FINRA NMA: A Practical Guide to Broker-Dealer Registration

The FINRA New Membership Application (NMA) is the formal process that firms must complete to become broker-dealer members of the Financial Industry Regulatory Authority (FINRA).

For many fintechs, this step is essential before they can bring a securities-related product or platform to market. Furthermore, the NMA review details make it a critical aspect to consider before launching in the market.

It examines a firm’s business model, financial readiness, supervisory systems, technology, and key personnel. It is also coordinated with the SEC’s broker-dealer registration requirements, meaning firms cannot move forward without addressing both regulators at once.

This article explains how the FINRA NMA operates, the documents and approvals required for a successful registration, and where firms most frequently encounter delays.

At InnReg, we support firms working through the FINRA NMA process, including mapping business lines to FINRA rules, drafting supervisory procedures, and coordinating Form BD, U4, and BR filings. Contact us to learn more.

What Is the FINRA New Membership Application (NMA)?

The FINRA New Membership Application (NMA) is the process through which a firm applies to become a registered broker-dealer. Membership is required for nearly all firms that plan to conduct securities brokerage business with the public.

The application examines whether the firm has the financial, operational, and supervisory systems in place to comply with regulatory obligations from the outset.

FINRA distinguishes between several types of membership applications, each serving a different regulatory purpose:

New Membership Application (NMA): Required for firms seeking to join FINRA for the first time.

Materiality Consultation: A preliminary discussion with FINRA used to determine whether a planned change triggers the need for a CMA. This step can save firms time by clarifying requirements before submitting a full application.

Continuing Membership Application (CMA): Required for existing member firms that wish to make material changes, such as adding new business lines, changing ownership structure, or opening additional branches.

In practice, fintech firms exploring models such as fractional shares, digital asset securities, or app-based trading features often discover that they fall within broker-dealer rules. Filing an NMA is not optional in these cases. Proceeding without registration exposes firms to significant regulatory risk, including enforcement actions and reputational damage.

Overview of the FINRA NMA Process

The FINRA NMA follows a structured path with defined timelines, fees, and checkpoints. While the process is standardized, the level of complexity and the time to approval depend heavily on the firm’s business model, the quality of its documentation, and its responsiveness during review.

Timeline Variations and Review Deadlines

FINRA’s rules set a maximum of 180 days from the point an application is deemed “substantially complete” to issue a decision. In practice, straightforward applications may be reviewed within 100 days, but innovative or complex models often require more time.

The timeline tends to lengthen when applications include incomplete or inconsistent documentation, when designated principals have not yet passed required licensing exams, when the business model involves emerging areas such as digital assets, or when firms take too long to respond to FINRA’s follow-up questions.

Because of these variables, it is prudent to plan for a multi-month process and maintain sufficient funding to cover operating expenses while approval is pending.

Application Fees and Typical Internal Costs

FINRA charges an initial membership application fee that ranges from about $7,500 to $30,000 for most new broker-dealers. Large firms or those engaging in more complex activities, such as carrying customer accounts, may face higher fees:

Number of Registered Persons Associated with Applicant | Small | Medium | Large |

|---|---|---|---|

Tier 1 | 1-10 | 151-300 | 501-1000 |

Tier 2 | 11-100 | 301-500 | 1001-5000 |

Tier 3 | 101-150 | N/A | >5000 |

Application Fee per Tier | Small | Medium | Large |

Tier 1 | $7,500 | $25,000 | $35,000 |

Tier 2 | $12,500 | $30,000 | $45,000 |

Tier 3 | $20,000 | N/A | $55,000 |

In addition to FINRA’s charges, firms should account for:

State fees for Firms: $60 - $600, depending on the state

Registered Representative (“RR”) Fees:

FINRA: $125 per RR

State: $25 - $285 per RR, depending on state

If applicable, Disclosure processing fee: $155

Fingerprint card processing fee: $31.25 or $41.25 per employee

Branch office application: $75 per branch, based on the number of branches already registered

Examination registration fees vary based on exam (i.e., Series 7, 24, 27, etc.)

