What Is an Electronic Money Institution (EMI)?

Entities that are authorized as an electronic money institution (EMI) hold one of the most important licensing categories in today’s fintech landscape. That’s because an EMI license allows non-bank companies to look similar to traditional banking products but operate under a different regulatory framework. Many of the most recognizable fintechs in Europe and beyond started with an EMI license before expanding further.

This article explains what an EMI is, how it works, and where it fits alongside banks and payment institutions. It also examines the global regulatory environment, licensing requirements, and safeguards designed to protect customer funds.

Along the way, we’ll highlight the compliance challenges and common misconceptions that fintech founders and compliance officers need to be aware of. By the end, you’ll have a clear picture of how electronic money institutions operate, what regulators expect, and how this model can support innovation in financial services without crossing into full-scale banking.

At InnReg, we help fintechs plan, obtain, and operate EMI and payments licenses across the UK, EU, and other key jurisdictions. Our team supports you with licensing strategy, safeguarding frameworks, AML controls, and day-to-day compliance operations. Contact us to learn more.

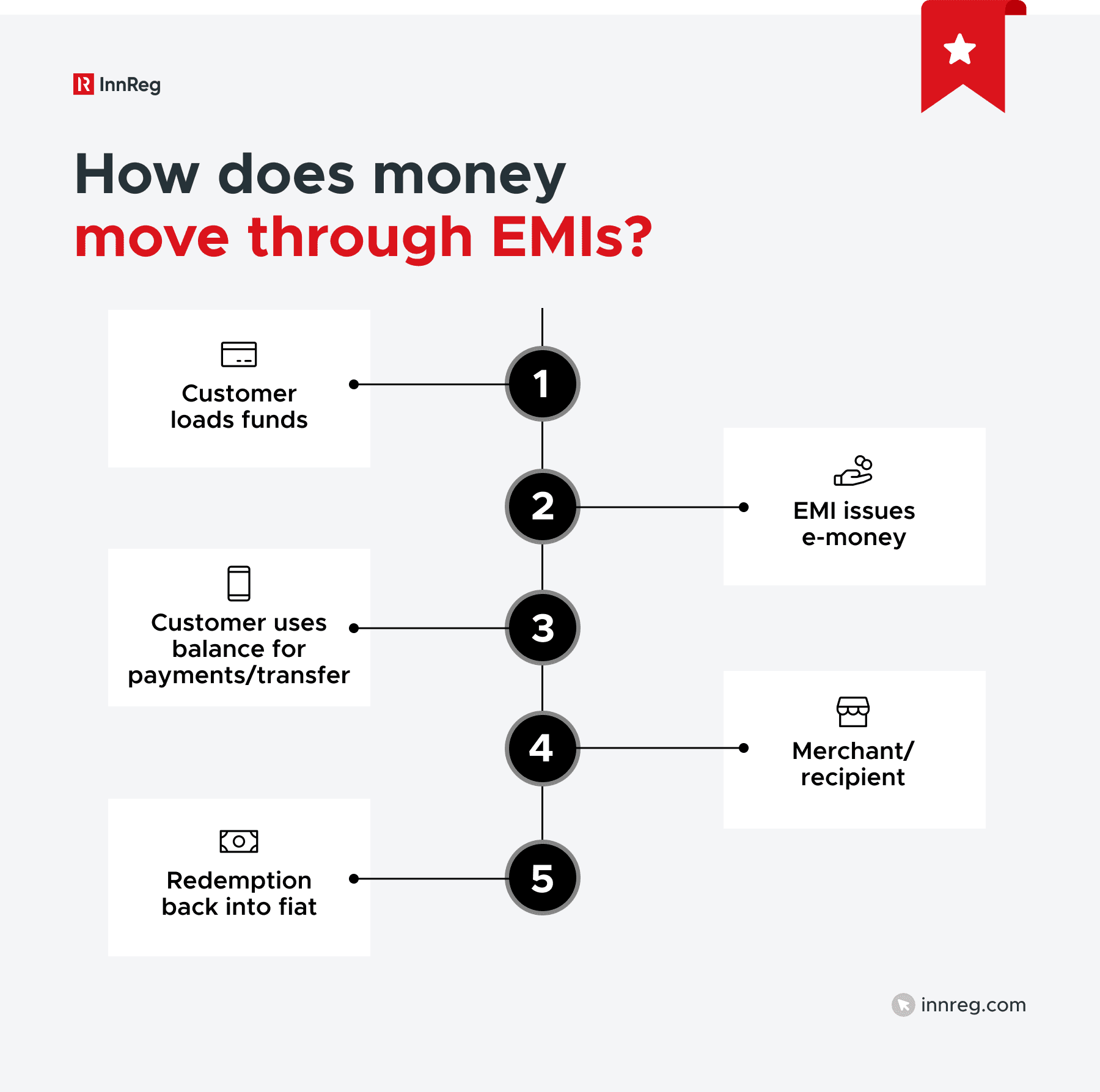

How an Electronic Money Institution Works

An EMI issues e-money, which is a digital representation of fiat currency stored electronically. Customers load funds into an EMI account, and those funds appear as a balance that they can use for payments, transfers, or withdrawals. The money remains in electronic form until it is redeemed back into traditional currency.

Services EMIs Can Provide

An EMI license allows firms to offer a range of services that make them look similar to banks in the eyes of customers. Common services include:

Digital payment accounts: EMIs can provide multi-currency accounts with IBANs or equivalent identifiers.

Money transfers: Domestic and cross-border payments are core to the EMI model.

Payment cards and e-wallets: Many EMIs issue prepaid or debit cards linked to customer balances.

Currency exchange: Multi-currency accounts and competitive FX services are typical features.

Payment initiation: Depending on permissions, EMIs can initiate transactions such as direct debits or standing orders.

These services have made EMIs attractive to both consumers and businesses that need fast, flexible payment solutions.

Services EMIs Cannot Provide

Just as important are the services that fall outside an EMI license. EMIs cannot lend customer funds or operate as deposit-taking banks. They are also restricted from offering investment products, providing insurance, or paying interest on balances.

This distinction is critical. Customers may see an EMI account as similar to a bank account, but in regulatory terms, the EMI is a payments entity, not a full financial institution. By design, the EMI framework allows innovation in payments while limiting riskier activities reserved for banks.

