Broker-Dealer, ATS, or Exchange? Understanding the Differences

The distinction between a broker-dealer, alternative trading system (ATS), and an exchange is a frequent source of confusion. This is particularly the case for fintechs that design trading platforms, matching engines, or alternative marketplaces.

Questions like “Can I register as a broker-dealer and operate an exchange?” or “When does a trading platform become an ATS?” come up regularly in regulatory discussions, investor diligence, and early product design. These classifications are not interchangeable, and misunderstanding them can create material regulatory risk.

This article explains the difference between broker-dealer, ATS, and exchange classifications under US securities law, with a focus on how these roles actually function in practice.

At InnReg, we help fintechs, broker-dealers, and ATS operators navigate regulatory classification and compliance requirements. From registration and licensing to building and managing ongoing compliance programs, our team supports complex trading and market structure models.

Why These Terms Are Commonly Confused

Confusion between broker-dealer, ATS, and exchange classifications is not a matter of semantics. It usually arises because these concepts intersect in real-world trading models, especially in fintech-driven market structures.

Many firms approach these classifications from a product or technology perspective rather than a regulatory one. A fintech may see itself as “just providing software” or “facilitating trades,” without realizing that regulators focus on how orders interact, who controls execution, and whether multiple parties are being matched.

However, misclassification can result in operating an unregistered ATS or exchange, which may lead to enforcement actions, forced shutdowns, or retroactive remediation. In practice, regulators are less concerned with labels and more concerned with functional behavior.

This issue surfaces most often during early-stage product development. Fintechs frequently design matching logic, liquidity pools, or order routing features before compliance implications are thoroughly evaluated. What begins as a simple bilateral trading model can evolve into multilateral interaction without a corresponding regulatory reassessment.

At that point, firms often realize that broker-dealer registration alone does not answer whether the platform itself is regulated as an ATS or exchange. Addressing this question early helps avoid costly redesigns and regulatory rework later.

See how InnReg helps fintech by providing regulatory and product strategy services →

Broker-Dealer: The Regulatory Foundation

Most trading models in the US securities markets start with broker-dealer registration. Even when a firm ultimately operates an ATS or participates in an exchange, the broker-dealer framework is typically the regulatory entry point.

What a Broker-Dealer Is (and What It Is Not)

A broker-dealer is a firm registered with the SEC and FINRA that is authorized to engage in securities transactions. It may execute trades for customers, trade for its own account, or both. A broker-dealer is a regulated market participant, not a trading venue or marketplace.