The NMA is resource-intensive, and many startups underestimate the internal time required to assemble a credible application package.

Regulatory Framework and Authorities Involved

Multiple regulatory bodies oversee different aspects of broker-dealer registration, and firms must meet the expectations of each before they can operate:

FINRA MAP (Rules 1012-1014) and the Fourteen Standards of Admission

FINRA administers the membership process through its Membership Application Program (MAP).

The program is guided by the FINRA Rule 1000 Series, particularly Rules 1012 through 1014. Rule 1014 outlines fourteen specific standards that applicants must satisfy, ranging from adequate financial and operational capacity to supervisory structure, personnel qualifications, and systems for recordkeeping and compliance.

These standards set the baseline for whether FINRA considers a firm ready to conduct business with the public.

Parallel SEC Registration (Form BD)

At the same time, firms must file Form BD with the US Securities and Exchange Commission.

This filing formally registers the firm as a broker-dealer at the federal level. In practice, the SEC does not finalize approval until FINRA completes its membership review, making the two processes intertwined.

For founders, this means preparing documents that satisfy both regulators simultaneously, rather than viewing them as separate steps.

See also:

State Securities Registration and Coordination

In addition to federal and FINRA requirements, broker-dealers must comply with state-level rules.

Many states accept electronic registration through FINRA’s Central Registration Depository (CRD), but some impose extra requirements or filings.

Firms planning to operate across multiple jurisdictions should expect variations in fees, disclosures, and timelines at the state level. Neglecting state coordination can create bottlenecks even after FINRA approval.

Need help with fintech compliance?

Fill out the form below and our experts will get back to you.

Pre-Filing Readiness Considerations

Before filing a FINRA New Membership Application (NMA), it is critical to assess whether your firm has the proper structure, personnel, and resources in place.

Several readiness factors consistently influence the pace and outcome of the review, and each warrants careful attention before proceeding:

Mapping Business Activities to Regulatory Expectations: Every proposed business activity directly influences FINRA’s review. The scope of activities determines required licenses, net capital thresholds, supervisory structures, and even the complexity of written procedures. A clear alignment between the business plan and regulatory requirements reduces the risk of back-and-forth with FINRA later in the process.

Required Personnel, Licensing, and Examination Requirements: FINRA generally requires at least two registered principals, including a General Securities Principal and a Financial and Operations Principal (FinOp). They must pass the relevant qualification exams (Series 24 and Series 27 or 28). Additional exams may be required for registered representatives depending on the firm’s activities. Submitting an NMA before principals are licensed can stall the review and extend the timeline.

Net Capital Planning and Operating Expense Coverage: The minimum net capital ranges from $5,000 for introducing brokers to significantly higher amounts for firms carrying accounts, engaging in proprietary trading, or complex trading. Applicants must also demonstrate they can fund at least a year of operations above their capital requirement, with evidence of where the money comes from.

Clearing Arrangements, Vendors, and Technology Preparedness: Fintechs often rely on third parties for clearing, custody, and technology infrastructure. FINRA expects documentation of these arrangements, whether through finalized contracts or draft agreements. If the firm’s platform includes proprietary technology, regulators may request a demonstration during the review. Applicants should be ready to show that the system functions as described and complies with requirements for recordkeeping, reporting, and customer protection.

Taken together, these factors form the foundation of a credible NMA submission. Addressing them in advance reduces delays and demonstrates that the firm is operationally and financially prepared for membership.

Core Documentation for the FINRA NMA

The application process is built around documentation. FINRA uses these materials to determine whether a firm meets its fourteen admission standards.

A weak or incomplete package often leads to extended back-and-forth, while a clear and consistent set of documents helps move the review forward.

Business Plan and Financial Assumptions

The business plan is the anchor of the FINRA NMA.