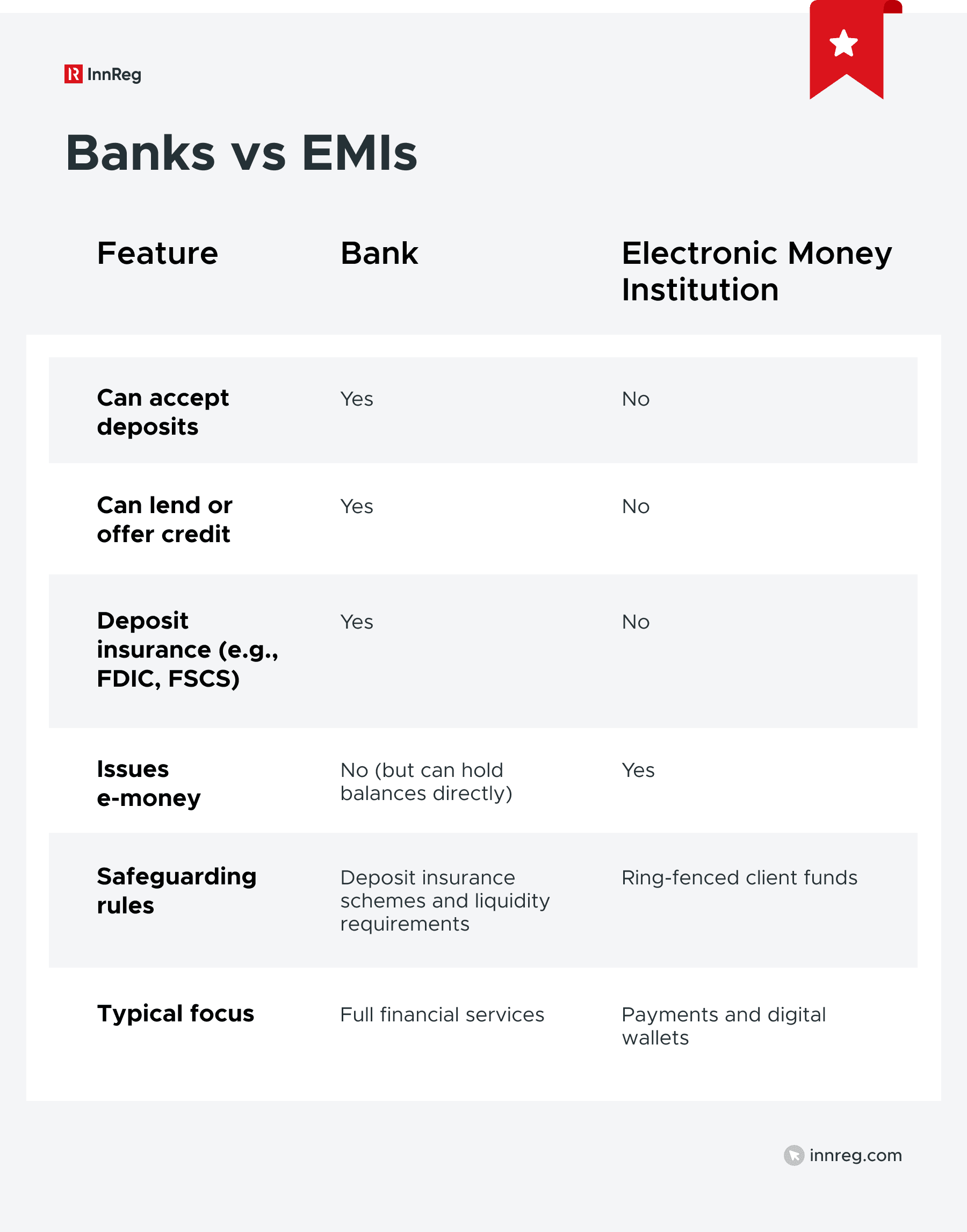

Electronic Money Institution vs. Bank

At first glance, an EMI can look like a bank. Both offer accounts, payment cards, and the ability to send and receive money. The difference lies in the regulatory permissions and the activities each type of institution is allowed to perform.

Banks are licensed to take deposits and provide credit. They can use customer deposits to fund lending, mortgages, and other financial services. They are also subject to deposit insurance requirements and prudential supervision designed to protect the wider financial system.

EMIs, by contrast, are focused on payments. They cannot take deposits in the legal sense, lend customer funds, or provide investment products. EMIs must safeguard and keep separate customer money from the institution’s own funds, and not use it for lending or investment purposes.

From a customer’s perspective, this creates both opportunities and limits. EMI accounts are often faster to open, internationally accessible, and supported by user-friendly technology. However, they lack traditional banking features such as overdraft facilities, interest-bearing accounts, or government-backed deposit insurance.

The table below highlights the core differences from a high-level view:

For fintech founders, an EMI license opens doors to the payments space without the heavy infrastructure of banking. But it also comes with strict boundaries, and those boundaries shape both product design and compliance obligations.

Global Regulatory Framework for Electronic Money Institutions

