What Is Insider Trading in Fintech? A Practical Guide

Most discussions of insider trading focus on high-profile cases. Far less attention is paid to how the risk actually arises inside day-to-day fintech operations.

Yet insider trading risk often grows out of ordinary situations. Early access to earnings data, upcoming partnerships, platform metrics, or strategic plans can quickly become a problem when that information is not public, and someone trades or shares it.

In this article, you’ll get a clear breakdown of insider trading. We’ll explain what it actually means, how it shows up in modern financial services companies, and why it matters for fintech teams trying to build and scale.

At InnReg, we help fintechs, broker-dealers, and RIAs manage insider trading risk with practical compliance support. From registration and regulatory strategy to policies, pre-clearance workflows, training, and surveillance oversight, our team helps you build controls that fit how you operate.

What Is Insider Trading?

Insider trading occurs when someone buys or sells securities while in possession of important information that is not available to the public. The concern is not the trade itself, but the use of an information advantage that the rest of the market doesn’t have.

Regulators focus on this type of information because of its potential to influence investment decisions. They refer to it as material nonpublic information, which is basically information that a reasonable investor would care about when deciding whether to buy or sell.

This often includes:

Earning results

Pending acquisitions

Major regulatory developments that have not yet been disclosed

To see how this plays out in practice, consider a common scenario. An employee learns that their company is about to report strong quarterly results. Before that information becomes public, they buy shares or tip off a friend. At that moment, the trade is driven by an information advantage that the rest of the market doesn’t have, which is where insider trading concerns arise.

Is Insider Trading Illegal?

Insider trading is often illegal, but not every trade made by an insider is a violation.

The legality depends on:

How the information was obtained

Whether it was material and nonpublic

What was done with the information

Illegal insider trading happens when someone trades securities while they have material nonpublic information and a duty not to use or share that information. That duty can come from an employment role, a contractual relationship, or a position of trust.

Here is a simple example. A founder knows their company is about to announce a major partnership that will likely move the stock price. If they buy shares before the announcement, that trade is likely illegal. The same issue arises if they tip a friend or family member, and that person trades instead. Both sides can face consequences.

That said, not every trade made by an insider is illegal. Executives, employees, and large shareholders are often allowed to trade their company’s stock, as long as they do so without relying on material nonpublic information and follow the required disclosure rules.

Legal vs. Illegal Insider Trading

The difference between legal and illegal insider trading usually shows up in the details, not the labels. Two people can place similar trades, and only one of them creates a regulatory issue. What matters is the context around the decision.

Aspect | Legal Insider Trading | Illegal Insider Trading |

|---|---|---|

Timing of the trade | Occurs during approved trading windows, after information has been publicly disclosed | Occurs before material information becomes public |

Access to information | Trader does not possess material nonpublic information at the time of the trade | Trader has access to confidential, market-moving information |

Use of controls | Trade follows company policies, pre-clearance steps, and reporting requirements | Trade bypasses or ignores internal controls and restrictions |

Disclosure and reporting | Required disclosures are filed accurately and on time | Disclosures are missing, delayed, or intentionally avoided |

Information sharing | No tipping or sharing of sensitive information | Information is shared with others who trade on it |

Regulatory view | Generally permitted when rules are followed | Considered a violation and subject to enforcement |

For fintech teams, this comparison has practical implications. Many enforcement actions begin with routine activity that lacks clear guardrails. By defining trading windows, approval requirements, and escalation paths early, companies reduce uncertainty and make it easier for employees to pause before a trade turns into a compliance issue.

