iGaming Regulation: What Fintechs and Vendors Need to Know

iGaming regulation is rapidly evolving. For fintechs operating in or near this space, understanding the rules is mandatory.

Regardless of whether you're building a platform that handles real-money transactions, providing KYC tools to gambling operators, or enabling crypto-based games, you’re intersecting with a complex, high-risk regulatory environment.

This article breaks down how iGaming regulation works across key markets, especially in the US, EU, and UK, who the regulators are, when licensing is required, and what compliance obligations apply.

At InnReg, we help fintechs operating near iGaming navigate regulatory requirements across payments, AML, licensing, and ongoing compliance. Our team supports innovative financial products in complex, high-risk environments.

What is iGaming?

iGaming refers to online gambling activities where users wager real money on games of chance. This definition encompasses online casinos, poker rooms, sportsbooks, fantasy leagues, sweepstakes, and crypto-based betting platforms.

These products often rely on embedded financial services, such as digital wallets, payment processors, and customer identity verification.

For fintechs, the relevance is direct. If your product facilitates deposits, withdrawals, onboarding, or user authentication in an iGaming context, it is operating inside a highly regulated ecosystem, even if you’re not the gaming operator. The regulatory touchpoints are broad: AML, KYC, payment infrastructure, data handling, and more.

iGaming regulation applies to both the gambling side and the financial side of the product. This overlap is where most compliance challenges emerge. Misunderstanding where the lines are, or which regulators have jurisdiction, can lead to serious risk exposure.

iGaming Regulation in the US

In the US, iGaming regulation is governed at the state level. This creates a fragmented legal environment where what’s permitted in one state may be illegal in another. Today, only a handful of states have legalized full online casino gaming, while many more have legalized online sports betting.

If a company operates or supports iGaming platforms, the first question is always: “Which states are you targeting?” That answer determines which gaming license(s) are required, which regulators the platform will work with, and what compliance standards apply.

Regulators Governing iGaming in the US | ||

|---|---|---|

FinCEN | The Department of Justice | State Gaming Commissions |

Classifies certain iGaming operators as financial institutions subject to Bank Secrecy Act requirements | Enforces federal laws like the Wire Act and UIGEA when operators cross state lines or serve restricted markets. | Govern iGaming on a state level (e.g., New Jersey Division of Gaming Enforcement or the Pennsylvania Gaming Control Board ) |

iGaming companies must also comply with state-specific rules around geolocation, age verification, responsible gambling, AML, and technical standards.

In many cases, they must partner with a licensed land-based casino or gaming entity to operate legally within a state.

For fintechs and vendors supporting US-based iGaming, navigating this patchwork of state rules is a core compliance task, especially for products that process payments, hold customer funds, or help platforms meet AML obligations.

See how InnReg helps fintech develop AML compliance programs →

iGaming Regulation in the EU

Similar to the US, iGaming regulation in the EU is handled primarily at the national level. There is no single pan-European license. Each member state decides what types of online gambling are legal, who can offer them, and under what conditions.

Some markets are fully regulated, like Spain, Denmark, and the Netherlands. Others remain more limited or closed. Operators must obtain a local license to legally serve residents in most EU countries, and non-compliance can lead to fines, domain blocking, or blacklisting.

Regulators across the EU typically require:

Local licensing and reporting

AML and counter-terrorism financing controls

Player protection measures (including responsible gambling frameworks)

Data privacy compliance under GDPR

Technical audits and testing for game fairness

For fintechs and service providers working with EU iGaming platforms, the key is localization. Each country’s rules differ, and working with a licensed operator doesn’t automatically cover your product unless it’s been vetted under that country’s regime. This is especially important for payment systems, identity verification, and risk tech vendors.

The regulatory bar in most of the EU is high but clear. Fintechs entering these markets should build compliance strategies around the specific requirements of each target country.

iGaming Regulation in the UK

The UK regulates online gambling through a comprehensive framework that applies across multiple product types such as casinos, sportsbooks, poker platforms, and lotteries. All operators must be licensed by the UK Gambling Commission (UKGC) to legally serve players in the region.

