The Fintech Guide to Gaming Compliance

Gaming compliance is a central issue for fintech companies experimenting with game-like features, rewards-based models, real-money contests, and similar models.

The moment a platform introduces in-app currency, tokenized prizes, or user incentives tied to financial outcomes, it may trigger a patchwork of complex regulations. Getting it wrong can mean more than just fines: it can shut down a product line or delay a launch indefinitely.

This article breaks down gaming compliance for fintechs, including how regulators see gaming mechanics in financial platforms, where the boundaries lie between legal innovation and prohibited activity, and what practical controls need to be in place before real users and real money are involved.

At InnReg, we help fintech teams evaluate gaming-style features through a regulatory lens, including gambling law risk, MSB and money transmitter exposure, and AML program requirements. From licensing strategy to building and operating compliance programs, we support launches where rewards, tokens, or real-money mechanics are involved.

What Is Gaming Compliance?

Gaming compliance addresses the legal and regulatory requirements that apply when a product includes gambling-style features, gaming mechanics, or contests involving monetary value. In fintech, it kicks in when platforms build mechanics around in-app currencies, cash-based prizes, or user competitions with financial stakes.

The rules are not always obvious. Depending on how the product is structured, gaming compliance may trigger anti-money laundering (AML) laws, consumer protection obligations, money transmitter licensing, or gambling restrictions. Each carries its own regulatory expectations, and in some cases, multiple regulators overlap.

For fintech teams working on new products, this area creates more questions than it resolves. Gaming compliance is not a static checklist. It is a moving boundary determined by how you design the product, how users interact with it, and where those users are located.

What Gaming Compliance Means for Fintech

For fintech companies, gaming compliance surfaces in places they do not always expect. It is not limited to casinos or betting apps. It applies to any product that blends financial incentives with game-like engagement, even if the product’s core function is investment, savings, or payments.

Each of these could trigger different rules depending on structure and jurisdiction. What matters is how users interact with money, risk, and reward.

When users can win or lose value based on outcomes outside their control, regulators may treat it as gambling. If money flows between users or across accounts, money transmitter rules usually apply.

Key Regulatory Frameworks Behind Gaming Compliance

There is no single law or agency that defines gaming compliance for fintech. Instead, it sits at the intersection of several regulatory domains, depending on how the product is structured and where it's offered.

US Federal Laws that Impact Gaming Mechanics

A handful of federal laws shape how gaming mechanics get regulated when they connect to financial activity. They apply whether or not your product is technically a gaming platform.

Key statutes to be aware of:

Bank Secrecy Act (BSA): If a platform handles user funds (deposits, withdrawals, in-game currency trades), AML rules probably apply. That means verifying identities, watching transactions, and filing reports in case of suspicious activity.

Unlawful Internet Gambling Enforcement Act (UIGEA): Sanctions the providers that knowingly process payments for illegal online gambling. Even if a platform operates legally in certain states, UIGEA becomes a problem when users from restricted areas can get in.

Federal Wire Act: Sending bets over state lines is considered violation under this act. Firms can run into problems when users and the business are both in permitted jurisdictions but the platform's servers aren't.

USA PATRIOT Act: Adds enhanced AML requirements, especially around customer due diligence and source-of-funds scrutiny.

Securities Exchange Act of 1934: If a gaming mechanic resembles investment activity, such as profit-sharing, token appreciation, or “staking”, you may fall under SEC oversight.

These laws do not apply only to gambling companies. Fintech platforms that use chance-based or competitive mechanics with financial stakes can trigger one or more of these rules.

International Considerations for Global Products

Platforms with users outside the US face compliance obligations abroad as well.

Countries enforce their own rules, and how they regulate games involving money, rewards, or digital currencies changes from one place to another:

United Kingdom: Gambling Commission oversees games of chance that offer prizes, covering most digital formats. Skill-based games might get an exemption, but the definitions are tight. Loot boxes and crypto gaming are currently being reviewed for possible reclassification.

European Union: Each member state enforces its own gambling laws, but AML standards are harmonized under the EU’s AMLD framework. Offering gaming features in one country may be legal, while in another it may require licensing or ban the model entirely.