EMI regulations look different depending on where you operate, though Europe pioneered the whole concept. The EU and UK were first to carve out specific EMI categories in their rulebooks. Other countries regulate the same activities but call them something else entirely.

For fintech founders shopping around for jurisdictions, you need to know how each country treats these entities. It makes a huge difference in where you decide to set up shop.

United Kingdom Under the FCA

In the UK, EMIs are regulated by the Financial Conduct Authority (FCA) under the Electronic Money Regulations 2011. Two categories exist: authorized EMIs with full permissions and small EMIs with limited scope.

Authorization requires a detailed application, governance checks, and ongoing compliance reporting. The FCA has increased scrutiny in recent years, with a sharper focus on safeguarding and anti-money laundering practices.

United States: Money Transmitter Licenses Instead of EMIs

The US does not have a direct EMI license. Instead, fintechs offering wallets, prepaid cards, or money transfer services must obtain money transmitter licenses at the state level and register federally as money services businesses (MSBs) with FinCEN.

This fragmented system makes nationwide coverage expensive and complex, often requiring firms to manage 50 different licensing regimes or work through a licensed partner bank.

Other Key Jurisdictions

Several countries have adopted EMI-like regimes:

Singapore regulates under the Payment Services Act, where a Major Payment Institution license covers e-money issuance.

Hong Kong requires a Stored Value Facility (SVF) license for digital wallets and prepaid products.

