RIA Testimonials: Rules and Compliance Requirements for Advisors

For many years, US securities rules did not allow investment advisors to use client testimonials in advertising. That changed when the Securities and Exchange Commission (SEC) adopted its modern Marketing Rule, which permits testimonials under specific conditions.

Since then, many RIAs have begun highlighting client feedback, online reviews, and referrals across their websites and social media. But RIA testimonials operate within a defined regulatory framework, with required disclosures, supervision expectations, and strict standards against misleading statements.

This article explains what RIA testimonials are, when they are allowed, and how they must be used under SEC rules. It also covers the distinction between testimonials and endorsements, key disclosure requirements, common mistakes identified in SEC exams, and practical steps RIAs can take to use testimonials in a compliant way.

At InnReg, we help RIAs build and manage compliant marketing programs, including policies, procedures, and review workflows for advertising under the SEC Marketing Rule.

What Are RIA Testimonials?

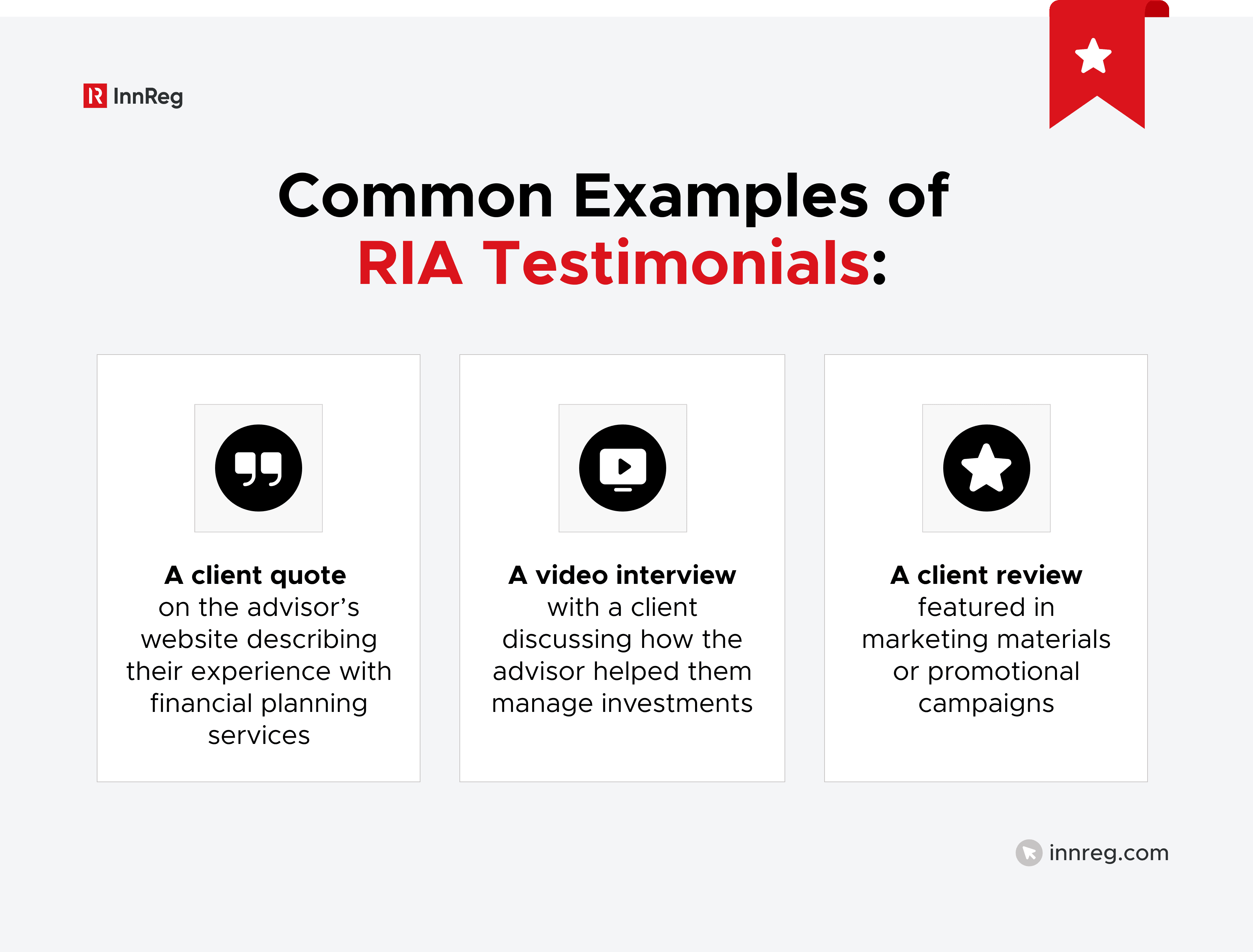

RIA testimonials refer to statements from current or former clients describing their experience with an investment advisor’s services. These statements are typically used in marketing materials to highlight client satisfaction, service quality, or outcomes.