It should clearly explain the firm’s model, including the:

Services offered

Target customer base

Anticipated revenue structure

Potential risks

FINRA will look for practical detail, not just high-level vision statements. Projections should tie directly to underlying assumptions, such as customer acquisition costs, expected transaction volumes, or pricing models.

Regulators will verify these assumptions against supervisory procedures and financial statements to test for consistency. An overly optimistic plan without supporting evidence is likely to prompt additional questions from FINRA and slow down the process.

Written Supervisory Procedures (WSPs)

Written supervisory procedures outline how the firm will meet the regulatory obligations day to day.

These documents must reflect the actual structure and risks of the applicant’s business. For example, a firm offering app-based securities trading will need different supervisory controls than one focusing on private placements.

FINRA expects coverage of core topics such as sales practices, communications oversight, anti-money laundering, cybersecurity, and recordkeeping. Each section should make clear who is responsible for supervision and how compliance will be documented.

Pro Forma Financials and Evidence of Capitalization

Applicants must provide pro forma financial statements, typically covering at least the first twelve months of operations.

These projections need to include detailed revenue and expense assumptions, showing that the firm can remain above its required net capital while funding operations.

If the numbers do not align with the business plan or appear unrealistic, the review can stall. Evidence of adequate capitalization is not just a formality; it is central to demonstrating financial ability.

Organizational Charts and Ownership Disclosures

FINRA requires transparency on who controls the firm and how decision-making is structured. An organizational chart should identify principals, supervisory staff, and reporting lines.

Ownership disclosures must include all direct and indirect owners, with their percentages and affiliations.

See also:

Clearing, Custody, and Vendor Agreements or Letters of Intent

If a firm will rely on clearing brokers, custodians, or key service providers, FINRA expects evidence of those relationships.

Executed agreements are preferable. However, draft contracts or letters of intent may be acceptable at the application stage. These documents demonstrate that the firm has secured the infrastructure necessary to operate.

For fintech firms in particular, regulators often look closely at vendor arrangements involving technology, data management, or compliance outsourcing. The agreements should show clear responsibilities and safeguards for regulatory obligations.

Cybersecurity, AML, and Recordkeeping Policies

Firms must submit policies that cover the areas regulators view as critical for investor protection and market integrity.

These include anti-money laundering programs that match the firm’s business model, cybersecurity protocols to safeguard customer data, and recordkeeping procedures that comply with books and records rules.

FINRA will assess whether these policies are realistic for the firm’s scale and technology environment.

Read our guide to learn how to use the FINRA Cybersecurity checklist →

For fintechs, this means policies should address key issues such as electronic communications, data storage, and third-party integrations. Regulators want to see that these areas are not treated as afterthoughts but are built into the firm’s operational design.