The UKGC imposes high standards in key areas:

Anti-money laundering protocols

Customer identity checks and due diligence

Player safety and responsible gambling practices

Game fairness and transparent payouts

Marketing conduct and affiliate oversight

Regulators in the UK are both proactive and well-equipped. Firms that miss the mark can expect financial penalties, operational restrictions, or the loss of licensure. Recent enforcement has focused heavily on customer affordability, source-of-funds analysis, and real-time monitoring of risky behavior.

For fintechs working with UK iGaming firms, the compliance bar is high. Payment tools, KYC systems, and fraud controls must be aligned with UKGC expectations, particularly if your service interacts with player money or personal data.

iGaming Regulation Across the Globe

iGaming laws differ significantly. Some countries have built clear regulatory frameworks. Others still treat online gambling as illegal or unregulated. This inconsistency creates risk for both operators and fintech vendors involved in the ecosystem.

In Latin America, markets like Brazil, Colombia, and Peru are moving toward licensing structures.

Across much of Asia, however, online gambling remains heavily restricted, with countries like China and parts of India taking a strict stance.

Once favored for their ease of entry, Malta, Curaçao, and the Isle of Man are beginning to take a different direction. Curaçao, notably, is layering in new standards around anti-money laundering, identity checks, and regulatory disclosures.

Africa is mixed. Kenya, Nigeria, and South Africa allow online betting under domestic licenses. Others have yet to implement formal iGaming oversight.

For fintechs, fragmentation is the main concern. What’s legal in one country may trigger enforcement in another. Supporting iGaming platforms across multiple jurisdictions means understanding the rules market by market.