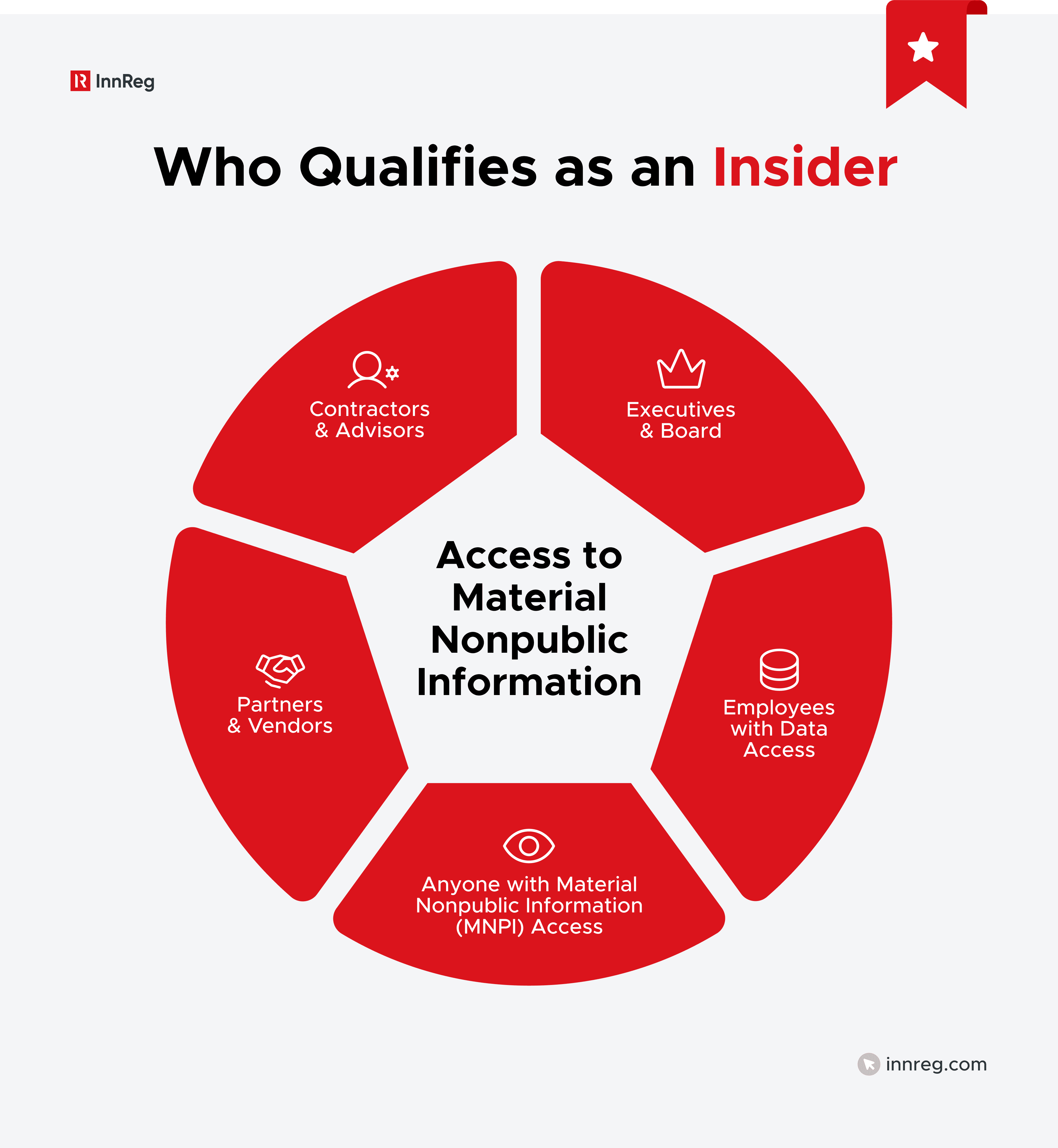

Who Qualifies as an “Insider?”

An insider can be anyone with access to material nonpublic information and a duty not to misuse it. This often extends well beyond senior leadership. Product managers, engineers, finance teams, and data analysts may all encounter sensitive information before it becomes public.

Insiders aren't limited to people inside the company. Contractors, consultants, auditors, legal counsel, and vendors may receive confidential information as part of their work. Even short-term or limited access can create obligations when the information is market-sensitive.

How Does US Law Regulate Insider Trading?

Insider trading in the United States is shaped by a mix of federal securities laws, court decisions, and regulatory enforcement. Rather than a single standalone rule, the framework focuses on how information is used and whether trading activity undermines fair markets.

SEC Rule 10b-5 and the Securities Exchange Act

Most insider trading cases in the US trace back to the Securities Exchange Act of 1934 and, in particular, SEC Rule 10b-5. This rule makes it unlawful to use deceptive or manipulative practices in connection with buying or selling securities.