Under the SEC’s Marketing Rule, a testimonial is defined as a statement by a current client, or investor in a private fund advised by the investment advisor, about their experience with the advisor or its supervised persons, that solicits or refers any current or prospective client or investor to be a client of the investment advisor.

The statement can appear in various forms, including written quotes, recorded videos, social media posts, or online reviews that the firm chooses to use in advertising.

Not every public comment about an advisor qualifies as an advertisement. However, when an RIA selects, republishes, or promotes a client statement as part of its marketing to solicit or refer clients, it generally becomes subject to the SEC’s advertising rules. This is why firms must carefully review how testimonials are collected, displayed, and supervised before using them in promotional materials.

Testimonial vs. Endorsement: Why the Distinction Matters

The SEC Marketing Rule draws a clear distinction between testimonials and endorsements. Both can appear in RIA advertising, but they are treated differently under the regulatory framework.

A testimonial refers to a statement from a current client or investor describing their experience with the advisor or its services, while soliciting or referring clients to the investment advisor. In contrast, an endorsement is a statement made by someone who is not currently a client or investor in a private fund advised by the investment advisor, such as a promoter, influencer, or professional partner recommending the advisor.

This distinction matters because different compensation disclosure requirements may apply depending on the situation. For example, if a third party promotes an advisor’s services and receives compensation, the arrangement may fall under endorsement rules rather than testimonial rules.

The difference can be summarized as follows:

Type | Who Makes the Statement | Typical Context |

|---|---|---|

Testimonial | Current client or investor in a private fund advised by the investment advisor | Client provides reviews, feedback, or experience statements |

Endorsement | Non-client promoter or third party | Influencers, referral partners, or marketing affiliates |

In practice, the line can become blurred. A social media post, podcast appearance, or referral arrangement may shift from a testimonial to an endorsement depending on who makes the statement.

Because of this, compliance teams should review promotional content carefully before publishing it. Misclassifying a testimonial as something else can lead to increased regulatory risk, including missing disclosures or improper marketing practices under the SEC Marketing Rule.

