Unfair, Deceptive, or Abusive Acts or Practices (UDAAP) Explained

UDAAP is one of the broadest and most consequential consumer protection standards in US financial regulation. It doesn’t operate as a checklist or a single rule. Instead, it shapes how regulators assess fairness, transparency, and consumer impact across the full lifecycle of a financial product.

For fintech companies, UDAAP risk often emerges outside traditional compliance silos. Product design choices, marketing language, fee structures, and operational workflows can all create exposure, even when no specific rule appears to be violated. That’s why UDAAP enforcement frequently surprises fast-moving teams.

This article breaks down how UDAAP is applied in practice. It explains the legal standards, the regulators involved, and the compliance risks most relevant to modern fintechs.

InnReg works with fintechs and regulated financial institutions to manage UDAAP risk in practice. Our team supports registration, compliance frameworks, and outsourced compliance functions tailored to complex business models from payment platforms to crypto firms. Contact us to learn more about our fintech compliance services.

What Is UDAAP?

UDAAP stands for Unfair, Deceptive, or Abusive Acts or Practices. It’s a consumer protection standard established under the Dodd-Frank Act and enforced primarily by the CFPB. Rather than prescribing specific conduct, UDAAP gives regulators broad authority to evaluate whether a financial product or practice causes consumer harm.

What makes UDAAP different is how it operates. A company can face UDAAP exposure even when it technically complies with other regulations. Regulators focus on outcomes and context and can raise concerns if a practice:

Misleads consumers

Limits their ability to make informed decisions

Takes unreasonable advantage of them

UDAAP applies across the consumer financial ecosystem. This includes banks, fintechs, lenders, payments companies, and service providers that support them. The standard cuts across the full customer experience. That breadth is why UDAAP often becomes a central issue in examinations and enforcement actions, particularly for innovative or fast-scaling business models.

If you are a lender, read our lending regulation guide here →

The Three UDAAP Standards

UDAAP is evaluated through three distinct but related standards. Regulators often rely on more than one at the same time. Understanding how each standard is applied is critical for identifying risk early, especially in fintech products where design and communication choices carry regulatory weight.

Unfair Acts or Practices

An act or practice is considered unfair if it causes substantial consumer injury, the injury is not reasonably avoidable, and countervailing benefits to consumers or competition do not outweigh the harm.

In practice, financial harm is not the only trigger. Time, confusion, loss of access to funds, or unreasonable obstacles can also qualify. For fintechs, unfairness concerns often arise from fee practices, account restrictions, servicing failures, or breakdowns in fund availability.

Deceptive Acts or Practices

A practice is deceptive if it is likely to mislead a reasonable consumer and the information is material to their decision-making. Intent doesn’t matter. What matters is the overall impression created.

Regulators apply a “net impression” standard. Technically accurate disclosures can still be deceptive if other statements or design choices mislead consumers. This is especially relevant for digital interfaces, marketing claims, and abbreviated disclosures common in fintech products.

Abusive Acts or Practices

Abusive acts or practices involve taking unreasonable advantage of a consumer’s lack of understanding, inability to protect their interests, or reasonable reliance on a company to act in their interest.

This standard is narrower but highly sensitive. Abusive risk tends to surface when products rely on consumer confusion, urgency, or complexity. Regulators often focus on whether a company structured a product or process in a way that predictably interfered with informed decision-making, particularly for vulnerable or less sophisticated users.

