What Is a Neobank? Definition, Examples, and Market Trends

Neobanks have become one of the fastest-growing segments in fintech, but many founders and compliance teams still ask the same question: what is a neobank, and how is it different from a traditional bank? These firms are reshaping financial services, yet their legal and regulatory footing is more complex than it appears.

This article breaks down the fundamentals: what neobanks are, how they operate, and how regulators view them in the United States and abroad. You’ll see where the compliance challenges arise and how leading players in 2026 are navigating those pressures.

We’ll also look at market trends shaping the sector, from adoption growth to regulatory scrutiny, and highlight practical lessons for fintech founders and compliance professionals. So let’s start with the basics:

At InnReg, we support neobanks through every stage of their compliance journey. We help with licensing, policy development, and operational compliance functions tailored to fast-moving fintech teams.

Neobank Definition

A neobank is a financial technology company that delivers banking-like services entirely online. These digital banking solutions operate through apps or web platforms without maintaining physical branches. They typically focus on core offerings such as checking, savings, debit cards, and payments, while relying on technology to streamline the customer experience.

The critical distinction is that most neobanks are not licensed banks. Instead, they partner with regulated banks to hold deposits and provide FDIC insurance. This structure allows them to move quickly and innovate without carrying the full capital and compliance burdens that come with a banking charter.

Neobanks vs. Traditional Banks vs. Online Banks

Neobanks may be confused with traditional banks or online banks. However, the legal entity is entirely different. Here are the key differences between neobanks, vs. traditional banks, and. online banks:

Feature | Neobank | Traditional Bank | Online Bank |

|---|---|---|---|

Bank charter | Usually no charter; partners with licensed banks | Holds a charter | Holds a charter |

Branch network | No physical branches | Nationwide or regional branches | No branches |

Deposit insurance | Through a partner bank if structured properly | Direct FDIC coverage | Direct FDIC coverage |

Product scope | Focused (checking, debit, payments) | Broad (loans, mortgages, investments) | Similar to traditional, but digital-only |

Regulatory oversight | Indirect, via partner banks | Direct oversight | Direct oversight |

