FINRA AWC: Letter of Acceptance, Waiver and Consent

A FINRA acceptance, waiver, and consent letter, often called an AWC, is one of the most common ways FINRA resolves enforcement matters. It’s also one of the moments where firms and individuals must carefully evaluate the alleged violations, potential consequences, and whether the proposed resolution aligns with their regulatory and business considerations.

For fintech founders, compliance officers, and legal teams, an AWC can raise immediate questions. What does it actually mean to sign one? Why did FINRA choose this path? And what does it signal about regulatory expectations going forward? Understanding the purpose and structure of an AWC is the first step to responding thoughtfully rather than reactively.

In this article, we'll explain what a FINRA letter of acceptance, waiver, and consent is and why it carries weight for regulated firms. We'll also share context to help compliance teams and business leaders better understand how AWCs are viewed by regulators.

At InnReg, we help FINRA-registered firms navigate enforcement risk and regulatory complexity. Contact InnReg to learn more about our compliance consulting and outsourcing services.

What Is a FINRA AWC (Letter of Acceptance, Waiver, and Consent)?

A FINRA acceptance, waiver, and consent letter, commonly called an AWC, is a settlement agreement between FINRA and a firm or registered individual. It allows resolution of an enforcement matter without going through a full disciplinary hearing.

When a firm or individual signs an AWC, they’re accepting FINRA’s version of what happened and agreeing to the proposed sanctions. They don’t have to admit or deny the alleged violations, but they do give up the right to challenge the findings or appeal the outcome. Once executed, the agreement is final and binding.

AWCs are widely used across broker-dealers, fintech platforms, and other regulated firms because they offer a faster and more predictable path to resolution.

However, speed does not mean low impact. An AWC becomes part of the public regulatory record and can carry long-term consequences, from disclosure obligations to future exam scrutiny. Understanding those implications is critical before agreeing to the terms.

When and Why Does FINRA Issue an AWC?

FINRA issues an acceptance, waiver, and consent when it believes an enforcement response is appropriate and a negotiated resolution makes sense. These letters typically follow exams or investigations in which FINRA identifies conduct it views as inconsistent with securities rules.

Instead of moving forward with a formal disciplinary hearing, FINRA may offer an AWC as a way to wrap things up more efficiently. This approach allows the regulator to address compliance concerns and impose sanctions without prolonged litigation. For firms, it often reduces uncertainty and shortens the timeline of what’s already a disruptive process.

AWCs also offer insight into FINRA’s enforcement priorities. They highlight where the regulator is focusing its attention and how its rules are being interpreted in real-world situations. For regulated firms and individuals, understanding why an AWC was issued can be just as important as understanding the penalties that follow.

Key Components of an Acceptance, Waiver, and Consent Letter

A FINRA acceptance, waiver, and consent letter follows a consistent structure. While the facts and penalties vary, the core sections are largely the same across enforcement actions. Each component serves a specific regulatory purpose and carries its own implications.

Here are the main sections of an AWC:

Component | What It Covers |

|---|---|

Findings | FINRA’s description of the conduct it believes violated its rules |

Sanctions | The penalties imposed to resolve the matter |

Waivers and Consents | The rights given up to settle the enforcement action |

Findings

The findings section is where FINRA lays out the conduct it believes is inconsistent with its rules. It describes what FINRA believes happened, when it happened, and which rules it thinks were violated.

This section is written in plain regulatory language, but it carries real weight. Once the AWC is signed, these statements become part of the public record and are how the case is understood by the outside world.

For compliance teams, the findings are worth reading carefully. They often highlight the behaviors and control gaps that caught FINRA’s attention, and they can offer a useful perspective on how similar issues may be viewed in other firms or future reviews.

Sanctions

The sanctions section outlines the penalties FINRA is imposing to resolve the matter. These may include fines, suspensions, bars, or limitations on business activities, depending on the nature and severity of the conduct.

Sanctions are not just punitive. They reflect how seriously FINRA views the underlying issues and the level of risk it believes the conduct created. The scope and duration of a sanction can signal whether FINRA sees the matter as an isolated failure or part of a broader compliance breakdown.

