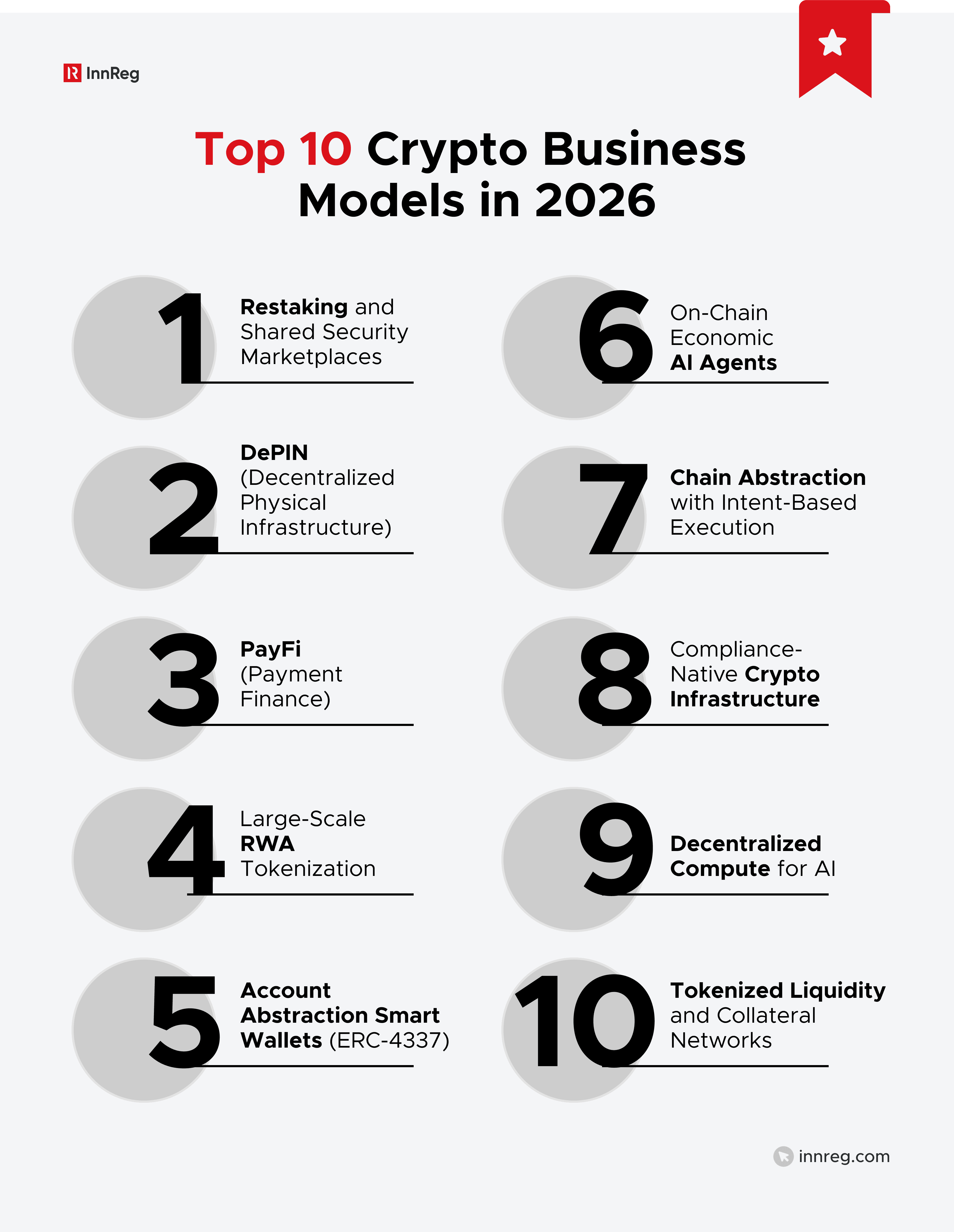

Top 10 Innovative Crypto Business Models in 2026

The models listed below reflect where crypto is actually being used to solve complex problems in infrastructure, finance, and coordination. Some are already in production, while others are still evolving, but gaining traction fast. Each section highlights how the model works, where revenue is generated, and what compliance teams should watch for:

1. Restaking and Shared Security Marketplaces

Restaking is one of the most important developments in crypto infrastructure since proof-of-stake went mainstream. It allows staked assets like ETH to be reused as economic security for other protocols.