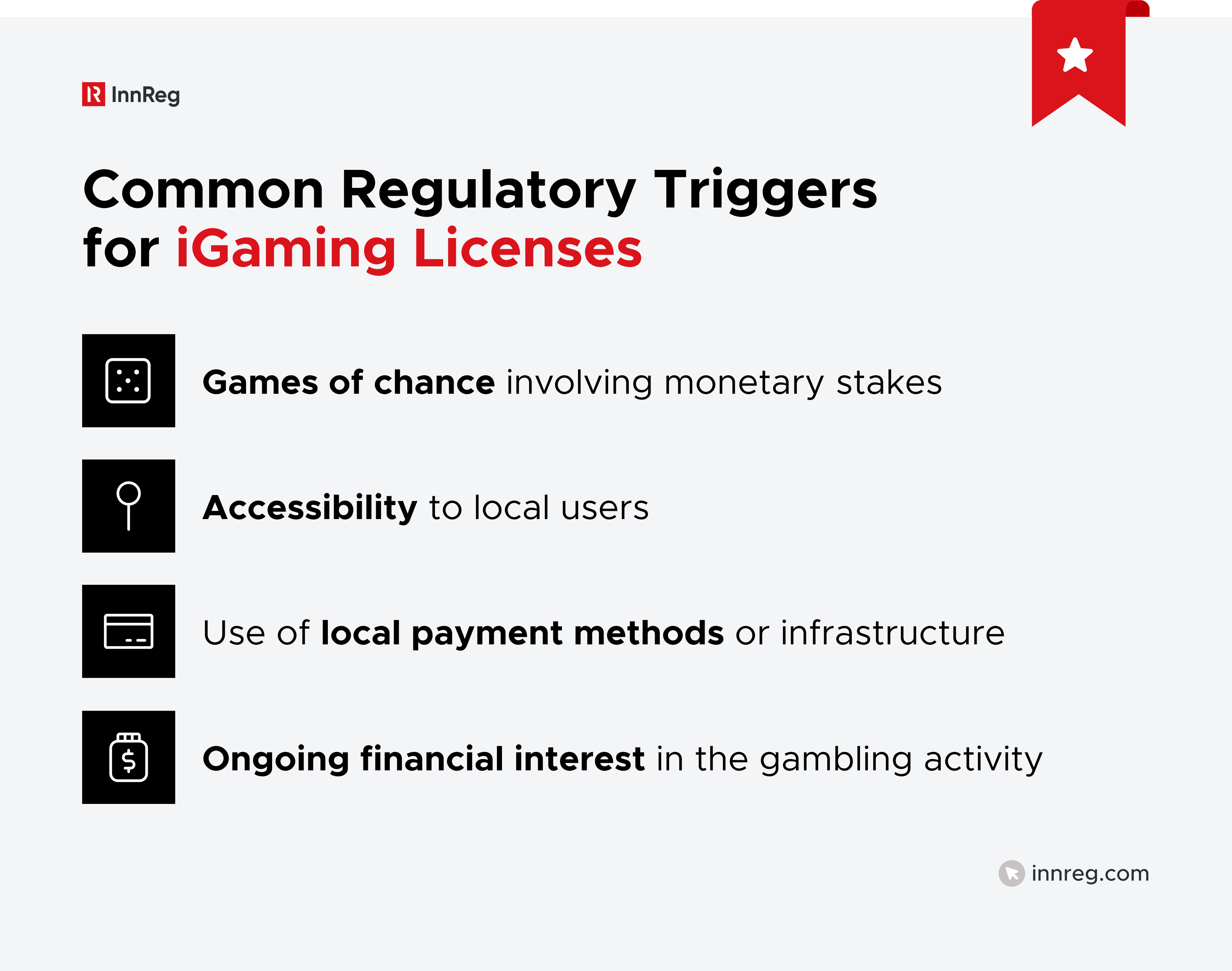

When Is an iGaming License Required?

An iGaming license is required anytime a company offers real-money gambling services in a jurisdiction where such activity is regulated. This applies to operators directly running the platform and, in some cases, to third parties involved in core compliance or financial functions.

To legally operate in markets like the UK, the Netherlands, or New Jersey, a business must be licensed or aligned with a licensed operator. Licensing requirements can extend to vendors and affiliates, depending on how directly they participate in the gambling operation..

For fintechs, the key is understanding how regulators define “offering” gambling services. Handling funds, verifying users, or powering bets may be enough to draw regulatory attention. Licensing obligations aren't limited to operators alone and can extend to critical vendors embedded in the transaction flow.

Core Compliance Obligations Under iGaming Regulation

Operating in regulated iGaming markets means ongoing compliance obligations that extend far beyond licensing. Regulators expect companies to build and maintain controls across:

See also:

AML, KYC, and Transaction Monitoring

AML (Anti-Money Laundering) and KYC (Know Your Customer) requirements are central to iGaming compliance. Regulators treat gambling platforms, in particular those handling real money, as financial institutions for AML purposes. That means full adherence to local and international financial crime standards.

At a minimum, regulated operators are expected to:

Perform customer identity verification before allowing deposits or gameplay

Monitor transactions for suspicious patterns

Maintain audit trails for reviews and regulatory inspections

File reports for high-risk activity (e.g., SARs or equivalent)

AML responsibility regularly extends to third-party vendors. Those involved in onboarding, payment handling, or behavioral risk screening are rarely seen as neutral infrastructure. This means that fintechs will be held accountable and fall under AML obligations tied to the iGaming businesses they support.

Expectations vary by jurisdiction. The UK, for instance, follows a risk-based approach aligned with FATF guidelines. The US applies Bank Secrecy Act standards through FinCEN.

Other countries apply local AML regimes that borrow from international frameworks. Regardless of region, regulators look closely at how operators and their partners identify, assess, and mitigate money laundering risks.

Additional Resources: | |

|---|---|

Need help with fintech compliance?

Fill out the form below and our experts will get back to you.