Rule 10b-5 is about honesty and fair dealing. If someone trades based on material nonpublic information and that conduct involves deception or a breach of trust, regulators may view it as a violation of this rule.

For example, if an employee trades shares after quietly learning about a pending merger, that trade can fall under Rule 10b-5 because it relies on confidential information that was not available to the public.

The rule is flexible by design, which allows regulators to apply it across many situations, including modern fintech and digital asset markets.

The “Classical” vs. “Misappropriation” Theory

The US insider trading law is built around two main legal theories. Both focus on the misuse of information, but they apply in slightly different situations.

The classical theory applies when someone trades securities of their own company while holding material nonpublic information. Think of a corporate officer or employee who knows about upcoming earnings or a merger and trades before the news is public. The issue here is a breach of duty to the company and its shareholders.

The misappropriation theory is broader and often more relevant for fintech teams. It covers situations where someone trades using confidential information that doesn’t belong to their own company. For example, a registered investment advisor learns sensitive deal information from a client and trades in a related company’s stock. Even though they aren't insiders of that company, using the information that way can still trigger liability.

These theories matter because they expand who can be held accountable. Anyone who misuses confidential information obtained through trust or access can fall within the reach of regulators.

Role of the SEC, DOJ, and FINRA in Insider Trading

Insider trading enforcement in the US involves several regulators, each with a distinct role.

Securities and Exchange Commission (SEC): The SEC focuses on civil enforcement. The SEC investigates suspicious trading, brings lawsuits, and seeks penalties such as fines, repayment of profits, and officer or director bars. Many insider trading cases start here.

Department of Justice (DOJ): The DOJ handles criminal enforcement. When insider trading involves intentional misconduct or significant harm, the DOJ may pursue criminal charges, which can result in large fines or prison sentences.

FINRA: This regulator oversees broker-dealers and registered individuals. FINRA monitors trading activity, conducts exams, and enforces industry rules. It can take action directly or refer cases to the SEC or DOJ.

For regulated fintech companies, this shared enforcement model means insider trading issues can attract attention from more than one authority at the same time. Clear policies and early controls help mitigate the risks.

See also:

Key Compliance Rules Related to Insider Trading

Insider trading rules don’t live in isolation. They show up through reporting requirements, trading controls, and ongoing obligations that shape how firms manage information and employee activity.

Need help with fintech compliance?

Fill out the form below and our experts will get back to you.

Insider Trading Reporting Obligations (Forms 3, 4, and 5)

Certain insiders are required to publicly report their trading activity through SEC filings known as Forms 3, 4, and 5. These filings give regulators and investors visibility into when insiders acquire or sell company securities.

Form 3 is filed when someone first becomes an insider, such as when they join a company as an executive or director. It establishes their initial ownership position.

Form 4 is used to report most changes in ownership, including purchases and sales, and it's generally due within two business days.

Form 5 is an annual filing that captures certain transactions that were exempt from earlier reporting or not required to be reported immediately.

For companies, these filings are more than paperwork because they often become a focal point during exams and investigations. When reports are late or inaccurate, they can raise red flags and prompt closer scrutiny. Clear processes that define who must file, when filings are due, and how trades are tracked help mitigate that risk before it escalates.

Rule 10b5-1 Trading Plans and the 2023 SEC Amendments

Rule 10b5-1 trading plans are designed to let insiders trade company stock without raising insider trading concerns. Under these plans, trades are scheduled in advance, at a time when the insider does not have access to material nonpublic information.

For example, an executive might establish a plan that automatically sells a predetermined number of shares each quarter. Once the plan is in place, trades happen according to the preset instructions, even if the executive later comes into sensitive information.

In December 2022, the SEC adopted amendments to Rule 10b5-1, with key compliance requirements taking effect in 2023. The changes added cooling-off periods before trades can begin, required new disclosures, and limited overlapping plans. The goal was to reduce abuse and increase transparency.

For companies, this means trading plans now require closer review and clearer documentation than they did in the past.

Trading Blackout Periods and Pre-Clearance Protocols

Trading blackout periods are times when insiders are restricted from buying or selling company securities. These periods often surround earnings releases, major transactions, or other events where sensitive information is being finalized.