Singapore, Hong Kong, Australia: These jurisdictions treat a broad spectrum of digital behaviors as potentially subject to gambling regulation. That can include fantasy sports, skill-based competitions, or token-driven mechanics. Licensing, disclosure obligations, and having a local presence might all be necessary.

Canada: Each province handles gaming regulation on its own. Ontario has set up a separate framework for online gaming and has taken enforcement action against platforms that failed geolocation requirements.

Global AML expectations: If a platform lets users move value, real or virtual, AML rules usually apply. The majority of jurisdictions follow FATF guidelines that require KYC, transaction records, and reporting across all business types.

Expanding internationally introduces new gaming compliance risks. What is legal in the US could be restricted or license-bound elsewhere. Features that look minor, like transferring in-game credits between users, create liability in certain markets.

Gaming Compliance vs. Gambling Compliance

The terms “gaming” and “gambling” are often used interchangeably, but they’re not the same in a regulatory context. Understanding the difference is critical because the classification determines whether you need a license and what kind.

Understanding the Difference

Gaming, including skill-based gaming, refers to interactive experiences that may involve contests, competitions, or gamified financial apps. It crosses into a compliance territory when money or something of value is involved.

On the other hand, gambling is generally defined as an activity that includes all three of the following elements: consideration (user pays or stakes something of value), chance (outcome involves some level of randomness).

When these elements are present, regulators typically classify the activity as gambling. That is when licensing, age verification, geolocation, and other regulatory controls usually apply.

Why the Distinction Matters for Licensing

Whether regulators define a product as gaming or gambling changes everything about licensing. Gambling demands formal authorization granted at the state or national level. Licensing is resource-intensive, varies across borders, and imposes strict operating conditions.

On the other hand, skill-based formats and promotional contests can sometimes bypass gambling licenses. However, it is important to note that this is not the same as operating license-free. States may require you to register prize promotions or sweepstakes. Some have unclear statutes that draw regulatory focus even without a clear-cut gambling element.

Fintech teams can not rely on assumptions or “intent” when evaluating exposure. Licensing depends on how the game operates, how users participate, and what they can win. It’s a legal classification, not a design decision.

See how InnReg helps fintech develop a regulatory strategy →

When Gaming Becomes Financial Activity

Not every game is viewed as a financial product. However, when platforms process real funds, give out rewards that have value, or allow user-transfers, gaming compliance enters the picture.

See also:

Virtual Currencies and MSB Risk

Platforms that allow users to buy, send, hold, or cash out virtual currencies, including points, tokens, or in-game credits, may be engaging in money transmission. That classification comes with federal and state-level compliance obligations.

The key factor is not whether the asset is “crypto” or “real money,” but if it has stored value and whether users can: convert it back into fiat or crypto, transfer it to another user or use it to buy off-platform goods or services.

If yes, regulators may treat the platform as a money services business (MSB). That brings FinCEN registration requirements, AML program obligations, and, depending on the states involved, money transmitter licensing.

Learn how InnReg helps fintech by providing compliance support to Money Services Businesses →

Some companies try to stay exempt by restricting their virtual currency:

No transfers between users

No cash-outs

Use is limited to one game or platform

These design features may help avoid MSB classification, but they need to be deliberate and documented. A seemingly minor feature, like enabling peer-to-peer token gifting, can change the platform’s risk profile entirely.

Fintech teams using in-app currency or tokens should map out value flows and control points early.

InnReg offers regulatory and product strategy services to help fintech set appropriate controls →

Need help with fintech compliance?

Fill out the form below and our experts will get back to you.