For firms and individuals, this section often drives the most immediate business impact. Sanctions can affect licensing status, supervisory responsibilities, and the ability to operate or raise capital.

Curious how FINRA decides on sanctions and penalties? Read our guide on Understanding FINRA Sanction Guidelines for a clear, practical breakdown →

Waivers and Consents

The waivers and consents section explains what rights the firm or individual gives up by signing the AWC. This typically includes the right to contest the findings or challenge the sanctions through a formal hearing.

This part of the letter is often brief, but significant. By agreeing to these waivers, the respondent closes the door on further dispute of the matter within FINRA’s disciplinary process. Once executed, the decision is final.

For compliance and legal teams, this section is a reminder that an AWC isn’t just a penalty document. It's a binding agreement that settles the matter in full. There’s no opportunity to revisit the facts or push back on the outcome down the road.

Want to better understand how FINRA disciplinary actions work and what triggers them? Read our guide on FINRA Disciplinary Actions: What They Are and How To Avoid Them →

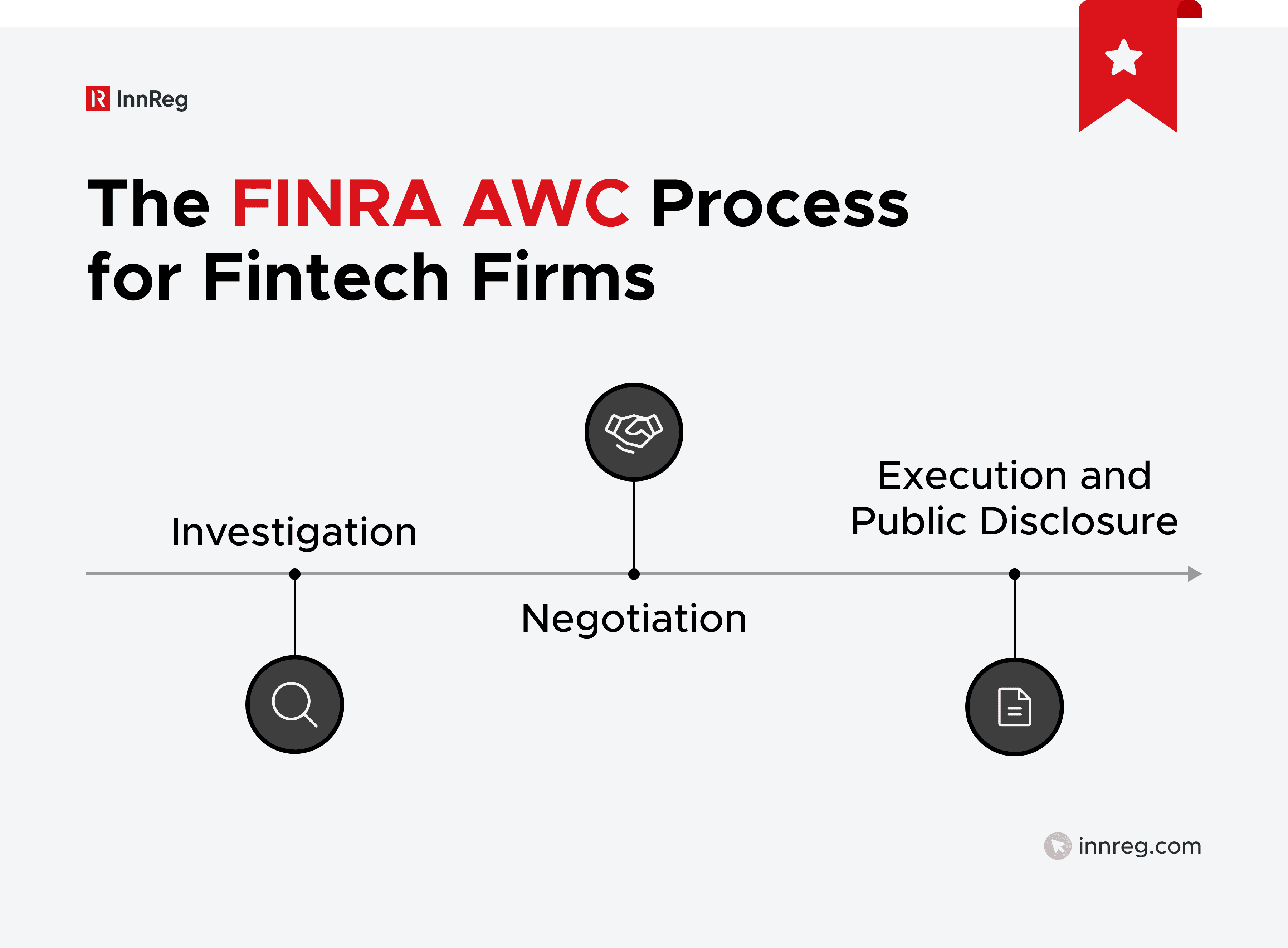

The AWC Process: Step-by-Step Guide for Fintech Firms

The AWC process generally follows a predictable sequence, though how long it takes and how complicated it gets vary by case. Understanding how each stage typically unfolds helps fintech firms prepare, coordinate internal teams, and respond more thoughtfully during a sensitive regulatory process.

See also:

Investigation

The AWC process usually begins with a FINRA investigation. This may stem from a routine examination, a targeted inquiry, or information FINRA receives from another source.

During this phase, FINRA gathers documents, reviews communications, and interviews relevant personnel. Requests can feel broad and time sensitive, especially for fast-growing firms that are still developing their compliance programs.

For fintech companies, early engagement matters. How information is organized, explained, and escalated internally during an investigation can shape how FINRA views the firm’s controls and culture, long before any settlement discussions begin.

Need help with broker-dealer compliance?

Fill out the form below and our experts will get back to you.

Negotiation

If FINRA decides enforcement is warranted, the conversation typically shifts toward a potential AWC. This is when the regulator shares proposed findings and sanctions, and both sides start discussing terms.