Pre-clearance protocols add another layer of control. Before placing a trade, an employee or executive must get approval from compliance or legal. This helps catch situations where someone may not realize they have material nonpublic information.

For example, a product lead involved in confidential partnership talks might think a personal trade is harmless. A pre-clearance review can flag that risk and pause the trade until the information becomes public.

Common Insider Trading Scenarios and Red Flags

Insider trading issues often start with small, everyday situations. Knowing the most common scenarios and warning signs helps teams spot problems early, before they turn into investigations or enforcement actions.

Tipping and Tippee Liability

Insider trading does not always involve placing a trade yourself. Sharing confidential information with someone else, known as tipping, can create just as much risk. If the person who receives the tip trades on that information, both parties can face consequences.

For example, an employee casually mentions upcoming earnings results to a friend. If that friend buys or sells shares before the information becomes public, regulators may treat both the employee and the trader as responsible.

This is why informal conversations matter. Texts, emails, and offhand comments can all become evidence if they involve material nonpublic information. Training teams to pause before sharing sensitive details is one of the simplest ways to mitigate tipping risk.

Trading Ahead of Earnings or M&A Activity

Trading activity around earnings announcements or mergers and acquisitions is one of the most common insider trading red flags. These events often involve information that can move markets quickly once it becomes public.

Consider a team member who knows a merger is close to being announced. If they sell shares before the deal is disclosed, that timing alone can attract regulatory attention. The same concern applies to buying shares ahead of strong earnings that have not yet been released.

Even when there is no intent to do anything wrong, the appearance of trading ahead of major events can raise questions. That’s why blackout periods and clear approval processes are especially important during earnings cycles and deal activity.

See also:

Misuse of Confidential Partnership or Platform Data

Fintech companies often handle sensitive information about partners, customers, and platform activity. When that data is not public, using it for trading purposes can create insider trading risk.

For example, a team member may see early metrics showing a surge in user activity tied to a new partnership. If they trade based on that insight, even if the data feels operational rather than financial, regulators may still view it as material nonpublic information.

This risk is not limited to employees. Vendors or advisors with access to platform data can also create exposure if controls aren't clear. Limiting access, tracking who sees sensitive information, and reinforcing how that information can and cannot be used help mitigate these issues.

Shadow Trading and Cross-Company MNPI Use

Shadow trading happens when someone uses nonpublic information from one company to trade in a related company’s securities. Even if the trade is not in the company that provided the information, the risk can still be there.

For example, an employee learns about a major supplier issue at their company. Instead of trading their own company’s stock, they trade in a key partner or competitor they believe will be affected. That particular use of confidential information can still raise insider trading concerns.

This scenario matters for fintech teams that operate in connected ecosystems. Partnerships, shared infrastructure, and overlapping markets can create indirect trading risks that are easy to overlook without clear guidance and training.

4 Examples of Insider Trading Cases

Real cases help show how insider trading rules are applied outside of textbooks. These examples highlight how different types of information, roles, and decisions have led to enforcement, even when the facts were not always obvious at first glance.

1. Martha Stewart and ImClone

The Martha Stewart case is one of the most well-known insider trading examples, even though it did not involve trading based directly on inside information. The issue centered on how information was used and how actions were explained afterward.

Stewart sold shares of ImClone Systems after learning that the company’s CEO was selling his stake ahead of negative FDA news. While she was not charged with insider trading itself, the case focused on obstruction and making false statements during the investigation.

The takeaway is important for compliance teams. Even indirect access to nonpublic information, and how someone responds once regulators start asking questions, can lead to serious consequences. Transparency and accurate recordkeeping matter just as much as the trade itself.

2. Raj Rajaratnam and Galleon Group

The Raj Rajaratnam case is often cited as a clear example of large-scale insider trading. Rajaratnam, the founder of hedge fund Galleon Group, was convicted for trading on confidential information obtained from corporate insiders and industry contacts.

In this case, the issue was not accidental access or poor controls. It involved an ongoing pattern of seeking out and using nonpublic information about earnings, acquisitions, and company performance. Many of the conversations were recorded, which made the misuse of information difficult to dispute.

For compliance teams, the lesson is straightforward. Insider trading enforcement is not limited to single trades or isolated decisions. Repeated use of confidential information, even when it comes through informal networks, can quickly escalate into serious criminal exposure.

