How to Prevent GPS Spoofing in Fintech

Location controls sit at the center of how fintech companies manage regulatory risk. They determine who can access a product, where transactions can happen, and whether a firm is operating within its licensing and sanctions boundaries.

GPS spoofing breaks that system by letting users fake their physical location. The fallout goes beyond fraud. It can trigger unauthorized market access, sanctions exposure, and failures in the compliance assumptions your program depends on.

This article covers how to prevent GPS spoofing in fintech, with a focus on the regulatory context. We look at the methods that matter in practice, what regulators are looking for, and how compliance teams can design location controls that are both defensible and realistic for fast-moving fintech operations.

At InnReg, we help fintechs address sanctions and jurisdictional access risk, including controls that account for GPS spoofing and VPN-based evasion. If you need help with compliance program design, monitoring workflows, or ongoing operations support, contact us today.

What Is GPS Spoofing?

GPS spoofing occurs when a device is intentionally made to report a false physical location. In other words, if your device is in London, GPS spoofing can make your location appear to be in New York City. This can be done through:

Software

Network manipulation

Modified device environments that override normal location signals

From a compliance standpoint, many fintech controls rely on that assumption without treating location as a manipulable input.

In practice, spoofing is not limited to sophisticated attacks. Consumer-grade tools are widely available and easy to use, which makes location manipulation a realistic risk for regulated products.

It is also important to distinguish GPS spoofing from related concepts:

GPS Spoofing | VPN Usage | Emulator or Rooted Devices |

|---|---|---|

Falsifies device-reported location | Masking IP-based location | Runs apps in modified environments |

Undermines geofencing and jurisdictional controls | Defeats IP-only blocking strategies | Enables broader control bypass, including location |

What Is GPS Spoofing in a Fintech Context?

In fintech, GPS spoofing is primarily used to bypass jurisdiction-based controls. Users manipulate their apparent location to access products, features, or markets that are restricted based on geography.

This typically affects fintechs that rely on location for:

Sanctions and country-level restrictions

State-based licensing and product eligibility

Fraud and account abuse detection

The compliance issue is not the spoofing itself, but the downstream regulatory exposure it creates. If a user accesses a restricted service from a prohibited location, regulators will focus on whether the firm had reasonable controls to detect and respond.

Regulatory Expectations Around Jurisdiction and Location Controls

Regulators generally view location controls as a foundational compliance mechanism, not a technical feature. When a fintech relies on geography to limit access to products or services, regulators expect the firm to understand how those controls can be bypassed and to address that risk deliberately.

Across agencies, the common theme is consistent. If a product is restricted by jurisdiction, the firm is responsible for enforcing that restriction in practice, not just describing it in policies or disclosures.

OFAC and Global Sanctions Regimes

OFAC sanctions are strict liability regimes. Intent is not required. If a user located in a sanctioned jurisdiction accesses a financial service, the focus shifts quickly to the firm’s controls.

OFAC has repeatedly emphasized the importance of using technical measures, including IP data and other location signals, to prevent access from prohibited countries. Firms are expected to use the data they already collect to identify sanctions risk, not ignore it or rely solely on user representations.

From a GPS spoofing perspective, OFAC risk arises when a firm relies on weak or single-layer location checks that can be easily manipulated.

FinCEN and BSA Frameworks

FinCEN has not published GPS-specific rules, but customer identification, monitoring, and suspicious activity reporting all connect directly tolocation controls.

Location inconsistencies frequently show up as red flags during AML reviews. Examples include:

Rapid changes in the country

Repeated use of anonymizing tools

Access patterns that do not match what a customer disclosed about themselves.

When these signals go unnoticed or are not escalated, regulators may view that as a gap in transaction monitoring. Fintechs subject to the BSA should treat location data as a risk input rather than background noise.

State and Functional Regulators

State regulators care about location because licensing works on a jurisdiction-by-jurisdiction basis. A fintech that is authorized in one state but operates in another without approval creates immediate regulatory exposure.

This is especially relevant for payments, lending, crypto, and other activities governed by state-level frameworks. When geofencing breaks down, regulators tend to treat the resulting activity as unlicensed, regardless of why the control failed.

State regulators care about results. If users in restricted locations gained access, the questions will focus on how location controls were designed, how they were tested, and what monitoring was in place.

SEC, FINRA, and CFTC Views on Geolocation Controls

Federal market regulators focus on investor protection, market access, and registration boundaries. For broker-dealers, trading platforms, and derivatives venues, location controls are often tied to eligibility and registration status.

Enforcement actions have shown that regulators do not accept superficial geofencing. IP-only controls that can be easily bypassed are often characterized as ineffective, particularly when firms are aware of evasion risks.