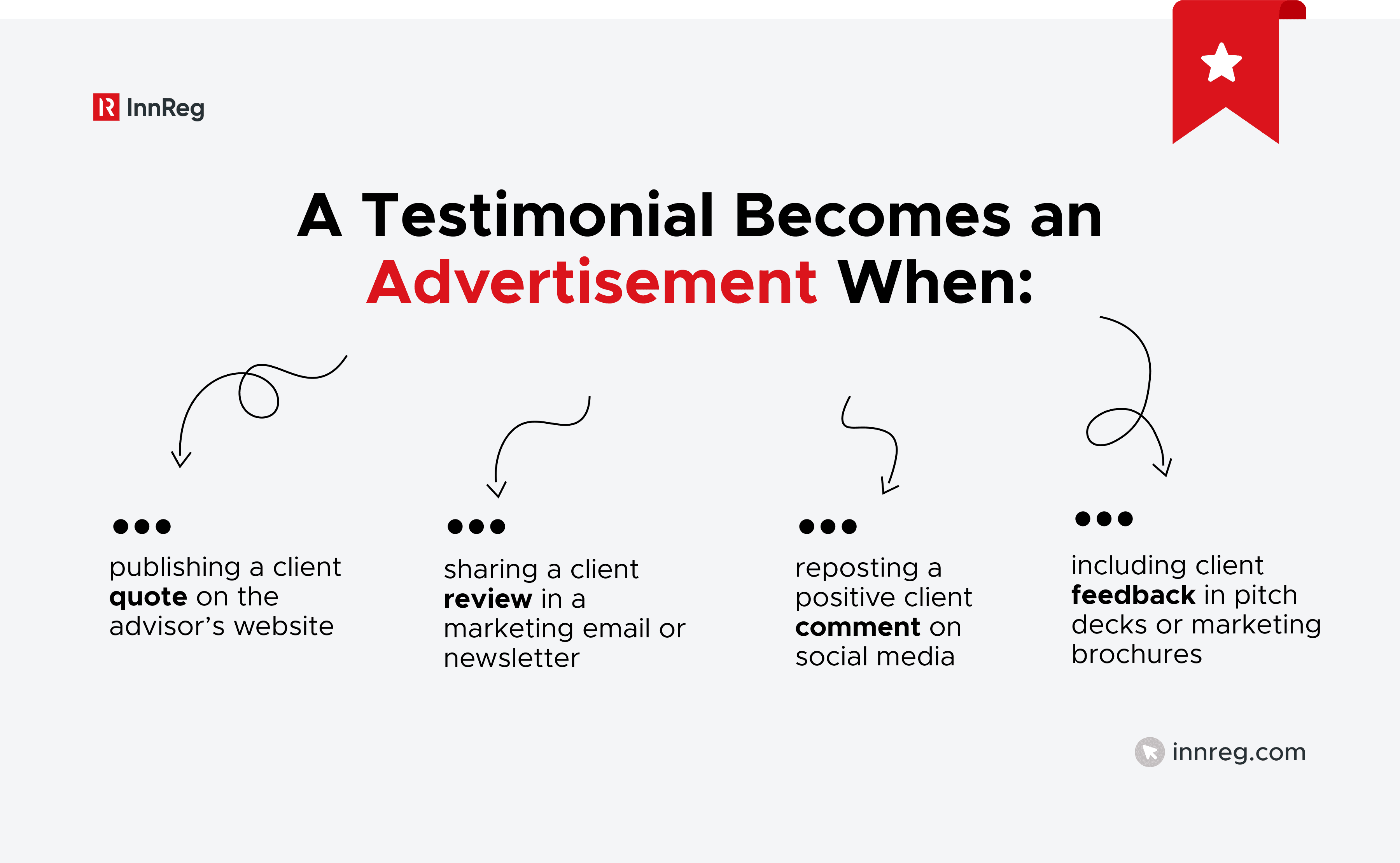

When an RIA Testimonial Becomes an Advertisement?

Not every client comment automatically becomes regulated advertising. The key factor is how the statement is used by the advisor. Under the SEC Marketing Rule, a testimonial generally becomes advertising when the RIA includes or distributes it as part of its marketing communications.

This often happens when firms highlight positive feedback in materials designed to attract new clients. For example, an advisor may feature a client quote on its website, repost a review on social media, or include client feedback in a presentation. Once the firm chooses to use that statement for promotional purposes, it typically falls within the scope of the marketing rule.

In contrast, independent comments that the advisor does not control or republish may fall outside the definition of advertising. For example, a client posting a review on their own social media account without the advisor promoting, paying for, or amplifying it would generally not be treated as the advisor’s advertisement.

However, the analysis can change quickly once the advisor interacts with the content. Selecting, highlighting, or republishing client feedback can transform a simple comment into regulated marketing material. Because of this, firms should have a review process for testimonials and for providing online reviews before using them in promotional channels.

Are RIA Testimonials Allowed?

RIA testimonials are allowed today, but only within a defined regulatory framework. The SEC’s Marketing Rule (Rule 206(4)-1) permits investment advisors to use testimonials in advertising, replacing the older rule that broadly prohibited them.

The rule allows RIAs to feature client feedback in marketing materials as long as certain conditions are met. These include disclosure requirements, oversight of promotional content, and compliance with the rule’s general prohibitions against misleading statements.

As a result, many advisors now display reviews and testimonials on websites, social media pages, and digital marketing campaigns. At the same time, firms must review how testimonials are presented and what disclosures accompany them.

This matters because the Marketing Rule applies broadly to advisor advertising. Testimonials are only one part of it. The rule also governs endorsements, third-party ratings, and other marketing communications used to attract clients.

The SEC Marketing Rule Explained (Rule 206(4)-1)

The SEC adopted the current Marketing Rule in December 2020, with a compliance date in November 2022. The rule consolidated two older regulations: the advertising rule and the cash solicitation rule.

Under this framework, testimonials and endorsements are allowed if they comply with specific disclosure, oversight, and recordkeeping requirements. Advisors must also follow the rule’s general prohibitions, which apply to all advertising content.

At a high level, the Marketing Rule requires RIAs using testimonials to:

Disclose that the testimonial was provided by a current client or investor

Disclose, when applicable, that compensation was provided, and the material terms of the compensation arrangement, along with a description of the compensation provided

Statement of material conflicts of interest resulting from the RIA's relationship with the provider of the testimonial

Avoid misleading or unsubstantiated statements

Maintain the required books and records related to the advertisement

The rule also introduced the concept of “promoters,” which includes individuals who provide testimonials or endorsements for compensation. These arrangements often require written agreements and additional disclosures.

Learn more about the SEC Marketing Rule →

What Changed Under the Modernized Rule

The previous advertising rule, adopted in 1961, largely prohibited testimonials in advisor advertising. This created tension with modern marketing practices, particularly the growth of online reviews and digital marketing channels.

The modern rule reflects how advisory firms communicate with clients today. It allows testimonials and endorsements while placing responsibility on advisors to present them in a fair and balanced way.

SEC-Registered vs. State-Registered RIAs

Most of the discussion around RIA testimonials focuses on the SEC Marketing Rule because it applies to SEC-registered advisors. However, state-registered RIAs may be subject to additional state advertising rules, and not every state follows the federal framework in the same way.

Some states have adopted similar approaches to testimonials and endorsements. Others still maintain stricter interpretations of advertising rules for state-registered firms.

Because of this, advisors operating under state registration should review their specific jurisdiction’s requirements before using testimonials in marketing materials. Compliance teams often need to evaluate both the SEC rule and applicable state guidance when designing testimonial policies.

For fintech RIAs that scale quickly or operate across multiple jurisdictions, this analysis can become more complex. Firms often address this by developing internal marketing review procedures and centralized oversight of advertising materials.

In practice, RIAs using testimonials should evaluate both federal and state regulatory expectations before publishing marketing content.

—

RIA testimonials are allowed under the SEC framework, but their use is still regulated. Firms may feature client feedback in marketing materials, though those statements must be reviewed and presented with the appropriate disclosures. As marketing expands across digital channels, many RIAs find that monitoring testimonials, endorsements, and reviews across platforms becomes an ongoing compliance task.