Canada enacted the Retail Payment Activities Act (RPAA), establishing federal oversight of payment service providers. E-money issuance itself remains governed by federal banking rules and provincial prepaid product laws, rather than a dedicated EMI regime.

Emerging markets in Africa and Latin America often use mobile money or payment service provider licenses to regulate non-bank digital wallets.

The choice of jurisdiction often balances market opportunity with the complexity of compliance. Partnering with local advisors or outsourced compliance providers like InnReg can help map out the right licensing strategy for each market.

Licensing and Regulatory Requirements for EMIs

Obtaining an EMI license is a detailed process that requires demonstrating financial stability, strong governance, and clear customer protections. While the exact requirements differ slightly between jurisdictions, the EU and UK frameworks are widely seen as the standard.

Capital Requirements and Business Planning

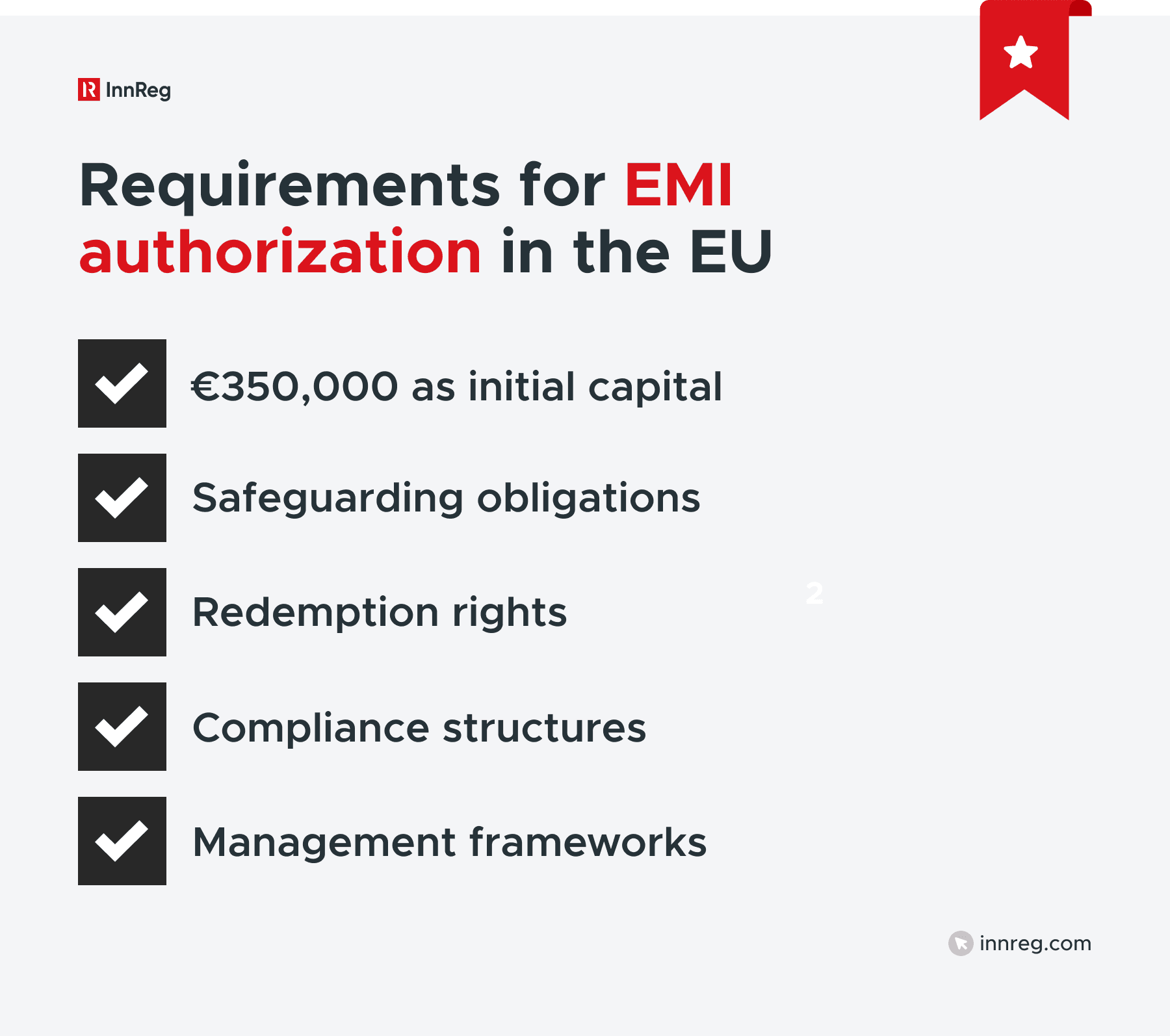

As previously mentioned, an EMI must start with an initial capital of at least €350,000 in the EU. This amount is designed to demonstrate to regulators that the institution has sufficient financial backing to operate responsibly. Beyond the starting capital, EMIs must maintain ongoing own funds linked to the volume of outstanding e-money or payment transactions.

Applicants are also required to provide a comprehensive business plan. Regulators expect details on the target market, financial forecasts, risk assessments, and how the company will remain viable. A vague or overly optimistic plan is a common reason for delayed or rejected applications.

Safeguarding and Redemption of Customer Funds

A core principle of EMI regulation is safeguarding customer money. Any funds received in exchange for e-money must be kept separate from the company’s own assets. This is usually done by:

Placing money in segregated client accounts at authorized banks.

Using an insurance policy or guarantee to cover the same value.

In addition, customers have a legal right to redeem e-money at par value at any time. EMIs must be able to process redemption requests promptly and without excessive fees.

Governance, Compliance, and Reporting Obligations

Regulators expect EMIs to demonstrate strong internal structures. Typical requirements include:

Fit and proper management: Directors and key executives must pass background and competency checks.

Dedicated compliance functions: EMIs must have officers who are responsible for anti-money laundering, fraud prevention, and regulatory reporting.

Operational resilience: Policies covering IT security, business continuity, and incident response are mandatory.

Ongoing reporting: EMIs must file regular returns, financial statements, and compliance reports to their regulator.