A Broker-Dealer Is: | A Broker-Dealer Is Not: |

|---|---|

|

|

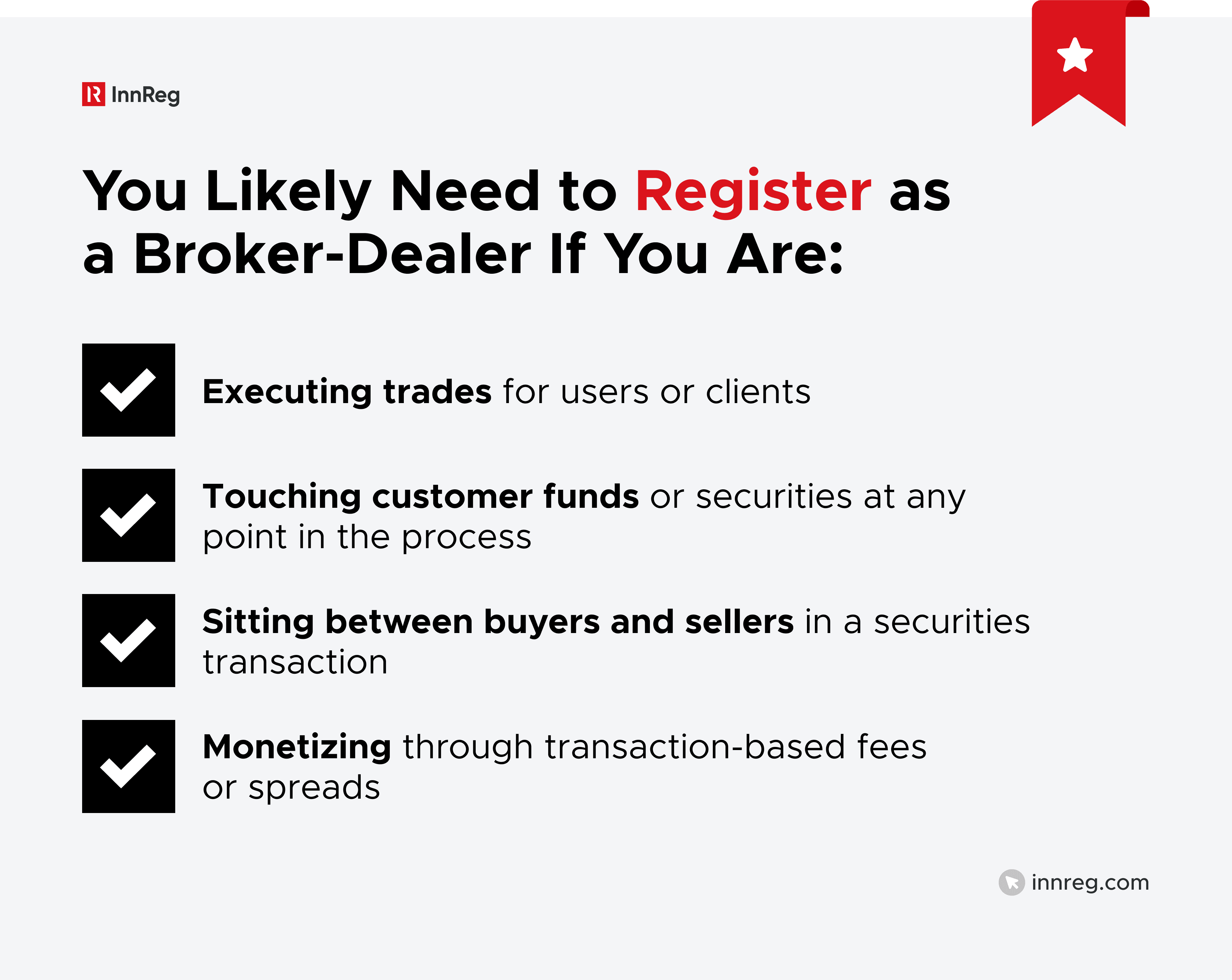

Core Activities That Trigger Broker-Dealer Registration

Registration is driven by function, not branding. Firms that regularly participate in securities transactions or receive transaction-based compensation often trigger broker-dealer requirements.

In practice, many fintechs trigger broker-dealer registration earlier than expected, particularly when monetization is tied to trading activity.

Why Most Trading Models Start Here

Registering as a broker-dealer is what makes regulated market access possible. Exchange membership, ATS operation with separate approval, and proprietary or OTC trading all flow from that starting point.

The cost of that access is operational discipline: supervision, AML, surveillance, and recordkeeping are embedded into the business, not layered on top. Delays typically appear when these requirements collide with a product design that assumed more flexibility than the rules allow.

This is the point where compliance input shifts from optional to necessary. Treating it as part of the build process, rather than a post-build review, tends to limit disruption.