Instead of bootstrapping their own validator set, new networks can tap into Ethereum’s validator base through a shared security marketplace. The most prominent implementation to date is EigenLayer, which has grown significantly since its mainnet phases rolled out in 2023-2024.

By 2026, this has become the practical default for protocols that need security without the overhead of creating it. Rollups, oracles, bridges, and other Actively Validated Services (AVSs) publish what they need and what they'll penalize, and validators opt in on their own terms. The whole model functions as an open market for crypto-native security, one that didn't really exist in this form just a few years ago.

The appeal is clear: protocols get instant security. Validators get new revenue streams. But adoption is still early-stage, especially outside of Ethereum. Many networks and operators are watching carefully before they commit.

Operator/Validator Economics and Risks

Validators that opt into restaking agreements take on a broader set of responsibilities and liabilities. Here are some of the economics and risks surrounding this business model:

Validator revenue comes from multiple layers: staking yield from Ethereum, plus AVS-specific payments or incentives. Some AVSs pay in their native token, others in ETH.

Each AVS has its own slashing terms and uptime rules, enforced through smart contracts. There’s no global standard yet, which makes participation highly manual.

Operators have to track obligations across services: missed uptime or performance failures on one AVS don’t affect Ethereum staking, but they can still result in meaningful penalties or reputational damage.

Interoperability tooling remains underdeveloped: while platforms like EigenLayer offer basic monitoring, validators often build custom systems to manage multiple AVS relationships.

Institutional adoption is slow but inevitable: regulated custodians and infrastructure providers are exploring restaking, but won’t scale participation without formal SLA frameworks and auditability.

Regulatory treatment depends on packaging: running a validator and restaking into AVSs is not inherently regulated, but platforms that pool funds, abstract control, or advertise yields to passive users may cross into securities territory in the US.

Restaking is a market primitive for programmable trust. As SLAs become standardized and validator tooling matures, expect this model to move from early adopters to institutional infrastructure.

Learn about tokenized securities and the regulations surrounding them here →

2. DePIN

Decentralized Physical Infrastructure Networks (DePIN) use token incentives to build real-world infrastructure without relying on centralized providers. Participants contribute resources like compute, bandwidth, storage, or energy, and earn tokens in return.

What started with Helium’s wireless hotspots has evolved into a broad category covering decentralized GPU networks, mobility systems, satellite relays, and more.

By the end of 2026, DePIN is expected to become one of the most active frontiers in crypto innovation. Protocols use tokens to incentivize supply, while building two-sided marketplaces for usage. The promise is that anyone can help power a network and get paid for it. But these models also introduce challenges around supply quality, economic stability, and compliance, especially as they scale across borders.

Revenue Models vs. Token Incentives

DePIN protocols are experimenting with different economic structures to drive both supply and demand. Here's how the most common ones break down:

Aspect | Token Incentives | Usage-Based Revenue |

|---|---|---|

Incentive Structure | Participants earn tokens for delivering services | Participants paid for the actual consumption of services |

Revenue Source | Primarily from protocol inflation or emissions | From user payments in stablecoins or native tokens |

Timing of Rewards | Often front-loaded to attract early adopters | Earned based on verifiable usage or delivery |

Sustainability Risk | High, if demand fails to scale | Lower, if demand grows with protocol adoption |

Enterprise Integration | Still evolving; limited; often lacks service-level guarantees | Generally more established, but varies depending on service reliability and verification mechanisms |

Performance Challenges | Unreliable node participation and uptime variability | Requires reliable nodes and robust verification |

Compliance Exposure | Varies by token design, governance, and jurisdiction; can trigger securities, tax, or sector-specific regulation | Also jurisdiction-dependent; regulatory treatment depends on service type and how payments are structured |

Jurisdictional Risk | Nodes may unknowingly violate local regulations | Must account for data localization and export laws |

DePINs are redefining who can build and monetize infrastructure. But to move past crypto-native circles and attract real-world demand, they’ll need stronger guarantees on performance, governance, and legal clarity. That’s where the next evolution of this model will likely play out.

3. PayFi (Payment Finance)

Short for Payment Finance, PayFi is an emerging crypto innovation that combines real-time settlement with programmable payment logic. It builds on stablecoin rails and account abstraction to enable:

Conditional payments

Streaming transfers

Smart contract-based treasury operations.