For fintech founders, these obligations mean that obtaining the license is just the starting point. Running an EMI requires continuous oversight and investment in compliance, technology, and governance. This is why many firms work with compliance specialists to design scalable programs that can keep pace with growth.

See also:

Safeguarding Funds in an Electronic Money Institution

The protection of customer funds is one of the most important responsibilities of an EMI. Unlike banks, EMIs cannot use customer balances for lending or investment. Regulators, therefore, require strict safeguarding measures to make sure customer money is protected even if the EMI fails.

Need help with payments compliance?

Fill out the form below and our experts will get back to you.

Segregation of Client Money

The most common approach is to segregate customer funds. EMIs must place client money into dedicated safeguarding accounts held with authorized banks or invest it in low-risk, liquid assets.

These funds are ring-fenced and cannot be mixed with the EMI’s operating capital. If the EMI becomes insolvent, the safeguarded accounts are excluded from the company’s assets and must be returned to customers.

Insurance or Guarantee Models

Some regulators allow EMIs to use an insurance policy or guarantee instead of, or in addition to, segregation. In this model, a third party, such as a bank or insurer, guarantees repayment of safeguarded funds if the EMI fails. While less common, this approach provides additional flexibility for EMIs operating in multiple jurisdictions or managing large transaction volumes.

Consumer Protection and Disclosure Requirements

Regulators require EMIs to be transparent with customers. Electronic money is not a deposit, and balances are not covered by government deposit insurance schemes such as the FDIC in the US or the FSCS in the UK. Instead, protection comes from safeguarding arrangements. EMIs must clearly disclose this to customers to prevent confusion with traditional banks.

Strong safeguarding is central to maintaining customer trust. Failures in safeguarding have led to regulatory sanctions and, in some cases, lengthy insolvency proceedings.

Compliance Challenges for Electronic Money Institutions

Operating as an EMI involves more than meeting licensing requirements. The real challenge comes after authorization, when firms must maintain compliance in a fast-moving environment. Regulators expect EMIs to manage risks with the same seriousness as banks, even though their business model is narrower.

AML and Financial Crime Risks

EMIs are attractive targets for criminals because they move money quickly and often operate across borders. Weak anti-money laundering (AML) or sanctions controls are a leading cause of regulatory action against EMIs.

Founders must build strong customer due diligence, transaction monitoring, and suspicious activity reporting from day one. Outsourcing AML compliance systems without proper oversight is a common pitfall.