Regly’s marketing compliance module helps fintech do just that. Based on 10+ years of InnReg’s experience, Regly’s compliance platform helps you flag potential risks using AI-powered tools and centralize reviews and approvals →

See also:

Conditions for Registered Investment Advisors Using Testimonials

The SEC Marketing Rule allows registered investment advisors to use testimonials, but only if certain requirements are met. These requirements focus on transparency, proper oversight, and preventing misleading marketing practices.

Need help with RIA compliance?

Fill out the form below and our experts will get back to you.

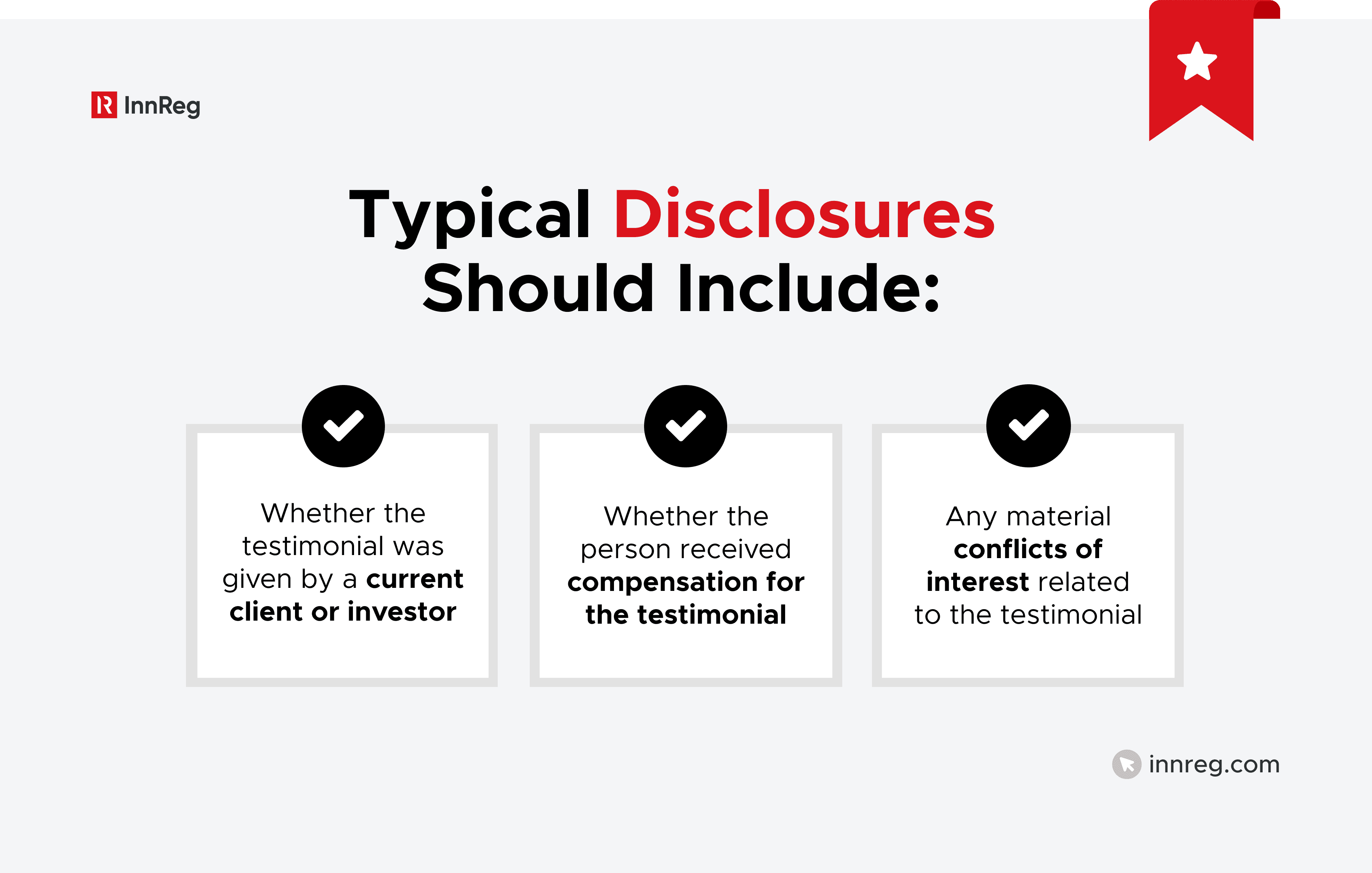

Required Disclosures at the Time of Use

The Marketing Rule requires specific disclosures whenever testimonials appear in advertising. These disclosures help investors understand the context behind the statement.

At a minimum, advertisements containing RIA testimonials must disclose whether the person giving the testimonial is a current client or investor. If the individual was compensated for the statement, that must also be disclosed.

The disclosures must be clear and presented alongside the testimonial so readers can easily understand the context.

Compensation: Cash, Non-Cash, and Referral Incentives

Compensation plays an important role in how testimonials are regulated. If an RIA provides compensation for a testimonial, additional disclosure and oversight requirements apply.