While traditional crypto payments focused on speed and borderlessness, PayFi models add automation, logic, and integration with backend financial workflows.

By 2026, PayFi is gaining traction in areas like B2B payments, DAO treasury management, employee payroll, and cross-border vendor relationships. Instead of sending lump sums, payments can be streamed by the second, unlocked on delivery, or paused on dispute, natively on-chain.

Startups like Superfluid, Sablier, and LlamaPay helped pioneer these models. More recent players are focusing on integrating compliance logic, audit trails, and ERP system hooks.

What makes PayFi compelling isn’t just speed. It’s the ability to wrap payments in policy: multi-sig approval flows, whitelisting, dynamic rate adjustments, or rule-based routing, all of which reduce friction in high-volume environments.

Difference Between PayFi and Traditional Crypto Payments

While both use blockchain for settlement, PayFi introduces more structure, predictability, and compliance readiness. Here’s how they compare:

Aspect | Traditional Crypto Payments | PayFi (Payment Finance) |

|---|---|---|

Payment Method | One-time, manual transfers | Streaming, conditional, or rule-based payments |

Core Use Case | Peer-to-peer or merchant payments | Payroll, treasury ops, B2B disbursement, DAO budgeting |

Settlement Speed | Fast, but requires full execution per transaction | Continuous or event-triggered settlement |

Compliance Integration | Generally limited | Increasing support for allowlists, AML checks, and auditability |

Automation Features | Minimal; relies on off-chain tools | Built-in logic for approvals, delays, rules, and dispute resolution |

Risk Management | Sender bears execution risk | Programmable fail-safes and staged execution reduce error exposure |

As PayFi matures, compliance teams will need to consider how programmable payments intersect with financial controls. Treasury flows governed by smart contracts are auditable but still exposed to bugs, improper logic, or access mismanagement.

For startups moving funds programmatically, strong internal policy and code review become part of the financial function itself.