Based on 10+ years of InnReg’s industry experience, Regly helps firms improve their AML programs and mitigate financial crime risks →

Operational Resilience and Cybersecurity

Payments rely on uninterrupted access. A system outage or data breach at an EMI can disrupt thousands of transactions and damage credibility with regulators. Supervisors expect EMIs to have business continuity plans, tested incident response procedures, and layered cybersecurity defenses. For smaller fintechs, balancing innovation speed with robust IT governance is a constant tension.

See also:

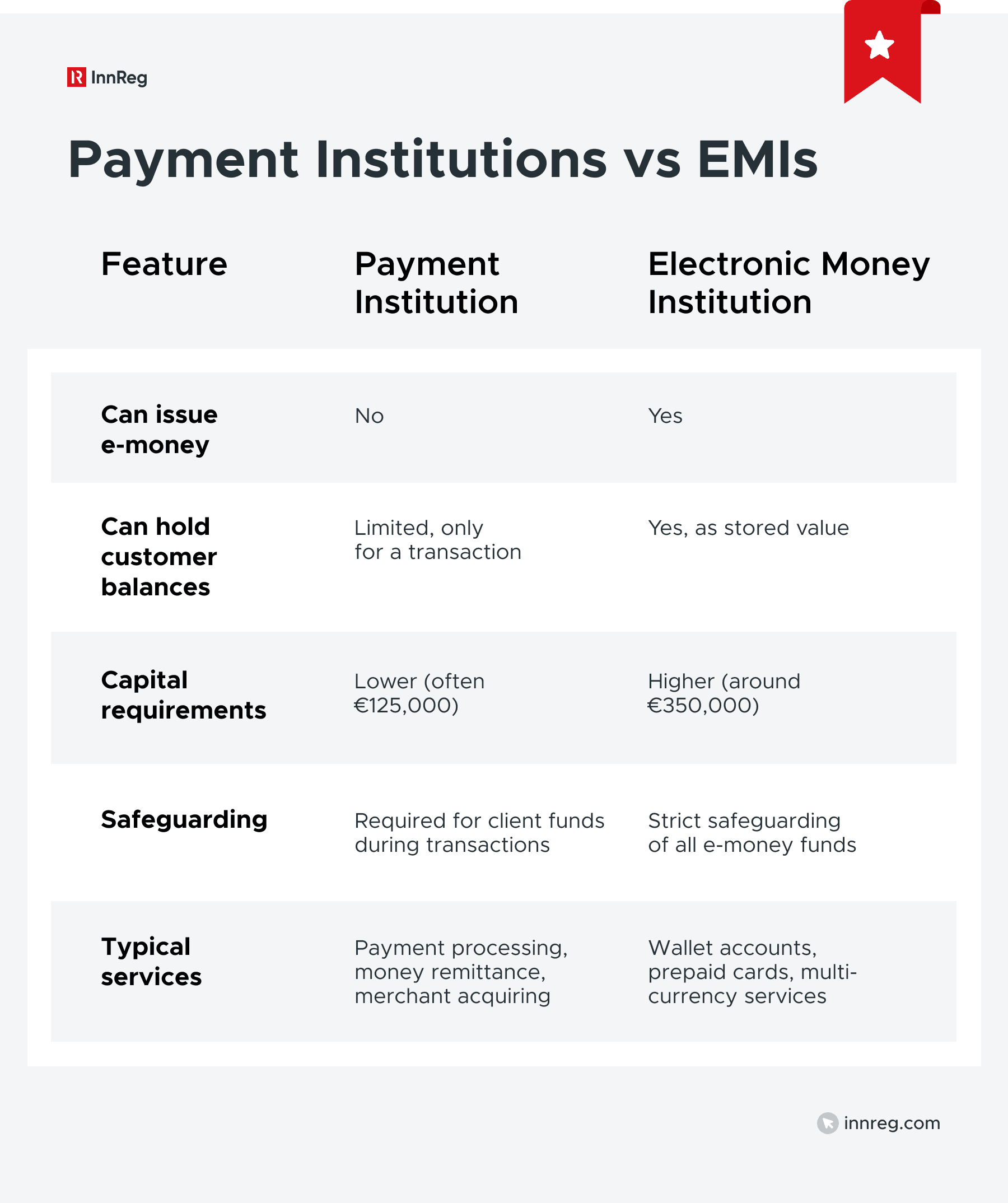

Electronic Money Institution vs. Payment Institution

Both EMIs and payment institutions (PIs) operate in the payments space, but their licenses cover different scopes. The distinction matters because it determines whether a fintech can hold customer balances or must only process payments.