Compensation can take several forms, including:

Cash payments for promotional statements

Gift cards or other non-cash incentives

Fee discounts or referral rewards

Marketing or promotional arrangements with third parties

Whenever compensation is involved, the firm must disclose that fact in the advertisement along with the material terms of the compensation arrangement and a description of the compensation. The disclosure should make it clear that the person providing the testimonial received something of value.

Written Agreements With Promoters

When compensated, promoters provide testimonials or endorsements, the SEC Marketing Rule generally requires a written agreement between the advisor and the promoter.

These agreements must describe the nature of the promotional relationship, including how the promoter will market the advisor’s services and how compensation is structured. The agreement typically establishes expectations around oversight and supervision, helping document the relationship for compliance purposes.

Disqualification and “Ineligible Persons”

The Marketing Rule restricts certain individuals from acting as promoters. These individuals are referred to as “Ineligible Persons.”

Examples may include individuals subject to certain regulatory sanctions or disciplinary actions. Firms must review promoter eligibility before entering testimonial or endorsement arrangements.

This screening is often incorporated into the firm’s compliance review process when evaluating promoters, influencers, or referral partners.

Recordkeeping Requirements

RIA advertising is subject to SEC books and records requirements, and testimonials are no exception.

Advisors must retain records related to their advertising activities, including documentation associated with testimonials and endorsements. This includes records of the advertisement itself, disclosures provided, and agreements with promoters when applicable.

Maintaining proper documentation helps firms demonstrate compliance during SEC examinations. It also allows compliance teams to track how testimonials were reviewed and approved before publication.

RIA Testimonials vs. Third-Party Ratings

RIA testimonials and third-party ratings can look similar in marketing, but the SEC treats them differently under the Marketing Rule. Testimonials reflect a client’s experience with an advisor, while third-party ratings come from external organizations or ranking providers. Because of that distinction, different disclosure and compliance requirements may apply.