3. Netflix Engineers Case

The Netflix engineers' case showed how insider trading risk can extend beyond executives and finance teams. In this situation, employees traded Netflix stock after learning confidential information about subscriber growth before it was publicly released.

The information didn’t come from a boardroom or earnings call. It came from internal data that the engineers had access to as part of their jobs. When that data was used for personal trading, regulators treated it as material nonpublic information.

This case is a useful reminder for fintech companies. Insider trading risk is closely tied to data access. When employees can see performance metrics, customer trends, or usage data ahead of public disclosure, clear rules and training matter just as much as technical controls.

4. Coinbase and OpenSea Enforcement

Recent enforcement actions involving Coinbase and OpenSea highlighted how regulators are applying insider trading concepts to crypto and NFT markets. In these cases, employees were accused of using confidential information about upcoming token or NFT listings to trade ahead of public announcements.

At OpenSea, a former employee was charged for allegedly buying NFTs he knew would be featured on the platform’s homepage, then selling them after prices increased. The case was brought under wire fraud and money laundering theories tied to the misuse of confidential business information. In July 2025, a federal appeals court overturned the conviction due to flawed jury instructions, showing how enforcement approaches in digital asset markets are still evolving.

In the Coinbase-related case, individuals were charged for trading crypto assets based on the advanced knowledge of which tokens would be listed next. Together, these cases signal that regulators expect firms to manage access to sensitive listing, product, and platform information, even as new asset classes continue to develop.

See also:

Insider Trading Risks in Crypto, NFTs, and Emerging Asset Classes

As financial products evolve, insider trading risk has not gone away. It has simply taken new forms. Crypto, NFTs, and other emerging asset classes raise familiar questions about information access, timing, and fairness, often without the guardrails found in traditional markets.

Insider Trading Concerns in Digital Tokens and NFTs

Digital tokens and NFTs create insider trading risk because a small group of people often knows what is coming before anyone else. Listing decisions, featured drops, protocol changes, and platform upgrades can all affect prices once they become public.

What makes this space harder is that roles are often less defined. Builders, community managers, and contractors may all have early access to market-moving information. Without clear rules around who can trade and when, these risks can spread quickly across a growing crypto or NFT team.

Applying Traditional Securities Laws to New Markets

One common misconception is that insider trading rules do not apply until regulators issue new, crypto-specific laws. In reality, enforcement often relies on existing securities laws and long-standing legal principles.

Regulators focus less on the label of the asset and more on the behavior. If someone uses nonpublic, market-moving information to trade, that conduct may still fall within current enforcement frameworks. This approach has allowed regulators to bring cases even as new asset classes emerge.

For fintech and crypto teams, the lesson is practical. Waiting for perfect regulatory clarity can create risk. Applying familiar controls around information access, trading restrictions, and oversight helps bridge the gap between innovation and existing legal expectations.

Compliance Priorities for Crypto and Web3 Teams

Crypto and Web3 teams often move fast, with small groups making decisions that can move markets. That speed makes it even more important to think about insider trading risk early, before habits and workflows are hard to change.

Clear rules around who can access sensitive information and when trading is allowed are a strong starting point. Teams should also think about how listing decisions, governance proposals, and protocol updates are shared internally and externally.

Training matters here, too. Many people entering Web3 come from non-traditional, regular finance backgrounds and may not realize how insider trading rules can apply. Simple guidance, practical examples, and clear escalation paths help teams mitigate risk without slowing innovation.

3 Ways Insider Trading Impacts Financial Services and Fintech

Insider trading is not just a legal issue. For financial services and fintech companies, it affects trust, market credibility, and how regulators view the business. Even a single incident can have ripple effects well beyond the trade itself.

1. It Erodes Market Integrity

Markets work because participants believe prices reflect publicly available information. When insider trading occurs, that balance breaks down, giving some participants an information advantage that the rest of the market does not have.

Over time, this behavior distorts pricing and weakens confidence in how markets function. If investors believe outcomes are driven by who knows what, rather than by fair disclosure, participation drops. That is a problem for any financial system that depends on trust.