Negotiation is not just about numbers. The scope of the findings, the language used, and the framing of the conduct all matter. Small changes in wording can influence how regulators, counterparties, and future exam teams view the AWC.

For fintech firms, this phase works best when legal, compliance, and business leaders are all in the room together. A shared understanding of what actually happened operationally, combined with a realistic read on regulatory expectations, can lead to more balanced outcomes, even when the goal is to settle.

Execution and Public Disclosure

Once both sides agree on the terms, the AWC is executed and becomes final. At that point, FINRA publishes the letter, making it available through its public enforcement records.

This public disclosure is often where the impact becomes most visible. The AWC can be reviewed by:

Clients

Investors

Vendors

Examiners

All of them may draw their own conclusions from the language and sanctions.

For regulated firms, this moment reinforces why careful review matters earlier in the process. What’s written in the AWC is how the matter will be understood going forward, long after the enforcement action itself has concluded.

Regulatory Implications of FINRA’s AWC

A FINRA acceptance, waiver, and consent does not end with the signing of the letter. Its effects often extend into other regulatory, operational, and business areas.

Here are the most common regulatory implications that follow an AWC.

1. Statutory Disqualification and Licensing Challenges

Some AWCs contain findings or sanctions that trigger statutory disqualification under federal securities laws. When this occurs, it can limit a firm’s ability to maintain registrations or prevent individuals from serving in certain roles.

These issues often arise at moments of change. Applying for new licenses, adding principals, or expanding into new activities can become more complicated once an AWC is on record. What might have been a straightforward approval process can turn into a more detailed regulatory review.

2. Permanent BrokerCheck Disclosure and CRD Records

Once a FINRA AWC is finalized, it's reflected in BrokerCheck and the CRD system. These records are accessible to regulators, counterparties, and the public, and they remain visible for the life of the disclosure.

That visibility has real implications for day-to-day business. Investors, banks, and potential partners routinely review BrokerCheck as part of their due diligence process. An AWC on file can prompt follow-up questions or requests for more context about what happened.