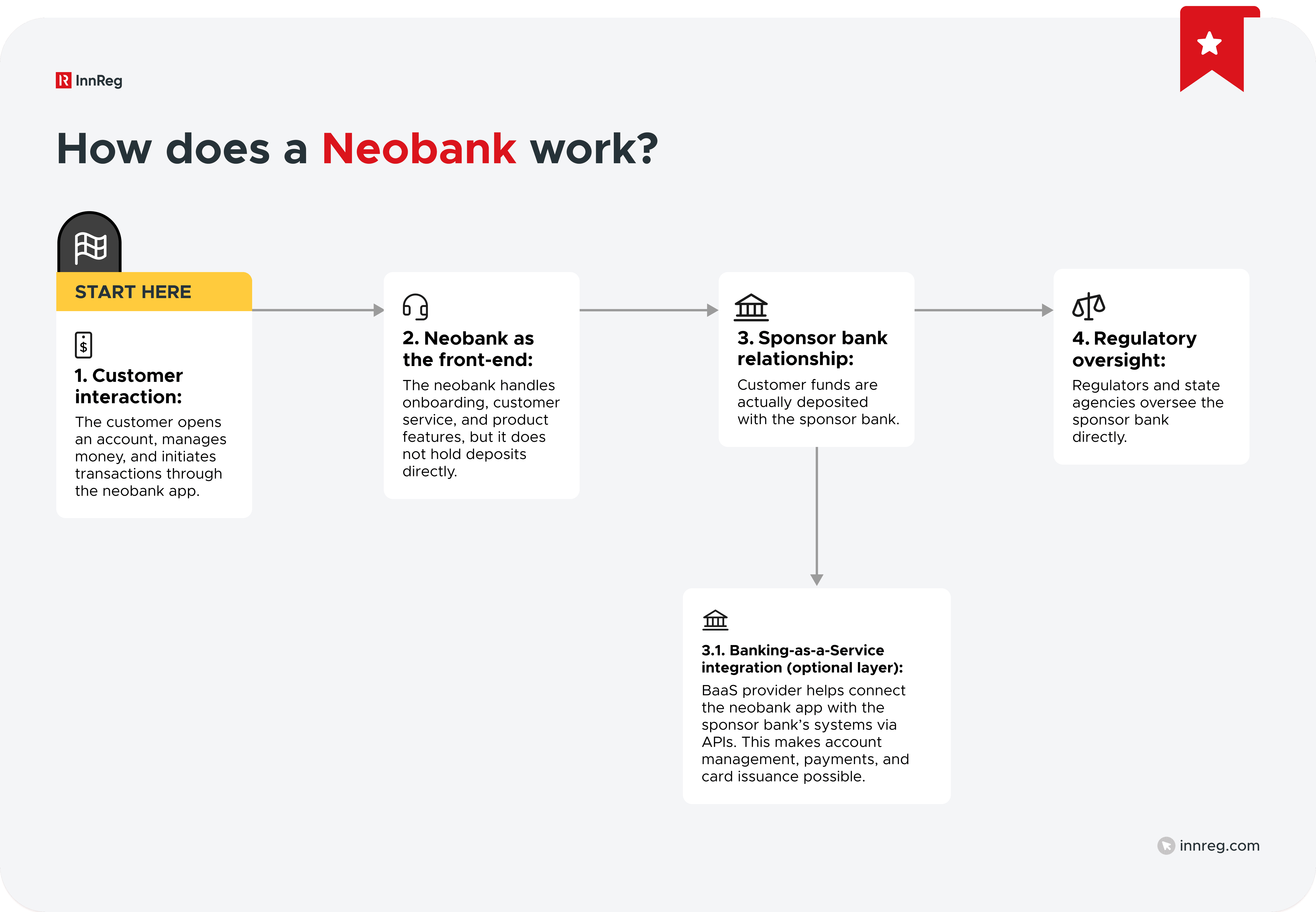

How Neobanks Work

Neobanks operate by combining financial infrastructure from licensed banks with customer-facing technology built by fintech firms. Instead of maintaining their own bank charter, most digital banking solutions rely on a sponsor bank to handle deposits, compliance obligations, and FDIC insurance. This partnership model allows them to focus on product design, user experience, and customer acquisition.

The sponsor bank relationship is key. Customer funds are deposited at the partner bank, which provides insurance coverage up to standard limits. Meanwhile, the neobank manages the app, onboarding flow, and customer support. This arrangement gives startups flexibility but also subjects them to oversight through their banking partner.

Common Products and Services

While offerings vary, most neobanks focus on a set of core products:

Checking and savings accounts with low or no monthly fees

Debit cards tied to those accounts, generating interchange revenue

Early wage access features that release direct deposits a day or two ahead of traditional schedules

Peer-to-peer transfers and low-cost international payments

Budgeting and financial management tools that are built into the app

Some neobanks expand further by integrating lending products, stock trading, or even crypto services. These are usually delivered through additional licenses, third-party integrations, or affiliated entities. Each expansion requires careful compliance planning since every new service can trigger oversight by a different regulator.

Are Neobanks Real Banks?

For fintech founders and compliance officers, one of the first questions is whether a neobank qualifies as a bank in the legal sense. The short answer is that most neobanks are not banks.

They don’t hold their own charters and therefore cannot independently accept deposits or make loans. Instead, they operate under arrangements with licensed banks that provide the regulatory foundation.

Legal Status in the US

In the United States, the definition of a bank is tied directly to whether the entity holds a charter. Only institutions with a national or state banking charter are considered banks under federal law.