Read our guide to learn about broker-dealer registration →

What Exchanges Are Under US Securities Law

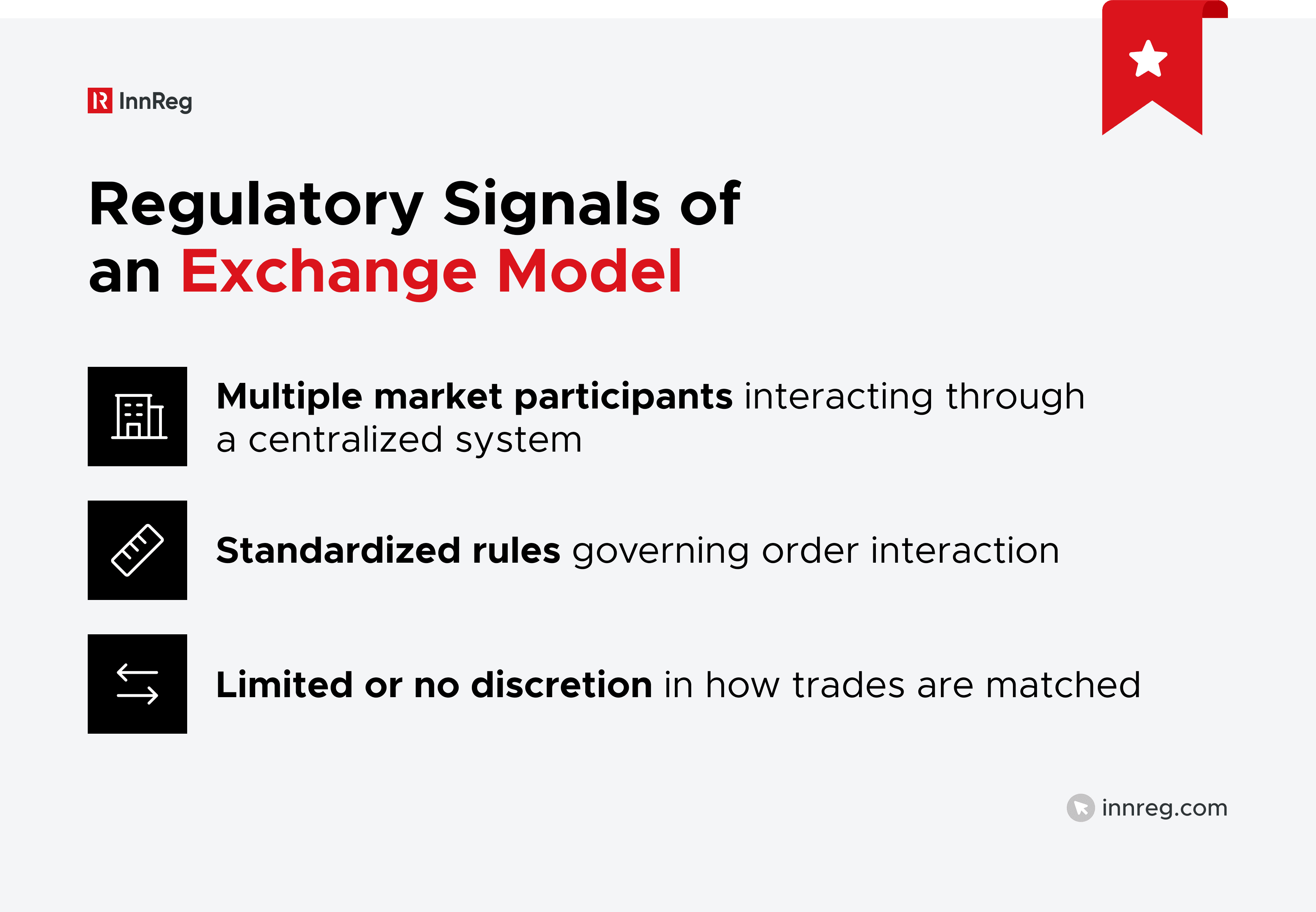

An exchange occupies a different regulatory position than a broker-dealer or an ATS. Under US securities law, an exchange is not a participant in the market but is the market itself, operating under a distinct registration and oversight framework.

The Securities Exchange Act of 1934 defines an exchange based on function, not branding. In practical terms, a system is viewed as an exchange when it brings together orders from multiple buyers and sellers and uses established, non-discretionary methods to match those orders.

If a platform performs the above functions at scale, it may fall within the SEC’s exchange definition, even if it doesn’t call itself an exchange.

Why Exchanges Are Self-Regulatory Organizations (SROs)

An exchange’s status as a self-regulatory organization places it in a fundamentally different position than other trading venues. Alongside operating the market, an exchange is tasked with regulating its members and enforcing compliance with its own rules.

These obligations include active market monitoring, formal rulemaking, disciplinary authority, and continuous engagement with the SEC. This layered regulatory role separates exchanges from ATSs, which remain subject to broker-dealer supervision rather than acting as regulators themselves.

See also:

Who Can Access an Exchange and Why Broker-Dealers Matter

Access to an exchange is not open to the public. Participation requires membership, which is typically limited to broker-dealers that meet financial, operational, and compliance standards.

As a result, broker-dealers act as the gateway between investors and exchanges, routing orders, managing execution, and carrying responsibility for customer-facing obligations. For fintechs evaluating market structure, this distinction often determines whether the business model sits upstream of an exchange, inside it, or alongside it.

Need help with broker-dealer compliance?

Fill out the form below and our experts will get back to you.

What Is an Alternative Trading System (ATS)?