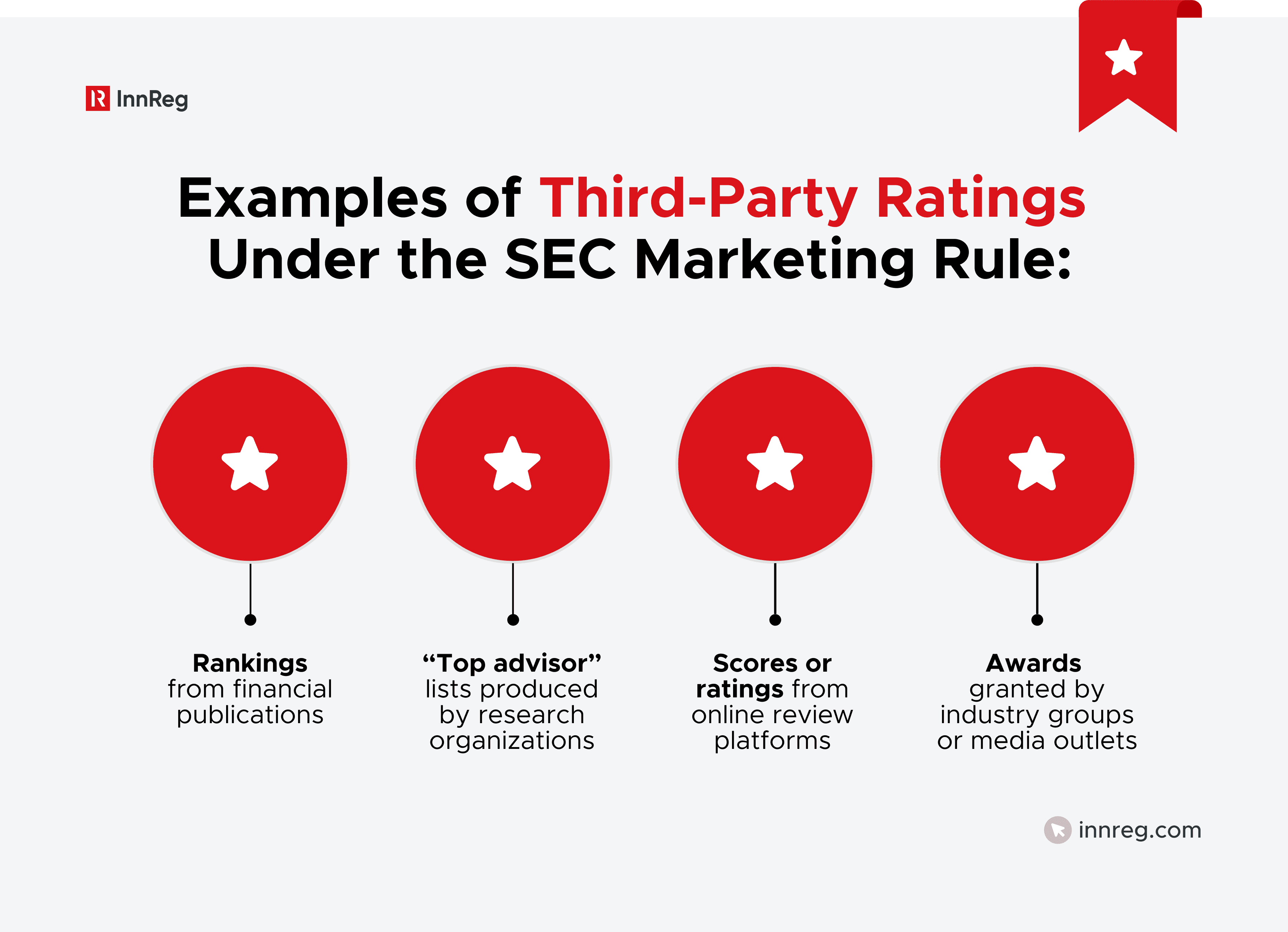

What Qualifies as a Third-Party Rating

Under the SEC Marketing Rule, a third-party rating refers to an evaluation of an advisor provided by an external party. These ratings typically appear in industry rankings, review platforms, or publications that compare advisory firms.

For a rating to qualify under the rule, it must be created by a person or entity that is not the advisor and is not related to the advisor. The rating must also be based on a structured methodology and cannot be designed to produce pre-determined results.

The rule also expects advisors to have a reasonable basis for believing that the rating was prepared according to objective criteria.

Required Disclosures for Ratings and Rankings

When RIAs use third-party ratings in advertising, the SEC requires additional disclosures to provide context for investors.

Typically, the advertisement must explain the date of the rating, the period of time upon which the rating is based, the identity of the third party that created it, and the criteria used in determining the ranking. If compensation was provided in connection with the rating, that fact must also be disclosed.

These disclosures allow readers to understand how the rating was produced and whether any potential conflicts of interest exist.

Common Mistakes With Google Reviews and “Top Advisor” Badges

Many RIAs now highlight online reviews or industry awards in their marketing. While these can be valuable marketing tools, they can also create compliance issues if they are presented without proper context.

A common mistake involves selectively highlighting positive ratings without explaining how the rating system works. Another issue occurs when advisors display a ranking badge or award but omit details about how the ranking was determined.

Online reviews can also raise questions when advisors promote them without reviewing whether disclosures are required. For example, reposting a client review or emphasizing a rating may trigger the Marketing Rule’s testimonial or advertising requirements.

Because of this, firms often apply the same internal review process to testimonials, ratings, and awards before using them in promotional materials.

See also:

General Prohibitions That Still Apply to RIA Testimonials

Although the SEC Marketing Rule allows testimonials, the rule’s general anti-misleading standards still apply to all RIA advertising. Advisors remain responsible for how testimonials are presented and cannot use them in a way that creates an inaccurate impression. These requirements apply whether testimonials appear in written materials, videos, or digital marketing.

Untrue or Unsubstantiated Statements: | Misleading Implications About Performance | Cherry-Picking Presentation | Testimonials About Third-Party Products |

|---|---|---|---|

RIA testimonials cannot include claims that are false, exaggerated, or unsupported. | Testimonials must not imply investment performance or outcomes that the advisor cannot support. | Marketing materials should avoid presenting client feedback in a way that distorts how services are typically experienced. | Testimonials referencing specific investments or strategies can create additional compliance risk. |

Untrue or Unsubstantiated Statements

Advisors cannot publish testimonials that contain statements they cannot support. If a client makes claims about results, performance, or outcomes, the firm must have a reasonable basis to believe the statement is true.

RIA testimonials cannot include claims that are false, exaggerated, or unsupported by evidence. Even if the statement comes directly from a client, the advisor remains responsible for the advertisement.

This is why compliance teams often review testimonials carefully before approving them for marketing use.

Misleading Implications About Performance

Testimonials can sometimes imply investment performance or outcomes, even when performance numbers are not shown. For example, a statement suggesting that a client “achieved strong returns” or “grew their wealth quickly” may create expectations that the advisor cannot support.

Under the Marketing Rule, RIA testimonials must not create misleading implications about investment performance or likely results.

Firms often address this risk by avoiding testimonials that reference performance or by adding contextual disclosures.

Performance-related language is one of the most common sources of marketing risk. To help firms avoid common mistakes, we have created a free Compliance Glossary for Fintech Marketing →

Cherry-Picking and Selective Presentation

Another concern involves selectively displaying only positive testimonials while ignoring other relevant information. While the rule does not require firms to present negative feedback, marketing materials cannot create a misleading overall impression.

For example, highlighting only highly favorable client experiences without appropriate context can be considered misleading advertising. The SEC has historically viewed selective presentation as a risk area in advisor marketing.

Because of this, firms often evaluate testimonials as part of a broader review of how their services are described in marketing materials.

Testimonials About Third-Party Products

Some testimonials may refer to specific investment products or strategies recommended by the advisor. This can create additional compliance concerns, especially if the testimonial implies that the product performed well.

RIA testimonials that reference third-party products must still comply with the rule’s general prohibitions against misleading statements.