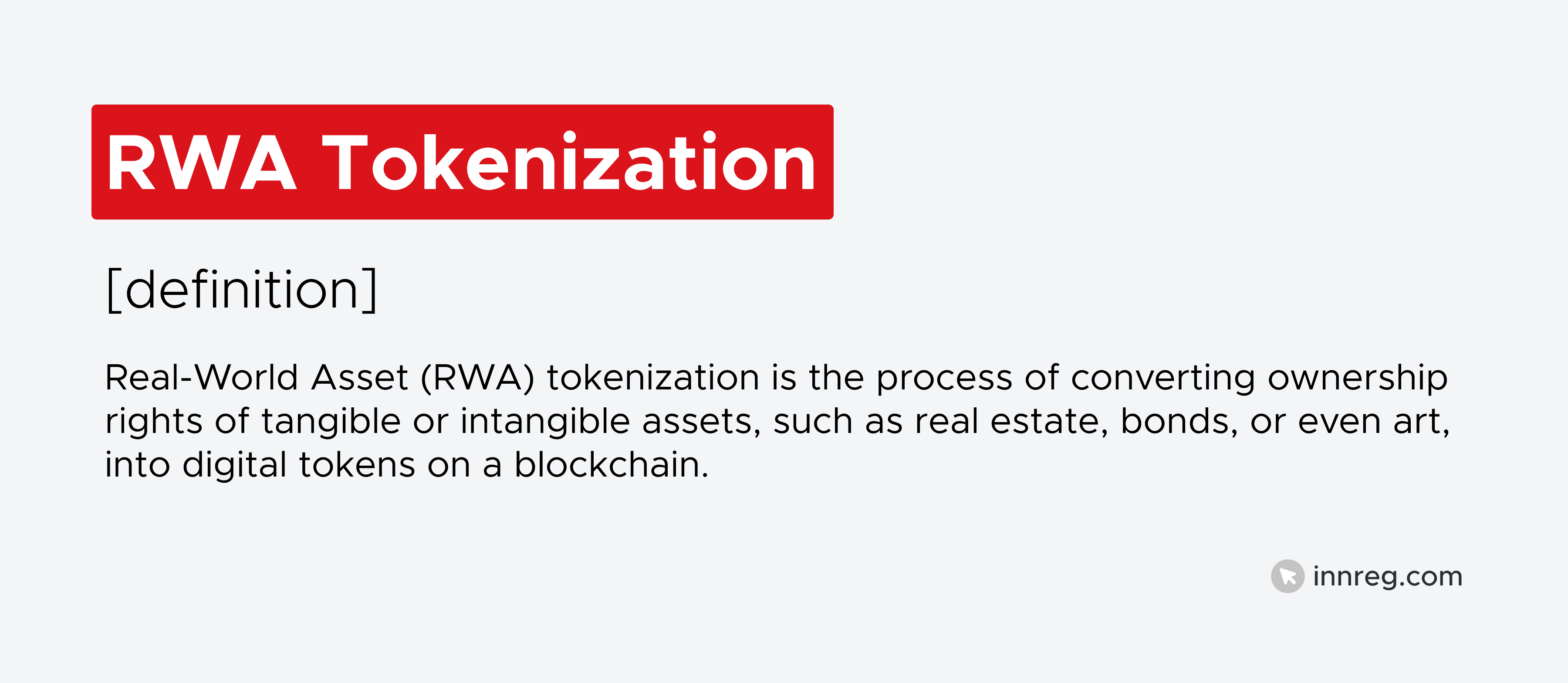

4. Large-Scale RWA Tokenization

Tokenized real-world assets (RWAs) are not a new idea, but the scale and structure of implementation are changing in 2026. What began with experimentation around stablecoins and tokenized treasuries has evolved into a broader ecosystem of on-chain financial instruments. These include real estate, private credit, trade finance, carbon credits, and more.

The shift is focused on building a regulated, interoperable infrastructure that can support:

Institutional flows

Cross-border settlement

Composable financial products

Leaders in this space have moved beyond pilot phases into real capital deployment. What’s different now is who’s participating. Banks, sovereign funds, and asset managers are actively exploring RWA tokenization for its efficiency gains, transparency, and access benefits. Many projects now operate under regulatory frameworks, often through special-purpose vehicles or partnerships with qualified custodians.

Tokenized RWAs are also being used as collateral in DeFi markets, offering new pathways for liquidity. However, integration with decentralized protocols introduces friction, especially around identity verification, redemption rights, and default resolution.

Before RWA tokenization can scale globally, a few persistent issues still need solving:

Fragmented legal frameworks: Asset tokenization interacts with securities law, property rights, and investor protection regimes, which differ significantly across jurisdictions.

Custody and control: Most tokenized RWAs rely on off-chain legal structures. This introduces central points of failure and limits the benefits of decentralization.

Interoperability across blockchains: Assets tokenized on private or permissioned chains often struggle to interact with DeFi or public infrastructure.

Standardization of metadata and asset registries: Without unified standards, secondary markets remain thin, and valuation is inconsistent.

Compliance boundaries for DeFi migration: Lending against tokenized RWAs often requires KYC, AML, and off-chain verification, raising questions about protocol-level enforcement and liability.

Despite these constraints, the momentum is real. Large-scale tokenization is where TradFi meets crypto infrastructure, and it’s moving faster now that major institutions are committed.

5. Account Abstraction Smart Wallets (ERC-4337)

For most people, crypto wallets have always worked the same way: one private key, one signing method, no flexibility. Account abstraction, formalized through Ethereum's ERC-4337 standard, breaks that mold. Smart wallets can now define their own rules for how transactions get approved and executed, which opens up features that would have been impossible with a traditional wallet: session keys, batched transactions, sponsored gas fees, and recovery options that don't depend on a single seed phrase.

By the end of 2026, account abstraction is expected to become a critical design layer for user experience and security. Fintechs, wallets, and DeFi apps are leveraging smart accounts to remove friction from onboarding, improve compliance workflows, and reduce user error. The shift is especially impactful for institutions and regulated platforms, where access control and auditability matter.

Under the hood, bundlers and paymasters handle the heavy lifting — relaying user operations and covering gas fees, while the smart wallet itself defines how transactions get authorized. That separation has opened the door to things like gasless onboarding for new users and custom approval flows for DAO treasuries.

Limitations of Current ERC-4337 Implementations

Despite its promise, ERC-4337 is still in the early innings of adoption. Several technical and operational issues are limiting its reach:

Bundler decentralization is still evolving: Most apps rely on centralized or semi-centralized bundlers to relay user operations, which raises censorship and availability concerns.

Paymaster funding models are fragile: Projects often sponsor user gas costs, but these models can become unsustainable at scale without usage-based monetization.

Tooling remains fragmented: Developers face inconsistent support across SDKs, chains, and frameworks, making integrations time-consuming.