Regulators are not expecting you to stop every attempt. What they want to see is a reasonable, risk-based control framework built around how users actually behave. GPS spoofing matters across these regimes when it reveals gaps in how jurisdictional rules are being enforced.

Common GPS Spoofing Methods Fintechs Encounter

GPS spoofing in fintech rarely looks exotic. In most cases, it involves ordinary tools used in predictable ways to bypass location-based restrictions. Understanding these methods is necessary to assess whether existing controls are proportionate to real-world risk.

Regulators and examiners most often see the following techniques in enforcement actions and supervisory reviews:

Software-Based GPS and Mock Location Tools

Mock location software allows a device to report fabricated GPS coordinates to any application that requests location data. These tools are widely available and require little technical skill to use.

On mobile devices, this is often done by enabling developer settings or installing apps that override native location services. From the application’s perspective, the location appears legitimate, unless additional integrity checks are in place.

This method is common in consumer-facing fintech apps that rely on device GPS as a primary control.

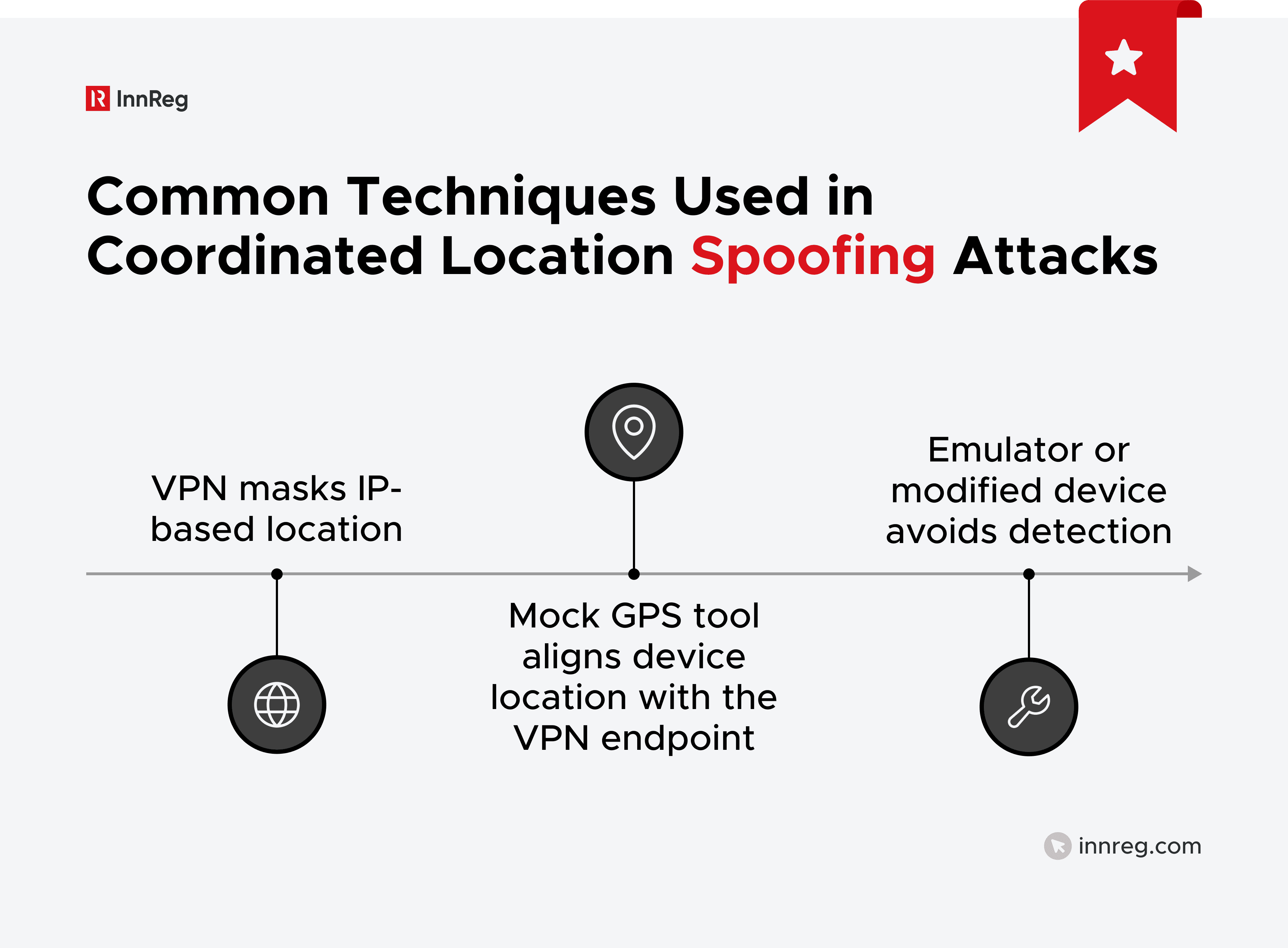

VPNs, Proxies, and IP-Based Location Masking

VPNs and proxies do not alter GPS data, but they mask network-level location by routing traffic through another jurisdiction. This defeats controls that rely primarily on IP geolocation.