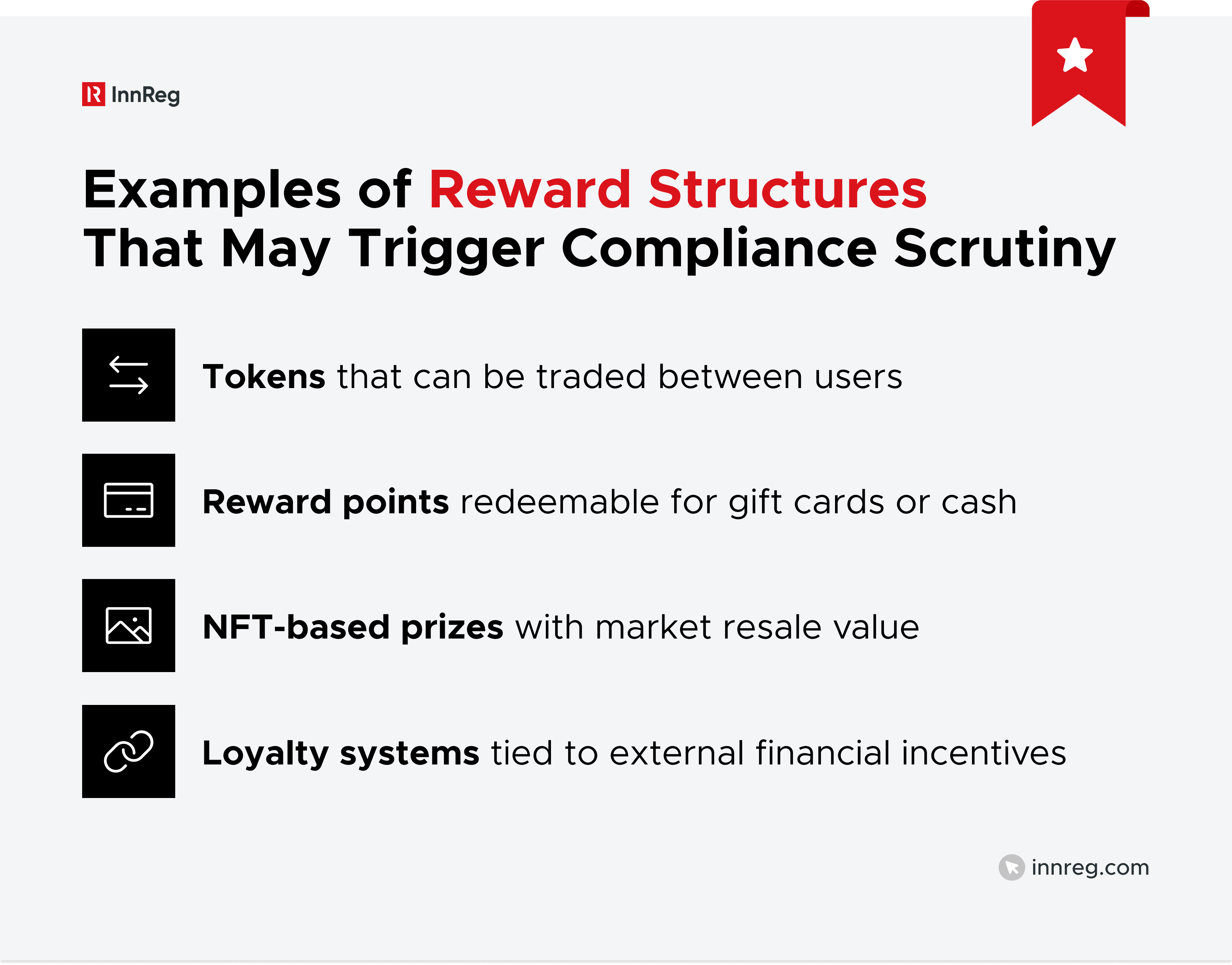

In-Game Rewards, Tokens, and Cash Equivalents

Not all in-game rewards raise regulatory concerns. But when those rewards have real-world value or liquidity, gaming compliance becomes a central issue. That includes any system where users can earn, win, or buy something that can be exchanged, sold, or redeemed outside the game.

What matters is not what the company calls the reward, but how users perceive, use, and exchange it. If players can treat it like money or convert it into money, regulators will likely treat it as value.

This is where fintech models often create unexpected risk. A budgeting app with a prize feature, for example, might resemble a sweepstakes. A savings app offering bonus tokens with retail value might be treated as prepaid access.