Multi-chain coordination is immature: Smart accounts are often siloed to a single network, limiting portability across L2s or alternative ecosystems.

Audit complexity is higher: More logic in the wallet means more risk of smart contract bugs, especially in recovery or authorization modules.

Compliance integration is early: While smart wallets could enforce whitelisting or transaction limits, few implementations offer standardized hooks for compliance teams yet.

Smart accounts will likely become the default for retail and institutional crypto users. But to get there, the infrastructure layer needs to become more robust, auditable, and standardized.

6. On-Chain Economic AI Agents

Think of on-chain AI agents as software that can actually do things with money. They hold crypto assets, execute transactions, and interact with protocols independently, no human in the loop required. The underlying logic comes from large language models, but they operate through smart contracts, which is what allows them to take real economic action on-chain:

Market-making

Yield strategy execution

Governance participation

Supply chain coordination

In 2026, on-chain agents are starting to feel less like experiments and more like something you can actually put to work. The big change is autonomy. These agents are no longer just running through rigid scripts. They can adjust as conditions shift, pull in outside data when needed, and make decisions based on the goals they’ve been given.

Projects like Olas have helped define what this category looks like, supported by a growing layer of infrastructure that makes it possible to run inference on-chain, tap into decentralized storage, and build agents in modular pieces.

You can already see where this is going in the real world. Teams are using these agents to rebalance DeFi portfolios, help run DAO operations, explore new ways to handle on-chain credit scoring, and even smooth out how payments and settlements move through logistics systems.

However, a few limitations are still holding back broader adoption:

Lack of formal verification: Many agents operate on probabilistic logic or opaque LLM calls, which makes outcomes harder to predict and test.

Latency and reliability: On-chain agents often rely on off-chain inference or oracle data feeds, which can fail or be manipulated.

Capital custody risks: Giving agents access to real capital creates serious operational risks if permissions or triggers are misconfigured.

Legal status is undefined: In most jurisdictions, agents have no legal personality, making dispute resolution or claims enforcement unclear.

Oversight complexity: Auditing autonomous decision paths is difficult, especially when agents evolve or retrain based on new inputs.

Despite these hurdles, agent-based infrastructure has the potential to change how crypto protocols interact with markets and users. For fintech teams, this model defines how responsibility, logic, and control will evolve in programmable finance.

See also:

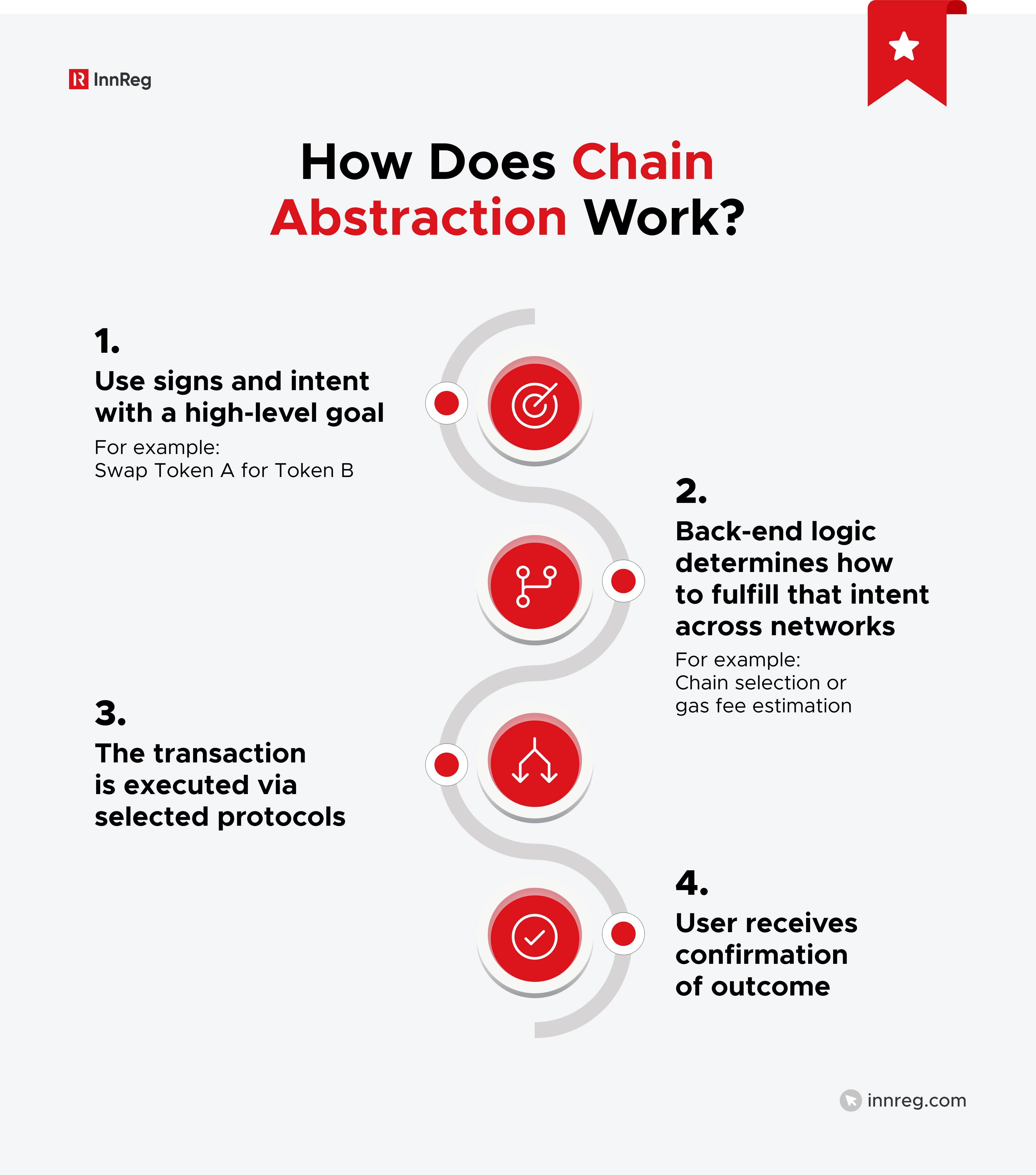

7. Chain Abstraction with Intent-Based Execution

Chain abstraction starts with a simple frustration: why should a user have to know which blockchain they're on to get something done? In 2026, that question is driving real product decisions. Intent-based architectures are emerging as the practical answer, where users sign off on what they want to accomplish and the system handles the rest, picking the right chain, finding the best route, and settling the transaction without asking the user to manage any of it.

In practice, this means a user can authorize something like a swap or a collateral post without touching an RPC* setting or a bridge interface. The system routes the transaction wherever it needs to go, whether that's a rollup, a shared sequencer, or an appchain.

Anoma, Essential, and Stack are among the projects developing this model, with infrastructure providers also building out the unified execution layers and cross-chain mempools that make it work. What's changing isn't just the technology; it's what users actually have to think about.

For developers, this introduces composability across ecosystems. For compliance teams, it raises visibility questions: when transactions abstract across chains, where do controls apply?

As intent-based execution gains adoption, here’s where the complexities show up:

Settlement geography becomes opaque: When a transaction hops through multiple networks, it’s not always clear where legal or tax obligations are triggered.

Transaction traceability weakens: Monitoring activity across abstracted chains requires tooling that’s still in early stages.

Compliance boundaries blur: If an intent spans chains with different compliance requirements, determining where enforcement applies becomes non-trivial.

Protocol-layer risks emerge: Bundlers and solvers who fulfill intents become critical infrastructure, with their own trust assumptions and potential for manipulation.

Abstraction can mask user intent: While UX improves, abstraction also hides complexity that compliance officers may still need to see.

Chain abstraction has the potential to shift how crypto infrastructure organizes execution. For fintech teams building across ecosystems, this model demands a new approach to observability, audit, and control logic. The opportunity is real, but so are the oversight gaps.

Note: RPC (Remote Procedure Call) refers to the endpoints (nodes) that wallets and applications use to communicate with a blockchain.

Need help with fintech compliance?

Fill out the form below and our experts will get back to you.

8. Compliance-Native Crypto Infrastructure

As regulatory expectations sharpen across jurisdictions, crypto infrastructure is evolving to meet the moment. In 2026, a new category is taking shape: compliance-native infrastructure. These are chains, protocols, and tooling stacks that embed regulatory features like KYC, transaction filtering, and jurisdictional logic at the protocol or service layer.

Unlike retrofitting compliance into general-purpose chains, these solutions are designed from the ground up to support regulated financial activity. This includes tokenized securities issuance, permissioned DeFi, stablecoin rails, and identity-anchored transactions.