If the testimonial suggests that a particular investment produced strong results, the firm must evaluate whether the statement could create unrealistic expectations or omit important context.

For this reason, many compliance programs review testimonials not only for disclosure requirements but also for how prospective clients might interpret them.

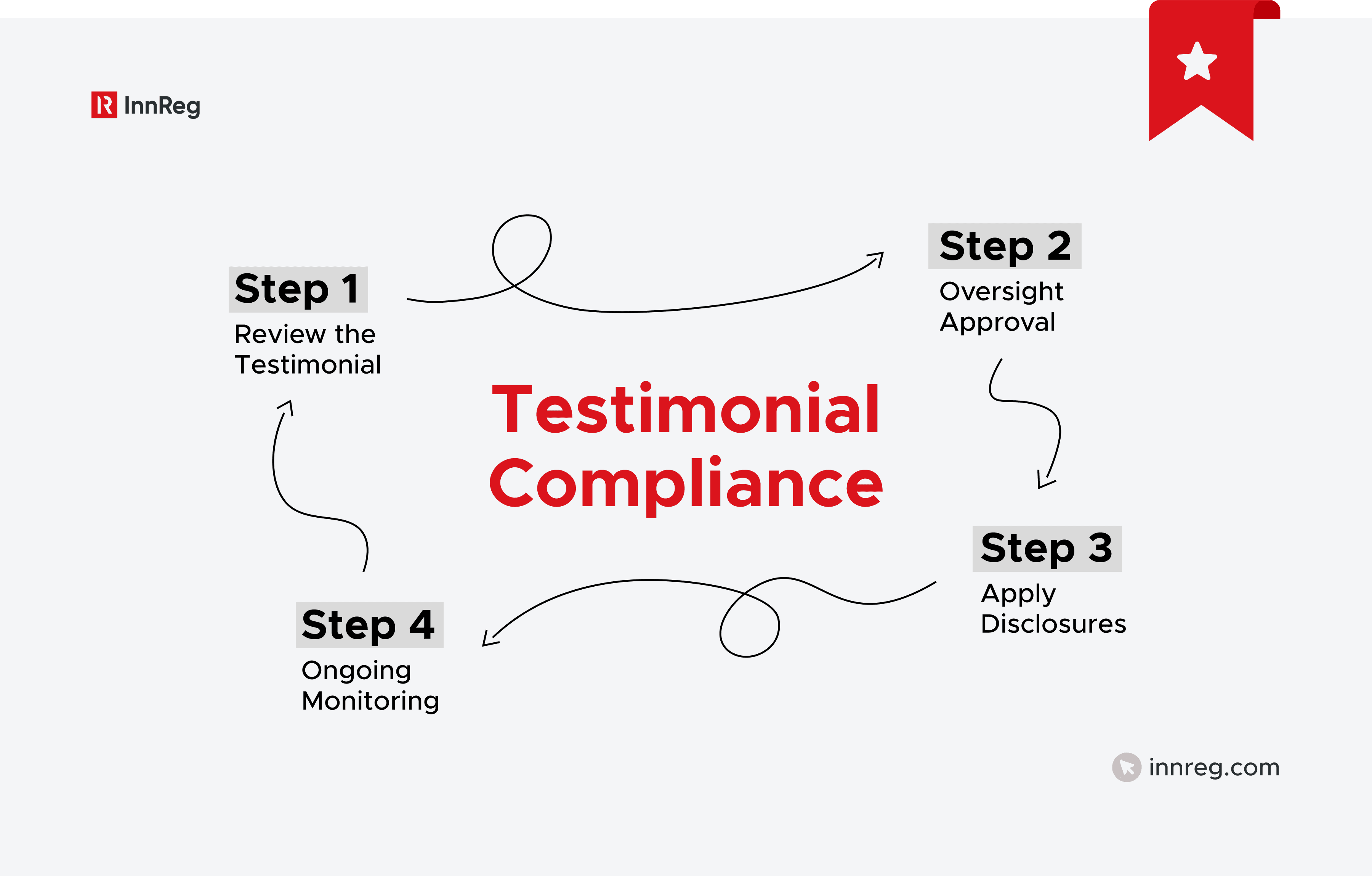

How to Use Testimonials as a Registered Investment Advisor

The SEC now allows testimonials, but firms typically still review them before publishing. In many RIAs, testimonials go through the same approval process as other regulated advertising.

1. Step-by-Step Review Process

Many firms handle testimonials through a defined review workflow before they appear in marketing materials. The process typically begins when marketing teams collect client feedback or identify reviews they would like to highlight.

Compliance teams typically review the testimonial to decide whether it falls within the SEC Marketing Rule’s definition of advertising. During that review, they may check whether disclosures are needed, consider whether the statement could imply performance, and look for language that could be misleading.

Maintaining a documented review process can also be useful. It shows that testimonials were reviewed before being published, which may become relevant during an SEC examination.