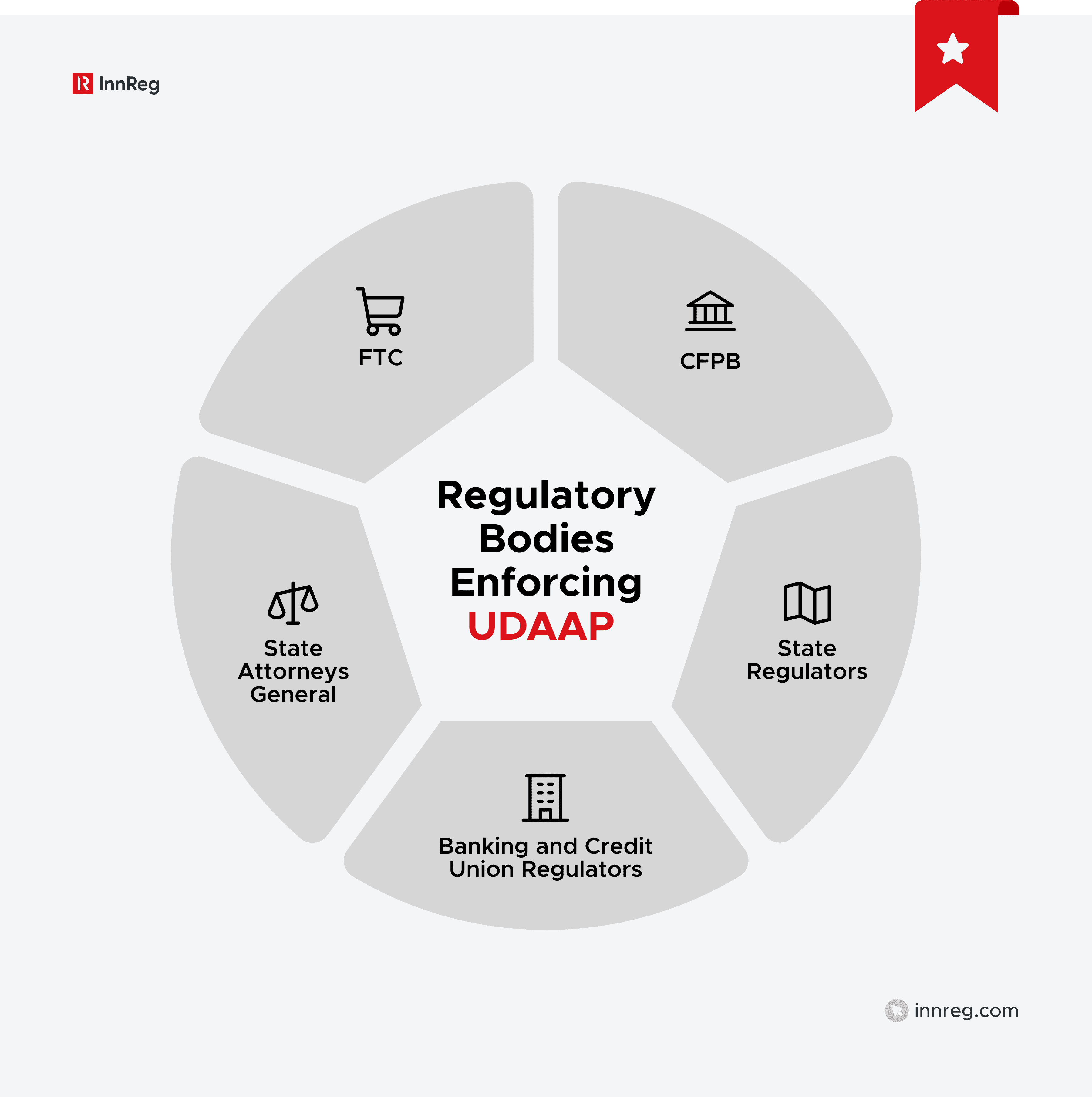

Who Enforces UDAAP in the US?

UDAAP enforcement is not centralized under a single regulator. Multiple authorities evaluate unfair, deceptive, and abusive practices depending on the type of institution, product, and activity involved. Understanding who has jurisdiction is an important part of assessing UDAAP risk, especially for fintechs with hybrid or partner-based models.

The primary enforcement bodies include:

Consumer Financial Protection Bureau (CFPB): The CFPB is the main federal authority responsible for enforcing UDAAP for consumer financial products and services. It identifies UDAAP issues through supervisory examinations, investigations, and enforcement actions. The Bureau’s examination manuals and public enforcement activity heavily influence how UDAAP is interpreted in practice.

Federal Trade Commission (FTC): The FTC enforces prohibitions on unfair and deceptive acts across commerce, including financial services that fall outside the CFPB’s jurisdiction. This can include certain payment services, marketing practices, and non-bank activities. In some cases, fintechs may face parallel exposure under both CFPB and FTC standards.

State Attorneys General and State Regulators: States actively enforce their own consumer protection laws, many of which closely resemble UDAAP. State regulators often coordinate with federal agencies but can also act independently. This is particularly relevant for fintechs operating across multiple states or relying on state licensing frameworks.

Banking and Credit Union Regulators: Federal and state prudential regulators assess unfair or deceptive practices as part of routine examinations. While these agencies may not always label findings as UDAAP, the underlying standards and expectations are similar.

From a compliance standpoint, UDAAP exposure is not tied to a single regulator. Depending on licensing, partnerships, and product scope, companies may face scrutiny from multiple authorities for the same underlying conduct.

Who Is Subject to UDAAP?