Examples include networks like Provenance and Concordium, off-chain compliance and analytics tools like Chainalysis’ KYT engines, and emerging zk-based privacy filters that aim to enable selective disclosure for auditors without exposing user-level data to the public.

This is especially relevant for fintechs that operate in gray zones where the line between self-custody, investment advice, and money transmission isn’t always clear. Compliance-native tooling reduces ambiguity and increases auditability, both of which are crucial when dealing with regulators or banking partners.

Here is how to decide where compliance-native models might excel or otherwise:

Compliance-Native Models Are A | |

|---|---|

Strong Fit For… | Weak Fit For… |

Regulated stablecoins and payment platforms | Fully decentralized, permissionless ecosystems |

RWA tokenization with investor onboarding | Anonymity-first protocols and zk-native networks |

Permissioned DeFi protocols (lending, AMMs, treasuries) | Applications that rely on composability across chains with mismatched compliance standards |

Broker-dealer infrastructure or digital asset securities | |

Compliance-native infrastructure doesn’t remove regulatory risk. But it does offer a practical framework for fintech teams building in high-touch environments. Instead of debating gray areas, these tools are designed to document, restrict, and prove control before regulators ask. For startups looking to scale without outgrowing their legal foundations, this is a shift worth watching.

Stablecoin regulation is a complicated landscape in 2026. Read more about it here →

9. Decentralized compute for AI

As AI workloads get heavier and more data-hungry, traditional centralized compute is starting to feel like a choke point. In 2026, decentralized compute networks are stepping in as an alternative, letting teams tap into GPU power on demand through blockchain-based marketplaces.

These networks allow developers to rent compute cycles from independent node operators running hardware across the globe. In return, operators earn crypto rewards or usage fees. The model is similar to how Filecoin incentivizes storage, but applied to model training, inference, and fine-tuning tasks.

Key players like Render and Akash are advancing this space, alongside AI-native blockchain projects experimenting with on-chain agent coordination and verifiable inference proofs. For crypto innovation, decentralized compute creates a technical foundation for scalable, censorship-resistant AI services.

It also introduces opportunities for fintechs. AI-driven compliance monitoring, fraud detection, and risk modeling require significant processing power. Running these functions on decentralized networks opens a path to potential cost efficiencies and verifiable independence, especially in regulated industries wary of single points of failure.

Yet, like every business model on this list, decentralized computer networks have their own constraints and implications:

Proof of performance is still fragile: Verifying that compute was performed honestly is an open challenge, especially for training tasks with no deterministic output.

Data localization requirements conflict with global node distribution: Some AI applications require data residency compliance, which decentralized networks may not easily support.

Operator identification and vetting are weak: Most compute providers are pseudonymous, creating KYC and sanctions risks if used in financial workflows.

Service reliability varies: Unlike centralized cloud providers, uptime and SLA guarantees are inconsistent across decentralized compute networks.

Legal classification is uncertain: Running regulated workloads on unvetted, decentralized infrastructure may trigger vendor due diligence requirements under banking or financial compliance rules.

Still, the growth of decentralized compute reflects a broader push to unbundle infrastructure from corporate control. For fintechs building AI-powered services, it may offer new levers if wrapped in the right governance and compliance layers.

Interested in knowing more about upcoming fintech trends this year? Click here to read more →

10. Tokenized Liquidity and Collateral Networks

Crypto’s liquidity layer is starting to take on a new shape. In 2026, a wave of tokenized liquidity and collateral networks is emerging, focused on making it easier to move, reuse, and deploy assets across protocols. Instead of sitting idle, liquidity is being treated more like programmable infrastructure that can be actively managed and put to work.

Rather than holding assets in siloed wallets or vaults, users deposit collateral into shared networks that expose it to multiple protocols simultaneously. Liquidity becomes modular, dynamic, and rentable. These systems use smart contracts to track who has rights to what, and under what conditions.

Projects like Gravitaare are pioneering frameworks for composable collateral markets, meta-liquidity routing, and credit delegation. Institutional players are also experimenting with tokenized repo markets and tri-party settlement using crypto-native rails.

The result is a more capital-efficient ecosystem. But it also introduces complexity, especially when collateral is tokenized, fractionalized, or pledged to multiple venues at once.