3. Disclosure Triggers on SEC and State Filings

A FINRA AWC can trigger disclosure obligations across SEC and state regulatory filings. These requirements often apply to registration forms, amendments, and periodic updates for both firms and associated individuals.

In many cases, disclosures are required sooner than expected. Once an AWC is in place, changes in status, control persons, or business activities can create new or accelerated filing obligations. Missing or delaying these updates can lead to additional regulatory scrutiny.

4. Risk to Banking, Custodian, and Vendor Relationships

An AWC can change how a firm is viewed by its banking partners, custodians, clearing firms, and vendors. These counterparties routinely monitor regulatory history as part of their risk and oversight processes.

After an AWC becomes public, follow-up is common. Partners may ask for additional information, reassess risk controls, or apply closer oversight to the relationship. For fintech firms, where partnerships are often essential to the business model, this attention can affect timelines and operations.

5. Spillover Actions from the SEC and State Regulators

A FINRA AWC can draw attention from other regulators. The SEC and state authorities often review FINRA enforcement actions to determine whether related issues fall within their own jurisdiction.

While additional action is not automatic, it's not unusual. Depending on the nature of the findings and the firm’s regulatory footprint, other regulators may open inquiries, request information, or seek explanations tied to the same conduct.

6. Heightened Scrutiny in Future FINRA Examinations

After an AWC, firms should expect closer scrutiny in future FINRA examinations. Exam teams routinely review prior enforcement actions to understand what went wrong and how the firm responded, and if the firm has continued with the non-compliant behavior.

That scrutiny often becomes apparent during the exam itself. Examiners may ask more targeted questions, request additional documentation, or spend more time reviewing related controls, especially in areas connected to the original findings.

Common Compliance Failures That Trigger an AWC

Many AWCs trace back to the same underlying compliance gaps. The specific facts differ, but FINRA tends to focus on breakdowns in supervision, controls, and oversight rather than one-off mistakes.

For regulated firms, spotting these patterns helps compliance teams figure out where to focus their attention and fix problems before they spiral into something bigger.

Inadequate Supervision and Weak Compliance Controls

Gaps in supervision are at the root of many AWCs. FINRA expects firms to have systems that fit the size, complexity, and risk profile of their business, not just a set of policies sitting in a binder.

Problems often arise when growth outpaces controls. Supervisory responsibilities may be unclear, reviews may be inconsistent, or escalation paths may not work as intended. Over time, these weaknesses can lead to repeated issues that attract regulatory attention.

Improper Use of Off-Channel Communication Tools

FINRA continues to focus on how firms communicate with clients and counterparties, particularly when business conversations shift to text messages, personal email, or messaging apps that are not approved or monitored.

These situations often start informally. Employees may see off-channel tools as faster or more convenient, especially in remote or mobile work environments. Without clear rules and enforcement, these practices can spread quickly.

Misleading Marketing, Advertising, and Social Media Content

Marketing and social media activity is a frequent source of enforcement risk. FINRA reviews how firms describe products, performance, and risks, especially when content is designed to attract retail audiences.

Problems often stem from tone and context. Statements that sound promotional, simplified, or aspirational can be misleading when required disclosures are missing or unclear. Social media posts and influencer content also raise similar concerns when they’re not reviewed or approved.

Learn how to align fintech marketing language with regulatory expectations using our Compliance Glossary for Fintech Marketing →

Failure to File or Monitor Suspicious Activity (AML Violations)

AML-related failures are another common thread in AWCs. FINRA expects firms to have systems in place that can identify, review, and escalate potentially suspicious activity in a timely and consistent way.

Issues often come up when monitoring tools aren’t calibrated properly or when alerts are not reviewed. Backlogs, inconsistent documentation, or unclear escalation paths all point to gaps in a firm’s AML program. When these weaknesses persist, they tend to raise red flags with regulators.

Books and Records Violations, Including Incomplete Archiving

FINRA places heavy emphasis on accurate recordkeeping. When required records are missing or incomplete, it often signals larger supervisory control issues.