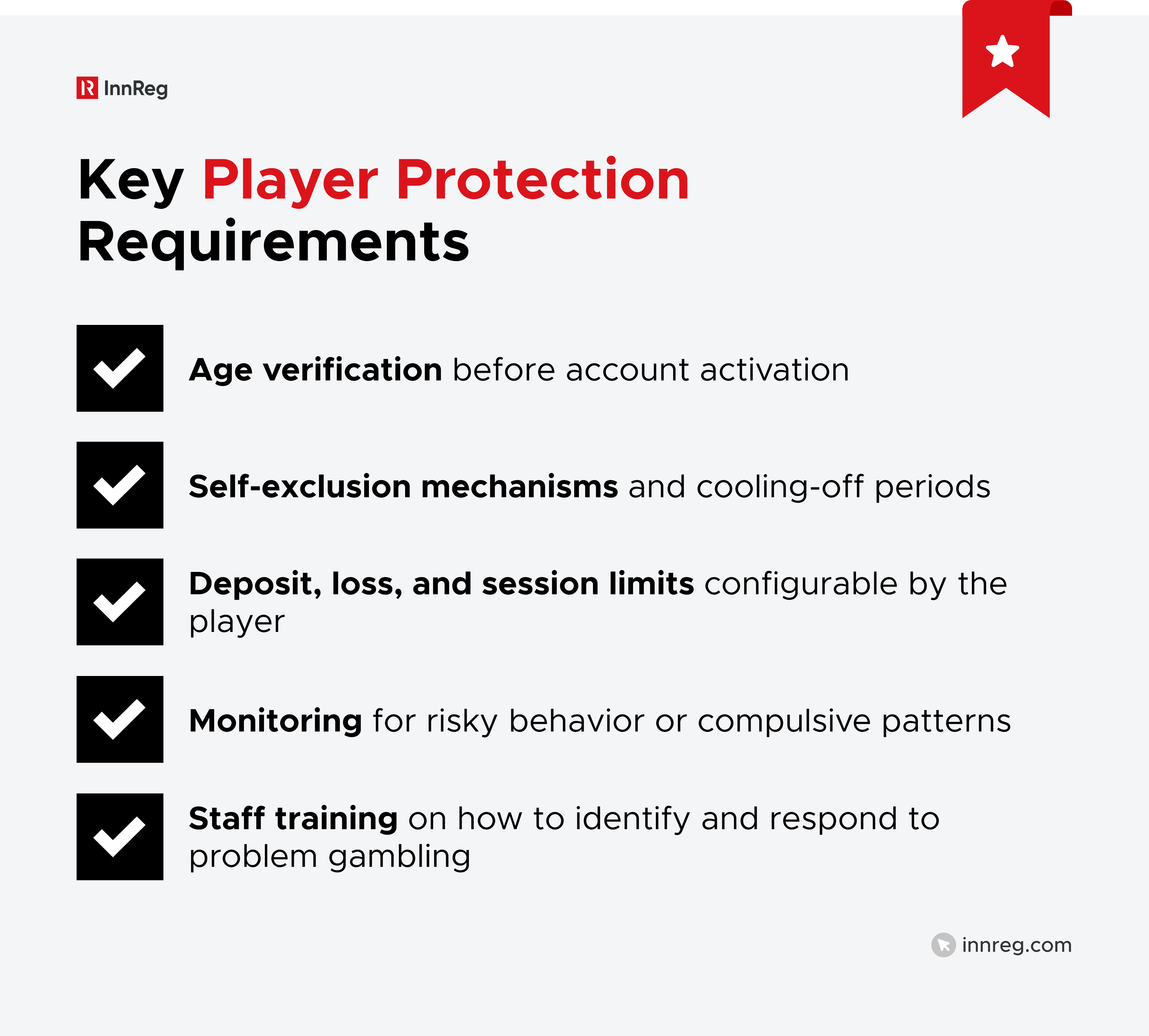

Player Protection and Responsible Gambling Controls

Most iGaming regulators expect operators to take clear steps to reduce player harm. These aren’t just policy items. They’re part of ongoing compliance oversight.

Fintechs that contribute to user experience, onboarding, or risk monitoring may be pulled into these controls, even if they’re not the operator. Tools that automate session tracking, trigger alerts, or handle identity screening are increasingly evaluated under responsible gambling requirements.