Skill-Based Games, Sweepstakes, and the Gray Areas

Skill-based games, sweepstakes, and hybrid mechanics often live in legal gray zones, where compliance risk depends on technicalities.

In most jurisdictions, skill-based games are exempt from gambling laws, but only if the outcome is truly determined by user skill, not chance. The tests vary: some states use a “predominant factor” test, while others apply a “material element” or “any chance at all” standard.

This means a game might qualify as skill-based in one state and as gambling in another. Sweepstakes carry their own rules. To avoid being treated as illegal lotteries, most require a “no purchase necessary” entry path, and some states require advance registration or bonding.

Legal Tests: Predominant Factor vs. Material Element

Regulators apply different legal standards to determine whether a game is one of skill or chance:

Predominant Factor Test

This is a more adaptable approach. If skill plays the biggest role in determining results, the game might not fall under gambling laws. New York, Texas, and Florida are among the states using this test.

For example, take a fantasy stock-trading app where users earn rewards based on how their portfolios perform over time. It could qualify as skill-based if the decisions players make matter more than random market shifts.

Material Element Test

This is stricter. If chance plays any meaningful role, the game may be considered gambling—even if skill is also involved. States like Arizona and Missouri apply this test.

Example: A game where users spin a wheel to win investment bonuses could trigger gambling concerns, even if the wheel is part of a broader skill-based experience.

—

Understanding which test applies in your target markets is essential. The same feature set can be compliant in one state and restricted in another. This is one reason fintech teams building gamified experiences need legal input early, especially when scaling across jurisdictions.

InnReg provides registration and licensing services to help fintech determine which licences to obtain →