For fintech platforms, the impact can be immediate. A perception that insiders or connected parties are trading on nonpublic information can raise questions about data controls, internal governance, and whether the platform treats users fairly. Even without formal enforcement, that reputational damage can be hard to reverse.

2. It Damages Investor Confidence

Investor confidence depends on the belief that markets are fair and transparent. When insider trading comes to light, that belief takes a hit. People start to wonder whether the system is stacked in favor of those with special access.

This matters even more for fintech companies still building their reputations. If users or investors think insiders are benefiting from information others don’t have, trust erodes quickly. That loss of confidence can slow growth, affect valuations, and make future fundraising harder.

A single incident can also change how stakeholders view the company’s controls. Investors may ask tougher questions about data access, employee trading rules, and oversight. Once confidence is shaken, rebuilding it often takes far more effort than preventing the issue in the first place.

3. It Exposes Fintech Firms to Regulatory and Reputational Risk

When insider trading concerns surface, regulators rarely look at the trade in isolation. They examine the company’s policies, controls, and culture to understand how the situation was allowed to happen.

For fintech firms, this scrutiny can extend beyond the individuals involved. Regulators may question how sensitive information is shared, who has access to it, and whether the company took reasonable steps to manage trading activity. Even if the issue starts with one person, the firm often feels the impact.

Reputational risk follows closely behind regulatory attention. News of an investigation or enforcement action can affect partnerships, customer trust, and future licensing efforts.

Ultimately, addressing insider trading risk early, before it turns into a headline, is far less disruptive than responding after the fact.

Common Myths About Insider Trading

Insider trading is surrounded by a lot of assumptions that do not hold up in real enforcement cases. These myths can give teams a false sense of comfort and lead to decisions that create unnecessary risk.

Myth #1: Insider Trading Only Applies to Public Company Executives

This is one of the most common misunderstandings. Insider trading rules aren't limited to CEOs, CFOs, or board members of public companies.

Anyone who has access to material nonpublic information can be treated as an insider, regardless of title. That includes employees, contractors, advisors, and even partners who receive confidential information through their work.

Myth #2: You’re Safe if You Don’t Personally Trade

Insider trading risk doesn’t stop with placing a trade yourself. Sharing material nonpublic information with someone else can be just as problematic.

If you pass along confidential details to a friend, family member, or colleague and they trade on it, regulators may still hold you responsible. Even casual conversations or messages can come under scrutiny if trading follows.

That’s why tipping rules matter so much. Being careful about what information you share, and with whom, helps prevent situations where good intentions lead to serious consequences.

Myth #3: Insider Trading Is a Victimless Offense

It can be tempting to think insider trading doesn’t really hurt anyone. After all, there is no obvious person on the other side of the trade who complains.

In reality, insider trading undermines trust in the market as a whole. Investors make decisions based on the belief that prices reflect public information. When some participants trade with hidden advantages, that trust starts to break down.

Over time, this affects participation, liquidity, and confidence. For fintech companies that depend on user trust and market credibility, those broader effects matter just as much as the individual trade.

Myth #4: Selling on Bad News Isn’t as Serious as Buying on Good News

Some people assume insider trading only matters when someone profits from good news. In reality, avoiding a loss by selling ahead of bad news can raise the same concerns.

For example, selling shares before negative earnings are announced can still be viewed as using material nonpublic information. Regulators focus on the information advantage, not whether the trade resulted in a gain or prevented a loss.

From a compliance perspective, the direction of the trade does not change the risk. What matters is whether the decision was influenced by information the public didn’t yet have.

Myth #5: Most Insider Trading Goes Undetected

It's easy to assume insider trading only becomes a problem if someone gets caught in a dramatic sting. In reality, detection methods have become far more sophisticated over time.

Regulators use trading data, timing analysis, communication records, and referrals from exchanges and firms to spot unusual patterns. A single trade placed at the wrong time can stand out, especially when it lines up with internal emails, messages, or calendar events.

For companies, this myth can be risky. Assuming no one is watching often leads to weaker controls. Strong policies and training help prevent issues that are far more visible to regulators than many people expect.