Enforcement activity is growing in this area. In the UK, operators have faced multi-million-pound fines for failing to intervene when players showed signs of gambling harm. Similar pressure can be perceived in Europe and emerging markets.

Payment Compliance and Banking Access

In iGaming, payments draw close regulatory attention. Authorities want a clear picture of how funds enter, move, and exit the system and who’s responsible at each point. This applies equally to operators and the fintech companies powering the infrastructure behind them.

iGaming Payments Common Points of Friction | ||

|---|---|---|

Banking Partners | Payment Processors | Cross-Border Flows |

May be hesitant to support gambling-related businesses | Must comply with gambling-specific rules, including UIGEA in the US | Can raise flags, especially in jurisdictions with restrictions or blacklists |

Oversight isn’t limited to one step. Platforms are expected to track deposits, manage withdrawals, and document everything.

This expectation also extends to fintech providers who build the tools that move, track, or reconcile funds.

Real-money integrations, especially in the US, can trigger legal duties under laws like UIGEA, which prohibit support of unauthorized gambling payments. If a provider misses key compliance flags, such as a flawed routing path or insufficient audit trail, it won’t be just the gaming commission asking questions. Banking regulators may follow quickly.

See how InnReg helps payment services companies navigate compliance →

Reporting, Taxation, and Technical Standards

Getting licensed is just the start. Regulatory upkeep involves regular submissions, transparent accounting, and system safeguards that support oversight.

Tax rules aren’t uniform. For example, the UK’s model revolves around gross revenue, while other regions rely on fixed payments or usage-based levies. In countries such as Italy, tax enforcement is particularly active.

On the technical side, regulators want proof. Random number generators need certification. Data in motion must be encrypted. And every report? It has to be filed in the right format, through the right channel, on time.

If a vendor touches financial data or user activity, they’re in scope. Tools supporting payments or compliance reporting may face direct oversight or need to feed local databases. In many cases, passive infrastructure isn’t really passive at all.