Neobanks usually do not pursue a charter, given the cost, time, and regulatory scrutiny required. Instead, they rely on sponsor banks that remain legally responsible for compliance obligations such as BSA/AML, consumer protection, and reporting.

A small number of firms have taken the opposite route. Varo Bank and SoFi are examples of digital banking solutions that invested the time and resources to obtain full charters, becoming regulated banks in their own right. This path brings autonomy, but also full exposure to capital requirements, examinations, and enforcement actions.

FDIC Insurance and How it Applies

FDIC insurance is another area of frequent confusion. Neobanks themselves are not covered by FDIC insurance. Instead, customer deposits are held at a partner bank that provides insured accounts. The insurance applies only because the deposits legally reside within the licensed bank, not within the fintech.

This distinction matters for branding and customer communications. Founders need to be careful about how FDIC coverage is described. Marketing should clearly state that deposits are insured through the partner bank. Compliance teams must review language closely to avoid misleading claims, since regulators have taken action when fintechs blurred this line.

Common Misconceptions About Neobank Branding

Branding often creates regulatory headaches for fintech founders. The most frequent issue is assuming a neobank can market itself as a bank. Without a charter, this not only proves to be inaccurate, but it can also lead to enforcement.

Here are common pitfalls:

Calling Yourself a Bank: In 2021, California regulators required Chime to stop using “Chime Bank” in its branding. The case made clear that fintechs must use precise language when describing their services. The company had to clarify that it is a fintech and that partner banks hold the deposits.

Overstating FDIC Protection: Deposits are FDIC-insured only through the partner bank, not through the neobank itself. Marketing must explain this clearly. That distinction must be explicit in public communications, customer agreements, and even in web domains.

Misusing Product Terms: Using “savings account” or “banking services” without proper context can mislead customers if the offering does not meet regulatory definitions. Compliance teams should review all marketing and customer-facing materials, not just legal agreements, to prevent misleading claims.

Blurring financial products: Combining deposits, investments, or crypto under a single brand can confuse users if disclosures are weak.

For fast-moving startups, branding may feel secondary to growth. In reality, it is a regulatory flashpoint that can erode customer trust if handled carelessly. Careful attention to language upfront can prevent enforcement actions and protect credibility with customers.

Neobank Regulation in the US

Neobanks sit in a complicated regulatory environment. Since most do not hold charters, their compliance obligations flow through the licensed banks they partner with. Still, multiple federal and state agencies have authority over aspects of their operations.