These violations commonly arise from day-to-day operational gaps. Communications may not be captured, retention settings may be misconfigured, or legacy systems may not align with current business activity. Over time, small gaps can add up.

Unsuitable Recommendations and Reg BI Failures

FINRA frequently brings enforcement actions tied to how recommendations are made and documented. This includes failures to understand a customer’s profile, explain risks, or act in the customer’s best interest.

Issues often develop when processes are inconsistent. Customer information may be incomplete, suitability reviews may be rushed, or documentation may not reflect the actual recommendation process. In fast-growing firms, these gaps can widen as volumes increase.

Undisclosed Outside Business Activities and Selling Away

Outside business activities and selling away remain common sources of enforcement risk. FINRA expects firms to know what their registered personnel are doing and to assess whether those activities create conflicts or supervision concerns.

Problems come up when disclosures are incomplete or not updated. Side projects, advisory roles, or informal investment activity can fall outside formal review if processes are unclear or inconsistently applied. Over time, this lack of visibility can lead to regulatory findings.

AWCs and the Fintech Trends Driving Enforcement

As fintech business models evolve, so does FINRA enforcement. Many recent AWCs reflect how new technologies, distribution models, and customer engagement strategies introduce fresh compliance challenges.

AI, Automation, and RegTech Exposure

AI and automation are now woven into how many fintechs operate. Firms rely on these tools for onboarding, surveillance, marketing, and decision support, often at significant scale.

Risk tends to show up when oversight doesn’t keep pace with adoption. Models get treated as black boxes, vendor tools run with minimal review, or exceptions slip through unnoticed. These gaps can draw regulatory attention when outcomes are inconsistent or poorly documented.

For compliance teams, governance is the core issue. Clear ownership, documented controls, and regular review go a long way toward demonstrating that automated systems are understood and managed, even as the technology keeps evolving.

See also:

Social Trading, Gamification, and Influencer Risk

Social trading features and gamified design have changed how users interact with financial products. Influencers and community-driven content now play a meaningful role in how firms attract and keep customers.

Regulatory risk increases when promotion outpaces supervision. Influencer statements, leaderboards, or reward-driven features can blur the line between education and recommendation. Without clear controls, firms may struggle to monitor how their products are presented to the public.

For compliance teams, visibility is everything. Clear approval processes, defined guardrails, and ongoing monitoring help align marketing innovation with regulatory expectations, especially in fast-moving digital channels.

Crypto Integration and Tokenized Securities

Many fintech firms are exploring ways to integrate crypto assets or tokenized securities into traditional financial products. These structures often sit at the edge of existing regulatory frameworks, which increases scrutiny.

Challenges tend to arise around classification, custody, and disclosure. When it's unclear how an asset is treated or which rules apply, supervisory and recordkeeping expectations can become difficult to meet. FINRA pays close attention to how firms assess and document these decisions.

For compliance teams, clarity matters. Documenting regulatory analysis and maintaining strong oversight helps firms demonstrate that they are disciplined regarding novel products, even as the technology continues to evolve.