UDAAP applies broadly across the consumer financial ecosystem. Coverage is driven by what a company does, not how it labels itself or where it sits in the value chain. For fintechs, this scope often extends further than expected.

Banks and Credit Unions

Banks and credit unions are directly subject to UDAAP through federal consumer protection laws and routine supervisory examinations. Regulators review UDAAP risk alongside safety and soundness, often focusing on fees, disclosures, servicing practices, and customer communications.

For these institutions, UDAAP is a standing examination risk, not an edge case. Findings can arise even when issues are framed internally as operational or customer service problems.

Fintech Companies and Non-Bank Financial Institutions

Fintechs offering consumer financial products or services are squarely within UDAAP’s scope. This includes lenders, payment companies, digital wallets, BNPL providers, and other consumer-facing platforms.

UDAAP risk often shows up where fintechs move quickly. Product design, growth marketing, and automation frequently create exposure before formal compliance frameworks are fully built out. This is a common issue for early-stage and scaling companies.

The SEC has clarified their Marketing Rule that might affect UDAAP →

Service Providers and Third-Party Vendors

Service providers can face UDAAP exposure when their activities contribute to consumer harm. This includes companies handling payments, onboarding, customer support, underwriting tools, or data processing.

Regulators expect supervised entities to oversee their vendors. Outsourcing a function does not outsource UDAAP risk. Failures at the vendor level often surface during examinations or enforcement actions against the primary institution.

Broker-Dealers, RIAs, and Adjacent Exposure

The CFPB does not directly regulate broker-dealers and RIAs, but UDAAP concepts still matter. State consumer protection laws, FTC authority, and parallel expectations under securities regulations create overlapping risk.

For fintechs operating near the securities boundary, UDAAP-style analysis often runs in parallel with SEC and FINRA standards. Misleading statements, complex fee structures, or confusing disclosures can attract scrutiny even outside traditional banking regulation.

Learn about the rules outlined in the Securities Exchange Act of 1934 →

See also:

Common UDAAP Compliance Risks for Fintechs

UDAAP risk for fintechs most often emerges at specific pressure points in the business. These include rapid product launches, growth-driven marketing, automated decisioning, and heavy reliance on third-party infrastructure.

Understanding where these risks typically surface allows compliance teams to prioritize reviews around product changes, customer-facing communications, and operational dependencies, rather than treating UDAAP as a generalized or abstract concern.

Need help with RIA compliance?

Fill out the form below and our experts will get back to you.

Marketing and Product Claims

Marketing claims often set the baseline for UDAAP analysis. Regulators compare promotional language against actual product behavior.

Common issues include claims about speed, cost, approval likelihood, or access to funds that are true only in limited cases. Statements like “instant,” “free,” or “no impact” frequently draw scrutiny when conditions, delays, or exceptions apply. This risk increases when disclaimers appear late in the funnel or only in terms and conditions.

Fees, Pricing, and Disclosures

Fee-related UDAAP risk is rarely about illegal pricing. It’s usually about timing, clarity, and consumer expectations.

Problems arise when fees are triggered by behaviors consumers do not reasonably anticipate, such as inactivity, partial payments, or automated actions. Late-stage disclosure or reliance on dense legal language is a recurring regulatory concern, especially in digital-first products where consumers make quick decisions.

Product Design and User Experience

User experience decisions directly affect consumer understanding. Regulators increasingly evaluate flows, defaults, and interface design as part of UDAAP analysis. Risk tends to surface when key information is buried, difficult to access, or visually minimized.

Design choices that make it easier to opt in than opt out, or harder to reverse an action, receive particular attention, especially when money movement or recurring charges are involved.

Sales Practices and Customer Communications

UDAAP risk also surfaces in how teams communicate with customers. This includes sales scripts, support responses, automated messages, and escalation handling.

Inconsistent or overly confident explanations can mislead consumers, even when the underlying documentation is accurate. Regulators often review recordings, transcripts, and chat logs during examinations.

Vendor, API, and Banking-as-a-Service Risk

Most fintechs depend on third parties for payments, onboarding, underwriting, or account infrastructure. Regulators do not view this as a mitigating factor.

UDAAP issues often stem from vendor failures such as delayed funds, incorrect balances, or broken disclosures. When a vendor’s system causes consumer harm, regulators expect the fintech to own the outcome, not defer responsibility contractually.