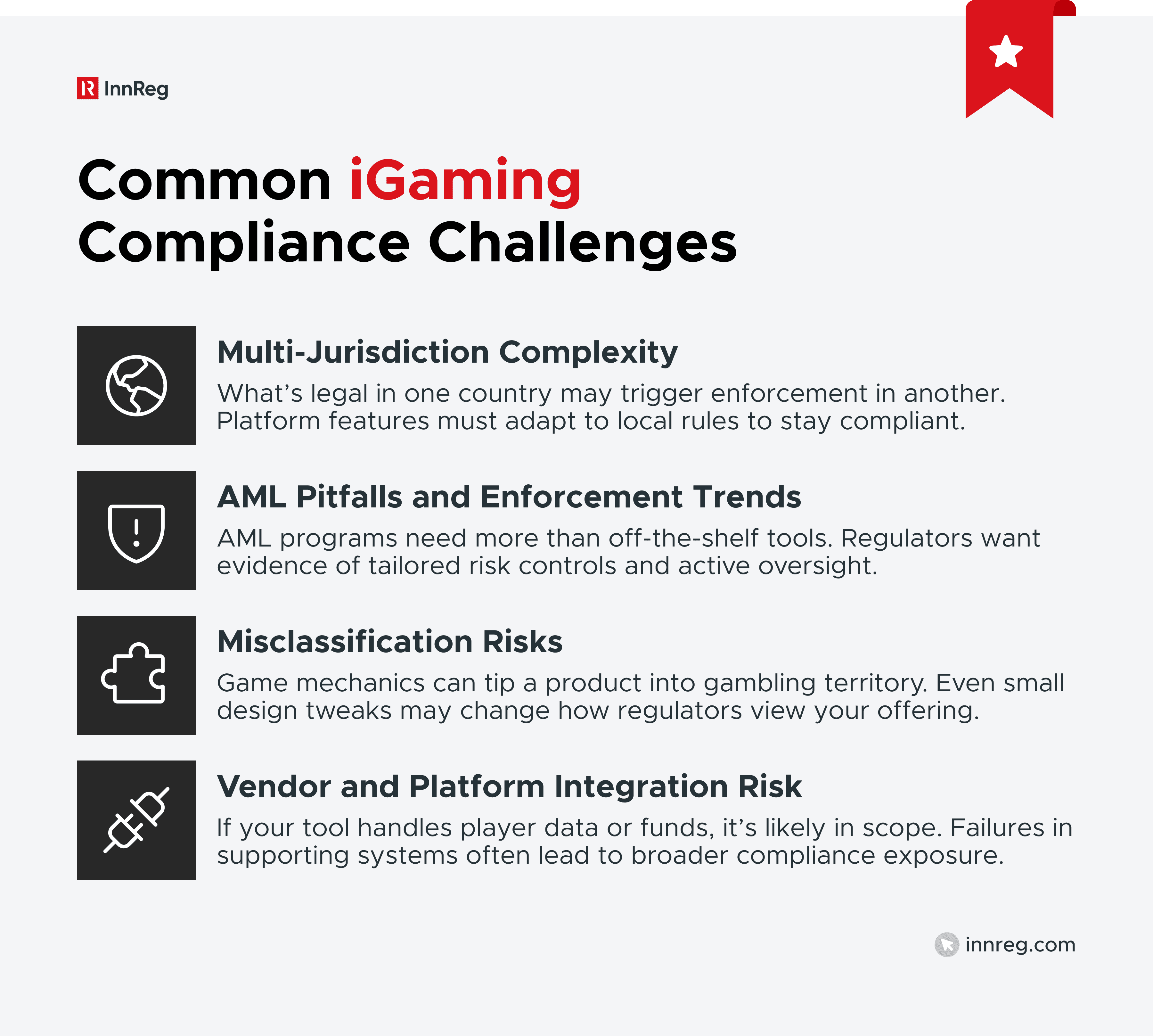

Common iGaming Compliance Challenges

Compliance challenges in iGaming rarely come one at a time. Most operators and vendors run into issues tied to jurisdictional overlap, AML enforcement, product classification, or third-party integrations.

Multi-Jurisdiction Complexity

Operating in multiple markets sounds like scale, but in iGaming, it often means compliance confusion. What’s legal in one country, or even one state, may be restricted or redefined elsewhere.

Platform features that are permitted in the UK might trigger enforcement in Germany or require a license in Ontario. Even seemingly minor differences, like terminology or payout structures, can shift how a regulator classifies the product.

Fintechs supporting iGaming need to adjust to local rules because what qualifies as compliant in the UK may cross a line in Germany.

AML Pitfalls and Enforcement Trends

AML obligations in iGaming go beyond surface-level controls. Authorities expect programs to demonstrate thoughtful design, proportional response mechanisms, and operational accountability.

Reliance on generic or pre-configured tools, without tailored oversight, is a recurring issue in enforcement actions.

For vendors, proximity to money matters. Whether it’s a wallet integration, a fraud rules engine, or a data feed, if the product supports player activity, regulators may expect you to show your part in the compliance process.

See how InnReg helps fintechs build effective KYC and AML compliance programs →

Misclassification Risks (Skill vs. Chance)

One of the more overlooked regulatory triggers is how a product is classified. Many gambling laws draw a line between games of skill and games of chance, and where your product lands on that spectrum has serious legal implications.

What passes as skill-based in one region might be treated as chance-based betting just across the border. Subtle elements like random outcomes, prize mechanics, or game pacing can carry significant legal weight.

For fintechs involved in onboarding, payments, or risk scoring, these classification differences matter. If your product supports a game that’s redefined mid-market, you may find yourself unexpectedly within gambling oversight and out of compliance.

Vendor and Platform Integration Issues

Some of the biggest compliance risks come not from operators themselves but from the systems they rely on.

When fintech tools handle deposits, verify players, or trigger risk checks, they move closer to the regulatory spotlight.