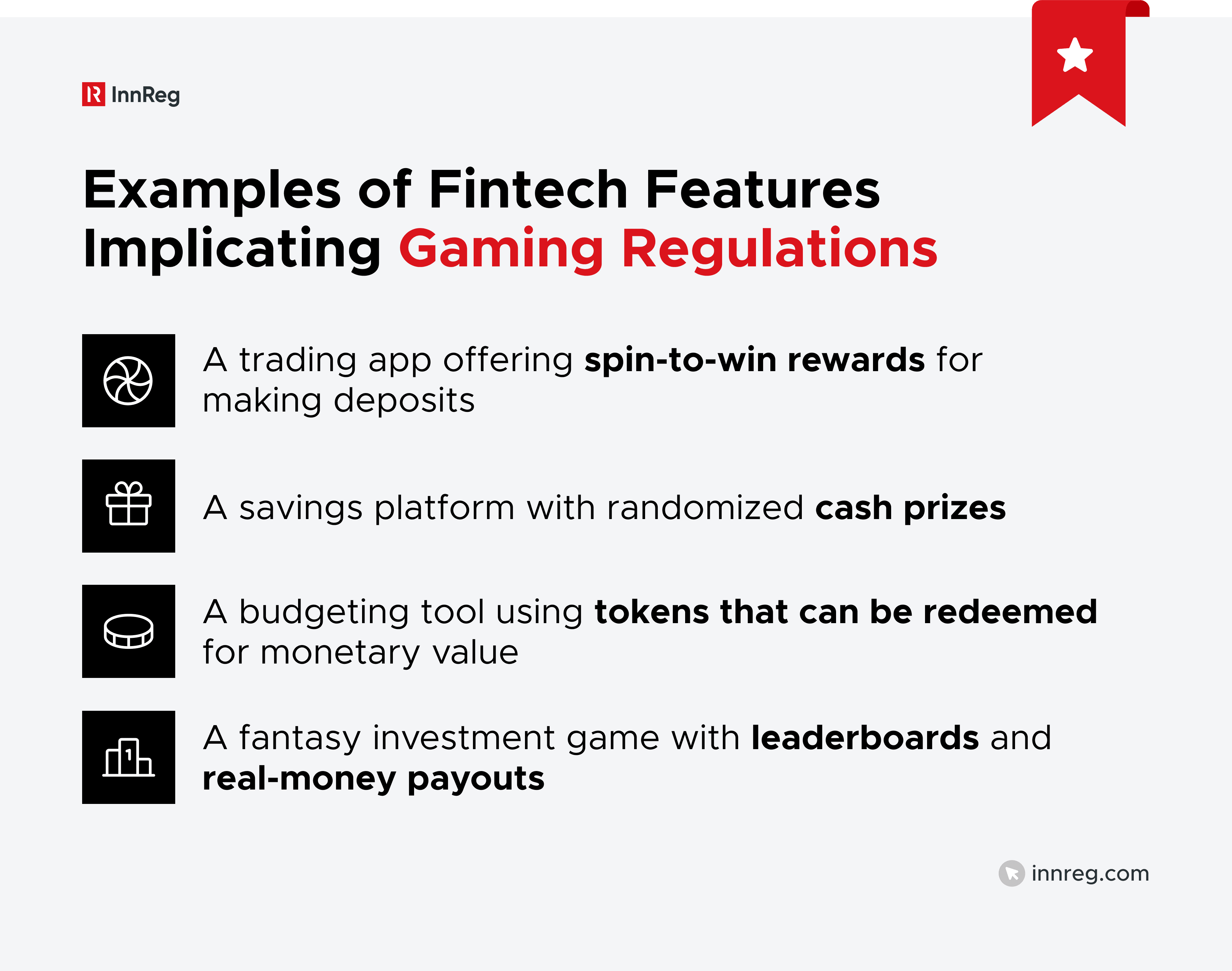

Examples of Models That Cross the Line

Some product designs unintentionally shift from engagement tools into regulated territory. These are not always obvious at the concept stage, but they often involve a combination of value, randomness, and user payment.

Features that may trigger gambling classification include:

Savings apps with randomized cash prizes: Even when structured like sweepstakes, these can resemble lotteries if entry depends on deposits and there’s no free alternative

Spin-to-win deposit bonuses: A trading app that offers a random bonus or stock reward in exchange for funding an account

Token rewards with external resale value: Platforms that issue tokens or NFTs which can later be sold in secondary markets

Fantasy investment contests with entry fees: Skill-based formats can raise gambling flags if they charge to enter and offer a prize pool

Although these models might not be outright violations, they generally demand structural tweaks, legal scrutiny, or licensing approaches. A growth feature that appears benign can pose actual regulatory threats when it isn't built on solid legal ground.