An alternative trading system sits between a broker-dealer and an exchange in the market structure. It’s not a separate registration category on its own. An ATS is a trading venue operated by a registered broker-dealer, subject to additional regulatory requirements under SEC Regulation ATS.

Under Regulation ATS, a system is considered an ATS if it brings together buyers and sellers of securities and provides a way to interact with orders. Yet it doesn’t qualify or register as a national securities exchange.

Learn more about Regulation ATS →

The defining point is its functions. Regulators look at whether the system facilitates multilateral trading interests and how it matches orders. Calling a platform a “network” or “protocol” does not change this analysis.

Why an ATS Is Considered a “Mini Exchange”

An ATS often looks exchange-like when viewed through an economic lens. Orders are brought together, interaction is governed by defined logic, and pricing emerges within the system’s boundaries.

The comparison ends at regulation. An ATS doesn’t regulate the market or its participants. It operates under the authority of its broker-dealer, without self-regulatory powers or independent rulemaking responsibility.

Why Every ATS Must Be a Broker-Dealer

An ATS cannot exist without a broker-dealer at its core. The broker-dealer is responsible for compliance, supervision, AML, recordkeeping, and regulatory reporting related to the system’s operation.

This structure places direct accountability on the broker-dealer for how the ATS operates in practice. For fintechs, this often means the ATS model brings more regulatory responsibility than expected, particularly as participation expands or trading volume increases.

For firms considering this structure, understanding ATS requirements early helps avoid building a platform that unintentionally exceeds its approved scope. In practice, this evaluation often intersects with broader regulatory strategy and product design decisions.

Learn more about ATS regulation and requirements →

Broker-Dealer vs. ATS

The difference between a broker-dealer and an ATS is often misunderstood because the two are closely connected. One is a regulated firm. The other is a trading system operated by that firm. They are not parallel classifications, and treating them as such leads to flawed regulatory analysis.

Why Broker-Dealer and ATS Are Not Peer Classifications

Broker-dealer status comes first and establishes the legal entity, the supervisory structure, and the regulatory obligations. An ATS sits on top of that foundation as one way the broker-dealer may choose to operate.

The sequencing matters. A broker-dealer can engage in a wide range of activities without ever running an ATS. The reverse is not true. An ATS cannot function unless a broker-dealer takes full responsibility for the system.

At bottom, the broker-dealer is what regulators regulate. The ATS is simply one operating model within that framework.

A broker-dealer’s baseline obligations apply regardless of whether it operates an ATS. These include supervision, books and records, AML, customer protection, and FINRA reporting. When an ATS is introduced, additional requirements apply to the system itself.

Those added obligations typically relate to:

How orders interact within the system

Who is permitted to access the venue

What disclosures must be made to regulators and participants

The result is an additional layer of compliance structure, not a replacement of broker-dealer rules.

Common Misunderstandings About This Relationship

A frequent misconception is that operating an ATS is an alternative to being a broker-dealer. Another is that a firm can “add” an ATS without materially changing its compliance posture.

In practice, launching an ATS often reshapes supervision, surveillance, and regulatory reporting across the entire firm, not just the platform. This is why regulators evaluate the broker-dealer and the ATS as a single, integrated operation rather than as separate components.

For fintechs, recognizing this relationship early helps frame realistic timelines, staffing needs, and regulatory strategy before the system goes live.

ATS vs. Exchange

ATSs and exchanges are often compared because they both facilitate trading. That similarity is superficial. The regulatory treatment of an ATS versus an exchange reflects fundamentally different roles in the market, even when the underlying technology looks comparable.

An ATS operates within the broker-dealer regulatory framework. It’s permitted to match trading interest, but it does so under the supervision and responsibility of its broker-dealer operator. The ATS doesn’t regulate participants beyond the operator’s terms of access.

An exchange occupies a broader position. It operates the marketplace and regulates it. That includes setting market-wide rules, overseeing participant conduct, and enforcing compliance through disciplinary processes. This authority is what separates an exchange from every other trading venue.

The difference between an ATS and an exchange is not about size or sophistication. It’s about authority. An ATS has no independent regulatory power. Oversight flows through the broker-dealer and FINRA, with the SEC maintaining ultimate authority.

An exchange, by contrast, carries self-regulatory responsibilities. It works directly with the SEC, proposes and enforces its own rules, and maintains surveillance over its market. This expanded role brings a different compliance burden and a different regulatory relationship.