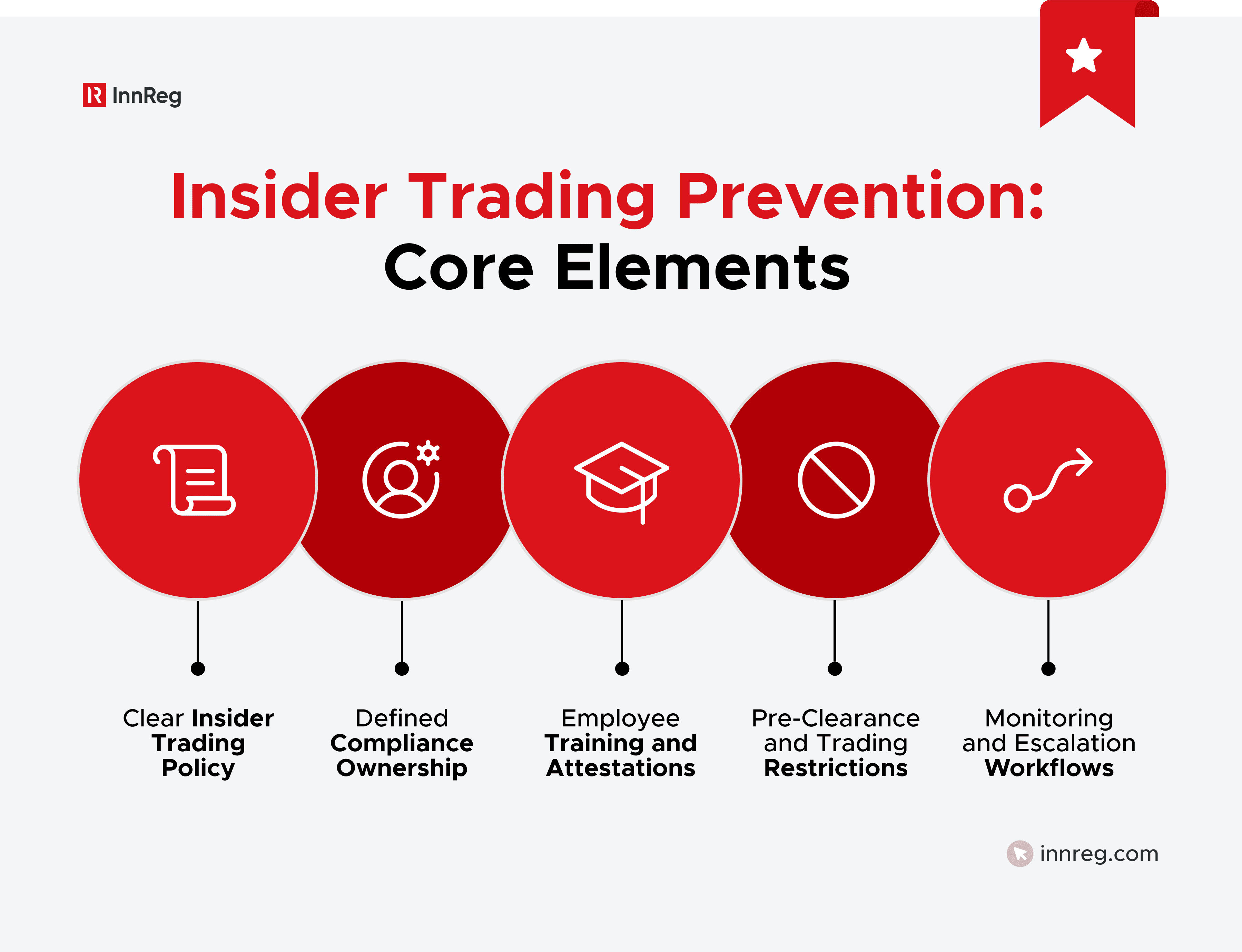

Best Practices for Managing Insider Trading Risk

Preventing insider trading is less about catching bad actors and more about setting clear expectations. When teams understand the rules and have practical guardrails in place, risky situations are easier to avoid before they escalate.

Have a Clear and Enforceable Insider Trading Policy

A strong insider trading policy gives people clear guidance on what’s allowed and what’s not. It should explain what counts as material nonpublic information, who the rules apply to, and when trading is restricted.

Policies work best when they are written in plain language and tied to real scenarios. For example, employees should know whether product metrics, partnership discussions, or listing decisions trigger trading restrictions. If a policy feels abstract or overly legal, it's less likely to be followed.