Here’s an overview of how these common risks come up during the customer’s lifecycle at various stages:

Customer lifecycle stage | Common UDAAP risk signals |

|---|---|

Advertising and acquisition | Overstated benefits, incomplete conditions |

Onboarding | Late disclosures, rushed consent |

Servicing and billing | Unexpected fees, posting delays |

Customer support | Inconsistent explanations, unresolved complaints |

Account closure | Friction, delayed access to funds |

UDAAP and Third-Party Risk Management

Third-party relationships are a recurring source of UDAAP exposure, particularly for fintechs built on vendor platforms and partner banks. From a regulatory perspective, consumer harm is what matters, not how responsibilities are allocated contractually.

Regulators consistently expect companies to understand, monitor, and control UDAAP risk across their vendor ecosystem.

See also:

Service Provider Oversight Responsibilities

Service providers that touch consumer-facing functions can create UDAAP risk even when they operate behind the scenes. This includes onboarding vendors, payment processors, customer support platforms, underwriting tools, and data providers.

Oversight expectations extend beyond due diligence at onboarding. Regulators look for ongoing monitoring tied to actual consumer impact, such as error rates, delays, complaints, and recurring operational issues. Static vendor reviews are rarely sufficient.

Banking Partners and Shared Compliance Risk

In banking-as-a-service models, fintechs and sponsor banks share regulatory exposure. Regulators generally view both parties as responsible for consumer outcomes.

Fintechs are expected to understand bank-level requirements, while banks are expected to oversee fintech activities. Misalignment between the two often leads to UDAAP findings, particularly when disclosures, customer communications, or remediation responsibilities are unclear.

Contractual and Ongoing Monitoring Considerations

Contracts play a role, but they do not define regulatory accountability. Indemnities and service-level agreements may allocate cost, but they don’t shield companies from UDAAP scrutiny.

Effective third-party risk management typically includes:

Clear ownership of consumer-facing obligations

Defined escalation paths for incidents affecting customers

Regular review of vendor-driven complaints and errors

When vendor performance degrades, regulators expect timely action, not attribution of fault. Companies that treat vendor oversight as an operational afterthought tend to discover UDAAP risk during exams rather than through internal controls.