Broker-Dealer vs. ATS vs. Exchange: Side-by-Side Comparison

Understanding the difference between a broker-dealer, an ATS, and an exchange becomes easier when viewed side by side:

Category | Broker-Dealer | ATS | Exchange |

|---|---|---|---|

Core role | Market participant | Trading venue operated by a broker-dealer | Centralized securities market |

Registration | SEC and FINRA | Broker-dealer + Reg ATS | Centralized securities market |

Who operates it | The firm itself | A broker-dealer | Exchange entity |

Who can participate | Customers and counterparties | Broker-dealers and approved participants | Exchange members (typically broker-dealers) |

Regulatory authority | SEC and FINRA | SEC and FINRA | SEC |

Market surveillance | Firm-level | Through broker-dealer | Exchange-level, market-wide |

Rulemaking power | No | No | Yes |

Primary regulator | SEC / FINRA | SEC / FINRA | SEC (with SRO authority) |

See also:

Who Regulates Broker-Dealers, ATSs, and Exchanges

There’s a meaningful difference in regulatory oversight across broker-dealers, ATSs, and exchanges:

Role of the SEC: Oversees broker-dealer registration, reviews ATS filings under Regulation ATS, and directly regulates national securities exchanges. For exchanges, the SEC maintains an active role in rule approvals and market oversight. For broker-dealers and ATSs, the SEC sets the regulatory framework while delegating much of the routine supervision to FINRA.

Role of FINRA: FINRA is the primary regulator for broker-dealers and, by extension, ATSs. It conducts examinations, reviews disclosures, and enforces compliance with SEC rules and FINRA rules. ATSs are examined through their broker-dealer operators, meaning ATS-related issues are typically reviewed as part of standard broker-dealer exams rather than through a separate process.

How oversight differs across classifications: Exchanges regulate their members while still subject to SEC oversight. Broker-dealers and ATSs don’tregulate others; they are regulated entities. This distinction drives how supervision works in practice. Broker-dealers and ATSs are overseen through exams and enforcement, while exchanges operate under a dual role as both market operators and self-regulatory organizations.

Common Compliance Challenges in ATS and Exchange Models

When firms explore ATS or exchange structures, attention tends to stay on technology and demand. Regulatory issues typically come into focus later, once the mechanics of the platform are examined in detail.