Payment institutions provide payment services but cannot issue e-money. They act as intermediaries, moving money from one party to another. Funds received by a PI are usually tied to a single transaction and must be passed on promptly. PIs are often used for services like merchant acquiring, payment gateways, or remittance platforms.

EMIs, on the other hand, can issue e-money and hold customer balances. This allows them to provide wallet-style accounts, prepaid cards, or multi-currency accounts. Because EMIs store value, their regulatory requirements are stricter, with higher capital thresholds and detailed safeguarding rules.

For fintech companies, this choice is strategic. If a fintech intends to offer customers an account with balances they can store and use over time, an EMI license is required. If the model focuses only on processing transactions without storing funds, a PI license may suffice.

EU and EEA Under the E-Money Directive and PSD2

The European Union created the concept of the EMI through the Second E-Money Directive (2009/110/EC). This framework gives non-bank companies the ability to issue e-money and provide payment services across the European Economic Area (EEA). For fintech firms, the EU remains the most developed and standardized environment for EMI licensing.

Passporting rights are a defining feature. Once authorized in one EU or EEA member state, an EMI can “passport” its license to operate in all other member states without applying for separate approvals. Companies like Revolut and Wise built their customer base by obtaining an EMI license in one jurisdiction and expanding across Europe under the passporting mechanism.

Each EMI applies for authorization in a specific country, and the local authority supervises compliance. Examples include the Central Bank of Ireland, the Bank of Lithuania, and BaFin in Germany. While the directive provides harmonized rules, the licensing process can vary in speed and intensity depending on the regulator’s approach.

The directive imposes several core requirements:

Initial capital of at least €350,000, with ongoing own funds linked to the volume of outstanding e-money.

Safeguarding obligations require customer funds to be held in segregated accounts with credit institutions or backed by insurance or guarantee arrangements.

Redemption rights, meaning customers can redeem their e-money for cash at any time at par value.

Fit and proper management, requiring background checks and expertise for directors and key executives.

Governance and compliance structures, including dedicated compliance officers, anti-money laundering policies, and ongoing reporting to regulators.

The EU also links EMI activity to the broader Payment Services Directive (PSD2). Many EMIs also hold permissions as payment institutions to provide services like money remittance or payment initiation alongside e-money issuance.

This overlap has created some regulatory duplication, which is one reason why the European Commission has proposed merging the frameworks under PSD3.

Capital Adequacy and Business Viability

Thin margins are a recurring issue in the sector. Many EMIs compete on low fees, but regulators will challenge business models that appear unsustainable. Capital must grow in line with transaction volume, and regulators expect firms to hold buffers to absorb shocks.

Best Practice: Plan for the financial reality of maintaining compliance staff, audits, and technology.

Cross-Border Operations and Jurisdictional Complexity

Passporting in the EU simplifies expansion, but serving multiple countries still adds complexity. Each jurisdiction may have additional consumer protection or reporting requirements.

Outside Europe, the landscape is fragmented, with different licensing categories such as money transmitters in the United States or stored value providers in Asia. Managing compliance across multiple regimes requires local expertise and careful coordination.

Common Misconceptions About Electronic Money Institutions

Despite their growing importance, EMIs are often misunderstood. Founders and even experienced professionals sometimes confuse what an EMI can and cannot do, which can lead to strategic mistakes or regulatory risk.

Are EMIs the Same as Banks?

No. EMIs may look like banks to customers because they offer accounts and cards, but they cannot lend, pay interest, or take deposits. Their role is limited to issuing e-money and facilitating payments. The distinction is crucial because treating an EMI like a bank in marketing or operations can draw regulatory scrutiny.

Is Customer Money Safe in an EMI?

Funds held with an EMI are protected differently from bank deposits. There is no government deposit insurance, but safeguarding rules require EMIs to keep customer money in segregated accounts or under an insurance arrangement.

If the EMI fails, these safeguarded funds must be returned to clients. The protection is real, but it is not identical to deposit protection in banking.