These tools are widely marketed and easy to deploy. Many users do not view them as evasive. From a compliance perspective, VPN usage becomes problematic when it is used to access restricted products or jurisdictions.

VPN-based masking is frequently combined with other spoofing techniques, which makes single-layer controls unreliable.

Emulator, Rooted, and Jailbroken Device Abuse

Emulators and modified devices allow users to run fintech applications in environments that bypass normal operating system safeguards. These environments make it easier to manipulate GPS data, suppress integrity checks, and automate access.

Rooted or jailbroken devices remove built-in security restrictions. Emulators simulate devices entirely. Both significantly expand the range of control bypass options available to a user.

In practice, spoofing techniques are rarely used in isolation. A typical pattern looks like this:

See also:

Why Basic IP Blocking Is Not Enough

IP blocking is often the first control fintechs deploy to manage jurisdictional risk. It’s simple to implement and easy to explain. It’s also easy to bypass, which is why regulators increasingly view IP-only strategies as incomplete.

Here are some reasons why regulators don’t trust IP blocking as a standalone effort:

Need help with fintech compliance?

Fill out the form below and our experts will get back to you.

Accuracy Limits of IP Geolocation

IP geolocation does not consistently reflect where a user is physically located. Mobile carriers, cloud infrastructure, and corporate networks frequently route traffic through centralized locations.

As a result, IP data may point to a different city, state, or even country than the user’s actual location. This creates both false positives and false negatives, neither of which is acceptable for regulated access controls.

How VPNs Defeat Single-Layer Controls

VPNs and proxies allow users to select the apparent country or region from which their traffic originates. Many services actively advertise this capability.

From a control standpoint, this means IP blocking only works against unsophisticated users. Anyone intentionally attempting to bypass location restrictions can usually do so within minutes.

Regulators have cited this weakness directly in enforcement actions, particularly where firms knew VPN usage was common but didn’t address it.

Common False Assumptions Compliance Teams Make

A few common assumptions tend to undermine IP-based controls, and each one breaks down for reasons that are easy to predict.

IP location reflects physical presence: IP addresses often resolve to infrastructure locations, not to where end users are sitting. Mobile carriers, cloud providers, and corporate networks route traffic through centralized hubs all the time. What you’re seeing in IP data is usually the network architecture, not the user’s physical location.

VPN usage is rare or accidental: VPNs are everywhere, and they aremarketed aggressively. A lot of users think of them as basic privacy tools, not workarounds. In regulated fintech environments, a VPN tied to geographic restrictions is usually intentional.

Blocking known VPN IPs is sufficient: VPN providers rotate their IP addresses constantly. Many now rely on residential and mobile IP ranges that look like normal traffic. Static blocklists go stale fast. If you’re only blocking known VPN IPs, you are almost certainly behind.

Location controls only matter at onboarding: Jurisdictional risk does not disappear once an account is opened. Users travel, relocate, or deliberately change access patterns over time. Regulators expect location restrictions to apply throughout the customer lifecycle, including logins and transactions.

Taken together, these failures explain why IP-only controls struggle under regulatory scrutiny. They also explain why location risk must be managed as an ongoing control, not a one-time check.

How to Prevent GPS Spoofing Using a Layered Control Framework

Preventing GPS spoofing requires accepting a basic premise. No single control is sufficient on its own. You will not stop every attempt, but a layered program can catch most manipulation and demonstrate the kind of reasonable effort regulators expect.

Effective programs combine device-level protections, network analysis, and behavioral monitoring so that one layer compensates for another layer’s weaknesses. This approach aligns with how regulators evaluate controls in practice:

Device Integrity and Mobile App Security Controls

Mobile devices are a common entry point for spoofing. If the device environment can be manipulated, location data cannot be treated as reliable.

Common controls at this layer include:

Detecting rooted or jailbroken devices

Identifying emulator usage

Blocking mock-location settings.

The goal is not to police devices, but to identify environments where location data is more likely to be falsified. Firms that rely heavily on mobile apps typically treat device integrity signals as gating criteria for higher-risk actions.