Over-Engineering Before Regulatory Clarity

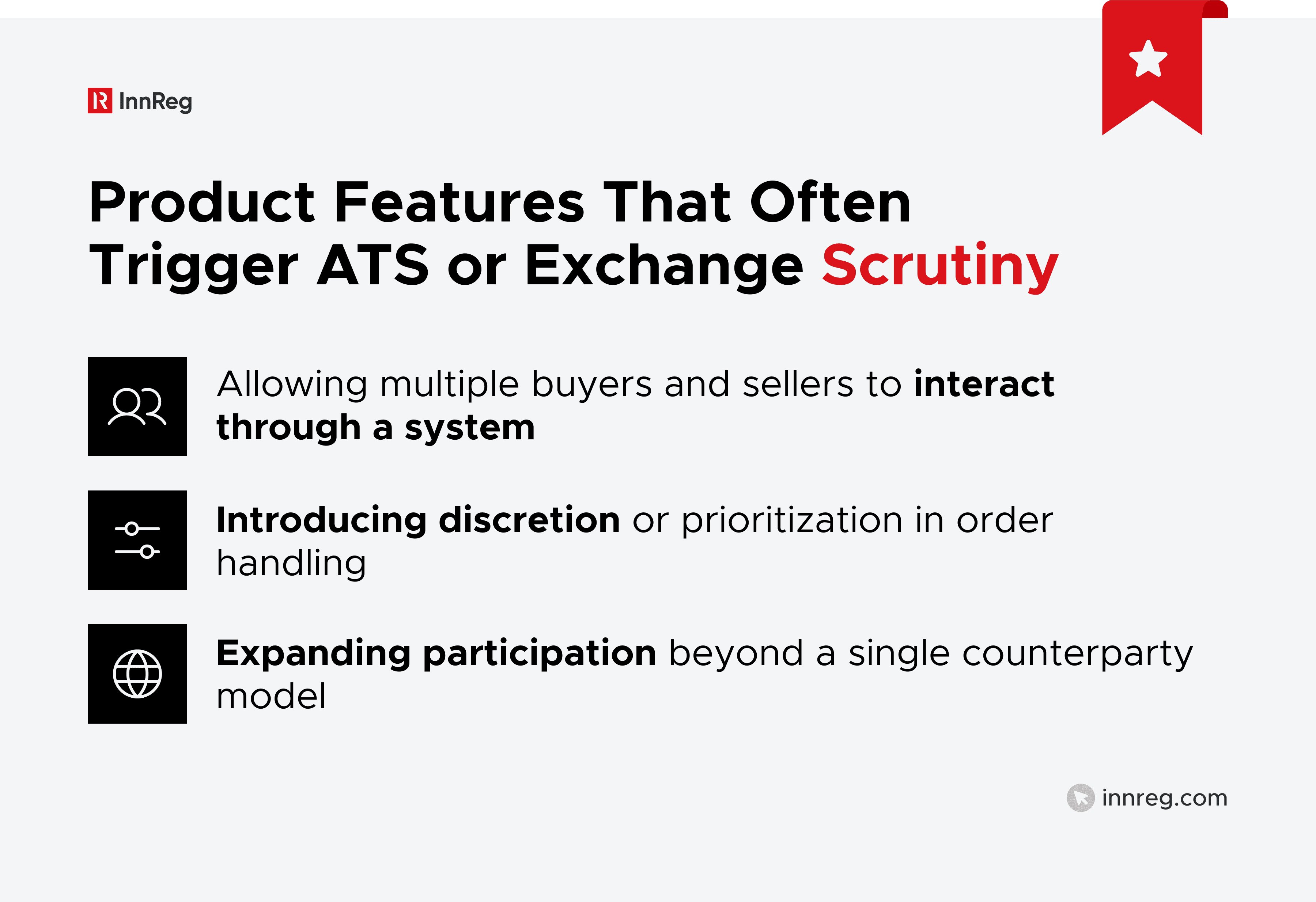

Product teams sometimes design advanced matching logic or access models before confirming how regulators will classify the platform. Features intended to improve liquidity or efficiency can inadvertently push the system into ATS or exchange territory.

Reworking core functionality after regulatory feedback is costly and time-consuming, especially once customers or counterparties are already active on the platform.

Building Matching Logic That Unintentionally Triggers ATS Status

Bilateral trading models rarely stay static. As platforms add order books, matching logic, or execution rules, the nature of the interaction changes. At that point, regulators may view the system as an ATS rather than a standard broker-dealer workflow, with corresponding regulatory requirements.

Underestimating Compliance Ownership and Cost

A common inflection point appears when platforms move beyond one-to-one trading. Features like automated matching or priority rules can alter the regulatory classification.

What was designed as a broker-dealer process may now fit the ATS definition, triggering additional regulatory obligations.

How to Determine the Right Classification for Your Business

Choosing between a broker-dealer, ATS, or exchange classification is not a theoretical exercise. It depends on how your platform actually operates and how regulators are likely to view that operation.

The right classification follows function, not intent, and it is often clearer once the full trading workflow is mapped.

Questions Regulators Will Ask

Regulators look first at how a platform operates. Labels and positioning take a back seat to the mechanics of order handling and execution.

Who has access, how orders are prioritized, whether interaction is multilateral, and where discretion exists all factor into the analysis. Once those elements are understood, classification questions tend to resolve themselves.

How to Evaluate Your Trading Workflow

Classification questions usually become clearer when a firm maps the full lifecycle of a trade. Looking at onboarding, order entry, matching, execution, and post-trade processes together provides a more accurate picture than reviewing any single feature in isolation.

Regulatory inflection points often appear as platforms evolve. Changes such as wider participation, automated matching, or multilateral interaction can alter how a broker-dealer model is viewed.

When to Involve Compliance Early

Compliance has the most impact when it is part of the design process. Once development is finished, choices narrow and changes become more expensive.

Involving compliance earlier allows product decisions to reflect regulatory realities, which is especially relevant for fintechs managing limited resources and long-term growth. That input often influences licensing approach, staffing needs, and the broader regulatory plan.

InnReg helps fintech develop efficient regulatory strategies →

—

The distinction between a broker-dealer, an ATS, and an exchange ultimately comes down to function. How orders interact, who controls execution, and how participants access the platform drive regulatory classification, not labels or intent.