Clear enforcement matters too. When expectations are consistent and consequences are understood, employees are more likely to pause and ask questions before a trade becomes a problem.

Assign Clear Ownership for Insider Trading Oversight

Insider trading prevention works better when everyone knows who is responsible for what. Without clear ownership, questions get delayed, and risky decisions slip through the cracks.

Compliance teams should be clearly identified as the point of contact for trading questions, approvals, and escalations. Employees should know who to reach out to if they are unsure whether information is sensitive or whether a trade is allowed.

For example, if a team member is working on a confidential partnership and wants to trade, they should know exactly who can review that request and how the decision will be documented. Clear roles reduce hesitation, speed up decisions, and help prevent mistakes before they happen.

Train Employees on Insider Trading Risks and Expectations

Policies alone aren't enough if people do not understand how they apply to their work. Regular training helps employees recognize insider trading risks in situations they actually encounter.

Employee training should go beyond definitions and focus on practical examples. For instance, walking through scenarios involving early access to metrics or confidential roadmap discussions helps people spot issues before they happen. Short, recurring sessions tend to be more effective than one-time presentations.

Attestations and certifications reinforce accountability. When employees periodically confirm that they understand and will follow trading rules, it creates a clear record and encourages more thoughtful decision-making around sensitive information.

Require Pre-Clearance and Enforce Trading Restrictions

Pre-clearance procedures help catch insider trading risk before a trade happens. Instead of relying on employees to make judgment calls on their own, trades are reviewed by compliance or legal first.

For example, an employee may want to sell shares during a busy product launch period. Even if they believe they aren't acting on sensitive information, a pre-clearance review can confirm whether restrictions apply or whether it's better to wait.

Trading restrictions work alongside pre-clearance. These rules define when trading is not allowed, such as during earnings cycles, major deals, or other periods when nonpublic information is circulating.

Together, these controls give employees a clear path to follow and reduce the chance that a routine trade turns into a compliance issue.

Monitor Trading Activity and Escalate Issues Promptly

As teams grow, it becomes harder to rely on manual checks alone. Automated surveillance helps monitor trading activity and flag patterns that may need a closer look, especially around earnings, listings, or major announcements.

For example, alerts can surface trades that happen unusually close to a disclosure or involve employees with access to sensitive information. That doesn’t mean something is wrong, but it gives compliance teams a chance to review activity early and document their response.

Clear escalation workflows matter just as much as the technology. When a flag appears, teams should know who reviews it, what steps come next, and how decisions are recorded. This keeps reviews consistent and avoids last-minute scrambling when questions arise.

Extend Insider Trading Controls to Vendors and Third Parties

Insider trading risk does not stop at your company’s walls. Vendors, advisors, and partners often have access to sensitive information and can create exposure if expectations aren't clear.

For example, a consultant involved in a confidential transaction may see information that could move markets. Without clear restrictions, they may not realize the same trading rules apply to them.

Strong programs extend controls to third parties. This can include confidentiality agreements, clear trading restrictions, and guidance on how sensitive information may be used. Setting these expectations early helps mitigate risk and avoid surprises later.

—

Insider trading is not just about high-profile cases or bad actors. For fintech and financial services teams, it's a practical risk tied to how information flows, who has access to it, and how decisions are made under pressure.

The most effective approach is not about adding friction for its own sake. Clear policies, training, and well-defined controls help people pause, ask questions, and make informed choices when sensitive information is involved.

Maria is a Compliance Consultant at InnReg delivering compliance solutions for fintech clients across broker-dealer, RIA, and money transmitter verticals. She brings prior experience at Finalis, Fenix Securities and PwC, with expertise in AML, CCO support, investment banking operations and securities compliance. She holds FINRA Series 14, 24, and 82 licenses and actively supports regulatory and compliance processes revolving broker-dealer activities.

How Can InnReg Help?

InnReg is a global regulatory compliance and operations consulting team serving financial services companies since 2013.

We are especially effective at launching and scaling fintechs with innovative compliance strategies and delivering cost-effective managed services, assisted by proprietary regtech solutions.

If you need help with compliance, reach out to our regulatory experts today:

Related Articles

Featured LinkedIn Posts