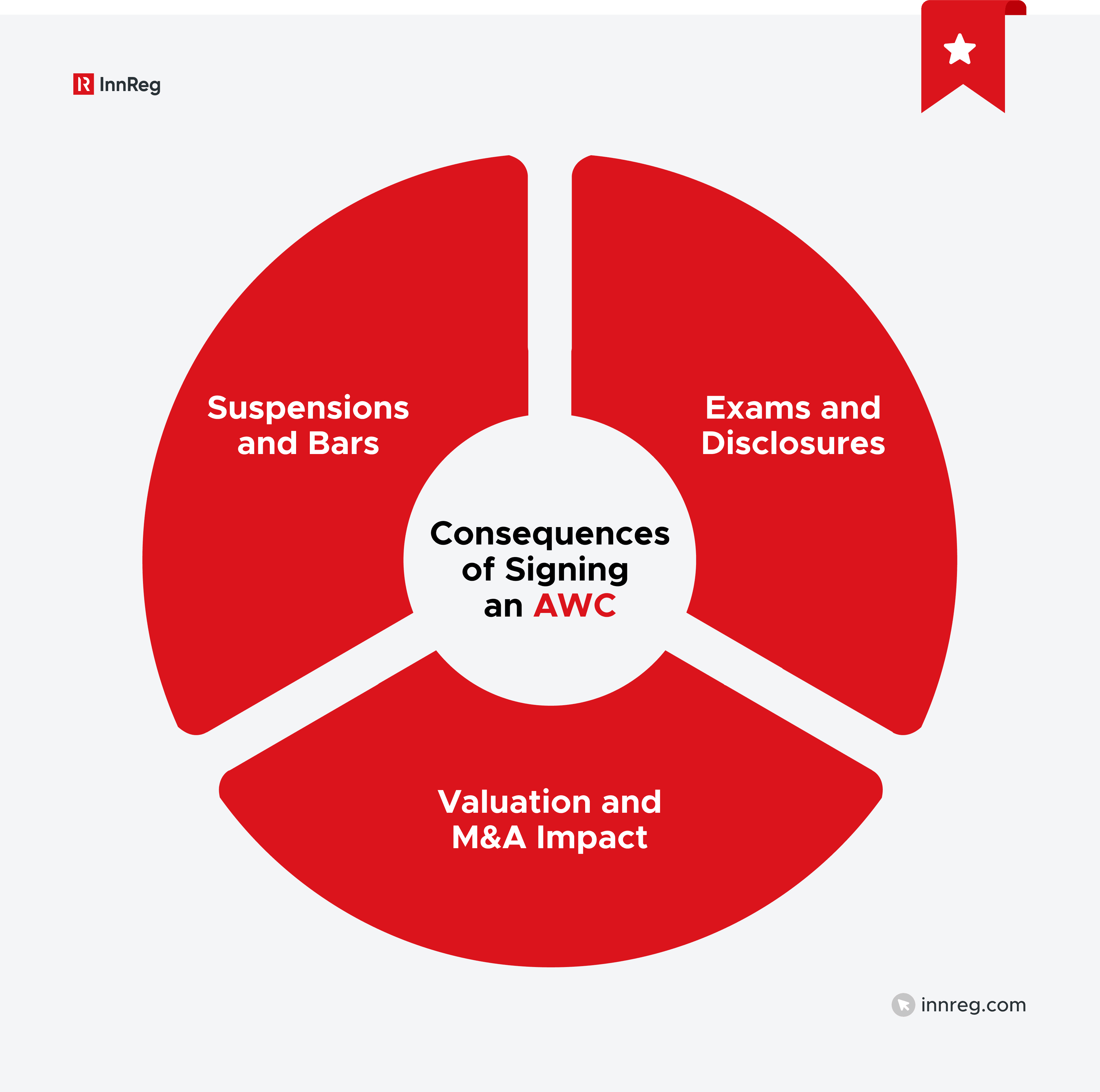

What Are the Long-Term Consequences of Signing an AWC?

Signing a FINRA acceptance, waiver, and consent can shape a firm’s regulatory profile long after the matter is resolved. While the enforcement action may feel finite, its effects often continue to influence operations, oversight, and future regulatory interactions.

Here are the most common long-term consequences firms and individuals should be aware of after an AWC is finalized.

Suspension, Bar, and Expulsion Risks

Some AWCs include sanctions that limit or halt a firm’s or individual’s ability to operate. Suspensions, bars, or expulsions are typically tied to more serious findings or repeated compliance failures.

The impact of these sanctions is practical and immediate. A suspension can disrupt day-to-day operations, while a bar or expulsion can end a regulated role altogether. For firms, this can ripple into leadership structure, supervisory coverage, and continuity planning.

From a planning perspective, these risks underscore the importance of understanding sanction terms fully. Clarity around scope, duration, and conditions helps firms assess operational impact and next steps, especially when key personnel are involved.