For fintechs, these questions surface early in product design and resurface as platforms scale. Understanding where a model fits before development gets too far helps avoid rework, delays, and regulatory friction later.

See also:

Frequently Asked Questions

1. Can a Broker-Dealer Operate Without an ATS?

Yes. Most broker-dealers operate without ever running an ATS. The two are not bundled classifications, and broker-dealer registration doesn’t require or assume ATS operation.

A broker-dealer can execute trades for customers, act as a market maker, route orders to exchanges, or trade for its own account, all without introducing an ATS. The decision to operate an ATS is a strategic choice based on business model and market opportunity, not a regulatory default.

Operating an ATS adds obligations and oversight, even for firms already registered as broker-dealers. Many firms avoid that added structure intentionally, preferring simpler execution models that still meet their commercial objectives.

2. Why Aren't All Broker-Dealers ATSs?

An ATS is only necessary when a broker-dealer chooses to match multiple buyers and sellers through a proprietary system. Most broker-dealers don’t need to operate a matching venue to serve their customers or generate revenue.

Firms that focus on execution services, advisory work, or proprietary trading typically route orders to existing exchanges or liquidity providers rather than building their own marketplace. These models require broker-dealer registration but never cross into ATS territory.

The obligations that come with ATS operation also act as a natural filter. Firms that don’t plan to facilitate multilateral trading generally have no reason to incur the added compliance burden. Only when the business model depends on matching participants internally does the ATS structure become relevant.

3. Can an ATS Become an Exchange?

Converting from an ATS to an exchange is legally possible but operationally demanding. The transition is not a simple upgrade. It requires a fundamental shift in both regulatory structure and institutional responsibility.

Exchanges carry self-regulatory authority, which means they regulate their members, enforce market rules, and maintain active relationships with the SEC on oversight matters. ATSs don’t have this power. They operate under broker-dealer supervision and remain subject to external regulation rather than exercising it themselves.

Moving from one structure to the other involves more than filing forms. The firm must build rulemaking processes, surveillance infrastructure, enforcement capabilities, and governance structures designed to function as a regulator. For most ATSs, this level of operational expansion is neither necessary nor feasible.

4. Why Do Most ATSs Never Convert?

Most ATSs look at exchange registration and decide against it. The benefits don’t cover the cost.

Running an exchange means running a regulatory operation. That includes writing rules for the market, getting tSEC approval, and keeping them current as conditions change. It’s not a one-time project. The work continues for as long as the exchange exists.

Surveillance responsibility grows substantially. Exchanges don’t just watch their own venue. They track member conduct across the market, which means broader systems, more personnel, and a compliance function that operates at a different scale than ATS oversight.

Enforcement comes with exchange status regardless of whether the firm wants it. Exchanges investigate members, run hearings, and hand out sanctions. The infrastructure can’t be optional or phased in later. Once registered, regulatory work is embedded in daily operations.

5. What Changes When an ATS Seeks Exchange Registration?

The regulatory model reverses. An ATS gets supervised. An exchange does the supervising.

Governance becomes mandatory and formal. Boards need independent directors. Compliance needs committees. Rulemaking shifts from compliance work to core operations, wherein exchanges write market rules and continuously manage SEC approval.

The surveillance scope also expands to cover member activity across all venues, not just the platform. That changes the technology requirements and staffing model.

Hiring increases across legal, compliance, surveillance, and operations. The SEC relationship moves from periodic filings to ongoing engagement. Preparation typically spans years. Most ATSs evaluate this and determine their business doesn’t need it.

Tarik is a Principal Compliance Consultant at InnReg with over 5 years of experience advising fintech clients across broker-dealer, RIA, and money transmitter verticals. He holds FINRA Series 3, 7, 24, 57, 63, 79, and 99 licenses, with expertise in regulatory strategy, supervisory systems, and compliance roadmap implementation.

How Can InnReg Help?

InnReg is a global regulatory compliance and operations consulting team serving financial services companies since 2013.

We are especially effective at launching and scaling fintechs with innovative compliance strategies and delivering cost-effective managed services, assisted by proprietary regtech solutions.

If you need help with broker-dealer compliance, reach out to our regulatory experts today:

Related Articles

Featured LinkedIn Posts