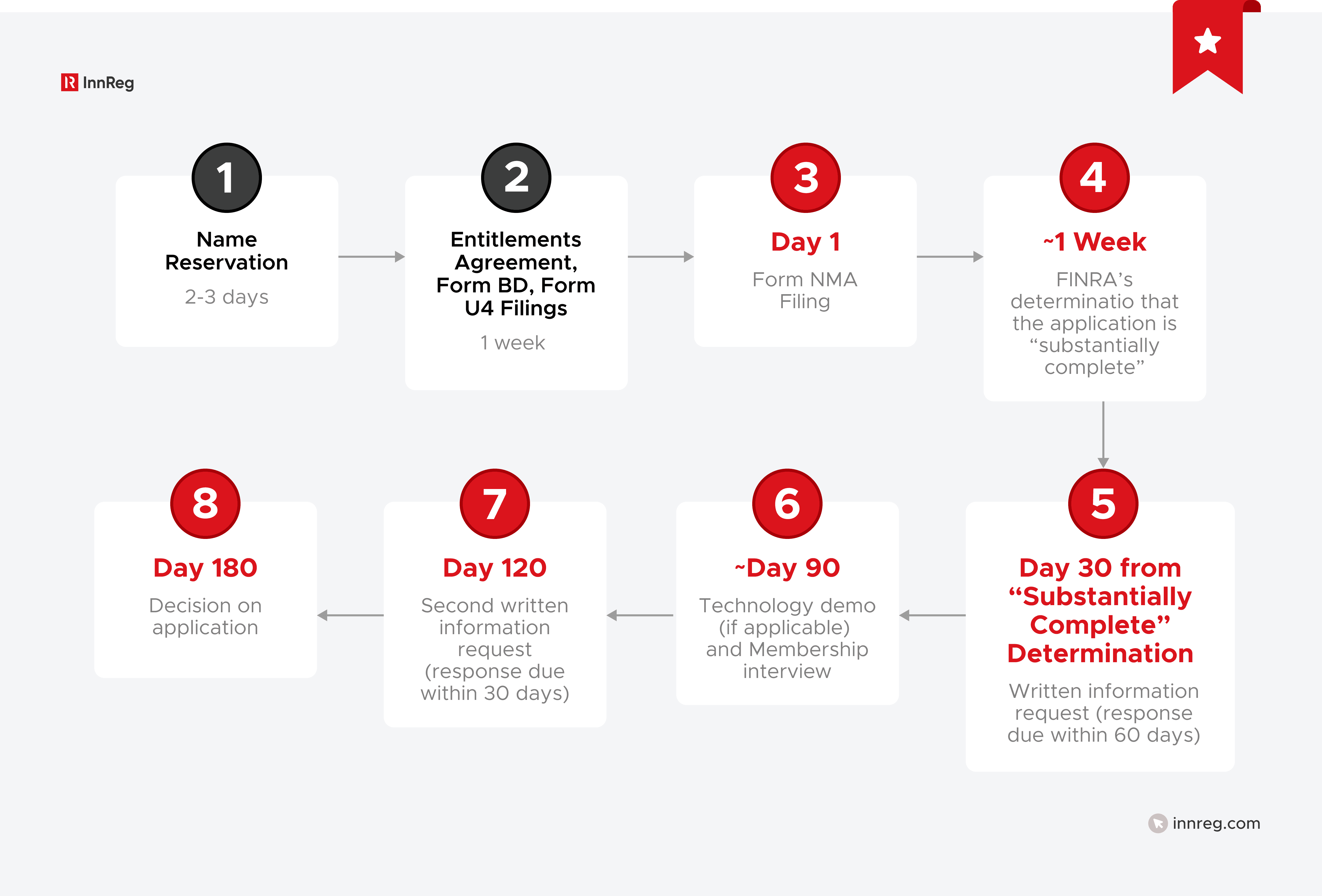

NMA Filing Sequence and Submission Requirements

Submitting a FINRA New Membership Application (NMA) is a process that involves several filings, system setups, and payments that must be completed in sequence:

Firm Name Reservation and Entitlement Procedures (Gateway/CRD)

Before filing any forms, firms must reserve a name with FINRA and set up system access through the FINRA Gateway and Central Registration Depository (CRD).

The firm designates a Super Account Administrator (SAA), who manages access for other users. Without this step, the application cannot move forward.

Funding the Flex-Funding Account and Fee Requirements

Applicants are required to pre-fund a FINRA Flex-Funding Account, which is used to pay membership, filing, and registration fees.

Deposits are made electronically, and the application will not be accepted until the account is funded.

Forms BD, NMA, U4, and BR: Scope and Purpose

A FINRA NMA submission relies on more than just one form.

At the federal level, Form BD registers the entity as a broker-dealer with the SEC. FINRA then relies on Form NMA, which provides the detailed business, financial, and supervisory information needed to determine whether the firm is ready for membership.

To register individuals, applicants file Form U4 for each principal or representative, disclosing qualifications and backgrounds.

If the firm intends to operate more than one office, Form BR extends the registration to branch locations at both FINRA and the state level.