Build on InnReg’s experience of working with 100+ innovative fintechs, Regly helps firms review marketing materials using AI-powered tools →

See also:

2. Internal Controls and Marketing Oversight

Testimonials are usually reviewed under the same supervisory framework that applies to other RIA marketing communications. Firms often define internal responsibilities for approving testimonials and determine where they may be used.

For instance, marketing teams may need to submit testimonials for compliance review before they appear on websites, social media, or promotional materials. Written supervisory procedures often describe how these reviews take place and who has the authority to approve them.

Clear oversight helps maintain consistent marketing standards across different channels.

3. Templates for Disclosures

Because testimonials require specific disclosures, many RIAs develop standardized language that can be applied when testimonials appear in marketing.

These disclosure templates may address whether the person providing the testimonial is a client, whether compensation was involved, and whether any conflicts of interest exist. Using standardized language can help maintain consistency across advertisements.

Disclosure templates also reduce the risk that required information is omitted when testimonials are published.

4. Ongoing Monitoring and Periodic Testing

Posting a testimonial does not end the compliance review. Marketing materials evolve, and testimonials may remain visible long after they were originally published.

As a result, firms often revisit their marketing channels from time to time to check that testimonials still comply with applicable rules and that disclosures are still accurate.

Periodic testing helps firms identify outdated testimonials, missing disclosures, or content that may require additional review.

FTC and FINRA Considerations for RIA Testimonials

The SEC Marketing Rule is the primary framework governing RIA testimonials, but it is not the only rule set that may apply. In some situations, other regulators such as the Federal Trade Commission (FTC) or Financial Industry Regulatory Authority (FINRA) may also influence how testimonials are presented in marketing materials.

When FTC Endorsement Rules Apply

Testimonials are not only addressed by securities regulators. The Federal Trade Commission also regulates endorsements used in marketing across many industries.

The FTC’s approach focuses on transparency. When someone promoting a firm has received payment, discounts, referral rewards, or similar incentives, that connection should be disclosed so audiences understand the context of the statement.

This can become relevant in marketing campaigns that extend beyond traditional advisory advertising (for example, influencer promotions, affiliate partnerships, or social media marketing).

When FINRA Rules May Also Apply

FINRA rules can become relevant when a firm operates a broker-dealer alongside its advisory business. In these situations, marketing content may fall under both SEC and FINRA advertising frameworks.

For example, dual-registered firms or affiliated broker-dealers may need to consider FINRA communications rules when using testimonials in marketing materials. These rules focus on fair and balanced communications and prohibit misleading or promissory statements.

FINRA has historically taken a cautious approach to testimonials, particularly when they imply investment performance or guarantees of success. As a result, firms with broker-dealer affiliations often apply additional internal review before publishing testimonial-based marketing.

Learn more about FINRA →

Practical Compliance Takeaways for RIA Testimonials

RIA testimonials can be used in marketing today, but they require structured oversight. The SEC Marketing Rule allows them under specific conditions, and firms remain responsible for how these statements appear in advertisements.

Below are several practical compliance takeaways that RIAs often consider when using testimonials in marketing materials:

Treat testimonials as regulated advertising: RIA testimonials generally fall within the scope of the SEC Marketing Rule when they are used in promotional materials. As a result, many firms route testimonials through the same internal review process used for other marketing communications.

Review testimonials before publishing them: Marketing teams may collect client feedback, but compliance teams typically review the content before it appears on websites, social media, or promotional materials. This review often evaluates whether disclosures are required and whether the language could create a misleading impression.

Include required disclosures with the testimonial: When a testimonial appears in advertising, the firm must disclose whether the individual providing the statement is a current client or investor. If the testimonial involves compensation or incentives, that relationship must also be disclosed clearly.

Avoid testimonials that imply investment performance: Statements suggesting strong investment returns or financial outcomes can create regulatory risk. Many firms avoid testimonials that reference performance unless the context can be clearly supported and presented without creating unrealistic expectations.

Apply consistent supervision across marketing channels: Testimonials can appear in many places, including websites, social media posts, presentations, and marketing campaigns. Compliance teams often apply the same review standards across all channels to maintain consistent advertising practices.

Maintain documentation and records: Advertising rules require RIAs to keep records related to marketing materials. Firms often retain copies of testimonials, disclosures, and documentation showing that the advertisement was reviewed before publication.

Monitor testimonials after publication: Testimonials may remain visible for long periods after they are first posted. Periodic reviews of websites and marketing channels can help firms identify outdated testimonials, missing disclosures, or content that may require additional review.

Tarik is a Principal Compliance Consultant at InnReg with over 5 years of experience advising fintech clients across broker-dealer, RIA, and money transmitter verticals. He holds FINRA Series 3, 7, 24, 57, 63, 79, and 99 licenses, with expertise in regulatory strategy, supervisory systems, and compliance roadmap implementation.

How Can InnReg Help?

InnReg is a global regulatory compliance and operations consulting team serving financial services companies since 2013.

We are especially effective at launching and scaling fintechs with innovative compliance strategies and delivering cost-effective managed services, assisted by proprietary regtech solutions.

If you need help with RIA compliance, reach out to our regulatory experts today:

Related Articles

Featured LinkedIn Posts