Cross-Checking GPS, IP, Wi-Fi, and Network Signals

Layered controls work by comparing multiple location indicators rather than relying on a single source. GPS data can be evaluated alongside IP location, network routing patterns, and nearby Wi-Fi signals.

When these signals align, risk is lower. When they conflict, the session deserves closer review. Location inconsistencies are often more informative than any single data point. This cross-checking is particularly important when users appear to be operating near jurisdictional boundaries or restricted regions.

See also:

Detecting Impossible Travel and Location Anomalies

Behavioral analysis plays a critical role in preventing GPS spoofing over time. Rapid movement between distant locations, repeated country changes, or location shifts that do not align with usage patterns are common indicators. Clear rules often catch the majority of misuse.

These signals are typically evaluated at login and transaction points. Regulators expect firms to notice when access patterns defy physical reality, not just when a user crosses a formal boundary. Effective anomaly detection doesn’t require advanced modeling.

Handling VPN and Proxy Detection

VPN usage is not inherently prohibited, but it materially weakens IP-based controls. As a result, VPN and proxy detection is often treated as a risk multiplier rather than a binary block.

Some firms restrict access when anonymizing tools are detected. Others allow limited functionality while increasing monitoring. What matters is that VPN usage is identified and addressed intentionally, not ignored.

Regulators focus less on the specific response and more on whether the firm understood and managed the risk. This is the layering that regulators often look for in fintechs:

Control Layer | What Regulators Evaluate |

|---|---|

Device integrity | Whether the environment can be trusted |

Signal corroboration | Whether location data is validated |

Behavioral monitoring | Whether anomalies are identified |

Lifecycle controls | Whether the risk is reassessed over time |

A layered framework demonstrates that the firm understands how spoofing actually occurs and has designed controls accordingly. That’s the standard that regulators apply in exams and enforcement reviews.

Operational Controls Compliance Teams Should Implement

Layered controls only work if they are applied consistently. In fintech environments, failures usually occur at handoff points between onboarding, authentication, and transaction execution. Operational discipline is what turns this control design into a defensible practice.

Regulators tend to focus here because this is where policy intent either shows up in system behavior or breaks down:

Onboarding Location Verification

Onboarding is your first chance to verify whether a customer is operating from a permitted jurisdiction. It’s also where many fintechs rely too heavily on self-reported data.

Effective onboarding controls typically combine declared address information with technical location signals. Discrepancies at onboarding should be treated as risk indicators, not dismissed as noise.

Common practices include:

Comparing the stated country or state against the IP and device location

Flagging VPN or anonymizing tools during account creation

Applying additional review for higher-risk jurisdictions or products

The goal is not to block aggressively, but to establish an initial risk baseline to monitor over time.

Ongoing Login and Transaction Monitoring

Jurisdictional risk does not end after onboarding. Users travel, relocate, and change access patterns. Location controls must account for that reality.

Many firms apply location checks at login and again at transaction execution, particularly for higher-risk actions. Monitoring location at multiple points reduces reliance on any single moment in time.

Common triggers include:

Log in from a new country or state

Sudden location changes between sessions

Transactions initiated from locations inconsistent with prior behavior

Regulators often ask whether location restrictions apply throughout the account lifecycle, not just at entry.

Escalation, Review, and Documentation of Location Red Flags

Controls that generate signals without follow-up are unlikely to satisfy examiners. Location-related alerts should feed into a defined escalation and review process.

This typically includes documenting the alert, reviewing supporting data, and recording the rationale for any action taken or not taken. What matters is not that every alert results in a block, but that alerts are reviewed and resolved consistently.

From a compliance standpoint, this documentation does two things. It supports internal oversight, and it gives you something to show during exams or investigations that proves you are actively managing location risk.

Programs that work well operationally treat GPS spoofing indicators as part of broader risk workflows, not as one-off technical events.

Best Practices for Documenting GPS Spoofing Controls

Strong controls lose value if they’re not clearly documented. In regulatory exams, location risk is evaluated as much through written evidence as through system behavior. Documentation is how firms demonstrate that GPS spoofing risk was understood, assessed, and actively managed.

Here’s what regulators typically expect to see in policies, procedures, and supporting records:

See also:

Policies and Procedures Regulators Expect to See

At a minimum, firms should document how location controls operate, what data sources are used, and how exceptions are handled. High-level statements are not sufficient on their own.

Effective documentation explains:

Which products or features are jurisdiction-restricted

What location signals are used to enforce those restrictions

How spoofing risk is identified and escalated

Policies should describe how controls work in practice, not how they are intended to work in theory.

Aligning Geolocation Controls With AML and Sanctions Programs

Location risk should not sit in a silo. Regulators expect it to be integrated into existing AML and sanctions frameworks.