Future Examinations and Disclosures

After an AWC, firms and individuals are often viewed through a more experienced regulatory lens. Past enforcement becomes part of the context that exam teams consider when planning scope and depth.

This shows up in various ways. Future exams may include more detailed questions, targeted testing, or closer review of related controls. Disclosure obligations may also expand as roles change or new filings are required.

For compliance teams, consistency matters. Being prepared to explain how issues were addressed and how controls evolved helps keep future interactions focused and productive, rather than reactive.

Impact on Valuations and M&A Activity

An AWC can influence how a firm is viewed during fundraising, acquisitions, or strategic partnerships. Investors and acquirers routinely review regulatory history as part of due diligence, and enforcement actions often prompt deeper questions.

The impact is not always immediate, but it can shape negotiations. Buyers may adjust valuation assumptions, request additional representations, or seek stronger compliance commitments post-closing. Timelines can also extend as due diligence becomes more detailed.

For firms considering growth or exit options, context is important. Being able to clearly explain the circumstances of an AWC and the steps taken afterward helps position the business more confidently during strategic discussions.

How to Mitigate AWC Risk in Your Compliance Program

AWCs often stem from issues that build up over time rather than from a single breakdown. The good news is that many of these risks can be reduced with thoughtful compliance design and consistent execution.

This section focuses on practical steps firms can take to strengthen controls, improve oversight, and reduce the likelihood of enforcement issues escalating to an AWC.

Conduct Internal Reviews and Mock Regulatory Exams

Regular internal reviews help firms spot issues before regulators do. These reviews look at how policies, systems, and day-to-day practices align with regulatory expectations.

Mock exams add another layer of perspective. They simulate how regulators review supervision, records, and controls, which can surface gaps that routine monitoring may miss.

For fintech firms, this approach supports readiness. Testing controls in a realistic way helps teams respond more confidently during actual examinations and reduces last-minute scrambling.

Strengthen Supervisory Systems and Escalation Protocols

Supervision works best when responsibilities are clear, and escalation paths are easy to use. Ambiguity around who reviews what, and when issues should be raised, often leads to missed signals.

As firms grow, informal processes can break down. Supervisory reviews may become inconsistent, or issues may linger without a clear resolution. Strong systems help move concerns to the right people at the right time.

For compliance teams, structure supports consistency. Documented review processes, defined ownership, and clear escalation standards help supervision keep pace with business activity, even as operations become more complex.

Monitor and Archive All Business Communications

Business communication happens across many channels, and regulators expect firms to know where those conversations take place. Gaps often appear when new tools are adopted without clear compliance oversight.

Effective monitoring starts with visibility. Firms need to understand which platforms are used for business purposes and whether those communications are being captured and reviewed. This includes email, messaging tools, and any approved collaboration software.

For compliance teams, consistency matters more than complexity. Clear rules, practical training, and regular checks help confirm that communications are supervised and retained as required, even as tools and workflows evolve.

Implement a Culture of Compliance from the Top Down

A strong compliance culture starts with leadership. When executives and managers treat compliance as part of how the business operates, that mindset tends to carry through the organization.

Tone is set through actions, not slogans. How leaders respond to issues, allocate resources, and engage with compliance teams sends a clear message. Employees notice whether expectations are reinforced or quietly ignored.

For regulated firms, culture supports consistency. Clear leadership support helps compliance policies translate into everyday behavior, reducing the risk of informal workarounds that can lead to regulatory attention.

Develop a Self-Reporting and Remediation Framework

Issues are easier to manage when they surface early. A self-reporting framework gives teams a clear path to raise concerns before they grow into larger problems.

Effective frameworks focus on clarity and follow-through. Employees should know what to report, how to report it, and what happens next. Remediation should be documented and tracked so progress is visible.

For compliance teams, this approach supports accountability. Clear reporting and remediation processes help demonstrate good faith efforts to address issues and can improve how regulators view a firm’s response when problems arise.

Train Teams on High-Risk Areas Like Social Media and Crypto

Targeted training helps teams understand where regulatory risk tends to concentrate. Social media use and crypto-related products often evolve faster than formal policies.