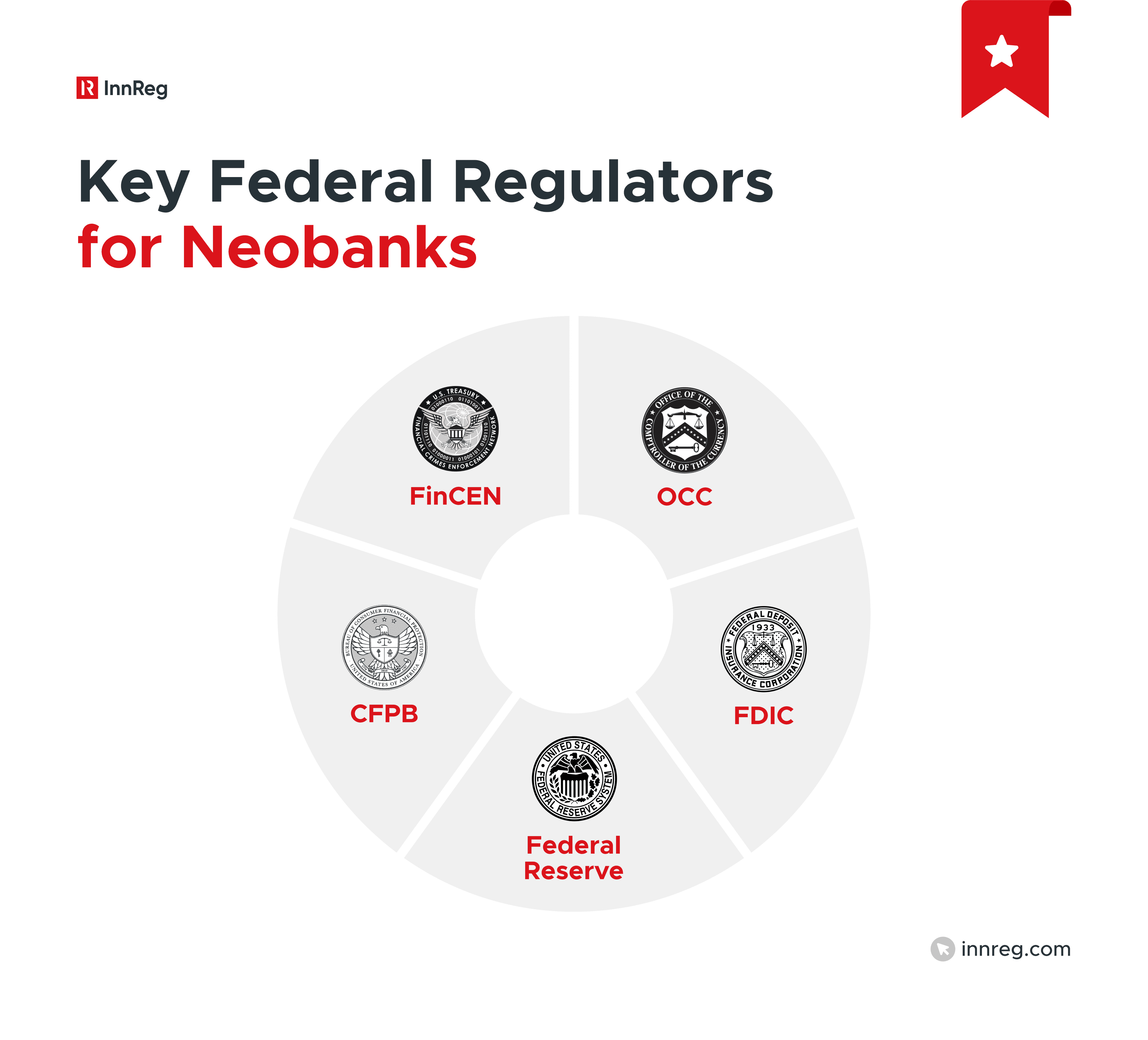

Key Federal Regulators

Several regulators play a role in overseeing the banking system, and by extension, the neobanks that rely on sponsor banks:

Office of the Comptroller of the Currency (OCC): Oversees national banks that act as partners. The OCC has issued guidance on third-party risk management in bank-fintech partnerships.

Federal Deposit Insurance Corporation (FDIC): Provides deposit insurance and supervises state-chartered banks that are not members of the Federal Reserve. Neobanks must communicate clearly that FDIC coverage applies through their partner banks.

Federal Reserve: Supervises bank holding companies and plays a role when neobanks partner with Fed member banks.

Consumer Financial Protection Bureau (CFPB): Enforces consumer protection laws, including Regulation E (electronic payments) and Regulation DD (truth in savings). It can also act directly against unfair or deceptive marketing practices.

Financial Crimes Enforcement Network (FinCEN): Administers federal AML rules under the Bank Secrecy Act. Even without a charter, neobanks that provide money transmission or payments may fall under MSB registration requirements.

State-Level Oversight and Licensing

States can regulate fintech firms directly, especially when the product involves money transmission or lending. If a digital banking solution offers products that look like money transmission or lending outside of its sponsor bank’s framework, it may need state licenses.

California’s action against Chime highlighted that states will step in if fintech branding or practices cross legal lines. State attorneys general also monitor consumer complaints tied to fees or misleading terms.