Liquidity vs. Collateral Models

Model | Core Function | Compliance Friction Points |

|---|---|---|

Traditional Lending Pools | Isolated deposits against protocol-specific terms | Clear ownership but limited capital reuse |

Shared Collateral Networks | Multi-protocol collateral allocation | Requires collateral tracking, enforceable slashing, and auditability |

Liquidity Renting / Leasing | Temporary access to idle capital | May trigger lending/licensing scrutiny depending on user profile |

Tokenized Repo and Credit Lines | On-chain replication of institutional structures | Complex legal structuring, especially with non-retail participants |

These models blur the lines between DeFi and structured finance. For compliance teams, the challenge is establishing enforceable claims, verifying counterparties, and preventing unintended exposure, especially when multiple platforms touch the same collateral.

Fintechs building in this space should treat liquidity as infrastructure, not just a financial feature. The more modular the system, the more important it is to have control logic, observability, and legal clarity built in from day one.

Comparing Business Models

Each of these crypto innovations brings its own tradeoffs. Some push the boundaries of compliance. Others rethink user experience, infrastructure design, or capital efficiency. To help fintech teams and advisors assess where to focus, here’s a comparative overview of the top 10 business models covered:

Model | Key Risks | Operational Complexity | Compliance Scope |

|---|---|---|---|

Restaking & Shared Security | Slashing penalties, validator liability across services | Medium-High | Moderate: Depends on packaging; passive staking may trigger scrutiny |

DePIN | Token inflation, low utilization, over-incentivization | High | Low–Moderate: Use case-dependent; telecom and data sectors may apply |

PayFi (Payment Finance) | Smart contract bugs, access mismanagement | Medium | Moderate–High: Tied to treasury, payroll, and disbursement compliance |

Large-scale RWA Tokenization | Legal enforceability, redemption risk, and custodial failure | High | High: Securities law, KYC/AML, cross-border restrictions |

Account Abstraction (ERC-4337) | Smart wallet bugs, bundler trust issues | Medium | Moderate: Limited today, but can support strong compliance controls |

Onchain Economic AI Agents | Unpredictable behavior, unclear accountability | High | Unclear: Legal personality and liability unresolved |

Chain Abstraction | Settlement opacity, solver manipulation, and fragmented observability | High | Moderate–High: Difficult to pin down the jurisdiction and enforcement point |

Compliance-Native Infrastructure | Over-restriction, limited interoperability | Medium | High: Purpose-built for KYC, filtering, and legal logic |

Decentralized Compute for AI | Inference manipulation, pseudonymous operators | High | Moderate–High: Varies by workload; may trigger vendor risk assessments |

Tokenized Liquidity Networks | Collateral misuse, rights conflict across venues | High | High: Lending, rehypothecation, and counterparty verification required |

There’s no one-size-fits-all model. The right direction depends on the product, risk appetite, jurisdiction, and user base.

For fintech founders and compliance teams navigating these models, it’s no longer just about what’s technically possible. It’s about what’s operationally defensible, regulatorily viable, and strategically aligned. That’s where business model design and compliance architecture converge.

—

Navigating the crypto innovation frontier requires more than technical execution. Each of these models introduces new compliance, licensing, and oversight challenges, often in gray zones that demand expert interpretation and structured controls. That’s where compliance becomes a business advantage.

At InnReg, we help innovative fintechs and crypto platforms build and operate compliant business models. From registration and licensing to end-to-end compliance program management, our team acts as an extension of yours.

Whether you're launching a tokenized platform or integrating smart wallets, we bring niche expertise and proven systems to help you scale responsibly. Got an innovative business model without regulatory clarity? Reach out to our experts today!

Adriana is a Principal Consultant at InnReg with 8 years of compliance experience specializing in VASP licensing and regulatory frameworks across Europe and LATAM. She has held senior compliance roles at leading global crypto and financial institutions, including Gate.io, Binance, Santander Bank, and BNP Paribas, with deep expertise in KYC/AML operations, MiCA adaptation, and building compliance programs from the ground up.

How Can InnReg Help?

InnReg is a global regulatory compliance and operations consulting team serving financial services companies since 2013.

We are especially effective at launching and scaling fintechs with innovative compliance strategies and delivering cost-effective managed services, assisted by proprietary regtech solutions.

If you need help with compliance, reach out to our regulatory experts today:

Related Articles

Featured LinkedIn Posts