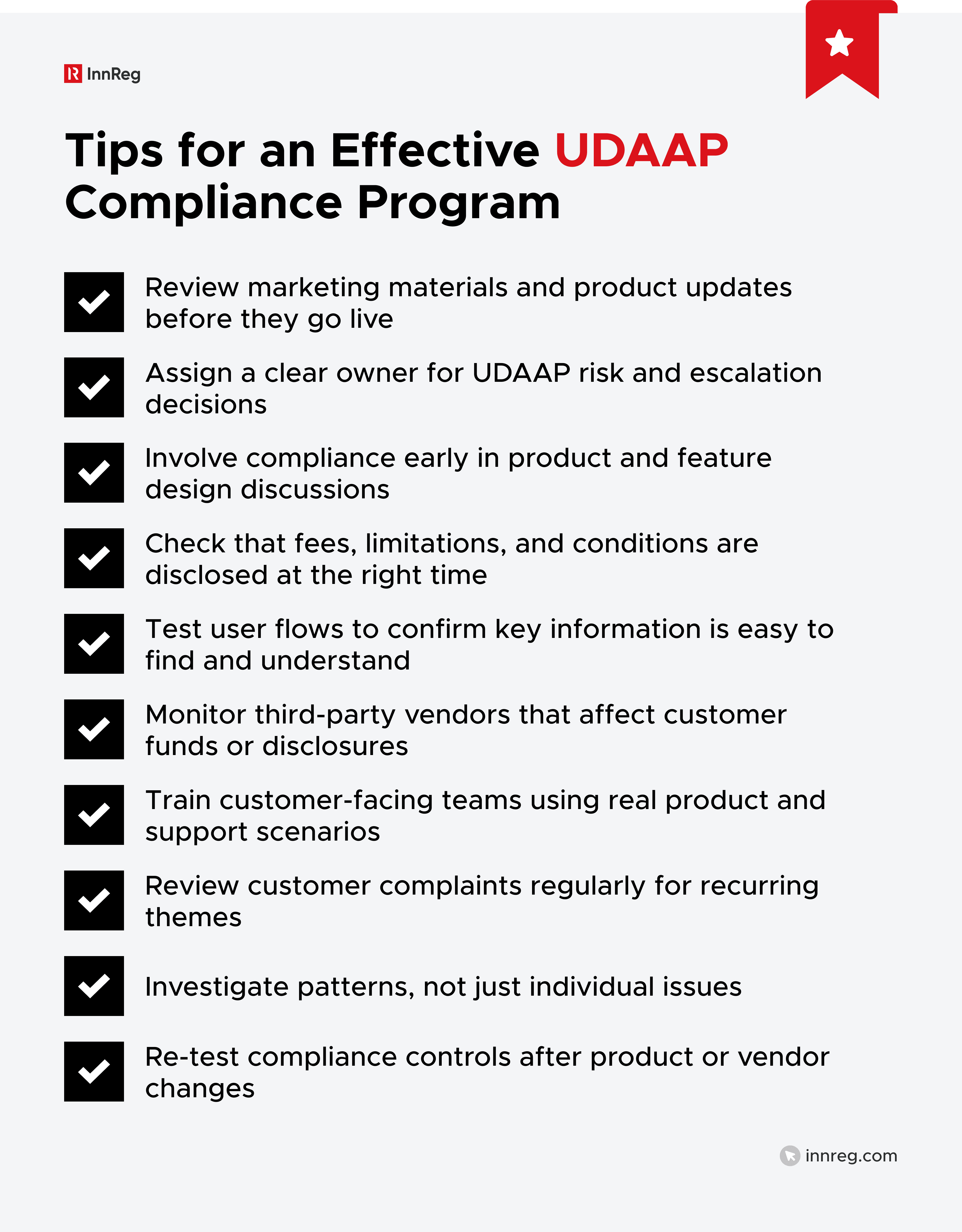

How to Build an Effective UDAAP Compliance Program

An effective UDAAP compliance program is not a standalone policy. It’s an operating framework that cuts across product, legal, compliance, and operations. Here are some steps to help your fintech align with UDAAP expectations and build an effective program:

Governance and Accountability

Clear ownership is foundational. Regulators expect defined responsibility for UDAAP risk at both the management and operational levels.

This typically includes executive oversight, documented escalation paths, and clarity around who can approve or block product and marketing changes. Ambiguity around ownership is a common weakness, especially in early-stage or rapidly scaling teams.

Policies, Procedures, and Internal Controls

Written policies should translate UDAAP principles into concrete expectations. High-level statements alone are not enough.

Effective programs link UDAAP risk to specific activities such as marketing reviews, product changes, fee updates, and vendor onboarding. Controls are strongest when they are embedded into existing workflows, rather than layered on after the fact.

Training and Ongoing Awareness

Training should focus on how UDAAP issues actually arise in day-to-day work. This includes marketing teams, product managers, customer support, and engineering leads.

Generic training tends to miss the mark. Role-specific examples and scenarios are far more effective, particularly for teams making consumer-facing decisions under time pressure.

See also:

Monitoring, Testing, and Audits

Ongoing monitoring helps identify issues before they become regulatory findings in an audit. This includes reviewing marketing materials, product changes, customer complaints, and operational metrics.

Testing should be risk-based and targeted. Regulators often look for evidence that companies test what they change, not just what they originally launched.

Complaint Management and Escalation

Complaints are one of the most direct indicators of UDAAP risk. Regulators regularly use complaint data to identify patterns and validate consumer harm.

Effective programs treat complaints as a feedback loop, not just a customer service function. Escalation thresholds, trend analysis, and root cause reviews are key expectations, particularly when similar issues appear across channels or over time.

—

UDAAP remains one of the most consequential and flexible standards in US financial regulation. For fintechs, UDAAP risk most often arises through product design, marketing, third-party dependencies, and day-to-day operations rather than isolated compliance gaps.

If you’re evaluating UDAAP risk in the context of a new product, regulatory exam, or ongoing operations, InnReg can help. We help manage UDAAP risk in practice by supporting clients with licensing and registration, compliance program design, and outsourced compliance operations. Reach out to InnReg to discuss how we can support your compliance objectives.

InnReg was founded in 2013 by Francesco Matteini, former Chief Compliance Officer who helped launch and scale some of the most innovative digital broker-dealers over the last two decades. He built compliance programs to support the first zero-commission broker and the first BD-sponsored investor social network. Since its founding, InnReg has attracted highly experienced fintech consultants with long careers in compliance, risk management, and a deep understanding of the fintech industry.

How Can InnReg Help?

InnReg is a global regulatory compliance and operations consulting team serving financial services companies since 2013.

We are especially effective at launching and scaling fintechs with innovative compliance strategies and delivering cost-effective managed services, assisted by proprietary regtech solutions.

If you need help with RIA compliance, reach out to our regulatory experts today:

Related Articles

Featured LinkedIn Posts