Bank-Fintech Partnership Compliance Obligations

Because sponsor banks are ultimately responsible for regulatory compliance, they impose strict oversight on their fintech partners. Common requirements include:

Implementing a Bank Secrecy Act/AML program, including customer identification and transaction monitoring.

Providing consumer disclosures that meet federal requirements, such as Reg E error-resolution notices.

Submitting to audits, reporting, and regular reviews by the sponsor bank’s compliance department.

Maintaining cybersecurity and vendor management standards consistent with banking regulations.

For fintech founders, this oversight can appear like direct regulation. In practice, this means the bank partner acts as both enabler and gatekeeper, with the power to restrict or terminate a neobank’s program if compliance risks are not well-managed.

See also:

International Neobank Regulation

Neobank regulation varies widely across jurisdictions. Some regions have created new categories of digital banking licenses, while others apply existing banking and payments rules to fintech firms. For founders operating internationally, understanding these distinctions is critical to structuring compliant offerings.

Need help with neobank compliance?

Fill out the form below and our experts will get back to you.

European Union and PSD2 framework

The EU’s Payment Services Directive 2 (PSD2) laid the foundation for open banking and has shaped how neobanks develop. Many fintechs began as electronic money institutions (EMIs) under PSD2, allowing them to hold customer funds and process payments without a full banking license.

Over time, firms like Revolut and N26 moved to acquire full charters, expanding into deposits and lending. The EU approach has created a tiered path for growth but comes with strict requirements on capital, safeguarding of funds, and strong customer authentication.

UK Approach to Challenger Banks

The UK regulator, the Financial Conduct Authority (FCA), together with the Prudential Regulation Authority (PRA), has been proactive in licensing digital-only challengers. Firms such as Monzo and Starling were granted full banking licenses early, which let them compete directly with incumbents.

The UK also uses a “mobilization” process, where new banks can start with restrictions while building compliance and operational capacity. This framework has helped challengers scale but also subjected them to close supervision, particularly around AML and financial crime controls.

Asia-Pacific Digital Bank Licenses

Several Asia-Pacific jurisdictions have launched specialized digital bank licensing regimes. Singapore and Hong Kong introduced digital-only licenses in 2019, requiring significant capital commitments and local incorporation.

Australia also created a framework for neobanks, though some early entrants struggled to maintain profitability. These licenses reflect a more cautious stance: regulators allow new digital players but require them to meet many of the same prudential standards as traditional banks from the start.

Latin America and Financial Inclusion

Latin America has seen the rapid adoption of neobanks, particularly in Brazil and Mexico, where large portions of the population were previously unbanked. Regulators in the region have often supported fintech compliance and innovation as a way to expand financial inclusion, though they also apply local banking and payments rules to neobank models.

Brazil’s Nubank is the standout case, operating under a full banking license and now serving tens of millions of customers across the region. Other markets, such as Mexico and Colombia, are tightening requirements as fintech adoption grows.

Compliance Challenges for Neobanks

Operating a neobank means navigating a set of compliance challenges that are both technical and regulatory. Because most neobanks are not chartered banks, their obligations come through sponsor banks or separate licenses. Each stage of growth introduces new risks that founders and compliance teams must address.

Deciding on Licensing or Chartering

The first major decision is whether to remain a fintech partnered with a bank or pursue a charter. Partnering allows faster market entry but creates dependence on another institution’s oversight. Securing a charter brings autonomy but requires capital, infrastructure, and the ability to meet direct regulatory expectations.

See also:

AML and KYC Requirements

AML and KYC rules apply to neobanks through their sponsor banks or MSB registration. This means strong onboarding processes, identity verification, and transaction monitoring. Weak programs can quickly lead to regulatory scrutiny or even fines, as seen in recent enforcement cases against fintechs.