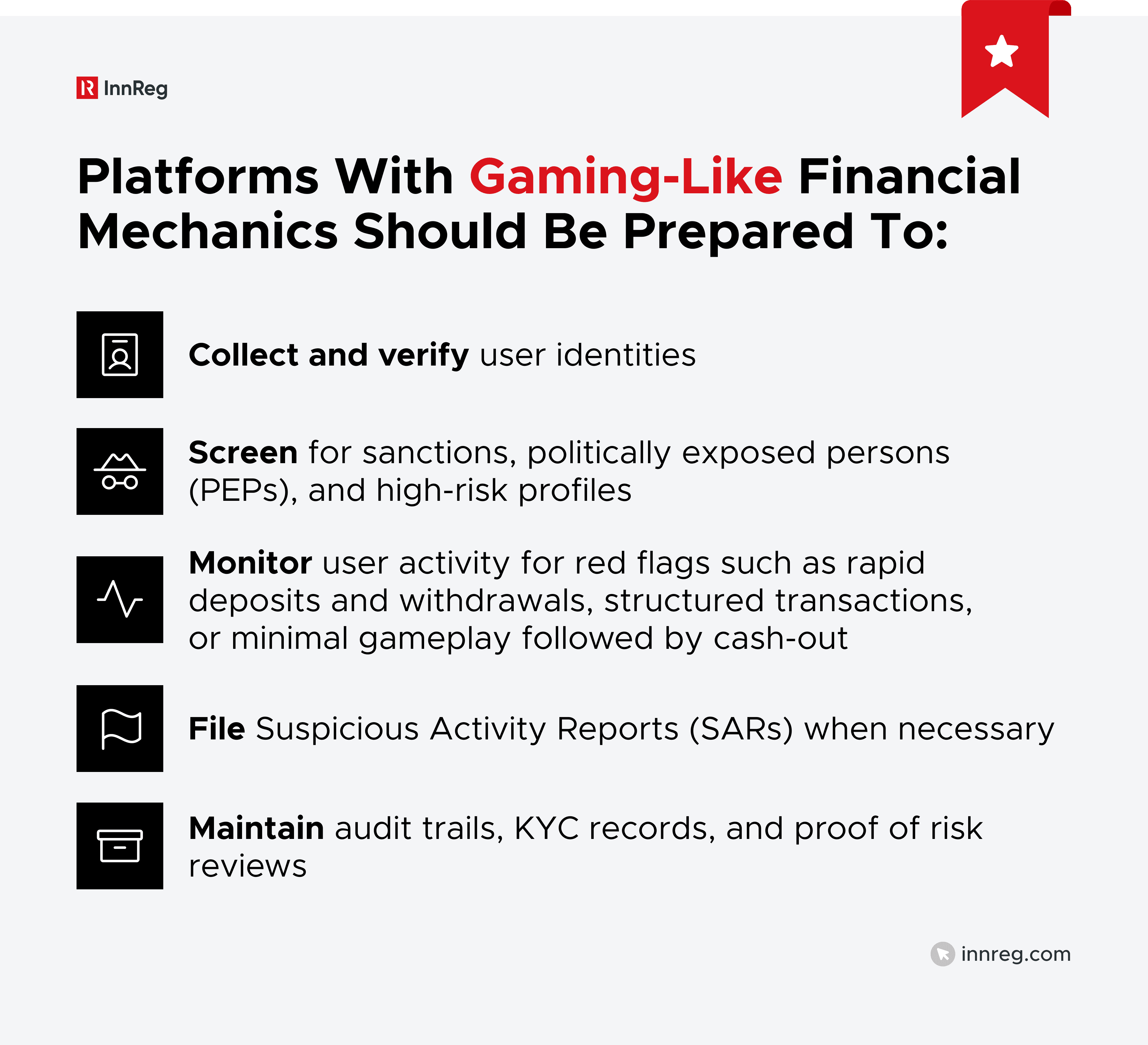

AML and KYC Expectations in Gaming Compliance

Once a platform involves real money, anti-money laundering (AML) and know your customer (KYC) obligations are no longer optional. Regulators and banking partners expect clear controls for identifying users, monitoring transactions, and flagging suspicious activity.

Learn how InnReg helps fintechs strengthen their KYC and AML efforts →

This is an area where fintechs commonly rely on compliance professionals or engage knowledgeable advisors at an early stage.

Payment partners can require an active AML program before permitting gaming-related transactions. At the same time, FinCEN sees numerous hybrid products as bound by Bank Secrecy Act (BSA) standards, even if the company disputes being a financial institution.

What FinCEN, Banks, and Vendors Expect

Banks, payment processors, and compliance vendors all review a product's risk level, especially where financial rewards or peer-to-peer value exchanges come into play.

What they are checking for:

Defined KYC and onboarding flows

AML policy documentation, including triggers for SARs

Transaction monitoring logic for identifying abuse, layering, or evasion

Geolocation controls to restrict access from high-risk or prohibited jurisdictions

Sanctions screening tools built into your user and transaction layers

Even if a product does not need a money transmitter license, these stakeholders might treat it like it does during onboarding, particularly if your platform handles deposits, rewards, withdrawals, or token transfers.

Holdup often happens when compliance documentation is vague or your risk story does not line up. Fintech teams that view compliance as just another launch checkbox, instead of a foundational piece, may end up in drawn-out vendor negotiations or lose access to essential services.

InnReg helps fintechs by providing vendor management services →

Additional resources: | |

|---|---|

See also:

Gamification in Financial Products: Where Regulators Draw the Line

Gamification can help make financial products more engaging, but it can also raise compliance concerns. Regulators are increasingly focused on how game-like features influence user behavior, especially when real money or financial risk is involved.

FINRA and SEC Focus Areas

Gamified interfaces are under growing scrutiny from FINRA and the SEC. Their concern is not the use of design patterns themselves, but their effect on user behavior, especially when they impact investment decisions or risk exposure.