The more embedded a product becomes in real-money activity, the more likely it is to be treated as part of the compliance chain. This includes payment gateways, KYC platforms, fraud engines, and even customer messaging systems tied to gaming behavior.

An integration that silently fails or overlooks a flag can create exposure across the stack. In many markets, regulators are looking past the license holder and asking how vendors uphold their piece of the puzzle.

How Fintechs and Service Providers Fit Into iGaming Regulation

iGaming compliance isn’t limited to operators. Vendors that touch money, identity, or player activity often find themselves within scope.

Payments, Wallets, and Money Movement

Fund movement brings scrutiny. Wallet tools, transactional APIs, and backend payment services all sit close to the regulatory line. In markets like the US, UIGEA puts payment providers on the hook for blocking illegal gaming activity. Other regions may demand reconciliation logs, alerts for risky behavior, or live data access.

See also:

Identity, Fraud, and Risk Tech

User verification systems, behavioral monitoring tools, and risk engines no longer operate in the background. KYC modules, fraud detection software, and player scoring algorithms are now seen as integral to regulatory compliance.

When these tools surface issues, like suspicious deposits or signs of problem gambling, their outputs often inform real-time decisions that impact both users and the business.

Detection alone isn’t enough in the eyes of most regulators. They expect follow-through: action taken, personnel involved, and documentation showing how the issue was handled.

Vendors that feed into these systems, especially those tied to payments or player risk, may be called to demonstrate their contribution to the compliance process.

Crypto Considerations in iGaming

Even where tokens aren’t explicitly banned, they raise AML, custody, and volatility concerns. Jurisdictions like the UK and the US expect the same level of scrutiny as fiat payments. Some regulators also require full traceability of on-chain activity, adding pressure on fintechs providing wallet or settlement support.

See how InnReg helps crypto and blockchain fintechs →

Emerging Markets and Shifting Regulatory Trends

New markets are opening. Older ones are tightening. For fintech vendors and infrastructure providers, that means navigating a fast-moving patchwork of rules, enforcement styles, and political agendas.

Brazil, India, Europe, and Other Key Shifts

The regulatory picture varies widely across the globe

Brazil is formalizing its betting rules, but implementation is a work in progress.

In India, compliance obligations hinge on location, and state lines determine legality. Across the EU, consistency is starting to fray: the Dutch are speeding up KYC processes, while Swedish regulators are watching how users behave.

Adapting to these differences requires more than cosmetic updates. Many platforms find themselves reworking how core systems function.

Crackdowns on Offshore Operators

Across markets like the UK, Australia, and several Asian countries, enforcement against unlicensed gambling activity is becoming more assertive.

It’s no longer just the operators under the spotlight: vendors, payment partners, and even affiliates are being pulled in.

In many cases, simply supporting the ecosystem, processing transactions, managing player data, or powering account setup can bring regulatory attention. Authorities are increasingly treating these roles as active contributions to illegal operations.

—

iGaming regulation continues to evolve, and it’s pulling fintech infrastructure along with it.

From payments and KYC systems to crypto wallets and fraud engines, supporting technologies are now seen as part of the compliance surface.

For fintechs operating near real-money play, that means regulatory exposure isn’t just possible but likely. Whether the platform is regulated directly or not, the systems underneath it are being asked to meet the same standards.

Ani is a Senior Compliance Consultant with over 10 years of experience in legal and regulatory compliance across fintech, RegTech, and cross-border payments. She has held roles at Remote and EY, with expertise in AML, GDPR, financial crime, and EU regulatory frameworks. She holds CAMS and CIPP/E certifications.

How Can InnReg Help?

InnReg is a global regulatory compliance and operations consulting team serving financial services companies since 2013.

We are especially effective at launching and scaling fintechs with innovative compliance strategies and delivering cost-effective managed services, assisted by proprietary regtech solutions.

If you need help with compliance, reach out to our regulatory experts today:

Related Articles

Featured LinkedIn Posts