Based on InnReg’s experience of working with 100+ fintechs, Regly helps firms apply KYC/KYB rules and conduct AML screening →

Consumer Protection and Disclosure Rules

Thirdly, Neobanks must also comply with consumer laws such as Reg E (electronic fund transfers) and Reg DD (truth in savings). Disclosures about fees, deposit insurance, and error resolution must be built directly into the customer experience. Compliance teams need to review marketing claims and product labels carefully, since regulators often act on misleading impressions.

Data Security and Privacy Obligations

Operating entirely online means data protection is central to compliance. Neobanks must meet expectations under the Gramm-Leach-Bliley Act and state privacy rules such as California’s CCPA. Sponsor banks also require proof that fintech partners can safeguard sensitive customer data through encryption, authentication, and incident response planning.

Managing Outsourcing and Third-Party Risks

Most neobanks rely heavily on outsourced technology and service providers, from cloud hosting to payment processors. Regulators expect banks, and by extension their fintech partners, to manage third-party risk carefully.

This includes audits, vendor contracts, and contingency planning. For a neobank, failing to manage a vendor issue can have direct regulatory and reputational consequences.

Recent Enforcement and Regulatory Trends

Regulators have increased their focus on neobanks and fintech firms, particularly in how they brand, manage AML obligations, and structure partnerships. Enforcement actions in recent years have highlighted the risks of moving quickly without strong compliance.

Branding Restrictions and the Chime Case

In 2021, California regulators required Chime to stop marketing itself as a bank. The company had used “Chime Bank” in its branding, even though it did not hold a charter.

The settlement reinforced a simple rule: without a banking license, a fintech cannot call itself a bank. Chime was forced to update its website, disclaimers, and advertising to make clear that deposits were held by partner banks.

Money Transmitter Settlements

Enforcement has also targeted weak AML programs. In 2025, Block, Inc. (Cash App) paid $80 million to settle allegations from 48 states that it failed to implement adequate customer due diligence and transaction monitoring.

Around the same time, Wise agreed to a multistate settlement over gaps in its AML program. Both cases show that regulators expect fintechs offering money transfers to meet the same standards as banks, even if they operate through different structures.

Interagency Guidance on Bank-Fintech Partnerships

Federal regulators have also updated their approach to partnerships. In 2023, the OCC, FDIC, and Federal Reserve issued joint guidance on third-party risk management.

The message was clear: sponsor banks must closely oversee their fintech partners, and that expectation flows down to neobanks. For fintech founders, this means compliance reviews, audits, and reporting are prerequisites for keeping partnerships in place.

Leading Neobanks in 2026

To understand the latest developments in the neobank landscape, let’s examine some leading examples. These digital banking solutions highlight how different models and regulatory approaches play out in practice.

Chime

Chime remains the largest US neobank by customer count. It operates through partnerships with The Bancorp Bank and Stride Bank, which hold deposits and provide FDIC insurance. Chime focuses on no-fee accounts, early wage access, and budgeting tools. Its rapid growth also brought scrutiny, particularly around branding, which regulators required it to adjust.

Varo Bank

Varo began as a partner-based neobank but obtained a national bank charter in 2020. This made it the first US neobank to operate independently of a sponsor bank. The charter allows Varo to offer lending products and expand services under direct OCC supervision. The move gave it autonomy but also subjected it to higher capital and compliance standards.

Revolut

Revolut started as an e-money institution in the UK and now holds a full banking license in the European Economic Area. It has built a “super app” with multi-currency accounts, stock trading, crypto, and payments. In the US, it still relies on a sponsor bank, showing how its regulatory structure changes across jurisdictions.

Monzo and Starling Bank

Both Monzo and Starling were early recipients of UK digital bank licenses. They operate as fully regulated banks under the FCA and PRA. Their focus on customer experience and digital-first operations helped them gain market share quickly. Importantly, both have now reached profitability, showing that digital challengers can build sustainable business models.

Nubank

Brazil’s Nubank has become one of the largest neobanks worldwide, with tens of millions of customers. It holds a banking license and has expanded across Latin America, targeting underserved populations. Its growth illustrates how neobanks can drive financial inclusion in markets with low traditional banking penetration.