This means location anomalies should feed into transaction monitoring, sanctions screening, and, where appropriate, suspicious activity review. When location data contradicts a customer’s profile, it should influence risk assessment and monitoring intensity.

Firms that treat GPS spoofing purely as a technical issue often struggle to explain how it ties into broader compliance obligations.

Defining Ownership and Accountability for Location Controls

One of the most common examiner questions is simple: Who owns this control?

Clear ownership should be assigned for:

Monitoring location-related alerts

Reviewing and resolving exceptions

Updating controls as products or jurisdictions change

Undefined ownership is often interpreted as unmanaged risk, especially when multiple teams or vendors are involved. This is an area where firms that outsource or extend their compliance function often need to be explicit about roles and responsibilities.

Documenting Location-Based Risk Scenarios and Mitigating Controls

Regulators respond well to scenario-based documentation. It shows that the firm has thought through realistic failure modes.

Examples include:

User attempts to access restricted features while traveling

VPN usage combined with an inconsistent device location

Sudden country changes during high-risk transactions

Each scenario should map to specific mitigating controls. This demonstrates a risk-based approach rather than blanket rules.

Evidence Retention and Audit Trails for Geolocation Decisions

When location controls trigger an alert, firms should be able to show what happened next. This includes logs, review notes, and decision rationales.

Useful evidence often includes timestamps, location signals reviewed, analyst notes, and any action taken. Audit trails matter most when the firm decides not to block activity, because that decision must be defensible later.

Well-structured documentation does not need to be lengthy. It needs to be accurate, current, and aligned with how controls actually operate.

Common Misconceptions About How to Prevent GPS Spoofing

GPS spoofing failures often trace back to incorrect assumptions rather than missing technology. These misconceptions show up repeatedly in exams, audits, and post-incident reviews.

For many fintechs, this weakens what would be a reasonable control framework otherwise. Here are some misconceptions to clarify so that you can make location controls easier to defend and operate:

“Users won’t try to bypass location controls”

Many fintech teams assume that only a small subset of users will attempt to bypass geofencing. In reality, spoofing tools are easy to find, inexpensive, and widely discussed online.

When access restrictions affect pricing, availability, or product features, some users will test the limits. Regulators expect firms to assume bypass attempts will occur, not to treat them as edge cases.

“Self-reported addresses are sufficient”

Customer-provided addresses are necessary, but they are not verification. Regulators have consistently taken the position that firms must validate critical compliance inputs when feasible.

If technical location data contradicts a declared address, ignoring that discrepancy raises questions. Self-attestation without corroboration is rarely persuasive in enforcement reviews.

“Third-party vendors eliminate all responsibility”

Outsourcing geolocation or fraud tooling does not transfer regulatory accountability. Firms remain responsible for how controls are configured, monitored, and escalated. Regulators frequently ask how vendor outputs are reviewed and acted upon. Using a vendor without oversight is treated as a governance issue instead of a mitigation.

“GPS spoofing can be fully prevented”

Absolute prevention is not the standard. Regulators don’t expect firms to block every spoofing attempt.

But they do expect firms to identify manipulation risk, apply layered controls, and respond consistently when indicators appear. Programs are evaluated on design and follow-through, not perfection.

Correcting these misconceptions shifts the conversation from whether spoofing is possible to whether the firm’s response is reasonable and defensible.

Key Takeaways for Fintech Founders and Compliance Teams

GPS spoofing is a recurring control failure that shows up in sanctions enforcement, licensing violations, and fraud investigations. Preventing GPS spoofing starts with treating location as a risk signal.

At InnReg, we help fintechs design and operate location-based controls as part of broader compliance programs. That includes registration strategy, control design, policy development, and day-to-day compliance operations.

For many clients, we act as an extension of their internal team or as their outsourced compliance function, integrating into existing systems and workflows without unnecessary complexity.

Adriana is a Principal Consultant at InnReg with 8 years of compliance experience specializing in VASP licensing and regulatory frameworks across Europe and LATAM. She has held senior compliance roles at leading global crypto and financial institutions, including Gate.io, Binance, Santander Bank, and BNP Paribas, with deep expertise in KYC/AML operations, MiCA adaptation, and building compliance programs from the ground up.

How Can InnReg Help?

InnReg is a global regulatory compliance and operations consulting team serving financial services companies since 2013.

We are especially effective at launching and scaling fintechs with innovative compliance strategies and delivering cost-effective managed services, assisted by proprietary regtech solutions.

If you need help with compliance, reach out to our regulatory experts today:

Related Articles

Featured LinkedIn Posts