Behavioral nudging | Frequent trading incentives | Misleading visual cues |

|---|---|---|

Does the interface prompt users to take more risk than they would on a neutral platform? | Are users pushed to make trades through rewards, badges, or streaks? | Do celebratory graphics create a false sense of gain or minimize the perception of financial loss? |

Regulators see these elements as potential forms of indirect financial advice or sales pressure. This holds particularly true when paired with real-money outcomes.

Read more on gamification and marketing compliance →

Crypto, NFTs, and GameFi: A New Frontier for Gaming Compliance

Fintech and gaming are colliding, and crypto complicates things further. Tokens, NFTs, and decentralized apps bring real-world value into what used to be purely virtual systems.

GameFi breaks down the walls between investing, playing, and making money. Regulators are focused on this area, particularly when platforms feature user wallets, staking options, or assets that can be bought and sold.

When Tokens and Wallets Trigger Financial Regulation

Wallets and tokens do not inherently create compliance issues. However, the ability for users to store, transfer, or withdraw value through a platform, especially when crossing platform boundaries, is treated by regulators as financial infrastructure.

Common triggers include:

Custody or storage of user-owned crypto assets

Ability to send tokens between users

Off-platform resale of in-game NFTs

Wallet integrations enabling cross-chain or fiat conversion

When these features exist, agencies may apply MSB rules, securities laws, or even banking-level requirements. For example, a token with a fluctuating market price and user investment may resemble a security.

Related resources: | |

|---|---|

AML, Securities Law, and OFAC Considerations

Most crypto platforms fall under AML requirements. If they work with wallets, tokens, or anything connecting crypto to fiat, and regulators expect an AML framework. This means that Identity verification is mandatory, as well as monitoring across crypto and cash, and screening for sanctions through sources like OFAC.

Utility tokens risk falling under securities law when they carry investment traits, gains, earnings, and governance that move money. What you label them doesn't matter to regulators. How they operate does.

Product and legal should dig into token allocation, user profit expectations, how tradable tokens are, and disclosure practices. These variables set the compliance risk level.

What an Effective Gaming Compliance Program Looks Like

Fintech platforms that touch chance, value, or user funds need internal systems that reflect their risk profile. This means aligning product, compliance, and engineering from day one.

Key components of an effective gaming compliance program:

Documentation: Formal policies covering AML processes, reward distribution, value transfer, and third-party oversight. Both regulators and partners want to see documented risk identification.

Role clarity: Clear ownership of compliance reviews and vendor management. Ambiguity here creates gaps fast.

Escalation paths: Defined responses to warning signs, e.g., account abuse, duplicate entries, vendor service problems, or fraud tied to rewards or digital asset transfers.

Vendor selection and review: Pick vendors who understand the regulatory landscape. Check their controls if they handle identity, payments, wallets, or randomization. Document your risk assessments and review them on a regular basis.

Testing and audits: Review your systems and vendor integrations and focus on randomization logic, value distribution, sanctions screening, and transaction monitoring.

—

Gaming compliance is a design constraint that affects product roadmaps, partner relationships, and launch timelines.

What looks like a minor engagement feature can create licensing requirements, trigger AML obligations, or block access to payment infrastructure.

The teams that handle this well bring legal and regulatory expertise into product discussions early, map out value flows before they're built, and design features with state-by-state variability in mind.

Ani is a Senior Compliance Consultant with over 10 years of experience in legal and regulatory compliance across fintech, RegTech, and cross-border payments. She has held roles at Remote and EY, with expertise in AML, GDPR, financial crime, and EU regulatory frameworks. She holds CAMS and CIPP/E certifications.

How Can InnReg Help?

InnReg is a global regulatory compliance and operations consulting team serving financial services companies since 2013.

We are especially effective at launching and scaling fintechs with innovative compliance strategies and delivering cost-effective managed services, assisted by proprietary regtech solutions.

If you need help with compliance, reach out to our regulatory experts today:

Related Articles

Featured LinkedIn Posts