Taken together, these filings create the structure regulators use to assess, approve, and monitor new broker-dealers.

Fingerprinting and Background Checks

All associated persons must provide fingerprints, submitted electronically or via card, so FINRA can conduct background checks through the FBI.

Any issues uncovered during this stage can delay the application or result in further scrutiny.

Standards for a “Substantially Complete” Application

FINRA does not begin its substantive review until it decides that an application is “substantially complete.”

This designation means every required form, supporting document, and fee has been submitted and properly recorded.

If even a single element is missing, whether it is a supervisory procedure, a fingerprint card, or proof of capital, the package will be returned, and the FINRA review timeline will not start.

FINRA Review Procedures

Once an application is deemed substantially complete, FINRA begins a detailed review. This stage involves assessing whether the firm satisfies the fourteen standards of admission under Rule 1014, while also testing the credibility and consistency of the materials submitted.

Evaluation Against Admission Standards

FINRA examines whether the firm demonstrates financial responsibility, operational readiness, qualified personnel, and effective supervisory systems.

Reviewers compare the business plan, WSPs, and financial projections against one another to identify inconsistencies.

Any gaps between what the firm claims in one document and what it supports in another may trigger additional questions.

Common Information Requests and Effective Response Practices

As part of its review, FINRA often sends written requests for clarification or supporting information.

The requests may address anything from the assumptions underlying financial projections to the responsibilities of supervisory staff or the details of vendor contracts. The pace of the review depends heavily on how quickly and clearly the firm responds.

Many firms find it useful to designate a single contact and use task management tools to keep responses timely and organized.

Technology Demonstrations and Evidence Requirements

If a firm’s business model relies heavily on proprietary platforms, FINRA may request a demonstration of the technology.

This is especially common for fintech firms where trade execution, client onboarding, or recordkeeping are conducted digitally.

Demonstrations allow regulators to confirm that systems work as described and meet compliance obligations such as record retention and supervisory access.

Impact of Application Amendments During Review

If a firm changes its business plan, personnel, or structure after filing, it may need to amend the application.

While amendments are common, they can reset parts of the review process. For instance, introducing a new product line or changing supervisory staff often requires updated documents and increased scrutiny. Applicants should weigh the impact of changes carefully before introducing them mid-review.

FINRA Membership Interview

The membership interview is one of the final steps in the NMA process. By this stage, FINRA has already reviewed the application materials and information requests.

The purpose of the interview is to confirm that the firm’s leadership understands its regulatory responsibilities and that the business is prepared to operate under FINRA’s standards.

Required Participants and Preparation Steps

The interview usually includes the firm’s CEO, Chief Compliance Officer, and Financial and Operations Principal, along with any other individuals central to daily operations.

Preparation involves reviewing the application materials in detail, aligning on supervisory responsibilities, and anticipating questions about business operations.

Firms that prepare their leadership team together, rather than leaving each principal to prepare in isolation, are typically better positioned to answer FINRA’s questions consistently.

Question Themes and Discussion Areas

FINRA’s questions often focus on the firm’s business model, compliance program, financial stability, and supervisory framework.

For fintech applicants, regulators may also probe into technology systems, vendor oversight, and how the platform manages risk.

While the questions are grounded in the application, interviewers often use this meeting to test how well leadership understands the practical implications of running a broker-dealer.

Outcomes and Post-Interview Documentation

The interview is not an exam with a pass-or-fail score. Instead, it is an assessment tool for FINRA to confirm readiness and clarify any outstanding issues.

Afterward, FINRA may request additional documentation or revisions before moving to a final decision.

In some cases, the interview highlights areas where conditions or restrictions may be applied to the firm’s membership agreement.

FINRA New Membership Decision and Agreement

After the interview stage, FINRA moves toward a decision on the application. The outcome is documented formally and establishes the terms under which the firm may operate.

Types of Decisions: Approval, Conditional Approval, Denial

A firm may be granted full approval to operate as a member, or it may receive conditional approval.