Employee training works best when it reflects real scenarios. Examples drawn from actual business activity make expectations clearer and more relevant. Generic training is easier to ignore.

For compliance teams, focus matters. Regular, practical training in higher-risk areas helps reinforce expectations and supports consistent decision-making as products and channels continue to change.

Use RegTech Tools to Automate and Document Controls

RegTech tools can support compliance teams by reducing manual work and improving consistency. Automation is often most effective in areas like surveillance, recordkeeping, and task tracking.

The real value, however, depends on how those tools are used. Technology should reinforce existing processes rather than replace judgment or accountability. Clear configuration and regular review are essential to support effective compliance.

For fintech firms, flexibility matters. Using tools that integrate with current systems and workflows helps compliance scale alongside the business, without adding unnecessary friction.

See also:

When to Settle vs. When to Fight

Deciding how to respond to a proposed AWC is rarely straightforward. Each situation involves legal risk, business impact, and regulatory judgment.

Here are the key considerations firms weigh when deciding whether to resolve a matter through settlement or continue to challenge the allegations.

Negotiating Terms of the AWC

Negotiation plays a meaningful role in many AWC resolutions. While FINRA controls the enforcement process, there is often room to discuss scope, language, and proportionality.

These discussions extend beyond penalties. How findings are framed, which facts are emphasized, and how conduct is described can all influence downstream impact. Careful review of the draft matters just as much as the headline sanctions.

For firms, preparation helps keep negotiations focused and productive. Clear documentation, internal alignment, and a practical understanding of regulatory expectations make it easier to explain business realities and work toward more balanced outcomes.

Recognizing Leverage and Legal Risks

Not every enforcement matter carries the same level of risk or the same room to negotiate. The strength of the facts, how clear-cut the rules are, and the firm's regulatory history all play into how discussions unfold.

Understanding your leverage starts with being realistic. Some cases leave room to push back, while others come with higher exposure if you decide to fight. Knowing which situation you're in helps firms avoid escalating when it's not worth it.

For compliance and legal teams, context matters. Weighing the legal risk alongside the operational and reputational fallout leads to better decisions about how hard to negotiate or when it's time to accept a resolution and move on.

Consulting with Compliance Counsel

AWC decisions often benefit from experienced guidance. Compliance counsel from experts like InnReg can help interpret regulatory language, assess exposure, and frame responses that align with regulatory expectations.

That specialized support surpasses legal analysis. Experienced counsel helps translate enforcement posture into practical business considerations, including licensing, disclosure obligations, and operational impact.

For fintech firms, experience matters. Advisors who understand both innovation and regulation can help teams navigate AWC decisions with a clearer perspective, especially when those decisions carry long-term implications.

—

A FINRA acceptance, waiver, and consent reflects how regulators view a firm’s controls, decision-making, and overall approach to compliance. For fintech firms and other regulated financial companies, understanding AWCs helps teams respond with clarity rather than urgency when regulatory issues arise.

That understanding is supported by strong oversight, clear accountability, and compliance programs designed to work in practice. These foundations reduce the likelihood that issues escalate into enforcement actions and make it easier to engage constructively when concerns surface.

Firms that treat compliance as part of how they operate every day, rather than something they set up once and then forget about, tend to make better and smarter decisions when enforcement risk shows up.

Bruno is a Principal Compliance Officer at InnReg advising fintech clients across broker-dealer, RIA, and money transmitter verticals. He brings prior experience at Santander Brasil and Passfolio, with expertise in regulatory strategy, supervisory systems, and compliance execution. He holds FINRA Series 4, 7, 24, 63, and 99 licenses.

How Can InnReg Help?

InnReg is a global regulatory compliance and operations consulting team serving financial services companies since 2013.

We are especially effective at launching and scaling fintechs with innovative compliance strategies and delivering cost-effective managed services, assisted by proprietary regtech solutions.

If you need help with broker-dealer compliance, reach out to our regulatory experts today:

Related Articles

Featured LinkedIn Posts