Market Trends Shaping Neobanks

In 2026, neobanks are no longer “new entrants.” They are competing directly with traditional banks and facing closer scrutiny from regulators. The most important trends for founders and compliance professionals center on scale, sustainability, and oversight.

See also:

Growth in Customer Adoption

Adoption keeps rising, especially among younger consumers in the US and among unbanked populations in Latin America and Asia. Higher volumes mean more exposure to fraud, AML monitoring, and cross-border compliance requirements. Scaling customer acquisition is no longer just a growth question; it is a compliance and risk management issue.

Monetization and Path to Profitability

Revenue models are under pressure. Many neobanks rely on interchange fees, which alone rarely support profitability. This has led to expansion into lending, premium subscriptions, and cross-selling financial products. Firms that cannot diversify risk become dependent on venture funding or limited revenue streams.

Convergence with Traditional Finance

The gap between digital challengers and incumbents is narrowing. Established banks are adopting features like early wage access, while some neobanks pursue charters to operate independently. Others collaborate with community banks or become providers of Banking-as-a-Service.

Expansion into Financial Super Apps

A growing number of neobanks are moving beyond deposits and payments to offer investments, insurance, and crypto. While this broadens revenue, it creates new compliance responsibilities under securities, insurance, and commodities law. For compliance officers, each expansion means managing new regulators and risk profiles.

Increasing Regulatory Scrutiny

Regulators have moved past observation and into action. Bank partners are under pressure to monitor fintech programs more closely, and agencies have signaled that more enforcement is coming. Here are some of the most recent regulatory scrutinies:

In July 2024, OCC, FDIC, and the Federal Reserve published a Joint Statement warning banks about risks in third-party arrangements related to deposit products and services. This signals that regulators expect banks to increase controls over partner fintechs.

In 2024, there were multiple FDIC consent orders citing deficiencies in banks’ oversight of their fintech partners, especially regarding Bank Secrecy Act / AML programs and third-party risk.

In June 2024, Evolve Bank & Trust faced action by the Federal Reserve for deficiencies in its AML, risk management, and consumer compliance programs. Neobanks using BaaS must assume their risk posture will be examined closely.

In short, neobanks must now be prepared for regular audits, stricter marketing reviews, and higher vendor risk standards.

Key Takeaways for Founders and Compliance Teams

Neobanks have redefined how financial services are delivered, but growth brings regulatory complexity. Most operate without charters, which means their obligations flow through sponsor banks. That arrangement allows for innovation but also puts compliance under constant scrutiny.

As customer bases grow, risks scale quickly. Larger transaction volumes demand stronger AML and KYC controls, while adding services like lending or investments pulls neobanks into new regulatory regimes. Regulators have already acted against fintechs that blurred the line between being a technology provider and a licensed bank.

At InnReg, we specialize in guiding fintech innovators through these challenges. Our team works as an outsourced compliance department, bringing deep experience in financial services, practical processes, and cost-effective solutions compared to in-house hires.

Whether you’re structuring a neobank, refining your compliance program, or responding to new regulatory pressures, we help align innovation with compliance so you can scale confidently. Speak with an expert today!

Ani is a Senior Compliance Consultant with over 10 years of experience in legal and regulatory compliance across fintech, RegTech, and cross-border payments. She has held roles at Remote and EY, with expertise in AML, GDPR, financial crime, and EU regulatory frameworks. She holds CAMS and CIPP/E certifications.

How Can InnReg Help?

InnReg is a global regulatory compliance and operations consulting team serving financial services companies since 2013.

We are especially effective at launching and scaling fintechs with innovative compliance strategies and delivering cost-effective managed services, assisted by proprietary regtech solutions.

If you need help with neobank compliance, reach out to our regulatory experts today:

Related Articles

Featured LinkedIn Posts