Conditions are typically tied to specific limitations, such as restrictions on business lines, requirements to hire additional staff, or commitments to strengthen certain procedures.

In some cases, FINRA may deny membership if it determines that deficiencies cannot be corrected within the scope of the application.

See also:

Typical Restrictions for Newly Approved Firms

Even when membership is approved, new firms often begin with restrictions that reflect their risk profile.

Common examples include:

Limits on proprietary trading

Restrictions on holding customer funds

Conditions tied to minimum capital requirements

These restrictions can be revisited later through a Continuing Membership Application if the firm seeks to expand or change its business.

Execution of the Membership Agreement and Effective Dates

When approval is granted, the firm must sign a membership agreement that formalizes the decision.

The agreement sets out the approved activities, any restrictions imposed, and the obligations the firm must meet.

The effective date marks the firm’s official entry as a FINRA member and the beginning of its ongoing compliance obligations.

Causes of Delay in the NMA Process

The NMA review is time-bound, but in practice, applications often run longer. Most delays stem from missing information or slow follow-up during the review:

Document Inconsistencies and Gaps: One of the most common reasons for delay is when the business plan, financial projections, and supervisory procedures do not align. For example, a plan that describes carrying customer accounts without showing related clearing arrangements will prompt follow-up questions. Missing or contradictory information almost always adds weeks to the timeline.

Principal and Licensing Deficiencies: Applications submitted without fully qualified principals or with exams still pending often stall. FINRA requires evidence that supervisory staff are licensed and able to assume their responsibilities from day one. Filing prematurely, before licensing is complete, usually extends the review.

Incomplete Clearing and Vendor Documentation: Firms that rely on third parties must provide documentation of those relationships. If contracts or letters of intent are absent, FINRA will not consider the infrastructure sufficient. This issue is particularly common for fintech firms that outsource technology or compliance functions.

Response Timeliness and Quality During Review: Once FINRA begins sending information requests, the speed and clarity of responses become critical. Late or vague replies can lead to repeated rounds of questions, extending the process well beyond the expected timeframe. Applicants who track requests systematically and assign a clear point of contact are better positioned to keep the review moving.

Technology Misalignment or Lack of Operational Proof: Where proprietary platforms are central to the business model, FINRA may request demonstrations. If the technology is incomplete, untested, or inconsistent with the policies filed in the application, the process slows. Regulators need to see operational readiness, not just theoretical designs.

Most delays in the NMA process can be traced back to issues that are preventable with preparation and organization. At InnReg, we work with broker-dealers and fintech firms to anticipate these challenges, streamline documentation, and manage the process more efficiently. Contact us to learn how our team can support your application.

—

The FINRA New Membership Application is one of the most demanding steps for any firm entering the securities industry. It requires careful alignment of business plans, supervisory systems, financial resources, and technology infrastructure.

For fintech firms in particular, the process can feel even more complex, as regulators often scrutinize new models, platforms, and third-party relationships with additional care.

While the rules and standards are well defined, the practical challenges lie in preparation, consistency across documents, and responsiveness during review.

Firms that underestimate these elements often face preventable delays. A well-prepared application, supported by experienced compliance professionals, sets a stronger foundation for approval and long-term operations.

Kushal Abeywickrama is the Chief Operating Officer at InnReg with over 10 years of experience in broker-dealer compliance, supervision, and regulatory operations across FINRA-regulated firms. He holds Series 7, 24, 4, 63, and 57 FINRA licenses and has previously held roles at HSBC and BlackSwan Technologies.

How Can InnReg Help?

InnReg is a global regulatory compliance and operations consulting team serving financial services companies since 2013.

We are especially effective at launching and scaling fintechs with innovative compliance strategies and delivering cost-effective managed services, assisted by proprietary regtech solutions.

If you need help with compliance, reach out to our regulatory experts today:

Related Articles

Featured LinkedIn Posts