Are Cryptocurrencies Considered E-Money?

No. Cryptocurrencies like Bitcoin and Ethereum are not classified as e-money under current laws. E-money is a digital representation of fiat currency. However, stablecoins pegged to national currencies may fall under e-money rules in some jurisdictions. For example, in the EU, fiat-referenced tokens under MiCA could be regulated in a way similar to e-money issuance.

How Hard Is It to Get an EMI License?

Many founders underestimate the process. Authorization can take 6 to 12 months or longer, depending on the regulator and the completeness of the application. Regulators assess business models, governance, safeguarding, and AML systems in detail. Securing the license is only the beginning because ongoing compliance is what keeps the license in force.

Recent Regulatory Updates and Market Trends

The EMI sector is evolving rapidly. Regulators are tightening rules, new technologies are reshaping services, and competition is pushing firms to specialize. Founders and compliance teams should be aware of several recent developments.

PSD3 and the Merger of EMI and PI Frameworks

The European Commission has proposed replacing the current E-Money Directive with PSD3 and a new Payment Services Regulation (PSR). This would merge payment institutions and EMIs into a single framework.

Existing EMIs will need to adapt and may be required to submit updated or new authorization applications under the new regime, though some draft texts propose a grace/grandfathering period and streamlined transitional procedures for licensed entities.

Firms should plan now for potential shifts in capital requirements, safeguarding, and reporting obligations, but also monitor the legislative process, as the final form and timing of PSD3 and PSR implementation remain subject to negotiation and possible national variances.

See also:

Safeguarding Reforms in the UK and EU

Both the UK’s FCA and EU regulators have sharpened their focus on safeguarding. They are introducing daily reconciliation, clearer recordkeeping, and statutory trust structures to make customer fund protection more robust. These changes are partly a response to past EMI failures, where poor safeguarding delayed customer reimbursements.

Stablecoins and the Future of E-Money

The line between e-money and crypto-assets is narrowing. In the EU, fiat-backed stablecoins fall under the category of “e-money tokens” in the MiCA framework. This means issuers may need to hold an EMI license or similar authorization. For fintechs building products that bridge crypto and fiat, this is a critical development to monitor.

Increased Regulatory Scrutiny and Enforcement Actions

Regulators are applying more pressure on EMI business models. Weak anti-money laundering controls, insufficient capital buffers, and governance gaps are now leading to enforcement actions, including license suspensions. Authorities are also scrutinizing marketing to make sure customers are not misled into thinking EMIs provide the same protections as banks.

Growth, Competition, and Innovation in EMI Services

The market for EMIs continues to grow. New entrants focus on niches such as multi-currency accounts for freelancers, payment rails for crypto platforms, or corporate expense management. At the same time, larger firms are consolidating, with acquisitions driven by the need for scale and established licenses. Innovation remains strong, but the compliance bar is rising.

Key Takeaways for Fintech Founders and Compliance Teams

Electronic money institutions have become a critical part of the payments landscape. They give fintechs the ability to issue e-money, provide digital accounts, and expand across markets without holding a full banking license. But those opportunities bring responsibilities. With reforms such as PSD3 and PSR on the horizon, these responsibilities will only grow more complex.

At InnReg, we help fintech companies design and operate compliance programs that scale with their ambitions. Whether you are applying for an EMI license or managing day-to-day obligations, our team combines fintech specialization with practical, outsourced compliance support.

If you’re planning to build or expand an EMI, let’s talk about how to approach it with confidence and efficiency.

InnReg was founded in 2013 by Francesco Matteini, former Chief Compliance Officer who helped launch and scale some of the most innovative digital broker-dealers over the last two decades. He built compliance programs to support the first zero-commission broker and the first BD-sponsored investor social network. Since its founding, InnReg has attracted highly experienced fintech consultants with long careers in compliance, risk management, and a deep understanding of the fintech industry.

How Can InnReg Help?

InnReg is a global regulatory compliance and operations consulting team serving financial services companies since 2013.

We are especially effective at launching and scaling fintechs with innovative compliance strategies and delivering cost-effective managed services, assisted by proprietary regtech solutions.

If you need help with payments compliance, reach out to our regulatory experts today:

Related Articles

Featured LinkedIn Posts